Mayonnaise Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.24 Billion |

| Market Size (2031) | USD 16.04 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

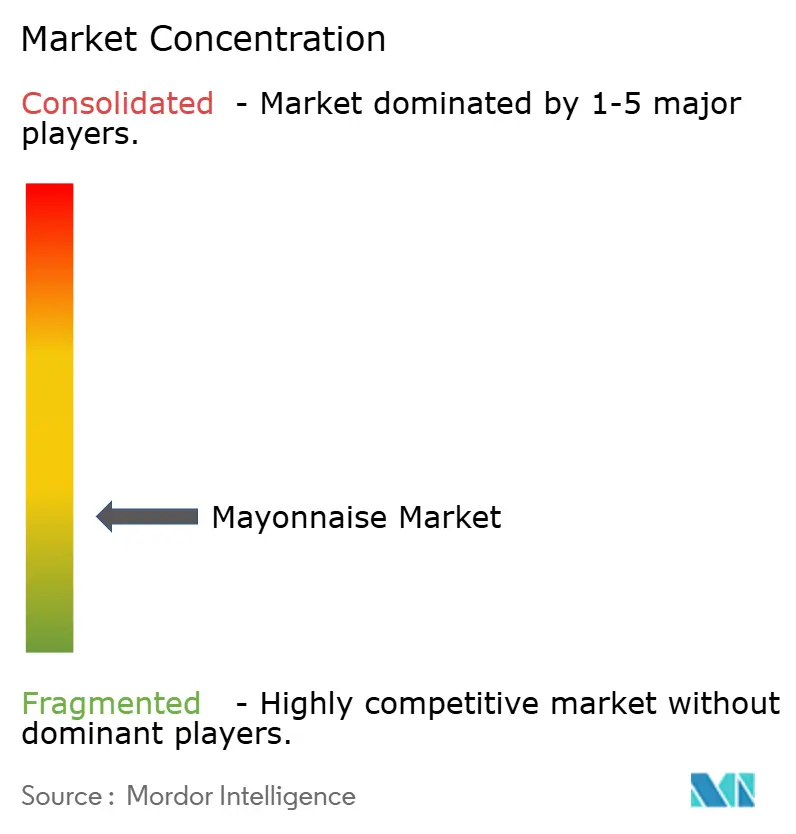

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mayonnaise Market Analysis by Mordor Intelligence

The mayonnaise market size was valued at USD 12.73 billion in 2025 and estimated to grow from USD 13.24 billion in 2026 to reach USD 16.04 billion by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). The steady rise reflects strong household usage, rising institutional demand, and broader flavor experimentation across retail and foodservice. The U.S. restaurant sector is expected to generate USD 1.5 trillion in sales in 2025, supporting dependable bulk condiment demand for the Mayonnaise market through quick-service and casual-dining channels, according to the National Restaurant Association[1]Source: National Restaurant Association, “2025 State of the Restaurant Industry Report,” National Restaurant Association, restaurant.org. Urban growth in Asia-Pacific and Latin America is also widening household consumption for the Mayonnaise market in places where penetration was lower in the past. Egg and vegetable oil cost swings have pushed the Mayonnaise market toward eggless recipes, alternative oil sourcing, and tighter supply planning across manufacturers. The planned combination of Unilever Foods with McCormick could further reshape shelf competition, contract supply terms, and private label pressure across the Mayonnaise market.

Key Report Takeaways

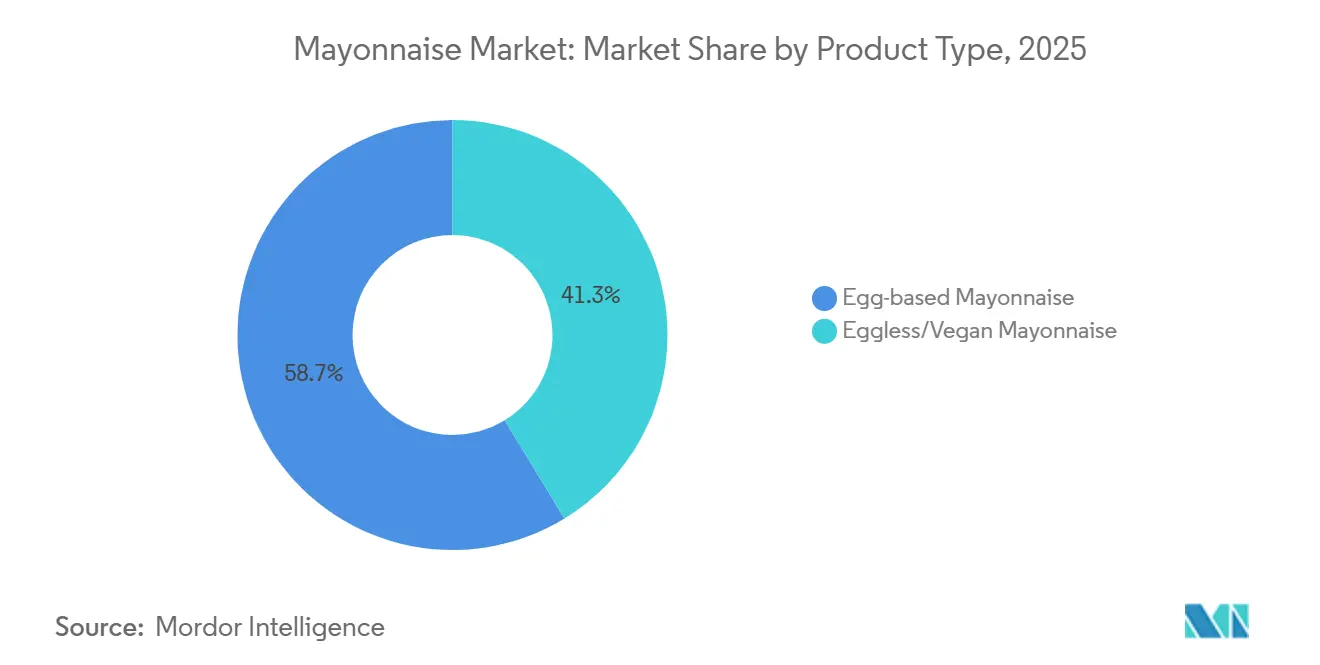

- By product type, egg-based mayonnaise accounted for 58.73% of the global market share in 2025, while eggless and vegan mayonnaise is expected to post the highest projected CAGR of 4.67% through 2031.

- By category, plain mayonnaise led with 63.56% revenue share in 2025, while flavored mayonnaise is forecast to expand at a 4.75% CAGR through 2031.

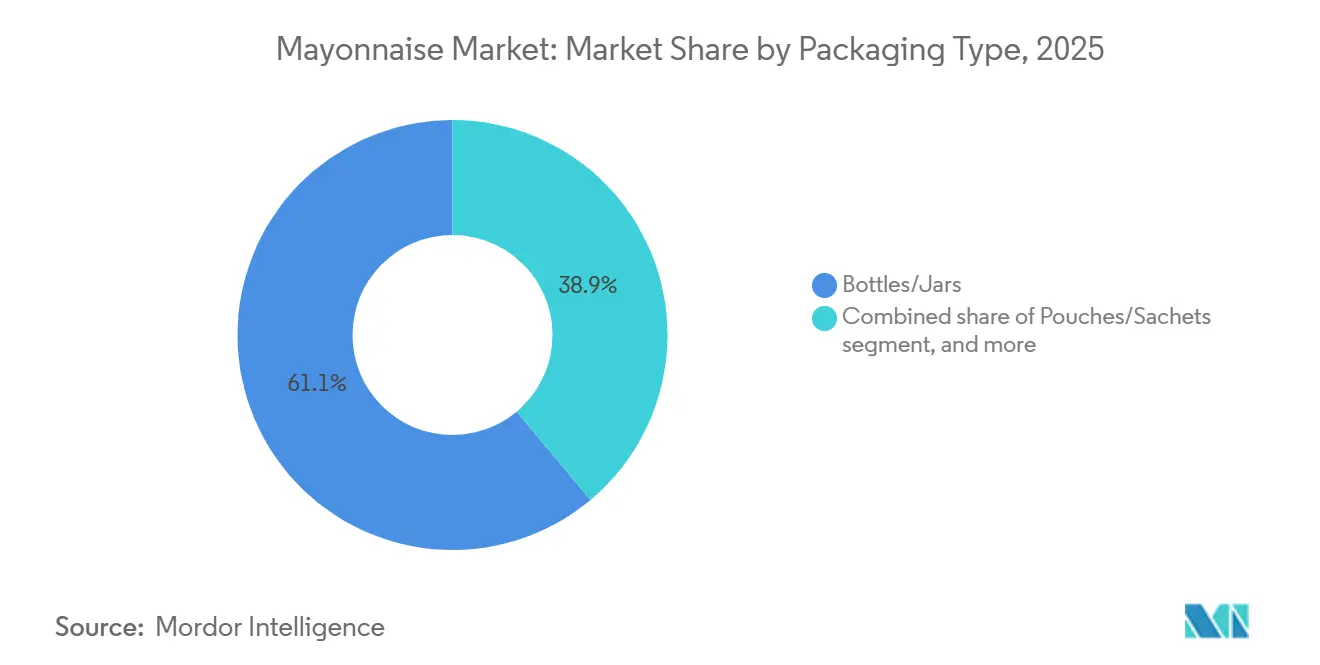

- By packaging type, bottles and jars accounted for 61.08% of the market share in 2025, while pouches and sachets are advancing at a 5.19% CAGR through 2031.

- By end user, household and retail consumers held 44.36% share in 2025, while HoReCa and foodservice posted the highest projected CAGR at 4.38% through 2031.

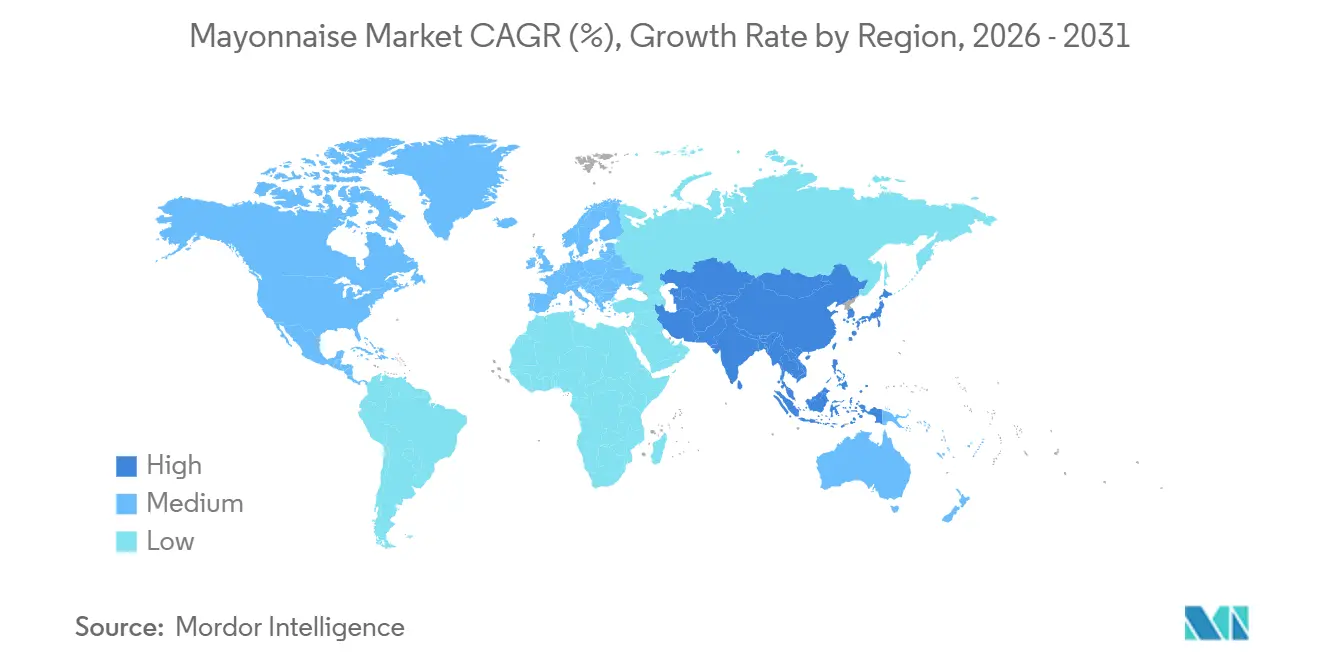

- By geography, North America held 41.72% of the Mayonnaise market share in 2025, while Asia-Pacific recorded the fastest expansion in the Mayonnaise market size at 4.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mayonnaise Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenience Condiments | +0.7% | Global | Short term (≤ 2 years) |

| Expansion of Foodservice and Quick Service Menus | +0.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing Popularity of Flavored Mayonnaise Variants | +0.6% | North America, Europe, Japan, Australia | Short term (≤ 2 years) |

| Packaging Innovation in Squeeze Bottles and Portion Packs | +0.5% | Global, early gains in QSR-dense markets | Medium term (2-4 years) |

| Premiumization Through Gourmet and Clean Label Mayo | +0.4% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Growing Demand for Eggless and Vegan Mayonnaise | +0.5% | Global, accelerating in Europe, India, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience condiments

Consumer shift toward ready-to-eat meals and on-the-go eating has repositioned mayonnaise from a cooking ingredient into a finishing condiment, dramatically expanding usage occasions. USDA data shows total food sales at US foodservice outlets reached USD 1.52 trillion in 2024, with USD 550.7 billion from limited-service establishments that rely on standardized sauces for consistent taste. The implication that most analysts miss is the "back-of-house reformulation" effect: as QSRs move toward central kitchen models, they increasingly co-develop proprietary mayo-based sauces and aioli blends with branded manufacturers under multi-year supply contracts, locking in volume and effectively insulating category revenue from household budget pressures. Sandwich, burger, and wrap formats that have become global meal defaults embed mayonnaise as a structural ingredient rather than an optional condiment, reducing demand elasticity. This structural embeddedness means that even in cautious consumer spending environments, volume tends to be preserved, shifting competitive pressure onto pricing and margins rather than unit demand.

Expansion of foodservice and quick service menus

QSR and fast-casual expansion across Asia, the Middle East, and Latin America is creating new institutional demand for mayonnaise in markets where household penetration remains low. The National Restaurant Association's 2025 report records that 64% of full-service and 47% of limited-service customers consider the dining experience more important than price, a dynamic that directly incentivizes operators to invest in premium sauces and condiments as differentiation tools. What is less commonly discussed is that QSR menu proliferation now functions as a category trial mechanism: consumers who encounter flavored mayo dips or aioli blends at restaurant chains frequently replicate those applications at retail, pulling volume upmarket. In 2026, Kewpie Singapore's sales executive confirmed rapid growth in ready-to-eat meal applications, including sachet formats supplied to McDonald's and NTUC FairPrice, demonstrating how foodservice serves as a distribution channel into new usage occasions. Bulk-pack and institutional formats, which carry higher per-kilogram margins for manufacturers, are growing in step with foodservice outlet counts.

Increasing popularity of flavored mayonnaise variants

Flavored mayonnaise is the single most commercially active sub-segment in the category right now, functioning as a high-margin trade-up that offsets any volume softening in standard variants. Unilever's data shows Hellmann's flavored portfolio sales nearly doubled in 2023, with the segment crossing 7% of total US mayonnaise dollar sales by early 2026[2]Source: Unilever PLC, “Unilever Foods to Combine with McCormick,” Unilever Investor Relations, unilever.com. The non-obvious dynamic is that flavor extension is also a loyalty mechanism: Hellmann's Canada's "Starting Five Flavors" campaign (chipotle, garlic, spicy, buttermilk-ranch, garlic-parmesan), activated with Toronto Raptors player Brandon Ingram in February 2026, targets younger consumers who associate condiment variety with food identity rather than culinary utility. Heinz simultaneously launched flavored Mayonnaise-Style Sauces in Canada in August 2025 (Smoky Bacon, Garlic Parmesan, Mango Habanero, Pickle), explicitly designed to eliminate the need for consumers to mix mayo with separate condiments. Asian-inspired and Mediterranean flavor profiles, sriracha, wasabi, truffle, and chipotle, are proving particularly sticky across demographics, suggesting this is a structural consumer shift rather than a passing trend.

Packaging innovation in squeeze bottles and portion packs

Packaging innovation is delivering both consumer convenience and improved manufacturer margins, making it one of the more commercially underestimated drivers in the category. The Association for Dressings & Sauces awarded McCormick's Frank's RedHot Squeeze Sauce its 2025 Package of the Year award, recognizing a flip-top closure using 50% post-consumer recycled (PCR) plastic that combines on-trend sustainability credentials with one-handed dispensing precision. MasterFoods (Mars) in Australia piloted paper-based squeeze-on packs between November 2024 and April 2025, representing five years and USD 3 million in research and development, validating that paper substrates can handle high-viscosity condiment formulations at a commercial scale. The QSR single-serve sachet format is gaining ground across food delivery and catering: portioned sachets reduce waste, simplify logistics, and support the premiumization of branded condiments over unlabeled restaurant-supplied options. Develey's 2026 expansion of light mayo in waste-saving pouches (featuring 60% less fat) illustrates how the same packaging innovation simultaneously addresses sustainability mandates and consumer health perceptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Perception Around Fat, Calories, and Oil Content | -0.3% | North America, Western Europe | Medium term (2–4 years) |

| Raw Material Volatility in Eggs and Vegetable Oils | -0.5% | Global | Short term (≤ 2 years) |

| Shelf-Life Sensitivity in Cleaner-Label Formulations | -0.2% | Europe, North America, Australia | Medium to long term (≥ 4 years) |

| Regulatory Pressure on Additives and Preservatives | -0.2% | Europe, North America, India | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Health perception around fat, calories, and oil content

Consumer concern about high-fat and calorie content creates a persistent demand headwind, particularly in health-conscious North American and Western European markets. The WHO's global initiative to reduce average sodium intake by approximately 30% by 2025 has prompted EU member states to set maximum salt content targets for sauces and condiments as part of national reformulation programs, adding regulatory complexity to already challenging clean-label projects. The more instructive dynamic, however, is how leading manufacturers are converting the health concern into a format and positioning opportunity: Kewpie's 2026 reformulation of "Kewpie Half" (its reduced-calorie variant) to a richer egg-yolk base, the same as its full-fat product, shows a counter-intuitive route to retention of the health-seeking consumer through quality improvement rather than ingredient reduction. Premium oil substitution (avocado, EVOO) is also proving effective, with brands such as Primal Kitchen and Ayoh repositioning mayo as a source of "good fats" to capture health-motivated buyers who might otherwise abandon the category. This health-to-premium conversion partially offsets volume attrition with value growth.

Raw material volatility in eggs and vegetable oils

Raw material cost instability represents the most acute short-term margin risk for mayonnaise manufacturers globally. HPAI outbreaks in the US forced producers to cull approximately 168 million birds between February 2022 and early 2025, with egg prices peaking at a wholesale high of USD 8.53 per dozen in New York in early 2025 before USDA's five-pronged containment strategy drove wholesale prices down over 90% from their peak[3]Source: U.S. Department of Agriculture, “Secretary Rollins Provides Update on Bird Flu Strategy, Egg Prices Continue to Fall,” U.S. Department of Agriculture, usda.gov . On the vegetable oil side, the US Bureau of Labor Statistics' Producer Price Index for crude vegetable oils reached 206.2 in April 2026, up from 190.7 in December 2025, partly driven by biofuel blend mandates in Brazil and Indonesia that have redirected soybean and palm oil from food to energy applications. The supply-side compounding effect, where both principal inputs may face simultaneous upward pressure from non-food policy decisions, is not fully priced into long-term supply contracts, creating margin compression risks, particularly for smaller manufacturers without hedging programs. Finnish food-tech firm Solar Foods' patent application for a Solein protein-based mayo (derived from CO₂ fermentation) that produces approximately 3 times more mayonnaise per unit of input material than conventional egg yolk powder signals a longer-term industry response to this structural vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Egg-Based Dominance Intact as Vegan Alternatives Accelerate

Egg-based mayonnaise held 58.73% of the mayonnaise market share in 2025, while eggless and vegan mayonnaise is projected to grow at 4.67% CAGR through 2031. Traditional taste preferences still anchor the segment, especially where mayonnaise is used as a staple spread and a cooking support ingredient. The legal standard of identity in the United States also helps preserve the role of egg-based recipes in the mainstream Mayonnaise market. Even so, the egg shock of 2024 and 2025 improved the visibility and relative affordability of plant-based alternatives across retail shelves.

Plant-based positioning is widening the audience beyond strictly vegan buyers, which matters for the long-term shape of the mayonnaise industry. Scientific work published by ICAR showed that oyster mushroom powder can support vegan mayonnaise with strong oxidative stability and favorable acceptability, which reinforces the technical viability of non-egg formulations. Solar Foods has also argued that its Solein protein platform can produce materially more mayonnaise per unit of input than conventional egg yolk powder, suggesting a different supply logic for the Mayonnaise market. These developments help the category serve vegetarian, flexitarian, and price-sensitive consumers without depending on one raw material pathway.

By Category: Plain Stability Masked by Flavored Category's Outperformance

Plain mayonnaise retains category dominance with a 63.56% value share in 2025, reflecting its embedded role as a household staple and QSR base formulation ingredient. Flavored mayonnaise is the fastest-growing category at 4.75% CAGR through 2026-2031, and its growth rate belies an even more significant strategic role: flavored variants are drawing new usage occasions, dipping, marinating, finishing, beyond the traditional spread application. Hellmann's Canada's launch of Dijonnaise in March 2026 exemplifies how premium flavored extensions are being designed for broader meal coverage; brand management at Unilever Canada explicitly positioned the product as shifting "mayo from a background ingredient to the main character".

Kewpie's 2026 reformulation of its "Kewpie Half" reduced-calorie variant to a richer egg-yolk-based recipe, while maintaining the calorie-reduction claim, illustrates how manufacturers are managing the tension between plain-category trade-down pressure and premiumization goals within a single SKU. The flavored segment is also uniquely resilient to private-label competition because of the research and development investment required to match branded flavor profiles, giving incumbents a defensible quality moat.

By Packaging Type: Bottles and Jars Sustain Volume While Pouches Signal a Structural Shift

Bottles and jars accounted for 61.08% of the global mayonnaise market by packaging value in 2025, reflecting the format's ubiquity on retail shelves in developed markets. Pouches and sachets are the fastest-growing format, with a 5.19% CAGR through 2026-2031, driven by three converging forces: QSR demand for portion-controlled single-serve formats, food delivery packaging requirements, and retailers' sustainability mandates to reduce waste. MasterFoods' Australian paper-based squeeze-on pack trial in November 2024 tested more than 1 million consumer units across sporting stadiums, petrol stations, and foodservice sites, validating the strong demand for sustainable sachet formats in commercial foodservice settings.

The Association for Dressings & Sauces' 2025 Package of the Year award to McCormick's Frank's RedHot Squeeze Sauce, incorporating 50% post-consumer recycled plastic, signals that sustainability credentials within bottles are now a purchasing criterion for major retail buyers. Squeeze bottles also remain a core format for foodservice: Develey's 2026 expansion of mayo in waste-saving pouches (a 60% lower-fat variant) in Germany demonstrates how mid-tier European manufacturers are using format innovation to simultaneously address sustainability and consumer health concerns. Tubs and bulk packs maintain steady demand from food-industrial and HoReCa channels, where minimising per-unit cost is paramount.

By End User: Retail Anchors Volume; HoReCa Drives the Value Narrative

Household and retail consumers held the largest end-user share at 44.36% in 2025, anchored by supermarket and hypermarket distribution in North America and Europe, where mayonnaise is a high-frequency repeat purchase. The HoReCa and foodservice segment is forecast to grow fastest at a 4.38% CAGR through 2026-2031, as restaurant operators increasingly standardize condiment specifications and leverage branded mayo for menu differentiation. A counterintuitive insight is that retail's absolute dominance masks a fragmentation into sharply divergent sub-channels: online retail is growing at a multiple of the brick-and-mortar rate as consumers stock specialty premium products, avocado oil mayo, clean-label organic variants, that are too niche for full supermarket ranging.

Specialty and gourmet store penetration for premium-tier products (Primal Kitchen, Graza EVOO mayo at USD 8.99-12.99 per unit) is outpacing conventional channel growth, pulling average selling prices upward across retail. For food manufacturers and industrial users, who represent a critical volume-stabilizing segment, the shift toward clean-label ingredients is creating reformulation work but also upstream supply opportunities for brands that can meet specifications without synthetic emulsifiers. Ybarra's 2025 launch of "Ybarra Experience", 4 gourmet HoReCa mayo and sauce variants (Chipotle Ahumado, Jalapeño Asado, Trufa, Cebolla Caramelizada), exemplifies the growing HoReCa sub-segmentation between commodity bulk and premium chef-grade products.

Geography Analysis

North America accounted for 41.72% of the global mayonnaise market in 2025, supported by high household penetration, a dense QSR network, and mature grocery distribution. The region remains the largest base for the Mayonnaise market because mayonnaise is embedded in daily meal formats and institutional menus. Canada is also seeing stronger premium and flavor activity, with Kraft Heinz adding 4 mayo-style sauce variants in 2025 to widen usage and lift category appeal. Europe is mature, but it stays active through reformulation, packaging upgrades, and export-oriented manufacturers that compete on product quality and channel discipline.

Asia-Pacific is the fastest-growing region, and its share of the Mayonnaise market is projected to expand at a 4.59% CAGR through 2031. Growth comes from different demand patterns across Japan, China, India, and Southeast Asia rather than from a single regional model. India was valued at USD 522 million in 2025, with momentum supported by QSR expansion in Tier 1 and Tier 2 cities and strong consumer openness to eggless formats. Kewpie also began full production on new manufacturing lines in Thailand and Indonesia in January 2025, strengthening the local supply of sauces and dressings across Southeast Asia. The Mayonnaise market in Asia-Pacific is also benefiting from exposure to Western menu formats while adapting products to local flavor expectations.

South America and the Middle East and Africa present different but complementary growth paths for the Mayonnaise market through 2031. In South America, rising urban foodservice demand is helping volume, even as firmer edible oil costs keep pressure on local manufacturing margins. In the Middle East, tourism and international restaurant chains are tying condiment demand more closely to foodservice growth and menu localization. African cities such as Nigeria, Egypt, and South Africa remain early-stage adoption corridors for the Mayonnaise market as modern retail access improves.

Competitive Landscape

The Mayonnaise market remains fragmented, with large multinational brands operating alongside regional specialists, country leaders, and private-label suppliers. The biggest structural move is the March 31, 2026 announcement that Unilever Foods will combine with McCormick in a USD 44.8 billion transaction, creating a condiments and flavor group with targeted annual revenue of USD 20 billion. If cleared, the deal could alter shelf negotiations, contract supply structures, and brand competition across North America, Europe, and Asia-Pacific. Even with that move, the Mayonnaise market does not center on a single dominant producer globally. Competitive intensity still comes from the constant overlap between branded scale, local taste adaptation, and retailer-owned products.

Capacity localization is another major strategy in the Mayonnaise market. Kewpie's U.S. subsidiary Q&B Foods ramped up its Clarksville, Tennessee, facility in 2025, which tripled North American mayonnaise and dressing production capacity and reinforced a regional manufacturing model. The company also expanded production in Thailand and Indonesia, showing that supply chain proximity is becoming a lasting competitive tool. Kraft Heinz used flavor-led extensions in Canada to defend shelf space and widen consumption occasions, which shows how incumbents are balancing scale with faster product refresh cycles.

The clearest white-space areas remain flavored variants in emerging Asian markets, mainstream-price plant-based products, and packaging that improves waste control. Solar Foods has already signaled how formulation technology may challenge egg-dependent production models through its Solein-based mayonnaise work. Chosen Foods also launched a national campaign around avocado-oil mayonnaise in 2026, showing how cleaner-oil positioning is becoming a visible point of differentiation. These moves suggest that the Mayonnaise market is competing through taste, ingredients, and format at the same time rather than through price alone.

Mayonnaise Industry Leaders

Unilever PLC

The Kraft Heinz Company

Kewpie Corporation

Nestlé S.A.

Sauer Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kewpie Corporation's US subsidiary Q&B Foods confirmed full operational ramp-up of its Clarksville, Tennessee plant, 60,000 tonnes annual capacity, the company's second US facility, which triples North American production capacity for mayonnaise and salad dressings, and was built on a USD 65 million investment.

- March 2026: Unilever and McCormick & Company announced a USD 44.8 billion combination of Unilever's Foods division, including Hellmann's, with McCormick, creating a global flavor and condiments group targeting USD 20 billion in annual revenue. The deal is expected to close by mid-2027, subject to regulatory approvals.

- August 2025: Kraft Heinz launched a new line of Heinz Mayonnaise-Style Sauces in Canada in 4 flavors: Smoky Bacon, Garlic Parmesan, Mango Habanero, and Pickle, targeting consumers who previously mixed standard mayo with other condiments for flavor customization.

- February 2025: Ybarra launched "Ybarra Experience," a premium HoReCa line of 4 gourmet sauces in 500 ml PET format, Chipotle Ahumado, Jalapeño Asado, Trufa, and Cebolla Caramelizada, distributed through Gallina Blanca Food Service channels.

Global Mayonnaise Market Report Scope

Mayonnaise is a thick, creamy condiment made by emulsifying oil with egg yolks or other ingredients, and is widely used in sandwiches, salads, dips, and other food preparations. The mayonnaise market is segmented by product type, category, packaging type, end user, and geography. By product type, the market includes egg-based mayonnaise and eggless/vegan mayonnaise. Based on category, the market is segmented into plain mayonnaise and flavored mayonnaise. By packaging type, the market covers bottles/jars, squeeze bottles, pouches/sachets, tubs/bulk packs, and other packaging formats. Based on end user, the market is categorized into HoReCa/foodservice, food manufacturers/industrial users, and household/retail consumers. The household/retail consumers segment is further divided into supermarkets/hypermarkets, convenience stores, online retail, and other retail channels. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD) and volume (tons).

| Egg-based Mayonnaise |

| Eggless/Vegan Mayonnaise |

| Plain Mayonnaise |

| Flavored Mayonnaise |

| Bottles/Jars |

| Squeeze Bottles |

| Pouches/Sachets |

| Tubs/Bulk Packs |

| Others |

| HoReCa/Foodservice | |

| Food Manufacturers/Industrial Users | |

| Household/Retail Consumers | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Product Type | Egg-based Mayonnaise | |

| Eggless/Vegan Mayonnaise | ||

| By Category | Plain Mayonnaise | |

| Flavored Mayonnaise | ||

| By Packaging Type | Bottles/Jars | |

| Squeeze Bottles | ||

| Pouches/Sachets | ||

| Tubs/Bulk Packs | ||

| Others | ||

| By End User | HoReCa/Foodservice | |

| Food Manufacturers/Industrial Users | ||

| Household/Retail Consumers | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the mayonnaise sector by 2031?

It is forecast to reach USD 16.04 billion by 2031 from USD 13.24 billion in 2026, with a CAGR of 3.92%.

Which region leads global demand for mayonnaise?

North America led in 2025 with a 41.72% share, supported by mature retail distribution and dense foodservice demand.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to post the fastest CAGR at 4.59%, helped by QSR expansion, local manufacturing, and broader exposure to Western menu formats.

Which product type still dominates consumer demand?

Egg-based mayonnaise remained the largest product type in 2025 with 58.73% share because traditional taste and established usage still anchor purchases.

Page last updated on: