Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 52.17 Billion |

| Market Size (2031) | USD 64.84 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

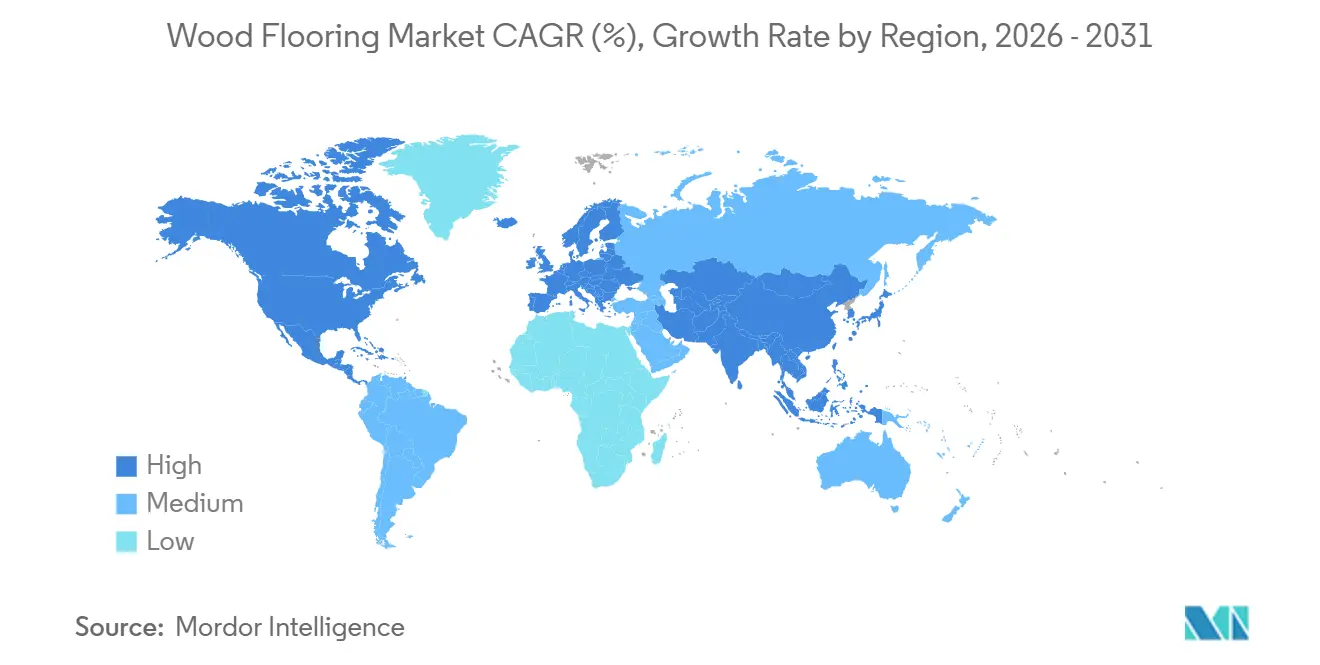

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

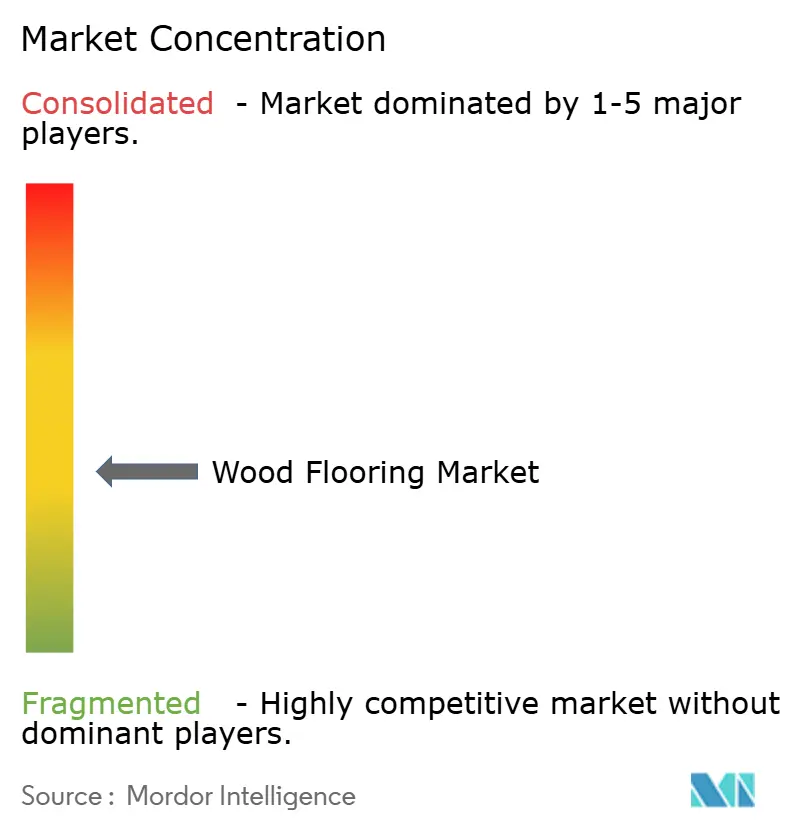

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Flooring Market Analysis by Mordor Intelligence

The wood flooring market size was valued at USD 49.95 billion in 2025 and is estimated to grow from USD 52.17 billion in 2026 to reach USD 64.84 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). This growth profile aligns with sustained renovation cycles and the preference for natural interiors in homes and workplaces, even while financing conditions limit near-term new construction. Adoption of pre-finished and engineered products that streamline jobsite timelines supports replacement demand in residential and commercial settings. Compliance-driven substitution toward ultra-low emission engineered planks continues to underpin mix upgrades in the wood flooring market. The sector remains a meaningful employer in the United States, with an estimated 45,000 jobs and a USD 4 billion contribution to GDP, reinforcing its role in regionally distributed manufacturing.

Key Report Takeaways

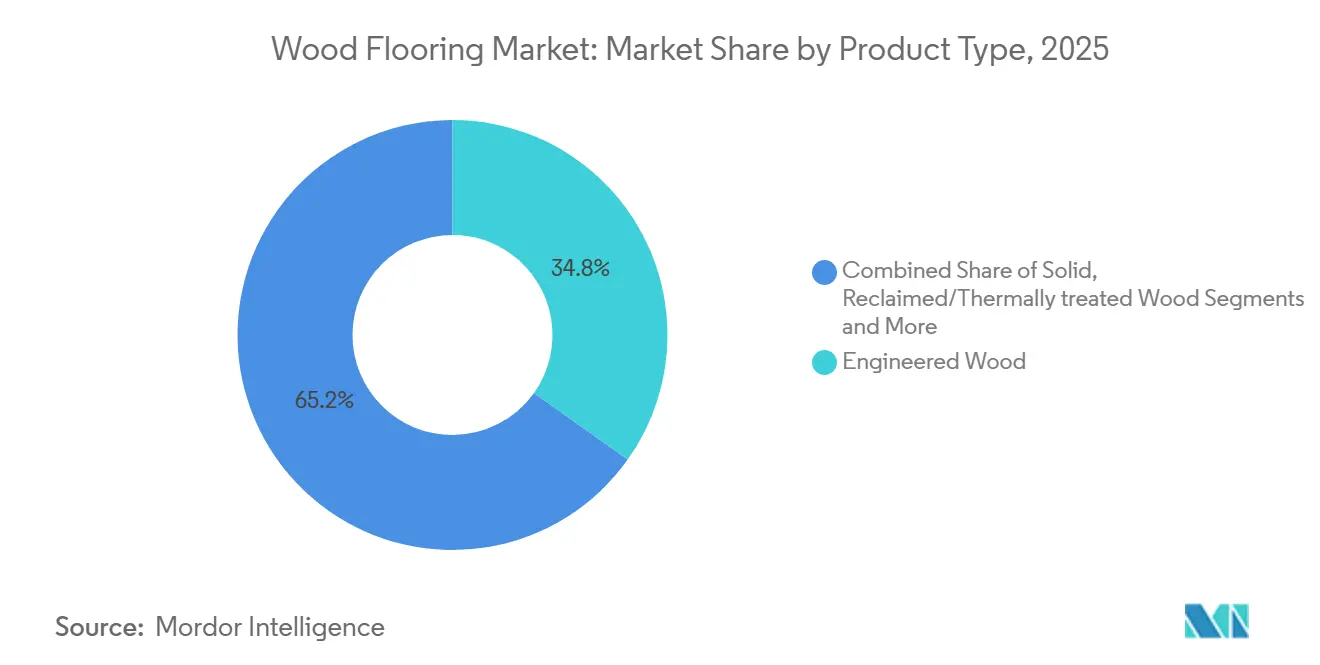

- By product type, engineered wood accounted for 34.84% of the wood flooring market share in 2025; reclaimed and thermally treated wood are projected to expand at a 5.27% CAGR through 2031.

- By installation method, nail-down commanded 43.38% of the wood flooring market share in 2025, while floating and click lock methods are projected to record the fastest 5.18% CAGR through 2031.

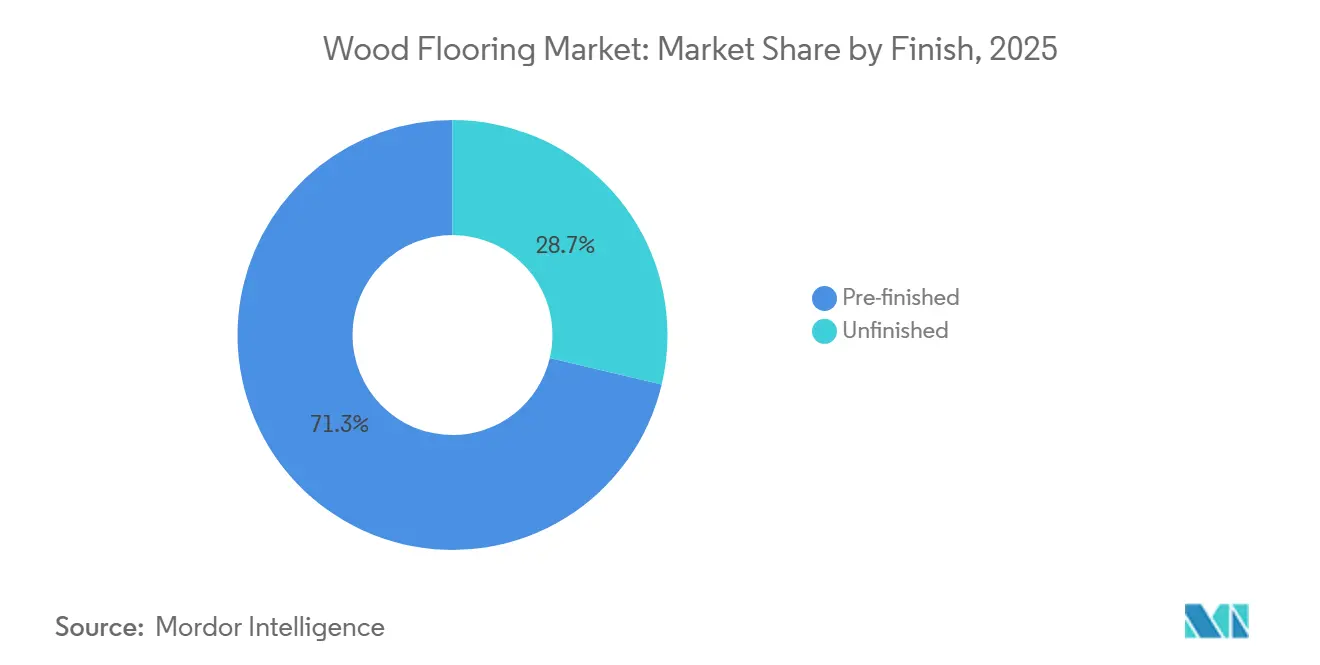

- By finish type, pre-finished accounted for 71.27% of the wood flooring market in 2025 and is forecast to grow at a 4.68% CAGR through 2031.

- By distribution channel, B2C retail consumers represented 67.35% of the wood flooring market share in 2025, while B2B is projected to expand at a 4.82% CAGR through 2031.

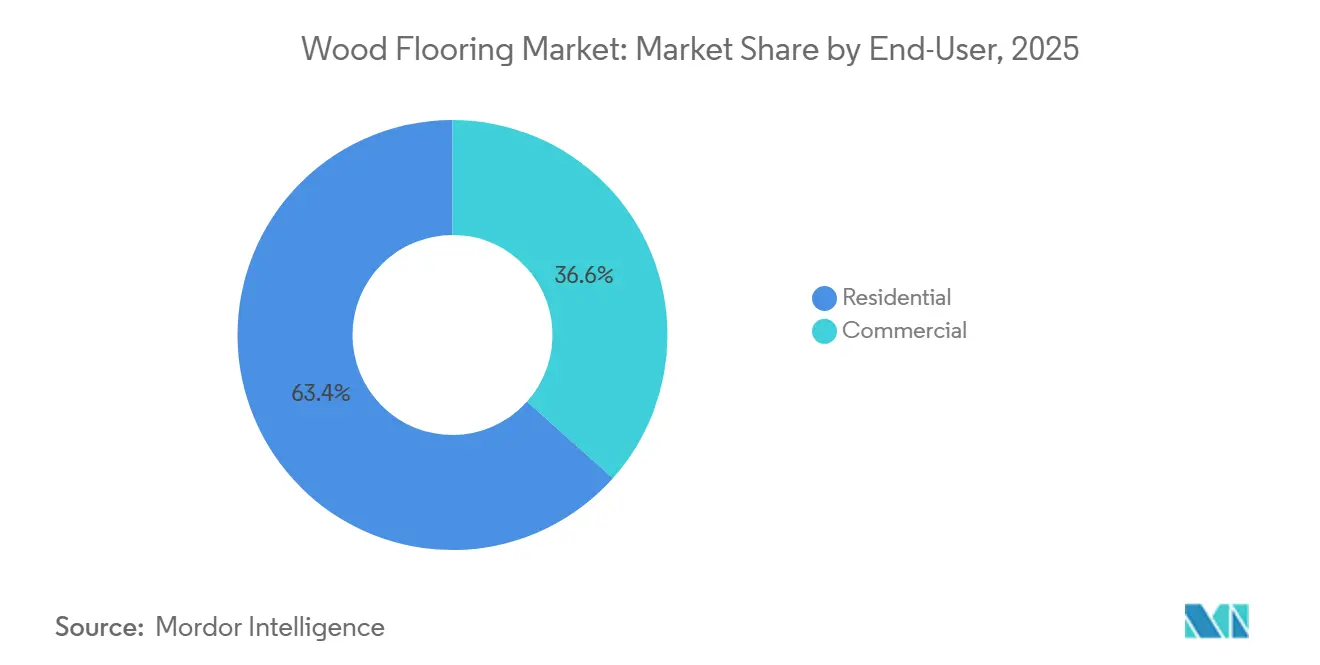

- By end user, residential represented 63.35% of the wood flooring market share in 2025, while commercial is projected to grow at a 5.10% CAGR through 2031.

- By geography, North America captured 31.38% of the wood flooring market share in 2025, and the Asia-Pacific is projected to post the highest 5.48% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in FSC-certified engineered planks | +0.7% | Global, led by North America and the EU | Medium term (2-4 years) |

| Urban premium apartment boom worldwide | +1.0% | Asia‑Pacific core, secondary gains in Latin America metros | Short term (≤ 2 years) |

| Renovation wave subsidies for thermally treated oak | +0.4% | EU and North America, spill‑over to Australia | Medium term (2-4 years) |

| Luxury biophilic interiors demand wide‑plank solids | +0.9% | Global, concentrated in high-income urban centers | Long term (≥ 4 years) |

| E-commerce AR/VR visualizers boost DIY online sales | +0.6% | North America and EU early adopters, expanding to APAC | Short term (≤ 2 years) |

| Mass‑timber office projects specify matching floors | +0.5% | North America and the EU, early gains in the Pacific Northwest and Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Forest Stewardship Council (FSC) Certified Engineered Planks

FSC certification has become a supply chain gatekeeper for engineered wood used in institutional and multifamily projects where submittals require chain of custody documentation. The National Wood Flooring Association’s Verified program, which audits air quality, material composition, and labor practices, pairs with FSC in bid specifications to streamline compliance reviews on public and private projects. Emission compliance is a central enabler since the Environmental Protection Agency's (EPA) Toxic Substances Control Act (TSCA) Title VI caps formaldehyde at 0.05 ppm for hardwood plywood veneer core, which manufacturers address with factory-controlled adhesives and cores that fit “TSCA-compliant engineered” positioning. Buyers in Europe frequently require FloorScore certification that evaluates 35 VOCs (Volatile Organic Compounds) and qualifies products for programs such as LEED v4.1 and WELL. Factory-finished engineered planks gained share in 2025 because pre-finished systems help compress job timelines while avoiding on-site finishing emissions in occupied buildings. Asian exporters leveraging plantation grown poplar in core veneers have historically delivered low landed costs, with 2025 reciprocal tariffs narrowing prior import cost advantages disclosed by major North American manufacturers.

Urban Premium Apartment Boom Worldwide

Urban luxury towers in Bengaluru, Jakarta, and Mexico City are specifying hardwood or engineered wood in living areas to differentiate units as developers target premium leasing and sales outcomes. Japan’s imports of assembled wooden flooring (HS 441871–79) in November 2024 rose just over 30 % month‑on‑month and about 25 % year‑on‑year, with China and Vietnam together supplying the majority of HS 441875 shipments to meet demand in urban condominium retrofits, as reported in trade data compiled from the Japan Lumber Reports and market sources in early 2025 [1]Japan Timber and Wood Products Market Price Reports | 01 – 15th Feb,2025. Southeast Asian developers tend to prefer engineered planks over solid hardwood to mitigate movement risks in humid climates, while floating systems over concrete help manage moisture. Regional design briefs prioritize natural textures and light tones, which favor wide board engineered oak and hickory. The wood flooring market continues to benefit from specification-led projects where high-rise construction seeks premium finishes for common areas and units. Despite persistent weakness in China’s residential starts through 2024, rising premium apartment activity in India and Southeast Asia offsets part of the softness in regional demand.

Renovation Wave Subsidies for Thermally Treated Oak

Public programs that fund home improvements are catalyzing retrofit activity where subfloor and moisture remediation lead to new wood flooring installs. New York’s Targeted Home Improvement Program assisted 1,214 homeowners in 2025, and the scope of work often included repairs that prepared homes for new wood floors[2]NY HCR https://hcr.ny.gov/T-HIP. Thermally treated oak appeals in coastal and humid markets because heat treatment above 200°C reduces hygroscopicity and increases stability demanded by retrofit buyers. Oak’s prominence in European parquet remained clear in 2024 as the species reached 83.8% of total parquet production, with thermally treated variants gaining adoption in Scandinavia and the Baltics. Retail feedback in 2025 showed relative softening for antique and reclaimed items, which suggests some buyers are trading toward thermally modified options that deliver stable performance with a contemporary aesthetic. This dynamic provides a niche but steady demand pulse for thermally treated options within the wood flooring market.

E Commerce AR/VR Visualizers Boost DIY Online Sales

Retailer investments in visualization tools are helping do-it-yourself buyers make faster decisions online, improving conversion for stock-engineered products. As of Q4 2024, 58% of independent flooring retailers planned web and e-commerce investments within 12 months, signaling continued digital channel expansion that feeds into the wood flooring market. Visualizers that overlay species, tones, and plank sizes on room photos reduce hesitancy and shorten decision cycles from weeks to days for typical homeowners. Floating and click-lock engineered planks dominate online listings because National Wood Flooring Association (NWFA) guidelines permit these systems to be installed without specialized tools when subfloors meet flatness tolerances. Distribution members within the National Association of Floor Covering Distributors report technology upgrades in warehouse management and CRM (Customer Relationship Management) that compress order-to-delivery timelines to as little as 48 hours. The combined effect allows homeowners to design, order, and receive materials faster, which sustains the renovation throughput that supports the wood flooring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of raw materials and installation | -0.8% | Global, acute in high‑labor‑cost markets (North America, EU, Australia) | Short term (≤ 2 years) |

| Environmental and Deforestation Concerns | -0.5% | Global, strongest in Europe and North America due to stringent forestry regulations, sustainability certifications (FSC/PEFC), and rising consumer preference for eco-friendly alternatives | Medium to long term (3–5+ years) |

| Susceptibility to Moisture and Climate Conditions | -0.4% | High impact in humid and extreme-climate regions (Asia-Pacific, South America, Africa, coastal markets); moderate impact in temperate regions | Short to medium term (1–4 years) |

| Strong competition from alternatives | -0.6% | Global, most pronounced in price-sensitive residential segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Raw Materials and Installation

Production costs are sensitive to hardwood lumber availability and mill throughput, which influences margins for both solid and engineered lines. United States hardwood lumber production decreased 29% between 2022 and 2024, a contraction linked to a 10% workforce decline of about 40,000 jobs and a related reduction in export value. Manufacturers have responded with vertical integration to secure supply, including sawmill acquisitions that mitigate stumpage price volatility and stabilize inputs for wood flooring lines. On the jobsite, wide plank solid installations often require glue-assisted nail-down methods for stability, adding labor time relative to floating click-lock engineered systems. Subfloor flatness tolerances set by NWFA increase preparation requirements in older buildings, which can add steps before installation begins. These conditions create near-term cost headwinds for some projects in the wood flooring market, especially in high labor cost regions.

Strong Competition from Alternatives

Competing categories continue to pressure real wood. In 2025, two-thirds of National Wood Flooring Association respondents reported that wood look luxury vinyl tile, waterproof polymer core, and laminate products are eroding real wood sales[3]Floor Trends https://www.floortrendsmag.com/articles/113164-shaw-industries-evp-on-consumer-buying-trends-regional-markets-and-2025-flooring-industry-outlook. Laminate shipments tracked by the European Producers of Laminate Flooring reached 313.5 million square meters in 2024, with North America up 8.85% and Western Europe and Eastern Europe down year over year. Alternative hard surfaces promote scratch and water resistance, along with ease of installation, which appeals to price-sensitive households during tighter credit cycles. Healthcare and education projects often specify resilient products in clinical and high-traffic zones, which narrows the addressable footprint for wood in parts of commercial work. Category investments by major resilient producers have also tightened lead times through near-shoring and capacity additions, which keep alternatives prominent in project specifications. As the wood flooring market adapts, manufacturers are emphasizing verified low emissions, enhanced durability, and faster installation formats to compete for share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engineered Wood Captures Mid Market Retrofits

Engineered wood flooring held 34.84% in 2025, driven by grade-level and below-grade suitability, expanding the wood flooring market’s addressable space in multifamily and urban retrofits. Reclaimed and thermally treated wood are projected to expand at a 5.27% CAGR through 2031, setting the pace among niche categories as specifiers balance stability, sustainability, and aesthetic goals. EPA TSCA Title VI formaldehyde caps, and aligned laminated product provisions that took effect in 2024, allow engineered wood producers to design compliant cores and adhesives under controlled factory conditions. The wood flooring market benefits as pre-finished engineered planks eliminate on-site finishing emissions and shorten tenant disruption windows in occupied buildings. Solid wood maintains loyalty in custom builds and restorations where quarter-sawn or rift-sawn cuts meet historical fidelity and performance criteria.

Thermally modified hardwoods appeal to retrofit buyers in humid climates where stability justifies a premium over standard kiln-dried oak, and the wood flooring market reflects this preference in coastal demand patterns. European parquet production contracted in 2024 to 51.5 million square meters, with oak at 83.8% of species used and multi-layer formats dominant, highlighting engineered wood’s structural role in the region. NWFA member ordering patterns in 2025 show white oak as the most specified domestic species, with a tilt toward light, natural tones that minimize glare and support biophilic design programs. In export flows, Asian manufacturers’ popular core engineered planks have historically offered low landed costs, though reciprocal tariffs disclosed by large United States suppliers in 2025 have narrowed import cost advantages. Within this context, engineered formats continue to anchor the wood flooring market where compliance, speed, and stability dictate specification.

By Installation Method: Floating Systems Unlock DIY Growth

Nail-down led legacy formats with a 43.38% share in 2025, reflecting continued use in new construction single-family homes and retrofit projects over wood subfloors. Floating and click lock systems are projected to grow the fastest at a 5.18% CAGR through 2031 as DIY adoption rises and as below-grade concrete applications require non-penetrating methods. NWFA guidance specifies flatness tolerances and expansion gaps for floating assemblies, which enable homeowners and pros to deliver predictable results with fewer specialized tools. Glue-down remains an important method for commercial spaces and for engineered planks over concrete, where moisture testing and vapor retarders are needed if emission rates or RH exceed thresholds. Glue-assisted nail-down is recommended for wide solid planks to counter cupping, trading higher installation time for long-term stability.

Loose lay stays niche and tends to concentrate in commercial areas that prioritize fast replacement. The wood flooring market’s method mix is increasingly shaped by subfloor type and end-use conditions, which is why engineered products with cross-method compatibility gain ground. Visualization tools that preview floating installations are also helping homeowners plan around transitions and room spans, which supports online ordering. In distributor channels, process automation and inventory visibility improve the ability to fulfill method-specific jobs in two days or less for standard profiles. This convergence of guidelines, tools, and logistics keeps floating and hybrid assemblies on a growth path in the wood flooring market.

By Finish: Pre-Finished Dominates on VOC Compliance

Pre-finished flooring held 71.27% in 2025 and is projected to grow at a 4.68% CAGR through 2031 as buyers prioritize low emissions and rapid project turnover. Factory-applied UV systems eliminate on-site sanding dust and finishing fumes, a significant advantage for multifamily and commercial projects with occupancy constraints. FloorScore certification validates 35 VOCs, including formaldehyde, and supports eligibility for frameworks such as LEED v4.1 and WELL in the wood flooring market. Aesthetic trends favor matte and low gloss finishes that reduce glare and mask micro scratches, which are commonly specified across open plan spaces. Advanced wear layers with aluminum oxide or ceramic bead additives extend abrasion resistance beyond typical site-finished capabilities.

Unfinished retains a meaningful role in high-end custom work and historic renovations where site staining and grain filling are required for exact color or texture matches. Site finishing creates a monolithic surface without micro bevels, which some clients prefer for formal rooms and galleries. Manufacturers are also responding to durability perceptions by introducing densified hardwood offerings such as AHF’s TimberTones, which reaches Janka hardness above 3,500 on hickory and claims multiple times improvement in dent and scratch resistance versus standard kiln-dried options. These upgrades keep pre-finished formats central to the wood flooring market as owners seek performance, compliance, and speed without sacrificing appearance.

By Distribution Channel: B2B Gains on Commercial Pivot

B2C retail consumers represented 67.35% in 2025, capturing home centers, specialty stores, online platforms, and other retail outlets. B2B contractor and builder channels are projected to expand at a 4.82% CAGR through 2031 as mass timber projects and multifamily developments route orders directly to manufacturers and distributors. Home centers stock entry-level click lock engineered items for immediate pickup, while specialty retailers differentiate with wide plank solids, custom stains, and vetted installer networks. As of Q4 2024, 58% of independent retailers planned near-term e-commerce investment, which supports visualization-led sales and direct-to-home delivery in the wood flooring market. Distributors expect stronger sales momentum in 2026 than retailers, supported by WMS and CRM tools that reduce order-to-delivery cycles to 48 hours for in-stock SKUs.

Manufacturers and distributors report that larger commercial and multifamily jobs are steadying backlogs relative to smaller retail remodeling orders. Healthcare added 62,000 jobs in May 2025, an indicator that often aligns with clinic and administrative expansions where wood is specified in non-clinical areas. Education facilities continue to adopt hard surface solutions in libraries, auditoriums, and common areas, with engineered wood gaining a role where acoustics and visual warmth are important. With digital selection tools and tighter logistics integration, B2B platforms are positioned to take incremental share in the wood flooring market as project-based demand expands.

By End User: Residential Retrofits Drive Volume

Residential applications represented 63.35% of demand in 2025, spanning single-family homes, townhouses, condominiums, and apartments, where replacement cycles and style updates lead. Commercial end users, including hospitality, healthcare, corporate offices, education, and retail, are projected to expand at a 5.10% CAGR through 2031 as biophilic programs and timber structures gain acceptance. Kitchen design trends for 2026 emphasize natural palettes and lighter wood tones, reinforcing demand for wide plank engineered offerings with matte finishes. United States housing starts reached 1,307,000 units at a seasonally adjusted annual rate in August 2025, which provides a base of structural activity around which retrofit cycles operate. State-level programs such as New York’s T-HIP supported household repairs for more than 1,200 homeowners in 2025, which often include subfloor stabilization and moisture remediation that enable wood installs.

On the commercial side, hospitality, education, and certain office projects specify wood for public spaces to convey natural warmth and to align with wellness-oriented interiors. Mass timber structures such as CLT and glulam help steer finish selections toward hardwood to maintain visual consistency with exposed structural members. FloorScore-certified pre-finished hardwood can contribute to the same LEED material credits as the timber structure, which simplifies green building documentation. As mass timber adoption expands within multifamily and low- to mid-rise commercial, the wood flooring market gains specification pull-through from matching visual and acoustic packages. The mix of residential replacements and targeted commercial buildouts keeps the end user profile diversified through the forecast period.

Geography Analysis

North America captured 31.38% in 2025, supported by ongoing new construction and active retrofit programs that channel funds into flooring-ready repairs. United States housing starts posted 1,307,000 units at a seasonally adjusted annual rate in August 2025, a level that supports steady volumes for both solid and engineered formats within the wood flooring market. The hardwood sector employs about 45,000 people and contributes USD 4 billion to GDP, underscoring the regional manufacturing base for wood flooring. Survey data for 2026 indicates that distributors expect stronger gains than retailers, consistent with a pivot toward B2B project pipelines. State programs such as New York’s T HIP that assisted 1,214 homeowners in 2025 also contribute to retrofit readiness that benefits the wood flooring market.

Asia-Pacific is projected to record the highest regional CAGR at 5.48% through 2031, driven by urban apartment construction in India, Southeast Asia, and Japan, which prioritizes premium interior finishes. Chinese housing starts contracted 24% in the first half of 2024, weighing on demand there while brightening prospects in neighboring markets where condominium retrofits and new builds continue. Japan’s assembled wooden flooring imports increased 30% month over month and 25% year over year in November 2024, with China supplying 65% and Vietnam 26% of HS 441875 shipments. Australia’s 2024-25 wood product imports reached USD 6.8 billion, with quarterly and annual price indices moving higher as of September 2025, which signals firm input costs. These dynamics support engineered formats and floating installations across humid and concrete-dominant markets in the wood flooring market.

Europe’s parquet market contracted 5% in 2024, with production in the FEP region down 5.3% year over year to 51.5 million square meters, the lowest output since the 2000s. Multi-layer engineered formats account for 83% of production, solid for 15%, and mosaic for 2%, with oak at 83.8% of species used, which illustrates the engineering and species mix shaping the wood flooring market. European laminate shipments totaled 313.5 million square meters in 2024, with Western Europe down 2.74%, Eastern Europe down 4.97%, North America up 8.85%, and Latin America up 8.51%, which frames the competitive interplay across regions. In South America, Brazil’s exports of wood, continuously shaped along any edges, ends, or faces, including flooring, reached USD 480.94 million in 2024 for HS 4409 shipments to the United States, reflecting sustained demand for selected exotic species. The Middle East and Africa continue to rely heavily on imports into hub markets such as the United Arab Emirates, while South Africa’s intra-African trade in finished wood carpentry shows variability in 2024 - 2025, making consistent supply chains important for regional distributors.

Competitive Landscape

The wood flooring market is moderately fragmented, with North American leadership split among Mohawk Industries, Shaw Industries, and AHF Products, while European players such as Kährs, Tarkett, and Barlinek hold regional depth. In 2025, two-thirds of NWFA respondents reported continuing share pressure from LVT (Luxury Vinyl Tile/Plank), WPC (Wood Plastic Composite), and laminate alternatives, which influences pricing power and channel strategies. Public disclosures by Mohawk show Q3 2025 net sales of USD 2.8 billion, with the company noting reciprocal tariffs affecting engineered wood and laminate, which reshape sourcing decisions. Shaw Industries, with annual revenue exceeding USD 6 billion, has invested about USD 90 million from 2024 through 2026 to expand resilient capacity in Georgia, illustrating portfolio balancing toward waterproof rigid formats that compete with wood in the 5-8 USD per square foot band. These moves set the tone for a competitive field where wood, laminate, and resilient products overlap in look, price, and performance.

Strategic investment is also visible in upstream integration and product innovation. AHF Products acquired two West Virginia sawmills in 2024 to secure a hardwood supply and mitigate stumpage volatility that has accompanied the 2022-2024 production downturn. The company launched TimberTones densified hardwood in 2025 with Janka hardness exceeding 3,500 on hickory and claims of multiple times dent and scratch resistance, a positioning aimed at answering durability concerns relative to resilient alternatives and high traffic use. Mohawk’s Uniclic mechanical locking platform, which originated in laminate, is now used in engineered wood to enable tool-free floating installations that reduce installer time. European manufacturers maintain an advantage in certified forestry and environmental declarations, which supports public sector tendering across Scandinavia and Germany, where embodied carbon baselines are set in policy.

Channel dynamics favor B2B growth and specification-led sales, which align with the wood flooring market’s shift toward engineered formats and pre-finished systems. Distributors expect stronger gains than retailers in 2026, supported by technology upgrades that compress delivery timelines to two days for stocked SKUs. NWFA data shows white oak leading species selection in 2025, and builders continue to standardize finishes that enable consistent multi-unit rollouts. With macro headwinds limiting new office starts, mass timber projects account for a growing share of timber-based construction value and help keep wood in the finish palette for high-visibility projects that emphasize sustainability. These patterns support a competitive landscape where innovation, verified emissions, and rapid fulfillment are central to defending and expanding share.

Wood Flooring Industry Leaders

Mohawk Industries

Shaw Industries Group

Armstrong World Industries

Mannington Mills Inc.

Barlinek SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AHF Products completed its purchase of the former Wellmade rigid core flooring manufacturing facility in Cartersville, Georgia, expanding its domestic production footprint and bringing the 328,000 square foot plant under its direct control to improve US-made supply and delivery for premium rigid core products

- August 2025: AHF Products announced plans to consolidate engineered wood operations and wind down production at the Somerset, Kentucky, facility by December 2025, concentrating production near end markets.

- June 2025: AHF Products launched Armstrong Flooring® TimberTones® Densified Hardwood, a new commercial‑grade flooring product made from 100 % real hardwood that uses a patented heat‑and‑pressure process to close open wood cells and deliver up to six times more dent resistance and four times more scratch resistance than traditional hardwood, along with waterproof and antimicrobial performance.

- May 2025: AHF Products launched TimberTones Densified Hardwood with Janka hardness exceeding 3,500 for hickory and claims of 6X dent and 4X scratch resistance versus standard kiln-dried hardwood.

Global Wood Flooring Market Report Scope

The wood flooring market encompasses the production, distribution, and sale of flooring materials made primarily from wood.

The wood flooring market is segmented by product type, installment method, finish, distribution channel, end-user, and geography. By product type, the market is segmented into Engineered Wood, Solid Wood, Reclaimed / Thermally-treated Wood, and Others. By installation method, the market is segmented into Nail-down, Glue-down, Floating / Click-lock, and Loose-Lay. By finish, the market is segmented into Pre-finished and Unfinished. By distribution channel, the market is segmented into B2C/Retail Consumers and B2B/Contractors/Builders. By end user, the market is segmented into residential and commercial. By geography, the market is segmented into North America, South America, Asia-Pacific, Europe, Latin America, and the Middle East and Africa. The report offers market size and forecasts in value terms (USD) for all the above segments.

By Product Type

| Engineered Wood |

| Solid Wood |

| Reclaimed / Thermally-treated Wood |

| Others |

By Installation Method

| Nail-down |

| Glue-down |

| Floating / Click-lock |

| Loose-Lay |

By Finish

| Pre-finished |

| Unfinished |

By Distribution Channel

| B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

By End-User

| Residential |

| Commercial |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Engineered Wood | |

| Solid Wood | ||

| Reclaimed / Thermally-treated Wood | ||

| Others | ||

| By Installation Method | Nail-down | |

| Glue-down | ||

| Floating / Click-lock | ||

| Loose-Lay | ||

| By Finish | Pre-finished | |

| Unfinished | ||

| By Distribution Channel | B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By End-User | Residential | |

| Commercial | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the wood flooring market?

The wood flooring market size is estimated USD 52.17 billion in 2026 and is forecast to reach USD 64.84 billion by 2031, at a 4.44% CAGR.

Which product types are leading and growing fastest?

Engineered wood is the largest, holding 34.84% in 2025, while reclaimed and thermally treated wood is projected to grow at a 5.27% CAGR through 2031.

Which installation methods are gaining share?

Nail‑down remains large at 43.38% in 2025, but floating and click‑lock are projected to grow fastest at a 5.18% CAGR due to DIY adoption and concrete subfloors.

Why are pre-finished floors favored in projects?

Factory finishes cut on-site time and emissions, often supported by FloorScore certification that qualifies for LEED and WELL compliance.

Which regions will see the strongest growth?

Asia‑Pacific is projected to post the highest regional CAGR at 5.48% through 2031, supported by urban apartment builds and condo retrofits.

How are channels shifting between retail and B2B?

B2C retail represented 67.35% in 2025, while B2B is projected to grow faster at a 4.82% CAGR on the back of specification-led commercial and multifamily projects.

Page last updated on: