India Private Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

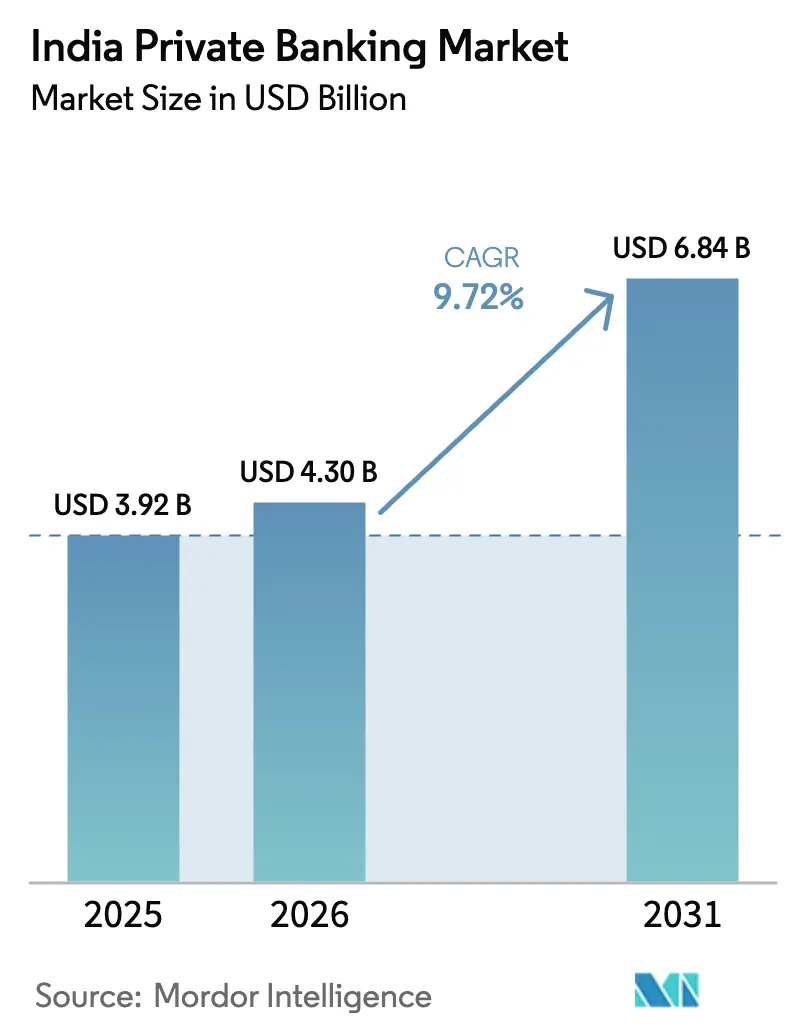

| Base Year Market Size (2025) | USD 3.92 Billion |

| Market Size (2026) | USD 4.3 Billion |

| Market Size (2031) | USD 6.84 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Private Banking Market Analysis by Mordor Intelligence

The India private banking market size is expected to grow from USD 3.92 billion in 2025 to USD 4.3 billion in 2026 and is forecast to reach USD 6.84 billion by 2031 at 9.72% CAGR over 2026-2031. Rising ultra-high-net-worth (UHNW) wealth, wider use of digital engagement tools, and a friendlier cross-border remittance framework are steering demand for bespoke advisory services. West India remains the principal hub, yet the North-East registers the fastest wealth creation as infrastructure corridors mature. Competitive intensity is high because the top five institutions already control 70% of the India private banking market, but differentiation through family-office capabilities and alternative investment access keeps margins resilient. Non-obvious growth stems from the convergence of onshore and offshore wealth structuring, the rise of domestic REITs, and a gradual shift from plain-vanilla asset allocation to impact-oriented direct deals, all of which expand wallet share without outsized balance-sheet risk.

Key Report Takeaways

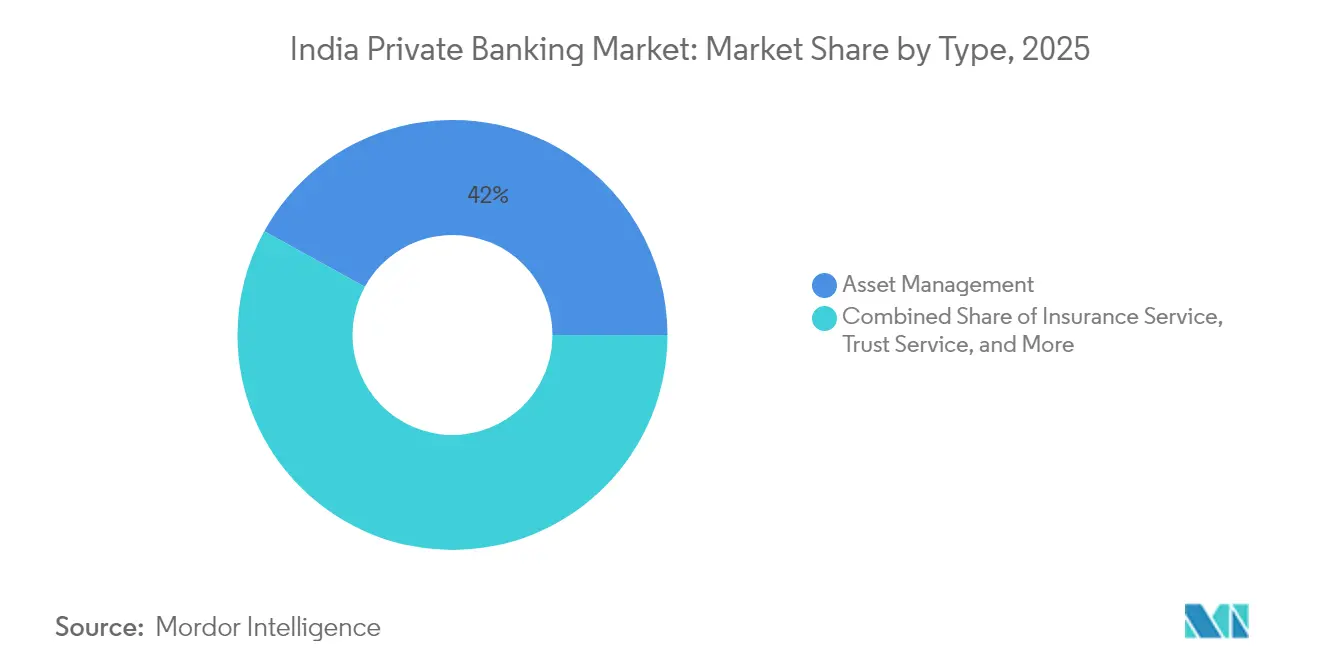

- By type, asset management captured 41.98% of India's private banking market size in 2025, while real-estate consulting is expected to expand at a 14.88% CAGR to 2031.

- By application, personal banking controlled 75.62% India private banking market size in 2025; enterprise wealth management is projected to rise at a 11.95 % CAGR through 2031.

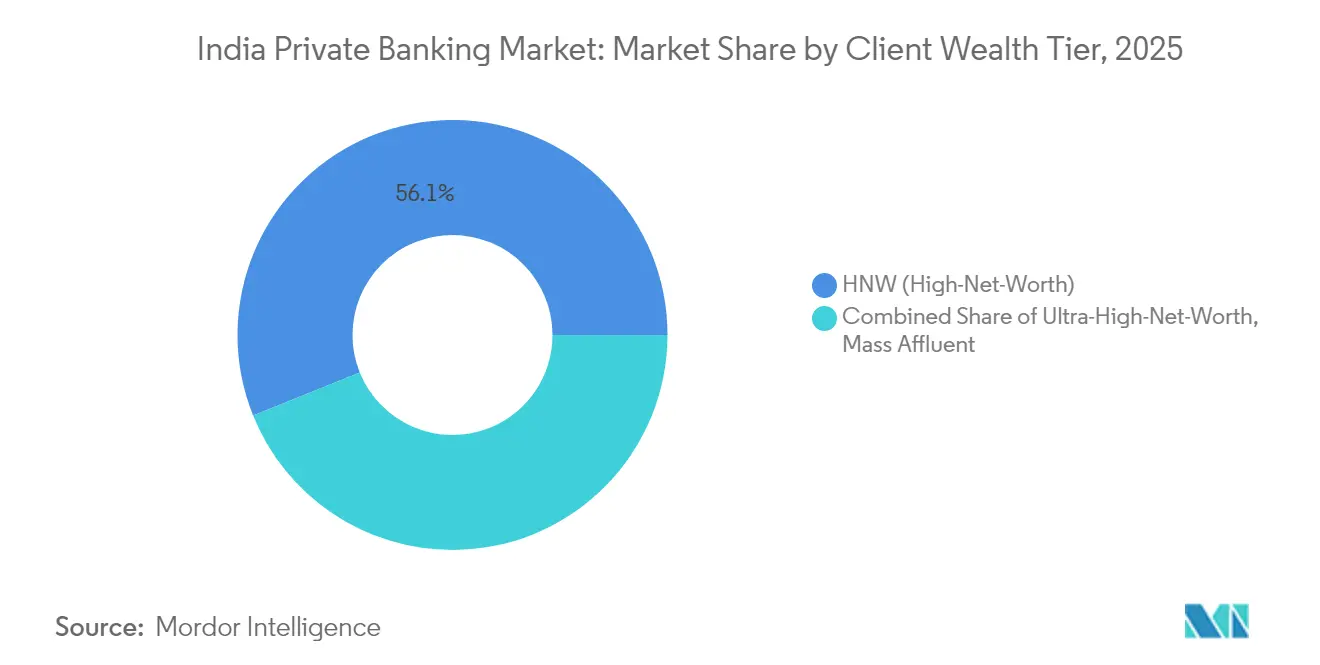

- By client wealth tier, high-net-worth accounts held 56.10% of India private banking market share in 2025 value, whereas the UHNW segment is forecast to grow the fastest at a 13.96 % CAGR.

- By geography, West India led with 30.05% of India private banking market share in 2025, and the North-East is positioned for a 15.71 % CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Private Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of ultra-high-net-worth individual (UHNW) population | +2.8% | National, with concentration in West India, North India | Long term (≥ 4 years) |

| Digital-first onboarding & advisory platforms gaining trust post-COVID | +1.9% | National, with higher adoption in metro cities | Medium term (2-4 years) |

| Liberalised Remittance Scheme (LRS) raising offshore investment appetite | +1.5% | National, with preference corridors to UK, Singapore, UAE | Medium term (2-4 years) |

| Rising allocation to alternative investments by Indian HNWIs | +1.7% | National, with early gains in Mumbai, Delhi, Bangalore | Long term (≥ 4 years) |

| Family-office professionalisation among first-generation entrepreneurs | +1.2% | Emerging in tier-1 and tier-2 entrepreneurial hubs | Long term (≥ 4 years) |

| On-demand ESG & impact-oriented portfolios requested by millennials | +1.0% | National, with strong pull in urban wealth centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of UHNW Population

As reported by industry experts, individuals holding more than USD 30 million in assets climbed 58% between 2019-2024 to 13,263, placing India third behind the United States and China.[1]Knight Frank, “Wealth Report 2024,” knightfrank.com. The surge drives demand for multi-generational estate planning, cross-border tax structuring, and direct private-equity exposure. Wealth is concentrated in technology, pharmaceuticals, and financial services founders who often formalize single-family offices soon after liquidity events. The number of Indian family offices rose from roughly 45 in 2018 to over 300 by 2024, handling combined assets of about USD 30 billion.[2]ET Online, “360 ONE WAM to acquire UBS India wealth biz in Rs 307 crore deal,” indiatimes.com.Their global outlook 68% hold offshore assets, forces private banks to integrate international custody, foreign real-estate advisory, and pre-immigration tax planning into core service menus.

Digital-First Onboarding & Advisory Platforms Gaining Trust

Three pandemic years transformed client engagement. Paperless KYC, video-based relationship reviews, and app-based portfolio dashboards cut onboarding turnaround from weeks to days, giving early adopters a clear cost-to-income advantage. Native digital platforms now push real-time market alerts, thematic portfolio insights, and straight-through execution for domestic and foreign securities, which resonates strongly with tech-savvy UHNW heirs. Banks that pair analytics-guided prospecting with hybrid human advice report a higher share of wallet, yet must invest continuously in cybersecurity, behavioral analytics, and cloud resiliency to preserve trust. The digital shift also unlocks tier-2 and tier-3 profitability because remote advisory reaches clients previously overlooked by branch-centric models.

Liberalised Remittance Scheme Raising Offshore Appetite

The Reserve Bank of India’s LRS cap of USD 250,000 a year has become a pivotal enabler of global diversification. Indian residents increasingly channel funds toward London-listed investment trusts, Singapore-based feeder funds, and Dubai residential property. Integrated onshore–offshore propositions command premium advisory fees because clients prefer a single dashboard that consolidates multi-jurisdiction holdings. Banks owning booking centers in Singapore or Dubai enjoy a head start, while purely domestic players race to sign correspondent agreements. The scheme also fuels dual-currency lending and estate-planning vehicles that blend Indian and overseas assets, cementing cross-border considerations as a mainstream advisory theme.

Rising Allocation to Alternative Investments

SEBI-registered Alternative Investment Funds (AIFs) reached USD 87.13 billion AUM by March 2024, and private-banking clients are prominent contributors.[3]The Hindu, “Outlook 2025: Emerging trends of real estate sector,” thehindu.com. High-conviction families now target venture capital, private credit, and thematic infrastructure vehicles for both return enhancement and impact alignment. Demand for co-investment rights, secondaries liquidity windows, and tokenized real-estate funds is accelerating. Relationship managers must therefore master deal sourcing, operational due diligence, and post-investment monitoring, skills once confined to institutional desks. Higher fee yields 200-300 basis points above mutual-fund averages, boost revenue yet also require stronger risk and suitability frameworks under SEBI’s evolving conduct rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asset-quality concerns amid unsecured retail credit boom | -1.2% | National, with higher concentration in urban centers | Short term (≤ 2 years) |

| Talent attrition to global wealth-techs pushing up cost-income ratios | -0.8% | National, with acute impact in Mumbai, Delhi, Bangalore | Medium term (2-4 years) |

| Fragmented regulatory oversight over wealth-management products | -0.7% | National, with compliance burden felt more by mid-sized players | Medium term (2–4 years) |

| Perception gap on confidentiality after high-profile data leaks | -0.6% | National, with heightened sensitivity among HNWIs in top metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Asset-Quality Concerns Amid Unsecured Retail Boom

India’s rapid expansion in unsecured retail credit presents growing systemic risks for private banking operations. In 2024, personal loans and credit card balances surged, raising alarms about borrower over-leverage and the potential for asset quality deterioration. Private banks are exposed both directly through unsecured lending to affluent clients and indirectly, as many wealth management clients have net worths tied to leveraged business or real estate assets. In response, the Reserve Bank of India introduced stricter norms in November 2024, including higher risk weights and provisioning requirements, which limit balance sheet flexibility and reduce credit availability for portfolio-backed lending. If asset quality weakens further, banks may adopt a more conservative stance, pulling back from innovative wealth products and alternative investment financing.

Talent Attrition to Global Wealth-Techs

The private banking sector is grappling with significant talent retention issues, as annual attrition rates for relationship managers remain high. Global wealth-tech firms and international banks are aggressively poaching experienced professionals by offering attractive compensation packages and equity-based incentives. This talent drain puts upward pressure on operational costs, prolongs recruitment cycles, and disrupts client relationships during advisor transitions. Newly hired relationship managers typically require 12 to 18 months to reach full productivity, leading to temporary dips in client satisfaction and revenue contribution. The challenge is further compounded by increasing demand for niche expertise in areas like alternative investments, cross-border wealth structuring, and family office services, all of which command premium compensation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Asset-Management Dominance with Real-Estate Advisory Surge

Asset management commands the largest slice of the India private banking market at 41.98% in 2025. This leadership is anchored in discretionary portfolio mandates, global custody, and structured notes distribution that collectively generate steady annuity-like fees. Broader uptake of ESG-screened strategies and offshore feeder funds is enlarging ticket sizes. Trust and tax-consulting services remain essential adjuncts because first-generation founders increasingly formalize succession blueprints ahead of any potential inheritance-tax reintroduction.

Real-estate consulting is the fastest-growing niche, poised for a 14.88% CAGR. Rising allocations to commercial offices, data centers, and overseas residential assets add complexity around zoning, financing, and exit structuring. Private banks that embed licensed valuers and cross-border property desks have begun displacing standalone brokers. Tokenized property funds and REITs further broaden access for UHNW clients seeking liquidity without direct asset management burdens. Banks, therefore, view real-estate advisory as both a growth vector and a hedge against equity-market volatility within the India private banking market.

By Application: Personal Banking Scale, Enterprise Momentum

Personal mandates represented 75.62% of 2025 revenue, reflecting deep-rooted demand for bespoke investment, tax, and lifestyle solutions. Portfolio credit lines, philanthropy structuring, and concierge privileges continue to differentiate offerings. Digital self-service complemented by human advice compresses operating costs while preserving high-touch rapport, a balance vital for margin defense.

Enterprise wealth management is forecast to compound at 11.95% annually through 2031. Mid-market corporations now outsource treasury, ESOP liquidation, and founder exit planning to specialist desks, generating fee pools beyond traditional retail channels. Business-owner wealth often blurs personal and corporate boundaries; an integrated proposition that aligns balance-sheet financing with family-office governance strengthens client stickiness. Cross-sell opportunities into employee financial-wellness programs and corporate trustee services reinforce lifetime value inside the India private banking market.

By Client Wealth Tier: HNW Scale, UHNW Velocity

High-Net-Worth clients maintain 56.10% market share in 2025, representing the sector's traditional core constituency with investable assets between USD 1-30 million. This segment includes successful professionals, mid-size business owners, and senior corporate executives requiring portfolio management, tax planning, and basic succession advisory services. HNW clients typically utilize standardized private banking products, including mutual fund portfolios, insurance planning, and basic trust structures. The segment's stability provides consistent fee income and serves as a pipeline for future UHNW relationships as clients' wealth accumulates over time. Digital platforms particularly benefit HNW client servicing through cost-effective advisory delivery and automated portfolio management tools.

Ultra-High-Net-Worth clients drive the highest growth at 13.96% CAGR during 2026-2031, despite representing a smaller market share, reflecting their sophisticated service requirements and higher revenue generation per client. UHNW clients demand bespoke advisory services, including family office establishment, multi-generational wealth planning, and direct investment opportunities in private markets. The segment's growth stems from India's expanding billionaire population, which increased from 102 in 2020 to 169 in 2024, and their complex financial needs spanning multiple jurisdictions and asset classes. Mass Affluent clients, while representing the largest population segment, generate lower per-client revenue but benefit from digital platform scalability and standardized product offerings.

Geography Analysis

West India maintains regional leadership with 30.05% market share in 2025, anchored by Maharashtra's concentration of 470 HNWIs and Gujarat's 129 HNWIs, reflecting the region's established financial services infrastructure and entrepreneurial ecosystem. Mumbai's position as India's financial capital drives private banking concentration, with major domestic and international banks maintaining their primary wealth management operations in the city. The region benefits from proximity to capital markets, established family business networks, and sophisticated advisory service providers. Gujarat's industrial base, particularly in chemicals, pharmaceuticals, and textiles, generates substantial entrepreneurial wealth requiring private banking services. The region's growth trajectory remains stable, supported by continued economic development and wealth creation in emerging sectors like renewable energy and technology services.

North India follows with significant market presence, led by Delhi's 213 HNWIs and the National Capital Region's expanding corporate sector. The region's wealth creation stems from real estate development, government contracting, and professional services, with increasing technology sector contribution from Gurgaon and Noida. South India demonstrates robust growth potential, driven by Bangalore's technology ecosystem, Hyderabad's pharmaceutical cluster, and Chennai's automotive manufacturing base. The region's wealth characteristics differ from traditional business families, with technology entrepreneurs and professionals requiring different advisory approaches focused on equity compensation, startup investments, and international expansion planning. North-East India emerges as the fastest-growing region at 15.71% CAGR during 2026-2031, supported by infrastructure development, natural resource extraction, and cross-border trade opportunities with Southeast Asia.Assam's GSDP growth of 8.10% in 2021-22, with per capita NSDP reaching USD 1,236 (INR 102,965), indicates expanding economic activity and wealth creation potential. The region benefits from government infrastructure investments, including transportation connectivity improvements and industrial development initiatives. East India and Central India maintain smaller market shares but demonstrate steady growth through industrial development and agricultural modernization. Private banks increasingly establish regional presence in these emerging markets, recognizing the long-term wealth creation potential and limited competitive intensity compared to established metros.

Competitive Landscape

The India private banking market is highly concentrated, with a small group of major players dominating the landscape. This concentration creates high barriers to entry, making it difficult for new entrants to compete without significant capital and infrastructure. Established banks benefit from deep client relationships, extensive networks, and integrated service offerings that are difficult to replicate. Differentiation increasingly hinges on technology integration and service personalization, especially as clients demand more sophisticated solutions. The relationship-driven nature of private banking favors players with long-standing reputations and comprehensive capabilities.

Leading institutions adopt varied strategic approaches to strengthen market position and meet evolving client expectations. Some emphasize technology-enabled advisory services and robust digital platforms, while others focus on family-office solutions and alternative investment access for ultra-high-net-worth clients. Strategic consolidation gained momentum in 2025, with notable transactions expanding asset bases and enhancing service delivery capabilities. Global banks are shifting from direct competition to partnership-driven models, acknowledging the importance of local expertise and regulatory familiarity. These alliances help balance global product access with the relationship intensity expected by Indian private banking clients.

Technology continues to emerge as a critical competitive lever, with banks investing in generative AI to improve client engagement, streamline operations, and support advisors. Meanwhile, untapped opportunities in Tier-2 cities and niche offerings such as succession planning, ESG-aligned portfolios, and tokenized investments present new growth avenues. However, success in these areas requires both regulatory navigation and internal capability development. The Reserve Bank of India plays a central role in shaping the sector, maintaining a regulatory environment that supports innovation while safeguarding financial stability. Licensing and compliance frameworks remain strict, discouraging low-commitment entrants but incentivizing well-prepared players to drive next-generation private banking models.

India Private Banking Industry Leaders

HDFC Bank Private Banking

ICICI Private Banking

Kotak Wealth Management

Axis Burgundy Private

Yes Private

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sumitomo Mitsui Banking Corp (SMBC) acquired a 20% stake in Yes Bank for INR 134.82 billion (USD 1.6 billion), marking the largest cross-border investment in India's banking sector. The deal gives SMBC two board seats and potential to raise its stake further.

- April 2025: 360 ONE WAM acquired UBS AG’s India wealth management business for INR 3.07 billion (USD 36 million), adding USD 3.12 billion (INR 260 billion) in assets under management. The deal enhances 360 ONE’s position as a top independent wealth manager and establishes a strategic partnership for integrated onshore-offshore services.

- March 2025: ICICI Securities has merged into ICICI Bank, becoming a wholly-owned subsidiary, with shareholders receiving 67 ICICI Bank shares for every 100 ICICI Securities shares. The move streamlines ICICI's wealth management operations and removes potential conflicts between its banking and securities services for private banking clients.

- February 2025: RBI implemented enhanced Liquidity Coverage Ratio guidelines, reducing wholesale deposit run-off rates from 100% to 40% and potentially freeing up USD 36 billion (INR 3 trillion) in banking system liquidity. The regulatory change particularly benefits private banks like Kotak Mahindra Bank, which rely heavily on wholesale funding for wealth management operations and lending to HNI clients.

India Private Banking Market Report Scope

Private banking helps clients to manage their financial assets. Private bankers handle the financial assets of individuals with a holistic approach and offer a personalized solution for the investment of those assets. The India Private Banking Market is segmented based on the banking sector (Retail Banking, Commercial Banking, Investment Banking, and others). The report offers market size and forecasts for the India Private Banking Market in value (USD Million) for all the above segments.

| Asset Management Service |

| Insurance Service |

| Trust Service |

| Tax Consulting |

| Real Estate Consulting |

| Personal |

| Enterprise |

| Mass Affluent |

| High-Net-Worth |

| Ultra-High-Net-Worth |

| North India |

| West India |

| South India |

| East India |

| Central India |

| North-East India |

| By Type | Asset Management Service |

| Insurance Service | |

| Trust Service | |

| Tax Consulting | |

| Real Estate Consulting | |

| By Application | Personal |

| Enterprise | |

| By Client Wealth Tier | Mass Affluent |

| High-Net-Worth | |

| Ultra-High-Net-Worth | |

| By Region | North India |

| West India | |

| South India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

How big is the India private banking market in 2026?

The India private banking market size stands at USD 4.3 billion in 2026 and is projected to grow to USD 6.84 billion by 2031.

Which service type brings in the most revenue for private banks?

Asset-management mandates lead, accounting for 41.98 % of 2025 revenue.

Which region is growing fastest for private banking in India?

The North-East is forecast to expand at a 15.71 % CAGR between 2026 and 2031.

What drives the surge in UHNW clients?

Entrepreneurial liquidity events in technology, pharmaceuticals, and financial services plus sustained GDP growth are swelling the UHNW cohort at a rapid pace.

Page last updated on: