Structural Core Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.93 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

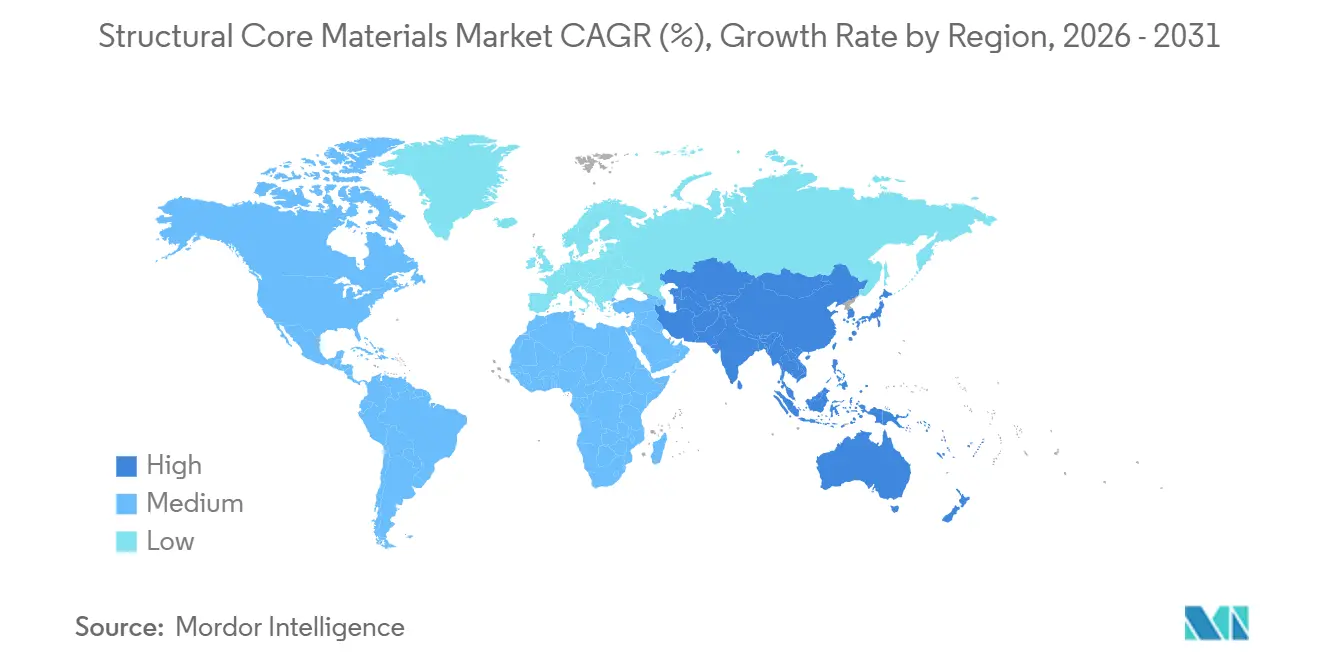

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Core Materials Market Analysis by Mordor Intelligence

The Structural Core Materials Market size is expected to increase from USD 2.68 billion in 2025 to USD 2.85 billion in 2026 and reach USD 3.93 billion by 2031, and is expected to grow at a CAGR of 6.64% over 2026-2031. The structural core materials market is growing, driven by a broader shift toward sandwich structures that combine low weight with strength, fatigue resistance, and stable performance across wind energy, aerospace, marine, transportation, and construction applications. Demand is rising as manufacturers replace metal parts and solid polymer assemblies with engineered composite structures that reduce mass without compromising stiffness or durability. Sustainability goals are reinforcing this trend, as recyclable thermoplastic grades and recycled PET-based products enable buyers to pursue lower-carbon material choices alongside structural performance. Competitive conditions remain balanced between a small group of technically qualified global suppliers in premium applications and a larger group of regional converters in more price-sensitive uses. The clearest opportunities through 2031 are tied to recyclable foam and honeycomb systems, certified aerospace interiors, electric transport structures, and modular building panels, where performance, processing efficiency, and compliance requirements are converging.

Key Report Takeaways

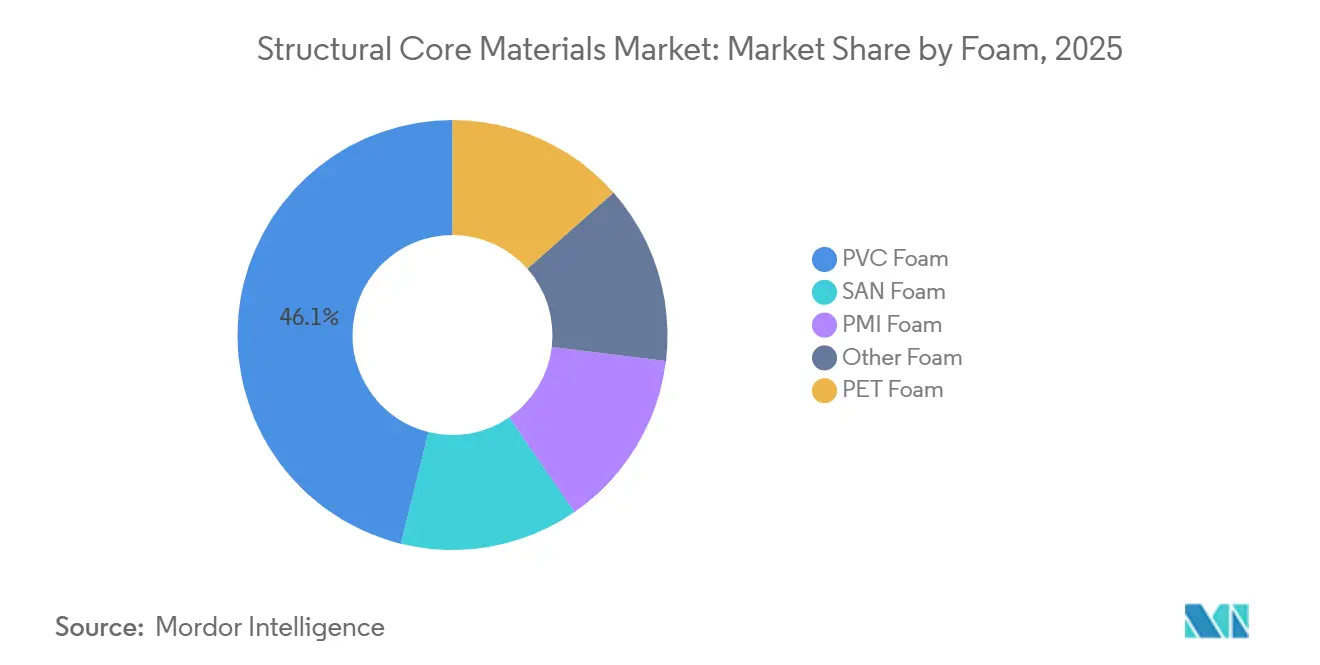

- By foam, Polyvinyl Chloride (PVC) Foam held 46.13% of the segment in 2025, while Polyethylene Terephthalate (PET) Foam is projected to grow at a 7.23% CAGR through 2031.

- By honeycomb, Aluminum Honeycomb accounted for 47.36% of the segment in 2025, while Thermoplastic Honeycomb is forecast to expand at a 7.83% CAGR through 2031.

- By outer skin type, Glass Fiber Reinforced Polymer represented 59.62% of the segment in 2025, while Carbon Fiber Reinforced Polymer is expected to advance at a 7.15% CAGR through 2031.

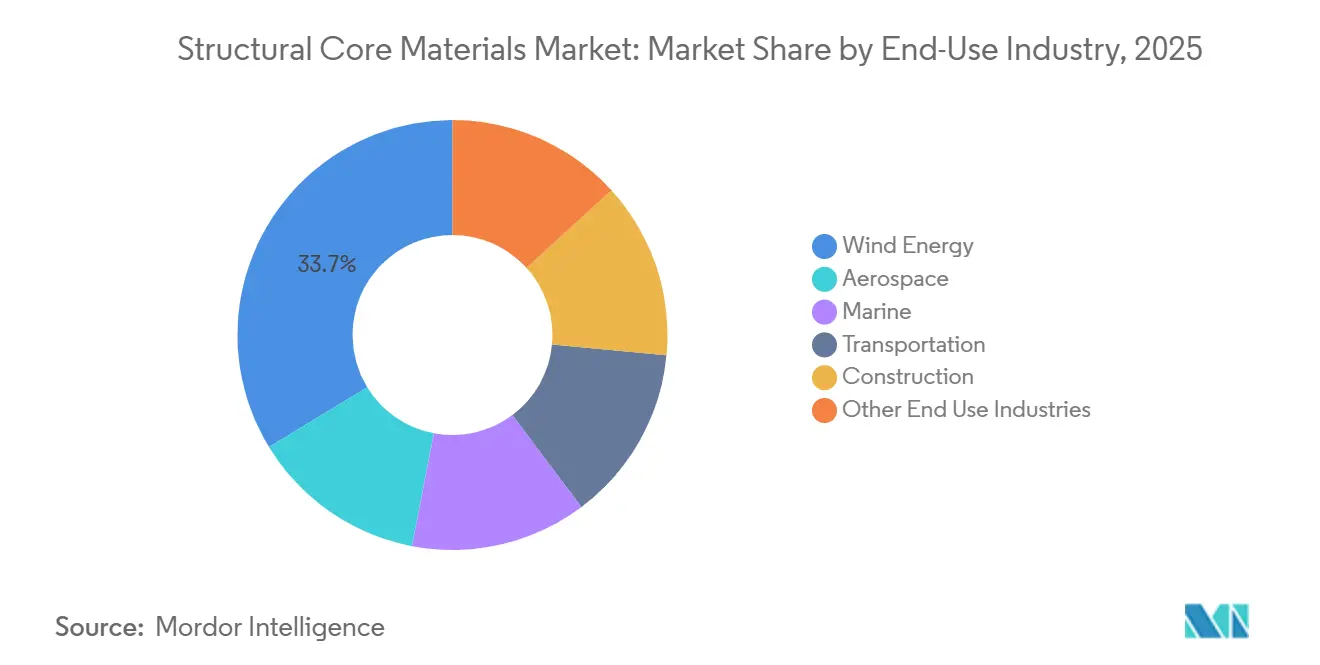

- By end-use industry, Wind Energy captured 33.72% of revenue in 2025, while Transportation is expected to record the highest CAGR at 6.74% through 2031.

- By geography, Asia-Pacific held 42.83% of revenue in 2025 and is projected to expand at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Structural Core Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wind Energy Blade Expansion | +2.3% | Global, concentrated in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Aerospace Weight Reduction Requirements | +1.6% | North America and Europe, with spillover to the Asia-Pacific | Medium term (2-4 years) |

| Lightweighting Demand for Electric Vehicles and Commercial Transport | +1.2% | Global, led by Asia-Pacific EV production corridors | Short term (≤ 2 years) |

| Shift Toward Recyclable and Thermoplastic Core Material Grades | +0.8% | Europe, expanding to North America | Medium term (2-4 years) |

| Modular and Prefabricated Construction Demand | +0.5% | Asia-Pacific, with secondary gains in the Middle East and Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wind Energy Blade Expansion: Sustained Volume Pull for Structural Foam and Honeycomb Cores

Wind energy remains the largest end-use segment in the structural core materials market because modern blade design depends on sandwich structures for stiffness, fatigue resistance, and weight control. Demand is rising as offshore blades grow longer, increasing the amount of core material required per blade even when installation growth is not keeping pace. Material selection within blades is also shifting, with polyethylene terephthalate (PET) foam gaining preference in root sections where closed-cell density performance and recyclability align with procurement priorities over traditional natural core options[1]Gurit Holding AG, “PET Foam Core, Structural Core Material,” Gurit, gurit.com. This is keeping the structural core materials market tied not only to new turbine counts, but also to the growing structural content required in larger platforms. The result is a steadier volume base for foam and honeycomb suppliers that can meet wind Original Equipment Manufacturer (OEM) requirements on consistency, processing, and sustainability.

Aerospace Weight Reduction: Composite Sandwich Specifications Set a New Structural Baseline

Aerospace demand is supporting the structural core materials market as composite sandwich designs are now embedded in commercial aircraft development rather than treated as specialty solutions. The Airbus A350 XWB incorporated more than 54% composites by structural mass and delivered a 25% fuel consumption reduction compared to equivalent aluminum-airframe aircraft. The Boeing 787 also reached close to 50% composite content by structural mass, reinforcing the same design direction across the next generation of aircraft programs. This keeps demand active for Nomex and aluminum honeycomb in cabin and secondary structures, and for Polymethacrylimide (PMI) foam in applications where low density and dimensional precision are essential. Growth is also broadening beyond legacy airframes, as Evonik is positioning ROHACELL for electric Vertical Take-Off and Landing (eVTOL) applications where low mass and structural efficiency are difficult to achieve with conventional materials.

Lightweighting Demand for Electric Vehicles and Commercial Transport: A New Volume Tier

Transportation is becoming a more meaningful part of the structural core materials market as electrification pushes manufacturers to reduce vehicle weight without compromising structural performance. Rising use of sandwich panels in underbody systems, enclosures, rail interiors, trailer walls, and bus panels indicates that the demand base is widening beyond aerospace and wind. Demand is concentrated in applications where structural efficiency, insulation, and fire performance need to be combined in a single panel system. Scott Bader introduced a composite flooring solution for rail in 2025 that used recycled PET foam and bio-based resin while meeting EN 45545-2 HL3 fire standards. As more transport programs adopt lightweight panel systems at commercial scale, the structural core materials market is moving into a larger and more competitive volume tier.

Shift Toward Recyclable and Thermoplastic Core Materials: Circular Economy Mandates Reshaping Procurement

Sustainability regulations and customer procurement standards are moving the structural core materials market toward recycled and thermoplastic formats that support end-of-life recovery and lower embodied carbon. Polyethylene Terephthalate (PET) foam benefits from being produced from post-consumer bottle feedstock, allowing buyers to link material choice with waste reduction goals. Gurit stated that it recycled 891 million post-consumer PET drinking bottles and 10,890 tonnes of operational PET waste in 2024, and also reported CO2 emissions up to 65% lower than those of conventional foam cores. Thermoplastic honeycomb is gaining attention for the same reasons, particularly where manufacturers require recyclable interior solutions and faster processing. Toray Advanced Composites completed NCAMP qualification for its Cetex LMPAEK thermoplastic composite in December 2025, placing FAA-accepted structural design allowables in the public domain and lowering adoption barriers for future thermoplastic sandwich assemblies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Qualification and Aerospace Certification Costs | -1.4% | Global, with greater intensity in North America and Europe | Medium term (2-4 years) |

| Polymer Precursor and Raw Material Cost Volatility | -1.1% | Global | Short term (≤ 2 years) |

| Limited End-of-Life Recyclability of Thermoset Composite Sandwich Structures | -0.7% | Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Qualification and Certification Costs: A Structural Barrier Protecting Incumbents at the Expense of Pace

High certification costs restrict the pace at which new suppliers can enter the structural core materials market, particularly in aerospace grades where each material system must complete lengthy approval cycles. Industry sources indicate that qualification can take 18 to 36 months for each material and platform combination. Major OEMs also maintain separate approval databases that require parallel documentation and testing. This structure favors incumbent suppliers that can distribute testing and compliance costs across long production programs and established customer relationships. A technically promising new foam or honeycomb product may face slow adoption if the certification pathway remains expensive or fragmented. Toray's NCAMP milestone is relevant in this context because publicly available FAA-accepted design allowables reduce the custom testing required for newer thermoplastic solutions[2]Toray Advanced Composites, “Toray Advanced Composites Completes NCAMP Qualification for Cetex High Performance Thermoplastic Composite Materials,” Toray Advanced Composites, toraytac.com.

Raw Material Price Volatility: Margin Compression Across Foam and Resin Systems

Raw material price volatility restrains the structural core materials market, as foam cores and bonding systems depend on chemical feedstocks subject to sharp price changes. PVC foam relies on vinyl chloride and related precursor chains, while polyurethane and resin systems depend on isocyanates, polyols, and other inputs tied to energy costs, supply concentration, and logistics disruptions. Producers cannot always pass cost increases through quickly, particularly under aerospace or wind energy contracts negotiated over longer time frames. This compresses margins and can slow investment in new capacity even when demand remains favorable. Reformulation and compliance costs in Europe add further financial pressure without providing immediate pricing relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foam: PVC Dominates While Recyclability Lifts PET Foam Ahead of All Peers

Polyvinyl Chloride (PVC) Foam held 46.13% of the foam segment in 2025, making it the largest material class in the foam category. This position reflects long-term use in marine hulls, wind blade sections, and transport panels, where machinability, cost, and resistance to dynamic stress support specification. Styrene Acrylonitrile (SAN) Foam sits between PVC and PMI on the performance scale and is used in marine tooling, motorsport, and selected transportation components requiring stronger thermal performance. PMI Foam is the preferred option for aerospace and advanced mobility applications, with Evonik's ROHACELL line supported by a long certification history, low density, and stable behavior under autoclave conditions. The foam segment of the structural core materials market is divided between high-volume incumbent grades and smaller premium formats that are difficult to substitute once qualified.

Polyethylene Terephthalate (PET) Foam is projected to expand at a 7.23% CAGR through 2031, making it the fastest-growing foam type in the structural core materials market. A 2024 peer-reviewed study found that fully recycled PET foam cores used in glass fiber sandwich panels delivered flexural behavior comparable to PVC-based alternatives, providing scientific support for substitution. PET addresses both mechanical requirements and circular procurement criteria in a single solution. The Other Foam category, including polyurethane and polystyrene grades, remains tied to construction panels, enclosures, and insulation applications where structural demands are lower and cost sensitivity is higher. PET Foam represents the primary growth driver for structural core materials market size through 2031, while PVC continues to define the current revenue base.

By Honeycomb: Thermoplastic Technology Disrupts Aluminum's Established Position

Aluminum Honeycomb represented 47.36% of the honeycomb segment in 2025, giving it the largest share in the category. Its position reflects established use in aerospace floor panels, nacelle fairings, and facade systems where crush resistance, dimensional stability, and qualification history make replacement difficult. Nomex Honeycomb remains relevant in aircraft interiors, where flammability compliance supports its role in bins, ceilings, and sidewall panels. Other Honeycomb types, including stainless steel and titanium variants, remain limited to specialized defense and space applications where structural demands exceed what more common alternatives can deliver. The honeycomb segment of the structural core materials market is anchored by mature materials with established qualification records.

Thermoplastic Honeycomb is growing at a 7.83% CAGR through 2031, making it the fastest-growing honeycomb type in the structural core materials market. Its growth is driven by compatibility with recyclable interior systems and processing routes that suit modern manufacturing requirements in certain applications. Composites United highlighted this through EconCore's ThermHexWAVY polyetherimide honeycomb core technology for aircraft interiors, designed to meet fire, smoke, and toxicity requirements while improving out-of-plane buckling resistance through a wavy cell wall geometry. Thermoplastic Honeycomb is now positioned as a technically credible aerospace option alongside its recyclability attributes. Within the honeycomb category, Thermoplastic Honeycomb is the strongest contributor to future growth in the structural core materials market.

By Outer Skin Type: Carbon Fiber Accelerating Within a Glass Fiber Reinforced Polymer (GFRP)-Dominated Landscape

Glass Fiber Reinforced Polymer (GFRP) accounted for 59.62% of the outer skin type segment in 2025, giving it the broadest installed base across volume applications in the structural core materials market. Its position reflects a combination of mechanical performance, corrosion resistance, and cost across wind energy, marine, construction, and light transportation applications. GFRP is compatible with multiple core types and manufacturing routes such as vacuum infusion and press bonding, accessible to both large converters and mid-sized fabricators. This process compatibility makes it the default outer skin choice where programs do not require the highest certification tier or the lowest possible weight. GFRP continues to anchor the current revenue structure of the structural core materials market.

Carbon Fiber Reinforced Polymer (CFRP) is projected to grow at a 7.15% CAGR through 2031, making it the fastest-growing outer skin type in the structural core materials market. This growth is linked to aerospace structures, eVTOL airframes, and premium electric vehicle enclosures where mass reduction per structural unit takes priority over material cost. A 2025 peer-reviewed study on CFRP sandwich structures with pyramidal lattice cores reported close to a 7 times improvement in specific compressive strength compared to conventional configurations. Natural Fiber Reinforced Polymer remains a smaller niche but is attracting attention in construction and consumer applications where bio-based content is a procurement consideration. Gurit's 2024 collaboration with Rubisco on a hemp fiber-faced panel with a recycled PET foam core illustrates how the structural core materials industry is testing lower-impact skin and core combinations within sandwich design principles.

By End-Use Industry: Transportation Closing the Gap on Wind Energy's Long-Held Share

Wind Energy led the end-use industry segment with 33.72% of revenue in 2025, giving it the largest share across application groups in the structural core materials market. Turbine blades rely on sandwich composite architectures for stiffness, fatigue behavior, and manageable weight over large spans. Aerospace follows as the next major end use, where floor panels, nacelles, cargo containers, and control surfaces depend on core materials that combine structural, acoustic, and thermal functions in a single system. Marine demand relies primarily on PVC and PET foam cores in hulls, decking, and subsea housings, where hydrostatic pressure resistance and fatigue behavior support premium pricing. Construction completes the group, with sandwich panels used in modular and prefabricated systems where factory assembly simplifies site work and reduces schedule pressure.

Transportation is expected to grow at a 6.74% CAGR through 2031, making it the fastest-growing end-use segment in the structural core materials market. Demand spans electric commercial vehicles, rail interiors, trailer walls, bus panels, and other formats where lighter structures improve payload, efficiency, or integration. Scott Bader's 2025 rail flooring example, built from recycled PET foam and a bio-based resin that meets EN 45545-2 HL3 fire standards, illustrates how transport applications are combining structural performance with sustainability and compliance requirements. This creates an additional demand base for the structural core materials market outside the established wind and aerospace segments. Suppliers face increased competition as transport buyers require a balance between cost, processing speed, certification, and circular material content.

Geography Analysis

Asia-Pacific accounted for 42.83% of revenue in 2025 and is projected to grow at a 6.12% CAGR through 2031. China is the region's primary demand anchor, as its wind turbine blade manufacturing base absorbs significant foam core volume and supports a broad composite materials supply chain. Japan contributes aerospace content through honeycomb and composite component activity, while South Korea supports demand through commercial shipbuilding applications, where lightweight sandwich panels are used in hull and superstructure design. India represents a smaller but growing source of demand as aerospace manufacturing investment and wind installations expand the need for certified and semi-certified core grades. These factors position Asia-Pacific as the largest regional production and consumption base in the structural core materials market.

North America and Europe form the next major tier of the structural core materials market, each shaped by distinct demand dynamics. North America is anchored by commercial and defense aerospace activity, a network of composite fabricators, and suppliers such as Hexcel with manufacturing operations in the United States. Hexcel reported USD 1.9 billion in 2025 net sales and guided to USD 2.0 billion to USD 2.1 billion for 2026, reflecting confidence in recovering aerospace build rates and continued demand for advanced core materials. Europe is more strongly shaped by regulatory pressure on material sustainability, which is accelerating the adoption of recycled PET foam and thermoplastic honeycomb in wind energy and transportation supply chains. Evonik's shift of ROHACELL production in Darmstadt to 100% renewable electricity in September 2024 illustrates how producers in the region are aligning operations with carbon disclosure and procurement requirements.

South America remains an early-stage part of the structural core materials market, with Brazil offering the clearest demand base through onshore wind development and related blade-material needs. Argentina and neighboring markets contribute more modestly through marine and infrastructure applications that still depend heavily on imported materials and finished panel systems. The Middle East and Africa present an opportunity tied to infrastructure investment, construction activity, and the gradual development of utility-scale renewable energy programs. These regions remain import-dependent, but lightweight sandwich panels may become more attractive where skilled labor is limited and modular construction can reduce site complexity. Regional participation remains limited, but these markets represent a growth layer expected to become more relevant later in the forecast period.

Competitive Landscape

The structural core materials market is moderately fragmented in premium-certified applications and more fragmented in commercial-grade applications, creating a mixed competitive landscape rather than a single, uniform structure. Gurit Services AG, Hexcel Corporation, Evonik Industries AG, DIAB Group, Euro-Composites S.A., and EconCore N.V. form the main cluster of technically established participants across aerospace honeycomb, high-performance foam, and engineered sandwich solutions. Their positions are supported by qualification history, process know-how, and the ability to supply consistent materials to demanding end uses. Competition in the structural core materials market is tighter in aerospace interiors, advanced mobility, and premium wind applications than in basic construction or lower-specification transport panels. Regional converters remain relevant in cost-sensitive tiers, while the highest-value opportunities continue to favor suppliers with certified products and strong application support.

Recent company actions illustrate how participants are defending and extending their positions in the structural core materials market. Hexcel announced a USD 350 million accelerated share repurchase in October 2025 and raised its quarterly dividend by 6%, reflecting management's confidence in the recovery of aerospace-linked demand. Evonik transitioned ROHACELL production in Darmstadt to 100% renewable electricity in 2024, reducing annual emissions by nearly 3,400 metric tons of CO₂. Gurit expanded its US Dallas facility in 2026 to support growing subsea demand, indicating that suppliers are using adjacent markets to reduce dependence on a single end-use cycle. These actions indicate that competition in this market is shaped by financial discipline, manufacturing resilience, lower-carbon production, and selective expansion into new application areas.

Technology positioning around recyclable and repairable sandwich systems represents another dimension of competition in the structural core materials market. EconCore's continuous thermoplastic honeycomb platform and ThermHexWAVY aerospace interior solution demonstrate how process innovation can improve both circularity and structural performance. DIAB and CompPair partnered in 2025 on healable composite sandwich structures for aerospace and mobility applications, reflecting a strategy focused on upgrading product functionality rather than adding volume capacity. The primary disruption risk for established participants is the successful qualification of recyclable alternatives at competitive cost in applications previously closed to them. Suppliers that can combine certification readiness, circular material content, and strong customer integration without compromising performance are positioned to capture value in this market.

Structural Core Materials Industry Leaders

Hexcel Corporation

Evonik Industries AG

3A Composites GmbH (SCHWEITER TECHNOLOGIES AG)

Gurit Services AG

Diab Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gurit announced the expansion of its U.S. Dallas facility to meet anticipated growth in subsea structural foam core demand. The expansion includes a new building expected to reach full operational status in Q3 2026. This follows a multi-year subsea supply contract signed in September 2025 and a concurrent expansion of Gurit's Australian operations, indicating the company's diversification beyond wind energy.

- February 2026: 3A Composites Americas launched GATORSPAN, a structural sandwich panel featuring an Extruded Polystyrene (XPS) foam core, designed for residential and commercial construction envelope applications. The product was showcased at the International Builders' Show (IBS) 2026. GATORSPAN combines structural sheathing, continuous insulation, and water barrier functions into a single factory-made panel, targeting modular and retrofit construction segments.

Global Structural Core Materials Market Report Scope

Structural core materials are lightweight internal layers used in sandwich composites to increase stiffness and shear strength without adding significant weight. Key types include foams (such as PVC and PET), wood (such as end-grain balsa), and honeycombs. These materials are used across the aerospace, marine, and wind energy industries.

The structural core materials market is segmented by foam, honeycomb, outer Skin Type, end-use industry, and geography. By foam, the market is segmented into PET foam, PVC foam, SAN foam, PMI foam, and Other foam. By honeycomb, the market is segmented into aluminum honeycomb, nomex honeycomb, thermoplastic honeycomb, and other honeycomb. By outer skin type, the market is segmented into glass fiber reinforced polymer (GFRP), carbon fiber reinforced polymer (CFRP), NFRP, and other outer skin types. By end-use industry, the market is segmented into aerospace, wind energy, marine, transportation, construction, and other end-use industries. The report also covers market size and forecasts for structural core materials across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| PET Foam |

| PVC Foam |

| SAN Foam |

| PMI Foam |

| Other Foam |

| Aluminum Honeycomb |

| Nomex Honeycomb |

| Thermoplastic Honeycomb |

| Other Honeycomb |

| Glass Fiber Reinforced Polymer (GFRP) |

| Carbon Fiber Reinforced Polymer (CFRP) |

| NFRP |

| Other Outer Skin Types |

| Aerospace |

| Wind Energy |

| Marine |

| Transportation |

| Construction |

| Other End Use Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Foam | PET Foam | |

| PVC Foam | ||

| SAN Foam | ||

| PMI Foam | ||

| Other Foam | ||

| By Honeycomb | Aluminum Honeycomb | |

| Nomex Honeycomb | ||

| Thermoplastic Honeycomb | ||

| Other Honeycomb | ||

| By Outer Skin Type | Glass Fiber Reinforced Polymer (GFRP) | |

| Carbon Fiber Reinforced Polymer (CFRP) | ||

| NFRP | ||

| Other Outer Skin Types | ||

| By End-Use Industry | Aerospace | |

| Wind Energy | ||

| Marine | ||

| Transportation | ||

| Construction | ||

| Other End Use Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Structural Core Materials Market?

The Structural Core Materials Market size is expected to increase from USD 2.68 billion in 2025 to USD 2.85 billion in 2026 and reach USD 3.93 billion by 2031, and is expected to grow at a CAGR of 6.64% over 2026-2031.

Which end-use sector contributes the most revenue today?

Wind Energy is the largest end-use segment, accounting for 33.72% of revenue in 2025, as modern turbine blades rely heavily on sandwich composite structures.

Which material categories are growing the fastest?

PET Foam leads foam growth at 7.23% CAGR, Thermoplastic Honeycomb leads honeycomb growth at 7.83%, and CFRP leads outer skin growth at 7.15% through 2031.

Why is Asia-Pacific so important in this space?

Asia-Pacific accounted for 42.83% of revenue in 2025 and remains the leading region due to China’s wind blade manufacturing base and demand from Japan, South Korea, and India.

Page last updated on: