Recycled and Bio-Based Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 58.17 Billion |

| Market Size (2031) | USD 75.78 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recycled and Bio-Based Flooring Market Analysis by Mordor Intelligence

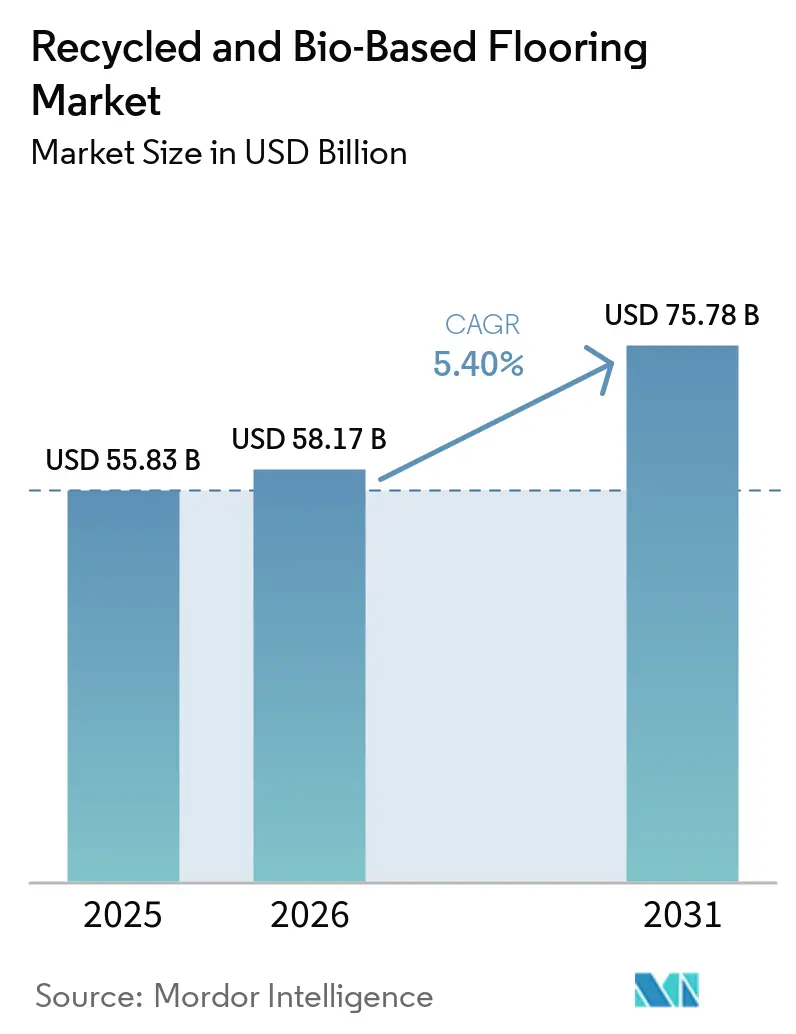

The recycled and bio-based flooring market size is expected to increase from USD 55.83 billion in 2025 to USD 58.17 billion in 2026 and reach USD 75.78 billion by 2031, growing at a CAGR of 5.4% over 2026–2031. This growth reflects a clear market shift, driven by tighter regulations, corporate carbon reduction goals, and advances in material technology that are gradually replacing virgin-resin products. Chemical recycling investments and mass-balance certification are opening verified feedstock routes into LVT and PVC workflows, which strengthens the case for circular-ready portfolios in competitive bids. Cost differentials and uneven take-back rules continue to affect reverse logistics and the availability of secondary raw materials, which influence pricing and project-level product selection in the global recycled and bio-based flooring market[1]European Commission, “Construction Products Regulation (CPR),” European Commission, ec.europa.eu.

Key Report Takeaways

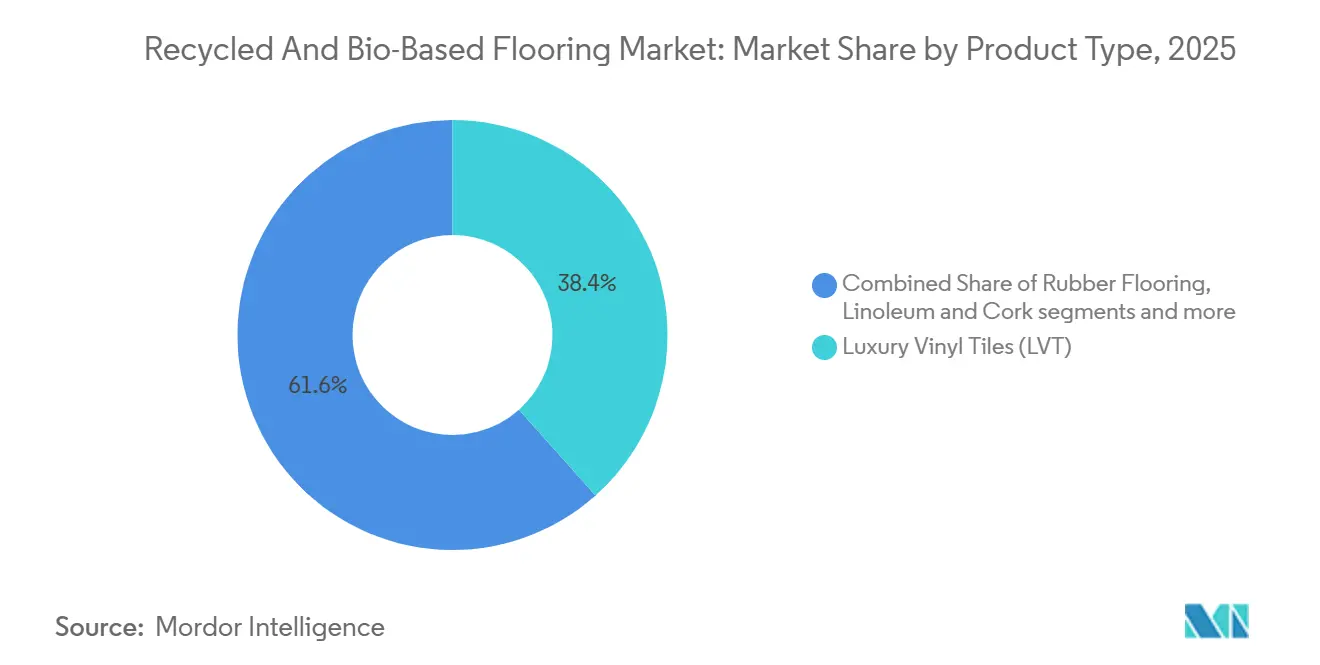

- By product type, luxury vinyl tiles accounted for 38.41% of the global recycled and bio-based flooring market in 2025, while engineered wood and bamboo are projected to expand at a 11.41% CAGR through 2031.

- By material source, recycled plastics accounted for 33.13% of the global recycled and bio-based flooring market in 2025, and bio-based polymers are projected to grow at a 11.93% CAGR through 2031.

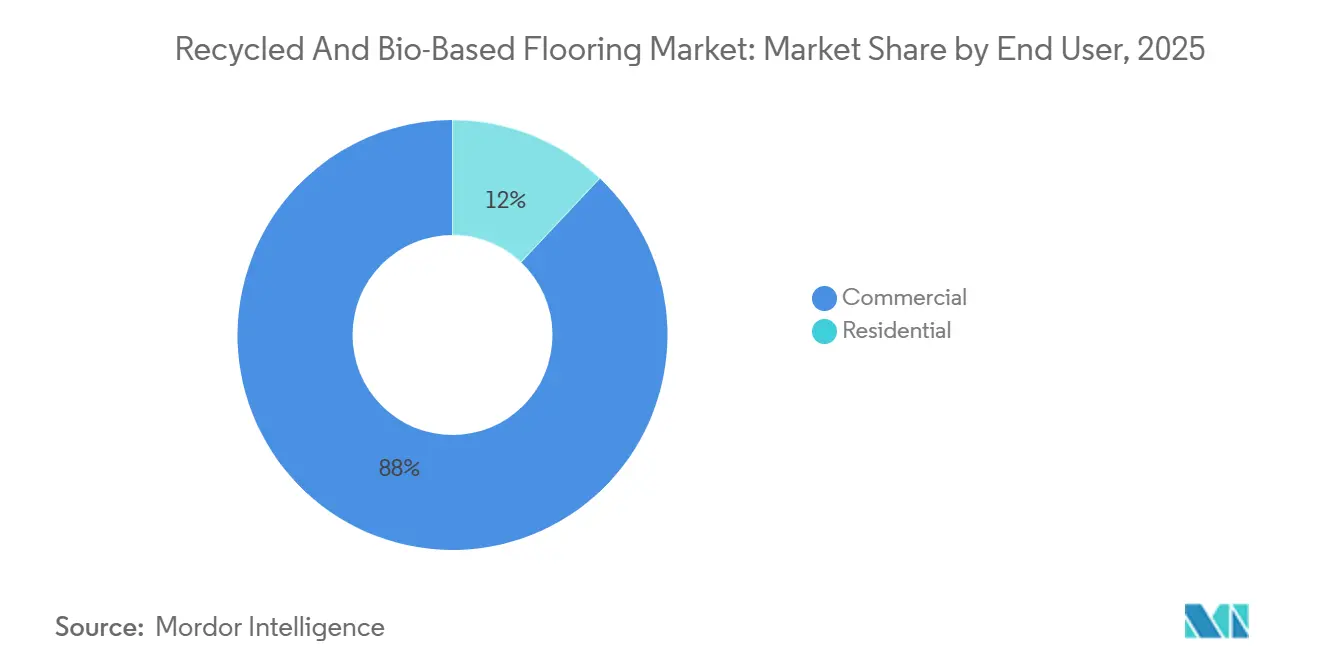

- By end user, the commercial segment accounted for 88% of the global recycled and bio-based flooring market size in 2025 and is expected to register a 9.57% CAGR through 2031.

- By distribution channel, B2B and contractors accounted for 86.35% of the global recycled and bio-based flooring market in 2025 and are projected to grow at a 10.16% CAGR through 2031.

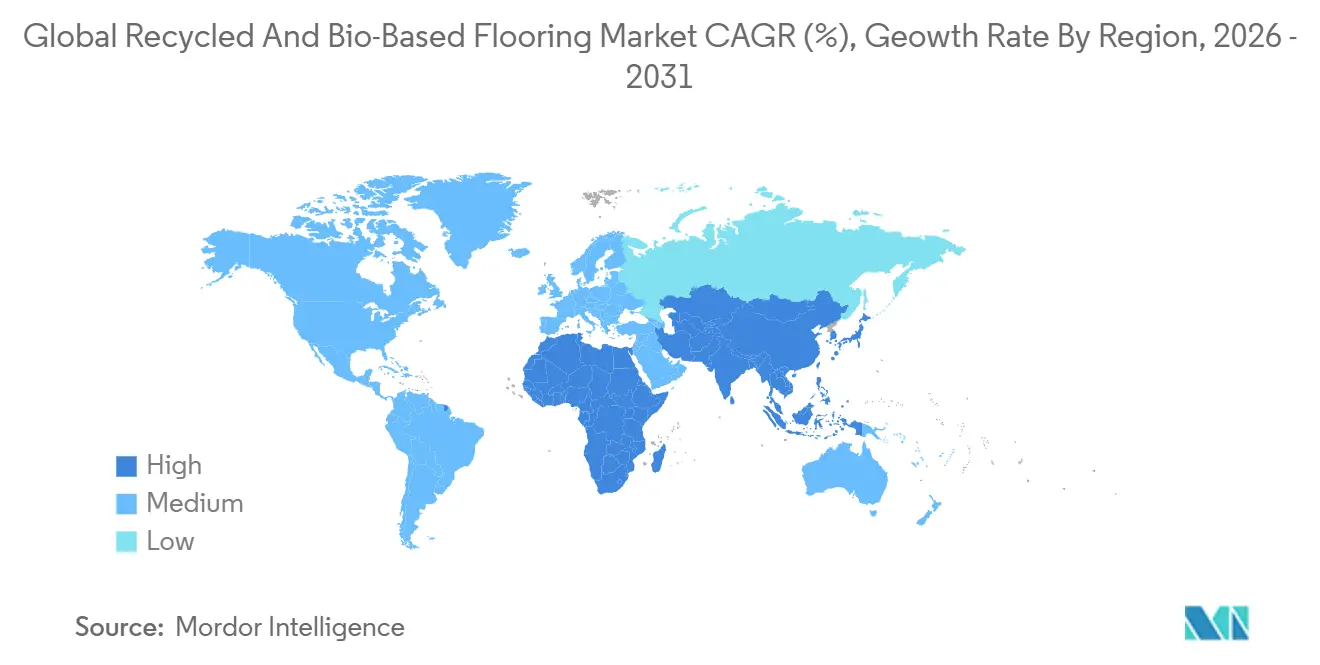

- By geography, Europe accounted for 30.04% of the global recycled and bio-based flooring market in 2025, while Asia-Pacific is projected to expand at an 8.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recycled and Bio-Based Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-Building Certification Push | +1.2% | Global, concentrated in North America, the EU, and developed Asia-Pacific | Short term (≤ 2 years) |

| Extended Producer Responsibility (EPR) Incentives | +0.9% | Europe, early adoption in select North American jurisdictions | Medium term (2-4 years) |

| Corporate Sustainable-Sourcing Mandates | +1.1% | Global, led by multinational portfolios in North America and the EU | Short term (≤ 2 years) |

| Bio-Polymer Cost Parity With PVC | +0.8% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Chemical Recycling of Post-Use Vinyl Tiles | +1.5% | Europe and North America first, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Blockchain Traceability for Recycled Content | +1.4% | EU and United Kingdom earliest due to digital passports, expanding to North America and APAC majors. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Green-Building Certification Push

LEED v5 tightened embodied-carbon expectations for building materials. It raised documentation thresholds for material health, making third-party Environmental Product Declarations (EPD) a practical requirement for specification in many commercial projects seeking points. BREEAM International assigns credits for products that meet defined recycled-content and low-carbon criteria, which directs specifiers toward resilient, carpet, and wood systems with verified declarations and traceable inputs[2]BRE Group, “BREEAM International,” Building Research Establishment, breeam.com. The WELL Building Standard v2.1 raises transparency by recognizing labeling and health product declarations that disclose ingredients to a fine threshold, and those expectations influence interior finish schedules across large project portfolios. These programs align with ISO 14021 on environmental claims and ISO 14025 on product declarations, providing procurement teams with a common language and method for comparing flooring alternatives. Public and institutional buyers in key jurisdictions reference these frameworks in bid documents, which increases demand for flooring with verified EPDs and supply-chain data in the global recycled and bio-based flooring market.

Extended Producer Responsibility (EPR) Incentives

France’s EPR framework for building products requires flooring producers to participate in accredited eco-organizations that finance collection, sorting, and material recovery, with fees scaled to recyclability and design choices that facilitate end-of-life processing. The Netherlands operates a flooring take-back scheme that imposes a levy on virgin-content LVT while granting relief for certified recycled-content ranges, nudging procurement toward circular designs. The EU’s revision of the construction products regulation introduces a digital product passport in 2027 that embeds provenance, recycled-content data, and end-of-life information, harmonizing reporting and improving traceability across member states. Manufacturers that invested early in reverse logistics and processing capacity are positioned to meet collection and material validation requirements as they tighten in the global recycled and bio-based flooring market. Fee signals and disclosure rules together reinforce design-for-disassembly and mono-material approaches, thereby enhancing the practical recyclability of installed flooring across repeated life cycles.

Corporate Sustainable-Sourcing Mandates

Gensler’s global procurement standard v2.1 requires suppliers to provide product-specific EPDs and documented environmental management systems, underscoring the importance of audited data and verified declarations for flooring vendors. The corporate sustainability directive applies to large companies in Europe and adds Scope 3 disclosure expectations for purchased goods and services, including tenant-improvement finishes such as flooring. United States federal purchasing guidance directs agencies toward recognized ecolabels and standards, effectively channeling public demand to products with third-party verification and certified feedstocks. Together, these policies and buyer standards accelerate the use of EPDs, recycled-content claims, and take-back agreements in bids, which influences who makes shortlists for large commercial fit-outs in the global recycled and bio-based flooring market. Suppliers that can demonstrate verifiable carbon intensities and credible end-of-life solutions tend to progress more quickly through prequalification under these programs.

Bio-Polymer Cost Parity With PVC

Capacity scale-up plans for PHA production target performance niches that require moisture resistance and support broader substitution in resilient assemblies over the forecast period[3]Danimer Scientific, “Form 10‑K 2025,” U.S. Securities and Exchange Commission, sec.gov. Partnership work on bio-based precursors for performance polymers signals continued process innovation that can reduce fossil-based inputs in carpet and resilient flooring chains. Certification frameworks such as ISCC PLUS now cover bio-circular and mass-balance claims for PVC production, which enables LVT producers to document and communicate carbon-intensity reductions to specifiers. Bio-attributed PVC shows significant reductions in cradle-to-gate emissions compared with conventional PVC, informing procurement decisions where embodied-carbon limits or credits are in place. LVT collections introduced by leading manufacturers make use of bio-attributed feedstocks to offer lower-carbon alternatives while maintaining installation speed and design variety in the global recycled and bio-based flooring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing vs. Conventional Flooring | -0.7% | Global, heightened sensitivity in India, Southeast Asia, and Latin America | Short term (≤ 2 years) |

| Durability Concerns in Heavy-Duty Settings | -0.6% | Global, strongest in industrial and high-traffic commercial environments | Medium term (2-4 years) |

| Feed-Stock Price Volatility | -1.2% | Global, tighter in North America and Europe, where secondary feedstock markets are more liquid | Short term (≤ 2 years) |

| Take-Back and Reverse-Logistics Gaps | -0.6% | North America outside EPR states, emerging Asia-Pacific, Latin America, and Africa. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing vs. Conventional Flooring

Price premiums persist for recycled-content and bio-based ranges due to feedstock sorting, quality control, and the capital intensity of newer processing systems, which delays parity at scale in cost-sensitive projects. Supply remains subscale for key bio-polymers relative to legacy resins, which limits the volume discounts that large buyers expect in mainstream specifications. Some public programs provide favorable treatment for certified recycled content, yet adoption in residential and lower-budget commercial segments can be cautious until installed costs narrow relative to conventional alternatives in the global recycled and bio-based flooring market. The EU’s Carbon Border Adjustment Mechanism phases in tariffs on imports that are embodied-carbon intensive, which can change near-term price comparisons for vinyl-based products across regional supply chains. As digital product passports and EPR rules standardize traceability, information asymmetries should decline, thereby supporting procurement decisions that reward verified circular attributes over time.

Durability Concerns in Heavy-Duty Settings

Specifiers remain cautious about wear-layer performance and long-term stability for certain bio-based and recycled formulations in high-traffic areas that demand strict moisture-emission controls and heavy rolling-load performance. Clear classification and warranty expectations continue to point toward products tested and labeled under recognized standards such as ISO 10874, which drives demand for third-party documentation across recycled and bio-based SKUs. Recycled rubber solutions face limits on allowable PAH concentrations in indoor uses, which often require blending strategies and add processing steps to meet compliance thresholds. Field validation data for newer circular feedstock streams is still being collected, which makes some institutional buyers cautious when approving alternatives to long-entrenched vinyl or ceramic systems in the global recycled and bio-based flooring market. Recent chemical-recycling investments and take-back programs are expanding the installed base of circular flooring, providing more evidence over time of durability in demanding environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LVT Dominance Meets Hardwood Disruption

LVT commanded 38.41% of the global recycled and bio-based flooring market share in 2025 as innovations in chemical recycling and mass-balance attribution opened pathways for circular PVC feedstocks to meet project specifications at scale. Investments such as Project Circle are designed to recover and purify post-use vinyl for reintroduction into flooring resins, which helps reduce variability and sustain quality in reprocessed inputs. Engineered wood and bamboo are set to be the fastest-growing product category, with a 11.41% CAGR through 2031, as mass-timber adoption expands and specifiers seek bio-based finishes that align with low-carbon structures in the global recycled and bio-based flooring market. Rubber flooring derived from reclaimed tire crumb continues to serve fitness, education, and healthcare settings where safety and resilience take priority, and new investment is scaling reclamation and processing capacity for circular rubber solutions. Linoleum and cork retain a role where buyers value bio-based content and low emissions, supported by policy incentives in select markets that recognize low embodied-carbon materials. The emergence of bio-attributed PVC feedstocks backed by ISCC PLUS claims is enabling LVT lines to report lower cradle-to-gate carbon figures without compromising installation speed or pattern variety.

Looking ahead, rubber’s growth trajectory is reinforced by capital inflows that expand take-back programs and manufacturing for high-demand commercial interiors, a trend that adds reclaimed volumes and reduces waste sent to landfills. Hardened-wood platforms backed by significant investment are targeting heavy-traffic applications that were once the domain of resilient products, broadening the application scope for engineered wood in offices and retail. LVT suppliers are also advancing through bio-attributed collections that document meaningful reductions in embodied carbon while maintaining broad design libraries that support commercial branding needs. With each investment and certification milestone, the global recycled and bio-based flooring market builds a deeper installed base to validate lifecycle claims, thereby improving confidence among specifiers for both resilient and wood-based products.

By Material Source: Plastics Lead, Polymers Surge

Recycled plastics, including PET and PVC, accounted for 33.13% of volumes in 2025, as established bottle-to-flake-to-flooring channels and improved traceability supported procurement at scale in the global recycled and bio-based flooring market. Bio-based polymers such as PLA and PHA are projected to grow at the fastest 11.93% CAGR to 2031, supported by capacity scale-ups and expanding application ranges in resilient assemblies. Digital material provenance platforms are adding batch-level verification for recycled content and chain-of-custody details, helping manufacturers and buyers meet emerging digital passport requirements. Certification under ISCC PLUS for bio-circular and mass-balance claims allows PVC suppliers to attribute bio-based inputs to finished resin streams with clear rules and third-party oversight. Bio-attributed PVC and downstream LVT collections show how supply partners are translating certified feedstocks into lower-carbon floors that fit mainstream commercial specifications.

Over the forecast period, safety constraints on crumb rubber, including limits on PAH concentrations for indoor applications, will shape compounding choices and may require blending to stay within regulatory thresholds. PHA capacity expansion plans underscore how non-edible feedstocks and process improvements can broaden the use of bio-polymers in performance-sensitive, resilient products over time in the global recycled and bio-based flooring market. Policymakers continue to align fee structures with circularity goals, which may improve end-of-life economics as take-back and sorting infrastructure matures. The combination of traceability platforms, certification schemes, and recycling investments is bringing more reliable secondary feedstock to market, helping buyers compare options on verified metrics rather than marketing claims.

By End User: Commercial Giants, Residential Awakens

The commercial segment accounted for 88% of volumes in 2025 and is projected to post a 9.57% CAGR through 2031 as corporate Scope 3 programs and building rating systems move buyers toward verified, low-carbon, and take-back-ready specifications in the global recycled and bio-based flooring market. Certification frameworks and owner standards that reference EPDs and product disclosures influence procurement for offices, healthcare, and education, where project teams seek clear documentation for embodied-carbon and material health claims. Leasing and service models are gaining traction in commercial settings because they align budgets with replacement cycles and require contractual take-back, which supports circular objectives. Portfolio strategies are also expanding to include PVC-free, resilient options, with suppliers advertising recyclability and take-back programs to support project documentation and asset-management goals.

Residential demand remains smaller than commercial, but is adapting as homeowners and developers weigh ease of installation, warranty coverage, and sustainability credentials during product selection in the global recycled and bio-based flooring market. E-commerce growth and visualization tools are changing how shoppers evaluate resilient and wood options, which expands the reach of certified offerings beyond showrooms and into online channels. Where public or utility programs recognize low-emission and low-carbon surfaces, residential adopters can use documented attributes as part of broader energy or wellness upgrades in renovations. Over time, expanding take-back logistics in commercial hubs may create secondary channels for refurbishment and reuse, which can inform future models that span mixed-use portfolios and build wider circular ecosystems.

By Distribution Channel: B2B Contractors Dominate, Retail Evolves

B2B and contractor channels captured 86.35% of volumes in 2025 and are projected to grow at 10.16% CAGR as integrated project delivery and specification standards consolidate purchasing around suppliers who can furnish EPDs, HPDs, and verified take-back plans in the global recycled and bio-based flooring market. Large design firms’ procurement standards require product-level documentation for bids, incentivizing contractors to prequalify manufacturers with robust sustainability files. Service-based models, such as flooring-as-a-service, shift upfront spending into operating budgets and embed uplift and reuse clauses that align with circular goals at the end of the term. B2C and retail channels, which represent the remaining share, are evolving through online assortments and delivery-to-install offerings that bring specification-grade products into residential projects.

Over the forecast period, B2B channels continue to benefit from policy instruments that reward documented circularity and low emissions, which are easier to operationalize in large projects with formal procurement and reporting teams. Specialty retailers remain relevant when projects require site assessments, substrate preparation, and acoustics guidance beyond simple product sales, which anchors a consultative role in high-complexity residential and small commercial work. As vendors expand direct digital engagement, the global recycled and bio-based flooring market will likely see more coordinated specification support, including data packages that speed submittals and approvals for low-carbon and recycled-content floors. Regulatory reporting and digital product passports should also enhance B2B demand visibility, thereby improving planning for take-back routes and recycling capacity over time.

Geography Analysis

Europe led with a 30.04% share in 2025, supported by policy actions that prioritize traceability, recycled content, and verifiable environmental claims in the global recycled and bio-based flooring market. The EU’s revision of the Construction Products Regulation will introduce digital product passports in 2027, embedding provenance, recycled content, and end-of-life data into QR-linked records for all covered construction products, including flooring. France’s EPR framework ties fees to recyclability, while the Netherlands’ take-back scheme levies on virgin-content products and relieves verified recycled-content products, helping shift procurement toward circular choices. Denmark offers rebates for documented low-carbon floors, which provide a direct financial incentive for bio-based and recycled options with verified footprints. Certification and reporting frameworks reinforce these shifts by making verified data central to both project scoring and corporate disclosures.

Asia-Pacific is projected to post an 8.82% CAGR through 2031, driven by urban projects and policy roadmaps that elevate material transparency and carbon performance. China’s dual-carbon policy continues to guide investment and specification standards that favor low-emission materials with documented attributes. Singapore’s Green Mark program recognizes product-level declarations and supports broader adoption of EPD-backed finishes in new buildings and major retrofits. Regional manufacturing footprints are also adapting to international sustainability expectations, including local production that incorporates certified bio-attributed content to serve both export and domestic projects. Australia’s public and education sectors show strong interest in leasing and take-back models that support circular outcomes, which help scale verified low-carbon floors in the region.

In North America, institutional procurement guidance directs federal agencies toward recognized ecolabels and standards, which channels significant demand to products with verified environmental claims and recyclability pathways in the global recycled and bio-based flooring market. British Columbia’s building-code updates that support mass-timber construction are helping to broaden the uptake of bio-based finishes and complementary low-carbon floor systems across Canada. Infrastructure funding across public facilities is enlarging bid pipelines for compliant surfaces that meet durability, emissions, and circularity requirements. In several Middle Eastern projects, green-building aspirations continue to shape interior finish choices, while parts of Latin America face cost and tariff structures that influence price comparisons against standard vinyl, which affects adoption pacing where budgets are constrained. Across regions, the trajectory of digital product passports and EPR-style collection rules will be a core determinant of how quickly traceable recycled inputs scale and how consistently take-back services operate for installed floors.

Competitive Landscape

The global recycled and bio-based flooring market is experiencing moderate consolidation, with leading groups accounting for a meaningful share, while regional specialists serve niche categories and local channels. Competitive strategies focus on feedstock verification, take-back infrastructure, and certification breadth, which together shorten approval cycles for large commercial projects. ISCC PLUS mass-balance claims are becoming a standard in procurement files for bio-attributed PVC and related inputs, and suppliers with certified chains of custody tend to advance more quickly in specifications[4]ISCC System, “Mass Balance and Bio-Circular Certification,” ISCC System, iscc-system.org. PVC-free resilient lines with recyclability and documented carbon profiles reflect how large brands are positioning around circularity and end-of-life stewardship to win bids that require evidence of material recovery pathways. Flooring-as-a-service models are emerging as a differentiator by bundling uplift and reuse, although these offers remain early outside a few markets with demonstrated traction.

Capital flows support consolidation and technology deployment, where circular feedstock control and process IP represent defensible moats in the global recycled and bio-based flooring market. Investments in industrializing hardened-wood platforms and scaling reclaimed rubber operations indicate investor confidence that low-carbon flooring categories can maintain pricing power as documentation and recovery logistics improve. Blockchain-based traceability adds a digital layer to material provenance claims, with early deployments aimed at supporting digital passport requirements and enhancing auditability across complex supply chains. Partnerships between flooring manufacturers and waste-processing innovators, including biological treatments for legacy scrap, are expanding the toolkit for diverting post-use materials away from landfills.

Product development teams are integrating sustainability documentation alongside traditional performance metrics, which helps satisfy standards for environmental declarations, antimicrobial efficacy, and construction product reporting. As architects and global design firms embed EPD and EMS requirements into bid packages, suppliers without audited systems or comprehensive declarations face tighter access to marquee projects. Polymer suppliers and flooring brands adopting ISCC PLUS and related schemes are now more aligned with public and private buyers who expect verified chains of custody and clear mass-balance accounting for bio-attributed claims. These shifts support the long-term expansion of certified circular products in the global recycled and bio-based flooring market and raise the bar for data transparency throughout the specification and procurement cycles.

Recycled and Bio-Based Flooring Industry Leaders

Tarkett S.A.

Interface Inc.

Armstrong Flooring LLC

Forbo Holding AG

Mohawk Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SMX launched its Digital Material Provenance Platform to enable QR-code verification of batch-level recycled content and support EU digital product passport compliance across early flooring supply-chain deployments.

- March 2026: Mutares completed the acquisition of the Hamberger Industriewerke flooring business (HARO), adding parquet, laminate, design flooring, and sports flooring manufacturing in Germany and Bulgaria with plans to expand the portfolio and international reach.

- March 2025: Tarkett formalized its partnership with Avery Automats to recycle all post-use LVT collected through the ReStart program into automotive floor mats, diverting 2.1 million pounds of flooring waste from landfills in 2024 and establishing a revenue-positive reverse-logistics model that satisfies Extended Producer Responsibility compliance in France and the Netherlands

Global Recycled and Bio-Based Flooring Market Report Scope

| Luxury Vinyl Tiles (LVT) |

| Rubber Flooring Rolls & Tiles |

| Linoleum & Cork Sheets |

| Engineered Wood & Bamboo Planks |

| Others |

| Recycled Plastics (PET, PVC) |

| Recycled Rubber (Tire-derived) |

| Recycled Wood Fiber |

| Bio-based Polymers (PLA, PHA etc.) |

| Bio-derived Cork & Linoleum |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Luxury Vinyl Tiles (LVT) | |

| Rubber Flooring Rolls & Tiles | ||

| Linoleum & Cork Sheets | ||

| Engineered Wood & Bamboo Planks | ||

| Others | ||

| By Material Source | Recycled Plastics (PET, PVC) | |

| Recycled Rubber (Tire-derived) | ||

| Recycled Wood Fiber | ||

| Bio-based Polymers (PLA, PHA etc.) | ||

| Bio-derived Cork & Linoleum | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the global recycled and bio-based flooring market?

The global recycled and bio-based flooring market size is expected to increase from USD 55.83 billion in 2025 to USD 58.17 billion in 2026 and reach USD 75.78 billion by 2031 at a 5.4% CAGR over 2026–2031.

Which region leads and which is growing fastest in this space?

Europe led with 30.04% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at an 8.82% CAGR through 2031.

Which product category has the largest share and which will grow fastest?

LVT held 38.41% share in 2025, and engineered wood and bamboo are projected to grow fastest at an 11.41% CAGR through 2031.

Who are the primary buyers and channels today?

Commercial end users accounted for 88% of volumes in 2025 and are set to grow at 9.57% CAGR, while B2B and contractor channels captured 86.35% of volumes and are projected to expand at 10.16% CAGR.

How are certification and policy shaping specifications?

LEED v5, BREEAM, WELL, CSRD, and EPA purchasing guidance are steering buyers toward products with EPDs, verified recycled content, and take-back programs, which strengthen demand for certified circular solutions.

What near-term challenges could slow adoption?

Price premiums, uneven take-back rules, and durability concerns in heavy-traffic settings remain the main hurdles, although certification, EPR programs, and digital product passports are improving data quality and end-of-life economics.

Page last updated on: