Consumer Finance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.44 Trillion |

| Market Size (2031) | USD 14.08 Trillion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Finance Market Analysis by Mordor Intelligence

The Consumer Finance Market size is expected to grow from USD 9.87 trillion in 2025 to USD 10.44 trillion in 2026 and is forecast to reach USD 14.08 trillion by 2031 at 6.17% CAGR over 2026-2031.

Growth in the consumer finance market is being supported by credit decision tools moving into digital commerce, the broader use of consent-based financial data, and policy actions that expand access to formal borrowing for underserved borrowers. These shifts reinforce one another: stronger data increases approval confidence, while faster digital journeys reduce abandonment and increase completed originations across consumer credit products. Large banks still hold a strong position in the consumer finance market because of deposit-backed funding, scale in compliance, and established risk controls, which support pricing discipline and portfolio resilience. At the same time, the consumer finance market is creating more room for fintech lenders that compete on speed, embedded offers, and sharper risk selection rather than branch density alone. Near-term pressure remains concentrated in funding costs and unsecured delinquency, yet the structure of current portfolios still appears more resilient than lending patterns seen before the global financial crisis.

Key Report Takeaways

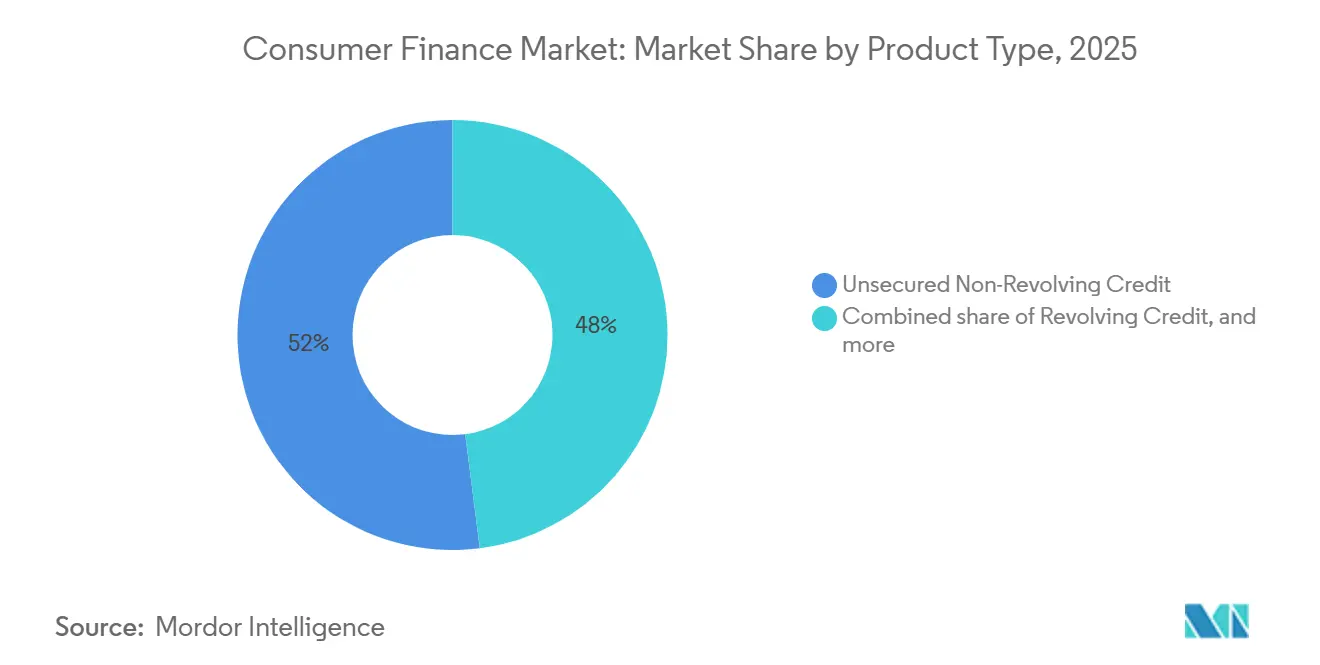

- By product type, unsecured non-revolving credit held 52% of the consumer finance market share in 2025, while revolving credit is projected to grow at 7.9% CAGR through 2031.

- By lender type, banks accounted for 61.9% of the consumer finance market share in 2025, while fintechs and digital lenders are projected to grow at a 10.7% CAGR through 2031.

- By distribution channel, branch/in-person captured 38.1% revenue share in 2025, while digital direct is projected to grow at 9.5% CAGR through 2031.

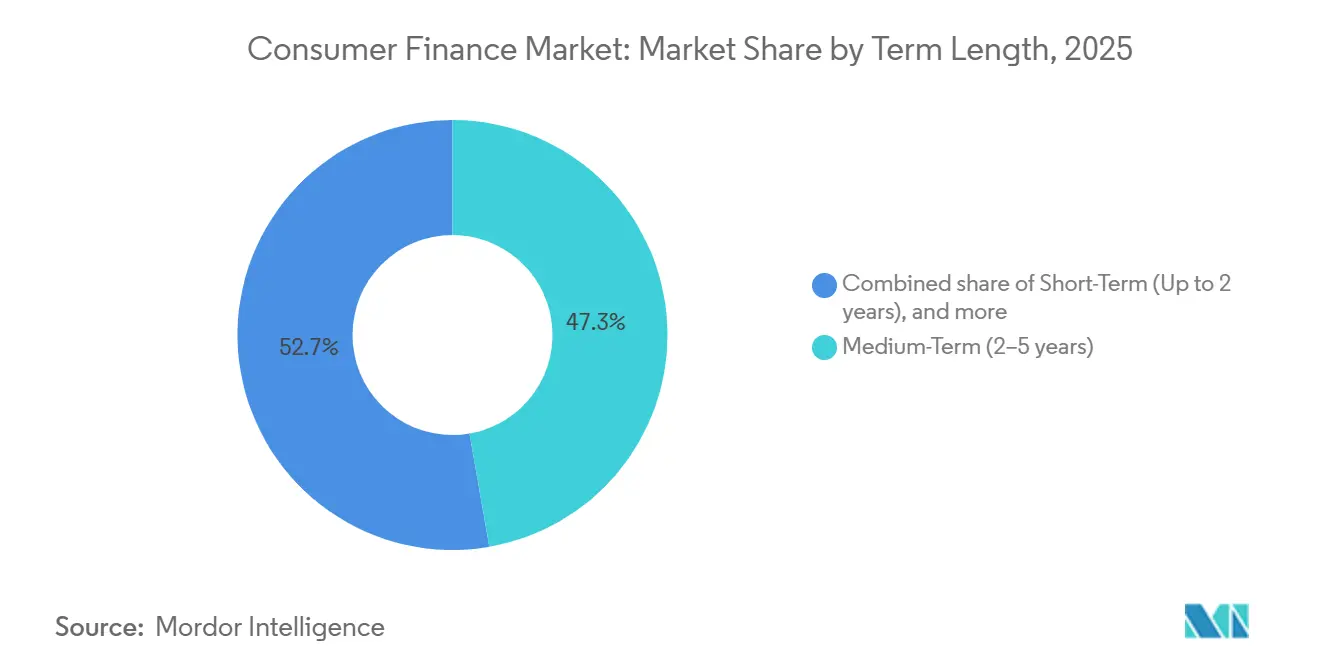

- By term length, medium-term loans captured 47.3% revenue share in 2025, while short-term credit is projected to grow at 8.2% CAGR through 2031.

- By loan purpose, vehicle purchase/auto-related captured 27.6% revenue share in 2025, while debt consolidation/refinancing is projected to grow at 7.5% CAGR through 2031.

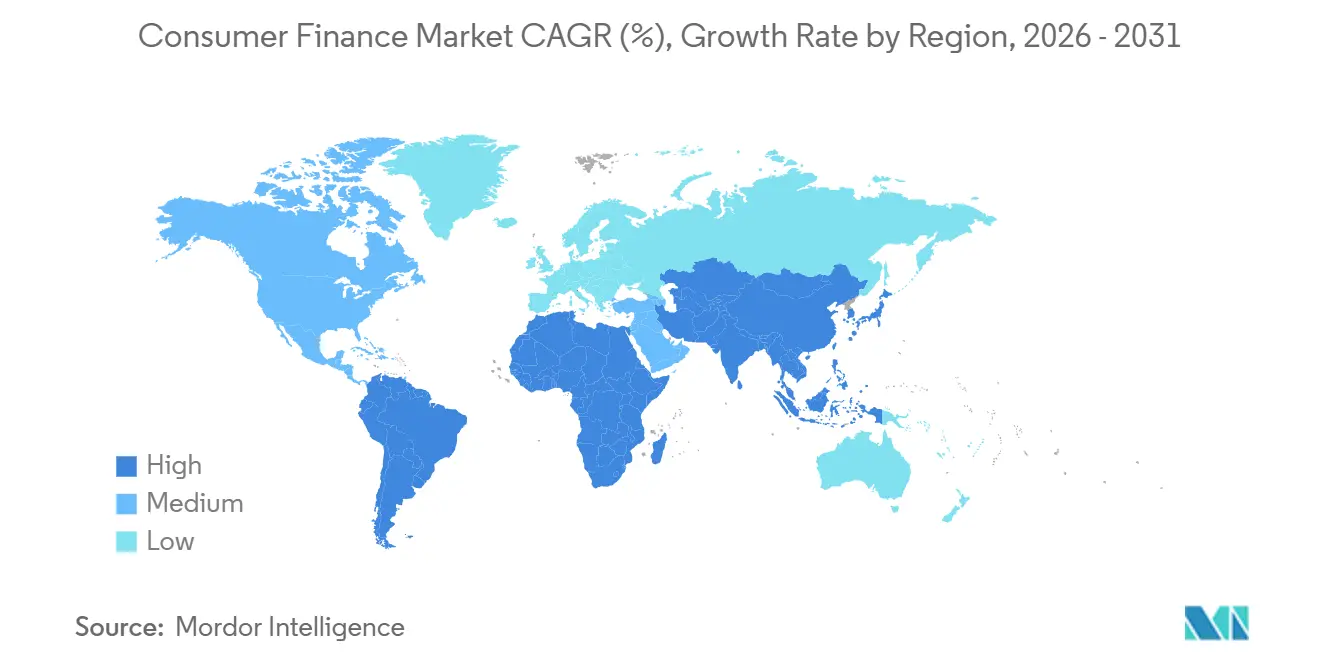

- By geography, Asia-Pacific captured 43.3% of the consumer finance market share in 2025, while Middle East and Africa is projected to grow at 8.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Embedded Finance at Point-of-Sale Expands Credit Take-Up | +1.2% | Global, concentrated in North America, Asia-Pacific, and Western Europe | Short term (≤ 2 years) |

| Open Banking Improves Underwriting Precision | +0.8% | North America and EU, with spill-over to GCC and India | Medium term (2-4 years) |

| BNPL Normalizes Short-Duration Consumer Credit | +0.7% | Global, with Asia-Pacific and the Middle East showing the fastest adoption | Short term (≤ 2 years) |

| AI-Enabled Collections Reduce Delinquency Leakage | +0.6% | Global, with early gains in North America and India | Medium term (2-4 years) |

| Cross-Border Worker Remittances Lift Small-Ticket Credit Demand | +0.4% | Middle East and Africa, South America, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Subprime Repricing Creates a Larger Risk-Adjusted Addressable Pool | +0.5% | North America, Brazil, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Embedded Finance at Point-of-Sale Expands Credit Take-Up

Lending is increasingly offered throughout the purchase journey rather than through a separate bank application, and that shift is changing how borrowers enter the consumer finance market. Credit offered at checkout tends to lift take-up because the financing decision appears when purchase intent is already high, and the transaction still feels immediate. This model also helps merchants convert more baskets into completed sales, giving lenders a stronger origination channel than stand-alone acquisition campaigns. As this pattern expands, the consumer finance market benefits from purchases that might otherwise have been delayed, reduced, or abandoned due to short-term budget constraints. Embedded delivery also favors lenders that can combine fast risk checks with seamless partner integrations across merchant systems and apps. In the United States, the active CFPB Section 1033 open-finance rule supports the data connectivity that point-of-sale underwriting increasingly depends on.

Open Banking Improves Underwriting Precision

Real-time access to transaction data is improving lenders' ability to assess income stability, repayment behavior, and cash flow volatility across a broader set of borrowers in the consumer finance market. This matters most for self-employed, gig, and thin-file applicants because bureau history alone often fails to capture their full repayment capacity. Better data reduces adverse selection, allowing lenders to increase approval confidence without lowering underwriting standards or widening loss tolerance. The commercial benefit is not limited to approval rates because more precise data also support better pricing discipline across borrower risk bands. India’s Account Aggregator framework is helping lenders embed consent-based data sharing directly into underwriting for self-employed and underserved borrowers, making open data use more operational and less experimental. As similar frameworks spread, the consumer finance market should see stronger decision quality in customer groups that were previously difficult to evaluate with traditional scorecards alone[1]ECONOMICTIMES.INDIATIMES.COM Fintech lenders corner 77% of India's personal loan market by volume in FY26 - The Economic Times.

BNPL Normalizes Short-Duration Consumer Credit

BNPL has moved from a niche checkout feature to a mainstream credit behavior influencing short-duration borrowing across the consumer finance market. Federal Reserve analysis showed that six major providers originated close to USD 160 billion in consumer credit products in 2025, with pay-in-4 plans contributing USD 78.3 billion and longer-term installments adding USD 47.1 billion[2]FEDERALRESERVE.GOV The Fed - “Buy Now, Pay Later” Beyond “Pay in 4”, A Comprehensive Product Overview. More than 60% of that issuance carried 0% APR, helping normalize installment borrowing for routine consumption rather than just for exceptional purchases. This shift is reducing the gap between stand-alone BNPL providers and card issuers, as installment mechanics are increasingly being integrated into existing card infrastructure. The competitive focus is now moving toward distribution, with lenders seeking placement inside search, wallet, and app journeys where purchase decisions increasingly begin. In May 2026, both Klarna and Affirm secured placement inside Google Search AI Mode and the Gemini app, showing how consumer lending is moving beyond checkout pages into AI-led commerce flows.

AI-Enabled Collections Reduce Delinquency Leakage

Collections capability is becoming a more important competitive variable as the consumer finance market expands across unsecured, short-duration, and digitally originated products. Lenders are placing more emphasis on early-warning models because small improvements in cure rates can materially change the economics of high-volume retail credit books. AI-led collections tools support earlier customer contact, better outreach prioritization, and more tailored treatment paths that align with account behavior. This matters most in fast-growing portfolios where traditional recovery infrastructure often trails origination growth and leaves avoidable leakage in the book. Over time, lenders with stronger collections intelligence can hold a broader borrower pool without needing the same level of risk premium that less responsive portfolios require. That makes service quality a meaningful differentiator in the consumer finance market, especially where expansion is outpacing legacy recovery processes' ability to adapt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Scrutiny Raises Compliance Cost per Originated Dollar | -0.9% | Global, most acute in North America and China | Medium term (2-4 years) |

| Funding Cost Volatility Compresses Net Interest Margins | -0.8% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Delinquency Sensitivity Remains High in Revolving and Unsecured Credit | -0.6% | North America, Brazil, and India | Short term (≤ 2 years) |

| Data Fragmentation Limits Cross-Sell Across Lenders and Geographies | -0.5% | Global, with early concentration in the Asia-Pacific, the Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny Raises Compliance Cost per Originated Dollar

Regulation is becoming a stronger operating constraint in the consumer finance market because each added disclosure, reporting, and suitability requirement raises cost before a loan is even booked. The burden is usually easier for large institutions to absorb because fixed compliance overhead can be spread across broad portfolios and multiple products. Smaller lenders feel the pressure more directly because rising compliance costs narrow the room for experimentation, pricing flexibility, and borrower acquisition. This dynamic can slow product diversity even when borrower demand remains healthy, especially in regulated unsecured and short-duration categories. In China, regulatory tightening has already shaped origination conditions, and PBOC data for Q1 2026 showed consumer loans excluding housing declining 0.2% year over year. The broader effect is a compliance-led shift of volume toward better-capitalized lenders with deeper operational infrastructure.

Funding Cost Volatility Compresses Net Interest Margins

Funding cost volatility remains a direct restraint on the consumer finance market because retail lending economics depend on the spread between lender funding and customer pricing staying wide enough to absorb losses and operating costs. Banks are better insulated because deposit funding is usually more stable than wholesale or structured funding channels used by many non-bank lenders. This gap becomes more important when lenders are active in riskier borrower cohorts where higher expected loss must already be priced into the product. If wholesale funding reprices too quickly, some non-bank lenders either accept lower profitability or tighten credit standards, sacrificing volume. The pressure is especially visible in unsecured and subprime books, where delinquency and funding sensitivity can rise together rather than separately. At the same time, some large fintech lenders are actively locking in longer-duration facilities, and Klarna doubled its Elliott forward-flow facility to USD 2 billion in March 2026 to support up to USD 17 billion of United States financing loans[3]BUSINESSWIRE.COM Klarna and Elliott Deepen Partnership With $2bn Facility Supporting $17bn of US Financing Expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unsecured Lending Anchors Volume, Revolving Products Drive Rate

Unsecured Non-Revolving Credit held a 52% share in 2025, making it the largest product block in the consumer finance market. Personal loans, student loans, and healthcare financing supported this lead because they address recurring household needs across income groups and life stages. In the United States, unsecured personal loan balances reached USD 276 billion in Q4 2025 and were held by 26.4 million consumers, which shows how broad the installed borrower base has become. Fintech lenders accounted for 42% of those originations, indicating that digital delivery is expanding access, even within a product category still shaped by bank and lender underwriting discipline. Secured non-real estate credit also remained substantial because auto lending kept ticket sizes and account volumes high, with average new-vehicle financing reaching USD 44,495 and Q3 2025 auto originations rising to 6.7 million accounts.

Revolving Credit is projected to grow at a 7.9% CAGR through 2031, making it the fastest-growing product type in the consumer finance market mix. Card-based installment features are narrowing the gap between traditional revolving credit and stand-alone BNPL offers, which is changing how lenders position short-duration borrowing. Federal Reserve data showed revolving consumer credit grew 3.4% in 2025, and December 2025 annualized growth reached 12.6%, pointing to a strong year-end acceleration in usage. That pattern suggests consumers are still using revolving products actively even as refinancing options and installment alternatives remain available across digital channels. Education and medical finance continue to represent important underserved niches because cost pressure in both categories is sustaining borrowing demand even when household budgets are under strain.

By Lender: Banks Lead by Breadth, Fintechs Win on Speed and Inclusion

Banks held 61.9% share of the consumer finance market size in 2025, which kept them at the center of origination, funding, and servicing activity across regions. Their advantage comes from deposit-backed funding, established compliance systems, cross-sell reach, and long-standing customer relationships that lower acquisition costs over time. JPMorgan Chase opened 10.4 million new credit card accounts in 2025, and its consumer lending loan growth is expected to exceed the industry average in 2026, showing how scale supports continued expansion. That kind of operating breadth allows major banks to defend pricing and manage regulatory load more efficiently than smaller lenders can in many borrower segments. NBFCs also maintain a meaningful place in the consumer finance industry because they often serve borrowers who fall outside strict bank eligibility thresholds but still require formal credit.

Fintechs and digital lenders are projected to grow at 10.7% CAGR through 2031, the fastest pace among lender types in the consumer finance market. Their momentum comes from faster underwriting, broader use of transaction data, and mobile-first product design that aligns with how most borrowers now search, apply, and repay. In India, digital-first NBFCs sanctioned 13.2 crore personal loans worth INR 2.15 lakh crore (USD 25.4 billion), in FY26 and accounted for 77% of total personal loan volume. Nubank reported a USD 32.7 billion loan portfolio in Q4 2025, up 40% year over year, while its 90+ day NPL ratio held at 6.6%, which shows that rapid growth can still coexist with disciplined credit control. These results suggest that the consumer finance industry is rewarding lenders that combine inclusion, scale, and data-led underwriting rather than relying only on branch reach or product legacy.

By Distribution Channel: Branch Holds Scale, Digital Direct Sets the Pace

Branch/In-Person held a 38.1% share in 2025, indicating that physical distribution still matters in the consumer finance market for complex, secured, and documentation-heavy products. Auto loans, durable financing, and advisory-driven personal lending continue to benefit from face-to-face interaction where customers still value explanation, reassurance, and document support. This channel also remains important in local lending systems where trust is built through existing relationships and repeat borrower familiarity. Broker and agent models continue to bridge lender reach and borrower acquisition in markets where digital readiness is still uneven across customer groups and use cases. Branch presence, therefore, remains relevant because it supports scale in products where friction cannot yet be removed completely without affecting conversion or confidence.

Digital Direct is projected to grow at 9.5% CAGR through 2031, making it the fastest-growing distribution route in the consumer finance market. Its momentum comes from faster onboarding, reduced document friction, and underwriting that can run inside mobile apps, lender sites, and partner ecosystems with fewer manual steps. Lenders using API-led workflows can shorten approval cycles from days to minutes when identity, income, and account data are accessible in real time and can be processed consistently. This matters most in unsecured lending because approval speed directly influences conversion, acquisition cost, and the borrower’s willingness to complete the application. The active CFPB Section 1033 rule in the United States strengthens the data access framework that digital-direct lenders need for instant and accurate credit decisions at scale.

By Term Length: Medium-Term Dominates, Short-Term Reflects New Credit Behaviors

Medium-Term loans with tenors of 2 to 5 years held a 47.3% share in 2025, making them the largest maturity bucket in the consumer finance market. This profile aligns with the repayment horizons that are most common in auto and personal loans, where monthly affordability and lender risk models are already well understood. The segment benefits from established underwriting frameworks that can balance ticket size, repayment discipline, and expected borrower income with less volatility than very short or very long terms. It also gives borrowers a practical middle ground because installments remain manageable without extending repayment too far into the future. Long-term lending still plays an important role in renovation, durable goods, and other consumer use cases where larger balances require a longer payoff structure.

Short-Term credit is projected to grow at a 8.2% CAGR through 2031, giving it the fastest pace within the term-length categories in the consumer finance market. The normalization of BNPL and salary-linked micro-credit is supporting this shift toward products with shorter repayment cycles and quicker approval expectations. Federal Reserve analysis showed that pay-in-4 volume rose 80% from 2023 to 2025 and reached USD 78.3 billion in the United States, which confirms how quickly short-duration borrowing has scaled. As these products become more familiar, borrowers are increasingly treating short-duration credit as a routine cash flow tool rather than a narrowly defined payment novelty. This trend is encouraging lenders to refine underwriting for small-ticket products that require very fast approval, clear disclosures, and tighter loss management.

By Loan Purpose: Auto Anchors Scale, Debt Consolidation Signals Stress and Opportunity

Vehicle Purchase and Auto-related loans held a 27.6% share in 2025, making them the largest purpose segment in the consumer finance market. Auto credit continues to benefit from replacement demand, high ticket sizes, and financing dependency across both mature and emerging lending systems. In the United States, Q3 2025 auto originations increased 6.2% year over year to 6.7 million accounts, indicating that volume remained strong despite affordability pressures. Average amounts financed on new vehicles rose to USD 44,495, keeping origination values elevated even as household payment burdens tightened. Education, medical, travel, and consumer durable financing also add breadth to the purpose mix because they reflect recurring household spending pressure rather than only discretionary demand.

Debt Consolidation and Refinancing is projected to grow at 7.5% CAGR between 2026-2031, making it the fastest-growing use case in the consumer finance market. This pattern shows that borrowers are actively moving expensive revolving balances into installment products that offer more predictable monthly payments and better visibility on payoff timing. United States credit card balances reached USD 1.15 trillion in Q4 2025, which gives lenders a very large refinancing pool to target through digital and bank-led channels. Pre-approved consolidation offers inside card apps and digital banking journeys can capture this demand with lower acquisition cost than outbound solicitation or third-party lead generation. The segment therefore reflects both household budget strain and a practical product opportunity for lenders that already hold rich customer repayment and transaction data.

Geography Analysis

Asia-Pacific held a 43.3% share in 2025, making it the largest regional block in the consumer finance market. China’s consumer credit market, excluding housing loans, reached CNY 21.02 trillion (USD 2.9 trillion) in 2025 and grew 6.1% year over year, underscoring the region’s sheer scale even before housing exposure is considered. PBOC data for Q1 2026 then showed a 0.2% year-over-year decline in consumer loans excluding housing, marking the first contraction in this metric since 1995 Q3 and signaling tighter lending conditions. In India, retail credit originations rose 40% year over year by value and 27% by volume in Q1 2026, with gold loans and digital NBFCs driving much of the momentum. Southeast Asia adds further runway because underbanked populations, rising device access, and two-wheeler-to-car upgrade cycles continue to widen formal borrowing demand across several consumer segments.

North America remains the second-largest regional block in the consumer finance market, and total United States outstanding consumer debt reached USD 18.22 trillion in April 2026, while non-mortgage consumer debt stood at USD 4.69 trillion. TransUnion projected unsecured personal loan originations in the United States to grow 11.2% in 2026, which is stronger than overall credit expansion and keeps personal loans one of the region’s more active product lines. Alternative data underwriting is widening access for near-prime and subprime borrowers, especially in personal loans and digital card-linked products where decision speed matters. Canada broadly follows the United States pattern with a more gradual regulatory pace, while Mexico benefits from household cash flow support tied to cross-border remittance activity. The region also shows the clearest split between resilient super-prime borrowers and more stressed subprime cohorts, which is shaping portfolio strategy, pricing discipline, and lender product focus through the forecast period.

Middle East and Africa is projected to grow at 8.7% CAGR between 2026-2031, the fastest regional pace in the consumer finance market size outlook. Europe remains a large but more regulated lending block, while Middle East and Africa is expanding faster because installment use is rising from a lower formal credit base and digital distribution is spreading quickly. Open banking frameworks and regulatory sandboxes in the GCC are helping accelerate fintech credit origination, particularly in Saudi Arabia and the United Arab Emirates where digital finance adoption remains strong. South America also contributes meaningful scale, and Nubank plans to invest BRL 45 billion (USD 8.2 billion), in Brazil in 2026 while serving 113 million customers, which underlines the region’s importance in digital consumer lending growth.

Competitive Landscape

The consumer finance market is moderately fragmented, with large universal banks, diversified financial institutions, non-bank financial companies (NBFCs), fintech lenders, digital banks, and embedded finance providers competing across different customer segments. Major institutions such as JPMorgan Chase, BNP Paribas, and Industrial and Commercial Bank of China (ICBC) retain strong market positions due to their diversified funding sources, extensive customer bases, established risk management frameworks, and broad product portfolios. However, competition has intensified as fintech lenders, marketplace platforms, and embedded finance providers leverage digital distribution, automated underwriting, alternative data, and faster loan origination to target underserved and niche borrower segments. As a result, competitive differentiation in the consumer finance market is driven by funding efficiency, digital capabilities, customer experience, credit analytics, product innovation, and distribution partnerships, rather than branch networks or institutional scale alone.

Strategic moves in 2026 show that leading companies are investing in funding, distribution, and proprietary intelligence rather than relying only on volume growth to defend their position in the consumer finance market. In March 2026, Klarna doubled its forward-flow facility with Elliott to USD 2 billion, supporting up to USD 17 billion of United States financing loans and securing longer-dated capacity against short-term rate volatility. In May 2026, Affirm and Klarna both gained placement inside Google Search AI Mode and the Gemini app, pushing installment credit into AI-led shopping journeys rather than limiting it to traditional checkout placement. Nubank also detailed a proprietary AI strategy in June 2026, with nuFormer already live in Brazil’s largest credit segment and expanding into personal loans in Mexico and Colombia. These moves show that competitive advantage in the consumer finance market is shifting toward integrated distribution, scalable funding, and internal data assets that improve both conversion and servicing.

Banks still hold a strong base in prime and mainstream lending, yet fintechs are capturing faster growth where approval speed and inclusion matter more than physical presence in the consumer finance market. This is clear in India, where digital-first NBFCs accounted for 77% of total personal loan volume in FY26, and in Brazil, where Nubank reached 131 million customers and a USD 32.7 billion loan portfolio by Q4 2025. Competitive pressure is therefore rising across both customer acquisition and servicing efficiency, not only across headline origination volume. The consumer finance market should continue to reward lenders that combine disciplined underwriting with low-friction delivery, strong data systems, and stable access to funding across cycles.

Consumer Finance Industry Leaders

JPMorgan Chase and Co.

Bank of America Corporation

Citigroup Inc.

Wells Fargo and Company

American Express Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nubank detailed its AI transformation strategy anchored in a proprietary foundation model (nuFormer), trained on 600 billion behavioral tokens, now live in Brazil's largest credit segment and expanding to personal loans in Mexico and Colombia; the strategy targets closing the USD 16 average-revenue-per-user gap versus USD 40 at incumbent banks.

- May 2026: Klarna and Affirm both secured BNPL placement inside Google Search AI Mode and the Gemini app via Google Pay in the US, embedding consumer lending options into agentic commerce workflows as the next distribution frontier beyond traditional checkout.

- May 2026: SoFi Technologies launched SoFiUSD, the first bank-issued stablecoin offered by a United States nationally chartered bank on a public blockchain, partnering with Mastercard to enable SoFiUSD settlement across its global payments network, extending SoFi's 14.7 million-member base into on-chain consumer financial services.

- April 2026: Nubank announced BRL 45 billion (USD 8.2 billion) in investment in Brazil for 2026, targeting AI-driven credit models, new product launches, and infrastructure expansion across its 113-million-customer base, while extending its United States de novo bank charter strategy.

Global Consumer Finance Market Report Scope

| Revolving Credit | Credit Cards |

| Overdrafts/Credit Lines | |

| Unsecured Non-Revolving Credit | Personal Loans |

| Education/Student Loans | |

| Medical/Healthcare Loans | |

| Other Unsecured Consumer Loans | |

| Secured Non-Real Estate Credit | Auto/Vehicle Finance Loans |

| Other Secured Consumer Loans (e.g., Consumer Durables, Equipment) |

| Banks |

| Non-Bank Financial Companies (NBFCs) |

| Fintechs and Digital Lenders (including Marketplace and Embedded Finance Platforms) |

| Other (Credit Unions, Cooperatives, etc.) |

| Digital Direct |

| Branch/In-Person |

| Broker/Agent |

| Embedded Finance/Point-of-Sale |

| Short-Term (Up to 2 years) |

| Medium-Term (2–5 years) |

| Long-Term (More than 5 years) |

| Debt Consolidation/Refinancing |

| Vehicle Purchase/Auto-related |

| Education |

| Medical/Healthcare Expenses |

| Travel |

| Consumer Durables |

| Other Personal/Household Purposes |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Revolving Credit | Credit Cards |

| Overdrafts/Credit Lines | ||

| Unsecured Non-Revolving Credit | Personal Loans | |

| Education/Student Loans | ||

| Medical/Healthcare Loans | ||

| Other Unsecured Consumer Loans | ||

| Secured Non-Real Estate Credit | Auto/Vehicle Finance Loans | |

| Other Secured Consumer Loans (e.g., Consumer Durables, Equipment) | ||

| By Lender | Banks | |

| Non-Bank Financial Companies (NBFCs) | ||

| Fintechs and Digital Lenders (including Marketplace and Embedded Finance Platforms) | ||

| Other (Credit Unions, Cooperatives, etc.) | ||

| By Distribution Channel | Digital Direct | |

| Branch/In-Person | ||

| Broker/Agent | ||

| Embedded Finance/Point-of-Sale | ||

| By Term Length | Short-Term (Up to 2 years) | |

| Medium-Term (2–5 years) | ||

| Long-Term (More than 5 years) | ||

| By Loan Purpose | Debt Consolidation/Refinancing | |

| Vehicle Purchase/Auto-related | ||

| Education | ||

| Medical/Healthcare Expenses | ||

| Travel | ||

| Consumer Durables | ||

| Other Personal/Household Purposes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for consumer finance?

The consumer finance market is forecast to grow from USD 10.44 trillion in 2026 to USD 14.08 trillion by 2031 at a 6.2% CAGR.

Which product category holds the largest share in consumer lending?

Unsecured Non-Revolving Credit led in 2025 with a 52% share, supported by personal loans, education credit, and healthcare finance.

Which lender group is expanding the fastest through 2031?

Fintechs and digital lenders are projected to grow at a 10.7% CAGR, ahead of other lender types, driven by faster underwriting and broader data use.

Why is digital direct lending gaining momentum?

Digital Direct is projected to grow at 9.5% CAGR because lenders can reduce document friction, speed up approvals, and use real-time data inside apps and digital journeys.

Which region leads global volume in consumer lending?

Asia-Pacific led with a 43.3% share in 2025, supported by large-scale credit activity in China, strong retail credit momentum in India, and continued runway across Southeast Asia.

What loan purpose is growing fastest in the next five years?

Debt Consolidation and Refinancing is forecast to grow at a 7.5% CAGR, helped by elevated credit card balances and strong demand for installment-based refinancing.

Page last updated on: