Market Overview

| Study Period | 2021 - 2031 |

|---|---|

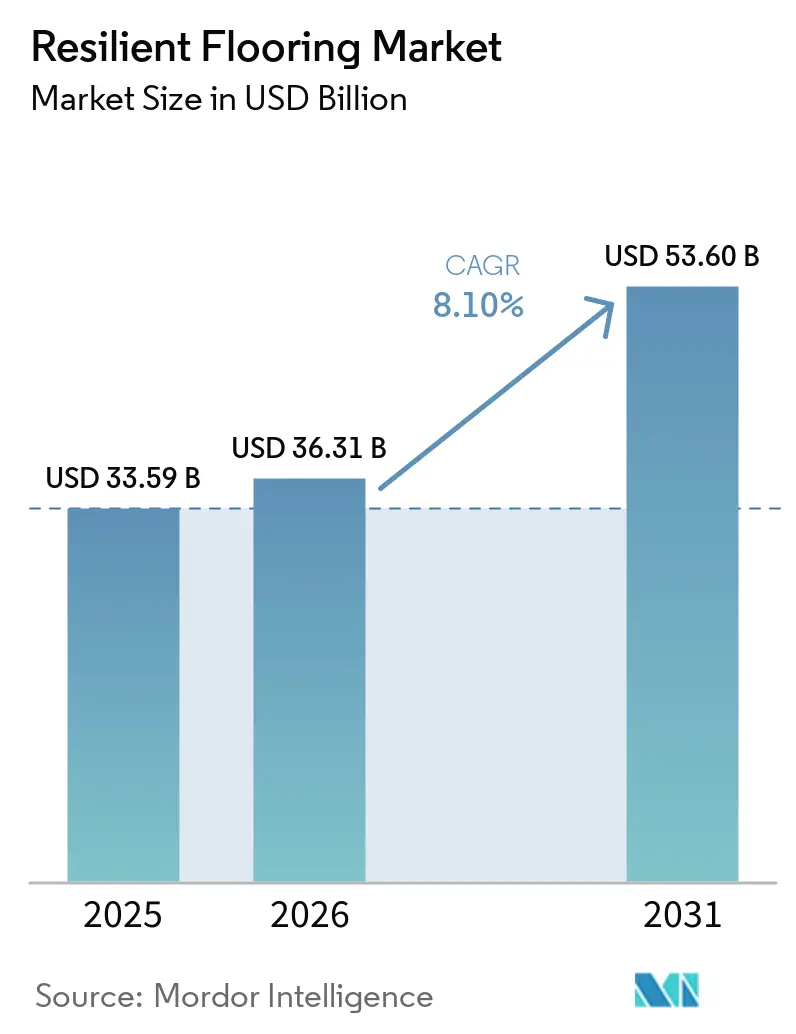

| Market Size (2026) | USD 36.31 Billion |

| Market Size (2031) | USD 53.60 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

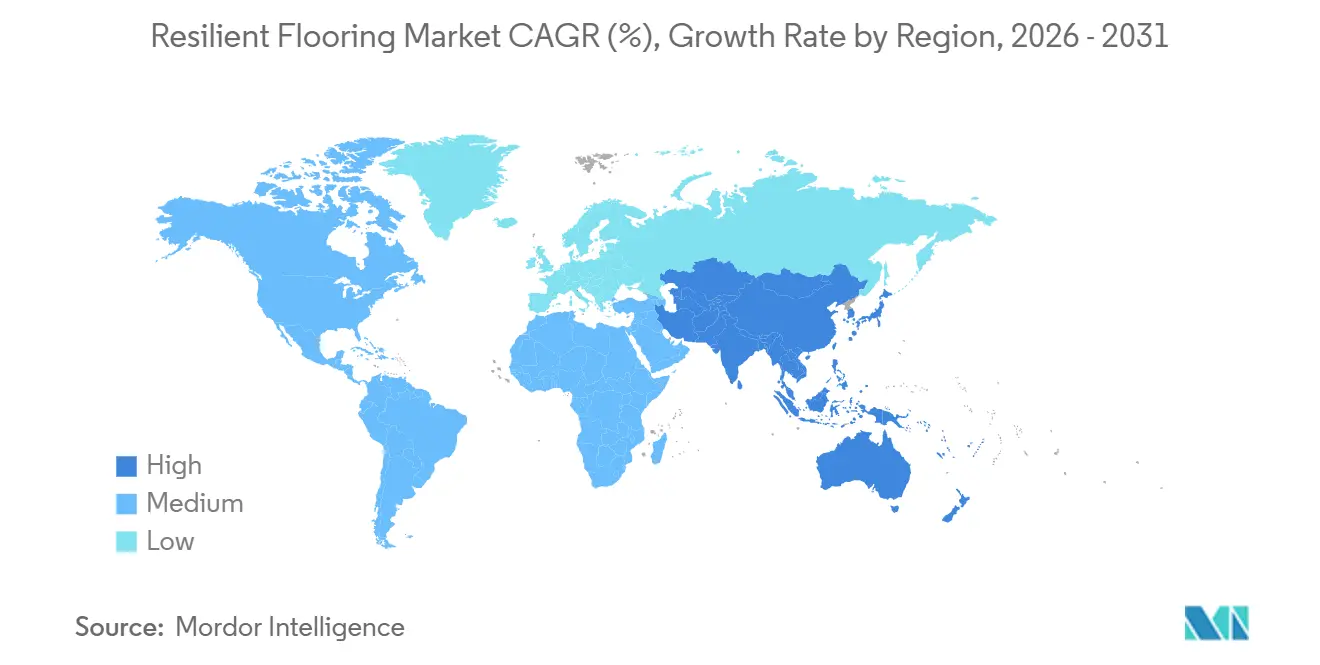

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

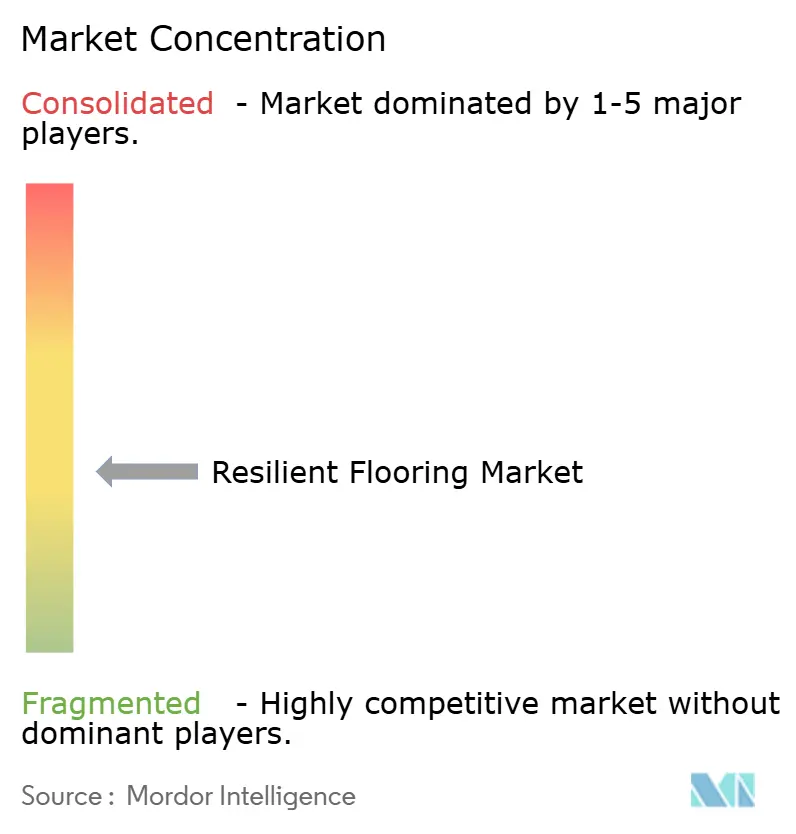

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resilient Flooring Market Analysis by Mordor Intelligence

The Resilient Flooring Market size is expected to grow from USD 33.59 billion in 2025 to USD 36.31 billion in 2026 and is forecast to reach USD 53.60 billion by 2031 at 8.10% CAGR over 2026-2031. Luxury vinyl tile (LVT) is the prime catalyst because it merges rapid installation with a wide design palette. Rigid-core formats such as stone plastic composite (SPC) and wood plastic composite (WPC) have shortened project schedules, driving contractor adoption while unlocking a do-it-yourself retail channel. Regulatory pressure on volatile-organic-compound (VOC) and phthalate content is pushing manufacturers toward low-emission formulations, increasing capital needs but also opening space for higher-value products. Asia-Pacific will remain the largest demand center thanks to housing and infrastructure stimulus, whereas North America is set to benefit from strong remodeling and flexible-office build-outs. Competitive strategies are tilting toward vertical integration and circular-economy initiatives that differentiate beyond price.

Key Report Takeaways

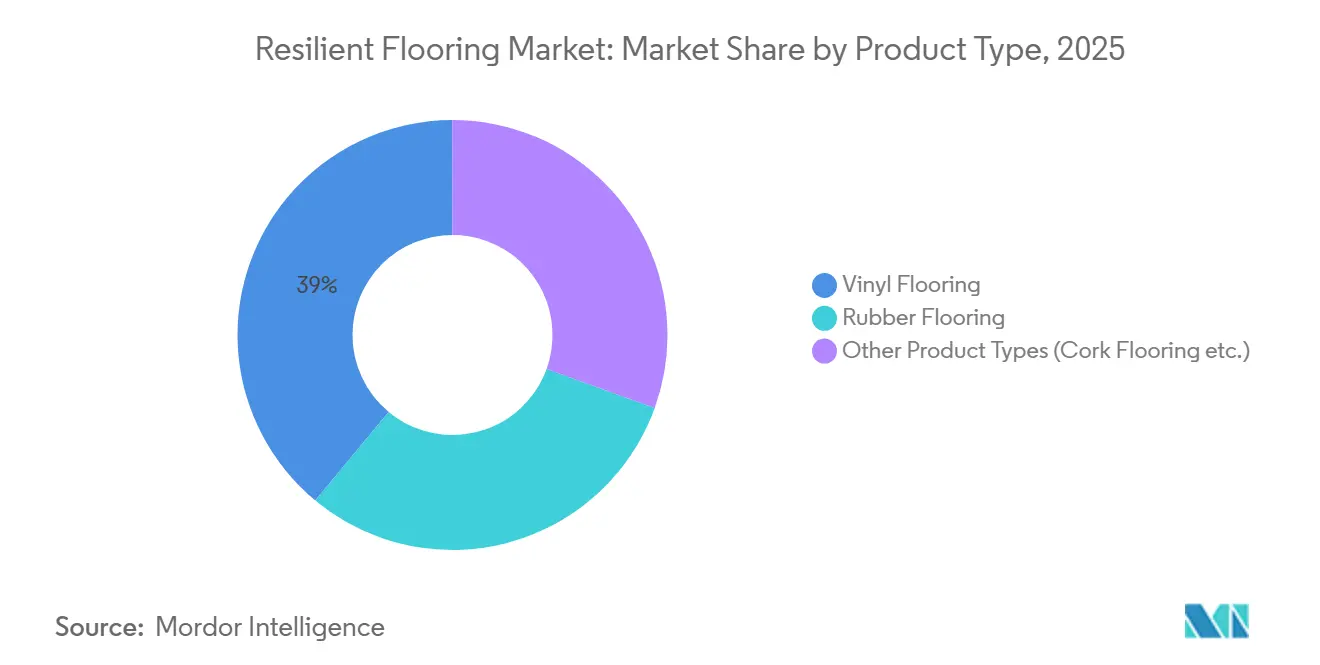

- By product type, vinyl flooring held a 38.98% resilient flooring market share in 2025 and is projected to post the fastest growth at a 9.85% CAGR through 2031.

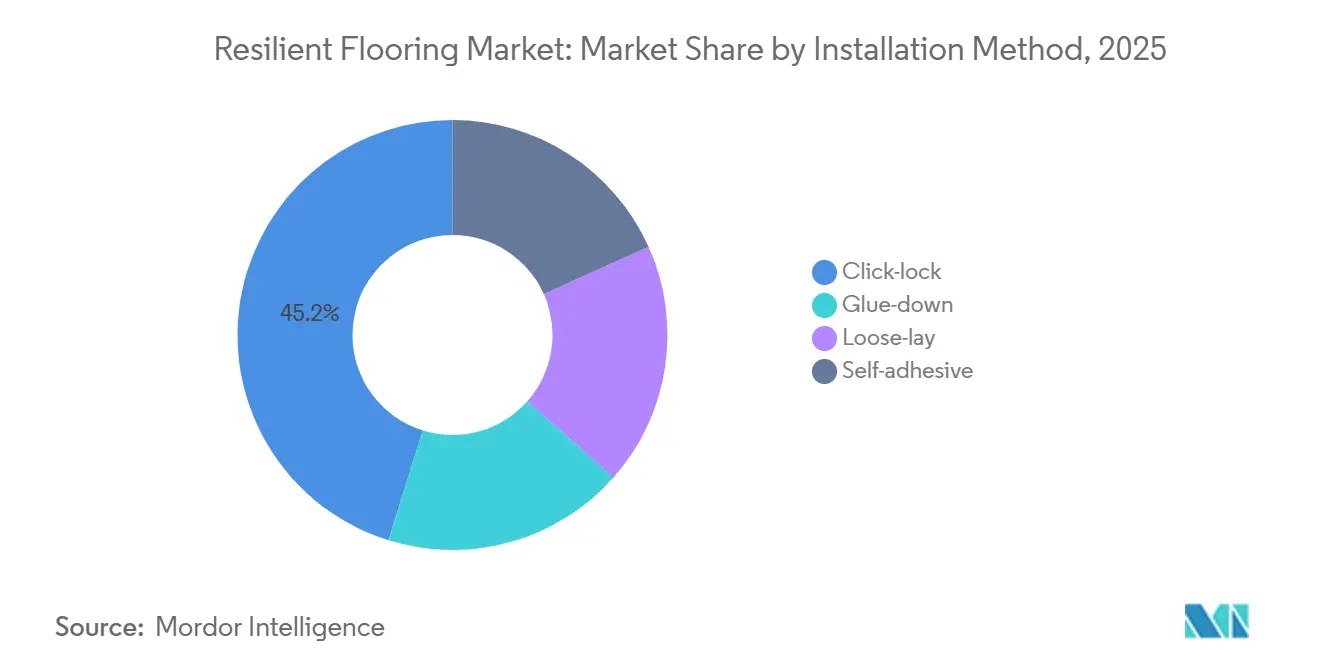

- By installation method, click-lock captured 45.19% of the resilient flooring market share in 2025 and is projected to expand at a 9.10% CAGR to 2031.

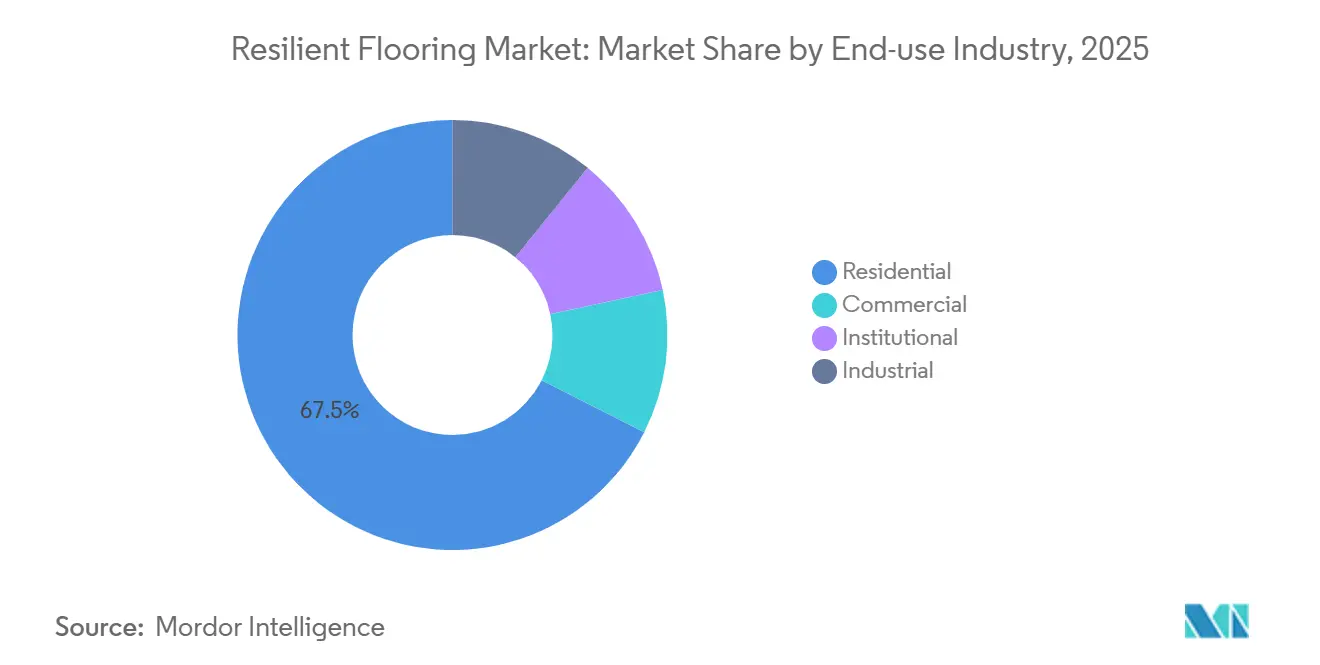

- By end-use industry, residential commanded 67.54% of the resilient flooring market size in 2025, while commercial is projected to grow at an 8.96% CAGR through 2031.

- By geography, Asia-Pacific accounted for 47.21% of demand in 2025; the region is anticipated to progress at an 8.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Resilient Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Penetration of Luxury Vinyl Tile (LVT) | +1.8% | Global, with concentration in North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Surge in Residential DIY Renovation Via Click-Lock Rigid-Core Products | +1.5% | North America, Europe, Australia | Short term (≤ 2 years) |

| APAC Housing and Infrastructure Stimulus Programmes | +2.1% | APAC core (China, India, Vietnam, Indonesia), spill-over to Middle East | Long term (≥ 4 years) |

| Growing Application of Resilient Vinyl Flooring in Commercial Spaces | +1.3% | Global, with emphasis on healthcare, retail, hospitality in developed markets | Medium term (2-4 years) |

| Leasing Models for Office Fit-Outs Driving High-Turnover Installs | +0.9% | North America, Europe, select APAC financial hubs (Singapore, Hong Kong) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of Luxury Vinyl Tile (LVT)

Rigid-core technology eradicates acclimation delays, allows direct installation over imperfect substrates, and reduces labor by 20-25% in the multifamily segment. Limestone-rich SPC cores resist telegraphing, while advanced embossing reproduces premium hardwood visuals at one-third the installed cost. Click-lock edges keep retail sites operational during overnight renovations and have displaced ceramic tile in wet areas of healthcare environments where swift turnover matters.

Surge in Residential DIY Renovation Via Click-Lock Rigid-Core Products

Home-improvement chains raised click-lock stock-keeping units by roughly 40% between 2024 and 2025, mirroring a spike in tutorial views for leading brands. Minimal tooling requirements empower homeowners, who subsequently refresh floors more often, generating repeat traffic for retailers. This DIY momentum now represents nearly one-third of U.S. residential volume.

APAC Housing and Infrastructure Stimulus Programmes

India earmarked INR 11.11 trillion for infrastructure in fiscal 2025-26, channeling funds to urban housing that prioritizes low-VOC finishes eligible for green-building credits[1]Government of India, “Union Budget 2025-26,” indiabudget.gov.in . Parallel measures in China released CNY 2 trillion to stabilize real-estate markets, propelling resilient flooring demand in tier-2 and tier-3 cities.

Growing Application of Resilient Vinyl Flooring in Commercial Spaces

Updated guidance from the Centers for Disease Control and Prevention favors seamless, non-porous surfaces, accelerating antimicrobial vinyl adoption in hospitals. Silver-ion infused ranges now guarantee bacteriostatic performance for up to 10 years, lowering total cost of ownership and shortening maintenance windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and Phthalate Regulations on PVC Products | -1.2% | Global, with most stringent enforcement in EU, North America, select APAC markets (Japan, South Korea) | Medium term (2-4 years) |

| Competition from Ceramic Tile and Engineered Wood | -0.8% | Global, with ceramic tile pressure in Middle East, engineered wood in North America and Europe | Long term (≥ 4 years) |

| Shortage of Certified Installers in Several Countries | -0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Phthalate Regulations on PVC Products

The U.S. Environmental Protection Agency’s December 2024 vinyl chloride review prefigures tougher controls that raise compliance costs[2]U.S. Environmental Protection Agency, “Risk Evaluation for Diisodecyl Phthalate,” epa.gov . Europe’s Regulation 923/2023 bans lead-based stabilizers from January 2026, lifting raw-material bills by 5-8% as producers shift to calcium-zinc systems. Similar emission limits in China trigger factory audits and recalls for non-conforming imports.

Competition from Ceramic Tile and Engineered Wood

Large-format inkjet-printed porcelain planks and three-ply engineered wood have narrowed installed-price gaps, especially where underfloor heating favors tile’s thermal conductivity. In U.S. education projects, ceramic still enjoys a 30-year service-life reputation, challenging vinyl on long-term value perceptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vinyl Strengthened by Rigid-Core Innovation

Vinyl flooring accounted for 38.98% of the resilient flooring market in 2025 and will post a 9.85% CAGR to 2031. This trajectory underscores how SPC and WPC planks are overcoming sheet vinyl’s subfloor demands while adding photorealistic visuals. Limestone fillers' demand rose as SPC volumes ballooned. Rubber remains a niche for fitness and transport settings, whereas linoleum attracts eco-centric specifiers despite its lengthier curing period. A boutique cork segment thrives on acoustic comfort but lags under heavy static loads.

Innovation is blurring material boundaries. Bio-attributed PVC feedstocks now feed mass-balance programs, and recycled-content formulations such as an 85% post-consumer blend qualify for multiple green-building points. The resilient flooring market size for vinyl is projected to widen faster than any alternative product because it absorbs embossing, waterproof cores, and antimicrobial additives more swiftly than rubber or linoleum can integrate comparable upgrades.

By Installation Method: Click-Lock Makes Labor a Variable, Not a Bottleneck

Click-lock held 45.19% of 2025 demand and is projected to grow at a 9.10% CAGR by eliminating wet trades and reducing project duration by up to half. Capital outlays for high-precision profiling machinery reached USD 2-5 million per line during the 2023-2025 expansion cycle. Glue-down keeps relevance in healthcare and education where bond permanence is critical, but its share is sliding as pressure-sensitive adhesives enable future uplift. Loose-lay is gaining in data centers for underfloor-cable access, and self-adhesive tiles target rental units needing rapid turnover.

The resilient flooring market size for click-lock installations will widen as retailers position them as entry-level DIY solutions and commercial contractors favor their reusability. This democratizes premium aesthetics, lowering reliance on an increasingly scarce skilled-installer pool.

By End-Use Industry: Residential Remains Dominant, Commercial Captures Momentum

Residential demand represented 67.54% of the resilient flooring market in 2025, a testament to homeowners’ appetite for hardwood and stone replicas without upkeep burdens. However, the commercial segment is forecast to grow fastest at an 8.96% CAGR to 2031. Healthcare facilities are paving corridors with antimicrobial vinyl under stricter infection-control regimes, while retailers note maintenance-call reductions after switching from ceramic tile. Hospitality specifies waterproof planks to eliminate grout maintenance in guest bathrooms.

Institutional buyers still lean toward homogeneous sheet for its weldable seams across vast spaces, and industrial sites pay premiums for static-dissipative or conductive options compliant with IEC 61340-5-1. Yet the resilient flooring market share delta between residential and commercial will narrow as office landlords favor replaceable solutions aligned with flexible leases.

Geography Analysis

Asia-Pacific held 47.21% of the resilient flooring market in 2025 and is advancing at an 8.76% CAGR through 2031. Indian infrastructure outlays and China’s property-sector stabilization are principal engines, while Vietnam attracts foreign direct investment that adds regional manufacturing heft. Mature economies such as Japan and South Korea register steady retrofit demand tied to aging demographics.

North America benefits from a buoyant remodeling cycle and flexible-office fit-outs. U.S. home-improvement retailers boosted click-lock SKUs by 40% from 2024 levels, underscoring DIY traction. Canada’s public-works pipeline sustains institutional demand despite labor constraints, and Mexico’s near-shoring wave fuels industrial installations along border corridors.

Europe balances renovation opportunities against the compliance costs of stringent VOC rules. Germany, the United Kingdom, and France top per-capita consumption, while Nordic nations adopt bio-based linoleum quickly. Southern Europe sustains ceramic tile’s cultural dominance, limiting vinyl’s residential penetration but embracing LVT in fast-track commercial refurbishments.

South America and the Middle East-Africa contribute emerging-market upside. Brazil’s federal housing programs support modest rebounds, whereas Saudi Arabia’s Vision 2030 megaprojects specify resilient flooring for hospitality components. The United Arab Emirates sees ongoing demand in retail precincts post-Expo 2020, and South Africa retains steady industrial requisitions amid import competition.

Competitive Landscape

Five global leaders - Tarkett, Mohawk Industries, Shaw Industries, Gerflor, and AHF Products - collectively control roughly 35-40% of sector revenue, leaving space for agile regional brands. Tarkett’s November 2024 purchase of Tarkett Sports widened its portfolio into athletics, capturing higher-margin niches. Mohawk’s consolidation of LVT production during Q3 2024 lowered fixed costs and funded USD 25 million in automated profiling to counter private-label incursions.

Technology is the new battleground. Sensor-embedded floors now relay foot-traffic data for predictive maintenance, cutting lifecycle spending by up to 20% over a decade. Patent filings around click-lock edges rose 25% year-on-year in 2024, and antimicrobial coatings have become a differentiator in healthcare bids. Design-oriented challengers like Karndean routinely launch 50-plus patterns each year, preempting commoditization and serving boutique hospitality accounts.

Circular-economy positioning is gaining traction. Take-back programs harvest post-consumer PVC for mechanical recycling, and bio-attributed feedstocks underpin low-carbon marketing claims. Firms lacking reinvestment capacity for low-VOC chemistry and automated lines face consolidation pressures, suggesting the resilient flooring market will tilt gradually toward better-capitalized stakeholders.

Resilient Flooring Industry Leaders

Tarkett

Mohawk Industries, Inc.

Shaw Industries Group, Inc.

AHF Products

Gerflor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Interface, Inc. launched three new resilient flooring products, expanding the range of color, design, and aesthetic options in the category. The launch featured two new LVT styles, "In The Mix" and "Raw Materials," along with an updated version of the company’s norament xp rubber products.

- July 2024: AHF Products introduced its latest resilient flooring solution, Ingenious Plank, across several of its brands, including Armstrong Flooring, Bruce, and Robbins. The core of this product is made from natural wood fibers encapsulated in a high-performance resin, making it 40% lighter than traditional rigid core products, which facilitates easier handling and installation.

Global Resilient Flooring Market Report Scope

Resilient flooring is usually a mixture of fillers, binders, and colors. Filler materials can include synthetic fibers, ground wood, or limestone, and the material that binds the mixture together is either asphalt or resin.

The resilient flooring market is segmented by product type, installation method, end-use industry, and geography. By product type, the market is segmented into vinyl flooring, rubber flooring, and other product types (cork flooring, etc.). By installation method, the market is segmented into click-lock, glue-down, loose-lay, and self-adhesive. By end-use industry, the market is segmented into residential, commercial, institutional, and industrial. The report also covers the market size and forecasts for resilient flooring in 23 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Vinyl Flooring |

| Rubber Flooring |

| Other Product Types (Cork Flooring etc.) |

By Installation Method

| Click-lock |

| Glue-down |

| Loose-lay |

| Self-adhesive |

By End-use Industry

| Residential |

| Commercial |

| Institutional |

| Industrial |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Qatar | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Vinyl Flooring | |

| Rubber Flooring | ||

| Other Product Types (Cork Flooring etc.) | ||

| By Installation Method | Click-lock | |

| Glue-down | ||

| Loose-lay | ||

| Self-adhesive | ||

| By End-use Industry | Residential | |

| Commercial | ||

| Institutional | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Vietnam | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Qatar | ||

| Nigeria | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the resilient flooring market?

The resilient flooring market size stands at USD 36.31 billion in 2026 and is forecast to expand at an 8.10% CAGR to reach USD 53.60 billion by 2031.

Which product type leads global revenue?

Vinyl flooring, bolstered by rigid-core technology, held a 38.98% market share in 2025.

Why are click-lock planks gaining popularity?

Click-lock formats cut installation time by up to 50%, require no adhesives, and fit DIY budgets.

Which region contributes the largest demand?

Asia-Pacific accounted for 47.21% of 2025 demand and will maintain the fastest regional CAGR at 8.76%.

Page last updated on: