Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

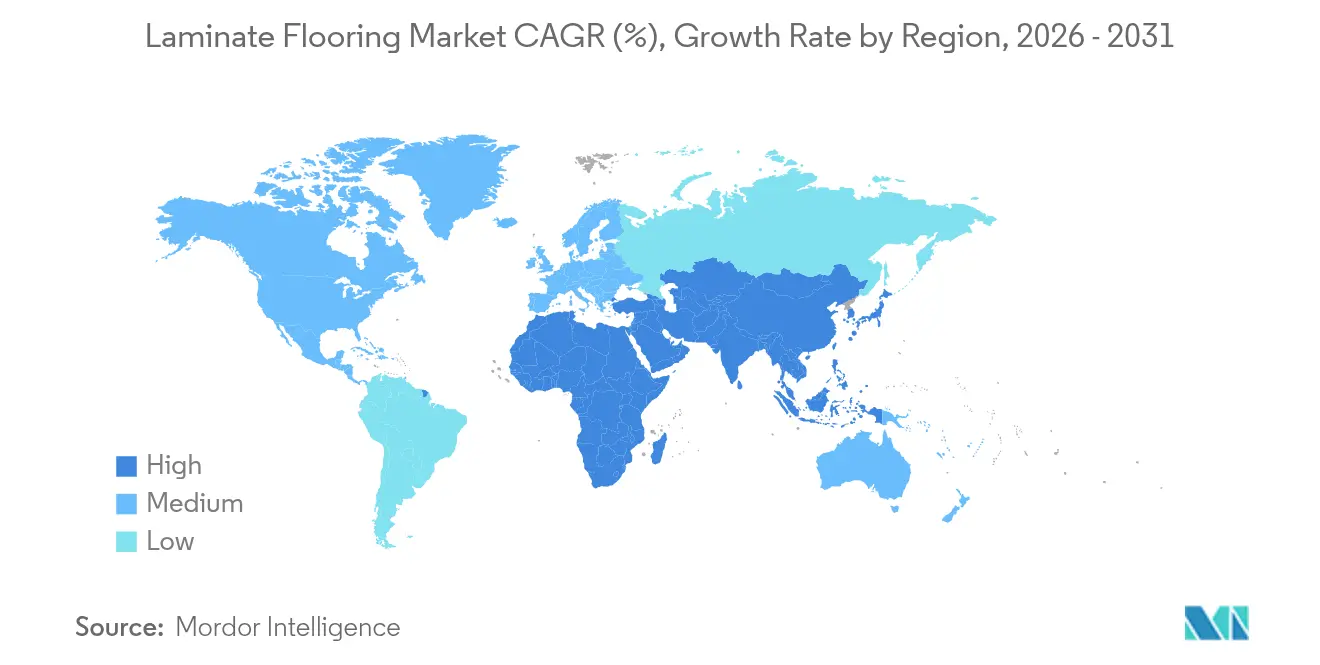

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laminate Flooring Market Analysis by Mordor Intelligence

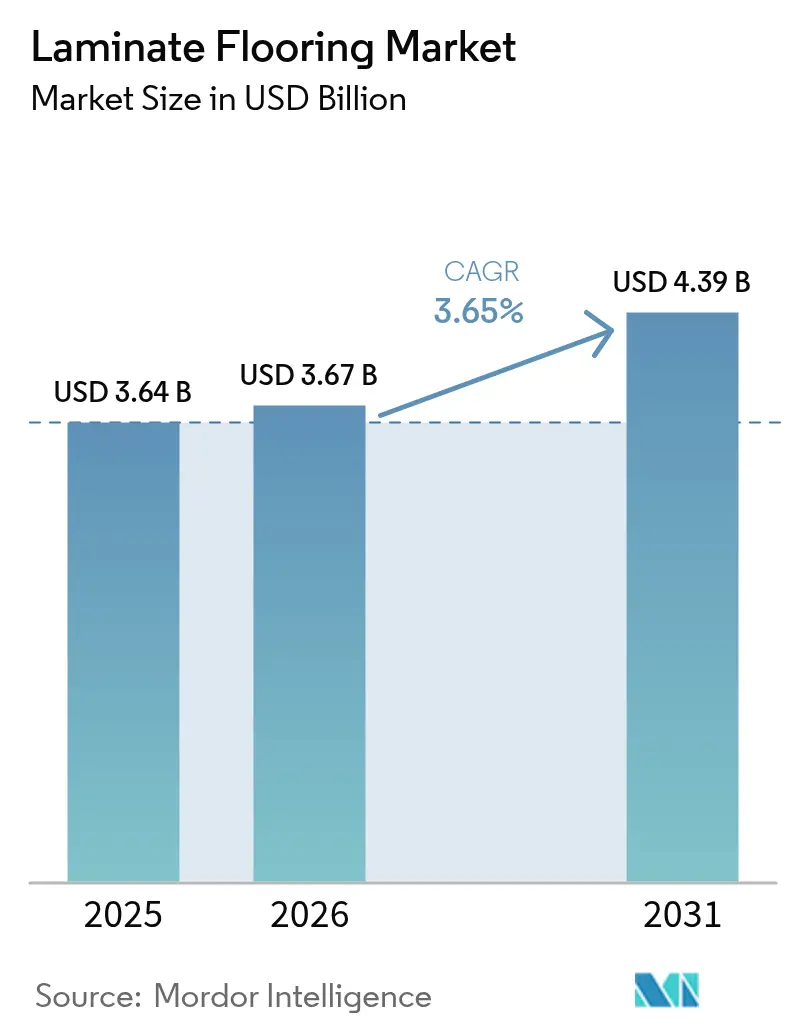

The laminate flooring market size was USD 3.64 billion in 2025, is set to reach USD 3.67 billion in 2026, and is forecast to rise to USD 4.39 billion by 2031, reflecting a 3.65% CAGR during 2026-2031. Momentum in the laminate flooring market in 2026 is supported by waterproof performance advances that extend use into kitchens, bathrooms, and below-grade spaces, which expands the total addressable demand beyond traditional living areas. Product and channel decisions in the laminate flooring market are increasingly shaped by formaldehyde emissions compliance and testing cadence under United States TSCA Title VI and Canada’s CANFER rules, which raise the bar for quality control and documentation across wood-based substrates. In the European Union, the new deforestation-free products regulation requires due diligence and geolocation traceability for relevant wood inputs, which may add process cost and lead time for operators in scope during 2026 and 2027. The laminate flooring market also benefits from broader sustainability documentation, since leading producers issue Environmental Product Declarations and help specifiers compare lifecycle data with confidence for green building programs. Circularity initiatives, including new recycling lines capable of recovering MDF and HDF for new decorative panels and laminate floors, point to structural efforts that can differentiate brands in 2026.

Key Report Takeaways

- By product type, high-density fiberboard (HDF) accounted for 63.61% of the laminate flooring market share in 2025, while medium-density fiberboard (MDF) is set to record the highest projected CAGR at 4.44% through 2031.

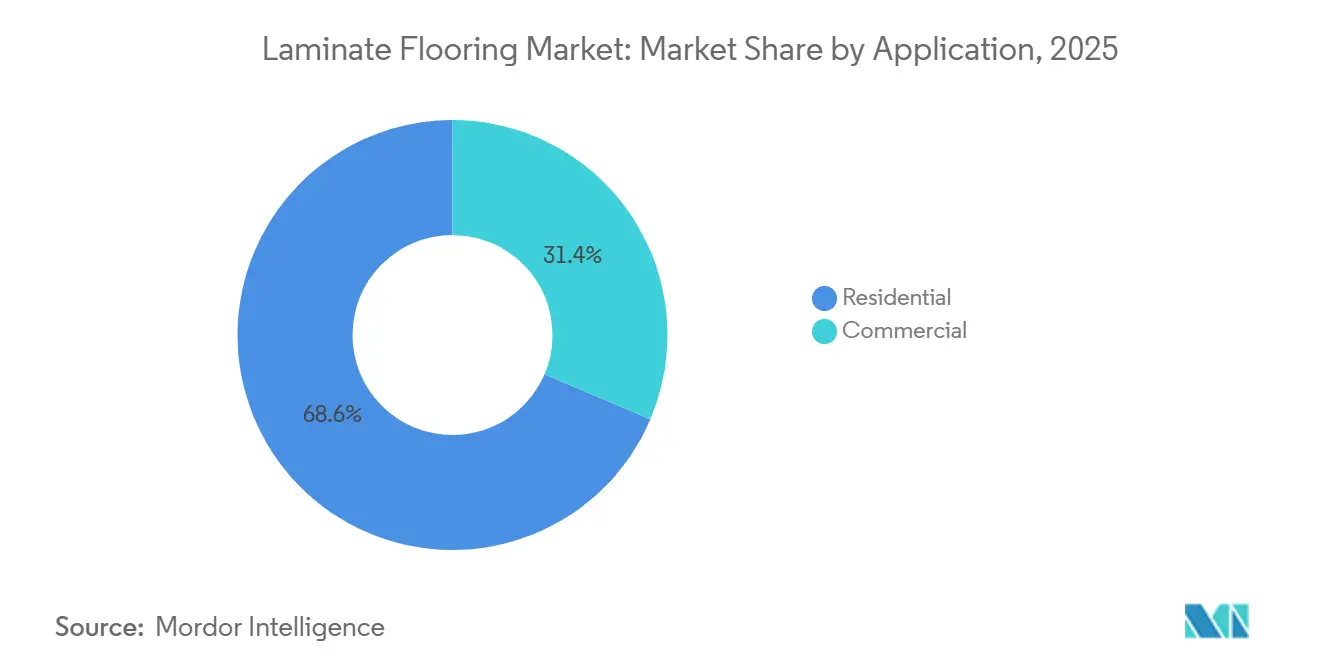

- By application, residential accounted for 68.55% of the laminate flooring market share in 2025, while commercial is set to record the highest projected CAGR at 4.16% through 2031.

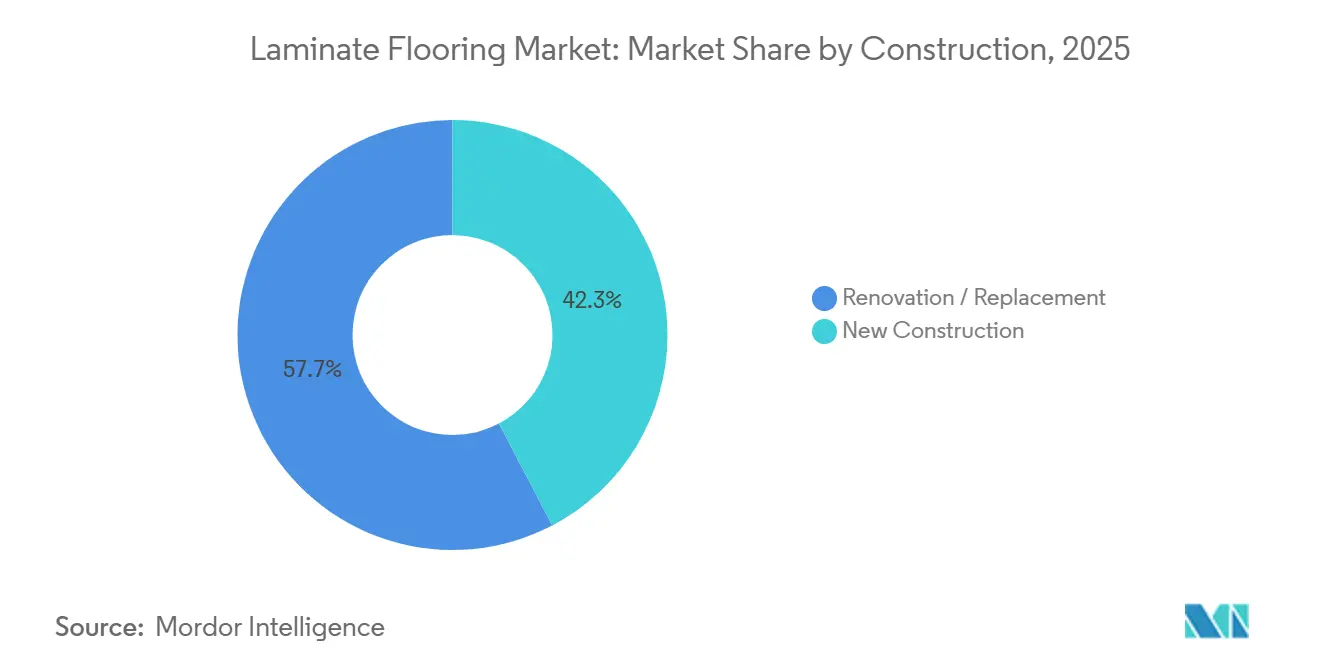

- By construction, renovation, and replacement held 57.68% of the laminate flooring market share in 2025, while new construction is expected to grow at a 3.92% CAGR to 2031.

- By geography, Asia-Pacific held 37.95% of the laminate flooring market share in 2025, while the Middle East and Africa are projected to expand at a 4.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laminate Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DIY-friendly residential renovation demand | +0.9% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Asia-Pacific housing and construction-led demand pool | +1.2% | Asia-Pacific core, spill-over to Western Asia and Africa | Long term (≥ 4 years) |

| Cost-performance and EIR realism vs hardwood and stone | +0.7% | Global | Medium term (2-4 years) |

| Waterproof and water-resistant laminates expand use zones | +0.8% | North America and the Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Tariff pressure on rigid vinyl nudges the share of laminate | +0.5% | North America, early gains in domestic production hubs | Short term (≤ 2 years) |

| Green procurement favors PVC-free, EPD, and traceable wood solutions | +0.6% | The Europe and North America commercial sectors spill over to Asia-Pacific institutions. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DIY-Friendly Residential Renovation Demand Powers Growth Despite Rate Lock-In

In 2026, renovation activity continues to steer the laminate flooring market because click-lock installation reduces labor needs and empowers homeowners to self-manage projects with predictable timelines. The laminate flooring market benefits when households delay moves yet still refresh interiors, since replacement cycles proceed room by room as budgets allow. Retail education and showroom demonstrations that highlight scratch, dent, and stain performance have helped reposition modern offerings, which supports replacement demand even while new construction cycles remain uneven. Design and format upgrades released by association members also support consumer pull by emphasizing natural textures and durable surfaces, which align with longer renovation cycles in mature economies. The net effect keeps the laminate flooring market closely linked to residential replacement spending, where a large installed base and practical upkeep advantages sustain recurring upgrades.

Asia-Pacific Housing and Construction-led Demand Pool

Asia-Pacific leads the laminate flooring market with a 37.95% share in 2025 and is projected to grow at a 5.80% CAGR from 2026 to 2031, indicating a broad base of construction-led demand that extends beyond pure renovation cycles. The laminate flooring market in 2026 sees a strong pull from urban housing and commercial buildouts in APAC, where faster build schedules and cost-sensitive procurement keep laminates competitive for large footprints. Regional public and private projects in Western Asia also underpin a forward pipeline that reduces volatility, which complements the renovation-led volumes in North America and Europe. The Middle East and Africa are further projected to register the fastest regional growth through 2031, which supports a rebalancing of the laminate flooring market across emerging demand pools. These dynamics keep the laminate flooring market exposed to long-horizon building programs that can offset temporary lulls in mature residential remodeling cycles.

Cost-Performance and EIR Realism Versus Hardwood and Stone

Advances in digital printing and embossed-in-register texturing have raised realism, making the laminate flooring market more competitive with mid-tier engineered hardwood or stone looks. Association updates in 2025 and 2026 showcased natural textures, matte finishes, and design directions that improve authenticity while keeping cost advantages versus alternative materials[1]European Producers of Laminate Flooring, “2025 Trends: Sustainable, Durable and Elegant,” EPLF, eplf.com . The laminate flooring market now leverages a balance between look, performance, and price, which is critical for households that prioritize scratch resistance and easy maintenance over refinishing options. Product platforms that combine high abrasion ratings with realistic surfaces improve trade-up potential in the laminate flooring market when consumers compare total installed cost. Sustainability innovations also contribute to value, since PVC-free and recyclable constructions from leading producers can serve design intent, regulatory needs, and cost targets in a unified specification.

Waterproof and Water-Resistant Laminates Expand Use Zones

Water protection technologies are expanding the addressable base for the laminate flooring market by enabling installation in kitchens, entryways, laundry rooms, and certain below-grade spaces. A leading technology example offers up to 72-hour standing water protection without visual swelling, which gives retailers and installers greater confidence in areas that experience spills and tracked-in moisture. The laminate flooring market gains further traction when waterproof claims pair with durable surface ratings, because commercial and hospitality areas demand both spill resilience and traffic resistance. Association communications in 2026 continue to emphasize design and durability themes, which support broader adoption as shoppers see live demonstrations of water resistance and authentic textures side by side. As more retailers center these use-zone expansions in their displays, the laminate flooring market captures projects that would have defaulted to rigid vinyl in prior cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Share loss to LVT and SPC on waterproof and dent resistance perception | -0.8% | Global, acute in multifamily new construction in North America | Medium term (2-4 years) |

| HDF core seam and edge swelling risk in wet incidents | -0.4% | Global, heightened in high-humidity regions | Short term (≤ 2 years) |

| Europe deforestation due diligence adds compliance cost and latency | -0.3% | Europe imports, spillover to United States exporters | Long term (≥ 4 years) |

| Tight formaldehyde emission regimes increase quality control costs | -0.5% | North America and the Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Share Loss to LVT and SPC on Waterproof and Dent Resistance Perception

Rigid core alternatives are often marketed as fully waterproof, and that message remains top of mind for many property managers and retail sales associates. In the laminate flooring market, this perception gap can delay recognition of recent waterproof advances and scratch performance improvements, which slows share recovery in moisture-prone applications. Improved showroom training and side-by-side demonstrations help close the gap by highlighting both realism and water performance under controlled tests. Association trend briefings continue to emphasize how updated designs and finishes meet everyday performance needs, which supports training content for sales associates and installers. As these demonstrations scale across channel partners, the laminate flooring market can reclaim projects where legacy waterproof narratives once tilted selection to rigid vinyl.

HDF Core Seam and Edge Swelling Risk in Wet Incidents

Water resistance claims vary by brand and technology, and some installers remain cautious with below-grade and bathroom placements until they see documented protection windows and field performance. The laminate flooring market must continue to demonstrate credible water resistance through technology disclosures, installation guidance, and after-sale warranties that reduce perceived liability. Clear product statements around standing water tolerance and edge protection, including examples of 72-hour protection, give installers more confidence in use cases that were once limited to alternatives. At the same time, compliance with formaldehyde emission standards in the United States and Canada requires routine testing and third-party oversight for composite wood cores, which adds process steps and demands supplier rigor across procurement and manufacturing[2]Health Canada, “Guidance Document: Formaldehyde Emissions from Composite Wood Products Regulations,” Government of Canada, canada.ca . As producers publish detailed technical documents and strengthen training, the laminate flooring market can mitigate installer risk perception and increase confidence for a wider range of rooms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HDF’s Density Edge Holds Share While MDF Builds the Value Tier

High-density fiberboard commanded 63.61% of 2025 sales and set the premium performance baseline for dimensional stability and strength in the laminate flooring market. In the laminate flooring market, HDF supports products with higher abrasion ratings and improved edge sealing, which helps in kitchens, entries, and high-traffic corridors. Producers continue to document emissions performance for HDF-based constructions to comply with TSCA Title VI and maintain product eligibility in regulated markets, which stabilizes channel confidence in 2026. Waterproof surface and joint systems paired with HDF core stability are central to channel education, and named technologies with 72-hour standing water protection have reinforced how HDF platforms can extend into new zones. These attributes help the laminate flooring market address projects that require both higher traffic performance and short-duration moisture tolerance without the cost premium of hardwood.

MDF held the balance of share in 2025 and is projected to grow fastest at a 4.44% CAGR between 2026 and 2031 as brands target cost-sensitive residential segments with credible performance, which broadens the laminate flooring market footprint across entry and mid-price points. The laminate flooring industry often positions MDF at accessible price bands that still meet emissions standards and durability expectations, which keeps category entry points attractive in retail. Manufacturers investing in PVC-free formats also expand the user base by addressing sustainability expectations, including recyclable constructions and third-party certifications that support commercial specifications. Over the forecast, HDF maintains its hold in premium use cases, while MDF gains share in large-footprint residential projects that price against resilient alternatives.

By Application: Residential Replacement Dominates While Commercial Gains on EPD-Backed Spec

Residential accounted for 68.55% of 2025 volumes, which reflects the laminate flooring market’s deep link to replacement cycles where click systems and durable finishes fit DIY timelines and budget planning in 2026. The laminate flooring market benefits from sustained product education that highlights dent and scratch resistance, authentic textures, and stable color collections for common home upgrades. Demand in pet households and active lifestyles aligns with AC-rated surfaces, which support steady residential traffic in kitchen-adjacent and entry spaces. Waterproof joint and surface technologies help extend usage into laundry rooms and other spill-risk areas, which adds incremental rooms per home over time. As retailers scale story-driven displays and side-by-side demonstrations, the laminate flooring market keeps its place on shortlists for budget-aware and design-aware homeowners.

Commercial held the remaining 31.45% in 2025 and is projected to grow fastest at a 4.16% CAGR through 2031 as specifiers lean into third-party documentation and circularity claims that validate environmental targets. EPD-backed disclosures, recyclability pilots, and resource-efficient material systems help satisfy institutional procurement requirements that are now common in office, retail, and hospitality. The laminate flooring market size for commercial accounted for 31.45% in 2025, and momentum improves as water-resistance is demonstrated alongside abrasion ratings that meet traffic expectations in corridors and guest areas. As large owners standardize specifications with lifecycle transparency, the laminate flooring market can win on look, maintenance profile, and documentation across multi-site portfolios. Broader sustainability communication by brands adds confidence for long-term use in public-facing spaces.

By Construction: Renovation’s DIY Appeal Sustains Share While New Build Rises on Emerging Projects

Renovation and replacement held a 57.68% share in 2025, which aligns with the laminate flooring market’s historical strength in installed-base refreshes, where homeowners value quick installation and predictable costs in 2026. The laminate flooring market continues to benefit as retailers emphasize waterproof and abrasion ratings that apply directly to entryways, kitchens, and living rooms. Guidance on emissions compliance and safe installation practices also supports confidence for projects in regulated jurisdictions, which helps drive steady sell-through[3]California Air Resources Board, “Composite Wood Products Program,” CARB, ww2.arb.ca.gov. Demonstrated waterproof performance, including 72-hour standing water protection on select systems, reduces friction on renovation choices for below-grade spaces as homeowners weigh cost against durability. These factors keep the laminate flooring market liquid across seasonal renovation windows.

New construction accounted for 42.32% of 2025 volumes and is projected to grow at 3.92% through 2031 as housing and commercial projects in emerging regions build the installed base that will underpin future replacements. The laminate flooring market benefits when developers select faster install systems that compress schedules without major trade coordination, especially across large residential towers and hospitality footprints. Regional procurement teams increasingly request emissions documentation and EPDs for wood-based materials, which favors organized suppliers with complete technical files. As builders target mid-range finishes that balance look and budget, the laminate flooring market can capture corridors, rooms, and amenity areas that do not require luxury wood detail. Over time, these new installations feed recurring replacement cycles that stabilize demand.

Geography Analysis

Asia-Pacific led the laminate flooring market with 37.95% share in 2025 and is projected to grow at a 5.80% CAGR during 2026-2031, which confirms sustained construction-led demand across housing and commercial projects that need durable, fast-install surfaces. Producers that combine emissions compliance, EPD-backed data, and waterproof options can align with public and private project requirements, which supports broader adoption in institutional and hospitality spaces. As regional showrooms emphasize natural textures and matte finishes, the laminate flooring market gains incremental preference among buyers who compare performance and installed cost to other surface materials. These drivers help sustain growth through multi-year build plans in 2026 and beyond.

Europe maintains an important position in the laminate flooring market, with growth moderated at a projected 3.00% CAGR during 2026-2031 as operators implement the deforestation-free products regulation with new due diligence and geolocation traceability requirements[4]European Commission, “Regulation on Deforestation-Free Products,” European Commission, environment.ec.europa.eu. The laminate flooring market in Europe also remains shaped by strict formaldehyde emission regimes and low-VOC expectations, which reward vertically integrated suppliers that control board production and testing in-house. Association trend reports highlight realistic textures and sustainable design cues, which keep European product introductions aligned with market preferences in 2026. As EU compliance dates approach for large operators in late 2026 and for smaller operators in 2027, the laminate flooring market could see short-term adjustments in sourcing and documentation practices that stabilize over the medium term. These structural changes raise the importance of traceable supply chains and verified disclosures.

North America is projected to grow at a 3.80% CAGR over 2026-2031, with the laminate flooring market tied to steady remodeling cycles and higher awareness of scratch performance in family and pet households. TSCA Title VI governs the laminate flooring market in the U.S. for composite wood emissions, which directs consistent testing and third-party oversight for products sold into regulated channels. In Canada, CANFER requires primary testing on prescribed cadences and specific methods, which informs manufacturer quality systems and documentation used by commercial specifiers in 2026. The Middle East and Africa are projected to post the fastest regional CAGR of 4.15% through 2031, which points to construction-driven demand where practical, water-resilient wood-look floors fit projects that manage cost and schedule tightly. As these regions expand installed bases in commercial and residential categories, the laminate flooring market develops a broader geographic spread that supports stable global growth.

Competitive Landscape

Competitive intensity in the laminate flooring market remains moderate in 2026, with the global top five players holding an estimated nearly half of the combined share and a long tail of regional producers competing through local distribution. Differentiation centers on waterproof performance, abrasion resistance, and visual realism, where brands demonstrate water protection windows and present authentic wood looks to win share in high-traffic and spill-risk zones. Sustainability credentials, including circularity pilots and third-party certifications for recyclable, PVC-free materials, add another lever for specification in commercial categories that depend on verified data. These strategies reflect how the laminate flooring market balances material science, compliance, and storytelling at the point of sale.

Technology and design investments remain a central theme, with association trend updates highlighting natural textures, matte finishes, and balanced aesthetics that align with consumer preferences in 2026. Waterproof surface and joint systems that achieve documented standing water protection help brands reposition laminate in rooms that were once considered out of scope, which expands the reachable pool for the laminate flooring market. Corporate disclosures also reference ongoing portfolio updates and operational initiatives, which support product flow and category visibility across key retail accounts in North America and Europe. As suppliers embed recyclability and resource efficiency into roadmaps, the laminate flooring market can appeal to institutions that prioritize verifiable environmental outcomes and lifecycle data. This blend of performance features and documented sustainability continues to guide specification outcomes.

Regional production strategies and compliance readiness influence competitive outcomes in 2026 as regulations tighten and documentation workloads increase. The laminate flooring market sees suppliers emphasize emissions compliance under TSCA Title VI and CANFER, since consistent testing and third-party oversight are prerequisites for many channels. In the EU, EUDR due diligence adds long-term traceability requirements for wood inputs, which rewards vertically integrated operators that can verify geolocation and sourcing practices efficiently. Brands communicating progress on recyclable, PVC-free construction and take-back pilots add a distinctive position as procurement teams formalize ESG screens for interior materials in 2026. As these factors converge, the laminate flooring market rewards suppliers combining technology, compliance, and evidence-backed sustainability.

Laminate Flooring Industry Leaders

Mohawk Industries

Shaw Industries

Tarkett

Swiss Krono Group

Kronospan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: CLASSEN Group’s CERAMIN received Cradle to Cradle Certified Full Scope Silver for its PVC-free polypropylene-based material technology, confirming a resource-efficient and fully recyclable platform with a high share of recycled polymer content.

- October 2025: Unilin invested USD 23.52 million in a new recycling line in Bazeilles, France, enabling industrial-scale recycling of MDF and HDF boards to produce new decorative panels and laminate floors, which advances the company’s floor-to-floor circularity program.

- June 2025: CLASSEN Group was awarded an EcoVadis Bronze medal for sustainability performance, placing the company among the top cohort of evaluated firms and underscoring continued improvements in responsible production metrics.

- March 2025: CLASSEN Group received a Cradle to Cradle Certified Material Health certificate in bronze for CERAMIN flooring, recognizing the material health and reusability attributes of its polypropylene-based substrate.

Global Laminate Flooring Market Report Scope

Laminate flooring comprises several synthetic layers, such as wear, design, core, and back layers, fused using lamination. The top layer, usually composed of melamine and aluminum oxide, protects against scratches and moisture, ensuring durability. Compared to engineered wood, solid hardwood, and stone floor coverings, laminate flooring is more affordable and easier to install and maintain.

The Laminate Flooring Market is segmented by product type, application, construction, and geography. By product type, the market is divided into high-density fiberboard (HDF) laminated flooring and medium-density fiberboard (MDF) laminated flooring. By application, the market is categorized into residential and commercial segments. By construction, the market is segmented into new construction and renovation/replacement.

Geographically, the market analysis covers North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. In North America, the market includes the United States, Canada, and Mexico. In South America, the market covers Brazil, Peru, Chile, Argentina, and the Rest of South America. In Europe, the market includes the United Kingdom, Germany, France, Spain, Italy, BENELUX (Belgium, Netherlands, Luxembourg), NORDICS (Denmark, Finland, Iceland, Norway, Sweden), and the Rest of Europe. In the Asia-Pacific region, the market covers India, China, Japan, Australia, South Korea, Southeast Asia, and the Rest of the Asia-Pacific region. In the Middle East & Africa, the market includes the United Arab Emirates, Saudi Arabia, South Africa, Nigeria, and the Rest of the Middle East & Africa. The report provides market size and forecasts for the laminate flooring market in value (USD) across all the above segments.

By Product Type

| High-Density Fiberboard (HDF) Laminated Flooring |

| Medium-Density Fiberboard (MDF) Laminated Flooring |

By Application

| Residential |

| Commercial |

By Construction

| New Construction |

| Renovation / Replacement |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | High-Density Fiberboard (HDF) Laminated Flooring | |

| Medium-Density Fiberboard (MDF) Laminated Flooring | ||

| By Application | Residential | |

| Commercial | ||

| By Construction | New Construction | |

| Renovation / Replacement | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the laminate flooring market?

The laminate flooring market size is expected to increase from USD 3.64 billion in 2025 to USD 3.67 billion in 2026 and reach USD 4.39 billion by 2031, growing at a 3.65% CAGR over 2026-2031.

Which applications are leading the demand in 2026?

Residential replacement remains the largest application by share in 2025, and commercial is projected to grow fastest through 2031 as EPD-backed documentation and water-resilient systems support specification.

Which regions are most important for near-term growth?

Asia-Pacific holds the largest share and is projected to grow at a 5.80% CAGR to 2031, while the Middle East and Africa are set to be the fastest-growing regions over the same period.

How are regulations shaping product design and sourcing?

TSCA Title VI and CANFER require emissions testing and oversight for composite wood cores, while the EU’s deforestation-free regulation adds due diligence and geolocation traceability for wood inputs.

What features are moving buyer decisions in 2026?

Documented waterproof performance, abrasion resistance, and authentic textures drive selection, while verified sustainability and EPDs support commercial and institutional specification.

Which competitive moves stand out right now?

Investments in circularity and recyclable platforms, such as a new MDF and HDF recycling line and PVC-free product families, are differentiating leaders and reinforcing compliance and ESG narratives in 2026.

Page last updated on: