Egg Free Mayonnaise Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

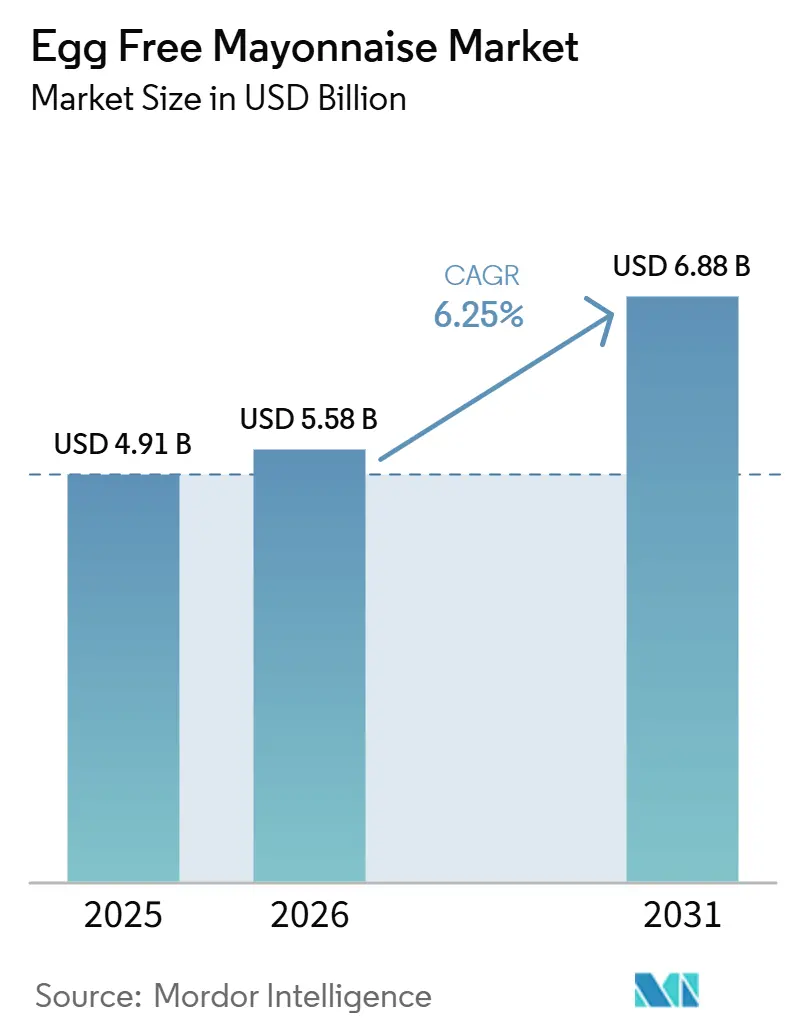

| Market Size (2026) | USD 5.58 Billion |

| Market Size (2031) | USD 6.88 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egg Free Mayonnaise Market Analysis by Mordor Intelligence

The egg-free mayonnaise market size is projected to be USD 4.91 billion in 2025, USD 5.58 billion in 2026, and reach USD 6.88 billion by 2031, growing at a CAGR of 6.25% from 2026 to 2031. Structural momentum comes from allergen-free positioning, rising plant-based diets, and a 2024-2026 collapse in aquafaba and pea-protein costs that finally aligns egg-free formulations with egg-yolk economics at an industrial scale. North America remained the revenue leader in 2025, but Asia-Pacific is the fastest riser, supported by India’s FSSAI vegan-certification regime and flavor localization in Japan and China that maintain emulsion stability while matching regional palates[1]Source: Food Safety and Standards Authority of India, “Vegan Food,” fssai.gov.in. Ingredient trends show soybean oil anchoring 43.85% of value thanks to rock-solid supply chains, whereas avocado-oil variants headline premiumization at an 8.14% growth clip. Flavored SKUs such as chipotle, garlic aioli, and sriracha are eroding taste-parity skepticism, and pouch formats are winning over bottles as Unilever’s edible-coating technology trims residual waste by up to 15 grams per pack. Food manufacturers and QSR chains intensified adoption in gallon formats during 2025 avian-flu disruptions, underscoring the category’s hedge value against volatile egg supply.

Key Report Takeaways

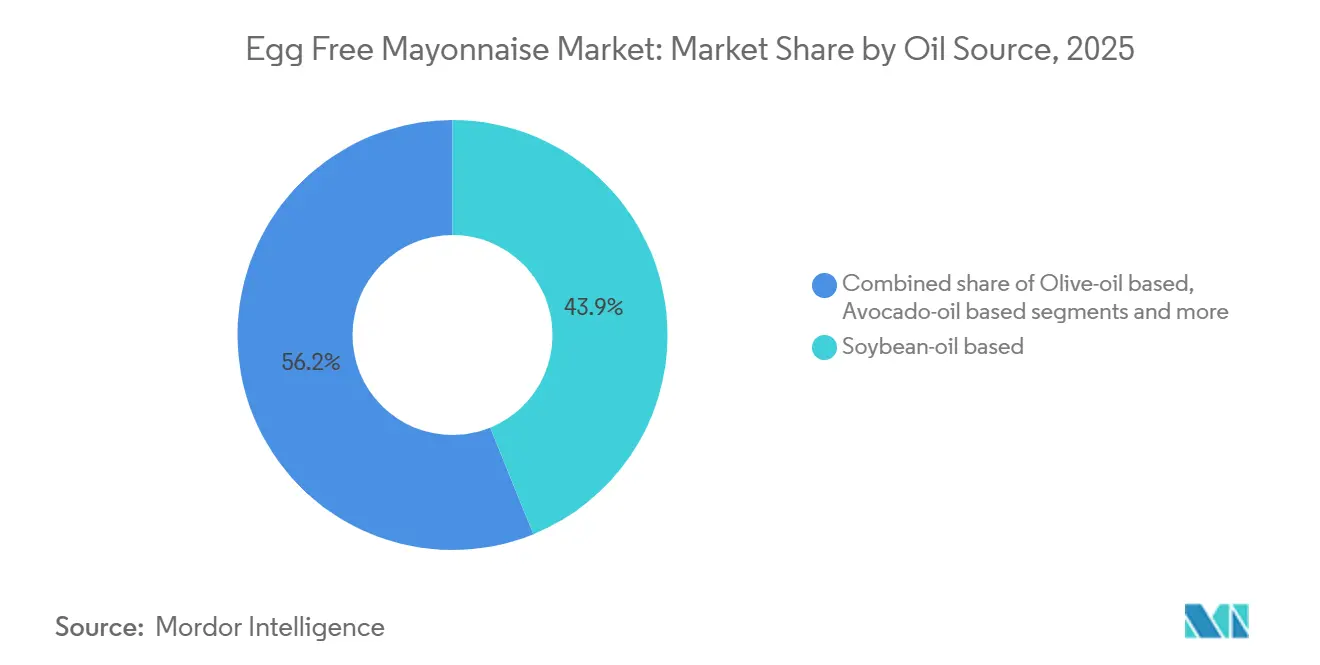

- By oil source, soybean formulations held 43.85% of the egg-free mayonnaise market share in 2025, while avocado-oil variants are forecast to expand at an 8.14% CAGR through 2031.

- By product type, plain offerings captured 67.62% of 2025 volume; flavored SKUs are advancing at an 8.02% CAGR to 2031.

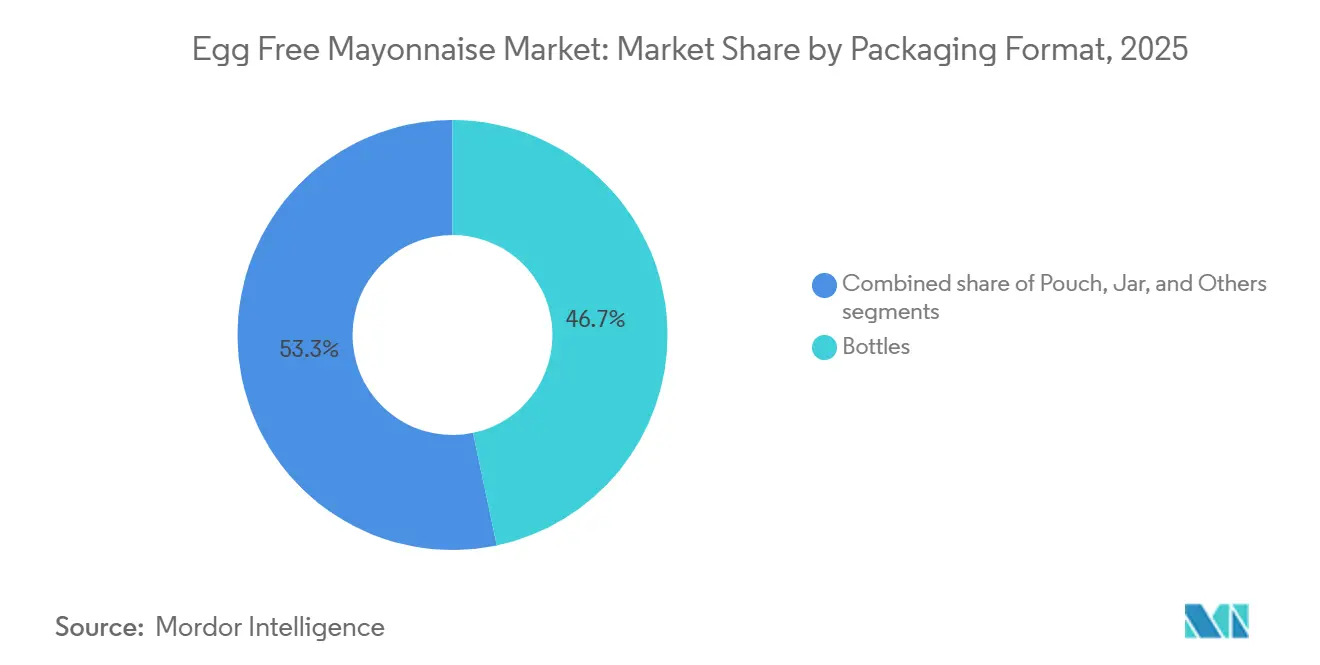

- By packaging, bottles delivered 46.24% of 2025 sales, whereas pouches are on track for 7.72% CAGR growth.

- By end user, household and retail channels represented 63.28% of 2025 demand, yet industrial food manufacturers are accelerating at a 7.56% CAGR through 2031.

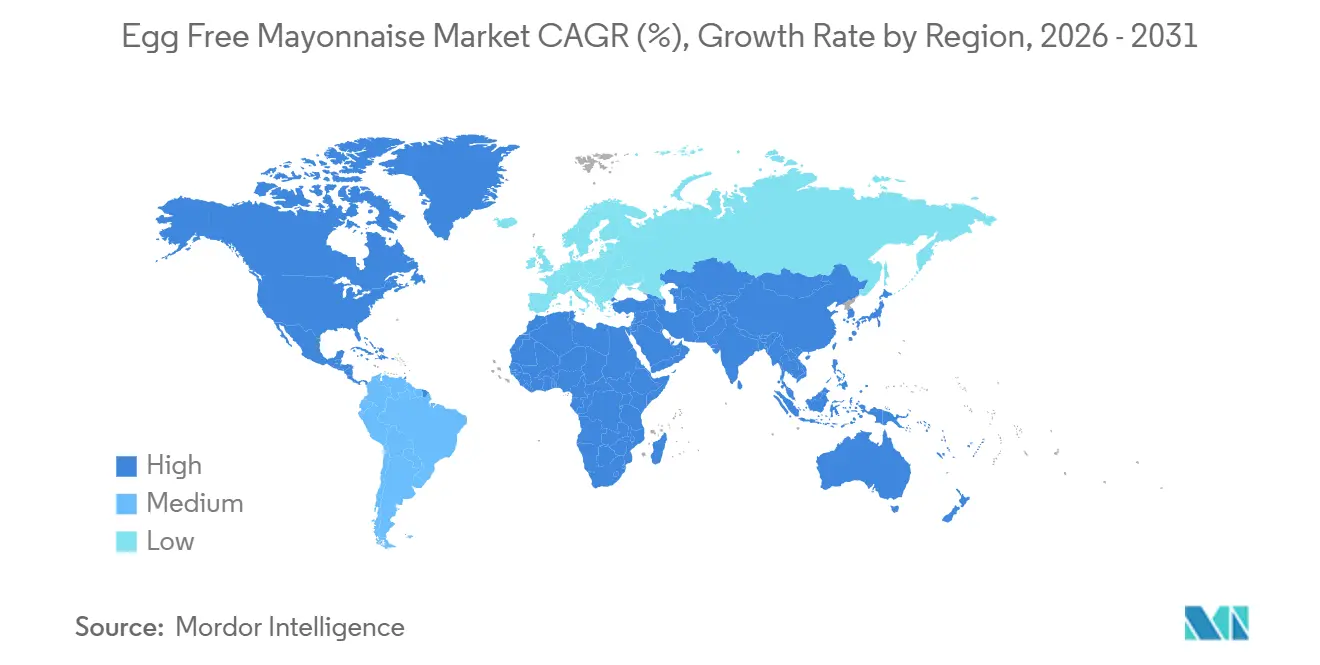

- By geography, North America commanded 38.92% revenue in 2025; Asia-Pacific is projected to record the fastest 7.25% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Egg Free Mayonnaise Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Vegan And Plant-Based Dietary Trends | +1.2% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising Awareness And Prevalence Of Allergies | +0.9% | Global, particularly North America and Europe with established allergen-labeling regimes | Long term (≥ 4 years) |

| Increased Ethical And Animal Welfare Considerations | +0.7% | North America, Western Europe, Australia; emerging in urban India and Southeast Asia | Long term (≥ 4 years) |

| Preference For Lower-Fat, Cholesterol-Free Mayonnaise Alternatives | +1.0% | Global, with early adoption in North America and Northern Europe | Medium term (2-4 years) |

| Expansion Of Vegan Vegetarian Product Lines By Major Brands | +1.3% | Global, led by North America and Europe; accelerating in Asia-Pacific | Short term (≤ 2 years) |

| Rapid Cost Declines Via Aquafaba And Novel Plant Proteins | +1.1% | Global, with manufacturing hubs in North America, Europe, and emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Vegan and Plant-Based Dietary Trends

Flexitarians, who occasionally replace animal products, now represent the largest audience for egg-free mayonnaise, driving growth in the plant-based food category. In June 2024, Unilever renamed its "Vegan Mayo" to "Plant-Based Mayo" after research showed that "vegan" could discourage flexitarians, whereas "plant-based" is seen as more inclusive and health-oriented. A 2023 University of Southern California study found that 27% of participants preferred "plant-based" labels compared to 20% for "vegan." This preference gap was even wider among red-meat consumers, a critical demographic for egg-free mayo brands seeking mass-market appeal. This labeling change is more than a superficial adjustment; it reflects a deliberate strategy to shift from niche to mainstream positioning. Hellmann's has achieved four consecutive years of growth in its plant-based product line and expects the category to double by 2030. This growth is driven by consumers who initially tried the products for health or environmental reasons but now favor them for their taste and convenience. The message for competitors is clear: brands that stick with "vegan" labels risk losing market share to those adopting broader plant-based messaging.

Rising Awareness and Prevalence of Allergies

In the U.S., approximately 0.9% of children and 0.8% of adults have egg allergies, making it one of the most common food allergens. The FDA's allergen-labeling guidance (Edition 5), effective January 2025, has increased the emphasis on cross-contact controls and ingredient transparency. Manufacturers labeling products as "egg-free" must now validate their sanitation protocols and ensure supply-chain traceability to confirm the absence of egg protein, including from incidental additives or processing aids[2]Source: U.S. Food and Drug Administration, “FDA Releases Allergen, Food Safety, and Plant-Based Alternative Labeling Guidances,” fda.gov. While these stricter regulations pose challenges for conventional mayonnaise producers, they provide a competitive edge to egg-free mayo manufacturers. The higher compliance requirements create obstacles for traditional producers attempting to co-pack or share production lines with egg-free alternatives, discouraging low-cost private-label competitors. Furthermore, the FDA's draft guidance on low-moisture ready-to-eat foods, also effective January 2025, highlights the need for hazard analysis and corrective actions to address allergen contamination. This reinforces the necessity for dedicated production lines or rigorously validated cleaning procedures. For egg-free brands, this regulatory environment creates a significant advantage: once they invest in allergen-free infrastructure, the costs for conventional players to adapt become prohibitive.

Increased Ethical and Animal Welfare Considerations

Concerns about industrial egg production methods, such as battery-cage systems and male chick culling, are prompting some consumers to choose egg-free alternatives, even if they do not identify as vegan. Eat Just emphasizes that its plant-based mayo uses 98% less water, produces 93% fewer carbon emissions, and requires 83% less land compared to traditional egg production. These claims strongly appeal to environmentally conscious millennials and Gen Z. Ethical considerations extend beyond animal welfare to labor practices. NIÚKE Foods, an Argentina-based company, markets its chickpea-based vegan mayo as handcrafted by an all-female workforce in Mendoza, presenting the product as both eco-friendly and socially impactful. This blend of ethical sourcing and functional equivalence is gaining traction in premium markets, where consumers are willing to pay 15-20% more than for conventional mayo. However, the scalability of this strategy remains uncertain. As production volumes increase, the feasibility of artisanal claims may diminish, requiring brands to shift their focus to industrial-scale benefits like reduced carbon footprints and water efficiency.

Preference for Lower-Fat, Cholesterol-Free Mayonnaise Alternatives

Consumers focused on health and those managing cardiovascular risks are increasingly choosing egg-free mayonnaise formulations, which offer zero cholesterol, a benefit that traditional egg-based products cannot provide. In 2025, Best Foods reformulated its plant-based mayo by substituting sunflower oil with canola oil due to global sunflower shortages. This adjustment not only earned the American Heart Association's Heart-Check certification, indicating compliance with FDA and USDA standards for coronary heart disease claims, but also strategically positioned the brand in the expanding "better-for-you" condiment market. As consumers become more attentive to ingredient labels and prioritize products that meet dietary guidelines, this shift reflects a strategic market approach. Moreover, a 2026 peer-reviewed study demonstrated that aquafaba-based mayonnaise possesses rheological properties similar to egg-based versions, including comparable viscoelastic behavior and oxidative stability. This development effectively addresses prior concerns about texture and shelf-life in egg-free products. Such technical validation allows brands to position egg-free mayo as not just an alternative but a functionally equivalent and nutritionally superior choice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flavor And Texture Skepticism Among Mainstream Consumers | -0.8% | Global, particularly in regions with strong culinary traditions favoring egg-based mayo (Southern Europe, parts of Asia) | Medium term (2-4 years) |

| Price Premium Compared To Conventional Mayonnaise | -0.6% | Emerging markets and price-sensitive segments in developed markets | Short term (≤ 2 years) |

| Ingredient Sourcing And Supply Chain Volatility | -0.5% | Global, with acute impact in regions dependent on imported specialty oils (Middle East, parts of Africa) | Short term (≤ 2 years) |

| Limited Product Variety In Certain Regions | -0.4% | South America, Middle East, Africa, and rural areas in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flavor and Texture Skepticism Among Mainstream Consumers

Despite technical advances in emulsion science, a segment of consumers remains unconvinced that egg-free mayonnaise can replicate the mouthfeel and flavor complexity of traditional formulations. This skepticism is most pronounced in markets with deep culinary traditions around egg-based condiments, such as France and Japan, where mayonnaise is a foundational ingredient in classic dishes. Unilever's 2024 reformulation of Hellmann's plant-based mayo, reducing rapeseed oil and adding sunflower oil and xanthan gum, was explicitly designed to address texture complaints and improve the "squeeze" experience, yet the need for iterative reformulation underscores that taste parity remains a work in progress. The 56% repeat-purchase rate reported by Eat Just in foodservice channels suggests that once consumers trial the product in a controlled setting (e.g., a restaurant sandwich), they are more likely to accept it, but converting first-time retail buyers who compare egg-free and conventional mayo side-by-side remains challenging. Brands are responding with blind taste tests and in-store sampling, but these tactics require sustained marketing investment and may not scale efficiently in price-sensitive markets.

Price Premium Compared to Conventional Mayonnaise

Egg-free mayonnaise typically commands a 15-25% price premium over conventional mayo, a gap that narrows during egg-price spikes but widens when egg supply normalizes. This premium reflects higher costs for specialty oils (avocado, olive), plant-protein isolates, and the smaller production runs that characterize a still-maturing category. In India, Veeba's eggless mayo retails at approximately INR 42 (USD 0.50) for a 100-gram pack, positioning it as a mid-tier product accessible to urban middle-class consumers but out of reach for rural households. The price gap is narrowing as aquafaba and pea-protein costs decline, yet it remains a barrier in emerging markets where conventional mayo is already a discretionary purchase. Brands that achieve cost parity, either through scale economies or by reformulating around lower-cost oils, will unlock mass-market penetration, but this transition may take 2-3 years as production volumes ramp and supply chains mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Oil Source: Avocado Oil Premiumization Outpaces Commodity Bases

In 2025, soybean oil-based egg-free mayonnaise accounted for 43.85% of the market revenue, supported by well-established supply chains, affordable per-unit costs (USD 0.46-0.53 per pound in mid-2025), and a neutral flavor profile that appeals to cost-sensitive manufacturers and private-label brands. Canola oil formulations, the second-largest segment, benefit from the American Heart Association's Heart-Check certification and a favorable omega-3 profile. This positions them as a "better-for-you" option, bridging the gap between commodity soybean and premium avocado variants. Avocado oil-based mayo, despite its higher price, is projected to grow at an 8.14% CAGR through 2031. This growth is driven by Chosen Foods' 44% increase in condiment sales and a strong 70% retail penetration across more than 22,500 U.S. stores. Additionally, consumers perceive avocado oil as both heart-healthy and a symbol of culinary sophistication.

Olive oil variants cater to a niche market, attracting Mediterranean-diet followers and gourmet consumers, but their strong flavor profile limits their versatility in applications like sandwiches and salads. The "Other Oils" category, which includes sunflower, coconut, and proprietary blends, is experiencing formulation innovation as brands mitigate risks associated with single-commodity dependence. Best Foods' 2025 shift from sunflower to canola oil exemplifies this risk-management approach. The move toward premium oils highlights a broader consumer willingness to pay for perceived health benefits, but it also increases supply-chain risks. Avocado oil sourcing is concentrated in Mexico, Peru, and Chile, regions facing water scarcity and cartel-related logistical challenges that can disrupt supply and drive up costs. To address these issues, manufacturers are blending avocado oil with canola or sunflower oil. This approach helps maintain a premium market position while mitigating price volatility. However, blending complicates labeling and may weaken the "pure avocado oil" claim that supports premium pricing, forcing brands to balance cost management with marketing authenticity.

By Product Type: Flavored Variants Drive Culinary Differentiation

Plain egg-free mayonnaise held 67.62% of 2025 volume, reflecting its role as a versatile base for sandwiches, salads, and foodservice applications where neutral flavor is paramount. Yet flavored SKUs, chipotle, garlic aioli, sriracha, basil, chili lime- are surging at 8.02% CAGR, signaling that taste parity breakthroughs and culinary experimentation are eroding the perception gap between egg-free and conventional products. Hellmann's introduced Italian Herb & Garlic and Chili Lime variants in 2024-2025, targeting consumers who view condiments as flavor enhancers rather than mere binders, and these innovations are driving repeat purchases among flexitarians who initially tried plain formulations for health reasons but now prefer the taste complexity of flavored options.

NIÚKE Foods' Argentina-based chickpea mayo is offered in Vegan Basil, Sriracha, and Garlic variants, demonstrating that even smaller regional players recognize flavored SKUs as a differentiation lever in a crowded market. The strategic implication is that flavored egg-free mayo is becoming a platform for culinary innovation, with brands testing bold profiles that conventional mayo producers may be reluctant to launch due to the conservative tastes of their core customer base. This creates a first-mover advantage for egg-free brands: by establishing ownership of niche flavors (e.g., truffle, harissa, miso), they can build loyal micro-segments that are insulated from price competition with plain formulations. However, flavor proliferation also fragments shelf space and complicates inventory management for retailers, potentially limiting distribution for smaller brands that lack the scale to support multiple SKUs.

By Packaging Type: Pouches Gain Share Through Sustainability and Convenience

Bottles accounted for 46.24% of the 2025 packaging share, favored for their resealability, shelf presence, and compatibility with existing retail fixtures. Jars, the traditional format for premium mayonnaise, remain relevant in gourmet and specialty channels but are losing ground to squeeze bottles and pouches that offer superior convenience and portion control. Pouches are expanding at 7.72% CAGR, driven by sustainability narratives (lighter weight, lower carbon footprint) and functional benefits such as easier dispensing and reduced product waste. Unilever's May 2024 launch of Hellmann's plant-based mayo in squeeze bottles with an edible vegan coating represents a breakthrough in packaging technology: the coating reduces internal product retention by up to 15 grams per bottle, improving consumer satisfaction and ensuring that bottles meet recycling weight thresholds. This innovation addresses a pain point specific to plant-based formulations, which tend to be more viscous and prone to sticking than egg-based mayo.

The "Other" packaging category, which includes single-serve sachets and bulk foodservice containers, is growing in institutional channels where portion control and hygiene are priorities. Eat Just's 1-gallon format, priced at USD 0.24-0.28 per ounce for foodservice operators, exemplifies the shift toward bulk packaging in QSR and catering applications. Kewpie's 64-ounce foodservice vegan mayo launch in 2025 similarly targets institutional buyers who prioritize consistency and cost-per-serving over retail branding. The packaging landscape is thus bifurcating: retail channels are moving toward convenience-oriented formats (pouches, squeeze bottles), while foodservice is consolidating around bulk containers that minimize per-unit costs and reduce packaging waste.

By End User: Industrial Food Manufacturers Hedge Against Avian Flu

Household and retail channels represented 63.28% of 2025 demand, driven by direct-to-consumer sales through supermarkets, hypermarkets, and online platforms. Yet industrial food manufacturers are the fastest-growing end-user segment at 7.56% CAGR, as QSR chains, prepared-food producers, and bakeries adopt egg-free mayo to hedge against avian-flu supply shocks and meet corporate sustainability commitments. Eat Just reported 5-times month-over-month demand growth during 2025 avian-flu outbreaks, with a 56% repeat-purchase rate among foodservice operators, underscoring the strategic value of dual-sourcing egg and egg-free emulsions. This B2B adoption is not merely a short-term response to supply disruptions; it reflects a structural shift as food manufacturers recognize that egg-free formulations offer price stability, allergen-free claims, and alignment with ESG targets.

The foodservice and HoReCa (hotel, restaurant, catering) segment is benefiting from the same dynamics, with QSR chains testing egg-free mayo in limited-time offers and permanent menu items to appeal to vegan and flexitarian diners. Kewpie's 64-ounce foodservice format and Eat Just's gallon containers are designed to meet the operational requirements of high-volume kitchens, where consistency, shelf-life, and cost-per-serving are paramount. Within household and retail, supermarkets and hypermarkets remain the dominant channel, but online retail is growing rapidly as direct-to-consumer brands like Chosen Foods and NIÚKE Foods leverage e-commerce to bypass traditional retail gatekeepers and capture data on consumer preferences. Convenience stores and "Other Distribution Channels" (specialty stores, health-food shops) serve niche segments but lack the scale to drive category growth.

Geography Analysis

North America held 38.92% of 2025 revenue, reflecting early adoption of plant-based diets, robust retail distribution, and the presence of major brands like Hellmann's, Best Foods, and Eat Just. The region benefits from established allergen-labeling regimes (FDA) and consumer familiarity with vegan products, yet growth is moderating as the category matures and penetration rates plateau in urban markets. Europe, the second-largest region, is characterized by strong regulatory frameworks (EFSA vegan certification, EU allergen rules) and high consumer awareness of animal welfare and sustainability issues, driving steady demand for egg-free mayo in Germany, the UK, France, and the Netherlands. Eat Just's £11.25 million (USD 14.3 million) partnership with Vegan Food Group to launch European production in Lüneburg, Germany in H2 2025 signals confidence in the region's growth trajectory and the strategic importance of local manufacturing to reduce logistics costs and tariff exposure.

Asia-Pacific is expanding at 7.25% CAGR through 2031, propelled by FSSAI vegan-certification rollouts in India, localized flavor adaptations in Japan and China, and rising disposable incomes in urban centers. India's FSSAI Vegan Foods Regulations (2022) and the 2025 amendment requiring Form I certificates for imports create a compliance framework that favors established players with validated cross-contamination controls and traceability systems[3]Source: TaxGuru, “Draft Regulations for Vegan Foods Amendment, 2025,” taxguru.in. Veeba, a leading Indian brand, has secured FSSAI license 10013013000578 and offers eggless mayo at INR 42 (USD 0.50) for 100 grams, positioning it as accessible to the urban middle class. Japan's Kewpie launched a 64-ounce foodservice vegan mayo in 2025, targeting institutional buyers and QSR chains, while China's market remains nascent but is expected to accelerate as plant-based diets gain traction among health-conscious millennials.

South America, the Middle East, and Africa remain smaller markets but are seeing early-stage growth driven by local entrepreneurs and niche brands. NIÚKE Foods' chickpea-based vegan mayo, handcrafted by an all-female workforce in Mendoza, Argentina, exemplifies the region's potential for artisanal, mission-driven brands that combine plant-based positioning with social impact narratives. However, distribution remains fragmented, with most sales occurring through direct-to-consumer channels and planned e-commerce platforms rather than broad retail placement. The Middle East and Africa face similar challenges, with limited product variety and high import costs constraining adoption, yet these regions represent long-term opportunities as urbanization and disposable incomes rise.

Competitive Landscape

Egg-free mayonnaise market leaders, primarily multinational corporations with extensive distribution networks, maintain dominance in a moderately consolidated market. These companies utilize their manufacturing, marketing, and distribution scale to create significant entry barriers for smaller or newer competitors. Simultaneously, innovative startups are transforming the traditional mayonnaise segment by introducing unique formulations and strategic positioning to meet changing consumer preferences. The market frequently experiences consolidation activities, such as acquisitions, enabling larger players to expand their product offerings and improve manufacturing capabilities.

Technology adoption has emerged as a key competitive differentiator. Companies are innovating with ingredients, exploring alternative plant-based sources and emulsifiers to replicate the taste and texture of traditional mayonnaise. Optimized manufacturing processes are enhancing yield, consistency, and sustainability, delivering cost efficiencies and environmental benefits. Additionally, advancements in packaging are improving convenience and shelf life, attributes increasingly valued by consumers and retail partners. These technological advancements not only strengthen brand loyalty but also help companies stay competitive as consumer expectations for quality and transparency continue to rise.

Leading companies, such as Kraft Heinz with its NotMayo product, are incorporating advanced artificial intelligence (AI) technologies into formulation development. This integration accelerates product innovation cycles and refines sensory characteristics to align with consumer preferences. Beyond the consumer market, significant opportunities exist in specialized sectors like industrial food manufacturing. In these sectors, egg-free mayonnaise offers unique value propositions, such as allergen-free profiles and improved operational efficiency. By leveraging these opportunities, companies can diversify applications beyond retail, positioning themselves for sustainable growth in a competitive market that rewards both innovation and scale.

Egg Free Mayonnaise Industry Leaders

Unilever plc

Kraft Heinz Company

Eat Just Inc.

Dr. Oetker KG

Danone SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Masaka Farms launched an eggless mayonnaise with a lemon‑cocktail flavor in Rwanda, positioning itself as one of the first local producers of a plant‑based, egg‑free mayonnaise aimed at expanding options for consumers seeking allergen‑friendly and vegetarian condiments.

- June 2024: Hellmann's renamed its vegan mayonnaise to plant-based mayo to increase market reach. The company introduced this animal-free version of its mayonnaise in 2018 to address the expanding vegan market segment. The reformulated product maintained vegan compliance, incorporating sunflower oil and xanthan gum while reducing rapeseed oil content.

- May 2024: Duke's, established in 1917 and known for its premium southern mayonnaise, introduced Plant-Based Mayo. This new product met the increasing market demand for plant-based alternatives and served both foodservice establishments and online consumers. The Plant-Based Mayo maintained Duke's quality standards with no artificial flavors, colors, or high fructose corn syrup, while being kosher and gluten-free. The product was available in 4/1 gallon containers through foodservice distributors, and consumers could purchase 16-oz jars through Duke's online store.

Global Egg Free Mayonnaise Market Report Scope

| Soybean Oil Based |

| Canola Oil Based |

| Avocado Oil Based |

| Olive Oil Based |

| Other Oils (Sunflower, Coconut, Blends) |

| Plain |

| Flavored |

| Jars |

| Pouches |

| Bottles |

| Others |

| Foodservice HoReCa | |

| Industrial Food Manufacturer | |

| Households Retail | Supermarkets Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Oil Source | Soybean Oil Based | |

| Canola Oil Based | ||

| Avocado Oil Based | ||

| Olive Oil Based | ||

| Other Oils (Sunflower, Coconut, Blends) | ||

| By Product Type | Plain | |

| Flavored | ||

| By Packaging Type | Jars | |

| Pouches | ||

| Bottles | ||

| Others | ||

| By End User | Foodservice HoReCa | |

| Industrial Food Manufacturer | ||

| Households Retail | Supermarkets Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the egg-free mayonnaise market be by 2031?

It is projected to reach USD 6.88 billion by 2031, expanding at a 6.25% CAGR between 2026 and 2031.

Which oil base is growing fastest in egg-free spreads?

Avocado-oil formulations are leading with an 8.14% CAGR through 2031 thanks to heart-health positioning and premium flavor perception.

Why is Asia-Pacific the fastest-growing region?

FSSAI vegan certification in India, localized Japanese and Chinese flavors, and rising urban incomes are driving a 7.25% regional CAGR.

What packaging formats are trending?

Lightweight pouches are gaining share at 7.72% CAGR due to lower carbon footprint and reduced product waste.

Page last updated on: