South America Banking-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

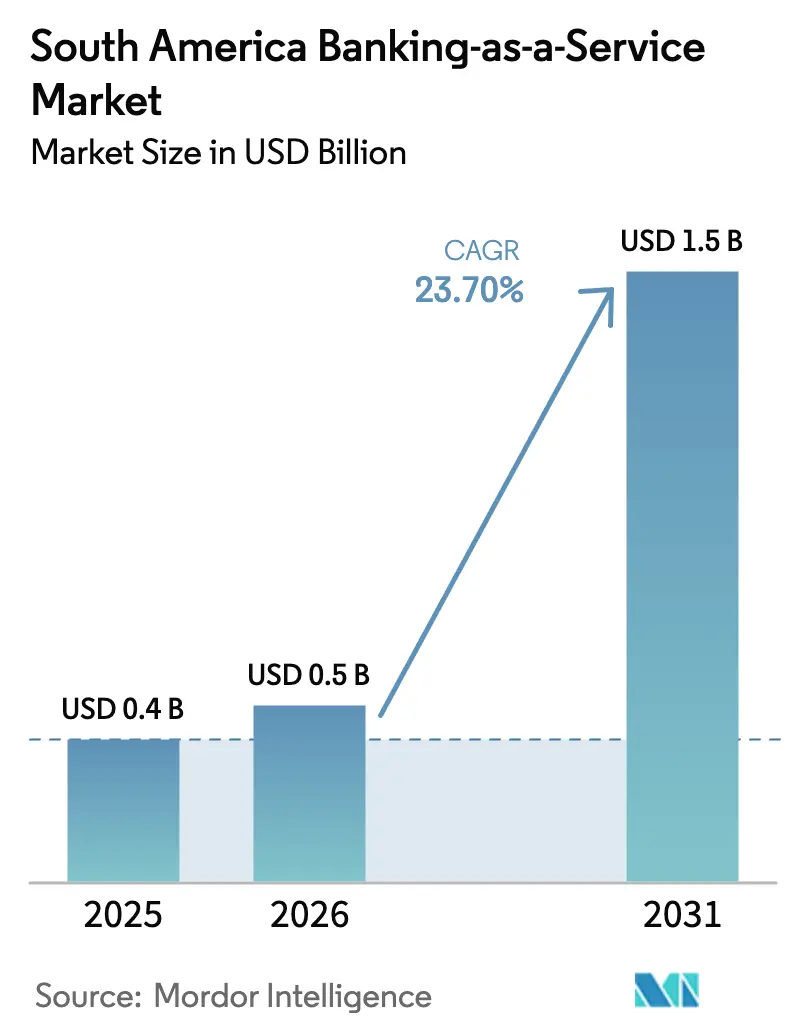

| Base Year Market Size (2025) | USD 0.4 Billion |

| Market Size (2026) | USD 0.5 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 23.70% CAGR |

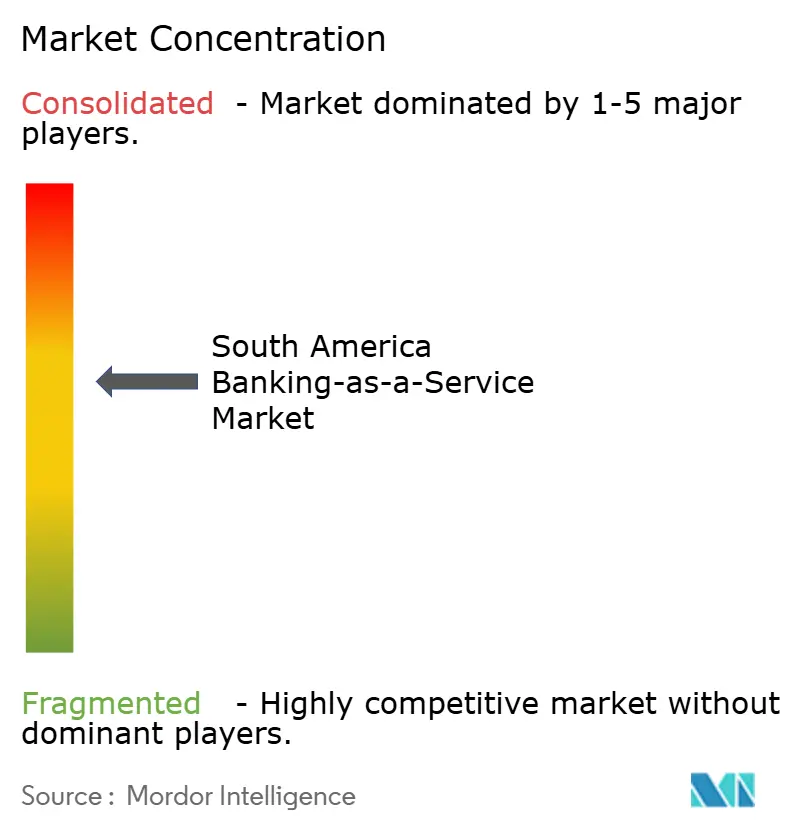

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Banking-as-a-Service Market Analysis by Mordor Intelligence

The South America Banking-as-a-Service Market size is projected to expand from USD 0.4 billion in 2025 and USD 0.5 billion in 2026 to USD 1.5 billion by 2031, registering a CAGR of 23.70% between 2026 to 2031.

Expansion is underpinned by Brazil’s leadership in instant payments via Pix, the maturation of Open Finance mandates, and the shift of non-banks toward API-first embedded finance models that place credit, treasury, and insurance within digital journeys at checkout or in merchant dashboards. The regulatory environment continues to formalize BaaS governance and third-party risk controls, which support scale for well-capitalized platforms and intensify due diligence expectations for service-taking entities[1]Banco Central do Brasil, “Open Finance,” Banco Central do Brasil, bcb.gov.br . Competitive intensity is rising as fintech companies use BaaS rails to compress lending spreads and accelerate product release cycles, crowding incumbents out of value-added services, issuer processing, and cross-border treasury use cases. Tokenization pilots, led by Brazil’s Drex program and stablecoin integrations with core banking, are preparing the ecosystem for programmable money and real-time settlement across local and cross-border flows in the next phase of the South America banking-as-a-service market.

Key Report Takeaways

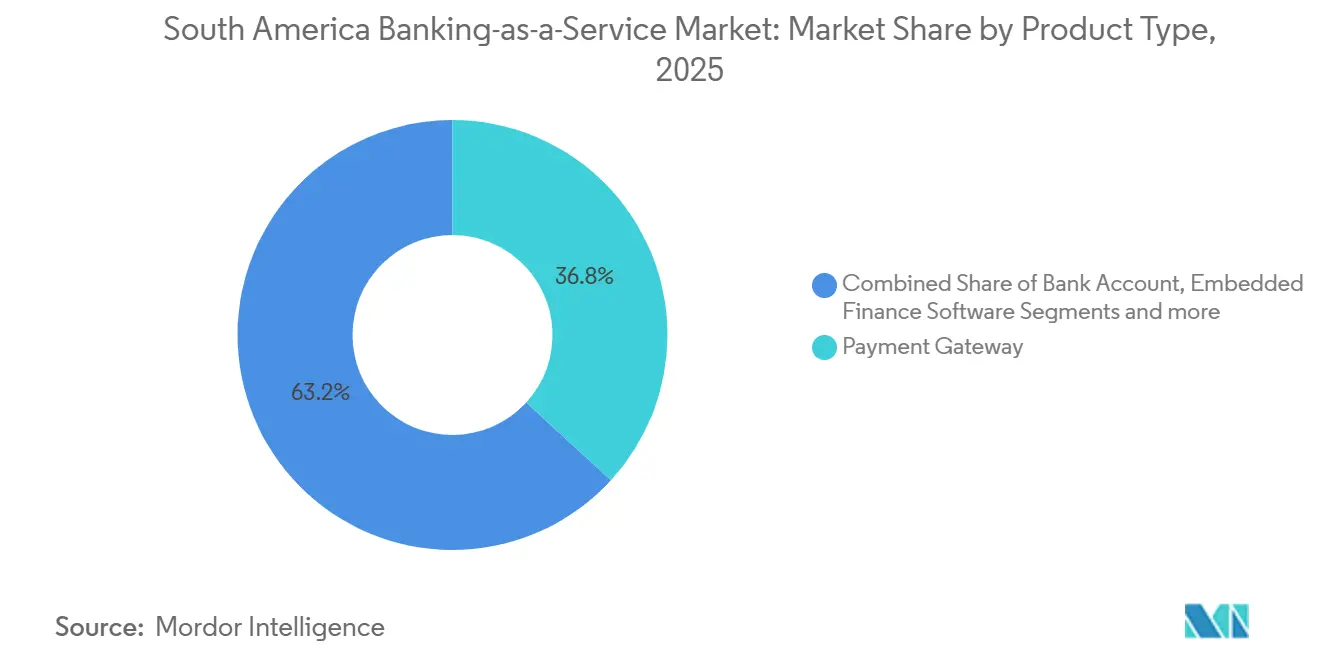

- By product type, payment gateways led with 36.8% revenue share in the South America banking-as-a-service market in 2025, while embedded finance software is projected to grow at a 24.8% CAGR through 2031.

- By enterprise size, large enterprises held a 64.4% share in the South America banking-as-a-service market in 2025, while SMEs recorded the fastest growth at a 23.4% CAGR to 2031.

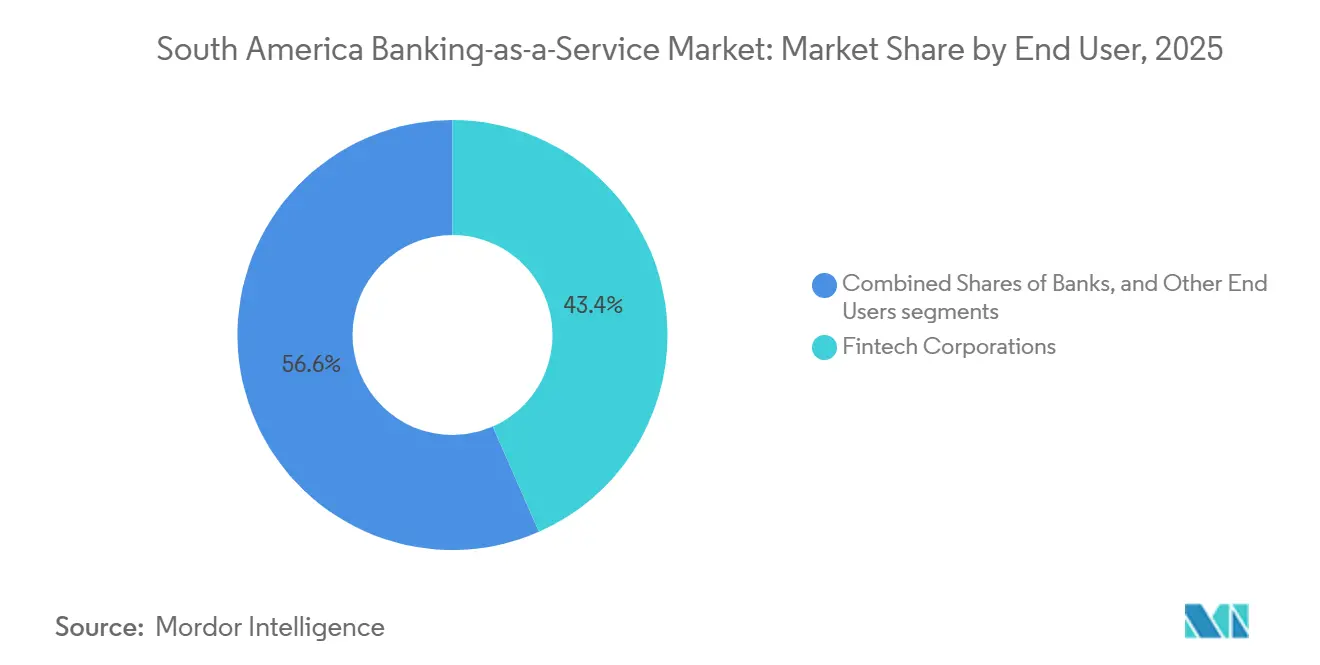

- By end user, fintech corporations captured a 43.4% share in the South America banking-as-a-service market in 2025 and posted the fastest trajectory at a 21.4% CAGR through 2031.

- By component, platform and infrastructure accounted for a 52.8% share in the South America banking-as-a-service market in 2025, while services are set to expand at an 18.9% CAGR into 2031.

- By geography, Brazil contributed 68.9% of the South America banking-as-a-service market in 2025, while Peru is forecast as the fastest-growing country at 17.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Banking-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-time payment rails enable embedded finance | +3.2% | Brazil (leading), Colombia, Peru, Chile (expanding) | Medium term (2-4 years) |

| Open Finance mandates accelerate API partnerships | +2.8% | Brazil (mature), Chile (April 2026 launch), Colombia (2025 decree) | Short term (≤ 2 years) |

| Banks monetize infrastructure via BaaS models | +2.1% | Brazil (68.87% share), Peru, Argentina | Medium term (2-4 years) |

| Card modernization drives issuer-processing demand | +1.6% | Brazil, Chile, Argentina, Peru | Long term (≥ 4 years) |

| Tokenized money pilots enable programmability | +0.9% | Brazil (Drex), regional spill-over | Long term (≥ 4 years) |

| Pix features intensify KYC/fraud orchestration | +1.4% | Brazil (Pix MED 4.1, device registration via IN 491/2024), regulatory influence (BCB) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Real-time Payment Rails Enable Embedded Finance

Brazil’s Pix system reached 174 million users by early 2025 and processed close to 7.9 billion transactions per month by December 2025, which shifted person-to-business flows ahead of peer-to-peer as instant account-to-account payments became standard in retail checkout and bill pay. The Central Bank’s launch of Pix Automático in June 2025 added recurring debit functionality under a single consent, enabling subscription billing for users without credit cards and deepening embedded payment experiences within consumer and SME apps. At the same time, Open Finance data-sharing in Brazil has enabled scaling of consents and API calls, allowing providers to embed credit lines, working capital, and insurance into merchant dashboards that run on top of Pix and other rails. Regional momentum supports similar trajectories, with Colombia’s real-time initiatives advancing and Peru’s interoperability mandates driving wallet adoption, strengthening on-ramps for embedded finance in retail and services[2]Bank for International Settlements, “Fast payments and financial inclusion in Latin America and the Caribbean,” Bank for International Settlements, bis.org . The South America banking-as-a-service market continues to rely on instant rails to compress payment latency, reduce acceptance costs, and unlock data-driven underwriting at the point of need across large enterprise and SME use cases.

Card Modernization Drives Issuer-Processing Demand

Recurring payments through Pix Automático intensify competition with stored-card credentials, which have accelerated network investment in tokenization, NFC acceptance, and virtual-card provisioning for subscription and mobility scenarios in Brazil and Chile. Visa’s acquisition of Pismo in 2024 brought cloud-native issuer processing and next-generation core capabilities under Visa’s distribution, enabling banks and fintechs to modernize card lifecycles and authorization logic with modular APIs at a regional scale. BIN sponsorship demand has risen among non-banks seeking co-branded and white-label issuance without fully licensed banking infrastructure, reinforcing issuer-processing platforms that bundle risk controls, real-time decisioning, and fraud tooling into turnkey stacks for the South America banking-as-a-service market. As contactless modernization remains uneven, software POS and issuer-generated virtual card numbers help fill acceptance gaps while supporting e-commerce and corporate expense use cases that keep card economics viable where A2A substitution intensifies. Over 2026, issuer-processing momentum is sustained by product-code updates, enterprise upgrades, and hybrid journeys that blend cards with instant payments to optimize acceptance, risk, and customer experience for the South America banking-as-a-service market[3]Visa, “Modernization accelerated: How Visa’s Pismo is transforming payments,” Visa, visa.com.

Tokenized Money Pilots Enable Programmability

Brazil’s Drex program runs wholesale and retail pilots that rely on Ethereum-compatible infrastructure and privacy-preserving tools to test programmable settlement, collateral management, and tokenized government-bond flows, with a two-phase public launch plan in 2026 subject to technical and policy validation. The programmability workstream targets escrow with conditional release, payroll and accounts payable with automated triggers, and dynamic utility billing that leverages trusted data oracles, all of which connect to Pix and existing account identifiers to ensure backward compatibility at scale. In parallel, banks and core platforms are integrating stablecoins into real-time ledgers and core systems, as shown by Matera’s integration of local Pix rails with USDC liquidity, which allows institutions to hold BRL, USD, and USDC within a unified environment for cross-border settlement and treasury operations. These tokenization initiatives prepare the South America banking-as-a-service market for institutional liquidity that can move on-chain with programmable controls while aligning with data protection and anti-financial crime requirements across jurisdictions. Over time, cross-border corridors piloted by public-private consortia aim to reduce correspondent delays and FX spreads, although binding multilateral frameworks depend on political consensus and monetary sovereignty safeguards.

Pix Features Intensify KYC/Fraud Orchestration

Device registration requirements introduced by Brazil’s Central Bank create a unique device identifier for Pix initiation and apply hard transaction and daily limits for unregistered devices, which shifts fraud controls toward pre-transaction authentication and continuous device risk scoring in 2026. The Special Return Mechanism, scheduled for enhancement in February 2026, extends fund-tracing and allows institutions to block and recover assets across multiple onward transfers, which requires standardized data exchange and playbooks among participating institutions to reduce loss severity in real time. Fraud-rejection mandates under suspicion and joint resolution obligations for BaaS governance place new emphasis on behavioral intelligence, API-layer anomaly detection, and coordinated interbank information sharing to address synthetic identities and mule networks. Providers across the South America banking-as-a-service market are responding with device fingerprinting, liveness detection, and automated negative-list sharing that align with AML circulars and privacy rules while minimizing false positives that disrupt urgent payments. The upshot is a step change in KYC orchestration from static onboarding toward continuous, risk-based authentication that adapts to transaction velocity, counterparties, and location signals as real-time channels scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory heterogeneity increases scaling complexity | -2.4% | Pan-regional, acute in Argentina, Peru, Chile | Medium term (2-4 years) |

| Instant-payment liabilities elevate operating risk | -1.8% | Brazil, Peru, regulatory influence (BCB fraud mandates) | Short term (≤ 2 years) |

| Divergent standards burden regional interoperability | -1.3% | Colombia, Mexico, Argentina, Chile | Long term (≥ 4 years) |

| A2A rails compress card economics | -0.7% | Brazil, Chile, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Heterogeneity Increases Scaling Complexity

Licensing thresholds, capital floors, data-residency mandates, and participant definitions differ by jurisdiction, which forces BaaS providers to maintain parallel entities and compliance stacks rather than passport a single authorization across South America[4]Organisation for Economic Co-operation and Development, “Balancing Prudential Regulation and Competition Considerations in Banking – Note by Brazil,” OECD, oecd.org. In Brazil, all payment institutions must obtain prior authorization and comply with strengthened oversight under the 2025–2026 regulatory priorities, which also formalize governance expectations for BaaS operations. Chile concluded open finance regulation under its Fintech Law, with phased implementation beginning in April 2026 and subsequent deadlines through 2029 that require staged compliance programs for payment initiators, banks, card issuers, and other actors. Peru’s supervisory authorities have initiated work on open finance but have yet to publish definitive technical standards, leaving market participants to build connectors against uncertain API endpoints and prolonging time to market. The South America banking-as-a-service market must also reconcile LGPD cross-border data rules and sectoral AML obligations in Brazil when architecting cloud footprints and data flows that must remain compliant across multiple jurisdictions.

Instant-Payment Liabilities Elevate Operating Risk

Instant settlement narrows the risk window for fraud detection and chargebacks, shifting mitigation from post-authorization workflows to real-time decisioning that evaluates user, device, and counterparty signals before funds move. High-profile incidents and social-engineering scams have prompted Brazil’s Central Bank to harden fraud governance by mandating device registration and enhancing return mechanisms that increase orchestration complexity for all Pix participants in 2026. In addition, transaction-rejection requirements under well-founded suspicion of fraud raise the bar for evidence-based decisions, which, in turn, can increase false positives if institutions do not calibrate behavioral models and negative lists with precision. Interoperable wallet ecosystems in countries such as Peru have improved inclusion and volume but diffused accountability for fraud events across providers, which can delay attribution and redress when mule networks span multiple platforms. As a result, the South America banking-as-a-service market is investing in adaptive authentication, liveness detection, and cross-bank collaboration to keep real-time fraud rates low while preserving the user experience at checkout and in recurring flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Embedded finance outpaces gateways on platform ubiquity

Payment gateways commanded 36.8% of the 2025 value as the default rail for Pix, card, and boleto acceptance across ecommerce, marketplaces, and mobility, while embedded finance software is projected to post a 24.8% CAGR through 2031, the fastest among product segments within the South America banking-as-a-service market. Brazil’s Open Finance framework, with expanding data-sharing consents and API usage, enables non-banks to embed credit, insurance, and treasury directly in operational dashboards, shortening decision cycles and allowing merchant users to bypass legacy interfaces. Platform providers such as Dock and QI Tech have scaled Pix transaction processing and credit issuance, demonstrating how horizontal API stacks power embedded journeys for financial and non-financial brands in the South America banking-as-a-service market. Core banking and bank account APIs continue to anchor wallet launches and neobank onboarding, while lending APIs use Open Finance data to refine alternative underwriting at a lower cost than traditional bureau-dependent approaches. As embedded models compress payment costs and combine transaction and behavioral data, margins expand in ways that pure gateways cannot replicate, which reinforces a shift from commodity routing to data-rich financial workflows.

The regulatory arc supports this transition, with Brazil setting out priorities for 2025–2026 that formalize BaaS obligations and strengthen third-party risk controls, which favor licensed platforms capable of sustained investment in compliance and cybersecurity. Embedded finance providers are also integrating programmable money through partnerships with Matera and Circle to unify BRL, USD, and USDC balances in real-time ledgers that connect local Pix rails to global liquidity for cross-border payments in the South America banking-as-a-service market. On the demand side, merchants seek end-to-end solutions that bundle checkout, reconciliation, settlement, and working-capital advances, which tilts share capture toward embedded software rather than standalone gateways over the forecast period. The result is a durable outperformance of embedded finance software as data-network effects improve underwriting and fraud models across more touchpoints, lifting unit economics and retention. Embedded software’s leadership is expected to consolidate as recurring payments and tokenized assets deploy at scale, creating new programmable workflows that sit upstream of payment authorization and settlement.

By Enterprise Size: SMEs embrace digital-first stacks at 23.4% CAGR

Large enterprises retained 64.4% of the 2025 value due to incumbent banking relationships, integration budgets, and the need for high availability and auditability, while SMEs are projected to grow at 23.4% CAGR on the back of low-code onboarding, consumption-based pricing, and embedded credit that reduces collateral friction in the South America banking-as-a-service market. Regulatory modernization in Brazil and active Open Finance adoption enable SME-focused providers to pull verified income and transaction histories, accelerating approvals and reducing operating costs, thereby strengthening SME demand for turnkey BaaS offerings. Public policy in Brazil has emphasized inclusion and credit expansion, and multilateral analysis underscores how fast payments contribute to SME digitalization and access to working capital. In Peru, SME modernization is supported by core-banking SaaS adoption, such as Mibanco’s migration to Temenos, which aims to achieve faster time-to-market and improved experiences at scale. These threads reinforce SME-led momentum for the South America banking-as-a-service market, where embedded apps bundle invoicing, collections, and financing into a single interface, reducing churn.

Enterprises continue to value vertically integrated platforms capable of meeting security and compliance demands while coexisting with ERP and legacy cores, which advantages providers with proven SLAs and multi-country credentialing. SMEs, by contrast, adopt out-of-the-box stacks that roll up KYC, AML, payment initiation, and reconciliation with minimal development overhead in the South America banking-as-a-service market. Open Finance data portability and credit portability, which are set to expand in 2026, will sharpen competition for SME refinancing and workflow ownership across payments and treasury. Over the forecast horizon, enterprise and SME adoption paths diverge in tooling and governance needs but converge on hybrid orchestration across instant payments, cards, and programmable balances, driving share gains for platforms with deep API catalogs.

By End User: Fintechs sustain 21.4% CAGR as incumbents digitize

Fintech corporations accounted for 43.4% of end-user demand in 2025 and are projected to grow at a 21.4% CAGR, reflecting the scale of digital-first challengers built on API-native architectures and simplified onboarding that shorten time-to-market in the South America banking-as-a-service market. Leading fintechs in Brazil, such as Nubank, have expanded client bases at double-digit rates, supported by deep mobile engagement and product expansion into payments, savings, lending, and investments. Merchant-focused ecosystems have also increased embedded working capital and treasury features in wallets, reinforcing fintech user retention and ARPU without adding branch or call center overhead. For banks, BaaS partnerships and Open Finance connectivity have become central to their digital transformation, with cross-border initiatives such as Pix-based acceptance abroad extending reach and brand across the region. As regulatory frameworks tighten around BaaS governance, banks and fintechs alike are evolving toward robust third-party risk controls and shared fraud defenses, which sustains overall category growth in the South America banking-as-a-service market.

Non-financial users such as retailers, platforms, and utilities increasingly embed BaaS for onboarding, payments, and credit at the point of interaction, as exemplified by integrations that enable direct debit and recurring payments in consumer services. These embedded experiences blur the lines between banks and fintechs, shifting advantage toward providers with orchestration spanning cards, instant payments, and tokenized assets in the South America banking-as-a-service market. Incumbent banks leverage BaaS APIs to accelerate product development while retaining balance-sheet control and regulatory capital management. Over time, convergence toward hybrid financial architectures supports multi-rail strategies and new monetization levers across customer segments. The South America banking-as-a-service market, therefore, grows on both challenger-led and incumbent-led vectors that prioritize speed, resilience, and alignment with compliance requirements.

By Component: Platform dominates at 52.8%, yet services expand 18.9% on compliance

Platform and infrastructure held 52.8% of the 2025 value, underscoring the capital-intensive nature of core ledgers, issuer processing, and high-availability payment connectivity in the South America banking-as-a-service market. Services, including KYC, AML, fraud prevention, and regulatory reporting, are projected to grow at a 18.9% CAGR to 2031 as BaaS governance, PSTI accreditation, and third-party risk rules raise the bar for compliance automation and independent assurance. Fraud-prevention orchestration has become a strategic layer as institutions adopt device registration, liveness, and behavioral analytics to keep real-time fraud rates low and improve recovery outcomes under return mechanisms. Providers differentiate through packaged compliance portals, API governance, and ready-to-use connectors that align with Open Finance standards and accelerate delivery across banks, fintechs, and credit unions in the South America banking-as-a-service market. Stablecoin integrations into core banking alongside Pix connectivity also create new service lines for cross-border treasury and settlement that monetize independently of domestic payment volume.

Service-layer revenue is further supported by subscription pricing for monitoring, audit-trail generation, and regulatory change alerts, which smooths revenue volatility compared with volume-based payment economics. Platform vendors with strong compliance packaging increasingly win enterprise deals that require robust SLAs and third-party audits, while services scale across both enterprise and SME customers in the South America banking-as-a-service market. As regulatory timelines unfold through 2026 and beyond, dual investment in platform resilience and services-led compliance will define competitive positioning, with licensed, security-certified providers consolidating share. Over time, programmable money and tokenized assets will stimulate additional service lines focused on smart-contract monitoring, key management, and on-chain AML analytics. The South America banking-as-a-service market will therefore balance platform scale with recurring services as institutions adapt to multi-rail and multi-asset environments.

Geography Analysis

Brazil accounted for 68.9% of the 2025 value, supported by Pix’s universal reach and the scale of Open Finance consents and API calls that underpin embedded finance models and real-time treasury in the South America banking-as-a-service market. Pix had 174 million users by early 2025 and processed close to 7.9 billion transactions a month by December 2025, while the Open Finance program continued to expand data-sharing adoption across consumers and SMEs. Regulatory milestones for 2025–2026 include formalizing BaaS governance, enhancing fraud controls, and strengthening PSTI oversight, collectively elevating baseline obligations and favoring licensed, well-capitalized platforms. Over the forecast period, features such as Pix Automático recurring payments and programmable-money pilots under Drex are set to open new use cases across subscriptions, escrow, and cross-border settlements in the South America banking-as-a-service market. Brazil’s leadership is expected to persist as providers integrate fraud defenses, compliance automation, and tokenization capabilities in line with central bank priorities.

Peru is projected to be the fastest-growing geography, with a 17.4% CAGR through 2031, driven by mandatory wallet interoperability that increases daily transaction volume and broadens acceptance across retail and services. The Central Reserve Bank of Peru announced a CBDC pilot in July 2024 focused on offline-capable retail payments and inclusion for users in low-coverage areas, which signals a policy direction supportive of programmable money and expanded access. SME modernization is accelerating as institutions such as Mibanco migrate core systems to cloud SaaS to improve time-to-market and operational efficiency for micro and small businesses, which represent the majority of Peru’s firms. These developments strengthen the conditions for BaaS adoption in Peru, particularly for SME-centric embedded finance and interoperable wallet-led payments in the South America banking-as-a-service market. As technical standards mature, providers are positioned to scale cross-rail orchestration and compliance services in line with supervisory expectations.

Chile finalized open-finance regulation in July 2024 under its Fintech Law and set phased compliance timelines beginning in April 2026, which will expand API-based data sharing and payment initiation over the coming years. Chile’s long-standing TEF infrastructure supports a high share of instant A2A spending and complements a high smartphone and banking penetration, which are favorable for digital payment acceleration in the South America banking-as-a-service market. Cross-border connectivity is growing as private providers deploy acceptance and cash networks, and as banks partner to enable Pix-based payments for Brazilians traveling in neighboring markets. Elsewhere in South America, Colombia is advancing a mandatory open-finance framework alongside the consolidation of real-time rails, while other countries are progressing with interoperable QR or instant-payment pilots at varying paces. Across the region, diversity of standards and timelines remains the chief variable that BaaS platforms must manage when planning multi-country expansions in the South America banking-as-a-service market.

Competitive Landscape

The South America banking-as-a-service market is moderately concentrated, with the top five providers estimated to hold significant combined market share, as mid-tier players compete for enterprise and vertical-specific accounts alongside large incumbents. Dock reports substantial scale in Pix transactions and active accounts as it expands across countries, reflecting horizontal reach and strong issuer-processing and payments capabilities. Celcoin has expanded BaaS and embedded finance through sustained investment and M&A, supporting both financial and non-financial clients with high Pix throughput for collections and bill pay workflows. QI Tech, the first entity licensed under Brazil’s SCD regime, has issued large volumes of credit and processed significant Pix traffic, positioning itself as a reference for embedded lending and payments orchestration in the South America banking-as-a-service market. FitBank and Pomelo expand issuer processing and BIN sponsorship across Brazil and Mexico to support co-branded issuance and modular card programs at a regional scale.

Strategic moves fall into three vectors. First, geographic expansion as platforms open new markets and extend acceptance networks, exemplified by cross-border Pix acceptance partnerships that allow Brazilian users to pay abroad while settling funds locally for merchants. Second, vertical integration, as networks and processors combine core systems and issuer capabilities, is seen in Visa’s acquisition of Pismo to deliver next-gen processing with cloud-native cores for banks across multiple regions. Third, embedded orchestration enables providers to scale API catalogs, unifying onboarding, payments, credit, and fraud under configurable workflows for fintechs, banks, and non-financial enterprises in the South America banking-as-a-service market. Funding activity remains active, with platforms raising growth capital to build issuer-processing capacity and tokenization features that underpin programmable cards and cross-border settlement. These strategies reflect a bid to capture enterprise share, reduce time-to-value for SMEs, and harden controls in light of 2026 regulatory expectations.

South America Banking-as-a-Service Industry Leaders

Dock (Brazil)

Celcoin

QI Tech

Pomelo

FitBank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Pomelo closed a USD 55 million Series C round co-led by Kaszek and Insight Partners to accelerate issuer-processing expansion in Brazil and Mexico, develop a stablecoin-native global card, and enhance payment tokenization and AI-powered chargeback management.

- November 2025: Brazil’s Central Bank and National Monetary Council enacted Joint Resolution No. 16 to define BaaS governance, risk management, and compliance obligations for BaaS providers, with compliance due by December 31, 2026.

- September 2025: The Brazilian Development Bank approved USD 9.3 million for PD Bank 3.0 to support an AI-enabled banking platform and BaaS integration initiatives.

- August 2025: QI Tech secured a USD 63 million extension to its Series B funding to expand API-driven financial services and embedded banking offerings across fintechs and enterprise partners.

South America Banking-as-a-Service Market Report Scope

| Payment Gateway |

| Bank Account/Core Banking |

| Lending and Credit Services |

| Embedded Finance Software |

| Other Product Types |

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| Banks |

| Fintech Corporations |

| Other End Users |

| Platform / Infrastructure |

| Services (Compliance, KYC, Fraud, etc.) |

| Brazil |

| Peru |

| Chile |

| Argentina |

| Rest of South America |

| By Product Type | Payment Gateway |

| Bank Account/Core Banking | |

| Lending and Credit Services | |

| Embedded Finance Software | |

| Other Product Types | |

| By Enterprise Size | Large Enterprises |

| Small & Medium Enterprises (SMEs) | |

| By End User | Banks |

| Fintech Corporations | |

| Other End Users | |

| By Component | Platform / Infrastructure |

| Services (Compliance, KYC, Fraud, etc.) | |

| By Geography | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and growth outlook for the South America Banking as a Service market?

The South America Banking as a Service market size is USD 0.5 billion in 2026 and is projected to reach USD 1.5 billion by 2031 at a 23.7% CAGR.

Which segments lead in value and growth within the South America Banking as a Service market?

In 2025, payment gateways led in value at 36.8% share, while embedded finance software is the fastest-growing at 24.8% CAGR through 2031.

Which countries are most important to growth in the South America Banking as a Service market?

Brazil held 68.9% of 2025 value due to Pix and Open Finance scale, while Peru is forecast as the fastest-growing at 17.4% CAGR to 2031.

How do instant payments influence competitive dynamics in the South America Banking as a Service market?

Pix and other real-time rails reduce acceptance costs and enable embedded finance at checkout, which compresses card economics and shifts value to data-driven lending and treasury services.

What regulatory changes matter most for the South America Banking as a Service market in 2026?

Joint Resolution No. 16 formalizes BaaS governance, while device registration and return-mechanism enhancements harden Pix fraud controls, raising baseline requirements for third-party risk and compliance.

How will tokenization and CBDCs affect the South America Banking as a Service market?

Drex pilots and stablecoin-core integrations enable programmable settlement and cross-border treasury, preparing the ecosystem for on-chain liquidity and smart-contract use cases as standards mature.

Page last updated on: