Hybrid Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.42 Billion |

| Market Size (2031) | USD 44.28 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

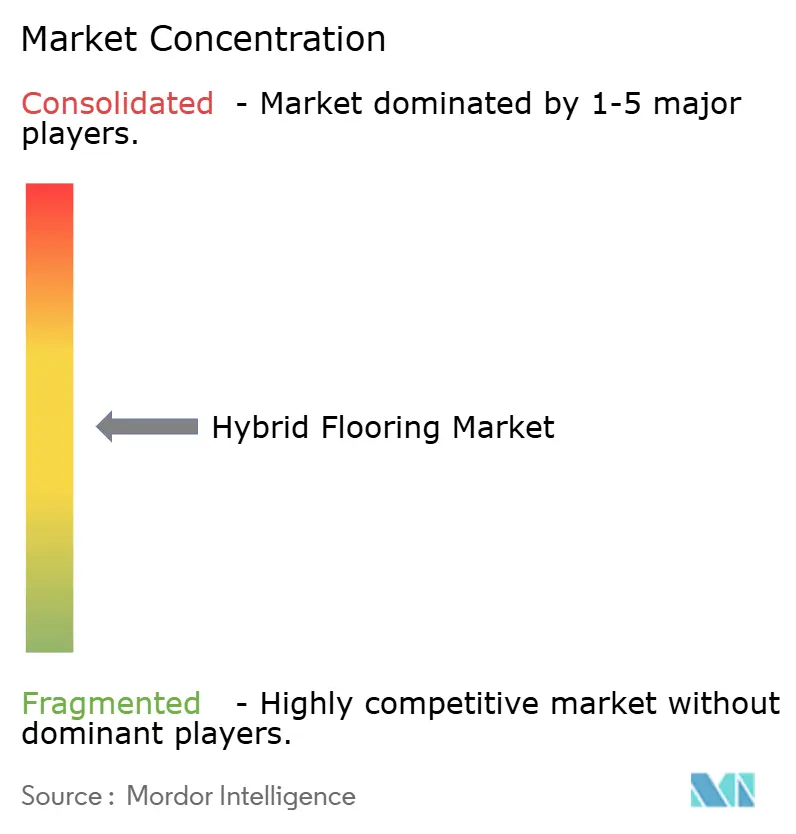

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Flooring Market Analysis by Mordor Intelligence

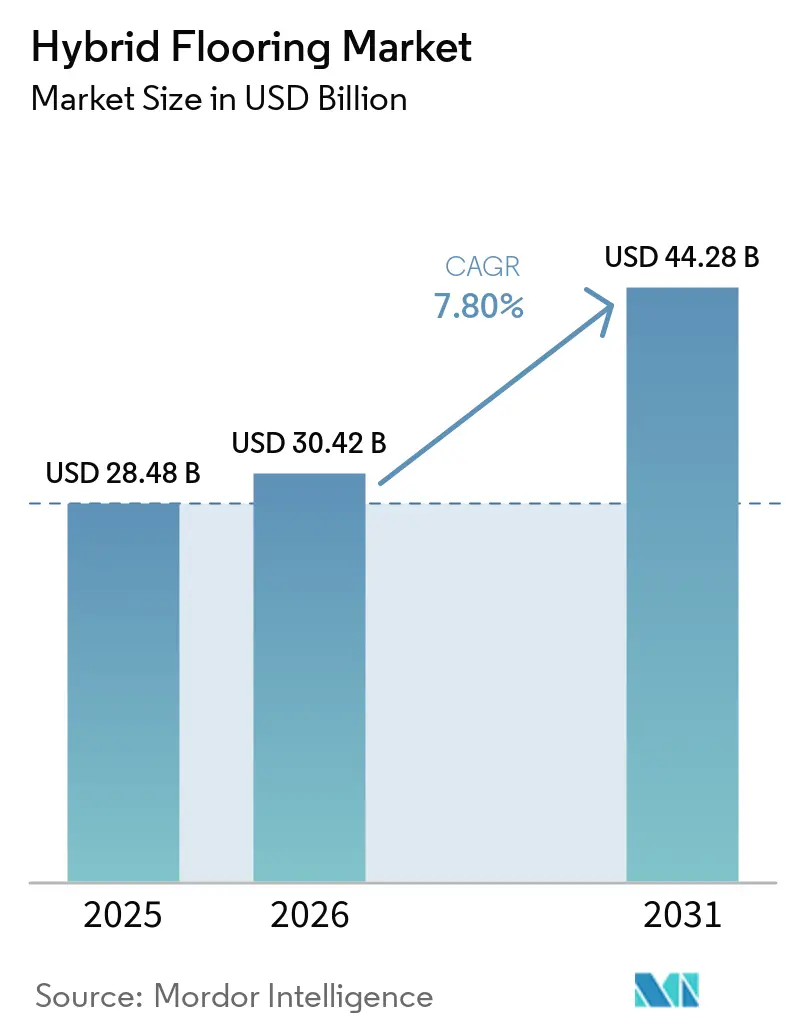

The hybrid flooring market size is expected to increase from USD 28.48 billion in 2025 to USD 30.42 billion in 2026 and reach USD 44.28 billion by 2031, growing at a CAGR of 7.8% over 2026-2031. Hybrid flooring is a rigid-core flooring category that uses a dense composite core, usually SPC, WPC, or newer PVC-free materials, along with a high-definition wear layer and, in many cases, built-in acoustic underlayment. This combination delivers waterproof performance and dimensional stability that laminate and traditional LVT typically do not. Building codes and warranty expectations sustain demand for rigid-core waterproof systems across remodeling and new build programs. Procurement and installation preferences keep click-based floating systems in focus as contractors compress fit-out schedules in occupied spaces. Regulatory scrutiny of VOCs and material health nudges specifications toward low-emissions solutions and PVC-free rigid cores, with performance parity proven in commercial settings. Asia-based production capacity supports global availability as importers navigate evolving labor and materials compliance requirements to keep shipments flowing. Trade policy and compliance checkpoints add uncertainty to landed costs, which, in turn, favors domestic or nearshore capacity strategies to reduce schedule risk and improve predictability in project execution[1]U.S. Department of Homeland Security, “2025 Updates to the Strategy to Prevent the Importation of Goods Mined, Produced, or Manufactured with Forced Labor in the People’s Republic of China,” dhs.gov.

Key Report Takeaways

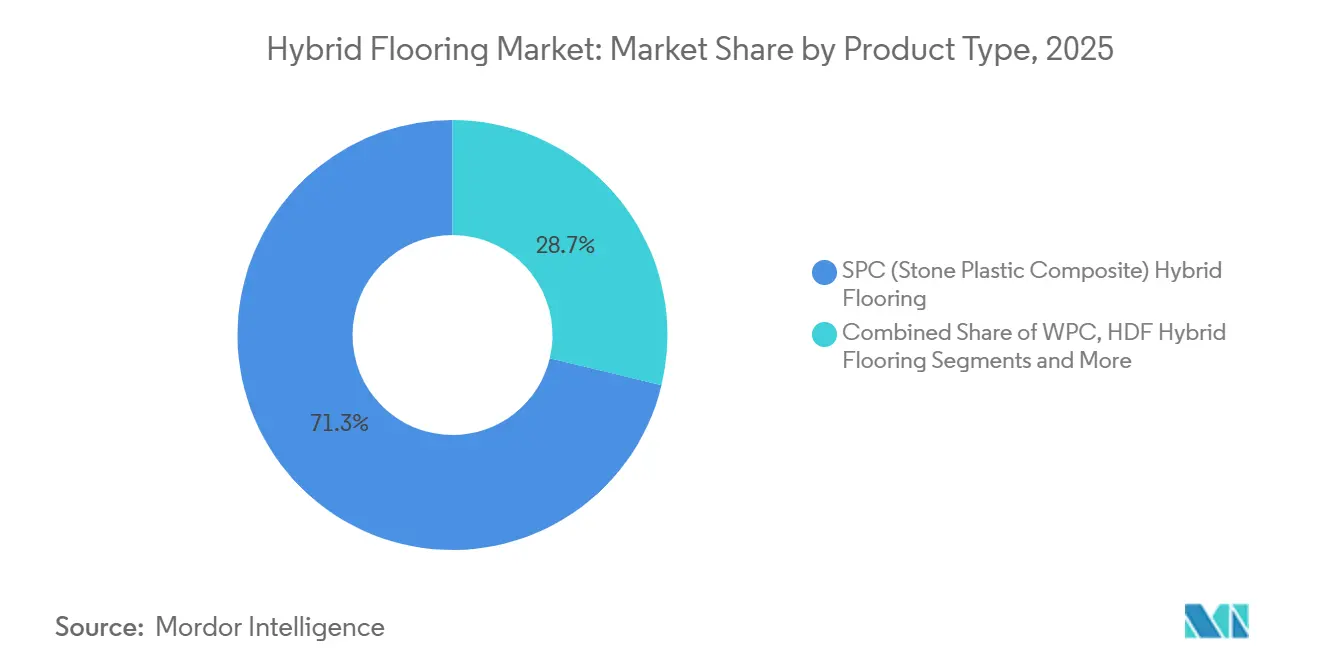

- By product, SPC led with a 71.25% revenue share in the 2025 hybrid flooring market; rigid high-density fiberboard (HDF) hybrid flooring is projected to expand at a 9.15% CAGR through 2031.

- By installation method, click-and-click-lock floating systems accounted for a 70% share of the 2025 hybrid flooring market and are projected to grow at an 8.50% CAGR through 2031.

- By construction type, renovation & remodel commanded a substantial 63.81% market share in 2025 and is forecast to grow at an impressive CAGR of 8.10% through 2031.

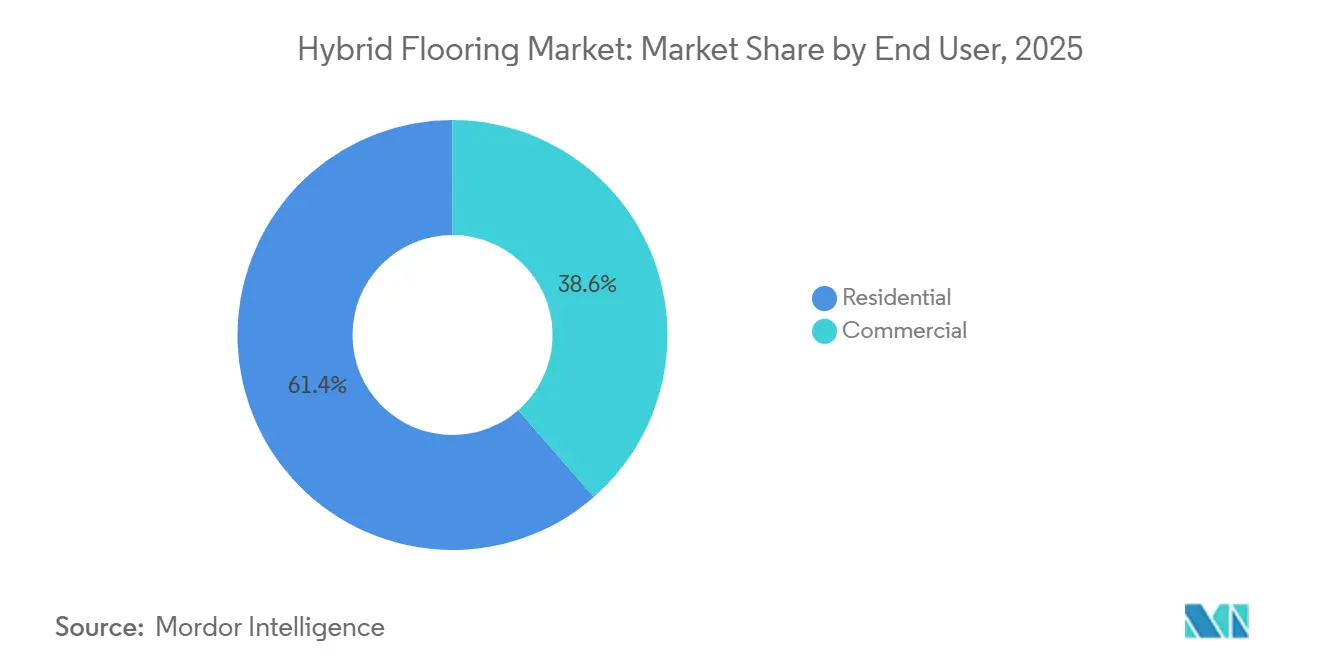

- By end user, residential accounted for a 61.43% share of the hybrid flooring market in 2025, while commercial/non-residential is projected to grow at an 8.67% CAGR through 2031.

- By distribution channel, B2C/retail accounted for a 67.72% share of the hybrid flooring market in 2025, while online/e-commerce within B2C is projected to grow at a 10.11% CAGR through 2031.

- By geography, Asia-Pacific accounted for a 42.62% share in 2025 and is projected to grow at a 9.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waterproof Hard-Surface Preference In Residential Remodels and Multi-Family | +1.2% | North America core, APAC multifamily surge, Europe steady | Medium term (2-4 years) |

| Click-Lock Floating Installs Reduce Labor Time and Enable DIY And Faster Commercial Fit-Outs | +0.9% | Global, with early gains in North America, the United Kingdom, and Germany | Short term (≤ 2 years) |

| APAC Scale in SPC Manufacturing and Rapid Adoption Accelerates Supply Innovation | +1.5% | APAC core, spill-over to MEA and LatAm, Vietnam, and India as secondary hubs | Medium term (2-4 years) |

| Commercial Refresh Cycles (Retail, Hospitality, Healthcare) Favor Durable, Low-Maintenance Rigid Core | +0.8% | North America, Europe, Middle East including UAE and Saudi | Medium term (2-4 years) |

| Shift Toward PVC-Free Rigid Cores For Sustainability And IAQ Credentials | +1.0% | Europe including Germany and Nordics, North America including California and Northeast, Japan | Long term (≥ 4 years) |

| Acoustic Compliance Needs in Multi-Family (IIC targets) Favor Padded Rigid Core Systems | +0.6% | North America multifamily including Connecticut and California, UK, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Waterproof Hard-Surface Preference In Residential Remodels and Multi-Family

Water resistance is a top selection criterion for consumers and specifiers, which continues to steer demand toward waterproof rigid-core systems that tolerate spills and moisture intrusion over long service lives[2]Sunly SPC, “2026 Top Trends in China Wholesale SPC Vinyl Flooring Industry,” sunlyspc.com. Dimensional stability under prolonged moisture exposure is central to product positioning in high-use areas, as it protects subfloors and preserves appearance under normal residential and light commercial use. Product platforms that strengthen edge integrity and lock design have become standard, with proprietary systems like WetProtect designed to keep surface water from reaching the subfloor while maintaining a secure mechanical lock. Multifamily and rental programs view these waterproof assemblies as risk mitigation tools that reduce unit downtime after incidents. In addition to moisture resistance, designers seek surface finishes and topcoats that resist staining and wear, maintain a uniform appearance, and require infrequent refinishing. The combined performance characteristics continue to draw lifecycle-driven buyers into the hybrid flooring market in both owner-occupied and rental settings.

Click-Lock Floating Installs Reduce Labor Time and Enable DIY And Faster Commercial Fit-Outs

Floating click systems compress project schedules by eliminating adhesive cure times and enabling staged occupancy, thereby supporting tenant retention and reducing downtime for revenue spaces. The format also opens a DIY path in smaller residential rooms, with angle-lock or drop-lock mechanisms enabling skilled homeowners to complete typical rooms in a single day. Labor savings in renovation scenarios are meaningful in markets where weekend or overnight work is the only viable option, and specialty retailers note installation cost avoidance as a recurring differentiator in their project bids. Fold-down locking formats help crews work closely to fixed obstructions such as door frames and casework, reducing demolition scope on retrofit jobs and avoiding schedule slippage tied to rework. Click systems also tolerate modest subfloor variation within published tolerances, which helps reduce prep steps on slabs that would otherwise require grinding or skim coating. Together, these installation levers support cost certainty for owners and more competitive bidding for contractors in high-churn commercial interiors.

Asia-Pacific Scale in SPC Manufacturing and Rapid Adoption Accelerates Supply Innovation

Asia-based producers maintain large-scale SPC extrusion capabilities and have continued to invest in automation to improve throughput and consistency, supporting on-time delivery to import markets. Manufacturers in the region offer a wide range of visuals and surface technologies with rapid sampling and color-matching workflows for designers. Regional diversification also continues as suppliers manage trade policy and logistics risk by staging final assembly and inventory closer to destination markets. In parallel, importers to North America and Europe are strengthening documentation practices and supplier audits to comply with enhanced enforcement on goods that may contain restricted inputs or labor, which has become a high-priority focus in select materials categories. These compliance programs target data transparency down to earlier material tiers, which pushes investment in traceability systems and lab testing workflows. The net effect is a steady supply with more robust provenance controls, which aids specifier confidence during procurement planning.

Commercial interiors prioritize materials that maintain a clean visual with manageable care routines, which benefits rigid-core assemblies with durable wear layers. Facilities teams value quick-turn repairs and the ability to replace damaged planks or tiles without disrupting larger areas, which helps maintain service levels for occupants and guests. Healthcare and education frequently request antimicrobial and easy-to-clean surfaces that support hygiene protocols while avoiding porous materials that harbor contaminants. These settings also benefit from stable dimensional performance under rolling loads and traffic that would stress less rigid surfaces. Hospitality operators seek aesthetics that align with brand identity while meeting project schedules in active facilities. These preferences keep performance and downtime reduction at the center of commercial specification discussions across the hybrid flooring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC Sustainability Scrutiny and VOC/Plasticizer Restrictions | -0.3% | Europe, including REACH markets, California, Japan | Long term (≥ 4 years) |

| Entry-Level SPC Quality Issues Causing Failures and Dealer Fatigue | -0.2% | North America, including the western U.S. and Canada, Australia | Short term (≤ 2 years) |

| Trade/Tariff and Forced-Labor Compliance Disruptions for China-Sourced Rigid Core | -0.1% | Global, U.S. CBP enforcement focus | Medium term (2-4 years) |

| Low Recyclability/End-of-Life Pathways for Multi-Material Rigid Cores | -0.0% | EU member states, California, and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PVC Sustainability Scrutiny and VOC/Plasticizer Restrictions

Sustainability and IAQ scrutiny are intensifying across public and private tenders, placing pressure on formulations that rely on restricted plasticizers or cannot meet low-VOC thresholds. United States jurisdictions have tightened VOC rules for floor finishes and adhesives, forcing manufacturers to keep their certifications and testing files up to date as part of the submittal package[3]City of Sacramento, “2025 California Green Code Non-Residential VOC and Formaldehyde Limits,” cityofsacramento.gov. European procurement frameworks and ecolabel programs continue to drive the market toward phthalate-free and recyclable pathways, which encourage substitution in sensitive applications. The transition adds compliance costs and time-to-market, which can slow launches in price-sensitive segments where margin headroom is limited. Suppliers that invest ahead of rule changes position themselves to win early in green building programs that require mandatory documentation. As codes and standards evolve, low-emissions and cleaner input profiles remain central to acceptance in public and institutional work.

Entry-Level SPC Quality Issues Causing Failures and Dealer Fatigue

Dealer feedback in recent cycles highlighted call-backs tied to entry-level rigid-core imports that cut corners on thickness, density, or locking profiles. These experiences prompted many distributors and retailers to rationalize assortments and favor thicker cores and more robust joint systems that can manage rolling loads and minor subfloor variation in everyday use. Manufacturers have responded with reinforced locking technologies and tighter quality controls to reduce joint separation and surface failures reported in field use. The recalibration has created clearer tiering between commodity and premium options, with premium lines pairing improved locks with better visuals to differentiate. As installers and dealers reset expectations, education on subfloor tolerance and prep requirements has become a larger part of sales and training. These changes help set realistic performance boundaries and steer buyers toward fit-for-purpose specifications in the hybrid flooring market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Rigid high-density fiberboard (HDF) hybrid flooring Surge While SPC Retains Dominant Installed Base

SPC (Stone Plastic Composite) secured 71.25% market share in 2025, while rigid high-density fiberboard (HDF) hybrid flooring is projected to expand at a 9.15% CAGR through 2031. Product roadmaps now emphasize rigid platforms that pair installation speed with stability under temperature swings, including sun-exposed spaces. Manufacturers with PVC-free cores highlight renewable content and low-VOC credentials while matching surface and locking performance that specifiers require in commercial and multifamily applications. These portfolios complement established SPC lines in retail and project channels that prioritize a balance of durability and cost. WPC continues to serve applications that favor softer footfall or higher acoustic damping in occupied buildings. The hybrid flooring market benefits from a wider choice across performance, sustainability, and cost tiers.

Buyers who prioritize material health and emissions are receptive to platforms with clear documentation and short lead times. SPC retains strength where rolling loads and heavy traffic dictate denser cores and thicker wear layers. Product differentiation increasingly comes from lock strength, surface protection, and verified emissions profiles rather than from core chemistry alone. As product families expand, the hybrid flooring industry offers clearer mapping between application requirements and product tiers.

By Installation Method: Click/Click-Lock Dominates Retrofit While Glue-Down Defends New-Build Commercial

Click/click-lock floating systems commanded 70% share in 2025 while growing at an 8.50% CAGR. Floating formats enable phased renovations and meet lease requirements in occupied commercial spaces by avoiding adhesive cure times. DIY and pro installers alike cite predictable schedules and simpler subfloor prep within published tolerances as compelling reasons to select click systems for refreshes. Fold-down joints also allow crews to work close to vertical obstructions without demolition, which helps keep projects on track. Where permanence and heavy rolling loads are primary, glue-down remains the favored option for healthcare and education specifiers. Loose-lay serves targeted needs in temporary and raised-floor applications. The hybrid flooring market balances these three methods according to occupancy and service-life goals.

Installers highlight that lock quality and plank tolerance are as important as total thickness in achieving a trouble-free install. Glue-down’s advantage in carts and gurney corridors coexists with floating’s advantage in tenant improvements. Loose-lay expands the toolkit for quick-turn programs in spaces that anticipate future reconfiguration. Clear communication of slab flatness and prep needs in bid documents helps right-size the installation method for each scope. Across project types, channel partners increasingly emphasize mockups and site testing before full deployment. This discipline reduces change orders and aligns product choice with real-world constraints.

By Construction Type: Renovation & Remodel Capturing Market Growth while New Construction Driving Compliance and Durability and

Renovation & remodel commanded a substantial 63.81% market share in 2025 and is forecasted to grow at an impressive CAGR of 8.10% through 2031. Occupied and income-generating buildings increasingly adopt floating formats to minimize downtime and facilitate zone-based work staging. Residential upgrades are trending toward waterproof finishes in kitchens and bathrooms, while commercial spaces emphasize rapid repairs and a cohesive aesthetic. Detailed documentation for indoor air quality (IAQ) and acoustics accelerates landlord approvals and streamlines tenant fit-outs.

New builds underscore rigorous code compliance, detailed emissions documentation, and superior durability in high-traffic environments. General contractors and property owners meticulously assess lifecycle maintenance and aesthetic retention, alongside initial investment costs. In settings with acoustic requirements, integrated-pad systems enhance efficiency by reducing layers and complexity. Projects benefit significantly from dependable lead times and on-site training, which ensures high-quality installations.

By End User: Commercial Segment Outpaces Residential as Facility Managers Prioritize Lifecycle Cost Over First Cost

Residential retained 61.43% share in 2025, while commercial/non-residential is projected to grow at an 8.67% CAGR through 2031. Homeowners emphasize waterproof visuals for kitchens, bathrooms, and basements, with a strong preference for easy-care surfaces. Multifamily developers focus on turnover speed, durable wear layers, and acoustic performance to meet building code and lease expectations. Commercial teams value uniform appearance retention and straightforward maintenance routines that reduce disruptions and protect brand standards. Healthcare and education specify smooth, cleanable surfaces that support hygiene protocols and intensive cleaning regimens. These preferences keep rigid-core solutions visible across renovation and refresh budgets.

In commercial settings, premium features such as reinforced locks, thicker wear layers, and antimicrobial topcoats help extend the time between replacements. Hospitality operators prioritize scheduling certainty and visual impact, which favors floating formats and large-format tile visuals. Corporate and retail facilities look for consistent color across batches and flexible installation windows. As remodeling momentum improves alongside credit and financing conditions, pent-up project lists support sequential volume recovery for commercial programs. Manufacturers communicate lifecycle cost advantages through case examples and maintenance guides to quantify the total cost of ownership. This framing continues to support uptake in the hybrid flooring market as budgets normalize.

By Distribution Channel: B2B Dominates as Centralized Procurement Favors Spec-Grade Products and Direct Relationships

By distribution channel, B2C/retail accounted for a 67.72% share of the hybrid flooring market in 2025, while online/e-commerce within B2C is projected to grow at a 10.11% CAGR through 2031. Centralized procurement for multifamily, hospitality, and institutional projects enables more effective warranty vetting, consistent inventory, and better technical support. National and regional developers engage directly with manufacturers to forecast and schedule, improving capacity planning and reducing stockout risk. Specialty dealers support design services and multi-trade coordination that align flooring selection with lighting, millwork, and acoustics in larger remodels. B2C retail continues to serve homeowners who value assortment and samples, though technical guidance for subfloors and acoustics is less consistent. Online channels aid visualization and discovery but yield lower returns due to differences in color and lighting. Across channels, project cadence and repeat volume keep B2B central to demand fulfillment in the hybrid flooring market.

Distributors and contractors increasingly collaborate on pre-positioned inventory for multi-property rollouts, improving deployment and compressing time-to-revenue. Warranty clarity and service-level agreements serve as differentiators in competitive bids. Direct training on installation methods and substrate prep reduces rework and call-backs. For residential retail, curated collections and in-home consultations help reduce uncertainty and increase conversion rates. Across both channels, acoustic and IAQ documentation has become part of the base selling package. This shared infrastructure points to ongoing channel maturation and deeper alignment around performance requirements.

Geography Analysis

Asia-Pacific accounted for 42.62% of the hybrid flooring market share in 2025 and is projected to grow at a 9.84% CAGR through 2031. Producers across China and neighboring hubs continue to run high-capacity extrusion and finishing lines that support broad SKU ranges and quick sampling cycles[4]Chinafloorings, “SPC Flooring Manufacturer from China,” chinafloorings.com. Investing in automation enhances throughput and product consistency, helping maintain stable service levels for export markets. Suppliers diversify final assembly locations to manage tariff and clearance risks and to position inventory closer to buyers. Compliance expectations are rising for traceability and labor standards, shaping sourcing strategies and import documentation for North America and Europe. As regulatory frameworks evolve, vendors with verifiable supply chains and flexible routing options are better positioned to win. The hybrid flooring market in Asia-Pacific retains cost and capacity advantages even as compliance rigor increases.

North America continues to deploy rigid-core across remodeling programs in kitchens, bathrooms, and basements, while commercial programs emphasize performance and downtime reduction. Domestic capacity investments and closer-to-market assembly reduce exposure to tariff swings and clearance delays, which helps stabilize project schedules. Public agencies and lenders reinforce acoustic and life-safety requirements in multifamily and mixed-use developments, which keep integrated-pad systems and code-ready assemblies at the forefront of specifications. Across the hybrid flooring market, buyers seek clear maintenance guidance and warranty pathways that property insurers recognize. Documentation on VOC and material content remains central to submittals in city and state jurisdictions with stricter rulemaking. The region balances project work with retail refreshes as housing and credit conditions ease.

Europe maintains steady specification activity in residential and institutional projects, with an emphasis on low-emissions materials and recyclable pathways in public procurement. Acoustic targets in shared residential buildings and student housing continue to influence product selection and underlayment choices. Brands lean into independent certification schemes to demonstrate compliance with VOCs and material health, which helps smooth approvals and procurement. Supply diversification and local finishing help manage delivery risk and lead times for public tenders. Designers continue to adopt larger-format visuals and refined wood looks across retail and hospitality. These trends, combined with code-driven acoustics and IAQ requirements, keep the hybrid flooring market active across European renovation and new-build programs.

Competitive Landscape

Leading brands leverage vertical integration, domestic and regional manufacturing, and well-developed retail and project channels to balance cost, quality, and availability. Capacity additions and continuous improvement programs position producers to serve demand without significant lead-time expansion, which is critical as project pipelines strengthen. Product development is focused on lock strength, surface protection, and low-VOC credentials, supported by third-party certifications that reduce friction during submittals and approvals. Suppliers with clear installation guidance and accessible training content continue to outperform in fragmented installer ecosystems. These execution strengths are central as the hybrid flooring market navigates tighter specifications in commercial, multifamily, and institutional work.

Sustainability-aligned innovation is broadening beyond materials into circular design and disassembly. Technology licensors and manufacturers are piloting platforms that enable upcycling or end-of-life separability, with the aim of scaling once collection rates and logistics improve. Brands are also extending product families that use renewable or recyclable content while maintaining performance in terms of stability and sound impact. In parallel, procurement teams continue to test and specify products that meet acoustic targets for multifamily and dense urban housing, supporting integrated underlay solutions. Compliance and documentation readiness around VOC and restricted substances remain table stakes in European public tenders and in the United States jurisdictions with tighter codes. These elements underpin premium positioning and create measurable differentiation in bids.

Execution at scale continues to define competitive separation. Companies that publish detailed install guides, provide on-site technical support, and manage consistent color and texture across batches reduce risk for contractors and owners. Product ecosystems that combine visual libraries with rapid sampling and reliable lead times give designers confidence in brand selection. In B2B pathways, national account relationships and inventory prepositioning shorten time-to-revenue for multi-property rollouts. In B2C, curated assortments and in-home design support reduce returns and raise satisfaction. Across channels, robust warranties and after-sales service sustain reputation and repeat business in the hybrid flooring market.

Hybrid Flooring Industry Leaders

Mohawk Industries

Shaw Industries Group

Tarkett

Mannington Mills

CFL Flooring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Karndean Designflooring launched Knight Tile Quiet, its first gluedown luxury vinyl collection with enhanced acoustic performance, targeting build-to-rent and purpose-built student accommodation.

- April 2026: Tarkett introduced the iQ Motion homogeneous vinyl flooring range, featuring terrazzo-like speckled finishes in 16 natural tones with a 20-year warranty.

- December 2025: i4F acquired Beaulieu International Group's rigid core and LVT patent portfolio, comprising over 100 patents, consolidating intellectual property that licensees leverage to accelerate product development.

Global Hybrid Flooring Market Report Scope

| Stone Plastic Composite (SPC) Hybrid Flooring |

| Wood Plastic Composite (WPC) Hybrid Flooring |

| Rigid High-Density Fiberboard (HDF) Hybrid Flooring |

| Other Hybrid Cores (e.g., MgO, Bamboo Composite) |

| Floating / Click-Lock |

| Glue-Down / Loose-Lay |

| New Construction |

| Renovation & Remodel |

| Residential |

| Commercial |

| B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B / Contractors / Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (SG, MY, TH, ID, VN, PH) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product | Stone Plastic Composite (SPC) Hybrid Flooring | |

| Wood Plastic Composite (WPC) Hybrid Flooring | ||

| Rigid High-Density Fiberboard (HDF) Hybrid Flooring | ||

| Other Hybrid Cores (e.g., MgO, Bamboo Composite) | ||

| By Installation Method | Floating / Click-Lock | |

| Glue-Down / Loose-Lay | ||

| By Contruction Type | New Construction | |

| Renovation & Remodel | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B / Contractors / Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (SG, MY, TH, ID, VN, PH) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the hybrid flooring market size outlook through 2031?

The hybrid flooring market size is expected to increase from USD 28.48 billion in 2025 to 30.42 billion in 2026, and to USD 44.28 billion by 2031, at a 7.8% CAGR over 2026-2031.

Which product types lead growth within hybrid flooring?

SPC holds the largest installed base, while rigid high-density iberboard (HDF) Hybrid Flooring are projected to be the fastest growing at a 9.15% CAGR through 2031, driven by sustainability and IAQ priorities.

Which end-user segment is growing fastest?

Commercial is projected to grow at a 8.67% CAGR as facility managers emphasize lifecycle cost, acoustic compliance, and low-VOC documentation in procurement.

Where is the installation method in demand the strongest?

Click-and-lock floating systems dominate retrofit and occupied-space fit-outs due to their scheduling advantages and easier subfloor preparation. At the same time, glue-down remains favored in heavy-rolling-load zones.

Which regions anchor demand for hybrid flooring?

Asia-Pacific leads by share and is projected to post the fastest growth through 2031, while North America and Europe maintain steady demand under stricter acoustic and VOC requirements.

Page last updated on: