United States Private Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

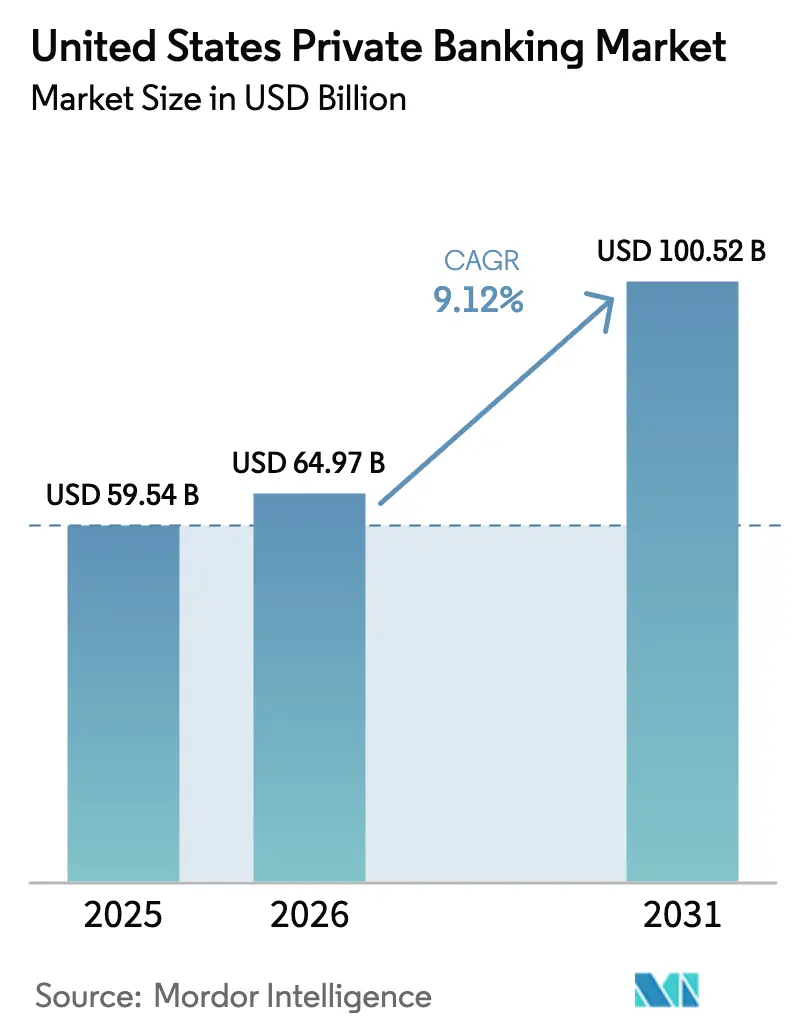

| Base Year Market Size (2025) | USD 59.54 Billion |

| Market Size (2026) | USD 64.97 Billion |

| Market Size (2031) | USD 100.52 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Private Banking Market Analysis by Mordor Intelligence

The United States private banking market size is expected to grow from USD 59.54 billion in 2025 to USD 64.97 billion in 2026 and is forecast to reach USD 100.52 billion by 2031 at 9.12% CAGR over 2026-2031. Expansion is fueled by robust demographic wealth creation, the rollout of SECURE Act 2.0 rollover incentives that convert retirement savers into fee-based advisory relationships, and rapid digitization that blends high-touch advice with AI-enabled scale. Client appetite for alternative assets, especially private credit and direct real-estate exposure, is lifting fee pools as private banks integrate specialized product desks within core advisory platforms. Meanwhile, wealth migration toward tax-advantaged states and technology hubs is reshaping regional competitive dynamics, prompting banks to expand branch footprints while doubling down on digital service delivery. Regulatory demands under Reg BI and heightened cybersecurity standards are raising fixed costs, giving scale-advantaged incumbents room to widen operational moats while forcing niche providers to differentiate through family-office style services and localized expertise.

Key Report Takeaways

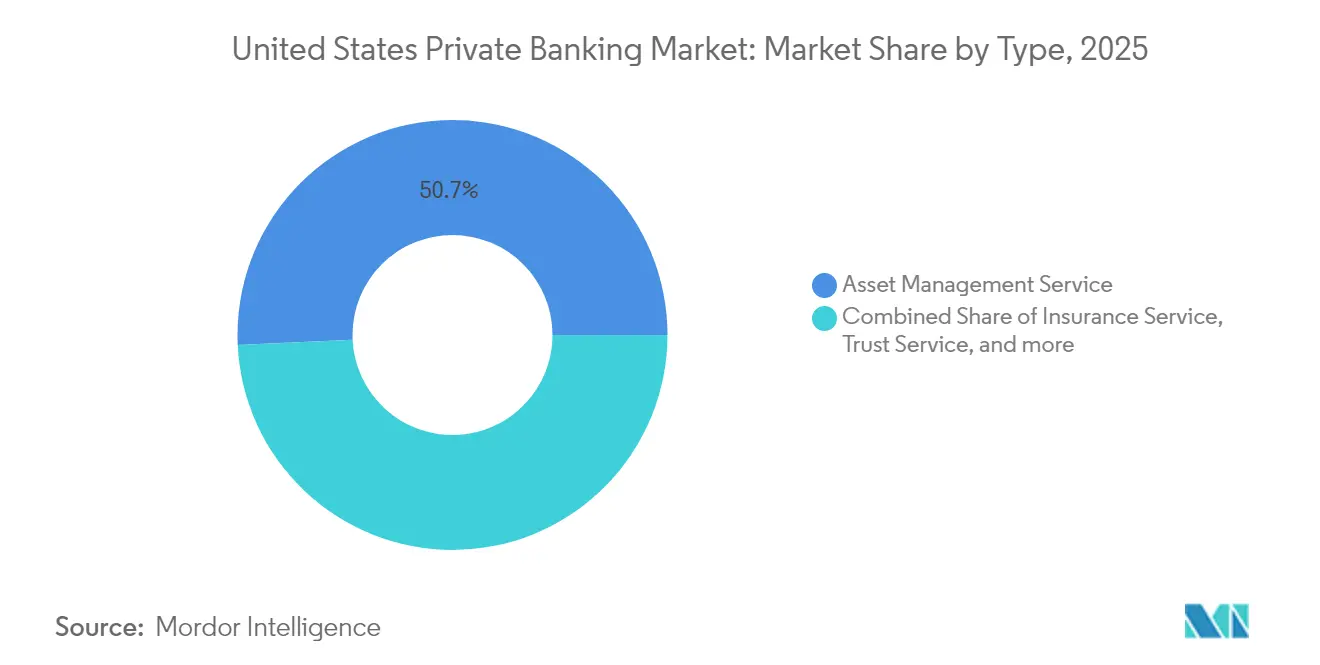

- By service type, asset management held 50.74% of the United States private banking market share in 2025, while real-estate consulting is forecast to grow at an 7.94% CAGR to 2031.

- By application, personal banking commanded 72.15% of the United States private banking market size in 2025, whereas enterprise services are advancing at a 7.28% CAGR through 2031.

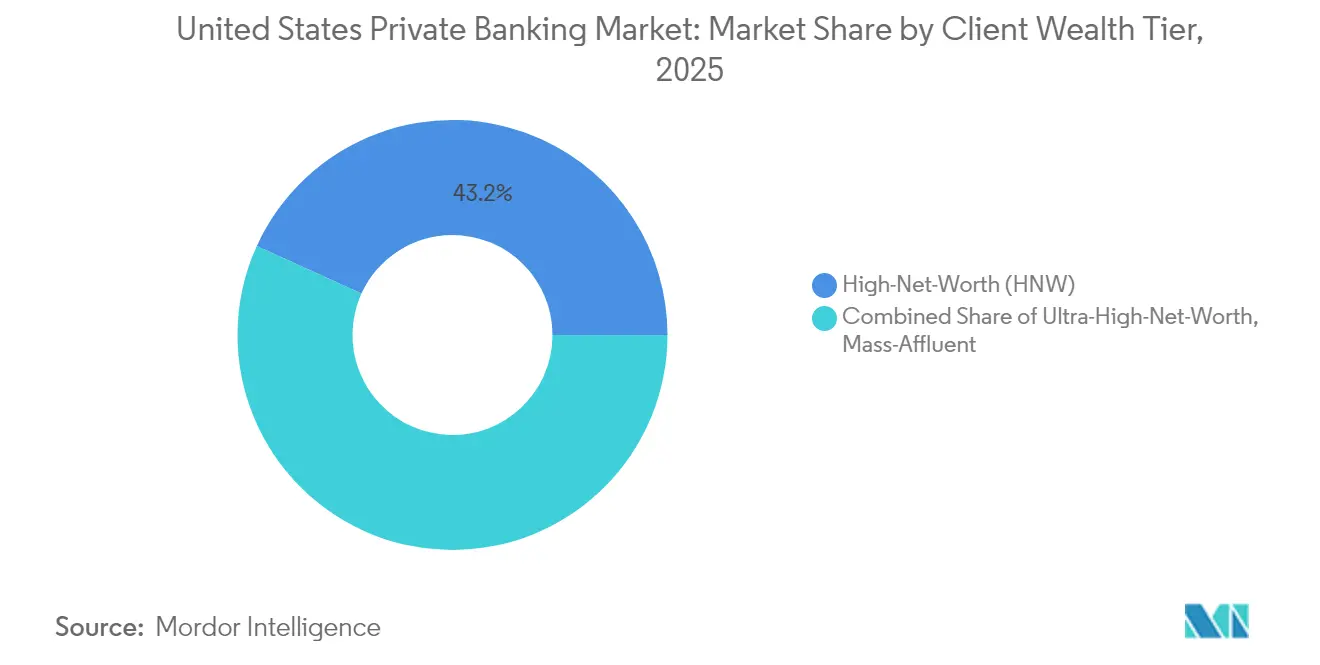

- By client wealth tier, high-net-worth clients accounted for 43.21% of the United States private banking market size in 2025; the ultra-high-net-worth segment is expanding at a 9.39% CAGR over 2026-2031.

- By geography, the Northeast led with 35.12% of the United States private banking market share in 2025, while the West is expected to record the fastest 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Private Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HNW population & investable assets | +2.8% | Global, concentrated in Northeast, West, South | Long term (≥ 4 years) |

| Heightened demand for holistic planning & family-office style services | +2.1% | National, strongest in Northeast and West | Medium term (2-4 years) |

| Digital-first & hybrid advisory adoption surge | +1.9% | National, led by West Coast innovation hubs | Short term (≤ 2 years) |

| Appetite for alternative / private-market products | +1.6% | National, UHNW concentrated in Northeast, West | Medium term (2-4 years) |

| Banks' private-credit distribution partnerships expand fee pools | +0.8% | National, strongest in financial centers | Medium term (2-4 years) |

| SECURE Act 2.0 rollover incentives convert retirement savers to advice relationships | +0.5% | National, concentrated in high-income regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising HNW and UHNW Population

The United States counts more than 23 million millionaires in 2025, up 7% from 2024 as continued equity and property appreciation accelerates capital formation among entrepreneurs and technology founders[2]Source: UBS, “Family Office Report 2025,” ubs.com. UHNW households average USD 2.7 billion in net worth, fueling demand for concierge-level services such as direct investment sourcing, philanthropic structuring, and multi-jurisdictional estate planning. Inbound wealth programs—most notably the EB-5 investor visa—keep channeling foreign capital into U.S. private banking pipelines, solidifying the client base in coastal wealth centers. Private banks with proven cross-border tax expertise and family-office infrastructure are capturing outsized wallet share as new UHNW entrants seek institutional-grade governance. The demographic tailwind remains pronounced through 2030 as generational wealth transfer picks up pace, ensuring a steady inflow of assets under management.

Heightened Demand for Holistic Planning and Family-Office Style Services

A 2025 industry survey shows 91% of affluent clients want integrated tax, estate, and philanthropic advice, yet fewer than 25% report receiving it today[3]Source: Bank of America, “Specialty Asset Management,” bankofamerica.com. The gap is driving banks to add trust attorneys, in-house CPAs, and real-estate consultants who can bundle traditionally siloed services into a single relationship. Family-office assets under administration in North America are on track to rise from USD 3.1 trillion in 2024 to nearly USD 5.4 trillion by 2030, highlighting the white-space opportunity for institutions that can scale boutique-level attention without eroding margins. Younger wealth holders emphasize ESG screening and impact investing, prompting banks to embed sustainability analytics into proposal tools and manager research workflows. The demand for holistic stewardship also expands annuity-like fee revenue, improving earnings visibility amid cyclical market swings.

Digital-First and Hybrid Advisory Adoption

Generative AI reached mainstream deployment in January 2025 when Goldman Sachs rolled out an assistant that drafts research summaries, crafts client emails, and automates trade recommendations[4]Source: Goldman Sachs, “AI Assistant Deployment,” goldmansachs.com.. Large banks are following suit, combining machine-generated insights with human oversight to deliver personalized portfolios at scale. Hybrid models that pair virtual onboarding with periodic in-person strategy reviews reduce servicing costs by up to 35% while preserving the trust component crucial for high-value relationships. Clients now expect seamless omni-channel access—mobile messaging, secure document vaults, and video consultations—driving platform modernization roadmaps across the sector. Institutions lacking modern tech stacks risk share erosion as digitally native competitors woo mass-affluent customers with lower fees and frictionless interfaces. Still, early adopters note rising compliance and data-governance spend, reinforcing the advantage held by balance-sheet strong incumbents.

Persistently low yields on traditional fixed income portfolios have pivoted wealth flows toward private credit, secondary PE funds, and real-estate syndications. U.S. Bank grew its private-credit platform 40% year over year in 2025 through distribution pacts that slice institutional-grade funds into USD 250,000 minimums for qualified buyers. Larger players such as Bank of America now oversee more than USD 13 billion in specialty assets, a metric that includes timberland, farmland, and mineral rights. Direct property services are gaining steam: clients request market-level due-diligence, lease-up monitoring, and 1031-exchange execution, pushing real-estate consulting to the fastest CAGR across service lines. For banks, alternatives bolster fee spreads and deepen stickiness but escalate due-diligence burdens, favoring institutions with robust manager-selection frameworks and conflict-mitigation protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from robo-advice and passive products | -1.4% | Nationwide, acute in mass-affluent | Short term (≤ 2 years) |

| Intensifying regulatory scrutiny | -0.9% | Major financial centers | Medium term (2-4 years) |

| Advisor talent war inflates compensation & churn risk | -1.1% | Major urban wealth centers | Medium term (2–4 years) |

| Escalating cyber-security / data-leak compliance costs | -0.8% | Nationwide, with cross-border implications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fee Compression from Robo-Advice and Passive Products

Assets managed by automated platforms topped USD 1 trillion in 2025, with Vanguard alone controlling USD 312 billion in digital advice mandates. As passive ETFs proliferate at sub-10 basis-point fees, price sensitivity bleeds into human-advised relationships, especially for portfolios under USD 1 million. Banks answer by embedding robo-allocation modules within full-service mandates, offering tiered pricing that preserves margin while signaling value transparency. Some early entrants have shuttered standalone robo tools after discovering thin economics, underscoring that trust-based counsel rather than price leadership remains the primary retention lever for high-balance households. Nonetheless, the secular fee-compression trend forces continuous efficiency upgrades, including straight-through account opening and AI-driven compliance checks, to keep cost-to-income ratios in check.

Intensifying Regulatory Scrutiny

Reg BI examinations now emphasize granular fee disclosures, product suitability, and dual-registrant conflict mitigation, pushing compliance budgets 8% higher in 2025 versus 2024. Department of Labor rules governing rollover advice add another oversight layer, directly affecting the SECURE Act 2.0 conversion pipelines that many banks target for growth. Simultaneously, Treasury guidance on AI risk management compels firms to document model governance, bias controls, and incident-response playbooks, raising barriers for smaller competitors. The cumulative regulatory drag squeezes margins and lengthens product-launch timelines, yet strong performers leverage compliance excellence as a trust builder when courting new assets under management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Asset Management Anchors Revenue Streams

Asset management accounted for 50.74% of the United States private banking market share in 2025, underscoring its centrality to relationship profitability. Ongoing capital-market volatility increases client reliance on tactical allocation, manager selection, and tax-loss harvesting, reinforcing the fee resilience of discretionary mandates. Real-estate consulting is projected to clock an 7.94% CAGR through 2031, making it the service-line growth engine as clients allocate toward income-producing property, 1031 exchanges, and fractional commercial deals. Trust and tax consulting continue to expand steadily as wealth transfer accelerates and state-level tax policies diverge, prompting affluent households to seek jurisdictional optimization. Insurance, while the smallest category, serves as a gateway into estate liquidity, long-term-care planning, and liability coverage, enriching cross-sell density across the client lifecycle.

Broader platform integration allows banks to migrate clients from single-service entry points into full-suite engagements, lifting average revenue per relationship. Institutions bundle capital-call lines with alternative investment subscriptions, marrying lending income with asset-management fees. Such cross-pollination defends wallet share against mono-line fintech entrants. The trend also feeds capital-efficiency metrics: clients with four or more product lines deliver up to 2.5× higher lifetime value than those limited to custody and trading services. Regulatory complexity across diverse business lines increases operational overhead, but scale economies in technology and compliance largely offset the incremental cost, especially for top-tier banks.

By Application: Personal Banking Dominates but Enterprise Demand Rises

Personal applications represented 72.15% of the United States private banking market size in 2025, reflecting the sector’s heritage of individualized portfolio stewardship. Mass-affluent and HNW investors continue to favor banks that combine personalized advice with mobile account access, biometric security, and curated alternative-investment marketplaces. Enterprise services, growing at a 7.28% CAGR, ride the tailwind of private-company liquidity events, executive stock-option planning, and cash-management mandates for professional partnerships. Banks that unify business and personal dashboards enable real-time snapshots of treasury positions alongside household balance sheets, delivering a differentiated advisory narrative.

Hybrid service architectures minimize friction: a founder may execute payroll through an enterprise portal in the morning and sweep excess cash into a laddered bond strategy by afternoon, all orchestrated via a single relationship manager. Integration also mitigates concentration risk by spreading revenue across corporate lending, FX, and personal-wealth lines. Compliance hurdles persist; advisors must navigate overlapping FINRA, SEC, and state regulations, particularly when recommending securities to closely held corporations. Yet the same complexity dissuades pure-play fintech challengers, allowing full-service banks to sustain premium pricing for bundled value.

By Client Wealth Tier: UHNW Growth Outpaces Other Segments

High-net-worth clients held 43.21% of 2025 assets, anchoring core profitability through diversified mandates that range from lending to philanthropic structuring. The ultra-high-net-worth cohort, though smaller in headcount, posts the fastest 9.39% CAGR as concentrated stock positions from IPOs, SPAC exits, and M&A transactions balloon personal balance sheets. Demand for direct private-equity co-investments, specialty real-estate vehicles, and bespoke derivatives hedging fuels revenue per client far above mass-affluent averages. Family-office service desks—providing CFO-like budget oversight, aircraft leasing advice, and global residency planning—differentiate incumbents amid fierce competition for marquee relationships.

Mass-affluent households remain strategically important as future HNW pipeline. Banks deploy tiered digital offerings with Robo-core portfolios, add-on advisor sessions, and automated tax-optimizing withdrawals to serve this segment profitably. Such scalable modules preserve operating leverage while instilling brand loyalty that eases conversion to full private-bank status as assets compound. Nonetheless, rising customer-acquisition costs and razor-thin fees heighten the urgency of AI-driven lead scoring and marketing analytics to pinpoint high-potential prospects.

Geography Analysis

The Northeast retained 35.12% market share in 2025, anchored by New York’s financial corridor, Boston’s biotech wealth, and continued inflows of global capital seeking U.S. dollar exposure. Despite its supremacy, net domestic migration trends have tilted southward, nudging banks to establish satellite wealth offices in Florida, North Carolina, and Georgia to follow client footprints. Real-estate advisory desks note accelerated condo and single-family purchases in Miami-Dade and Palm Beach counties, mirroring a broader shift toward zero-state-income-tax jurisdictions. The West is set to record a 6.74% CAGR through 2031, the fastest among regions as technology IPO windfalls, venture-capital distributions, and equity-compensation packages swell household investable assets. Silicon Valley remains the AUM nucleus, yet secondary hubs such as Austin and Denver are scaling rapidly, supported by corporate relocations and favorable business climates. Private banks expand into these metros via boutique acquisitions and co-working-style client lounges that resonate with tech founders. Real-asset demand trends westward too, with clients acquiring multifamily developments in Phoenix and Seattle, spurring banks to strengthen commercial-lending desks specialized in construction financing.

The South benefits from a USD 100 billion wealth migration wave between 2024 and 2025 as affluent households pursue lower taxes and warmer climates. Banks ramp hiring of bilingual advisors in Texas and Florida to serve Latin American inbound clients seeking dollar-denominated safety. Enterprise service uptake accelerates among family-owned businesses in energy, logistics, and healthcare, prompting tailored lending solutions such as asset-based lines secured by receivables. Miami emerges as a cross-border wealth hub, channelling investments into both U.S. and Caribbean property markets, thereby diversifying fee sources. Midwest wealth remains steady, rooted in manufacturing dividends, agricultural land appreciation, and a resurgence in mobility and clean-tech startups around Detroit and Chicago. Growth lags coastal regions yet provides stable lending spreads and sticky deposit bases. Banks leverage community ties, sponsoring local cultural initiatives that reinforce brand trust.

Competitive Landscape

The United States private banking market displays moderate concentration, with the largest players managing a significant portion of overall client assets. Leading institutions such as JPMorgan Private Bank and Bank of America Private Bank leverage their universal banking models to offer an integrated suite of services, combining lending, investment, and custody solutions. Their scale advantage is further strengthened by substantial technology investments aimed at enhancing advisor productivity and client experience. For example, JPMorgan’s upcoming platform upgrade integrates AI-driven trade recommendations into advisor workflows, while Goldman Sachs uses generative AI to streamline document handling. These innovations reduce operational friction and allow advisors to focus more on strategic wealth planning.

Regional and mid-tier banks are adopting specialization strategies to remain competitive in the evolving market. Commerce Bancshares expanded its footprint in the Southeast through a key acquisition, bringing in new trust assets and enabling the cross-selling of niche offerings such as private aviation and yacht financing. Similarly, TowneBank’s acquisition in Richmond supports its focus on middle-market business owners seeking coordinated personal and corporate financial solutions. These regional moves illustrate the value of concentrating resources in fast-growing, demographically attractive markets. Strategic geographic clustering, combined with tailored service offerings, allows smaller players to defend and grow market share despite resource limitations.

Fintech challengers continue to target specific segments of the wealth management value chain, including alternative investments, tax strategies, and digital estate planning tools. However, their lack of core banking infrastructure and increasing regulatory scrutiny pose limitations to long-term competitiveness. Traditional banks have responded by partnering with or absorbing fintech solutions, offering enhanced digital services without surrendering control over client relationships. As a result, the competitive battleground has shifted from pure innovation to execution—particularly in delivering hybrid digital-human experiences, maintaining robust product platforms, and ensuring regulatory compliance. Institutions that master these elements are more likely to attract and retain high-value clients amid shifting economic conditions.

United States Private Banking Industry Leaders

JPMorgan Private Bank

Bank of America Private Bank

Morgan Stanley Private Wealth Management

Wells Fargo The Private Bank

UBS Wealth Management USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Commerce Bancshares announced a definitive agreement to acquire FineMark Holdings for USD 585 million, expanding wealth management capabilities across Florida, Arizona, and South Carolina markets with over USD 7.7 billion in assets under administration.

- May 2025: FNBO completed acquisition of Country Club Bank of Kansas City, creating a combined institution with nearly USD 35 billion in assets and expanding wealth management capabilities through Country Club Bank's USD 2.8 billion trust assets under management.

- April 2025: TowneBank completed its merger with Village Bank and Trust Financial Corp, strengthening presence in the Richmond Metropolitan Statistical Area and creating revenue synergies with Towne Financial Services Group. The integration demonstrates regional expansion strategies focused on high-net-worth market penetration through established local relationships.

- March 2025: Bar Harbor Bankshares announced a USD 41.6 million all-stock merger with Guaranty Bancorp, creating a combined entity with approximately USD 4.8 billion in assets and USD 3.2 billion in Assets Under Administration across Maine, New Hampshire, and Vermont markets.

United States Private Banking Market Report Scope

The private banking services industry offers a range of specialized services, including investment advisory, asset management, and gift and estate planning. These services cater to high-net-worth clients and ultra-high-net-worth clients.

The private banking market in the United States is segmented by type and application. By type, the market is further segmented into asset management service, insurance service, trust service, tax consulting, and real estate consulting. By application, the market is further segmented into personal and enterprise. The report offers market sizes and forecasts in terms of revenue (USD) for all the above segments.

| Asset Management Service |

| Insurance Service |

| Trust Service |

| Tax Consulting |

| Real-Estate Consulting |

| Personal |

| Enterprise |

| Mass-Affluent |

| High-Net-Worth |

| Ultra-High-Net-Worth |

| Northeast |

| Midwest |

| South |

| West |

| By Type | Asset Management Service |

| Insurance Service | |

| Trust Service | |

| Tax Consulting | |

| Real-Estate Consulting | |

| By Application | Personal |

| Enterprise | |

| By Client Wealth Tier | Mass-Affluent |

| High-Net-Worth | |

| Ultra-High-Net-Worth | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the United States private banking sector?

The United States private banking market size is USD 64.97 billion in 2026.

How fast is the United States private banking market expected to grow?

It is projected to expand at a 9.12% CAGR, reaching USD 100.52 billion by 2031.

Which service line holds the largest share in private banking?

Asset management leads with 50.74% market share in 2025.

Which U.S. region shows the fastest private-banking growth?

The West is forecast to post a 6.74% CAGR through 2031.

Why are alternative investments important to private banks?

Client demand for private credit and real estate boosts fee revenues and differentiates advisory offerings.

Page last updated on: