Market Overview

| Study Period | 2021 - 2031 |

|---|---|

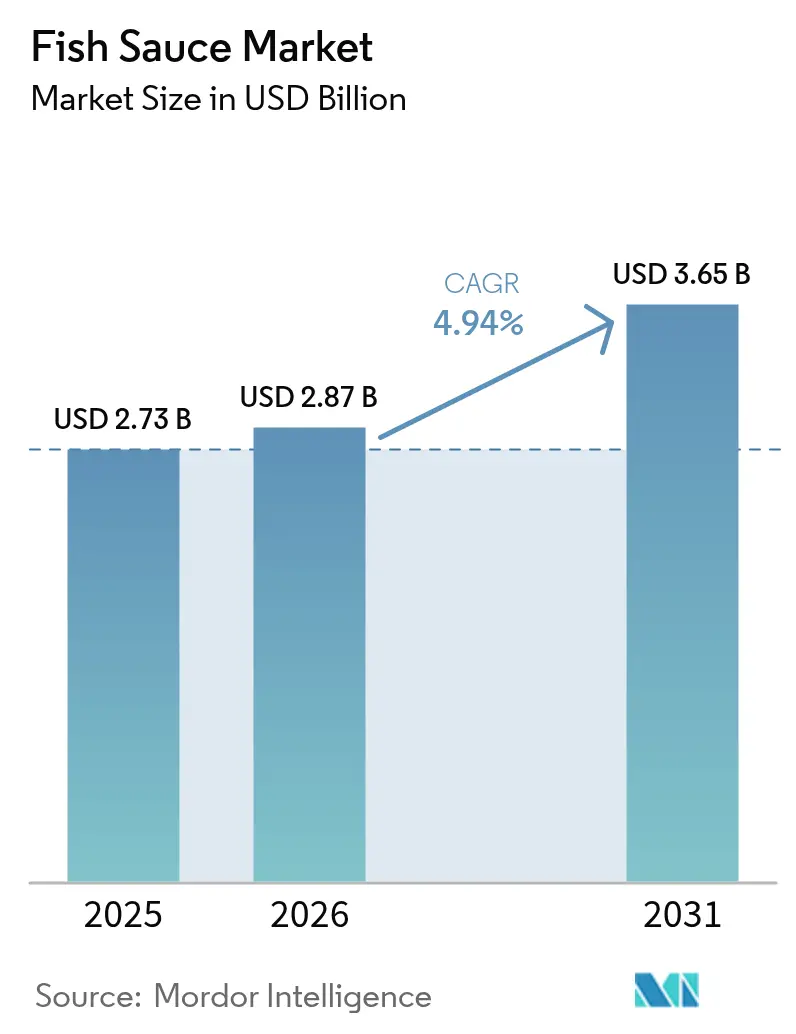

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fish Sauce Market Analysis by Mordor Intelligence

The fish sauce market size in 2026 is estimated at USD 2.87 billion, growing from 2025 value of USD 2.73 billion with 2031 projections showing USD 3.65 billion, growing at 4.94% CAGR over 2026-2031. This growth is driven by a global embrace of Asian flavors, heightened spending on halal foods, and a shift towards clean-label condiments. Yet, climate pressures on anchovy stocks create a pronounced supply-demand tension, jeopardizing long-term price stability. In response, larger producers are turning to vertical integration, blockchain traceability, and expanding capacities to ensure a steady flow of raw materials. These strategies align with rising demand from quick-service restaurants and ready-meal manufacturers, who value the sauce's umami intensity, shelf stability, and versatility across cuisines. At the same time, regulators in affluent nations are tightening sodium-reduction targets, pushing producers to navigate the delicate balance between taste authenticity and reformulation, all while considering portion-controlled packaging.

Key Report Takeaways

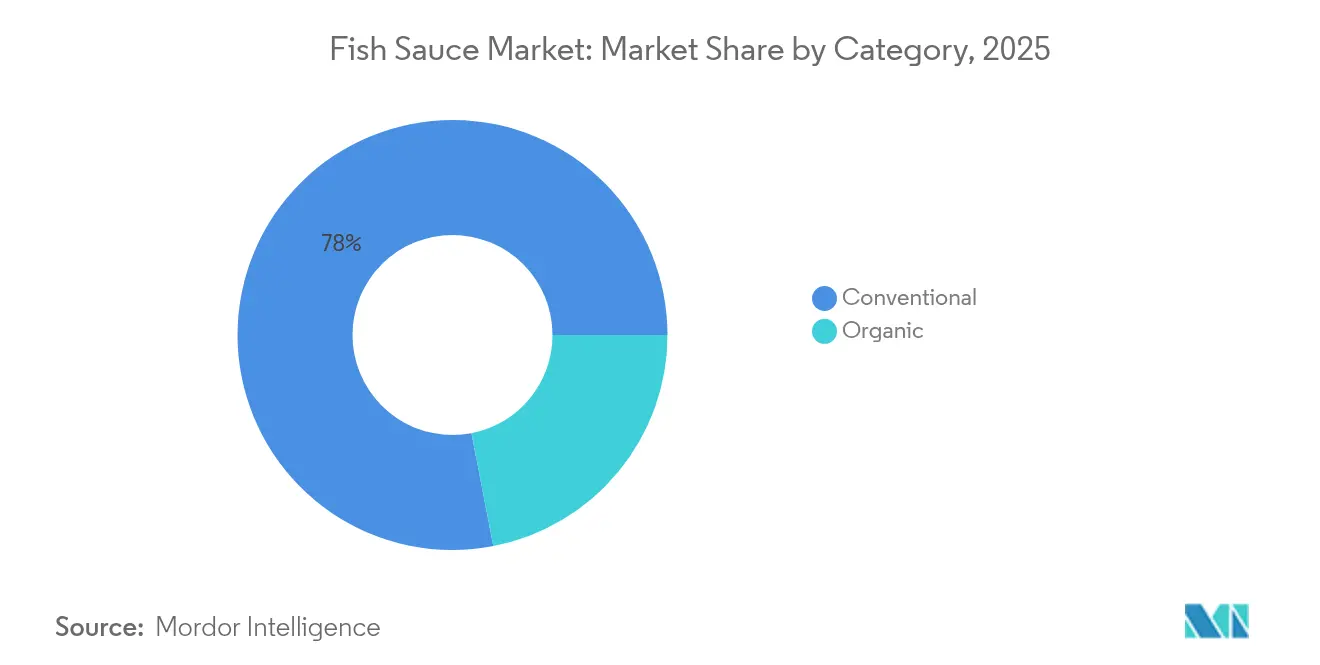

- By category, conventional products commanded 78.04% of the fish sauce market share in 2025, while organic variants are expanding at a 6.43% CAGR through 2031.

- By flavor, plain varieties captured 81.71% revenue share in 2025; flavored options are forecast to advance at a 6.33% CAGR to 2031.

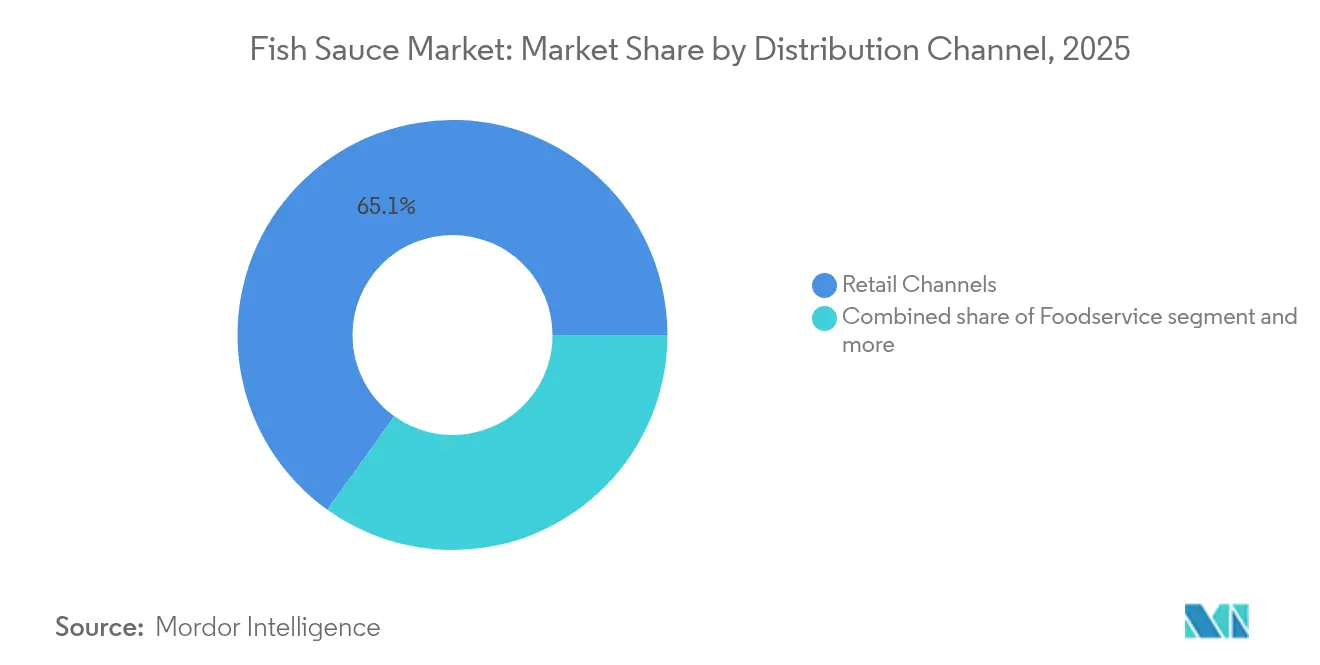

- By distribution channel, retail formats accounted for 65.11% of the fish sauce market size in 2025; foodservice channels are pacing ahead at a 5.48% CAGR over 2026-2031.

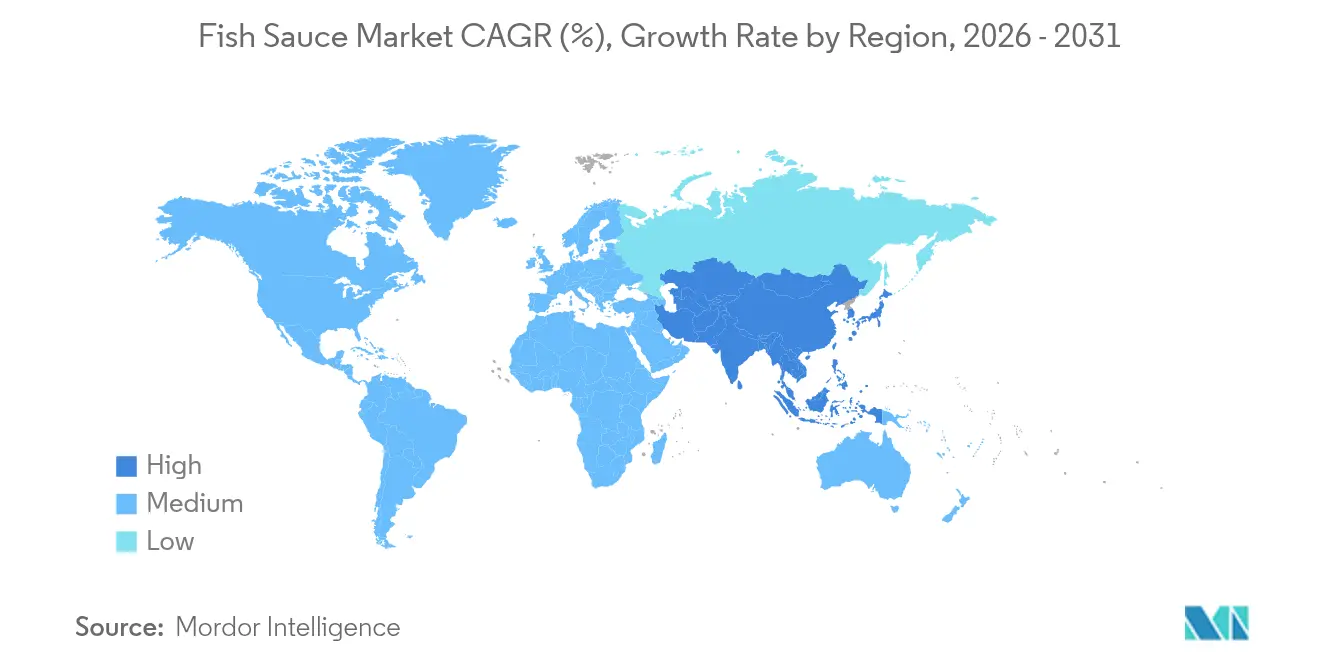

- By geography, Asia-Pacific led with a 74.92% share of the fish sauce market in 2025, whereas the Middle East and Africa are set to grow fastest at 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fish Sauce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asian cuisine globalisation | +1.2% | Global, with strongest penetration in North America and Europe | Medium term (2-4 years) |

| Clean-label demand for natural umami | +0.8% | North America, Europe, and urban APAC markets | Long term (≥ 4 years) |

| Expansion of Asian food-service chains | +0.9% | Global, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Ready-to-eat and processed food growth | +0.7% | Global, with emphasis on convenience-oriented markets | Medium term (2-4 years) |

| Culinary tourism and influencer culture | +0.5% | Global, social media-driven adoption patterns | Short term (≤ 2 years) |

| Blockchain traceability adoption | +0.3% | Export-oriented regions, premium market segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Asian Cuisine Globalisation

Asian flavors are increasingly becoming a staple in global foodservice, spurred by demographic changes and cultural blending. An analysis by Unilever Food Solutions, sifting through 237,000 keywords from 312 million searches across 21 countries, highlights that Chinese and Japanese cuisines have secured spots among the top 5 global favorites[1]Source: Unilever Food Solutions, “Future Menus 2025,” unileverfoodsolutions.com . Meanwhile, Korean and Filipino flavors are witnessing a rapid rise in popularity. This trend isn't confined to ethnic eateries; mainstream restaurants are also adopting a "borderless cuisine" approach, seamlessly blending Eastern umami into Western dishes through thoughtful ingredient swaps. Migration and travel play pivotal roles in this culinary shift, with 76% of travelers expressing a desire for authentic local food experiences. This, in turn, fuels a demand for these familiar flavors back home. Generation Z stands out in this culinary landscape, relishing experimentation and valuing quality at reasonable prices, all while favoring experiential dining over conventional meals. As globalization continues to weave its tapestry, ingredients like fish sauce are evolving from niche ethnic components to essential culinary enhancers, finding their way into a myriad of menu categories.

Clean-Label Demand for Natural Umami

As consumers increasingly scrutinize ingredient lists, the clean-label movement gains momentum, pushing the condiment industry to reformulate. This shift positions traditional fish sauce, made solely from fish and salt through natural fermentation, as a prime umami source. While consumers seek recognizable components and shun synthetic additives, fish sauce's authentic umami complexity stands unmatched[2]Source: Sabert, “Trends 2025,” sabert.com. This authenticity becomes crucial as food manufacturers face pressure to ditch artificial flavor enhancers and preservatives. Moreover, as sustainability takes center stage, consumers prioritize traceability and environmental responsibility in their choices. Producers showcasing traditional methods, sustainable sourcing, and transparent supply chains bolstered by certifications and blockchain traceability find themselves with premium positioning opportunities.

Ready-to-Eat and Processed Food Growth

As the convenience food sector expands, manufacturers are turning to fish sauce to infuse authentic flavor profiles, setting their products apart in competitive markets. This trend is evident in Thailand's ready-to-eat food industry, spurred by urbanization and smaller household sizes. Innovations in single-serve packaging and portion-controlled formats cater to evolving consumer lifestyles, seamlessly integrating fish sauce into convenient meal solutions. Demographic shifts, such as an aging population and urban dwellers pressed for time, further amplify this trend, as these consumers seek convenience without compromising on flavor authenticity. Recognizing fish sauce's potential to elevate umami profiles in soups, marinades, and ready meals, manufacturers are seizing cross-category adoption opportunities. Yet, with rising pressures to reduce sodium, there's a delicate balancing act: maintaining authentic taste profiles while aligning with health-conscious trends.

Culinary Tourism and Influencer Culture

Food influencers and travel content are exposing global audiences to authentic Asian flavors and cooking techniques, amplifying demand through social media-driven food culture and culinary tourism. This phenomenon isn't limited to traditional media; platforms like TikTok and Instagram rapidly spread viral recipe content, showcasing fish sauce in both traditional and fusion dishes. Beyond just travel, culinary tourism drives consumers to recreate authentic flavors at home, boosting retail demand for specialty ingredients that were once only found in ethnic markets. By emphasizing authentic ingredients and traditional techniques, food influencers are solidifying fish sauce's role as a vital umami component, especially when showcasing its versatility across various cuisines. Brands see this trend as a chance to engage consumers through recipe content, cooking demos, and cultural storytelling, fostering brand loyalty and broadening usage occasions. This influence is especially strong among younger demographics, who value authenticity and cultural exploration in their culinary choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sodium | -1.1% | Global, with strongest regulatory pressure in developed markets | Medium term (2-4 years) |

| Raw material price fluctuations | -0.9% | APAC production regions, global supply chain impact | Short term (≤ 2 years) |

| Authenticity import checks tightening | -0.4% | Export-dependent regions, premium market segments | Long term (≥ 4 years) |

| Limited consumer awareness outside Asia | -0.6% | North America, Europe, emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over High Sodium

Public health initiatives aimed at reducing sodium intake are putting significant pressure on traditional fish sauce producers to reformulate their products. This comes in light of the World Health Organization (WHO) singling out fish sauce as a high-sodium condiment in need of intervention. WHO recommends a daily sodium intake of less than 2,000 mg. However, the global average stands at a concerning 4,310 mg, with fish sauce and other processed foods playing a notable role in this excess. The FDA has set voluntary sodium reduction targets across 155 food categories, signaling a regulatory trend that might soon extend to imported condiments. This is further underscored by microsimulation analyses, which hint at considerable healthcare savings from widespread industry reformulation. Yet, traditional fish sauce fermentation poses a challenge: it relies on high salt concentrations for both preservation and flavor, complicating efforts to reformulate without losing product integrity. Educating consumers is paramount, especially since fish sauce's potency means that even small servings can provide intense flavor with relatively lower sodium levels than many processed foods. To successfully adapt, producers might explore innovations like low-sodium alternatives, potassium chloride substitutions, or concentrated formulations that maintain flavor intensity while cutting down on sodium content per serving.

Authenticity Import Checks Tightening

As import regulations tighten and authenticity verification becomes paramount, traditional producers find themselves at a disadvantage. In contrast, larger manufacturers, equipped with advanced compliance capabilities, stand to benefit. The EU's Common Organization of Markets Regulation and Fisheries Control Regulation set forth stringent traceability mandates. These are particularly challenging for smaller producers, especially when it comes to catch documentation and supply chain verification[3]Source: Southeast Asian Fisheries Development Center, “Traceability Needs,” seafdec.org. In the U.S., the FDA's PREDICT system and foreign facility inspections heighten compliance challenges for exporters eyeing the American market. Insufficient documentation can lead to detention without physical examination. Vietnam's 2017 standard for traditional fish sauce, while safeguarding authentic production, complicates international trade. Importers now face the added task of ensuring adherence to specific fermentation durations and ingredient limitations. This evolving regulatory landscape seems to favor those with the means to adopt robust quality management systems, secure third-party certifications, and leverage blockchain for traceability. As a result, there's a risk of market share consolidation among these larger entities. Meanwhile, smaller artisanal producers grapple with the dilemma of either bolstering their compliance infrastructure or aligning with larger distributors adept at navigating these intricate regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Dominance Faces Organic Disruption

In 2025, conventional fish sauce held a dominant 78.04% market share. However, organic variants are on a rapid ascent, boasting a 6.43% CAGR projected through 2031. This shift underscores a growing consumer preference for clean-label alternatives. The stronghold of the conventional segment can be attributed to its well-established production infrastructure, cost benefits, and broad distribution, especially in traditional Asian markets where price sensitivity is a key factor. On the other hand, organic certifications resonate with consumers' increasing demand for transparency and sustainable practices. This alignment not only creates premium market opportunities but also enables higher profit margins, even with reduced volumes. The organic segment's appeal is further enhanced by its stringent raw material sourcing, which emphasizes certified sustainable fisheries and organic salt. This resonates with eco-conscious consumers who are ready to pay a premium for genuine sustainability.

Regulatory bodies are leaning towards organic methods, with USDA organic standards and their international counterparts offering a leg up in developed markets. The organic segment's growth mirrors a broader clean-label movement, where consumers are gravitating towards minimally processed products with familiar ingredients. This trend naturally aligns traditional fermentation methods with organic values. Facing this shift, conventional producers are under pressure to embrace sustainable practices. If they falter, they risk losing ground to organic alternatives, especially in premium retail spaces where organic products not only enjoy prime shelf placement but also a stronger consumer preference.

By Flavor: Plain Varieties Lead While Spiced Innovations Accelerate

In 2025, plain fish sauce held an 81.71% market share, solidifying its role as the cornerstone of genuine Asian cuisine. Meanwhile, flavored variants are experiencing rapid growth, with a 6.33% CAGR projected through 2031. The plain segment's stronghold is attributed to its adaptability, serving as a primary ingredient in both home kitchens and professional food services. Chefs often favor customizing flavors with their spice blends over relying on pre-seasoned options. Traditional methods of production, centered on fermenting pure fish and salt, yield intricate umami profiles. These profiles are foundational to a myriad of dishes in Vietnamese, Thai, and Filipino culinary traditions.

Innovations in flavored fish sauces cater to consumers who prioritize convenience and those experimenting with fusion cuisines. By infusing ingredients like chili, garlic, and lime during fermentation or blending post-production, these sauces have carved a niche. They resonate especially with Western consumers, who, while delving into Asian flavors, gravitate towards these familiar taste profiles. This strategic alignment has facilitated broader acceptance. The upward trend underscores adept product development, balancing authentic umami roots with regional flavor inclinations. This strategy not only broadens the appeal but also extends the sauce's use beyond its traditional Asian confines. There's a burgeoning market for premium flavored variants. By marrying age-old fermentation techniques with artisanal spice selection, these products stand poised for gourmet retail and upscale dining venues.

By Distribution Channel: Retail Strength Meets Foodservice Momentum

In 2025, retail channels commanded a dominant 65.11% market share, capitalizing on their vast distribution networks and deep-rooted consumer familiarity. Meanwhile, the foodservice segment is on an upswing, projected to grow at a 5.48% CAGR through 2031, driven by the rising popularity of Asian cuisines and innovative menu trends. The retail sector has forged strong ties with ethnic grocery chains and specialty food stores. Mainstream supermarkets are also jumping on board, recognizing the surging consumer interest in fish sauce. Modern trade is expanding, with hypermarkets and supermarkets broadening consumer access to a wider range of products. At the same time, convenience stores are adeptly capturing impulse buys and catering to single-serve needs.

The rise of online retail is unlocking avenues for direct-to-consumer sales and subscription models. This is especially true for premium and artisanal products, which leverage storytelling and brand differentiation to command higher margins. The foodservice industry's growth is a testament to the restaurant sector's embrace of Asian flavors. Fast-casual chains and upscale dining spots are now seamlessly weaving fish sauce into a variety of dishes, moving beyond its traditional Asian roots. Culinary schools are playing a pivotal role, integrating fish sauce education into their curriculums, ensuring chefs are well-versed in its diverse applications. This growing momentum in the foodservice sector presents a golden opportunity for suppliers. Those who can consistently deliver quality, offer technical support, and assist in menu development will find restaurants eager to integrate fish sauce into their offerings.

Geography Analysis

In 2025, Asia-Pacific commanded a dominant 74.92% market share, underscoring its rich cultural integration and robust production infrastructure. However, the region grapples with supply chain vulnerabilities, notably those stemming from the toll of climate change on anchovy stocks. Anchored by production hubs, Vietnam and Thailand shine, with Vietnam alone churning out around 418 million liters annually. Notably, data from the American Culinary Federation indicate that the average Vietnamese consumer consumes approximately 1 gallon per year. Yet, traditional production methods are under siege from environmental shifts. Projections from the University of British Columbia warn of over 20% fish stock losses in the South China Sea, even with moderate warming. In response, the region pivots towards a growth strategy centered on technological innovation and sustainability. A testament to this shift is CP Foods, which has implemented blockchain traceability systems across its supply chains, aligning with international export standards. Moreover, China's resurgence and its changing demand patterns play a pivotal role in shaping regional pricing and supply distribution, especially for premium exports.

North America and Europe are witnessing a surge in Asian cuisine adoption, propelled by the globalization of Asian flavors and the rise of fusion cooking. Notably, flavors from China and Japan have ascended to the top 5 global culinary preferences. A deep dive by Unilever Food Solutions highlights a trend: Eastern umami flavors are seamlessly weaving into Western dishes. This cross-cultural culinary fusion is broadening the scope of usage occasions, extending well beyond traditional ethnic contexts. While both regions enjoy a well-established import infrastructure and a consumer base eager to experiment with premium ingredients, they aren't without challenges. Regulatory hurdles, especially sodium reduction initiatives and import authentication mandates, loom large. The FDA's voluntary sodium reduction targets and the EU's stringent traceability regulations pose compliance challenges. These regulations tend to favor larger producers, equipped with advanced quality management systems, potentially sidelining smaller artisanal imports.

Middle East and Africa are on an upward trajectory, boasting an impressive 6.61% CAGR expected through 2031. This growth is largely attributed to the expanding Muslim populations and the burgeoning halal food market. In fact, global spending on halal food is set to touch a staggering USD 1.7 trillion by 2025. A significant boost comes from Malaysia, which boasts a holistic halal ecosystem. This ecosystem, with its robust regulatory frameworks and certification infrastructure, is paving the way for trade expansion across Muslim-majority markets. Meanwhile, Indonesia has rolled out new halal certification requirements, effective October 2024. While this presents a golden opportunity, it also poses compliance hurdles for exporters eyeing the world's largest Muslim demographic. Urbanization, rising disposable incomes, and a cultural embrace of Asian cuisines to immigration and global business ties are further fueling the region's food service expansion and premium product adoption. South America, too, is catching the wave. With its Asian immigrant communities and a penchant for culinary experimentation, urban centers are witnessing a surge in fusion cuisine concepts. Affluent consumers are particularly drawn to these, seeking genuine and authentic flavor experiences.

Competitive Landscape

The fish sauce market remains moderately concentrated, with leadership fragmented due to traditional production methods and regional specializations. These factors not only hinder consolidation but also empower niche players to uphold their market positions through authenticity and quality differentiation. Companies boasting integrated supply chains and technological prowess are thriving in this landscape. A prime example is Masan Group's CHIN-SU Phu Quoc facility, which spans 22,000 square meters, processes over 10,000 tonnes of fish annually, and adheres to ISO and HACCP certification standards.

Strategic differentiation now hinges on traceability and sustainability. Companies are increasingly turning to blockchain technology, not just for compliance, but as a badge of premium positioning and a ticket to export markets. As traditional high-sodium profiles grapple with regulatory scrutiny, there's a shift towards health-conscious reformulations and convenience. Single-serve packaging and ready-to-use formats are emerging as solutions, catering to evolving consumer lifestyles.

Companies adopting comprehensive quality management systems are reaping competitive rewards. A case in point is CP Foods, whose blockchain-enabled QR code systems underscore the dual benefits of digital transformation: bolstering consumer trust and ensuring regulatory adherence. The market is witnessing the rise of disruptors, notably alternative protein developers and clean-label advocates. These players, harnessing fermentation expertise, are crafting novel umami solutions. In response, established brands are pursuing organic certifications, carving out premium market positions, and forging strategic partnerships to broaden their distribution across varied geographies.

Fish Sauce Industry Leaders

Masan Group

Unilever PLC

Viet Phu Inc. (Red Boat Fish Sauce)

Rayong Fish Sauce Industry Co. Ltd

Thai Fishsauce Factory (Squid Brand)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thai Union Group formed a joint venture with Nippon Suisan Kaisha Ltd. to create TN Fine Chemicals Co., Ltd., investing over 80 million baht in new production equipment to convert seafood by-products into high-grade tuna oil for infant formula applications, targeting sales exceeding 125 million baht with key export markets in Japan, the US, and the EU. This strategic move demonstrates vertical integration trends in seafood processing while creating value-added products from traditional waste streams.

- June 2024: TraSeable implemented blockchain-enabled seafood traceability pilot programs in Pacific regions, tracking approximately 50,000 fish through tablet-based digital systems that demonstrate affordable technology solutions for small-scale producers and regional operators.

- March 2024: TransGenie launched blockchain-based traceability solutions specifically designed for aquaculture supply chains, offering immutable record-keeping for catch data, processing milestones, and transport documentation that addresses fraud prevention and sustainability verification requirements.

Global Fish Sauce Market Report Scope

Fish sauce is made from brackish water, seawater, and freshwater fish with a salt concentration of 22-26%, w/v. It is mainly used as a condiment to flavor rice and other cereal dishes, especially in Thai dishes.

The global fish sauce market is segmented by product type, composition, end-user, and geography. By product type, the market is segmented into industrial and traditional. By composition, the market is segmented into mass and premium. The market is segmented by end-users into food manufacturers, retail, and food service. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Category

| Conventional |

| Organic |

By Flavor

| Plain Fish Sauce |

| Flavored / Spiced Fish Sauce |

By Distribution Channel

| Food Processors | |

| Foodservice | |

| Retail Channels | Hypermarkets/Supermarkets |

| Convenience and Specialty Stores | |

| Online Retail | |

| Other Retail Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Category | Conventional | |

| Organic | ||

| By Flavor | Plain Fish Sauce | |

| Flavored / Spiced Fish Sauce | ||

| By Distribution Channel | Food Processors | |

| Foodservice | ||

| Retail Channels | Hypermarkets/Supermarkets | |

| Convenience and Specialty Stores | ||

| Online Retail | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the fish sauce market in 2026?

It stands at USD 2.87 billion and is forecast to climb to USD 3.65 billion by 2031.

Which region generates most revenue?

Asia-Pacific contributes about 74.92% of global value, thanks to entrenched cultural consumption and robust production capacity.

What is driving recent sales momentum in North America?

Mainstream adoption of Asian flavors in fast-casual dining and home cooking has widened retail distribution and menu applications.

How are sodium-reduction policies influencing product development?

Producers are trialing potassium blends, concentrated formulas, and precision dosing caps to cut sodium without diluting flavor authenticity.

Which product segment is growing fastest?

Organic variants lead with a 6.43% CAGR as health-conscious shoppers seek clean-label and sustainably sourced condiments.

Page last updated on: