Open Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

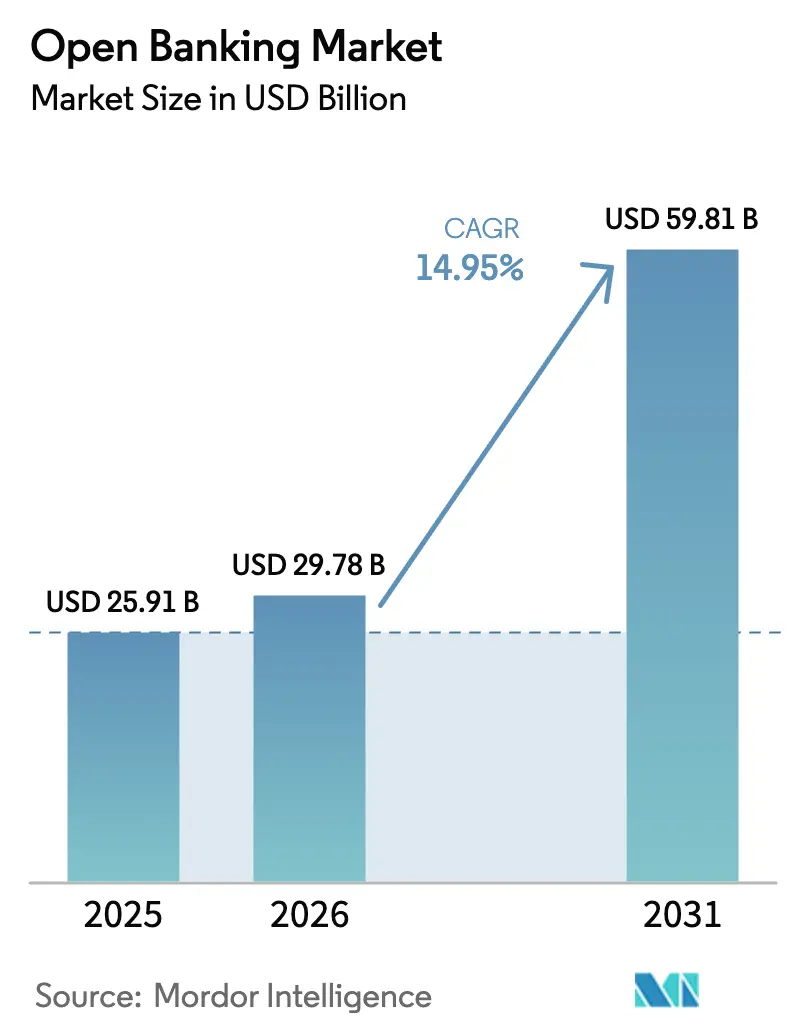

| Market Size (2026) | USD 29.78 Billion |

| Market Size (2031) | USD 59.81 Billion |

| Growth Rate (2026 - 2031) | 14.95% CAGR |

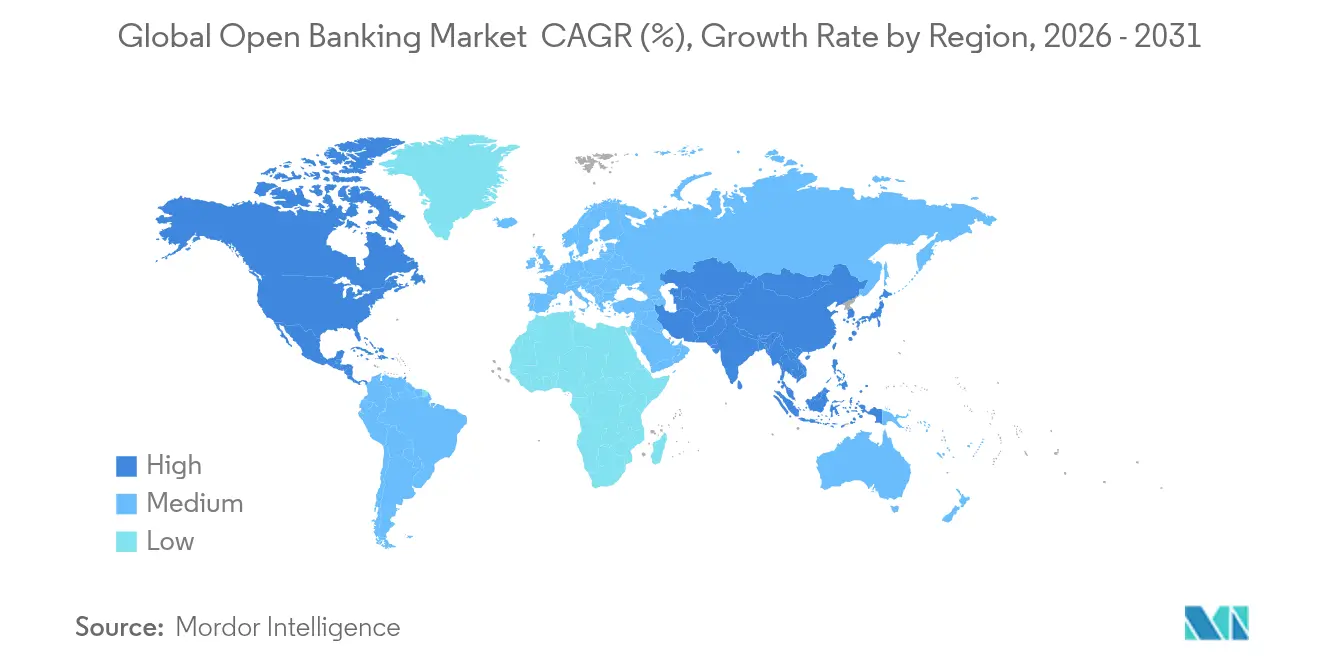

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

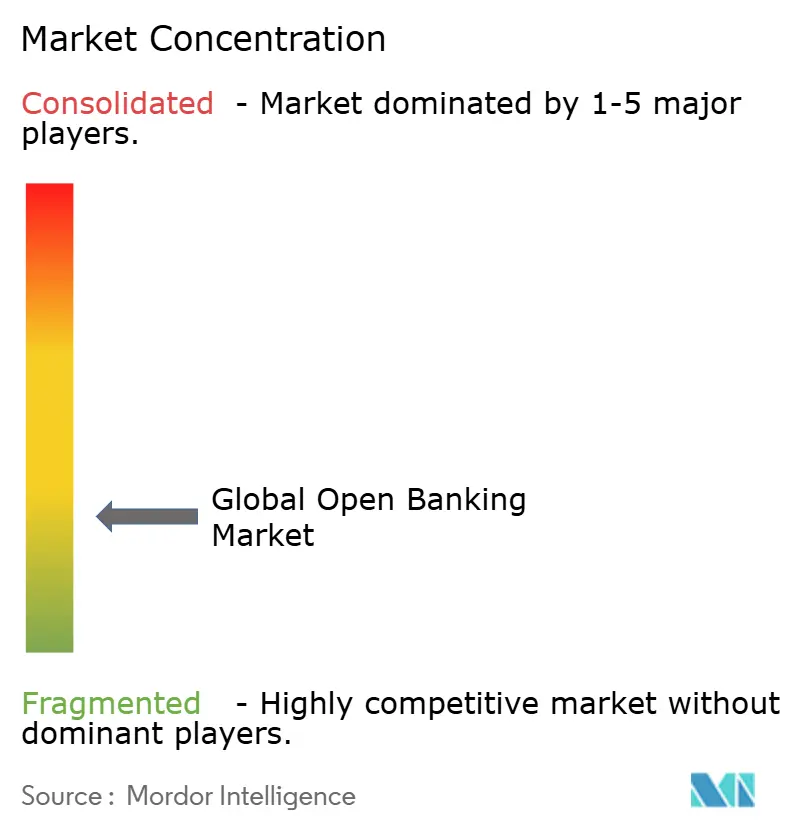

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Open Banking Market Analysis by Mordor Intelligence

The Global Open Banking Market size is projected to expand from USD 25.91 billion in 2025 and USD 29.78 billion in 2026 to USD 59.81 billion by 2031, registering a CAGR of 14.95% between 2026 to 2031.

Regulatory mandates in Europe and the United States, rising demand for data-driven financial services, and rapid API adoption underpin this growth trajectory. Payment Initiation remains the largest service category, but data-aggregation use cases are scaling quickly as banks pursue personalization strategies. North America leads current revenue while Asia-Pacific records the fastest expansion, signaling a pivot from compliance-led deployments in mature regions to inclusion-focused rollouts across emerging economies. Competitive intensity stays moderate as a diverse mix of banks, fintech specialists, and technology networks invest in API performance, consent management, and embedded-finance partnerships.

Key Report Takeaways

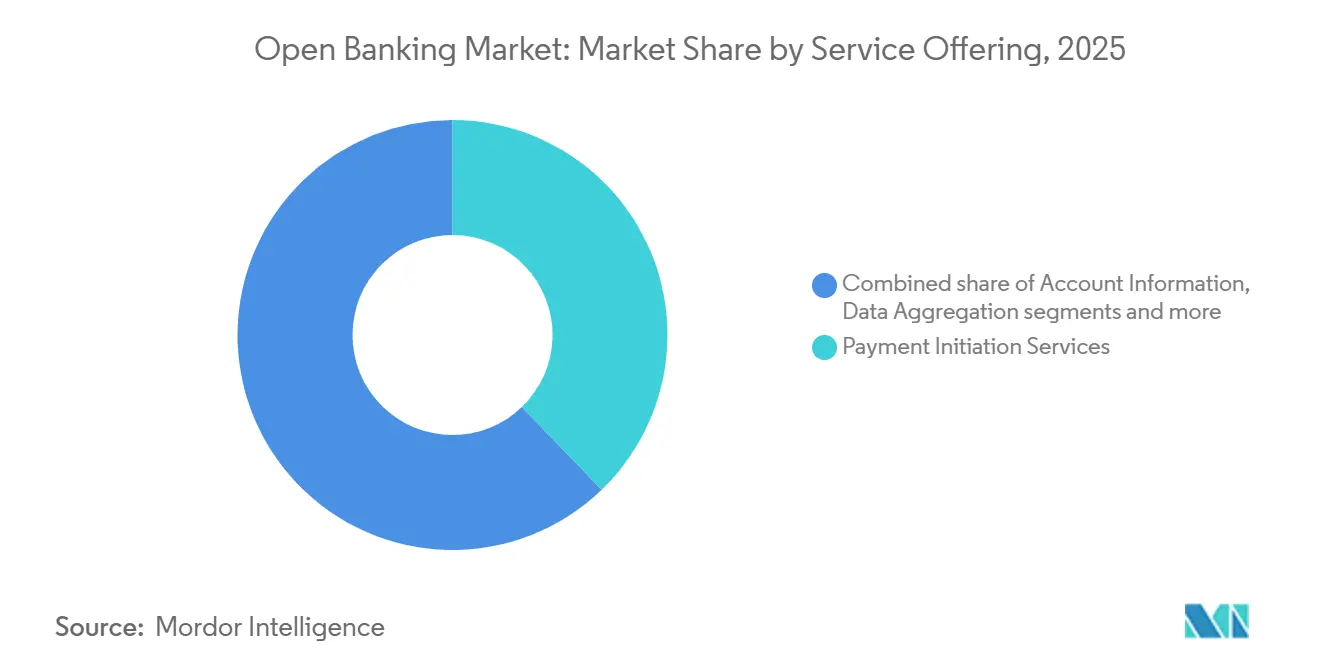

- By service offering, payment initiation services led with 37.80% revenue share of the open banking market in 2025; data aggregation & enrichment is projected to expand at an 17.35% CAGR through 2031.

- By end user, retail banking customers accounted for a 53.40% share of the open banking market size in 2025, while third-party fintech developers are advancing at a 15.85% CAGR through 2031.

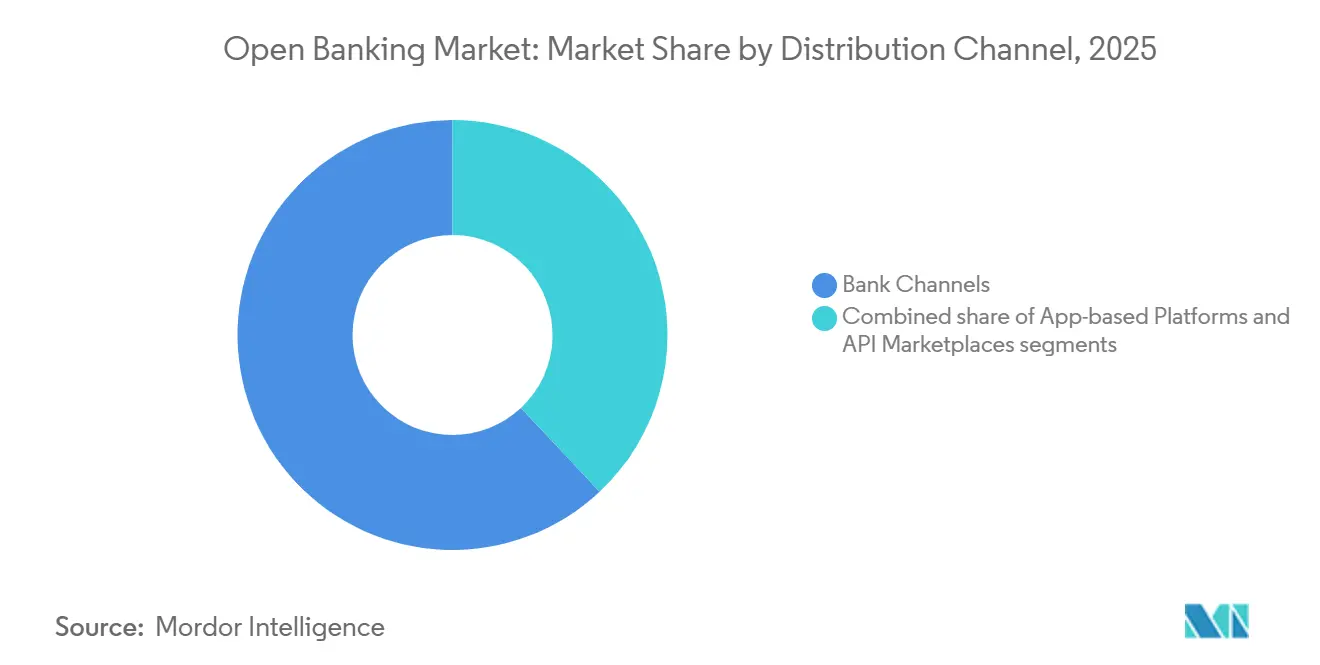

- By distribution channel, bank channels held 62.00% of the open banking market share in 2025; app-based platforms record the highest projected CAGR at 15.40% to 2031.

- By deployment model, cloud solutions captured 65.40% of the market of the open banking market in 2025 and are forecast to grow at 13.10% CAGR, outpacing on-premise and hybrid options.

- By geography, North America commanded 31.85% revenue of the open banking market in 2025, whereas Asia-Pacific is set to grow at 14.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Open Banking Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened PSD2 & global regulatory mandates | +3.2% | Europe, North America, APAC | Medium term (2-4 years) |

| Real-time A2A payment adoption surge | +2.8% | Global | Short term (≤ 2 years) |

| Personalised data-driven banking demand | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Embedded-finance pull from non-bank platforms | +1.9% | Global | Medium term (2-4 years) |

| Cross-utility open-data convergence | +1.4% | Europe, North America | Long term (≥ 4 years) |

| Cloud-native infrastructure scalability & security advantages | +1.6% | Global, strongest in North America; accelerating in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened PSD2 & Global Regulatory Mandates

The PSD3 regulations on performance thresholds and consent dashboards are designed to professionalize API management, driving efficiency in integration processes. These measures are expected to reduce long-term costs for fintechs and establish uniform access rights across 95 jurisdictions with formal open-banking frameworks[1]European Banking Authority, “PSD3 Consultation Paper,” eba.europa.eu . Similarly, the CFPB's Section 1033 rule in North America mandates banks to provide consumer-authorized data through secure interfaces, aligning with global trends. By implementing consistent standards, the reliance on bespoke connections is minimized, simplifying integration efforts. This regulatory shift allows smaller financial institutions to access ecosystem services with reduced compliance costs. Collectively, these developments are set to create a more standardized and accessible open-banking landscape worldwide.

Real-time A2A Payment Adoption Surge

In 2023, global instant-payment volumes reached 266.21 billion transactions, reflecting the growing adoption of real-time payment systems worldwide[2]ACI Worldwide, “Prime Time for Real-Time 2024,” aciworldwide.com . By 2028, these transactions are expected to comprise over 25% of all electronic payments, underscoring a significant shift in payment preferences. The implementation of the Instant Payments Regulation in Europe, set for 2025, will make it mandatory to accept euro-denominated real-time transfers, further accelerating this trend. Visa's deployment of Tink-powered pay-by-bank infrastructure demonstrates the increasing focus on direct-to-account payment solutions. Additionally, the expansion of UK Variable Recurring Payments, which already represent a notable share of local open-banking transactions, highlights the growing role of open banking in reshaping payment ecosystems. Collectively, these developments indicate a gradual erosion of card-based payment dominance as real-time and account-to-account payment methods gain prominence.

Personalized Data-driven Banking Demand

A significant 73% of consumers show a preference for subscription management tools that consolidate account data for streamlined usage. Additionally, 60% of these consumers trust their primary banking institutions to effectively manage such tools[3]Finextra, “Consumers Keen on Subscription Management,” finextra.com . Financial institutions leveraging cash-flow analytics report enhanced underwriting accuracy compared to traditional legacy scoring methods. To remain competitive, banks are incorporating external datasets, including utility payments, telecom bills, and social media signals, into their predictive modeling processes. These advanced models enable banks to deliver personalized financial solutions, such as proactive savings recommendations and automated budgeting tools. This strategic approach reflects the growing emphasis on data-driven decision-making to meet evolving consumer expectations.

Embedded-finance Pull from Non-bank Platforms

E-commerce, software, and marketplace operators are increasingly integrating financial services such as lending, digital wallets, and insurance into their platforms to enhance user engagement and streamline transactions. These companies rely on banking-as-a-service providers to manage regulatory compliance and settlement infrastructure efficiently. By 2030, banks in the Asia-Pacific region project that digital adjacencies will generate over 40.1% of their total revenue, driven by partnerships with technology firms targeting underbanked populations. Regulatory sandboxes in key markets like India, Singapore, and Indonesia are accelerating these developments by establishing clear frameworks for data-sharing consent. This regulatory clarity enables smoother collaboration between financial institutions and technology providers, fostering innovation in financial services. As a result, the integration of embedded finance is expected to play a pivotal role in expanding financial inclusion and driving revenue growth in the region.

Restraints Impact Analysis of Open Banking Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns | –2.1% | Global | Short term (≤ 2 years) |

| Fragmented API standards raise costs | –1.8% | Europe, North America | Medium term (2-4 years) |

| Rising bank API monetisation fees | –1.2% | Global | Medium term (2-4 years) |

| Transaction latency on legacy cores | –0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Concerns

The expansion of API surfaces has increased vulnerability to cyberattacks, compelling financial institutions to reassess their security frameworks. Upcoming US regulations are poised to transfer breach liability to data-originating banks, driving a surge in compliance-related expenditures. Trust in institutions remains low, with only 57% of Americans fully confident in their ability to protect shared data, signaling a critical perception gap that could hinder consumer participation. This lack of trust may slow the adoption of opt-in services, impacting the growth of secure data-sharing ecosystems. Additionally, the continued reliance on screen scraping, where secure APIs are unavailable, exacerbates security risks and operational inefficiencies. These factors collectively underscore the urgent need for robust API security measures and enhanced consumer trust-building initiatives.

Fragmented API Standards Inflate Integration Cost

Europe hosts over 5,000 distinct bank APIs, many of which were developed prior to PSD2 and lack standardized performance assurances. This fragmented landscape has necessitated that fintech companies rebuild API connectors individually for each market, increasing operational complexity. The introduction of PSD3 is set to enforce the use of dedicated interfaces, aiming to streamline integration processes across the banking ecosystem. However, financial institutions with outdated legacy systems face significant migration expenses, which pose challenges to achieving short-term returns on investment. These costs, coupled with the technical hurdles of transitioning to compliant systems, are likely to impact the pace of adoption. As a result, the near-term financial benefits of PSD3 compliance may remain limited for institutions burdened by legacy infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Open Banking Market Segment Analysis

By Service Offering:

Payment Initiation Leads Data InnovationIn 2025, Payment Initiation Services accounted for 37.80% of the open banking market, driven by increasing merchant demand for cost-efficient account-to-account payment solutions. The segment's expansion is further supported by regulatory initiatives promoting instant payment systems and the implementation of Variable Recurring Payments (VRP) to streamline dynamic subscription management. Data Aggregation & Enrichment, with a compound annual growth rate of 17.35%, highlights the banking sector's strategic focus on deriving value from actionable insights rather than raw transaction data. The adoption of predictive cash-flow scoring tools, which enhance decision-making precision, signals a significant shift from traditional descriptive analytics to advanced prescriptive analytics. These developments reflect the evolving priorities of financial institutions as they seek to optimize operational efficiency and customer engagement. Collectively, these trends underscore the transformative impact of technology and regulation on the open banking ecosystem.

Every day, budgeting tools still rely on Account Information Services, which provide users with a consolidated view of their financial data, enabling better financial planning and management. Meanwhile, Funds Confirmation APIs play a crucial role in high-value commerce by verifying account balances before transactions, significantly reducing fraud losses and ensuring secure payment processes. As institutions increasingly implement consent management at scale, the "others" cluster comprising consent dashboards, risk-scoring engines, and fraud-monitoring platforms has gained prominence. These tools enhance transparency, improve risk assessment, and strengthen fraud detection capabilities. Together, these elements highlight the Open Banking market's evolution from mere transactional efficiency to more intelligence-driven and value-added offerings.

By End User:

Retail Dominance Meets Developer InnovationRetail Banking Customers formed 53.40% of the overall demand in 2025, reflecting consumers’ appetite for consolidated account views, bill switching, and pay-by-bank checkout. This trend highlights the increasing importance of seamless and integrated banking experiences for individual consumers. Small and medium-sized enterprises (SMEs) are turning to automated expense workflows and cash-flow forecasting to enhance operational efficiency and financial planning. These tools enable SMEs to streamline their processes and make more informed decisions. Meanwhile, corporate treasurers are delving into API-driven solutions for liquidity sweeps and reconciling receivables, aiming to optimize cash management and improve financial transparency. Fintech developers are leading the charge with a robust 15.85% CAGR, capitalizing on open APIs that facilitate niche applications, ranging from gig-worker income smoothing to crypto-fiat on-ramps. This growth reflects the increasing demand for innovative and tailored financial solutions across various market segments.

Developer adoption strengthens network effects, as each new application enhances the ecosystem's overall value and drives increased data sharing. To attract and retain innovative partners, banks are focusing on improving sandbox environments, optimizing technical documentation, and ensuring higher uptime through robust SLAs. These efforts aim to create a more reliable and developer-friendly ecosystem, fostering collaboration and innovation. Government agencies and utility providers, categorized as "Others," are actively testing use cases such as benefit disbursement and energy-usage financing. These pilot projects highlight the Open Banking market's potential to enable seamless cross-sector digital public services. The growing adoption across industries demonstrates the market's capacity to drive innovation and operational efficiency in diverse sectors.

By Distribution Channel:

Traditional Banks Embrace Digital TransformationBanks’ proprietary channels still accounted for 62.00% revenue in 2025, evidencing client reliance on primary-bank mobile apps even as external aggregators proliferate. This dominance highlights the strong relationship between banks and their customers, as well as the convenience and security offered by these apps. Meanwhile, app-based fintech platforms are witnessing a robust 15.40% CAGR, highlighting users' growing preference for tailored budgeting and investing experiences that utilize secure data pulls. These platforms cater to niche financial needs, offering personalized solutions that traditional banking apps may not fully address. Additionally, API marketplaces, where banks market modular services, present a novel avenue, transforming these regulated entities into infrastructure providers. This shift enables banks to monetize their technological capabilities and opens up fresh revenue streams by allowing third-party developers to integrate banking services into their platforms.

The COVID-19 pandemic significantly accelerated mobile engagement, creating opportunities for app-centric business models to thrive. Increasing transaction limits on biometric authentication have further enhanced the adoption of these models. Financial institutions are strategically investing in advanced developer portals and webhook-based event notifications to expand their service delivery. This approach enables banks to move beyond native applications and integrate seamlessly into partner ecosystems. By embedding financial services into everyday consumer software, banks are fostering deeper connections with their customers. These developments highlight a growing trend of tighter integration between financial services and consumer technology platforms.

By Deployment Model:

Cloud Infrastructure Dominates ModernizationCloud deployments command 65.40% 2025 revenue and grow at 13.10% CAGR as institutions migrate core processing to scalable, resilient environments that can shoulder exponential API call volumes. Cloud implementations are becoming increasingly critical as the Open Banking market expands, fueled by the adoption of ISO 20022 real-time messaging standards and the integration of AI-driven fraud analytics. These advancements demand enhanced burst computing capacities, which cloud environments are well-equipped to provide. While on-premise installations continue to thrive in tightly regulated areas due to compliance requirements, they face mounting cost pressures. These pressures stem from the need for ongoing patch management, frequent hardware refresh cycles, and the inability to match the scalability and flexibility offered by cloud solutions.

Hybrid models function as transitional frameworks, enabling organizations to systematically mitigate risks associated with legacy core systems. Regulatory bodies are increasingly providing detailed guidelines on cloud outsourcing, ensuring compliance and operational clarity for financial institutions. The Federal Reserve's supervisory technology pilots highlight a strong policy inclination toward adopting cloud-native payment solutions. By leveraging continuous integration pipelines and containerization, cloud-first banks are enhancing their operational agility and accelerating the deployment of innovative features. These advancements allow for the rapid introduction of tools such as consent dashboards and developer sandboxes, which are critical for improving customer engagement and developer collaboration. Consequently, cloud-first strategies are positioning banks to achieve faster time-to-market while maintaining regulatory alignment and technological competitiveness.

Geography Analysis

North America Open Banking Market

In 2025, North America accounted for 31.85% of the revenue, driven by the Financial Data Exchange's voluntary standard and the widespread use of tokenized APIs by over 100 million consumers for data sharing. The introduction of the Section 1033 rule is expected to formalize consumer rights while fostering collaboration across the industry. The Open Banking market in the region is anticipated to grow further as merchants increasingly adopt pay-by-bank options, particularly amid ongoing debates over interchange fees. This growth trajectory highlights the region's ability to leverage regulatory frameworks and technological advancements to enhance market adoption. North America's leadership in Open Banking reflects its strategic alignment of consumer needs, regulatory support, and technological innovation.

APAC Open Banking Market

The Asia-Pacific region is projected to achieve a strong 14.20% CAGR through 2031, supported by robust public digital infrastructures such as India's UPI rail and Australia's Consumer Data Right. Regulatory initiatives in Singapore and Indonesia, including fintech sandboxes, are accelerating approvals and enabling markets to bypass legacy systems, fostering rapid adoption. The region's growth is further underpinned by its ability to integrate innovative solutions into its financial ecosystem, creating a competitive edge. These developments position Asia-Pacific as a key player in the global Open Banking market, leveraging regulatory foresight and technological advancements. The region's focus on scalable and inclusive financial infrastructure underscores its potential for sustained growth in the forecast period.

LATAM and MEA Open Banking Market

Latin America's Open Banking market is gaining momentum, with Brazil's open-finance framework serving as a model for neighboring countries like Colombia, which are implementing mandatory payment initiation. The region's growth is characterized by its ability to adapt regulatory frameworks to local needs, fostering innovation and market expansion. Meanwhile, the Middle East and Africa are developing regional BaaS hubs that localize compliance, enabling cross-border financial services tailored to diverse audiences. These ecosystems highlight the importance of aligning regulatory strategies with market demands to drive adoption and growth. The varied trajectories across these regions illustrate the Open Banking market's adaptability to distinct regulatory and infrastructural contexts, ensuring its relevance and scalability.

Competitive Landscape

The concentration of revenue among the top five providers holds one-quarter of total revenue, underscoring the fragmented nature of the market, creating opportunities for rapid shifts in market share through mergers, acquisitions, or vertical specialization. Visa's acquisition of Tink and Mastercard's collaboration with Thought Machine showcase payment networks' strategic moves to bolster API capabilities, aiming to protect interchange revenues and delve into direct-to-account payment flows. Meanwhile, traditional banks like Deutsche Bank are evolving into service platforms, allowing merchants to adopt pay-by-bank APIs rather than just competing on deposit rates. This evolution signals a broader industry trend: financial institutions are gravitating towards platform-based models to enrich their service offerings and maintain market relevance. These shifting dynamics underscore the growing significance of API-driven innovation as a key to competitive advantage in the payments landscape.

Niche players are carving out spaces in areas like cash-flow underwriting, subscription management, and SME treasury services, leveraging data insights that often elude larger incumbents. Cross-border payments stand out as a lucrative growth avenue; harmonized APIs promise to cut down correspondent banking fees and settlement delays. Entities like SWIFT, CPMI, and various regional instant-payment schemes are collaborating, pushing the envelope in this domain. Successful market strategies spotlight the developer experience, emphasizing clear documentation, transparent uptime metrics, and vibrant community engagement. Such tactics aim to forge robust network effects, heighten switching costs, and cement competitive standings.

The evolving payments ecosystem reflects a broader shift towards innovation and adaptability. Payment networks and financial institutions are increasingly prioritizing API-driven solutions to stay competitive and relevant. By focusing on platform-based models and leveraging data insights, both incumbents and niche players are addressing emerging market demands. Collaborative efforts in cross-border payments and advancements in instant-payment schemes are further driving growth opportunities. Winning strategies in this market emphasize enhancing the developer experience and fostering community engagement. These approaches aim to establish strong network effects and secure long-term competitive positioning.

Open Banking Industry Leaders

Plaid Inc.

TrueLayer Ltd.

Trustly Group AB

Yapily Ltd.

Finicity (Mastercard)

- *Disclaimer: Major Players sorted in no particular order

Open Banking Market Companies Covered in this Report

- Tink AB

- Plaid Inc.

- TrueLayer Ltd.

- Trustly Group AB

- Yapily Ltd.

- Finicity (Mastercard)

- MX Technologies Inc.

- Figo GmbH

- Bud Financial Ltd.

- Token.io

- Volt.io

- Frollo

- Belvo

- Brankas

- Salt Edge Inc.

- Banco Bilbao Vizcaya Argentaria

- Revolut Ltd.

- Citi

Recent Industry Developments in Open Banking Market

- June 2025: Experian and Plaid formed a partnership to embed real-time cash-flow data into Experian Consumer Reports, improving underwriting for thin-file borrowers.

- April 2025: Capital One closed its USD 35.3 billion acquisition of Discover Financial Services after securing Federal Reserve approval.

- January 2025: Openbank extended German coverage by offering local IBANs and personal loans up to USD 24,997.

- November 2024: Bank of New Zealand acquired BlinkPay to deepen domestic open-banking capabilities.

Global Open Banking Market Report Scope

Open banking in the financial services industry facilitates financial data sharing via application programming interfaces between banks and other service providers. Banks have often maintained closed systems that house clients' financial data. This report aims to provide a detailed analysis of the open banking market. It focuses on market dynamics, emerging trends in the segments and regional markets, and insights into the various product and application types. It also analyzes key market players and the competitive landscape. The open banking market is segmented by banking services, which include banking and capital markets, payments, digital currencies, and value-added services; by distribution channel, including bank channel, app market, distributors, and aggregators; by deployment model, including on-premises, cloud, and hybrid, and by geography including North America, Europe, Asia-Pacific, South America, and the Middle East. The report offers market size and forecasts for the open banking market regarding revenue (USD) for all the above segments.

Segmentation Overview

| Data Aggregation & Enrichment |

| Funds Confirmation |

| Others |

| Retail Banking Customers |

| SMEs |

| Corporate & Commercial Enterprises |

| Third-party Fintech Developers |

| Others |

| Bank Channels |

| App-based Platforms |

| API Marketplaces |

| Cloud |

| On-premise |

| Hybrid |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| Account Information Services | Data Aggregation & Enrichment | |

| Funds Confirmation | ||

| Others | ||

| By End User (Value) | Retail Banking Customers | |

| SMEs | ||

| Corporate & Commercial Enterprises | ||

| Third-party Fintech Developers | ||

| Others | ||

| By Distribution Channel (Value) | Bank Channels | |

| App-based Platforms | ||

| API Marketplaces | ||

| By Deployment Model | Cloud | |

| On-premise | ||

| Hybrid | ||

| By Geography (Value) | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global open banking market?

The open banking market is valued at USD 29.78 billion in 2026.

How fast is the global open banking market expected to grow?

The market is forecast to expand at a 14.95% CAGR, reaching USD 59.81 billion by 2031.

Which region leads in open banking revenue?

North America leads with 31.85% market share in 2025.

Which service segment is growing fastest?

Data Aggregation & Enrichment services are expanding at an 17.35% CAGR through 2031.

Why is cloud deployment dominant in open banking?

Cloud solutions provide scalable capacity for high API call volumes and account for 65.40% market share in 2025.

How fragmented is the competitive landscape?

The revenue distribution indicates a high market concentration, with the top five companies accounting for a substantial share.

Page last updated on: