Mineral Core Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.31 Billion |

| Market Size (2031) | USD 13.20 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

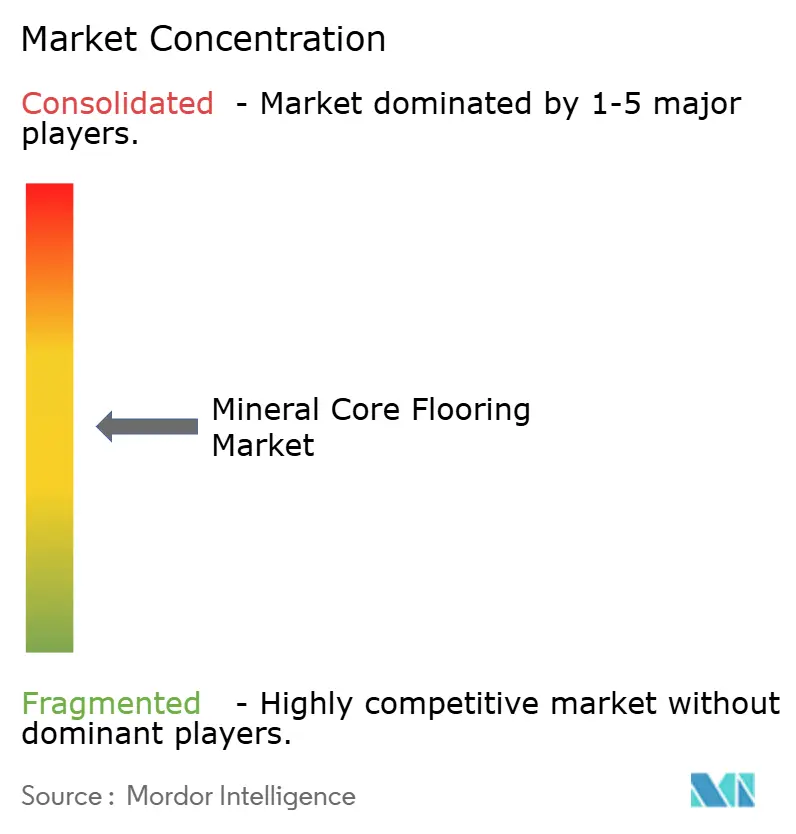

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mineral Core Flooring Market Analysis by Mordor Intelligence

The mineral core flooring market size is projected to expand from USD 8.72 billion in 2025 and USD 9.31 billion in 2026 to USD 13.20 billion by 2031, registering a CAGR of 7.2% between 2026 and 2031. Durable waterproof performance in wet spaces and time-saving installation workflows continue to guide product design and channel strategies in 2026. Competitive positioning emphasizes private-label depth at big-box retailers and fast-turn domestic lines that reduce project risk. Regulatory focus on PVC composition and low-VOC compliance influences specifications and procurement checklists in North America and Europe. Supply chain strategies in 2026 will reflect greater nearshoring and closer alignment with certification frameworks to mitigate quality variance and maintain buyer confidence.

Key Report Takeaways

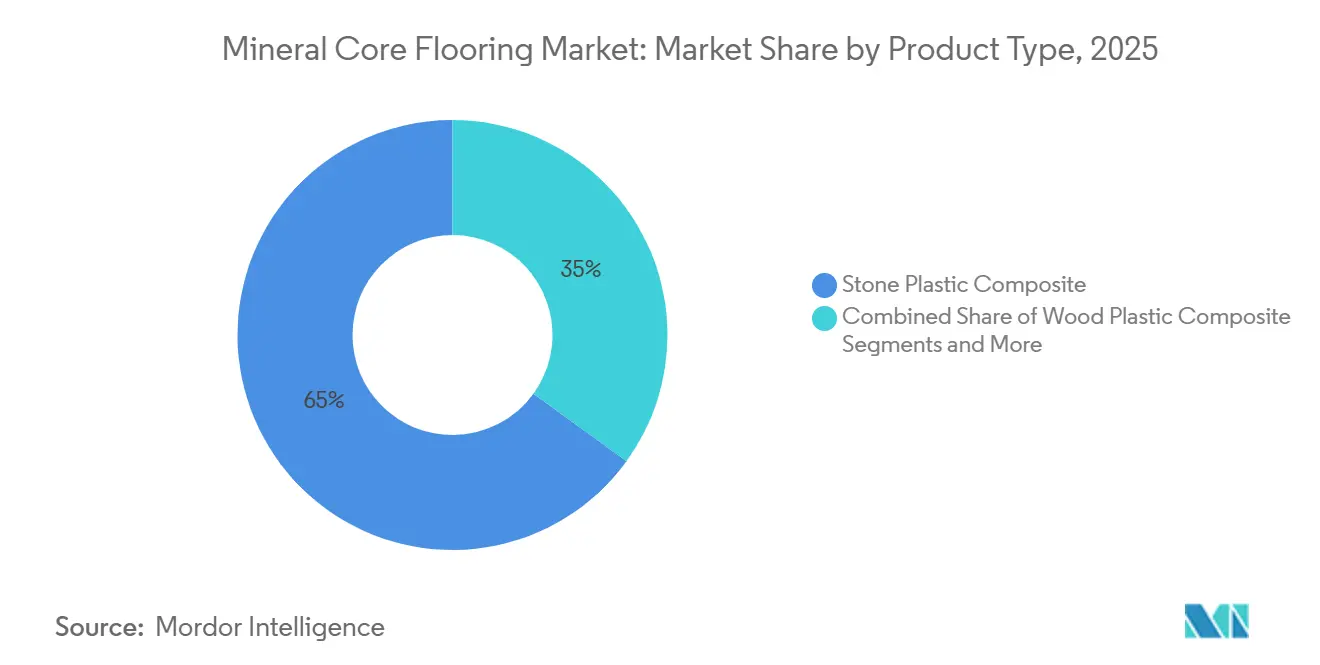

- By product type, stone plastic composite captured 65.0% of the mineral core flooring market share in 2025, while wood plastic composite is projected to grow at 7.67% CAGR between 2026 and 2031.

- By format, planks captured 70.0% of the global mineral core flooring market share in 2025, while tiles are projected to grow at 7.90% CAGR between 2026 and 2031.

- By thickness, 4-6 mm captured 47.34% of the global mineral core flooring market share in 2025, while >8 mm is projected to grow at 8.15% CAGR between 2026-2031.

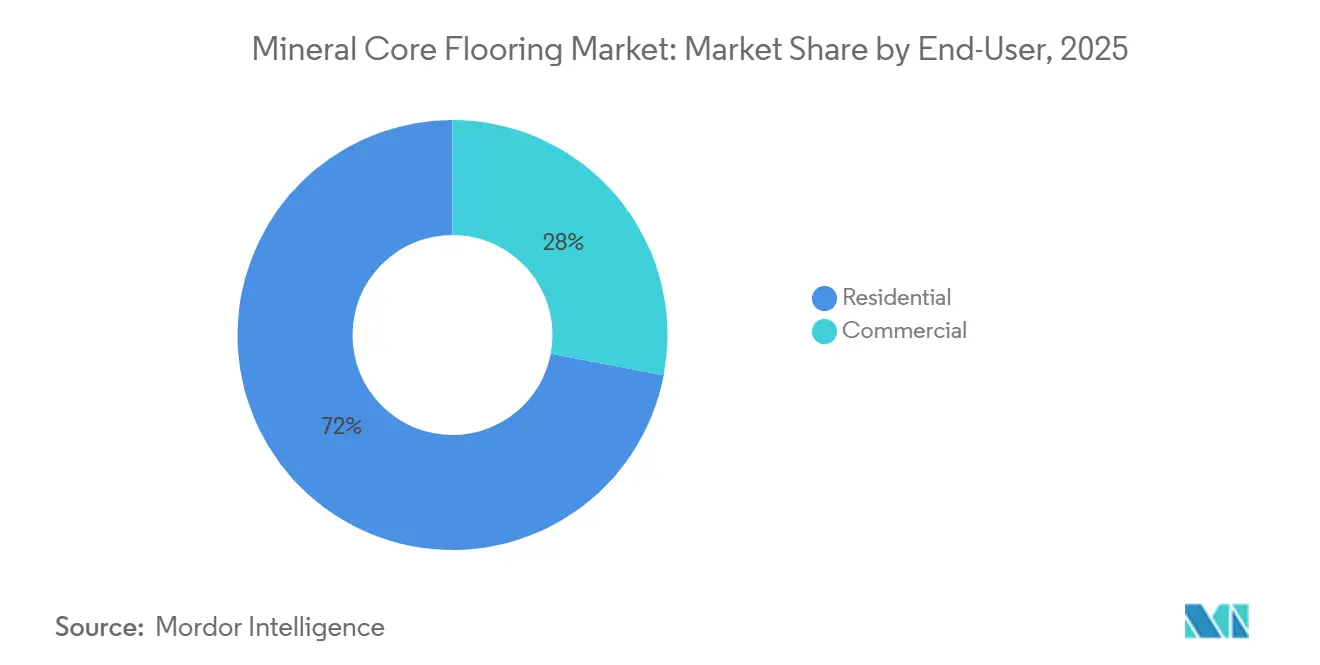

- By end user, residential captured 72.0% of the global mineral core flooring market share in 2025, while commercial is projected to grow at 7.70% CAGR between 2026 and 2031.

- By distribution channel, B2C/Retail captured 75.0% of the global mineral core flooring market share in 2025, while B2B/Contractors/Builders is projected to grow at 7.47% CAGR between 2026 and 2031.

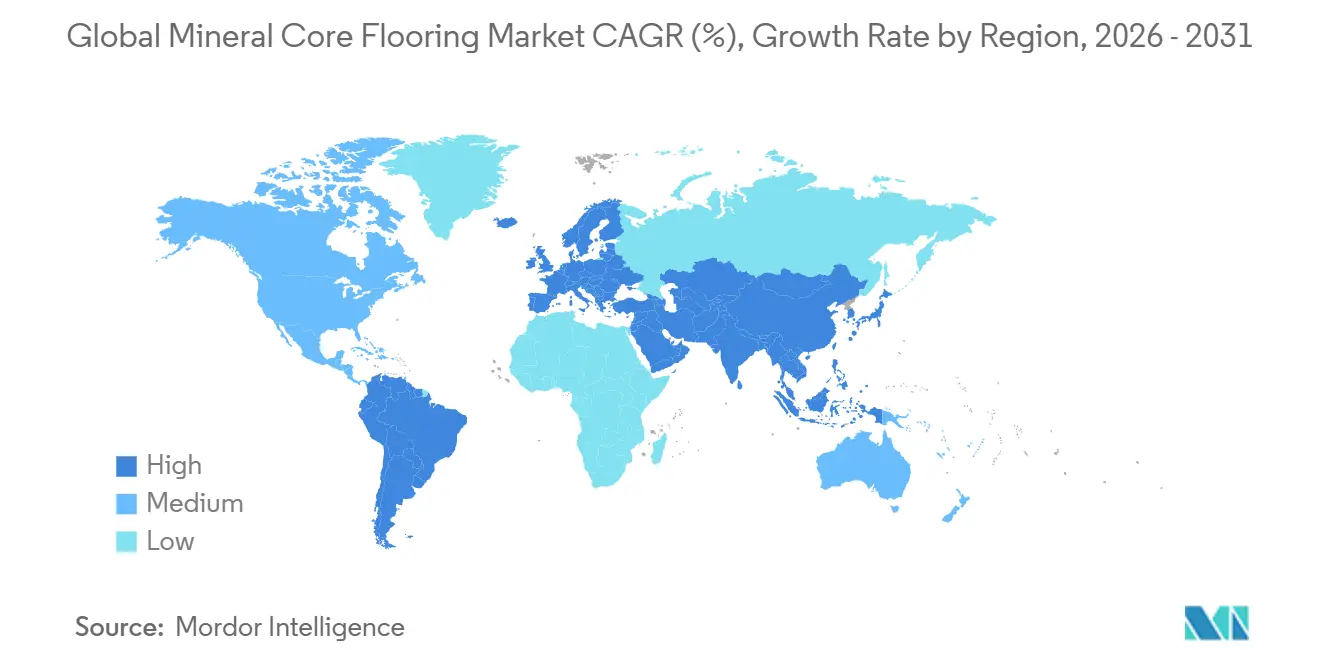

- By geography, North America captured 30.0% of the mineral core flooring market share in 2025, while Asia-Pacific is projected to grow at 8.5% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mineral Core Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Click-lock installation reduces labor cost and enables DIY adoption | +1.4% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Waterproof rigid core captures share from laminate and wood in wet areas | +1.8% | Asia-Pacific core markets, spillover to Middle East & Africa | Medium term (2-4 years) |

| Tolerance to imperfect subfloors accelerates remodeling and replacement cycles | +1.3% | North America and EU, parts of Latin America | Long term (≥ 4 years) |

| Private-label expansion at home centers and specialty retail scales fast SKU rotation | +1.5% | United States and Canada | Short term (≤ 2 years) |

| Nearshoring and domestic SPC capacity cut lead times and supply risk | +1.7% | North America and parts of EMEA | Medium term (2-4 years) |

| Low-VOC, PVC-lite or mineral composite innovations unlock spec-driven demand | +1.5% | Global with strong EU and North America influence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Click-Lock Installation Reduces Labor Cost and Enables DIY Adoption

Click-lock systems enable tool-light installation with fewer trade dependencies, shortening job timelines and reducing direct labor for homeowners and pros alike. Product lines that ship with integrated pads and clear locking instructions enable walk-on use soon after installation, which supports a single-day project turnaround for small rooms. Retailers and private labels position these floating systems as accessible upgrades that do not require adhesives, which simplifies preparation and cleanup. In 2026, merchandising in large home centers continues to highlight waterproof rigid-core options under exclusive brands, which reinforces the do-it-yourself value story. Installer guidelines and brand warranty documents reinforce substrate and acclimation requirements for click systems, helping reduce callbacks and extend product life in residential and light commercial environments[1]Floor & Decor, “NuCore Performance Warranty and Installation Instructions,” Floor & Decor, flooranddecor.com.

Waterproof Rigid Core Captures Share from Laminate and Wood in Wet Areas

Fully waterproof rigid-core constructions remain preferred in kitchens, baths, and basements where moisture exposure is frequent, and where warranties explicitly address spills and damp conditions. Contractor workflows benefit from floating installation over clean, dry substrates, which eliminates adhesive dry time from the project plan in many cases. Procurement teams in hospitality, education, and healthcare also favor resilient rigid-core, where downtime must be minimized while maintaining resistance to foot traffic and repeated cleaning. Retail planograms in 2026 continue to expand waterproof rigid-core facings under exclusive labels, which steer shoppers away from entry-grade laminates in high-moisture zones[2]The Home Depot Investor Relations, “Annual Report 2024,” The Home Depot, ir.homedepot.com. This pull-through effect remains visible in North America and several European markets where certification-aware buyers demand listed products for public or semi-public projects.

Tolerance to Imperfect Subfloors Accelerates Remodeling and Replacement Cycles

Rigid-core platforms are engineered to float over many existing surfaces within defined flatness tolerances, which limits subfloor preparation steps on remodel jobs. Clear installation guidance for tile-over-tile and concrete substrates reduces scope creep and supports faster scheduling for Main Street commercial and residential turns. Market demand focuses on formats that bridge minor surface variations without telegraphing, helping contractors complete more square footage per day. Specification teams weigh substrate tolerance alongside indoor-air criteria such as FloorScore or GREENGUARD Gold, which encourages the use of tested floating assemblies in occupied facilities. The net effect is steady adoption in retrofit segments where leveling budgets are constrained and where speed-to-completion matters for revenue continuity[3]Resilient Floor Covering Institute, “ASSURE Certified Rigid Core Flooring,” RFCI, rfci.com.

Private-Label Expansion at Home Centers/Specialty Retail Scales Fast SKU Rotation

Exclusive-label assortments at big-box retailers are expanding in 2026, increasing control over merchandising, pricing, and replenishment cadence for rigid-core categories. Proprietary programs pair rapid style refreshes with certification requirements that prequalify products for many projects, simplifying consumer choice and store associate training. Specialty chains that operate warehouse footprints emphasize broad visual libraries and job-lot availability to capture project-driven demand[4]IR.FLOORANDDECOR.COM 10-K - 02/19/2026 - *IR Theme - Data Rays. These private-label strategies also support value positioning during periods of cost volatility, as retailers can adjust specifications and sourcing within exclusive brands. In 2026, the private-label channel continues to set expectations for waterproof, easy-to-install rigid-core options across the United States retail.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC regulatory pressure and end-of-life recycling challenges | -1.2% | European Union and North America | Long term (≥ 4 years) |

| Quality variance and counterfeit or low-spec imports erode buyer confidence | -1.6% | North America and global trade corridors | Short term (≤ 2 years) |

| Trade or tariff exposure and AD or CVD risks drive pricing volatility | -1.8% | United States, European Union, select export hubs | Medium term (2-4 years) |

| China overcapacity commoditizes SPC and compresses margins | -1.4% | Global supply markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PVC Regulatory Pressure and End-of-Life Recycling Challenges

EU restrictions on lead in PVC and similar substance controls require strict feedstock management and documentation throughout the flooring value chain. These rules place pressure on recycled streams when legacy additives remain present, limiting recycled-content options for rigid-core lines without advanced separation or dissolution technologies. Corporate recycling programs and take-back systems have matured, yet scaling circular feedstock remains complex due to collection logistics and quality assurance constraints. In North America, third-party certifications for indoor-air performance and ingredient health shape procurement policies for public buildings and schools, which guide product formulations and supply documentation. The combined effect is additional costs and process oversight for producers, alongside specification advantages for certified lines that meet strict criteria.

Quality Variance and Counterfeit or Low-Spec Imports Erode Buyer Confidence

Enforcement activity has identified counterfeit products bearing unauthorized certification marks, which raises compliance and liability concerns for importers and retailers. The presence of mislabeled or substandard goods can damage category trust and increase claims for retailers that stock low-spec ranges. Buyers respond by giving preference to audited programs and well-documented supply chains that verify compliance with heavy metal thresholds and phthalate limits. Large retailers and brand owners are tightening vendor qualification, reducing the risk of post-installation failures caused by weaker cores or deficient locking systems. The improvement cycle continues in 2026 as certifications and warranties become entry criteria for shelf placement and bid lists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stone Plastic Composite Anchors the Category, While Wood Plastic Composite Gains on Comfort and Acoustics

Stone plastic composite led with 65.0% in 2025 within the global mineral core flooring market, and Wood Plastic Composite is the fastest-growing product category with a 7.67% CAGR over 2026–2031. The global mineral core flooring market favors SPC for its dent resistance and strong dimensional stability in moisture-prone rooms, making it the default choice for kitchens and bathrooms. Product development in WPC highlights a warmer underfoot feel and acoustic damping, broadening its use in multi-family and premium residential applications. Retailers and project owners weigh logistics and installation ergonomic factors, and many WPC lines continue to gain share where installer fatigue and elevator constraints matter. Innovation pipelines also show increased attention to material health and indoor air, which supports specification in healthcare, education, and government buildings.

SPC maintains a stronger presence in projects that expect heavy use, wet cleaning, and tolerance to minor substrate variance. At the same time, WPC expansion reflects end-user comfort priorities and acoustic requirements for upstairs living or multi-tenant structures. The global mineral core flooring market sees both platforms improve locking precision and surface wear layers, which stabilizes performance across price tiers. Manufacturers highlight third-party verification to address quality concerns and to meet bid prerequisites on public developments. At the same time, brand strategies diversify visuals and textures to emulate better wood and stone formats that guide retail selection. In this product view, procurement teams match each construction to room usage and noise criteria to extend the installed lifecycle. The mineral core flooring industry also benefits from clearer installation guidance and expanded warranty language that reflect modern use cases in residential and Main Street commercial settings.

By Format: Planks Dominate for Speed and Wood Looks, While Tiles Advance on Pre-Grouted Systems

Planks accounted for 70.0% of the 2025 format share in the global mineral core flooring market size, while tile formats are on track to expand at a 7.90% CAGR through 2031. Planks remain the leading choice for residential replacements due to their installation speed and wood-look visuals that align with consumer preferences. Merchandising in 2026 continues to give plank formats the broadest in-store exposure, which reinforces consumer familiarity. Tile formats, including pre-grouted SPC, are gaining momentum where ceramic aesthetics are desired and faster project completion is desired. Floating assembly over prepared surfaces reduces downtime and supports tight retail and hospitality schedule windows.

Tile adoption is growing in commercial retrofit projects, where weight limits, subfloor conditions, or acoustic targets make rigid-core tiles more attractive than ceramic tiles. The global mineral core flooring market reflects this shift by showcasing slip and fire performance data to meet code requirements alongside indoor-air credentials. Producers also expand herringbone and larger-format visuals, simplifying complex layouts through updated locking systems. Category leaders work with distribution partners to stock critical square footage locally, which helps contractors stage rooms across phased projects. The result is an expanding role for tile in spaces that historically defaulted to ceramic, without increasing load or extending cure time.

By Thickness: Mid-Range Leads Value Projects, While >8 mm Builds Premium Positioning

The 4-6 mm thickness range accounted for 47.34% of the 2025 volume in the global mineral core flooring market, supported by cost-effective builder and remodel jobs. Thicker products above 8 mm are expected to post the fastest growth at a 8.15% CAGR from 2026 to 2031, reflecting demand for comfort underfoot and enhanced acoustics in higher-end residential and multi-family applications. Product lines in the 4–6 mm bracket maintain a strong presence with efficient floating installs and adequate wear protection for most residential needs. Thicker constructions add integrated pads and more robust surface layers, which help address noise transfer and perception of solidity. Vendors align these offers with premium rooms or multi-unit noise codes to support upgrade paths at retail.

Choices in the 6-8 mm bracket serve as a bridge for projects that need modest acoustic improvement without the full premium step. The global mineral core flooring market balances this middle tier with focused SKUs to avoid overlap and to maintain clarity at the point of sale. Retailers and brands emphasize that wear-layer selection and certification status are central to durability and building compliance. Procurement teams often standardize on two bands, a value 4-6 mm set and a premium >8 mm set, to streamline tender packages. Where elevator access or installer ergonomics come into play, denser or thicker boards are matched to worksite realities to sustain productivity and finished quality.

By End User: Residential Remains the Volume Base, While Commercial Gains on Retrofit Needs

Residential accounted for 72.0% of the 2025 volume in the global mineral core flooring market, with kitchens and bathrooms continuing to lead waterproof installations. Commercial end uses are poised for faster growth at 7.70% CAGR through 2031, supported by maintenance savings and strict indoor-air requirements for public spaces. Main Street commercial sees momentum driven by quick-turn installation methods and product resilience under rolling loads and frequent cleaning. Hospitality corridors, retail aisles, and select healthcare zones adopt rigid-core to balance look, cleanability, and downtime. Procurements reflect a tilt toward listings that carry verifications for air quality and restricted substances.

In residential channels, premium lines expand where thicker constructions and upgraded visuals drive step-up purchases. The global mineral core flooring market also intersects with small-office and mixed-use remodels that require commercial performance in residential layouts. Multi-family renovators deploy commercial-grade rigid-core at residential price points to achieve fast turns. Certification-backed inventories allow public bidders to pass prequalification without extended testing, thereby shortening the cycle time for funded projects. That dynamic sustains a balanced growth profile, with residential remaining the foundation and commercial demand gradually increasing its share.

By Distribution Channel: B2C/Retail Holds Share Leadership, While B2B/Contractors Expand on Project Velocity

B2C/Retail held 75.0% of the 2025 value in the global mineral core flooring market, with home centers and large specialty chains maintaining heavy traffic and on-hand inventory. The B2B/Contractors/Builders channel is forecast to grow at a 7.47% CAGR through 2031, supported by domestic capacity that enables reliable lead times for volume orders. Exclusive brands at big-box retailers remain central to consumer choice in 2026, due to curated assortments and visible certification marks that aid decision-making. B2B programs strengthen through job-site delivery services, quick-ship menus, and credit terms that match contractor cash cycles. Supplier relationships evolve to prioritize predictable restock for active developments.

Specialty chains operate hybrid models with B2C showrooms and B2B desks to capture both homeowner upgrades and pro refits. The global mineral core flooring market benefits from this blended approach that maximizes store throughput and leverages local warehousing. Distributors adjust inventory toward pre-qualified rigid-core lines that satisfy bidding documents and municipal mandates. In 2026, contractors and builders source more domestically for time-sensitive projects, while retailers emphasize omnichannel convenience for DIY and small contractor segments.

Geography Analysis

North America accounted for 30.0% of the global market value in 2025, supported by private-label expansion and additional domestic capacity announced for resilient categories. The United States accounts for the majority of regional demand, and sourcing strategies favor a blend of nearshored and domestic lines that stabilize lead times. Certification requirements for schools and healthcare facilities shape assortments and bidder prequalification processes. Canada and Mexico round out the region, with activity aligned with local retail strategies and targeted commercial projects. Large chains continue to consolidate volume behind exclusive programs and consistent stocking positions.

Asia-Pacific is the fastest-growing region, with a 8.5% CAGR over 2026–2031 in the global mineral core flooring market, driven by rising urban demand and continued export capacity. Buyers weigh regional policy and certification landscapes as they plan cross-border supply models for North America and Europe. Exporters prioritize documentation that supports compliance with low-VOC and restricted substances requirements to satisfy destination-market checks. APAC producers are increasing attention to thicker construction and premium finishes as customers request better acoustics and robust locking systems.

Europe balances consumption with ongoing policy evolution that impacts PVC content, labeling, and environmental declarations in the flooring category. Procurement for government and healthcare projects maintains rigorous indoor-air and substance rules, which support certified rigid-core offerings. Nearshoring options expand to improve service levels, while imports remain important for the breadth of range. Europe also features targeted trade measures that influence sourcing decisions in related flooring categories and signal a more protective stance. In this context, specification teams focus on compliance, lifecycle cost, and fast installation to meet refurbishment timetables.

Competitive Landscape

The mineral core flooring market remains moderately concentrated in 2026, with leading suppliers combining design, certification, and nearshored capacity to serve major retailers and commercial bidders. Top players strengthen positions through capital programs that expand resilient output and through portfolio moves that emphasize durable click systems and enhanced wear performance. Product differentiation includes broader visuals, upgraded acoustic pads, and low-VOC positioning aligned to common specification frameworks. Vendor qualification processes increasingly require third-party validations to verify compliance with heavy metal thresholds and phthalate limits for rigid-core lines.

Strategic moves in 2026 highlight alignment between sustainability roadmaps and resilient product development. Sustainability statements and circular programs from integrated flooring manufacturers guide the use of recycled streams and bio-attributed inputs where feasible under current rules. Partnerships in circular chemistry and plasticizers continue to feature in announcements by premium resilient suppliers with multi-region manufacturing footprints. These investments enable specification wins in healthcare, education, and government segments that demand documented environmental performance.

On the channel front, private-label strength at home centers and specialty chains shapes assortments and category pricing. This model emphasizes fast rotation, visible certification badges, and reliable restock that support project execution. Nearshoring continues to rebalance portfolios as suppliers seek to maintain service continuity during policy shifts. In 2026, companies with verified quality systems and domestic or regional backup capacity hold advantages in both retail and specification-driven sales.

Mineral Core Flooring Industry Leaders

CFL Flooring

Mohawk Industries

Taizhou Huali New Materials Co., Ltd

Novalis Innovative Flooring

NOX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: J2 Flooring introduced the Strata Collection, an 8 mm SPC with click installation and integrated underlay, described as waterproof and designed for greater subfloor tolerance in commercial and residential settings, with a lifetime wear guarantee.

- February 2026: Forbo Flooring Systems released Sphera Elite b+ homogeneous vinyl flooring incorporating biocircular PVC (43% recycled content, plant-based oils), achieving >50% lower embodied carbon (A1–A3) than standard homogeneous vinyl, per an independently verified EPD, and targeting healthcare and education specifications in Europe.

Global Mineral Core Flooring Market Report Scope

| Stone Plastic Composite |

| Wood Plastic Composite |

| Other Product Types |

| Plank |

| Tile |

| Sheet |

| ≤4 mm |

| 4–6 mm |

| 6–8 mm |

| Above 8 mm |

| Residential | |

| Commercial | Offices |

| Retail | |

| Hospitality | |

| Healthcare | |

| Education | |

| Other Commercial End Users |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East & Africa |

| By Product Type | Stone Plastic Composite | |

| Wood Plastic Composite | ||

| Other Product Types | ||

| By Format | Plank | |

| Tile | ||

| Sheet | ||

| By Thickness | ≤4 mm | |

| 4–6 mm | ||

| 6–8 mm | ||

| Above 8 mm | ||

| By End User | Residential | |

| Commercial | Offices | |

| Retail | ||

| Hospitality | ||

| Healthcare | ||

| Education | ||

| Other Commercial End Users | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the global mineral core flooring market size and growth outlook through 2031?

The global mineral core flooring market size is USD 9.31 billion in 2026 and is projected to reach USD 13.20 billion by 2031 at a 7.2% CAGR.

Which product type leads demand in mineral core flooring?

Stone Plastic Composite leads with 65.0% share in 2025, while Wood Plastic Composite records the fastest growth at 7.67% CAGR to 2031.

Which formats are gaining the most traction in mineral core flooring?

Planks hold 70.0% of 2025 format share, while tiles show faster growth due to pre-grouted systems and retrofit demand at 7.90% CAGR.

Which regions are most important for mineral core flooring in 2026?

North America holds the largest 2025 share at 30.0%, and Asia-Pacific is the fastest growing region at 8.5% CAGR through 2031.

How are retailers influencing mineral core flooring adoption?

Exclusive private-label programs at big-box retailers drive assortment, certification visibility, and availability for DIY and small contractor projects.

What certifications matter most in mineral core flooring specifications?

FloorScore and ASSURE-certified products are commonly required for projects targeting LEED or WELL, which shortens bid timelines and reduces risk.

Page last updated on: