Market Overview

| Study Period | 2020 - 2031 |

|---|---|

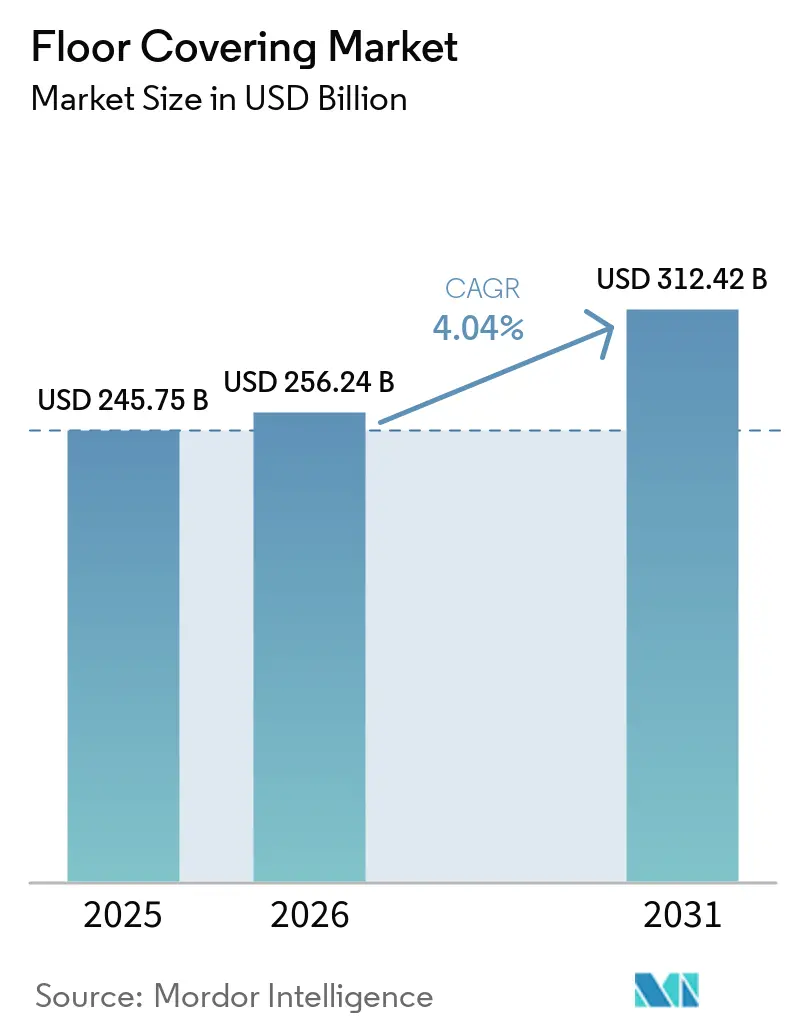

| Market Size (2026) | USD 256.24 Billion |

| Market Size (2031) | USD 312.42 Billion |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floor Covering Market Analysis by Mordor Intelligence

The floor covering market size is USD 245.75 billion in 2025, expected to reach USD 256.24 billion in 2026, and projected to rise to USD 312.42 billion by 2031, reflecting a 4.04% CAGR from 2026 through 2031. Growth in the floor covering market is balanced between resilient product innovation and changing end-market cycles, with vinyl and rigid-core formats gaining share on the strength of fast installs and moisture performance. Commercial demand is set to outpace residential as healthcare and education modernization drives durable, hygienic surfaces, while office and retail standards pivot toward flexible, low-maintenance systems. Supply chains in the market continue to regionalize under tariff pressure, with more domestic capacity coming online to reduce lead times and mitigate cost swings. Digital visualization and buy-online-pick-up-in-store models compress selection-to-install timelines, supporting a shift toward contractor-led fulfillment in larger, schedule-driven jobs.

Key Report Takeaways

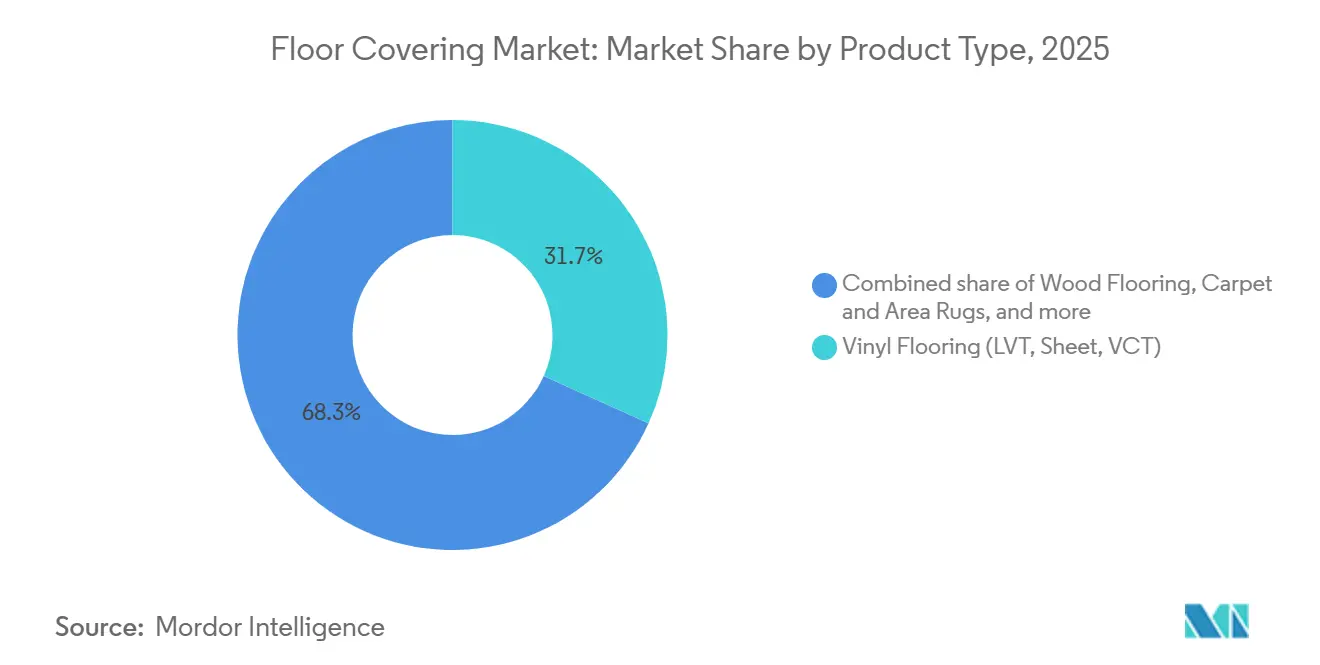

- By product type, vinyl flooring led with 31.73% share in 2025 in the floor covering market, while luxury vinyl tile is forecast to expand at a 6.13% CAGR through 2031.

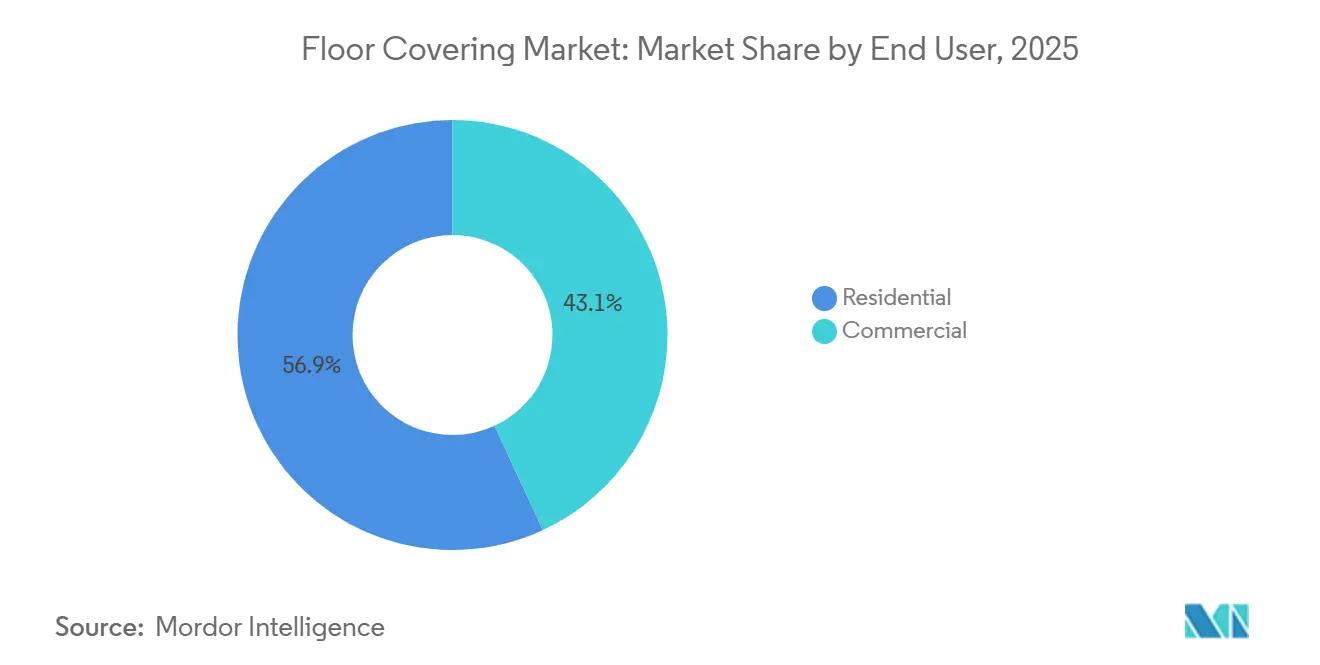

- By end user, residential held a 56.92% share in 2025 in the floor covering market, while commercial is projected to grow at a 5.74% CAGR through 2031.

- By distribution channel, B2C retail accounted for a 41.63% share in 2025 in the floor covering market, while contractor channels are projected to expand at a 4.72% CAGR through 2031.

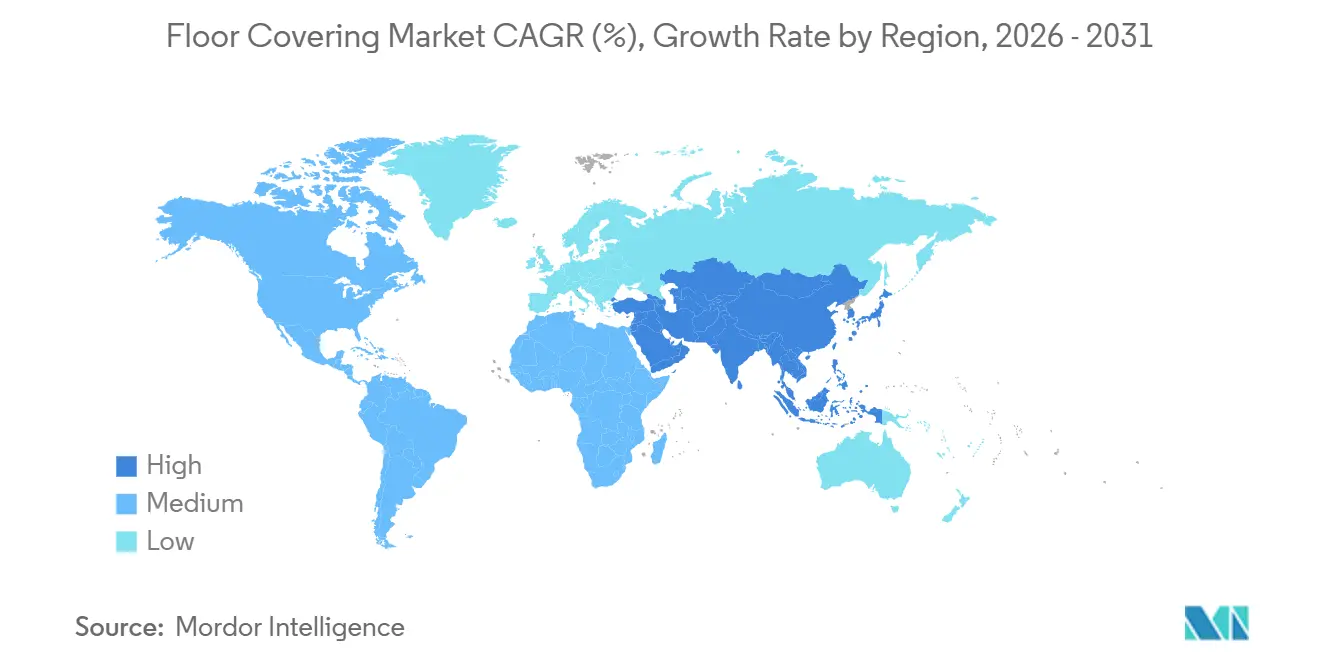

- By geography, Asia-Pacific led with a 37.13% share in 2025. The Middle East & Africa is projected to grow at a 5.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of LVT/SPC for durability, design, and faster installs | +1.2% | Global, with early gains in North America, Asia-Pacific, and emerging Middle East & Africa markets | Medium term (2-4 years) |

| Asia-Pacific new-builds and renovations sustaining tile and vinyl demand | +0.9% | Asia-Pacific core, spillover to Middle East infrastructure corridors | Long term (≥ 4 years) |

| Commercial modernization (healthcare, education, retail) favoring resilient floors | +0.8% | North America and Europe, with rising institutional projects in the Asia-Pacific | Medium term (2-4 years) |

| Omnichannel buying (BOPIS/online visualization) accelerating selection-to-install | +0.6% | Global, led by North America and Europe, with rising Asia-Pacific urban adoption | Short term (≤ 2 years) |

| Sustainability certifications influencing specifications | +0.5% | Europe and North America are primary, with selective Asia-Pacific adoption. | Long term (≥ 4 years) |

| Tariff-driven nearshoring resilient production is reshaping supply | +0.4% | North America's primary, secondary impacts in Latin America and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of LVT/SPC for Durability, Design, and Faster Installs

Luxury vinyl tile continues to scale on design realism, waterproof performance, and faster installation that reduces downtime for both residential and commercial retrofits. Stone plastic composite cores add dimensional stability and dent resistance, while high-fidelity digital printing lifts visual quality across wood and stone looks at accessible installed costs. Supply strategies are shifting as producers expand local capacity, which tightens lead times and stabilizes service for the floor covering market. AHF’s acquisition of a rigid-core factory in Cartersville, Georgia, adds 200 million square feet of domestic SPC capacity, signaling a pivot from import reliance to regional hubs for resilient formats. Shaw is investing USD 90 million to more than double SPC and LVT output in Ringgold, Georgia, by 2026, with specifications tuned for smaller runs and advanced textures that support premium positioning in the floor covering market[1]Shaw Industries Editorial Team, “Shaw Invests in Domestic Resilient Manufacturing,” Shaw Industries, shawinc.com. Speed remains a differentiator, as click-lock and tool-free assemblies enable same-day traffic and reduce skilled-labor bottlenecks across retrofit-heavy workloads in the market.

Asia-Pacific New-Builds and Renovations Sustaining Tile and Vinyl Demand

Asia-Pacific remains the largest regional base in the floor covering market, with demand buoyed by urban densification and a structural pivot from new-builds to renovations in key cities. China’s policy emphasis on quality-focused retrofits supports resilient surfaces that can be installed quickly with limited disruption in occupied buildings. India’s housing and infrastructure programs continue to lift the specification rate of durable, low-maintenance floors across public and private projects. Manufacturers are also placing new capacity in Southeast Asia to serve both local consumption and export lanes, which strengthens regional resilience in the market. Commercial sectors across Asia-Pacific are increasing the use of modular systems that simplify replacement while supporting lifecycle cost targets. This balance between retrofit and new construction should sustain tile and vinyl throughput across varied price points in the floor covering market.

Commercial Modernization (Healthcare, Education, Retail) Favoring Resilient Floors

Healthcare remains a leading commercial buyer due to infection-control mandates, rapid turnover of outpatient spaces, and maintenance efficiency priorities. The United States healthcare sector added 62,000 jobs in May 2025, far outpacing the 12-month average of 44,000, and that growth underpins consistent refurbishment activity in clinics and hospitals. BLS In education, projects focus on acoustics and durability, with heavy-traffic ratings and protective topcoats helping buildings manage large daily footfall and frequent reconfiguration. Corporate facilities consolidate footprints and invest in demountable, static-dissipative, and easy-repair flooring systems that align with hybrid work and data center needs. Indoor air quality frameworks are shaping specifications in Europe and North America, where public buyers and industry standards widely reference GREENGUARD Gold certification for total VOC emissions. UL Sustainability programs, such as closed-loop material recovery and PVC-free resilient platforms, are now central to procurement criteria and align with third-party documentation practices across the floor covering market.

Omnichannel Buying (BOPIS/Online Visualization) Accelerating Selection-to-Install

The floor covering market is moving toward faster, digital-supported journeys where visualization and BOPIS reduce decision friction and compress timelines to installation. Lowe’s acquisition of Artisan Design Group is designed to link online sampling, design collaboration, and installer dispatch for a more integrated path to purchase. Manufacturers and software providers are embedding 3D room configurators into dealer portals, which improves buyer confidence and helps lower returns by setting realistic expectations for color and texture. Retailers that reach higher digital-touchpoint penetration rates report stronger conversion, and the advantage compounds when sample logistics and installation scheduling are unified under one interface in the market. Product launches also leverage interactive visual tools, as seen with MSI’s portfolio, which aligns curated assortments to room-scene visualizers and on-trend graphics. As consumers spend more time online during early research and shortlisting, contractors benefit from clearer specifications and fewer change orders, reinforcing a shift of volume toward professional installation for time-sensitive projects in the floor covering market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material volatility (PVC resins, wood, ceramics) | -0.8% | Global, acute for PVC import exposure, and in regions where pricing power is limited | Short term (≤ 2 years) |

| Shortage of certified installers is driving up installed costs | -0.6% | North America is intensive, emerging in Western Europe | Medium term (2-4 years) |

| Regulatory scrutiny on PFAS/VOC and plastic waste | -0.4% | North America and Europe are the primary growth areas in Asia-Pacific | Long term (≥ 4 years) |

| End-of-life recycling constraints for multilayer floors | -0.3% | Europe and North America are primary limited to the Asia-Pacific infrastructure. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Volatility (PVC Resins, Wood, Ceramics)

Vinyl producers face resin cost uncertainty as policy changes alter trade economics and supply availability for the floor covering market. The removal of value-added tax rebates on PVC exports in China, effective April 1, 2026, tightened near-term supply and created incentives for export frontloading that disrupted normal flows[2]ICIS Market Reporting, “China Removes VAT Rebates on PVC Exports Effective April 2026,” ICIS, icis.com.In North America, new capacity from major suppliers increased competition and restrained contract price escalation for PVC through late 2024, tempering revenue recovery for producers with high input sensitivity in the market. Wood categories grapple with labor costs at mills and weather-related harvesting variability, while premium species scarcity inflates log prices and compresses downstream margins in engineered and solid formats. Ceramic inputs experience regional swings that extend lead times and complicate import planning during demand surges. Manufacturers respond with longer-term supply contracts, vertical compounding, and product reengineering, but capital requirements and qualification cycles can slow adoption rates for smaller players in the floor covering market.

Shortage of Certified Installers Driving Up Installed Costs

The installation workforce is aging and shrinking faster than vocational pipelines can replace it, which elevates installed-cost inflation for the floor covering market. According to the United States Bureau of Labor Statistics, about 112,300 flooring installers and tile and stone setters were employed in the United States in 2024, and the occupation is expected to generate around 8,400 openings annually over the next decade, largely due to retirements and workers exiting the trade. Wage differentials versus other licensed trades add to attrition pressure, and independent contractor status for many installers limits access to benefits that attract younger talent. As capacity tightens, dealer reports cite higher rates for glue-down resilient installs and longer scheduling windows, which makes lead-time reliability a competitive advantage for click-and-lock formats. Quality variability rises when less-experienced crews backfill demand, increasing callbacks, warranty claims, and reputational risk for retailers and brands in the market. Training programs are scaling but have yet to fully close the gap, so installation-friendly products with pre-attached underlayments and simplified locking systems see faster uptake in both residential and commercial renovations across the floor covering market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid-Core Innovation Drives Vinyl’s Dominance

Vinyl flooring held 31.73% of the floor covering market share in 2025 as rigid-core systems moved into both residential and commercial settings that need waterproofing, faster installs, and reliable dimensional stability. The floor covering market has leaned toward LVT formats where digital printing delivers lifelike visuals and protective coatings extend service life under abrasion and staining. Stone plastic composite designs helped expand use in moisture-prone areas such as kitchens and baths, while wood plastic composite remains a preferred option for projects emphasizing sound control and underfoot comfort. Ceramic and porcelain continue to serve heavy-traffic and premium design needs, though longer installs and grout maintenance temper their penetration into projects with strict schedules. In wood, engineered platforms captured more projects as locking systems and moisture-resistant cores improve stability over traditional solid, which remains constrained by log supply and mill economics. Suppliers with in-house compounding, embossing control, and faster changeover times are positioned to serve small-batch orders supporting premium selections for the floor covering market. Shaw’s capacity expansion in Georgia targets flexible runs, enhanced embossing, and tighter dimensional tolerances that support loose-lay specifications.

Growth is strongest where specification criteria pair waterproofing with click installation that avoids long cure times. The floor covering market size for LVT is projected to expand at a 6.13% CAGR between 2026 and 2031 as rigid-core platforms improve dent resistance and edge-lock performance. Commercial buyers favor resilient options for hygiene, repairability, and lifecycle cost control, while retailers curate SKU assortments around wood signatures and stone visuals supported by robust wear layers. AHF’s 200 million square feet of rigid-core capacity improves domestic availability and reduces exposure to ocean freight volatility. Across product types, closed-loop and low VOC innovations are opening doors in education and healthcare tenders that require EPDs and certified emissions labels. The floor covering market continues to consolidate around product attributes that shorten downtime, meet air quality standards, and improve total cost of ownership for institutional buyers.

By End User: Commercial Gains Outpace Residential’s Larger Base

Residential accounted for 56.92% of 2025 demand as replacement cycles and equity-funded remodels sustained a large installed base of homes. The floor covering market saw owners favor rigid-core waterproof products for kitchens, baths, and basements where moisture and wear drive earlier replacement, while value-focused buyers leaned into click-install options to offset labor shortages. Multifamily pipelines remain high, with about one million apartments in the construction stage during 2024, which indicates steady turnover and refresh cycles through mid-decade. Within new single-family and condo deliveries, schedule certainty and immediate occupancy favor floating installs and pre-finished surfaces. Home-center assortments focused on curated, on-trend visuals paired with warranties that address stains, dents, and impacts to build trust with DIY and pro customers.

Commercial, at 43.08% of 2025 volume, is growing faster than residential as healthcare and education projects accelerate. Flooring tied to healthcare accounted for a large portion of United States commercial sales in 2025, supported by the sector’s job growth and compliance requirements for infection control and cleaning efficacy. Education facility projects centered on acoustics and durable finishes with high-traffic ratings, while office programs prioritized flexible layouts and modular reconfiguration that accommodates hybrid work[3]U.S. Bureau of Labor Statistics, “Employment Situation News Release, May 2025,” U.S. Bureau of Labor Statistics, bls.gov. As a result, resilient and PVC-free platforms gained traction in bid specifications that blend performance, sustainability, and maintenance simplicity in the floor covering market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

B2C retail held 41.63% of 2025 volume as home centers and specialty stores stayed central to consumer discovery, tactile product assessment, and immediate availability for time-sensitive projects. Retailers increased investment in digital content, appointment scheduling, and in-home estimation services to reduce friction and accelerate conversion in the floor covering market. Contractor channels are expanding as builders, property managers, and institutional buyers source direct for large jobs with defined timelines and logistics needs. This channel shift reflects the growing weight of commercial and multifamily backlogs, where bundled design, delivery, and installation create value for buyers facing labor constraints.

Digital tools like 3D visualization and API integrations into dealer portals are elevating upstream confidence and reducing returns on color or texture mismatches. In contractor channels, e-procurement platforms and direct manufacturer portals are growing, with transaction volumes expected to expand as buyers seek transparency and integration with project management systems. Retailers are also adding protection plans in partnership with third-party providers to create ancillary revenue and differentiate customer experience in a pricing-sensitive environment. Product availability compliant with low VOC and PFAS-related rules is influencing assortment decisions in regulated states, which can steer buyers toward brands with nationwide eligibility[4]California Legislature, “AB 1817 and SB 682 Text and Status,” California Legislative Information, leginfo.legislature.ca.gov. The floor covering market continues to rebalance toward models that align selection, logistics, and installation under coordinated workflows to offset installer constraints and schedule complexity.

Geography Analysis

Asia-Pacific holds the largest regional position with a market share of about 37.13% in the floor covering market, anchored by urban density and sustained renovation needs in Tier 1 and Tier 2 cities. In China, policy emphasis on quality and urban renewal supports resilient formats that install quickly in occupied buildings, while in Southeast Asia, manufacturing investment is creating new bases that serve both local and export demand. Demand for modular, easy-repair surfaces is consistent in commercial spaces that value durability and quick turnaround between tenant moves. In North America, a high pipeline of multifamily units under construction indicates steady refreshing cycles for leasing and turnover programs through mid-decade. Healthcare and education continue to anchor commercial specification activity, with documented hygiene and air quality credentials shaping product selection in the floor covering market. Capacity additions in the United States by Shaw and others are shortening lead times and strengthening supply continuity, which helps contractors maintain schedules.

Europe’s renovation-led demand is governed by stringent indoor air standards and sustainability documentation, which elevate requirements for GREENGUARD Gold, EPDs, and PVC-free alternatives in public procurement. Brands with robust take-back programs and circular designs are gaining preference in tenders that reward verified recovery and low embodied carbon. Modular resilient systems and carpet tile with acoustic underlays remain prevalent in corporate and institutional applications that prioritize noise reduction and reconfiguration. Retail and hospitality refits continue to adopt resilient surfaces that meet slip-resistance thresholds and are easy to maintain under high footfall in the floor covering market. Ceramic tile remains a key export for Southern European producers, with shipments serving the United States demand despite domestic renovation softness. As carbon-border measures mature, regional manufacturing may gain further relative advantage in public sector bids that account for transport emissions in total project scoring.

The Middle East & Africa records the fastest pace among regions, with the floor covering market growing at a 5.72% CAGR through 2031 on project pipelines in Western Asia and infrastructure demand in key African economies. Hospitality and mixed-use developments in the Gulf feature premium resilient and ceramic systems rated for extreme temperatures and slip resistance under public assembly codes. Public procurement in the GCC increasingly references ISO and LEED-aligned documentation, strengthening the case for brands with comprehensive third-party credentials. In South America, construction activity is recovering, with residential segments anchor demand and public infrastructure supporting commercial volumes where budget cycles permit. Regional tariff shifts, including higher import taxes on PVC in Brazil in late 2024, influence resin costs and can affect mix and pricing for resilient platforms in the floor covering market. Over the forecast horizon, regionalization strategies and documented sustainability performance will shape competitive standing as buyers weigh compliance, risk, and lifecycle cost in procurement.

Competitive Landscape

The floor covering market is highly fragmented, with thousands of manufacturers competing across regional bases and product niches, and no single brand near a controlling position. Suppliers differentiate through vertical integration, speed to market, and compliance credentials, as buyers elevate documentation and service reliability in selection criteria. Domestic manufacturing investments are central to resilient categories, where large United States plants in Georgia add scale and flexibility in SPC and LVT to compete with imports. AHF’s Georgia rigid-core facility provides major domestic capacity for SPC, reinforcing a pivot toward regional production hubs that improve lead times and mitigate tariff exposure. Sustainability leadership remains a key axis of competition, with PVC-free resilient formats and carbon-reduction roadmaps gaining weight in institutional bids across the floor covering market.

Consolidation in distribution and preparation materials supports better contractor service, with leading adhesives and subfloor brands aligning logistics and technical support to jobsite timelines. Sika’s full ownership of Schönox in North America increases cross-selling opportunities and positions its portfolio for integrated solutions alongside resilient installers and commercial contractors. Retail ecosystems are also consolidating solution pathways, as seen in Lowe’s acquisition of Artisan Design Group to integrate design, distribution, and installation workflows under one umbrella. Digital enablers are critical, with 3D configuration and visualization tools embedded into dealer portals so customers can preview colorways, textures, and layouts and reduce returns, which increases net conversion in the floor covering market.

Product innovation focuses on wear performance, acoustic management, and assembly systems that reduce reliance on scarce skilled labor. Expanded embossing libraries and deeper wear layers support premium pricing in retail, while antimicrobial coatings and static-dissipative features align with healthcare and data center requirements. Suppliers publish more third-party documentation and maintain certifications such as GREENGUARD Gold to meet public procurement policies in Europe and North America. Public and private owners are increasing lifecycle expectations and requesting take-back options, which positions companies with established reclamation programs and circular designs for share gain. These dynamics reward scale, documented quality systems, and operational agility, while the absence of a dominant player ensures that regional specialization and service continue to play a decisive role in the floor covering market.

Floor Covering Industry Leaders

Mohawk Industries

Tarkett SA

Shaw Industries Group, Inc.

Grupo Lamosa

Victoria PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Mannington Mills announced its strategic decision to exit the residential carpet business, redirecting resources toward growth and innovation in luxury vinyl, hardwood, laminate, and commercial flooring categories to sharpen competitive positioning in resilient and hard-surface segments.

- February 2026: MSI launched the Nove Collections (Nove, Nove Plus, Nove Reserve) featuring extra-wide 9"×48" glue-down luxury vinyl tile planks with CrystaLux protection layers ranging from 6 MIL to 22 MIL Ultra wear, delivering durability and on-trend blonde and medium wood visuals across three performance tiers.

- February 2026: Capital Carpet & Flooring acquired Business Interiors Floor Covering to expand commercial capabilities with a combined 40,000-square-foot logistics and inventory facility and deeper presence in luxury hotels, law firms, and biotechnology installations.

- January 2026: Versatrim acquired Artistic Finishes to unify a portfolio of floor moldings, stair solutions, and accessories for retailers and installers seeking comprehensive trim systems.

Global Floor Covering Market Report Scope

Any material used to provide a walking surface over a floor structure is referred to as a floor covering. It may also relate to the surface covering the subflooring structure or the fundamental floor. The floor-covering market is segmented by product, end-user, distribution channel, and geography. By product, the market is segmented into carpet and area rugs, wood flooring, ceramic tiles flooring, laminate flooring, vinyl flooring, stone flooring, and others. By end user, the market is segmented into commercial and residential. By distribution channel, the market is segmented into home centers, flagship stores, specialty stores, online stores, and other distribution channels. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and Middle East & Africa. The report also covers the market sizes and forecasts for the floor-covering market in value (USD) for all the above segments.

By Product Type

| Carpet & Area Rugs |

| Wood Flooring |

| Ceramic & Porcelain Tiles |

| Laminate Flooring |

| Vinyl Flooring (LVT, Sheet, VCT) |

| Stone Flooring |

| Other Products |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Carpet & Area Rugs | |

| Wood Flooring | ||

| Ceramic & Porcelain Tiles | ||

| Laminate Flooring | ||

| Vinyl Flooring (LVT, Sheet, VCT) | ||

| Stone Flooring | ||

| Other Products | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

Which product category is driving the fastest growth in the floor covering market?

Luxury vinyl tile within resilient formats is the fastest-growing category, supported by rigid-core assemblies that deliver waterproof performance and faster installs relative to legacy surfaces.

Which end market is expected to grow fastest in the floor covering market through 2031?

Commercial is expected to grow faster than residential, with healthcare and education leading specification activity due to hygiene standards and modernization programs.

How are tariffs and nearshoring changing the floor covering market supply base?

Late-2025 tariffs on selected imports are accelerating United States investments in SPC and LVT, cutting lead times and reducing import exposure for resilient formats.

What certifications increasingly influence product selection in the floor covering market?

GREENGUARD Gold emissions labels and EPDs are baseline requirements in many public bids, with additional scrutiny on PFAS and low VOC compliance in regulated markets.

How do digital tools affect buyer decisions in the floor covering market?

Visualization and 3D configuration tools boost purchase confidence and reduce returns, while BOPIS and integrated installer dispatch shorten selection-to-install timelines.

Page last updated on: