Asia-Pacific Private Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 44.30 Billion |

| Market Size (2026) | USD 48.63 Billion |

| Market Size (2031) | USD 77.48 Billion |

| Growth Rate (2026 - 2031) | 9.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Private Banking Market Analysis by Mordor Intelligence

The Asia-Pacific Private Banking Market size is projected to be USD 44.30 billion in 2025, USD 48.63 billion in 2026, and reach USD 77.48 billion by 2031, growing at a CAGR of 9.77% from 2026 to 2031.

Asia remains the world’s main engine of growth in 2026 after contributing a majority share of the expansion in 2025 and 2026, which keeps the Asia-Pacific Private Banking Market firmly positioned at the center of global wealth creation. Demand is shaped by multi-year shifts such as intergenerational wealth transfer, professionalization of family capital, and cross-border mobility that reward institutions with scale and strong booking-center connectivity. Regulatory programs in Hong Kong and Singapore deepen cross-boundary distribution and reporting alignment, which supports portable mandates and larger advised balances across the Asia-Pacific Private Banking Market. The opportunity set is also reinforced by stable institutional sponsors and thematic demand in digital infrastructure, climate transition, and healthcare innovation that help clients diversify outcomes in the Asia-Pacific Private Banking Market.

Key Report Takeaways

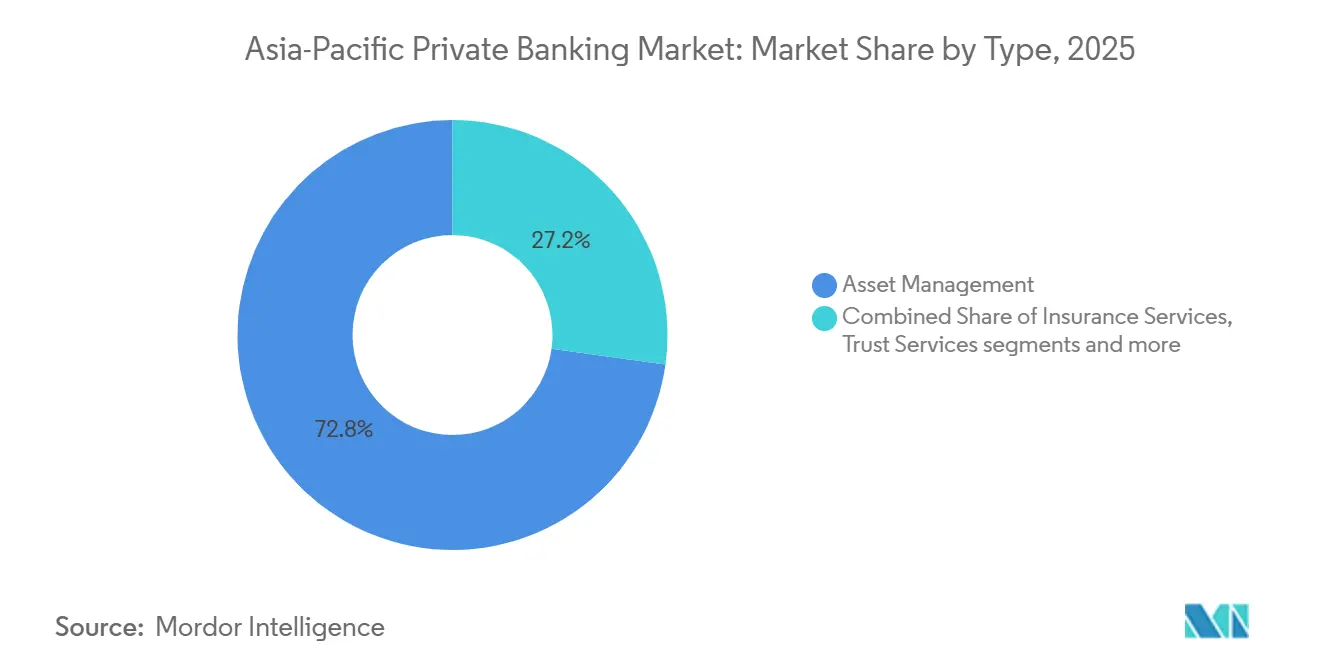

- By type, Asset Management led with 72.80% share of the Asia-Pacific Private Banking market size in 2025 and is projected to post the fastest 12.80% CAGR through 2031.

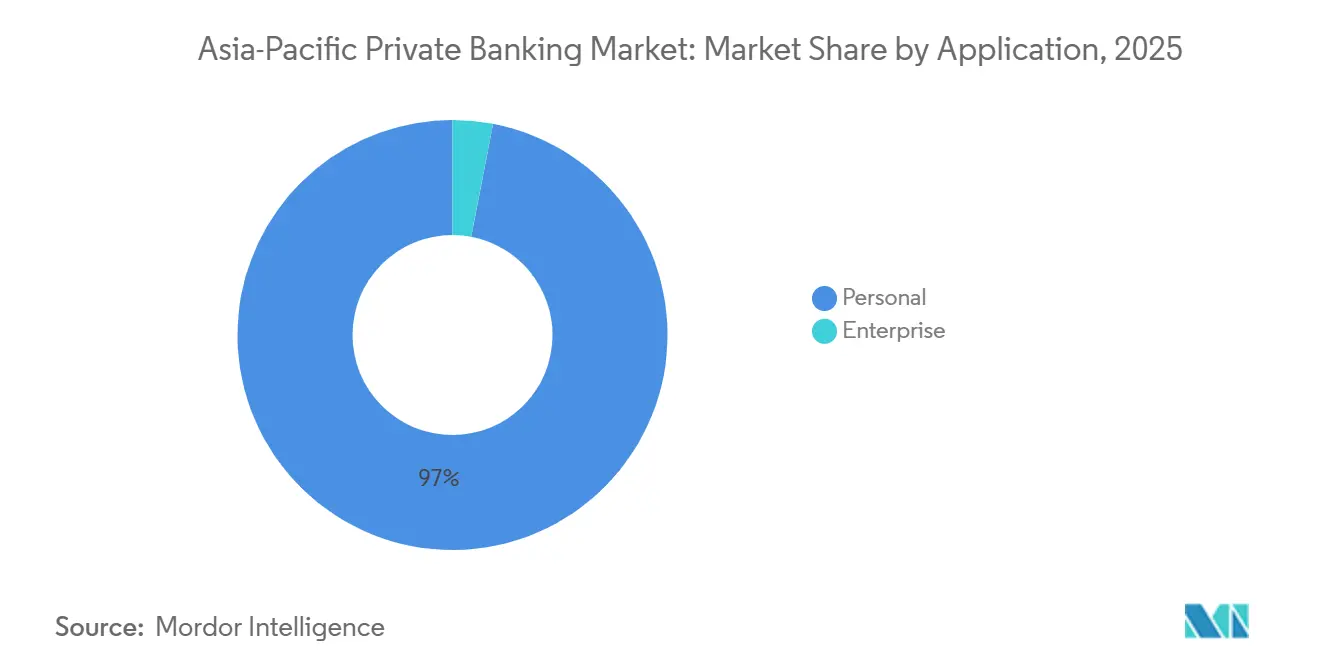

- By application, the Personal segment accounted for 96.99% of the Asia-Pacific Private Banking market size in 2025 and is forecast to grow at 12.00% CAGR through 2031.

- By geography, China held 30.50% of the Asia-Pacific Private Banking market size in 2025, while Southeast Asia is set to expand at an 11.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Private Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of HNWI & UHNW populations | +2.8% | Global, with concentration in China, India, Hong Kong, Singapore | Medium term (2-4 years) |

| Significant inter-generational wealth transfer trends | +2.1% | APAC core, particularly Hong Kong, Singapore, China, and India | Long term (≥ 4 years) |

| Growth of family offices in Hong Kong and Singapore | +1.5% | Hong Kong & Singapore, with spillover to Southeast Asia | Medium term (2-4 years) |

| Increasing demand for alternative and sustainable assets | +1.3% | Global, led by Singapore, Hong Kong, and Australia | Medium term (2-4 years) |

| Rising popularity of cross-border wealth passporting programs | +1.2% | Hong Kong & Singapore are primary hubs, with reach to Greater China and ASEAN | Medium term (2-4 years) |

| Productivity gains from AI-enabled hybrid advisory services | +0.9% | Global, with early adoption in Singapore, Hong Kong, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of HNWI & UHNW Populations Fuels Sophisticated Mandate Demand

Asia continues to generate a rising share of world output and wealth in 2026, which sustains the client base of the Asia-Pacific Private Banking Market and accelerates the need for sophisticated multi-asset portfolios. As Asia contributes most of the global growth in 2025 and 2026, more entrepreneurs and founders monetize equity and channel proceeds into discretionary mandates and cross-border custody within the Asia-Pacific Private Banking Market. Policy tools that enable cross-boundary investment, such as Hong Kong’s enhanced Wealth Management Connect framework, improve the portability of client assets and support larger advised balances across booking centers [1]Eddie Yue, “Eddie Yue on Hong Kong’s Wealth Management Market,” Hong Kong Monetary Authority, hkma.gov.hk. Younger inheritors in the region expect seamless, real-time advice with transparent fees, which pushes banks to blend human expertise with digital engagement models in the Asia-Pacific Private Banking Market. Authorities are also aligning cross-border reporting on digital assets and more standardized disclosures, which allows private banks to design broader product menus while preserving compliance standards across the Asia-Pacific Private Banking Market. This combination of macro momentum, policy support, and client expectations strengthens demand for discretionary management, alternative access, and trust solutions that are central to the Asia-Pacific Private Banking Market.

Significant Inter-Generational Wealth Transfer Trends Reshape Legacy Planning

The Asia-Pacific Private Banking Market stands at the leading edge of intergenerational wealth transfer, with banks reporting multi-trillion-dollar transitions underway that will change portfolio goals, time horizons, and governance needs. Banks are formalizing advisory frameworks that link near-term liquidity, mid-term compounding, and long-term legacy protection through insurance and trust structures in response to client demand in the Asia-Pacific Private Banking Market. This shift brings greater interest in impact strategies and private markets allocations as heirs weigh value-based outcomes alongside returns. Financial institutions also emphasize founder-to-heir education and family governance, which helps clients prevent fragmentation of wealth across generations and maintains long-term banking relationships in the Asia-Pacific Private Banking Market. [2]Standard Chartered, “Inheritance Meets Innovation: The Future of Wealth in Asia,” Standard Chartered, sc.com Cross-border booking and multi-jurisdictional trust capabilities are rising in importance as families split residence and operating footprints between hubs like Singapore and Hong Kong. The depth of this demographic shift continues to steer product roadmaps, risk management, and service design across the Asia-Pacific Private Banking Market.

Growth of Family Offices in Hong Kong and Singapore Concentrates Expertise

Family offices in Hong Kong and Singapore continue to concentrate specialist talent, direct-investing know-how, and governance expertise, which creates high-value servicing opportunities for the Asia-Pacific Private Banking Market. Authorities in both hubs have refreshed program and tax frameworks to attract sophisticated capital, which directs more mandate flow to onshore and offshore platforms that private banks operate in the Asia-Pacific Private Banking Market. Institutional sponsors in the region report steady demand for private equity, real assets, and credit across cycles, which aligns with the portfolio design goals of single and multi-family offices. As founders implement succession plans, the advisory mix shifts toward trusts, governance, and direct deals, which increases the need for dedicated family office coverage desks in the Asia-Pacific Private Banking Market. Private banks that build scalable servicing stacks around reporting, co-investment pipelines, and cross-border tax-substance requirements are well placed to win share of wallet from institutionalizing families in the Asia-Pacific Private Banking Market. This concentration of expertise in the two hubs underpins a durable flywheel of capital formation, investment access, and talent development across the Asia-Pacific Private Banking Market.

Increasing Demand for Alternative and Sustainable Assets Diversifies Portfolios

As rates normalize and dispersion rises, clients seek growth and resilience through private markets, sustainable strategies, and transition-linked themes within the Asia-Pacific Private Banking Market. Asset managers in the region highlight structured opportunities in climate finance, including transition technologies, which channel private capital toward measured decarbonization paths that clients value. Regional outlooks show continued interest in multi-asset and income strategies due to earnings visibility and cash flow support, which complements private credit, infrastructure, and secondaries. Wealth managers package access to private equity, healthcare innovation, and logistics themes through curated programs that improve transparency and ease of monitoring for Asia-Pacific Private Banking Market clients. Global private banks also frame sustainable allocations with clearer reporting against client objectives, which aligns values with performance in the Asia-Pacific Private Banking Market. This ongoing rotation toward alternatives and sustainability expands advisory depth and strengthens client stickiness across the Asia-Pacific Private Banking Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing costs of AML/CRS compliance | -1.4% | Global, with heightened burden in Hong Kong, Singapore | Medium term (2-4 years) |

| Shortage and rising expenses of experienced relationship managers | -0.9% | APAC core, especially Hong Kong, Singapore | Short term (≤ 2 years) |

| Geopolitical factors driving asset relocation from key hubs | -0.6% | Hong Kong, with a selective impact on mainland China-linked flows | Medium term (2-4 years) |

| Fee compression in WealthTech entry-level segments | -0.7% | Global, pronounced in Singapore, Australia, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Costs of AML/CRS Compliance Strain Operating Leverage

Private banks face heavier compliance tasks, such as cross-border reporting and digital asset disclosure frameworks expanding across Asia, which lifts cost-to-serve and slows product velocity within the Asia-Pacific Private Banking Market. Authorities are preparing to implement the Cryptoasset Reporting Framework and other enhancements to tax transparency, which require significant upgrades to data, controls, and client lifecycle processes in the Asia-Pacific Private Banking Market. Supervisors in Hong Kong are also building new supervisory technology to increase the effectiveness of risk monitoring, which reinforces the need for scalable compliance infrastructure across the Asia-Pacific Private Banking Market. Firms with multi-jurisdictional clients must harmonize documentation, screening, and monitoring standards across booking centers to reduce friction for legitimate customers. The near-term effect is sustained investment in technology and operations, which favors scale players in the Asia-Pacific Private Banking Market. Over time, more risk-based supervision can reduce duplicative effort, but the transition raises operating complexity for the Asia-Pacific Private Banking Market.

Shortage and Rising Expenses of Experienced Relationship Managers Elevate Talent Costs

Demand for seasoned relationship managers outpaces supply in core hubs as client needs become multi-jurisdictional and cross-product, which raises hiring and retention costs across the Asia-Pacific Private Banking Market. Entrepreneur-led wealth and next-generation inheritors often require structured lending, business transition planning, and family governance, which increases the premium on advisors with broad technical fluency in the Asia-Pacific Private Banking Market. Banks respond by expanding training programs and career pathways to build capacity for high-quality advisory at scale in the Asia-Pacific Private Banking Market. Institutions also invest in workflow tools and model portfolios to free front-office time for client engagement rather than administration in the Asia-Pacific Private Banking Market. Talent depth remains a strategic differentiator, which sustains competition for bilingual and culturally fluent advisors across the Asia-Pacific Private Banking Market. The imbalance between demand and supply of experienced coverage teams continues to influence cost-income outcomes in the Asia-Pacific Private Banking Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Asset Management Dominates with Strongest Momentum

Asset Management accounted for 72.80% of the Asia-Pacific Private Banking market share in 2025 and is projected to grow at a 12.80% CAGR through 2031 as clients deepen discretionary mandates and broaden alternatives access. The service stack strengthens with model portfolios, risk analytics, and curated co-investments that improve consistency and transparency for the Asia-Pacific Private Banking Market. Regulatory programs that expand cross-boundary distribution and tokenization pilots also support scalable product manufacturing for Asset Management in the Asia-Pacific Private Banking Market. Hong Kong’s continued effort to deepen wealth connectivity with the mainland gives managers a wider investor base and a stronger platform to deliver institutional-grade solutions. Combined with client preference for diversified income and growth, this ecosystem positions Asset Management to keep leading the Asia-Pacific Private Banking Market.

Trust Services, Insurance Services, and advisory-led consulting remain essential complements as families formalize governance and succession structures across the Asia-Pacific Private Banking Market. Portfolio construction now embeds ESG and transition metrics more routinely, which requires accurate disclosure and third-party data integration for private clients in the Asia-Pacific Private Banking Market. Tokenization pilots and digital bond issuance roadmaps suggest a path to lower friction in distribution and secondary liquidity, which could widen the addressable base for institutional-quality strategies over time. As coverage teams adopt AI-enabled tooling to improve proposal speed and risk monitoring, asset management capabilities become more repeatable and scalable within the Asia-Pacific Private Banking Market. The result is a deeper and wider platform that continues to anchor revenue and client outcomes across service lines in the Asia-Pacific Private Banking Market.

By Application: Personal Segment Commands Near-Exclusive Share

The Personal segment held 96.99% of the Asia-Pacific Private Banking market size in 2025 and is forecast to grow at a 12.00% CAGR through 2031, reflecting the individual and family focus that defines this business. Entrepreneur and founder wealth continues to shape needs around liquidity, exits, and legacy, which aligns with bespoke lending, governance, and discretionary management offerings across the Asia-Pacific Private Banking Market. Intergenerational handovers increase demand for trusts, insurance-based solutions, and next-gen education that banks are formalizing into structured advice programs in the Asia-Pacific Private Banking Market. The depth of mobile and digital adoption in core hubs encourages 24/7 engagement expectations, which continue to pull banks toward hybrid advisory for the Asia-Pacific Private Banking Market. Personal segment dynamics are therefore unlikely to change in the forecast period as institutions invest to match client preferences across channels and jurisdictions in the Asia-Pacific Private Banking Market.

The Enterprise segment remains small but relevant for select use cases such as pre-liquidity planning for founders and employee wealth programs, where private banking can complement corporate banking. Institutions with integrated wholesale and private platforms can cross-originate opportunities that fit personal mandates while preserving corporate-banking guardrails in the Asia-Pacific Private Banking Market. Banks also expand utility services like securities lending access for clients seeking incremental portfolio income, which links enterprise-grade market infrastructure to personal portfolios in the Asia-Pacific Private Banking Market. As product access, reporting, and cross-border frameworks continue to improve, the personal segment keeps its dominant position while Enterprise-linked flows stay complementary within the Asia-Pacific Private Banking Market. The interplay of advisory depth, digital convenience, and global connectivity underpins the growth runway for personal mandates in the Asia-Pacific Private Banking Market.

Geography Analysis

China accounted for 30.50% of the Asia-Pacific Private Banking market size in 2025, while Southeast Asia is projected to deliver the fastest 11.00% CAGR through 2031 due to favorable demographics and policy clarity in priority hubs. Hong Kong continues to operate as an offshore command center for China’s international investors, with enhanced cross-boundary schemes and product access that support connectivity for the Asia-Pacific Private Banking Market. Singapore’s regulatory predictability and family office programs draw entrepreneurs and inheritors who diversify holdings globally across the Asia-Pacific [3]Private Banking Market. HSBC Private Banking, “Singapore Leads Global Entrepreneur Migration,” HSBC, privatebanking.hsbc.com. India, Japan, South Korea, and Australia each contribute meaningful client demand through different channels, which broadens the regional base for the Asia-Pacific Private Banking Market. A multi-hub approach helps institutions capture flows as clients rebalance between onshore and offshore exposures in the Asia-Pacific Private Banking Market.

Hong Kong’s Wealth Management Connect and related programs continue to evolve, which brings more flexibility to product scope and investor participation for the Asia-Pacific Private Banking Market. Singapore’s ongoing work on capital markets tokenization and industry frameworks signals a clear path for digital asset rails that can integrate with private wealth distribution over time in the Asia-Pacific Private Banking Market. Australia’s superannuation system maintains significant institutional capital that can complement private wealth allocations and structures across the Asia-Pacific Private Banking Market. Japan advances corporate reform and balance sheet optimization, which supports private activity and exits that recycle into managed wealth programs in the Asia-Pacific Private Banking Market. Southeast Asia’s technology and consumer ecosystems expand the base of future wealth creators, which sustains long-term demand for advisory and investment solutions in the Asia-Pacific Private Banking Market.

Regional integration through trade and regulatory frameworks will keep shaping where assets are booked and how products are distributed across the Asia-Pacific Private Banking Market. Banks benefit from building capabilities in multiple centers to match client footprints and ensure resiliency in operating models for the Asia-Pacific Private Banking Market. Product innovation and better disclosure standards around sustainability and digital assets also support investor protection and confidence in the Asia-Pacific Private Banking Market. As connectivity between North Asia and Southeast Asia grows, cross-border planning, lending, and investment continue to expand in scope within the Asia-Pacific Private Banking Market. These dynamics anchor the long-term growth narrative that supports robust client outcomes in the Asia-Pacific Private Banking Market.

Competitive Landscape

The Asia-Pacific Private Banking Market shows moderate concentration with several universal banks, regional champions, and focused boutiques competing on scale, product depth, and talent. Institutions with strong onshore platforms in China and balanced offshore hubs in Hong Kong and Singapore hold structural advantages in client acquisition and cross-selling breadth across the Asia-Pacific Private Banking Market. Firms differentiate by offering curated access to private markets, sustainability themes, and enhanced reporting for transparency across the Asia-Pacific Private Banking Market. Hybrid advisory models underpin productivity and scalability, while high-touch coverage remains vital for ultra-high-net-worth clients in the Asia-Pacific Private Banking Market. Regional connectivity and governance track records continue to drive client trust and long-term share of wallet within the Asia-Pacific Private Banking Market.

Leading players are rolling out targeted initiatives that match the evolving needs of founders and inheritors. One example is a life-stage advisory framework that organizes liquidity, compounding, and legacy planning to simplify decision-making for families in the Asia-Pacific Private Banking Market. Another is the launch of digital platforms that give clients always-on visibility into private asset data and strategy updates, which supports transparency in the Asia-Pacific Private Banking Market. Banks also introduce new securities financing and lending access features that help clients optimize collateral and portfolio yield in the Asia-Pacific Private Banking Market. Regional boutiques with strong cultural fluency and family office relationships continue to compete through personalization and cross-border networks in the Asia-Pacific Private Banking Market.

Looking ahead, three competitive levels are prominent across the region. First, the ability to manufacture and distribute multi-asset strategies, including private credit and transition-linked themes, remains central for the Asia-Pacific Private Banking Market. Second, continued investment in data and AI improves advice quality and risk management, which strengthens scalability without diluting client intimacy in the Asia-Pacific Private Banking Market. Third, strategic positioning across Hong Kong and Singapore, combined with selective presence in priority onshore markets, helps institutions manage policy and geopolitical risk in the Asia-Pacific Private Banking Market. These themes point to steady consolidation among mid-tier firms and targeted expansion by scale leaders in the Asia-Pacific Private Banking Market.

Asia-Pacific Private Banking Industry Leaders

UBS Global Wealth Management

J.P. Morgan Private Bank

DBS Private Bank

Bank of Singapore

HSBC Global Private Banking

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: OCBC Bank launched a securities lending program in collaboration with Citi Securities Lending Access Platform, enabling OCBC Securities and Bank of Singapore customers to lend idle assets to institutional borrowers. The bank formed a specialist securities financing unit led by Jansen Chua to capitalize on rising institutional demand, expanding portfolio utility for wealth clients.

- October 2025: HSBC Private Bank launched an enhanced entrepreneurial wealth proposition in Singapore that integrates Global Private Banking with Corporate and Institutional Banking capabilities. The initiative supports entrepreneurs through growth, IPO preparation, and succession planning, including an Innovation Exchange that connects clients with ventures in Asia’s innovation economy.

- October 2025: OCBC Bank launched a wealth advisory upskilling program for mortgage specialists to deepen client relationships across wealth and banking services. The program equips specialists to provide holistic advisory services beyond home loans for affluent customers across the region.

- August 2025: The Monetary Authority of Singapore advanced tokenization in financial services through industry frameworks, market infrastructure work, and commercial networks. MAS also introduced the Global-Asia Digital Bond Grant Scheme in January 2025 with grants of up to 30% of eligible expenses for qualifying issuers until December 31, 2029, to catalyze digital bond issuance.

Asia-Pacific Private Banking Market Report Scope

Private banking refers to the provision of personalized financial services and products to high-net-worth individuals (HNWIs). It encompasses a broad spectrum of wealth management solutions, delivered seamlessly under a single institutional framework for client convenience.

The Asia-Pacific private banking market report is segmented by type (asset management, insurance services, trust services, tax consulting, real-estate consulting), application (personal, enterprise), and geography (China, India, Japan, South Korea, Australia, Southeast Asia, Rest of Asia Pacific). The market forecasts are provided in terms of value (USD Billion).

| Asset Management |

| Insurance Services |

| Trust Services |

| Tax Consulting |

| Real-Estate Consulting |

| Personal |

| Enterprise |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Southeast Asia(Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) |

| Rest of Asia Pacific |

| By Type | Asset Management |

| Insurance Services | |

| Trust Services | |

| Tax Consulting | |

| Real-Estate Consulting | |

| By Application | Personal |

| Enterprise | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia(Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the Asia-Pacific Private Banking Market growth outlook to 2031?

The Asia-Pacific Private Banking Market is expected to expand from USD 48.63 billion in 2026 to USD 77.48 billion by 2031 at a 9.77% CAGR, supported by Asia's role as the global growth engine and stronger cross-border connectivity.

Which service type leads the Asia-Pacific Private Banking Market today?

Asset Management leads with a 72.80% share in 2025 and is projected to grow at a 12.80% CAGR through 2031 as clients deepen discretionary mandates and alternatives access.

Which client segment drives the most Asia-Pacific Private Banking Market revenues?

The personal segment accounts for 96.99% in 2025 and is set to grow at a 12.00% CAGR, driven by entrepreneur wealth, intergenerational transfers, and multi-jurisdictional planning needs.

Which geographies are most influential in the Asia-Pacific Private Banking Market?

China holds 30.50% in 2025, while Southeast Asia is projected to grow the fastest at 11.00% CAGR due to supportive policies in hubs like Hong Kong and Singapore and broader regional demographic momentum.

How are regulations shaping the Asia-Pacific Private Banking Market?

Enhancements to Hong Kong’s cross-boundary programs and Singapore’s tokenization and market-structure initiatives are improving product access, reporting alignment, and investor protections across hubs.

What themes are shaping client portfolios in the Asia-Pacific Private Banking Market?

Clients are increasing allocations to private markets and sustainable strategies and are adopting hybrid advisory that blends model portfolios with personalized coverage to improve resilience and transparency.

Page last updated on: