United Kingdom Retail Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

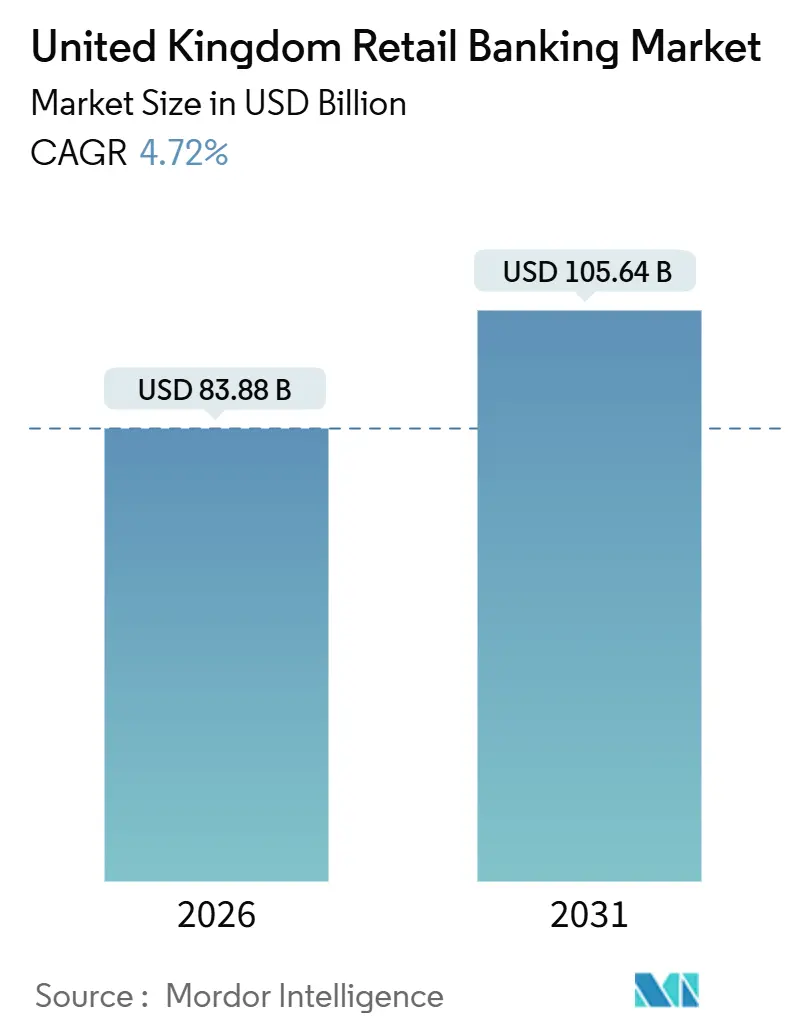

| Market Size (2026) | USD 83.88 Billion |

| Market Size (2031) | USD 105.64 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Retail Banking Market Analysis by Mordor Intelligence

The United Kingdom retail banking market stands at USD 83.88 billion in 2026 and is projected to reach USD 105.64 billion by 2031, reflecting a market size expansion at a 4.72% CAGR. Growth momentum in the United Kingdom retail banking market is reinforced by structural hedge reinvestment benefits that support net interest income even as policy rates decline. Open-banking APIs are driving account aggregation and switching at scale in the United Kingdom retail banking market, while regulated buy-now-pay-later formalizes a large unsecured installment segment. Net interest margins remained resilient through 2025 as maturing hedges rolled into higher-yielding instruments despite Bank Rate cuts, which supports near-term revenue durability in the United Kingdom retail banking market. Regulatory settings around affordability tests, consumer duty expectations, and digital payments rules shape how banks price risk, allocate capital, and structure product journeys in the United Kingdom retail banking market[1].

Key Report Takeaways

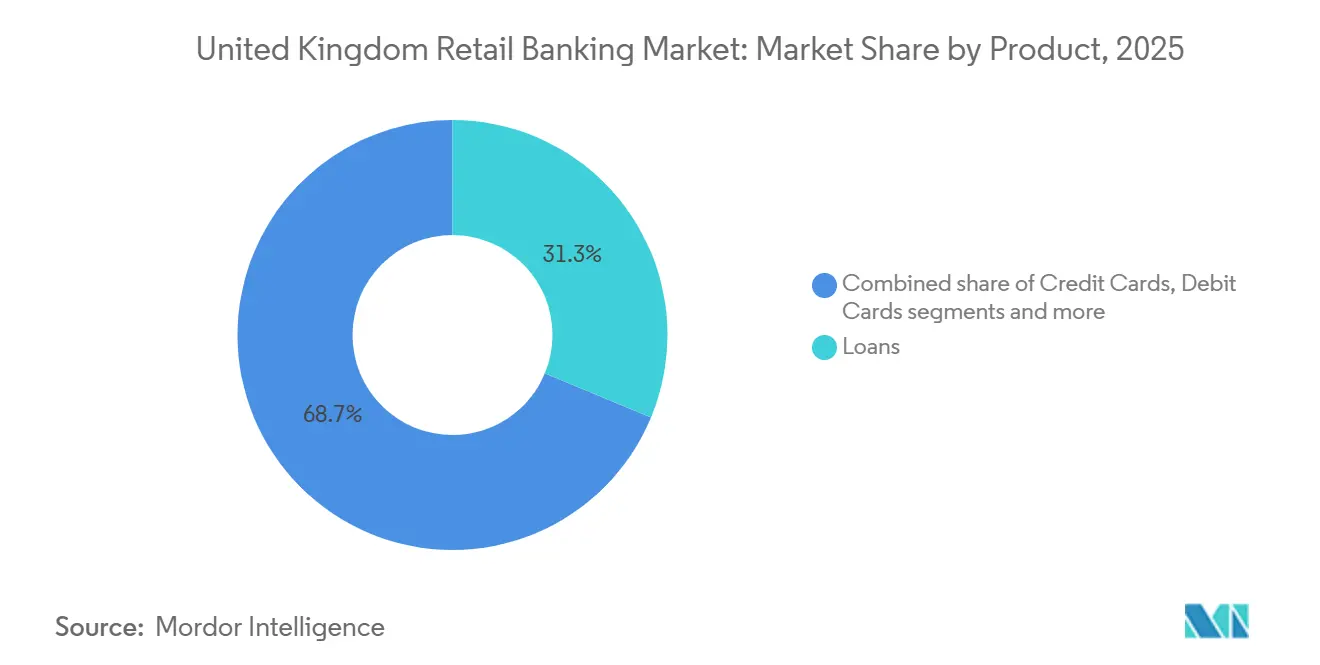

- By product, loans led with 31.26% market share in 2025, while other products are forecasted to expand at a 6.89% CAGR to 2031.

- By channel, online banking held a 52.51% share in 2025 and is projected to grow at a 7.27% CAGR through 2031.

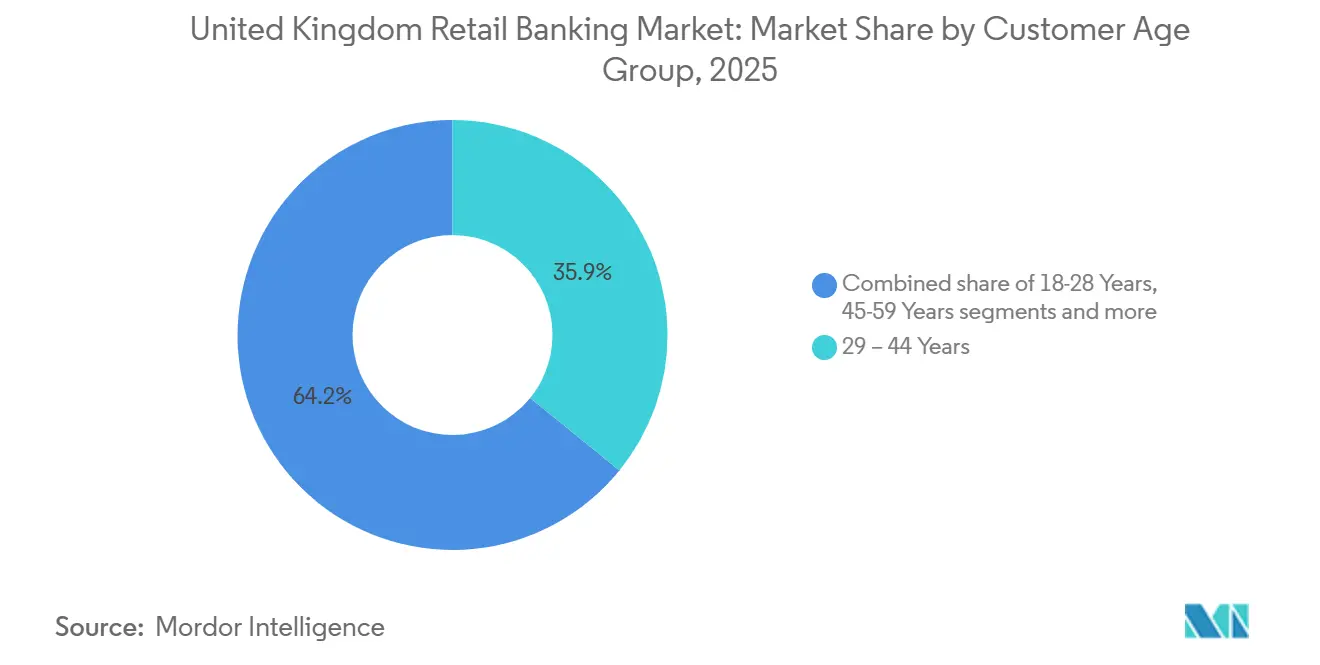

- By customer age group, the 29–44 segment held 35.85% in 2025, while the 18–28 segment is forecasted to grow at a 6.33% CAGR through 2031.

- By bank type, national banks commanded a 67.57% share in 2025, and neobanks and challengers are projected to grow at a 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Retail Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bank Rate-Induced Expansion of Net-Interest Margins | +0.9% | Global (United Kingdom-domiciled banks) | Medium term (2-4 years) |

| Mandatory Open-Banking APIs Accelerating Account-Switching & Aggregation | +0.6% | National, with early gains in London, Manchester, Edinburgh | Short term (≤ 2 years) |

| Rapid Adoption of Mobile Banking in the United Kingdom | +0.7% | National | Short term (≤ 2 years) |

| Fixed-Rate Mortgage Maturity Wave Driving Re-Mortgage Volumes | +0.8% | National, concentrated in the South East, London | Medium term (2-4 years) |

| Regulated Buy-Now-Pay-Later Boosting Unsecured Lending Penetration | +0.5% | National | Medium term (2-4 years) |

| Rise of ESG-Linked Deposit Products under the United Kingdom Green Finance Strategy | +0.4% | National, urban centers lead | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bank Rate-Induced Expansion of Net-Interest Margins

The average Bank of England (BoE) interest rate in the first half of 2024 was 5.25%, which led to a significant improvement in deposit margins and net interest margin (NIM). This mechanical uplift supported top-line resilience during a period when competitive pressures on deposits did not fully pass through lower headline rates. Portfolio dynamics such as higher hedge yields and moderated deposit migration offset rate cuts in the near term. Adjustments to affordability testing parameters created flexibility in retail underwriting without breaching systemwide constraints. The combined effect sustains revenue durability as policy rates trend lower in 2026[2]Barclays, “FY 2024 Results Presentation,” Barclays PLC, home.barclays .

Mandatory Open-Banking APIs Accelerating Account-Switching & Aggregation

As of March 2025, the total number of active open banking users in the United Kingdom stood at around 13.3 million, reflecting steady growth and a broader trend towards digital financial services. Over 23 million one-off payments were successfully processed using open banking by early 2025, with 3.7 million successful Variable Recurring Payment (VRP) transactions recorded in March alone. The Data Use and Access framework created a durable governance structure through a “Future Entity,” with the FCA providing supervisory clarity and embedding open banking as permanent infrastructure. API performance metrics demonstrated reliability across billions of monthly calls, reflecting a mature ecosystem that supports higher switching and aggregation. Cross-border interchange interventions by the PSR reinforced incentives for account-to-account payments in specific use cases. Technical standards, including ISO 20022 and clear complaint-handling pathways through the Financial Ombudsman Service, complete the operational stack for adoption[3]Financial Conduct Authority, “Research Note: Open banking and open finance in the UK,” Financial Conduct Authority, fca.org.uk .

Rapid Adoption of Mobile Banking in the United Kingdom

Mobile has become the primary channel for everyday banking. Daily mobile-banking usage reached 33% in July 2024, up from 18% five years prior, as banks migrated transactional journeys to app-native interfaces. Banks report that app-based journeys now handle the vast majority of sales and service tasks, supported by AI assistants and integrated wealth features in premium propositions. Ongoing branch optimization accompanies the digital shift while customer complaint volumes remain stable as more activity moves in-app. Regulation emphasizes transparent digital journeys and fraud reimbursement standards for push payments that banks must embed into their mobile workflows. These channel and compliance shifts reinforce the digital-first trajectory in the United Kingdom retail banking market[4].

Fixed-Rate Mortgage Maturity Wave Driving Re-Mortgage Volumes

A large cohort of fixed-rate mortgages maturing in 2025 lifted external remortgage activity and sharpened pricing competition among major lenders. Quoted two-year and five-year rates eased from early-2025 peaks, creating an attractive refinancing window for low loan-to-value borrowers. Product innovation extended to higher loan-to-income options within risk controls, aided by adjustments to affordability stress tests. Platform data showed a rise in remortgage searches, including later-life borrowers seeking to refinance into retirement. These factors together support volume growth in secured lending flows in the United Kingdom retail banking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Caps Compressing Card-Fee Income | -0.4% | United Kingdom-EEA cross-border transactions | Short term (≤ 2 years) |

| Branch Closures Creating Rural Financial Exclusion Risk | -0.3% | Rural areas, Northern England, Wales, Scotland | Medium term (2-4 years) |

| FCA Consumer Duty Escalating Compliance & Product-Design Costs | -0.5% | National | Short term (≤ 2 years) |

| Loan-Impairment Spike from Cost-of-Living Squeeze | -0.6% | National, acute in the Midlands, North | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps Compressing Card-Fee Income

The PSR’s market review into cross-border interchange fees followed material post-Brexit increases for card-not-present transactions, which elevated costs for United Kingdom merchants. The October 2025 consultation advanced a permanent cap approach based on a merchant indifference test, with litigation delaying interim relief and outcomes expected to land in 2026. Banks face fee compression while maintaining fraud prevention investments that the PSR views as necessary for system integrity. Domestic interchange remains bound by EU-derived caps, while cross-border pricing constraints shift economics toward account-to-account alternatives in select flows. The overall effect reduces card-fee income growth in the United Kingdom retail banking market.

Branch Closures Creating Rural Financial Exclusion Risk

Branch networks contracted sharply over the past decade, with closures concentrated in rural and lower-income areas that also exhibit higher digital exclusion. Policymakers mandated minimum access to cash within defined radii, and a program of shared banking hubs is scaling, though coverage lags demand. Older adults and very low-income households remain more reliant on physical channels, which lifts contact-center demand and reduces first-contact resolution when closures occur. Customer attrition rises among branch-dependent users, and alternative finance providers have exploited service gaps in deprived neighborhoods. Mutuals have extended branch commitments to cushion access risks, which helps address vulnerable customer needs in the United Kingdom retail banking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: "Other Products" Sprints Ahead as Fee-Based Bundles Diversify Revenue

Loans accounted for 31.26% of product share in 2025 within the United Kingdom retail banking market, while other products are set to grow at a 6.89% pace to 2031 as banks expand packaged accounts, wealth bundles, and embedded finance. Fee-generating services gained prominence as lenders balanced risk-weighted assets with capital-light revenues, aided by premium propositions that integrate concierge, travel, and wealth support. Transactional accounts remain ubiquitous, yet commoditization encourages banks to layer services that lift cross-sell and retention in the United Kingdom retail banking market. Deposit preferences reflect dynamic rate expectations, which saw savers rotate between fixed and easy-access options across 2024 and 2025. Payment volumes stayed high, with debit card activity dominating domestic transactions and credit card balances split between interest-bearing users and transactors. Compliance requirements cover fair value in packaged accounts and BNPL regulation, which formalizes installment credit protections in the United Kingdom retail banking market.

The United Kingdom retail banking market size attribution within product lines shows loans as the largest contributor by share in 2025, and other products as the fastest-growing category through 2031. Wealth propositions added premium features to strengthen primary-banking status and deepen balances across current, savings, and investment relationships. Mortgage portfolios served as the anchor for balance sheet growth while credit card books reflected mixed behavior between revolvers and transactors. Deposit flows responded to changing rate expectations as households weighed savings yields against spending pressures. Product governance and reporting standards evolved in parallel with broader Consumer Duty and BNPL oversight requirements.

By Channel: Digital Dominance Reshapes Cost Structures but Hybrid Models Anchor Trust

Online banking held 52.51% in 2025 and is expected to expand at 7.27% through 2031, outpacing offline, as mobile becomes the primary access point in the United Kingdom retail banking market. Banks reported that app-centric journeys now drive most retail sales, while AI-enabled assistants improve self-service rates in digital channels. Contact centers and branches still carry advisory and complex resolutions, which support hybrid delivery despite branch optimization. Mutuals and select regionals preserved larger physical footprints to support vulnerable and high-net-worth segments who prefer in-person engagement. Digital channel compliance emphasizes transparent promotions, fraud reimbursement, and interoperable messaging to standardize customer protection in the United Kingdom retail banking market.

The United Kingdom retail banking market size contribution from online channels grew as app engagement deepened and share shifted away from branch-only usage. Neobanks leveraged cloud-native stacks and API-first design to compress time-to-market for new features, which raised customer expectations of speed and personalization. Incumbents invested in data, AI, and engineering productivity to simplify journeys and reduce cost-to-serve. Payment security, confirmation-of-payee, and APP fraud reimbursement rules are being embedded in mobile flows to maintain trust. The result is a stable hybrid model where digital handles routine needs at scale and physical channels protect service quality for complex tasks in the United Kingdom retail banking market.

By Customer Age Group: Gen Z and Millennials Drive Digital-First Velocity While Boomers Monetize Equity

The 29–44 segment held 35.85% in 2025 and remains central to mortgages, current accounts, and accumulation products in the United Kingdom retail banking market. The 18–28 cohort is the fastest growing at 6.33% through 2031, as most either hold or plan to hold digital-only accounts and show high mobile payments usage. Digital adoption gaps narrowed among older cohorts as simplified interfaces encouraged uptake of mobile and wallet features. Young adults favored mobile management and BNPL more than older groups, while debit usage remained universal across age bands. Later-life borrowing showed rising remortgage interest, including equity-rich households refinancing into retirement.

The United Kingdom retail banking market size dynamics by age are shaped by income, life stage, and digital capability, which influence product mix and channel preference. Millennials carry higher card spend and slightly higher delinquency in some cohorts, which strengthens the case for proactive affordability analytics and alerts. The 60+ cohort holds substantial savings and ISA balances and shows rising comfort with simplified mobile journeys. Younger users value speed and budgeting tools, while older users seek service reliability and clear support paths. BNPL regulation that brings affordability checks and file reporting will be important for younger segments with higher adoption rates in the United Kingdom retail banking market.

By Bank Type: Incumbents Sustain Share via M&A and AI as Neobanks Force Unbundling

National banks held a 67.57% share in 2025, supported by deposit franchises, recognized brands, and capital strength in the United Kingdom retail banking market. Consolidation reinforced scale, including deals that added current accounts, deposits, and mortgage books while enabling IT rationalization. Neobanks and challengers are the fastest growing cohort at 9.23% CAGR, using API-native architectures and agile delivery to ship features quickly. Mutuals maintained a strong mortgage presence and first-time-buyer support, with targeted branch commitments that differentiate service. Forthcoming capital reforms and proportionate frameworks aim to balance resilience with competitiveness across bank tiers in the United Kingdom retail banking market.

The United Kingdom retail banking market share remains anchored by the largest incumbents, while digital challengers shift customer expectations on onboarding and product iteration. Incumbents scaled AI programs and modernized data platforms to compress costs and improve journey quality. Strategic refocusing and reinvestment followed asset sales and targeted acquisitions in consumer finance. Mutuals pursued growth through transformative deals and reinforced commitments to local presence. These adjustments maintain a competitive balance where scale, technology, and distribution breadth define positioning in the United Kingdom retail banking market.

Geography Analysis

Regional variation in the United Kingdom retail banking market is shaped by income distribution, housing dynamics, and digital infrastructure rather than cross-border capital flows. London and the South East concentrate high balances and volumes, with ISA holder distribution and remortgage searches highlighting the weight of those regions. Saturation in remote banking reduces incremental gains at the margin, which encourages banks to focus on underserved customer needs in the Midlands and the North. Savings ratios rose during 2024 in response to cost-of-living pressures, which influenced deposit mix and risk appetite. Policymakers and industry bodies emphasized inclusion and access as the United Kingdom retail banking market deepened its digital-first trajectory.

Devolved nations and major regional cities carry strategic weight beyond their share of assets due to talent hubs, ring-fenced bank headquarters, and technology centers. Banks expanded regional campuses for risk, operations, and engineering roles to capture cost arbitrage and access skills. Government and central bank locations outside London added to regional relevance as decentralization progressed. Office take-up data show a multi-year rebalancing of capacity, which aligns with distributed tech teams for digital modernization. These factors sustain a broader national footprint for the United Kingdom retail banking market.

Urban-rural divides persist as mobile-first adoption accelerates while broadband gaps limit digital uptake in some areas. Older and lower-income households show higher reliance on cash and in-person support, which increases the importance of hubs and co-located community branches. Access-to-cash mandates and hub rollout plans aim to mitigate exclusion, though implementation lags in the most affected constituencies. Consumer Duty vulnerability guidance reinforces proactive identification of limited digital capability and low resilience. Fraud reimbursement rules further protect less digitally confident users in the United Kingdom retail banking market.

Competitive Landscape

The United Kingdom retail banking market exhibits moderate concentration with an oligopolistic core, with the largest banks holding the majority of primary current accounts and mortgage balances, while challengers reach profitability and scale. Incumbents delivered strong returns and returned capital while reshaping portfolios through disposals and targeted acquisitions. Productivity programs focus on AI deployment, cloud modernization, and engineering efficiency to reduce costs and lift customer satisfaction. Neobanks and fintechs leveraged open-banking rails and cloud-native cores to compress product cycles and unbundle services. The competitive balance turns on distribution breadth, funding costs, and pace of digital execution in the United Kingdom retail banking market.

White-space opportunities cluster in embedded finance, later-life lending, and climate-transition funding. Product ecosystems around housing help retain mortgage customers and extend lifetime value. Capital allocation to green housing and social outcomes aligns with national goals and customer savings in energy-efficient homes. Specialist plays in SME and niche mortgages benefit from proportionate frameworks and risk expertise. These levers support differentiation while maintaining resilience in the United Kingdom retail banking market.

Strategic moves underscore how incumbents and challengers adjust to the same regulatory and macro backdrop at different speeds. Santander’s pending acquisition of TSB will expand its current account base and mortgage position at a planned cost. Barclays completed the Tesco Bank acquisition, adding a sizable mortgage and deposit franchise to its United Kingdom unit. NatWest integrated Sainsbury’s Bank assets and advanced a multi-year cloud and AI transformation with leading partners. Regulatory influence shapes competitive boundaries: the FCA Consumer Duty's emphasis on vulnerable-customer outcomes favours incumbents' omnichannel breadth (61% of Gen Z prefer face-to-face support for complaints, yet 81% use mobile apps for transactions), while Basel 3.1's January 2027 implementation and the Strong and Simple Framework for SDDTs may narrow capital-cost gaps, allowing challengers like OakNorth and Metro Bank to price more aggressively in SME and specialist-mortgage niches. These actions reinforce scale while enabling targeted reinvestment in the United Kingdom retail banking market.

United Kingdom Retail Banking Industry Leaders

Lloyds Banking Group PLC

Barclays Bank UK PLC

HSBC UK Bank plc

NatWest Group PLC

Santander UK PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Banco Santander reached an agreement to buy TSB from Banco de Sabadell, strengthening its United Kingdom presence; the deal is expected to close in Q1 2026, creating one of the United Kingdom’s largest retail banking franchises.

- July 2025: Lloyds introduced Athena, an AI-powered knowledge hub for frontline staff, significantly improving internal search efficiency and expected to save thousands of hours in customer-service time.

- July 2025: HSBC UK launched a flagship wealth centre in Mayfair as part of its strategy to strengthen wealth management and international services for Premier and Private Banking clients.

- January 2025: HSBC UK launched a flagship wealth centre in Mayfair as part of its strategy to strengthen wealth management and international services for Premier and Private Banking clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom retail banking market as all fee and interest income generated from current and savings accounts, unsecured personal lending, mortgages, payment cards, and related digital-banking services offered to individuals and very small enterprises. Products aimed at corporates, investment banking desks, and capital-markets activities stay outside this scope.

Scope exclusion: corporate and wholesale banking revenues are not counted.

Segmentation Overview

- By Product

- Transactional Accounts

- Savings Accounts

- Debit Cards

- Credit Cards

- Loans

- Other Products

- By Channel

- Online Banking

- Offline Banking

- By Customer Age Group

- 18-28 Years

- 29-44 Years

- 45-59 Years

- 60 Years and Above

- By Bank Type

- National Banks

- Regional Banks

- Neobanks & Others

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we interviewed branch managers, digital-only executives, consumer finance academics, and fintech associations across London, Birmingham, Manchester, and Edinburgh. Conversations clarified pricing spreads, neobank account churn, and channel cost curves, enabling our team to reconcile modeled margins with on-ground realities.

Desk Research

Mordor analysts began with publicly available tier-1 datasets such as Bank of England monetary statistics, FCA strategic reviews, UK Finance mortgage and card volumes, the Office for National Statistics household income series, and IMF macro indicators. Regulatory filings, investor presentations, and reputable trade journals helped sharpen product split ratios, while paid tools, D&B Hoovers for bank financials and Dow Jones Factiva for press flow, supplied timely corporate moves. These sources, together with other government releases and association papers consulted but not listed here, built the factual base.

Market-Sizing & Forecasting

A top-down construct starts with Bank of England deposit and loan stock, reconstructs fee pools from payment-volume estimates, and then aligns with FCA household penetration data. Select bottom-up checks, sampled bank financials and typical APR×volume tests, re-anchor totals. Key model drivers include personal deposit growth, mortgage originations, average net interest margin, digital-bank adoption, real GDP, and policy rate trajectories. Multivariate regression projects each driver, after which scenario analysis adjusts for regulatory or rate shocks; gaps in bottom-up inputs are bridged with regional peer benchmarks or prudent elasticity ranges.

Data Validation & Update Cycle

Outputs pass variance scans against historical trends and peer ratios before a senior analyst reviews anomalies. Reports refresh once a year, with interim patches if material events, rate resets or major M&A, shift the baseline. A final pre-release sweep ensures clients receive the latest vetted view.

Why Mordor's UK Retail Banking Baseline Inspires Confidence

Published figures often diverge because firms mix corporate banking, apply divergent rate paths, or lock forecasts to outdated exchange rates. By ring-fencing strictly retail income streams and refreshing assumptions each quarter, Mordor presents a decision-ready midpoint, whereas others may overstate growth by folding in investment services or understate it through conservative digital-adoption curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 80.1 B (2025) | Mordor Intelligence | - |

| USD 91.0 B (2024) | Global Consultancy A | Includes wealth-management and SME cash-management fees |

| USD 71.1 B (2024) | Industry Association B | Uses narrower product list, omits credit-card interchange |

| USD 71.0 B (2024) | Regional Consultancy C | Applies constant 2023 FX rate and excludes digital-only banks |

Taken together, the comparison shows that when scope, FX, and product granularity are harmonized, Mordor's disciplined bottom-up checks atop a transparent top-down spine deliver the balanced, reproducible baseline that stakeholders can trust.

Key Questions Answered in the Report

What is the projected size and growth outlook for the United Kingdom retail banking market by 2031?

The United Kingdom retail banking market is projected to reach USD 105.64 billion by 2031 at a 4.72% CAGR from a 2026 market size of USD 83.88 billion.

Which product categories are leading and growing fastest in the United Kingdom retail banking?

Loans led with a 31.26% share in 2025, while other products that include packaged accounts and wealth bundles are the fastest growing at a 6.89% CAGR through 2031.

How is the channel mix changing in the United Kingdom retail banking?

Online banking held 52.51% in 2025 and is expected to grow at 7.27% through 2031, reflecting the shift to mobile-first usage and digital sales at scale.

Which customer segment is expanding fastest in the United Kingdom retail banking?

The 18–28 cohort is expanding at a 6.33% CAGR, while the 29–44 group held the largest share at 35.85% in 2025.

How are regulations shaping United Kingdom retail banking through 2026?

Consumer Duty and open banking standards, BNPL regulation effective in 2026, and APP fraud reimbursement rules are reshaping product design, digital journeys, and consumer protections.

What recent strategic moves are reshaping the competitive field in the United Kingdom retail banking?

Santander’s acquisition of TSB, Barclays’ integration of Tesco Bank, and NatWest’s purchase of Sainsbury’s Bank assets are expanding scale, while AI and data programs at incumbents are accelerating modernization.

Page last updated on: