Retail Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.79 Trillion |

| Market Size (2031) | USD 5.20 Trillion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail Banking Market Analysis by Mordor Intelligence

The Retail Banking Market size is expected to increase from USD 3.56 trillion in 2025 to USD 3.79 trillion in 2026 and reach USD 5.20 trillion by 2031, growing at a CAGR of 6.52% over 2026-2031.

The retail banking market is being supported more by the lasting shift toward digital product origination and servicing than by interest-rate support, which is already easing across several banking systems. The United States banks still delivered strong earnings in 2025, with sector net income of USD 295.6 billion and loan balances of USD 13.5 trillion, but that performance increasingly reflects a split between banks that already monetize digital engagement well and those still carrying heavy transformation costs. The retail banking market is also being reshaped by the dominance of online banking, the continued strength of consumer lending, and the faster customer-acquisition pace of neobanks in younger, lower-margin cohorts. Regional growth patterns remain uneven, with North America retaining scale leadership and the Middle East and Africa expanding faster on the back of mobile-led inclusion and digital bank licensing. The main pressure point for the retail banking market is profitability, because margin compression, branch cost drag, and legacy modernization needs are forcing banks to shift more quickly toward fee income, automation, and selective consolidation.

Key Report Takeaways

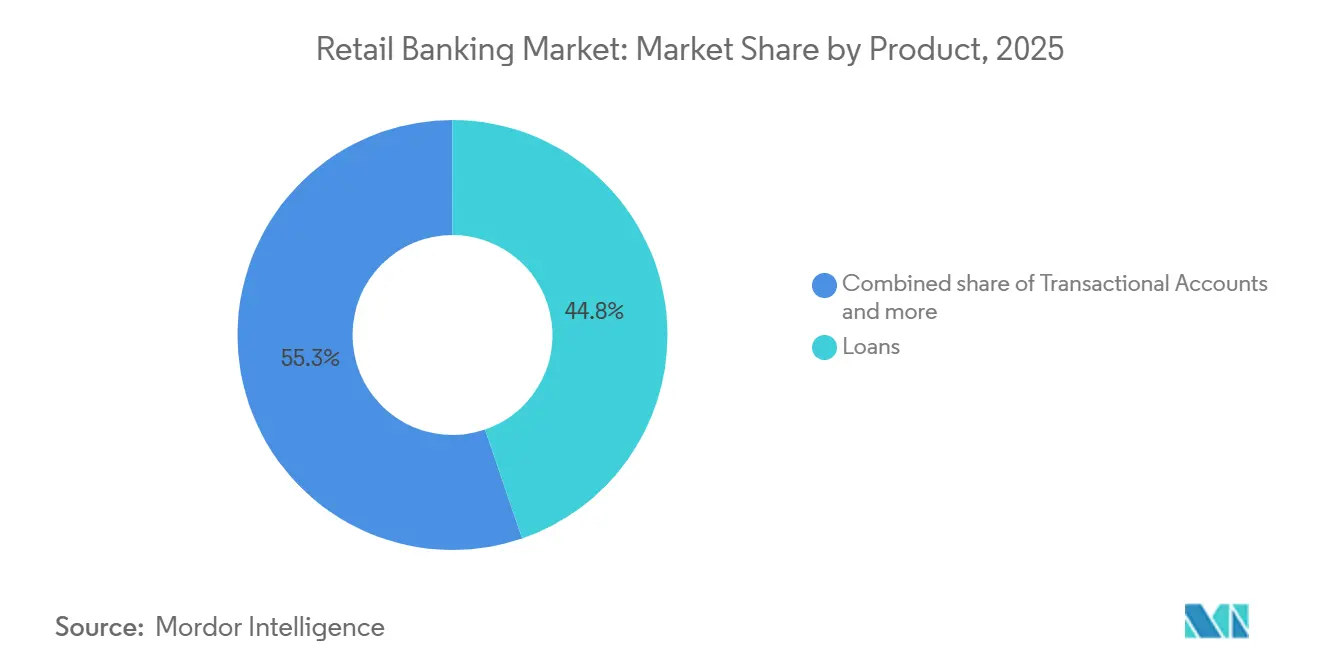

- By product, loans captured 44.75% of the retail banking market share in 2025, while debit cards are projected to grow at 7.76% CAGR between 2026-2031.

- By channel, online banking accounted for 71.48% of the retail banking market in 2025 and is forecast to expand at a 6.16% CAGR through 2031.

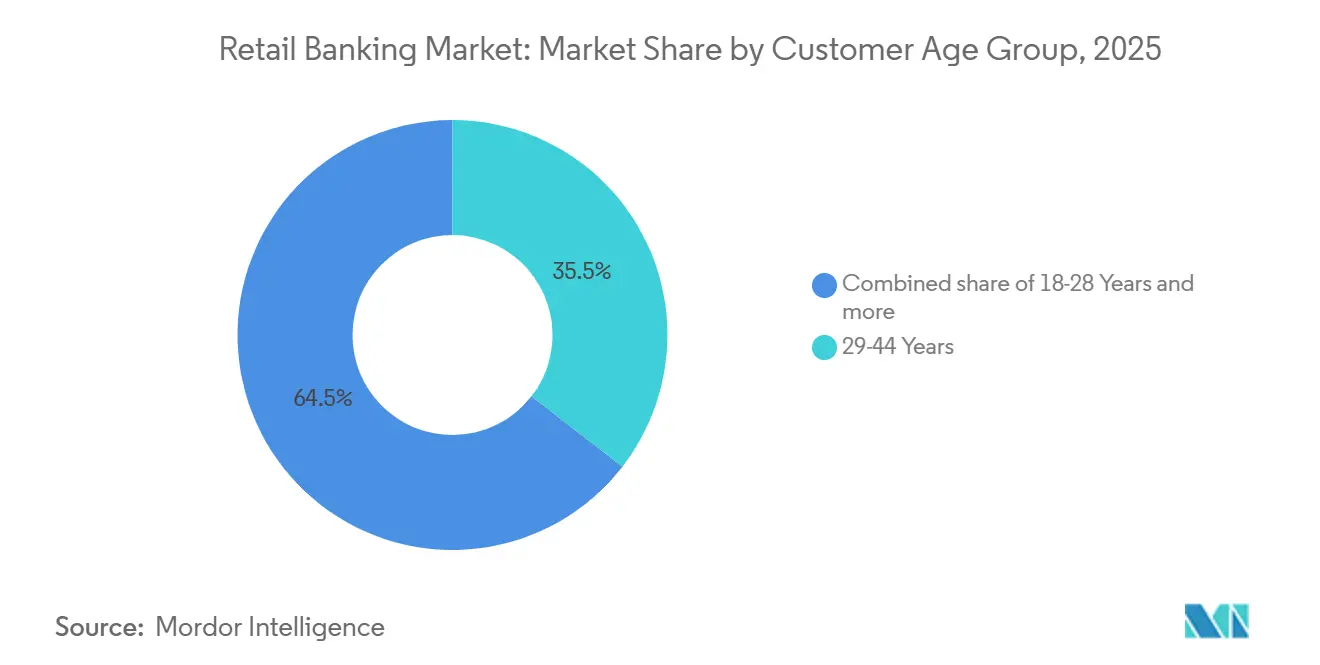

- By customer age group, the 29-44 segment held 35.49% of the retail banking market in 2025, while the 18-28 segment is projected to grow at 6.87% CAGR between 2026-2031 in the market.

- By bank type, national banks captured 67.84% of the retail banking market share in 2025, while neobanks are projected to grow at 8.20% CAGR between 2026-2031 in the market.

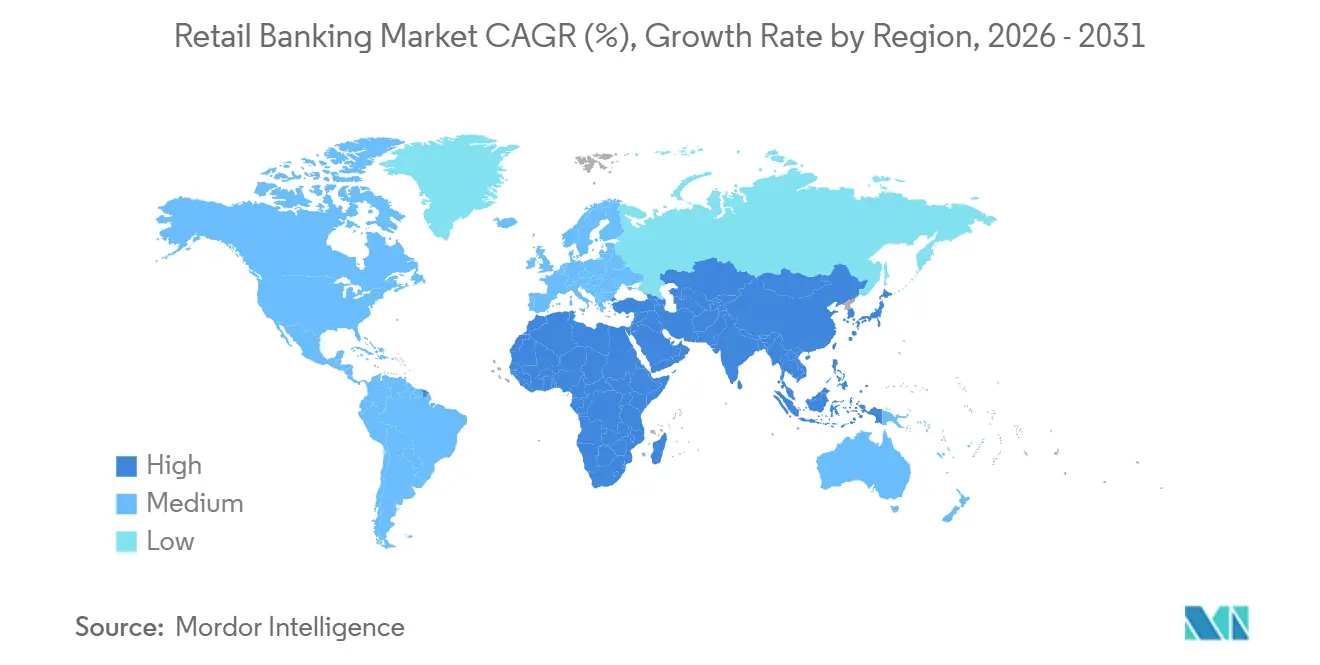

- By geography, North America accounted for 38.02% of the retail banking market in 2025, while the Middle East and Africa are projected to grow at a 7.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retail Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Instant payments adoption driving account primacy | +1.2% | Global, concentrated in Asia-Pacific, Europe, and Latin America | Short term (≤ 2 years) |

| Mobile-first banking preference accelerating digital onboarding | +1.4% | Global, with the highest intensity in Asia-Pacific and Sub-Saharan Africa | Short term (≤ 2 years) |

| AI-personalized offer conversion improving cross-sell economics | +0.9% | North America, Europe, APAC | Medium term (2-4 years) |

| Open banking data portability enabling third-party product distribution | +0.6% | Europe, the United Kingdom, Australia, Brazil | Medium term (2-4 years) |

| Fee-lite digital account acquisition expanding addressable customer base | +0.7% | Emerging markets, North America Gen Z | Short term (≤ 2 years) |

| Real-time fraud analytics scale reducing false-positive friction | +0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Instant Payments Adoption Driving Account Primacy

Instant payment rails are changing, and the institution a consumer treats as their main banking relationship is changing too. The EU Instant Payments Regulation entered into force in October 2025 and requires euro-area payment service providers to offer instant credit transfers at fees no higher than standard transfers[1]CLEARINGPOST.COM European Batch Clearing Volumes Decline as Instant Payments Cross Quarter of Credit Transfer Traffic | ClearingPost. That policy shift has already shown up in transaction behavior, with EBA CLEARING's RT1 platform averaging 6.1 million daily transactions in January 2026, up from 3.66 million in January 2025, while daily settlement values rose to EUR 6.4 billion (USD 7.0 billion). India followed a similar path at a much larger scale, with UPI processing 228.5 billion transactions in 2025, up 33% year over year. For the retail banking market, this means the bank that controls the instant payment experience is more likely to control transaction data, daily engagement, and the next cross-sell opportunity.

Mobile-First Banking Preference Scaling Digital Acquisition Costs Below Branch Economics

Mobile banking is now the main consumer touchpoint in many banking systems, and that shift is moving faster than branch restructuring. In the United States, 54% of bank customers named mobile apps as their primary banking method in 2025, marking the 6th straight year that mobile led all channels. On the global demand side, the World Bank reported that 79% of adults now hold a financial account, while 84% of adults in low and middle-income countries own a mobile phone, and 3 billion people have smartphones[2]WORLDBANK.ORG The Global Findex Database 2025. Digital economics are also materially different, with more than USD 2.1 trillion in banking transactions processed through mobile channels in 2025 and a digital cost per transaction of USD 0.04 compared with USD 4.00 for a branch interaction. The 2026 Digital Banking Performance Metrics Report also showed that 51% of loan applications at participating institutions were submitted digitally in 2025 and that digital users generated 1.56 new product relationships per user, further underscoring the value of mobile-led acquisition in the retail banking market.

AI-Personalized Offer Conversion Shifting Revenue Mix Toward Fee Income

AI-led personalization is becoming a revenue tool rather than a back-office experiment. DBS generated SGD 1 billion (USD 740 million) in economic value from AI and analytics initiatives in 2025, up from SGD 750 million (USD 582.52 million) in 2024, based on measured differences in outcomes between AI-led offers and control groups. TD Bank Group launched TD AI Prism in June 2025, and the bank said the model processes 100 times more customer data variables than previous systems for predictive use cases[3]TD.MEDIAROOM.COM TD Announces Launch of Groundbreaking Predictive Foundation Model - Jun 11, 2025. CIBC also pushed this pattern further in 2025 through its CRTeX engine, which improved conversion by 3% and lifted click-through rates by 20% after launch. In the retail banking market, richer transaction data and stronger mobile engagement now create a compounding advantage, as better data enables better offer timing, stronger fee conversion, and a wider gap between large banks, neobanks, and smaller institutions.

Open Banking Data Portability Enabling Third-Party Product Distribution

Open banking is moving from a compliance requirement to a wider product distribution model. In the United Kingdom, the Financial Conduct Authority published FS25/4 in August 2025 and formalized the governance transition under the Data (Use and Access) Act 2025 for the future open banking structure. In Europe, the Financial Data Access regulation was still moving toward final text adoption in late 2025 and is expected to extend portability beyond payment accounts to savings, investments, and insurance. This creates a clear risk for banks that only provide infrastructure, because the customer-facing platform can capture the relationship while the bank retains the lower-margin balance-sheet role. In the retail banking market, banks that use APIs to build their own distribution ecosystems are better positioned to protect customer ownership, as seen in the June 2025 launch of the UPI-linked co-branded credit card by PhonePe and HDFC Bank.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy core modernization burden consuming IT budget and slowing innovation | -1.1% | Global, most acute in North America, Europe, and Japan | Long term (≥ 4 years) |

| Margin compression from deposit rate competition and rate cycle normalization | -0.8% | Global, most acute in India, China, and the United Kingdom | Medium term (2-4 years) |

| Cyber risk compliance escalation increasing operating expenditure | -0.5% | Global, the highest in the EU, the United Kingdom, and the United States | Short term (≤ 2 years) to Medium term (2-4 years) |

| Branch network cost drag slowing operating efficiency improvement | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Core Modernization Burden Throttling Innovation Velocity

Legacy core systems continue to absorb a large share of bank technology budgets and slow product change. Large financial institutions still allocate 70%-85% of IT spending to maintaining older systems, which leaves limited room for new capabilities and digital integration. The problem is becoming harder to manage because older skill pools are shrinking while resilience and data reporting requirements are becoming more demanding. The EU's Digital Operational Resilience Act, effective from December 17, 2024, is increasing pressure on banks to modernize systems designed for batch processing rather than real-time control and third-party oversight[4]PENTAGONINFOSEC.COM DORA Compliance Cost & Timeline: What EU Banks Actually Spend | Pentagon Infosec. In the retail banking market, banks that meet new compliance requirements by layering fixes onto old cores risk locking in higher migration costs later, slowing innovation, and keeping the operating gap wide between digital leaders and late movers.

Margin Compression From Rate Competition Narrowing the Revenue Buffer

Profitability is also being constrained by tighter net interest margins in several banking systems. India's scheduled commercial banks reported a 21 basis-point year-over-year decline in net interest margins to 2.99% in Q4FY25, driven by slower credit growth, higher deposit costs, and a 14.1% increase in term deposits. Indonesian state bank profits fell 4.55% in 2025, while sector net interest margin declined to 4.56% in December 2025 from 4.62% a year earlier. Major Chinese state banks also reported margin compression in 2025, with declines of up to 21 basis points in their annual reports. In the retail banking market, this is becoming a structural issue because incumbents still need to fund digital investments and protect deposits simultaneously, leaving less room to absorb weaker spreads without changing the revenue mix.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Loans Lead Revenue, While Debit Cards Reflect Faster Transaction Growth

Loans accounted for 44.75% of the retail banking market in 2025, making them the largest product group. That position still reflects the central role of consumer credit in retail bank earnings, especially where household borrowing remains deep and diversified. India offers a strong recent example, with the retail loan book recording 16.2% year-over-year credit growth in FY26 and gold loans rising 123% year over year. The scale of that growth shows why lending continues to anchor the revenue mix even as transaction-led products gain more daily engagement. The retail banking market still depends on lending depth to support revenue, balance sheet utilization, and relationship extension into adjacent products.

Debit cards are the fastest-growing product segment, with a forecast CAGR of 7.76% for 2026-2031, suggesting stronger transaction volume rather than a change in credit demand. In Thailand, PromptPay accounted for 44% of online spend and 43% of in-person spend in 2025, demonstrating how debit-linked instant payment rails are changing everyday payment behavior. Transactional accounts and savings accounts still remain important because they support primary account relationships, salary inflows, and funding stability across the retail banking market. Credit cards also remain relevant in higher-income systems, with JPMorgan Chase opening 10.4 million new credit card accounts in 2025 as its card franchise expanded. Other products, including insurance, investments, and merchant services inside banking apps, are growing from a small base and are becoming more important as banks look for fee income beyond traditional spread businesses.

By Channel: Online Banking Leads, While Branch Networks Shift Toward Advisory Use

Online banking accounted for 71.48% of the retail banking market in 2025 and remains the primary channel. Its forecast CAGR of 6.16% for 2026-2031 also shows that digital revenue growth is still outpacing the overall market pace. Digital adoption has moved beyond account access and is now embedded in acquisition, onboarding, servicing, and product expansion. Alkami and Cornerstone Advisors reported that 87% of checking accounts are linked to active digital users and that 82% of mobile users are actively engaged. Those usage levels confirm that digital is no longer a secondary touchpoint for the retail banking market.

Wells Fargo passed 33 million mobile active users in early 2026, and its Fargo assistant reached 1 billion customer interactions in under 3 years, demonstrating how digital engagement is now being scaled across large incumbent banks. Offline banking continues to lose market share in routine transactions, but it is not disappearing from the retail banking market. Bank of America plans to open more than 150 new financial centers across 60 markets by end-2027, including 70 in 2026, indicating that physical networks are being repositioned rather than removed. The physical branch model is becoming more selective, with transactional locations under pressure while premium advisory centers remain valuable in wealth corridors. This leaves the retail banking market with a two-speed branch strategy where digital handles daily banking and physical formats focus on complex needs and higher-value customer relationships.

By Customer Age Group: The 29-44 Cohort Holds Revenue Weight, While 18-28 Drives Faster Expansion

The 29-44 age group captured 35.49% of the retail banking market in 2025, making it the largest customer cohort by revenue contribution. This is the life stage when mortgages, savings balances, cards, insurance, and investment relationships are usually at their widest. That is why this cohort remains central to AI-led cross-sell programs and multi-product relationship strategies in the retail banking market. CIBC's CRTeX launch in 2025 supports that pattern, as the bank reported a 3% improvement in conversions and a 20% increase in click-through rates after deployment. The 29-44 group, therefore, remains the revenue anchor because product intensity is higher and relationships are broader than in younger cohorts.

The 18-28 age group is the fastest-growing segment, with a forecast CAGR of 6.87% through 2031, making it the key acquisition battleground in the retail banking market. Chime reported 10.2 million active members in Q1 2026 and said that more new bank accounts were opened through Chime than through any other single financial institution in the United States, exceeding its closest competitor by more than 50%. Older cohorts, especially 45-59 and 60+, are growing more slowly but still matter because they usually hold higher balances and support the economics of advisory-led physical banking. Younger cohorts are expanding faster, but current revenue per customer remains lower, so present acquisition economics are still difficult for many incumbents. The long-term value of this segment in the retail banking market depends on whether digital-first acquirers can deepen relationships as these customers move into higher-balance and higher-credit years.

By Bank Type: National Banks Retain Scale, While Neobanks Gain Ground in New Accounts

National banks held 67.84% of the retail banking market share in 2025, which reflects their balance sheet depth, capital access, and broad product coverage. Their leadership in the retail banking market also stems from their ability to spread technology spending across very large customer bases while keeping lending, deposits, cards, and payments within the same relationship. JPMorgan Chase's Consumer and Community Banking division reported USD 19.6 billion in Q1 2026 revenue, up 7% year over year, and added 450,000 net new checking accounts in the quarter. That performance shows that large incumbents can still grow organically when digital engagement keeps acquisition efficient. Regional banks remain under more pressure because they sit between the scale of national banks and the agility of digital challengers.

Neobanks are the fastest-growing bank type with a forecast CAGR of 8.20% for 2026-2031, even though they still represent only a small part of total revenue. Revolut reported USD 1.7 billion in net profit in 2025 and added 16 million new retail customers, while Nubank surpassed 135 million global customers by March 2026 and became the third-largest financial institution in Mexico by customer count. The pace of that expansion shows why the retail banking market is seeing stronger pressure in new account acquisition than in current revenue share. Regional bank consolidation is also accelerating, with more than 180 bank M&A deals announced in 2025 for a combined USD 49 billion, compared with USD 16.3 billion in 2024, and Fifth Third completing its USD 10.9 billion acquisition of Comerica in February 2026. The result is a market where scale incumbents still control current revenues, but neobanks are taking a larger share of future customer relationships in the retail banking market

Geography Analysis

North America accounted for 38.02% of the retail banking market in 2025, making it the largest regional market. The United States remains the main anchor, with banks reporting USD 295.6 billion in net income in full-year 2025 and loan balances of USD 13.5 trillion, up 5.9% year over year. The region also benefits from mature credit card ecosystems, large consumer balance sheets, and deep ties between banking and capital markets. Canada is moving through a similar transition, with TD Bank Group targeting USD 2-2.5 billion in cost optimization through digital migration, AI integration, vendor consolidation, and a planned 10% reduction in its North American branch network by end-2026. Mexico is becoming a more active competitive zone, as Revolut launched full banking operations there in January 2026, and Nubank has already crossed 15 million customers in the country.

Europe remains in transition as instant payments, open banking rules, and selective consolidation reshape the regional structure of the retail banking market. France's STET platform reported that instant transfers accounted for 20% of all credit transfers in 2026, underscoring how quickly real-time payments are moving into the mainstream. Germany is attracting new digital competition, with JPMorgan launching Chase digital banking in 2026, using a 4% savings rate offer to build deposits before broadening its products. France is also becoming a major battleground, where Revolut said it had reached 7 million French customers by early 2026, including 2.5 million added in 2025. The United Kingdom is dealing with a different adjustment, as thousands of branch closures coincide with a more formal open banking governance architecture under the Data (Use and Access) Act 2025.

The Middle East and Africa are the fastest-growing regions with a forecast CAGR of 7.95% for 2026-2031, supported by mobile-led inclusion, digital bank licensing, and new digital-native models such as Wio Bank in the UAE and onebank in Egypt. Wio Bank reported AED 1.24 billion (USD 337.7 million) in revenue in 2025, up 55%, demonstrating the scale digital banking can already reach in the region. Asia-Pacific remains the most internally mixed region in the retail banking market because payments growth, credit growth, and margin pressure are moving at different speeds across countries. India continues to scale quickly, with UPI processing 228.5 billion transactions in 2025 and domestic retail credit growing 16.2% in FY26, while HDFC Bank deployed a centralized generative AI platform with more than 15 high-impact pilots in 2025. China's large state banks are working through a margin compression cycle, while Japan's megabanks are responding through digital alliances, such as the May 2026 tie-up between Mizuho Bank and Rakuten Bank.

Competitive Landscape

The retail banking market remains semi-consolidated at the top and widely fragmented below. Large institutions still hold a disproportionate share of deposits, consumer loans, and cards, while a long tail of regional banks, community banks, and digital entrants competes more aggressively for marginal customers and new-account flows. That split is pushing the retail banking market toward two distinct competitive models: one based on scale and technology depth, and another on speed, pricing, and focused digital acquisition. JPMorgan Chase illustrates the scale of its technology investment, with USD 19.8 billion in 2026 and AI solutions in production that doubled year over year. That level of spending is difficult for most smaller banks to match, widening the capability gap in personalization, fraud management, and digital onboarding.

Several large banks are now responding through platform redesign and business reshaping rather than only through product launches. Santander is pursuing a global platform strategy through its ONE Transformation program, targeting EUR 1 billion in AI-related gains by 2028 and deploying its Gravity 2.0 cloud-native core banking platform across 26 markets. HSBC has been moving in the opposite direction by exiting lower-priority retail operations, with 11 retail business exits completed in 2025, including Sri Lanka, Bangladesh, Bahrain, Germany, Uruguay, and France. DBS is also making a distinct technology push, deploying 10,000 personal AI agents in late 2025 and becoming the first Asia-Pacific bank to pilot Visa Intelligent Commerce for agentic retail payments. These examples show that the retail banking market is no longer competing only on branch scale or pricing, because strategic differentiation now depends more on platform design, data use, and portfolio focus.

White space remains in digital niches where product supply is still limited relative to demand. Islamic digital banking is one example, with the UAE's Rouya Islamic Digital Bank launching a Mastercard cashback credit card in April 2026 and Pakistan's Raqami Islamic Digital Bank starting operations in February 2026 on local cloud infrastructure. The retail banking market is therefore opening space not only for large universal banks and mainstream neobanks, but also for digital specialists that target underserved customer groups with clearer product positioning. This keeps competitive pressure broad even when top-tier banks remain dominant in current revenue pools.

Retail Banking Industry Leaders

JPMorgan Chase and Co.

Industrial and Commercial Bank of China Ltd.

Bank of America Corporation

China Construction Bank Corporation

HSBC Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EQB (Equitable Bank, Canada) secured final regulatory approval to acquire PC Financial — the banking subsidiary of President's Choice / Loblaw — and enter a long-term exclusive partnership with the PC Optimum loyalty programme, gaining access to Loblaw's national retail and digital channels for financial product distribution. The deal repositions EQB as a scaled digital-first bank with embedded retail distribution.

- April 2026: BPCE finalised the acquisition of 100% of novobanco for EUR 6.7 billion (USD 7.3 billion), making Portugal its second domestic retail banking market and strengthening its position as the fourth-largest banking group in the Eurozone. The transaction is expected to be immediately earnings-accretive.

- March 2026: Revolut completed the mobilization phase of its United Kingdom banking license, enabling full banking services, including deposit protection under FSCS, for its 13 million British customers. In the same month, Revolut filed a formal application for a national banking license in the United States, targeting a market where it had already accumulated millions of app users without a full banking charter.

- February 2026: Fifth Third Bancorp completed its USD 10.9 billion acquisition of Comerica, creating the 9th-largest United States bank with approximately USD 294 billion in assets. The merger combines Fifth Third's digital retail capabilities with Comerica's middle-market franchise across 26 states, establishing a scaled competitor in the United States regional banking segment.

Global Retail Banking Market Report Scope

| Transactional Accounts |

| Savings Accounts |

| Debit Cards |

| Credit Cards |

| Loans |

| Other Products |

| Online Banking |

| Offline Banking |

| 18-28 Years |

| 29-44 Years |

| 45-59 Years |

| 60 Years and Above |

| National Banks |

| Regional Banks |

| Neobanks and Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Transactional Accounts | |

| Savings Accounts | ||

| Debit Cards | ||

| Credit Cards | ||

| Loans | ||

| Other Products | ||

| By Channel | Online Banking | |

| Offline Banking | ||

| By Customer Age Group | 18-28 Years | |

| 29-44 Years | ||

| 45-59 Years | ||

| 60 Years and Above | ||

| By Bank Type | National Banks | |

| Regional Banks | ||

| Neobanks and Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the retail banking market?

The retail banking market stood at USD 3.56 trillion in 2025 and is expected to reach USD 3.79 trillion in 2026 before rising to USD 5.2 trillion by 2031.

What is driving growth in retail banking through 2031?

Growth is being supported by instant payments, mobile-first banking, digital loan origination, and AI-led personalization that improves product conversion and customer retention.

Which product segment leads revenue in retail banking?

Loans remain the largest product segment with a 44.75% share in 2025, reflecting the continued importance of consumer credit in retail bank earnings.

Which channel dominates customer engagement and revenue generation?

Online banking leads with 71.48% of revenue in 2025, supported by high digital adoption, active mobile usage, and lower servicing costs than branches.

Which customer group is expanding the fastest?

The 18-28 age group is the fastest-growing cohort, with a forecast CAGR of 6.87% through 2031, making it the main acquisition battleground for incumbents and neobanks.

Which region is growing the fastest in retail banking?

Middle East and Africa is the fastest-growing region at a forecast CAGR of 7.95% for 2026-2031, supported by digital bank licensing, mobile money, and demographic growth.

Page last updated on: