Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

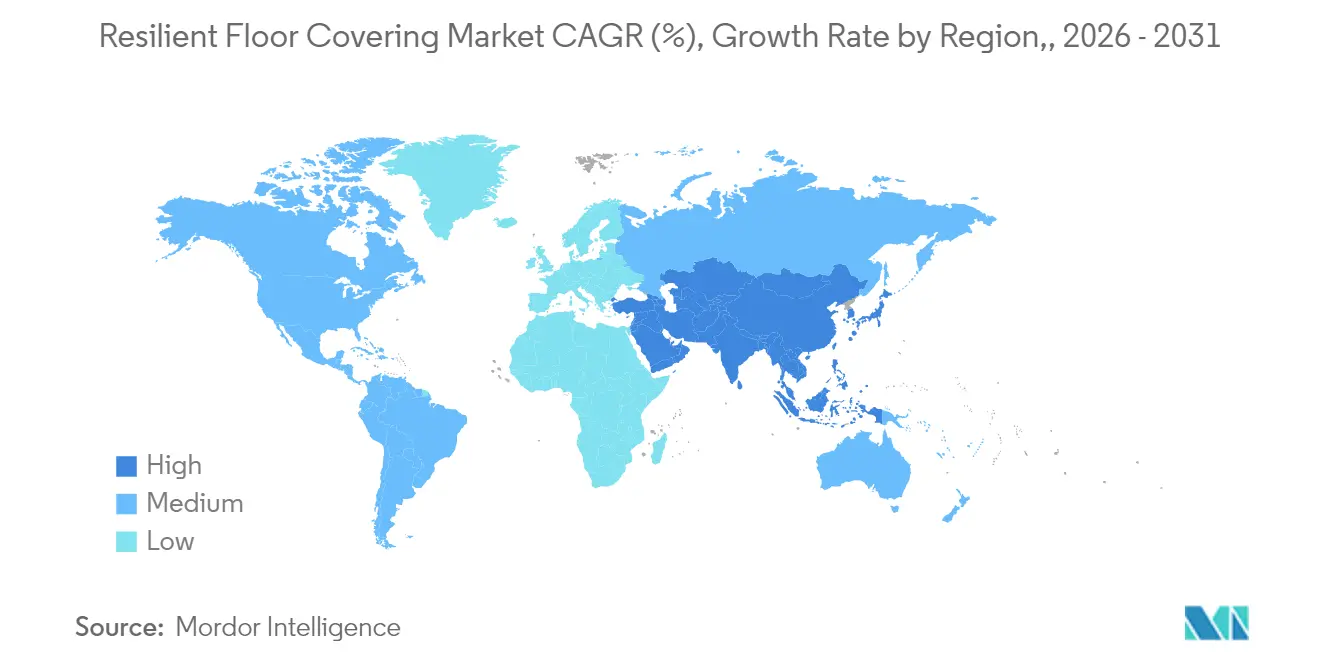

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

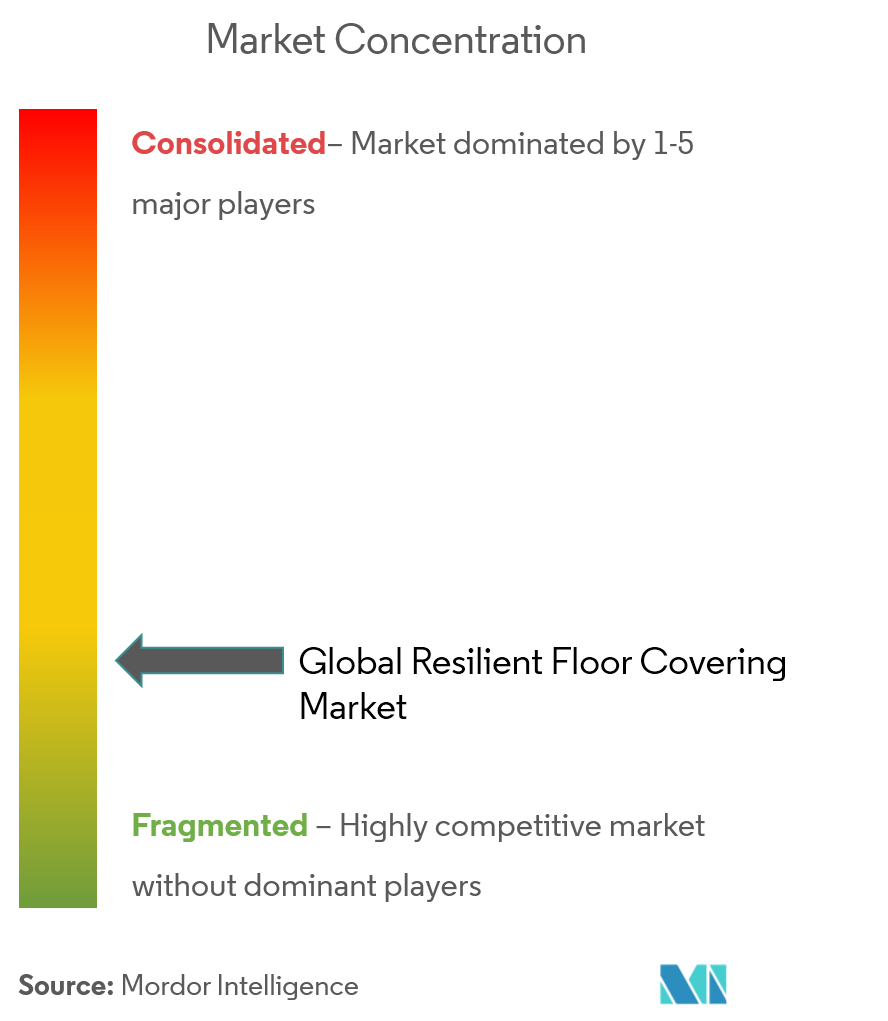

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resilient Floor Covering Market Analysis by Mordor Intelligence

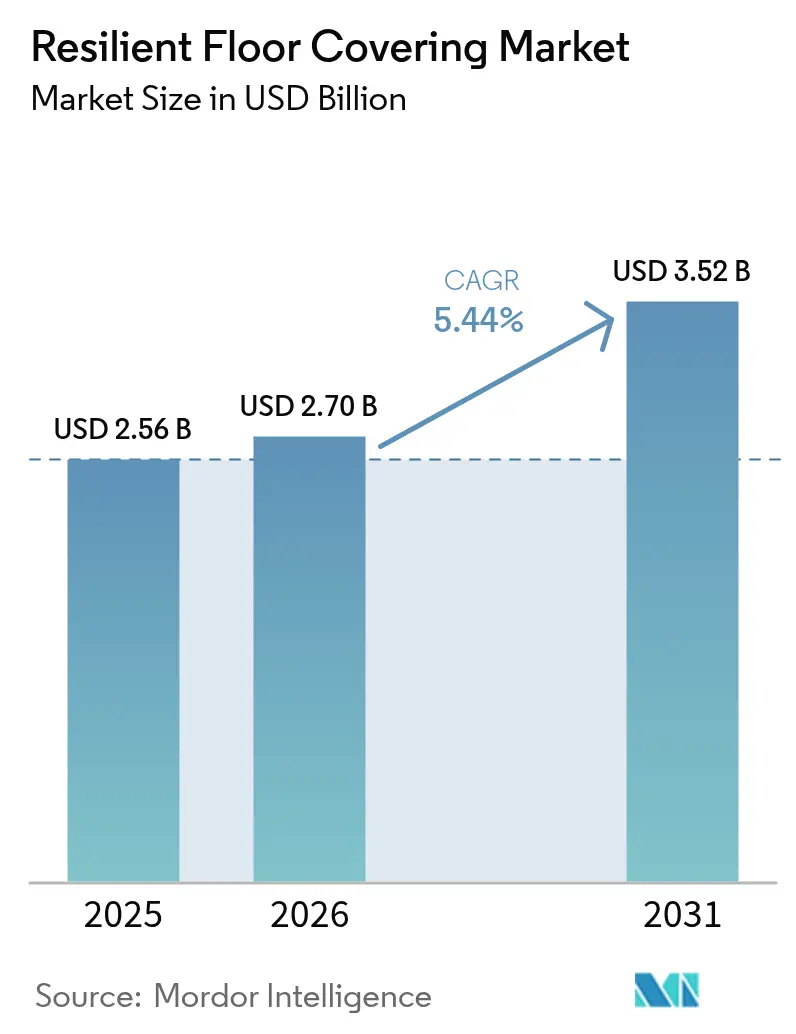

The resilient floor covering market size was valued at USD 2.56 billion in 2025 and estimated to grow from USD 2.7 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031). Consistent demand stems from luxury vinyl tile (LVT) upgrades in homes, an expanding healthcare construction pipeline in Asia-Pacific, and steady product innovation that keeps resilient flooring competitive against ceramics, laminate, and hardwood. Digital printing, embossed-in-register texturing, and rigid-core engineering have expanded design choices and improved impact resistance, while PVC-free options strengthen environmental credentials without eroding performance. The U.S. Environmental Protection Agency issued a draft risk evaluation for DINP plasticizer, citing potential human-health risks under certain use conditions[1]Source: Environmental Protection Agency, “Draft Risk Evaluation for Diisononyl Phthalate (DINP),” epa.gov. Supply-chain shifts toward near-shore production in North America and Europe are reducing tariff exposure and lead times, making localized inventory easier to manage. Climate-driven building codes that emphasize water resistance and easy sanitation further reinforce adoption, positioning the resilient floor covering market as a reliable growth segment within the wider finishes sector.

Key Report Takeaways

- By product type, luxury vinyl tile accounted for 29.94% of revenue in 2025; stone plastic composite is projected to expand at an 8.22% CAGR to 2031 in the resilient floor covering market.

- By installation type, glue-down solutions held 46.12% of the resilient floor covering market share in 2025, while click-lock systems recorded the highest projected CAGR at 7.63% through 2031.

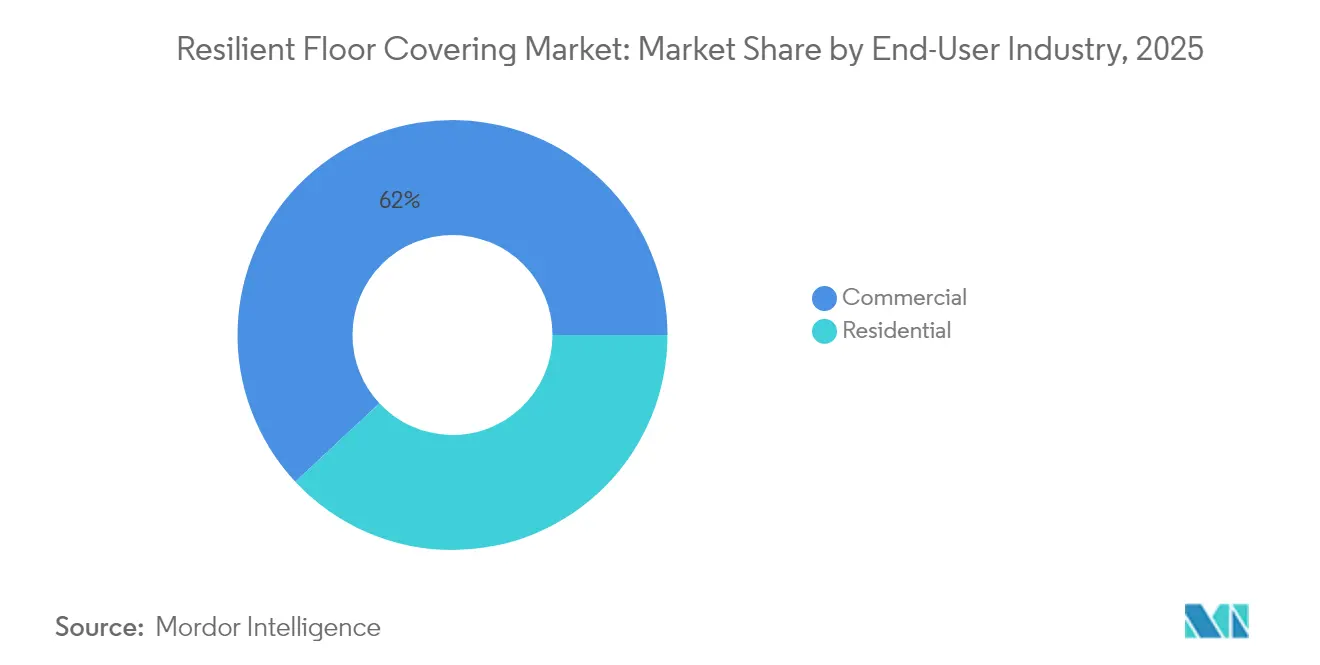

- By end-user, the residential segment accounted for 38.05% of the resilient floor covering market size in 2025 and is advancing at an 8.09% CAGR through 2031.

- By geography, Europe commanded 31.70% of global revenue in 2025; Asia-Pacific is set to grow the fastest at a 9.03% CAGR to 2031.

- Mohawk Industries, Tarkett, Shaw Industries, Armstrong Flooring, and Mannington Mills hold significant market share in 2024, leaving space for mid-tier specialists.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resilient Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of LVT in Residential Remodels | + 0.7% | North America, Europe, Australia | Short term (≤ 2 years) |

| Healthcare Build-out in Asia-Pacific Requiring Hygienic, Slip-Resistant Floors | + 0.6% | Asia-Pacific, particularly China, India, Asia-Pacific | Medium term (2-4 years) |

| Waterproof SPC/WPC Demand for Climate-Resilient Housing | + 0.5% | Global, with concentration in coastal and flood-prone regions | Medium term (2-4 years) |

| Digital Printing and EIR Finishes Elevating Aesthetics | + 0.4% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Low-VOC Regulations Fueling Eco-Labelled Resilient Materials | + 0.3% | Europe, North America, developed Asia-Pacific | Medium term (2-4 years) |

| Circular Linoleum and PVC Take-Back Boosting Green Certifications | + 0.2% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of LVT in Residential Remodels

Home renovation remains the primary demand engine for LVT. Homeowners choose the product for realistic visuals, affordability, and resistance to moisture that simplifies open-plan layouts connecting kitchens, dining areas, and family rooms. Digital printing creates sharp wood and stone graphics that rival natural materials at lower price points, while click-lock profiles shorten installation time by eliminating adhesives. Even when housing starts stalled in 2024, LVT grew in share by displacing carpet and laminate, demonstrating resilience in downturns. The driver sustains significant lift for the resilient floor covering market through at least 2027, particularly in replacement projects across the United States, Germany, France, and Australia.

Healthcare Build-out in Asia-Pacific Requiring Hygienic, Slip-Resistant Floors

Hospitals and clinics under construction across China, India, Indonesia, and Vietnam demand seamless, non-porous sheets that resist microbial growth and enable strict infection control. Suppliers now combine integrated cove-rise detailing, heat-welded seams, and embedded antimicrobial layers to comply with evolving health standards. Asian governments subsidize specialty flooring for critical-care wards, creating steady tender volumes. With more than 2,000 public-sector bed additions scheduled through 2028 in India alone, healthcare construction contributes consistent momentum to the resilient floor covering market.

Waterproof SPC/WPC Demand for Climate-Resilient Housing

Stone Plastic Composite and Wood Plastic Composite boards maintain dimensional stability in flood-exposed basements, coastal vacation rentals, and hurricane-prone multifamily properties. Insurance guidelines issued in 2024 for Florida and Philippine coastal provinces now endorse rigid-core products as a mitigation strategy, influencing builder choice. Homeowners appreciate that SPC floors can be mopped dry and reoccupied quickly after water intrusion, minimizing claim costs. These factors lift SPC adoption rates and widen the user base beyond residential to include hospitality lobbies and small-format grocery chains.

Digital Printing and EIR Finishes Elevating Aesthetics

Advances in ink-jet heads and synchronized embossing let manufacturers align wood grain visuals with tactile ridges, producing floors that pass casual inspection as real timber or slate. Small-batch customization permits boutique hotels to specify exclusive colorways without large minimum orders, opening new premium niches for the resilient floor covering market. Decorative possibilities spur architectural interest, leading to more frequent specifications for retail flagships and corporate amenity zones where branded design is essential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC Feed-stock Price Volatility Compressing Margins | -0.6% | Global, with heightened impact in import-dependent regions | Medium term (2-4 years) |

| Anti-Dumping Tariffs on Asian LVT | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Environmental Scrutiny of Chlorinated Plastics | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Skilled-Installer Shortage Elevating Failure Rates | -0.2% | Global, particularly acute in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PVC Feed-stock Price Volatility Compressing Margins

Polyvinyl chloride costs fluctuate with oil and energy markets, disturbing price lists and squeezing margins, especially for producers lacking backward integration. Spikes in 2024 forced rapid re-quotations on large commercial bids, straining distributor relationships. Europe’s push toward bio-attributed vinyl and North America’s recycling programs create partial buffers, yet unpredictable input costs continue to drag on profitability across the resilient floor covering market.

Anti-Dumping Tariffs on Asian LVT

Trade remedies enacted by the United States and the European Union raised import duties on certain Chinese LVT ranges, prompting rapid sourcing shifts. While domestic plants in Georgia, Tennessee, and Poland ramp up capacity, near-term supply gaps lead to higher landed prices. Project timelines stretch as distributors adjust to new lead times, tempering short-term growth potential for the resilient floor covering market until regional output stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: SPC Disrupts Traditional Vinyl Dominance

Luxury vinyl tile holds 29.94% of overall demand and remains the most versatile offering in the resilient floor covering market. High-definition graphics, low maintenance, and competitive pricing underpin its continued leadership. Stone Plastic Composite is expanding more quickly, advancing at an 8.22% CAGR on the strength of rigid cores that minimize telegraphing over uneven substrates and withstand heavier impacts. Wood Plastic Composite stays relevant at the upper end of residential due to its softer underfoot feel and superior acoustics, though price premiums suppress volume. Conventional vinyl sheet persists in operating theaters and education corridors, where welded seams improve hygiene. Vinyl composition tile continues to decline as institutional buyers shift to no-wax surfaces. Niche alternatives—linoleum, rubber, and cork—collectively equal about 15% of turnover, driven by sustainability ratings and specialized acoustic needs.

SPC’s limestone-reinforced spine gives installers a dimensionally stable plank that tolerates heat swings, supporting projects in sun-belt markets and glass-walled high-rises. Manufacturers run hybrid production lines capable of alternating LVT and SPC on a single shift, maintaining balanced inventories and responsive order cycles. Mass-market retailers advertise easy cleanup, dent resistance, and low lifetime cost, expanding rigid-core visibility and accelerating its share gains inside the resilient floor covering market size hierarchy.

By Installation Type: Click Systems Challenge Traditional Adhesives

Glue-down methods control 46.12% of the 2025 volume because permanent adhesion remains critical in hospitals, supermarkets, and schools, where rolling equipment and high foot traffic impose shear loads that floating floors struggle to support. They also facilitate welded seams that form monolithic coverings, easing sanitation protocols. However, Click-lock planks grow at 7.63% CAGR as contractors seek shorter build programs and reduced labor expense. Locking edges engage with light tapping, letting installers cover up to 100 m² in a day, cutting downtime for busy households and fast-tracking commercial renovations. Loose-lay formats, comprising heavier tiles secured by friction and perimeter tape, cater to data centers and offices where under-floor cable access is imperative. The variety of installation choices sustains parallel growth tracks and enhances the overall adaptability of the resilient floor covering market.

By End-User Industry: Residential Sector Leads Growth Trajectory

Residential projects produced 38.05% of revenue in 2025 and are set to grow at 8.09% CAGR. Waterproof performance, simplified cleaning, and an expanding style library resonate with homeowners upgrading kitchens, mudrooms, and lower-level leisure spaces. Repair and remodel activity in mature U.S. suburbs, German multifamily blocks, and Japan’s aging condominiums continues to prioritize quick-fit planks that minimize occupant disruption. The commercial category remains broad. Healthcare facilities adopt homogeneous resilient sheets that tolerate aggressive cleaning agents. Education installs cushioned LVT to reduce ambient noise and lower maintenance budgets. Retail brands specify digitally printed planks to unify store prototypes across regions, while corporate offices incorporate bio-based designs that strengthen sustainability reporting. Industrial segments stay niche yet steady; anti-static vinyl serves electronics assembly, and chemical-resistant sheets secure pharmaceutical laboratories. Hospitality flags combine wood-look SPC in guest rooms with stone-appearance tiles in lobbies to create cohesive yet durable settings within the resilient floor covering market.

By Distribution Channel: Specialty Retailers Defend Against Digital Disruption

Independent flooring showrooms continue to dominate because in-person consultations help clients navigate wear-layer ratings, sound-absorbing underlays, and color coordination. Installers often partner with these stores, closing the loop on labor shortages. Home-center chains use big-box reach and palletized inventory to address entry-price shoppers seeking weekend DIY upgrades. E-commerce platforms display augmented-reality room visualizers and ship small-parcel sample packs within 48 hours, enabling hassle-free selection online. Hybrid retailers such as Floor and Decor blend digital browsing with in-store design kiosks for an omnichannel experience. A handful of manufacturers now operate flagship galleries where architects can evaluate new technologies before specifying. This mix of channels stabilizes demand across economic cycles and diversified buyer types, making the resilient floor covering market less volatile than many other building-product categories.

Geography Analysis

Europe contributes 31.70% of worldwide revenue, sustained by stringent indoor-air regulations, retrofit subsidies, and circular-economy directives that incentivize closed-loop recycling. Germany and France anchor demand with social-housing upgrades, while Scandinavian municipalities choose bio-based linoleum for schools. Tarkett’s ReStart® program captures site offcuts and end-of-life material, demonstrating a regional blueprint for material recovery. Refurbishment spending remains brisk as energy-efficiency grants reward occupants who seal building envelopes and add low-VOC surfaces, favoring resilient flooring’s quick installation over existing substrates.

Asia-Pacific represents the fastest growth at 9.03% CAGR, underpinned by megacity residential towers, hospital expansions, and expanding disposable income. China alone absorbs millions of square meters of resilient sheets for public hospitals and large-format retail malls. India’s urban housing missions require cost-effective, waterproof solutions that stand up to monsoon humidity. Japan and South Korea request premium acoustic layers to complement lightweight steel construction. Across ASEAN, infrastructure pipelines in Indonesia, Thailand, and Vietnam lift consumption as builders pivot from ceramic tiles to easier-to-handle click-lock planks, reinforcing the scale-out trajectory of the resilient floor covering market.

North America generates roughly a quarter of global sales, and tariff actions have triggered rapid on-shoring. New lines in Georgia and Ontario support local distributors, trimming shipping times and safeguarding supply. Canadian provinces specify low-VOC products for provincial facilities, while Mexico builds capacity to serve domestic housing and export opportunities under free-trade frameworks. The region sees consistent renovation fueled by aging housing stock, with SPC planks often chosen to resolve historic moisture issues in basements and ground-floor extensions. Demand diversification across single-family, multifamily, and light commercial enhances the structural stability of the resilient floor covering market size in North America.

Competitive Landscape

The five largest manufacturers combine for 1/3rd of worldwide sales, indicating a moderately concentrated but innovation-driven field. Mohawk Industries leverages vertical integration, transforming post-consumer vinyl and recycled polymers into PureTech, a PVC-free line that meets low-carbon construction targets[2]Source: Mohawk Industries, “PureTech Launch Overview,” mohawkindustries.com. . Tarkett’s global take-back network underscores its circular-economy leadership, enabling quicker raw-material inventory cycles and lower Scope 3 emissions[3]Source: Tarkett Group, “ReStart® Take-Back & Recycling Program,” tarkett.com.. Shaw Industries, expanding Georgia rigid-core capacity, seeks to replace import volumes with domestic output, while Armstrong Flooring focuses on technical performance sheets for intensive-care units. Mannington Mills positions high-graphic SPC planks through boutique distributors, reinforcing its design-led identity.

Below the top tier, Responsive Industries scales production in India to service Asia-Pacific growth corridors, and Gerflor refines healthcare-centric wall-to-floor integration for infection-critical zones. Emerging niche entrants concentrate on climate-specific or PVC-free formulations, staking claims in white-space categories. Competitive intensity skews toward product differentiation and sustainability metrics, not price wars, which preserves margins and facilitates steady reinvestment in the resilient floor covering market.

White-space opportunities revolve around renewable polymer chemistries, installer-friendly click profiles, and sensor-ready flooring that feeds building-performance dashboards. Regulatory drift toward PVC alternatives accelerates R&D pipelines, meaning companies that commercialize compliant formulas early can seize future tender lists. Continuous digital-print upgrades push the boundary between authentic and replicated visuals, raising consumer valuations and protecting price points. These dynamics, coupled with a mid-level concentration index, foster active competition yet leave room for agile challengers to capture specialized demand segments.

Resilient Floor Covering Industry Leaders

Mohawk Industries Inc.

Tarkett S.A.

Shaw Industries Group Inc.

Armstrong Flooring LLC

Mannington Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mohawk Industries launched PureTech, a PVC-free resilient plank composed of 80% recycled content, targeting projects seeking aggressive Environmental, Social, and Governance credits.

- February 2025: AHF Products reintroduced Armstrong Flooring MedinPure, a PVC-free homogeneous sheet incorporating Diamond 10 technology for hospital durability.

- November 2024: Shaw Industries invested USD 90 million in Ringgold, Georgia, to more than double SPC and LVT output by 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers resilient floor coverings as all sheet, tile, and plank surfaces made from vinyl-based composites, linoleum, rubber, cork, wood-plastic core, and similar flexible materials that are neither textile, ceramic, stone, nor solid wood. The valuation reflects factory-gate revenue from new product sales, replacement, and major renovation demand across residential and non-residential buildings worldwide.

Scope Exclusion: Adhesive expenditures, maintenance chemicals, carpets, and artificial turf are excluded.

Segmentation Overview

- By Product Type

- Luxury Vinyl Tile (LVT)

- Dry-Back (Glue-Down)

- Click-Lock Floating

- Loose-Lay

- Vinyl Sheet

- Vinyl Composition Tile (VCT)

- Stone Plastic Composite (SPC) / Rigid Core

- Wood Plastic Composite (WPC)

- Linoleum

- Rubber

- Cork

- Luxury Vinyl Tile (LVT)

- By Installation Type

- Glue-Down

- Floating / Click-Lock

- Loose-Lay

- By End-User Industry

- Residential

- Commercial

- Healthcare Facilities

- Education Buildings

- Retail & Supermarkets

- Hospitality & Leisure

- Corporate Offices

- Industrial & Manufacturing

- By Distribution Channel

- Offline

- Specialty Stores

- Home Centers & DIY Chains

- Online

- Offline

- Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed distributors, builders, architects, and procurement heads across North America, Europe, Asia-Pacific, and the GCC. These conversations validated shipment seasonality, standard installation losses, emerging PVC-free demand, and typical ex-factory margins, allowing us to challenge desk assumptions and reconcile regional anomalies.

Desk Research

We began with trade data from UN Comtrade and Eurostat, construction spending series from the U.S. Census and Euroconstruct, and output indices published by the National Bureau of Statistics of China and India's MOSPI. Industry guidance from associations such as North American Floor Covering Manufacturers, the European Resilient Flooring Institute, and the Vinyl Sustainability Council helped refine product mixes. Company 10-Ks, investor presentations, and tender portals added price and capacity clues, while paid access to D&B Hoovers and Dow Jones Factiva let us cross-check producer revenues and news flow. This list is illustrative; many other public and proprietary sources fed the evidence base.

Market-Sizing & Forecasting

We anchored the 2025 baseline with a top-down reconciliation of global resilient flooring output and import-export flows. We then ran selective bottom-up checks, sampling average selling price multiplied by producer volumes in six key countries to fine-tune totals. Core drivers in our model include new floor area completions, renovation ratios, vinyl price movements, urban household formation, policy incentives for low-VOC materials, and LVT penetration rates. A multivariate regression with lagged construction starts and GDP per capita projects demand to 2030, while scenario analysis adjusts for raw-material volatility. Where supplier data were patchy, we bridged gaps with region-specific installation factors vetted through channel interviews.

Data Validation & Update Cycle

Before sign-off, results pass a three-layer review: automated variance flags, peer analyst audit, and senior analyst approval. We refresh every twelve months and trigger mid-cycle updates when raw-material shocks, major capacity additions, or regulation shifts alter demand outlooks.

Why Mordor's RESILIENT FLOOR COVERING Baseline Stands Firm

Published figures vary because firms pick different product baskets, price bases, and update cadences. Some fold broad laminate or carpet lines into 'resilient,' while others convert volume to value using retail prices; naturally, totals diverge.

Key gap drivers are scope breadth, currency year, and whether aftermarket services are counted. Our study focuses strictly on first-sale manufacturer revenue, uses constant 2024 USD, and is refreshed yearly, whereas external services often blend installation income or adopt multi-year exchange averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.56 B (2025) | Mordor Intelligence | - |

| USD 42.23 B (2025) | Global Consultancy A | Includes adhesives and installation labor; uses distributor price points |

| USD 36.2 B (2024) | Industry Journal B | Broader 'flooring' scope; mixes laminate and ceramic substitutes |

External services quote values as high as USD 42.23 billion for 2025, while another study places 2024 demand at USD 36.2 billion. According to Mordor Intelligence, the narrower resilient floor covering segment totals USD 2.56 billion in 2025. In sum, our disciplined definition, transparent variables, and annual refresh give decision-makers a dependable, traceable baseline they can benchmark with confidence.

Key Questions Answered in the Report

What is the current resilient floor covering market size?

The resilient floor covering market is worth USD 2.7 billion in 2026 and is projected to reach USD 3.52 billion by 2031.

Which segment leads the resilient floor covering market?

Luxury vinyl tile remains the top product, holding 29.94% of 2025 revenue.

Which product category is growing the fastest?

Stone Plastic Composite is forecast to grow at an 8.22% CAGR through 2031 because of its rigid, waterproof core.

Why is Asia-Pacific the fastest-growing region?

Rapid urbanization, healthcare construction, and rising consumer income push Asia-Pacific demand to a 9.03% CAGR.

How large is the residential opportunity?

Residential applications already account for 38.05% of global revenue and are expanding at 8.09% CAGR on sustained remodeling activity.

What installation method is taking share from glue-down?

Click-lock floating planks are gaining momentum with a 7.63% CAGR due to faster, adhesive-free assembly that suits both DIY and professional crews.

Page last updated on: