United States Hot Sauce Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Hot Sauce Market Analysis by Mordor Intelligence

The United States hot sauce market size was valued at USD 1.25 billion in 2025 and is estimated to grow from USD 1.29 billion in 2026 to reach USD 1.57 billion by 2031, at a CAGR of 4.0% during the forecast period 2026-2031. Hot sauce is transitioning from an occasional condiment to a staple in American meals, buoyed by increased household use and heightened visibility on restaurant menus. Younger consumers, particularly Gen Z and millennials, are driving this demand surge. Investor disclosures from McCormick reveal that these younger demographics now allocate more of their budget to hot sauce than to ketchup, signaling a significant shift in condiment preferences. Furthermore, restaurant chains and foodservice operators are bolstering the hot sauce market, leveraging branded sauces to bridge menu trials with retail sales. Regulatory and scientific influences are also reshaping the market's direction. The FDA's proposed front-of-package sodium disclosure and recent peer-reviewed studies on capsaicin are steering the market towards low-sodium, clean-label, and functional products. However, challenges persist. The market grapples with input cost pressures, as pepper supplies remain vulnerable to Mexican crop conditions and freight-related fluctuations, jeopardizing output and squeezing profit margins[1]Source: United States Department of Agriculture, "U.S. Horticultural Imports From Mexico: 14 Years of Expansion", ers.usda.gov.

Key Report Takeaways

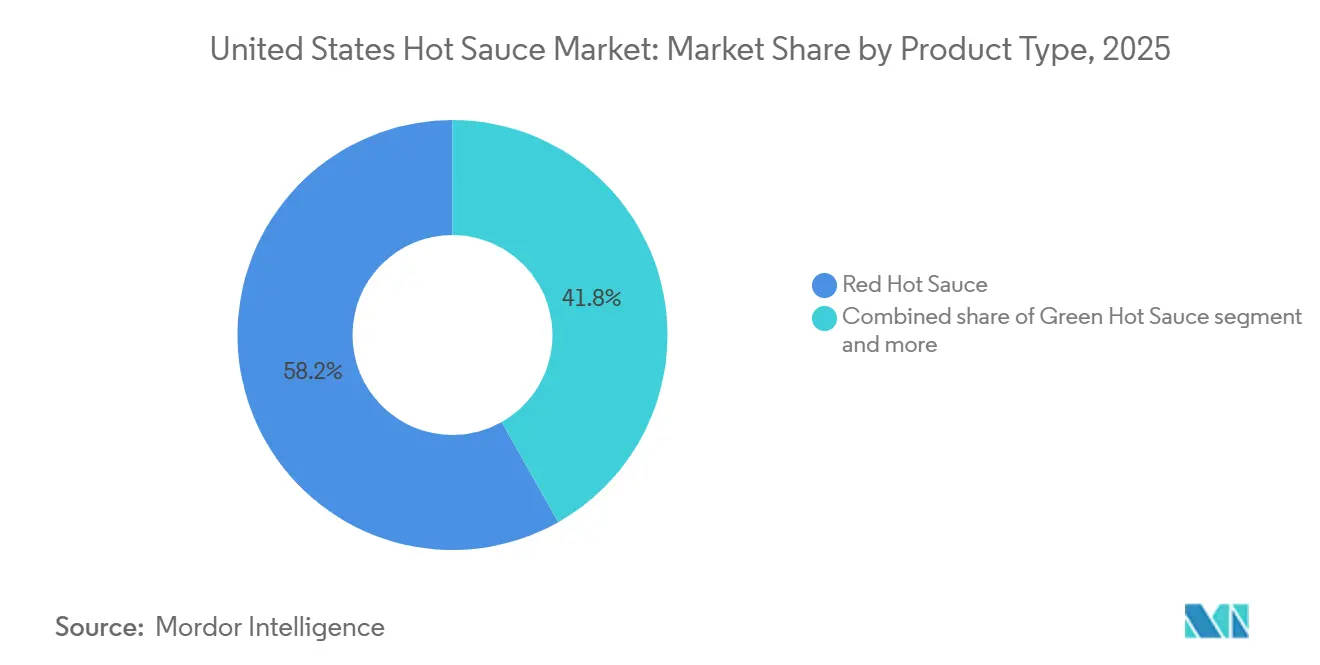

- By product type, red sauces accounted for the largest share of the United States hot sauce market, at 58.18% in 2025, while green sauces are projected to grow at the fastest CAGR of 6.50% during 2026-2031.

- By flavor, plain accounted for the largest share of the United States hot sauce market, at 69.24% in 2025, while flavored products are projected to grow at the fastest CAGR of 5.98% during 2026-2031.

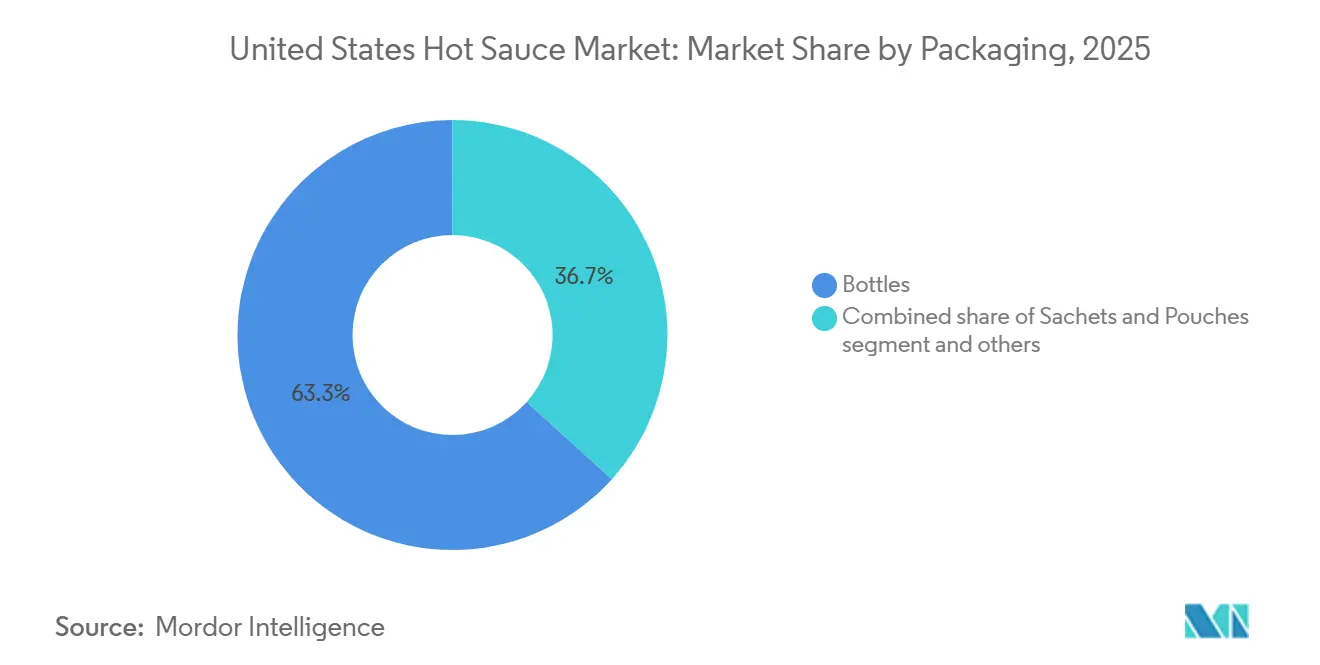

- By packaging, bottles accounted for the largest share of the United States hot sauce market, at 63.29% in 2025, while sachets and pouches are projected to grow at the fastest CAGR of 6.19% during 2026-2031.

- By distribution channel, retail accounted for the largest share of the United States hot sauce market, at 59.37% in 2025, while HoReCa is projected to grow at the fastest CAGR of 6.31% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hot Sauce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream adoption of spicy condiments in everyday meals | +1.0% | National, with highest penetration in the South and Southwest | Short term (≤ 2 years) |

| Premiumization through craft, artisanal, and small-batch formulations | +0.8% | National, with early gains in coastal urban markets and Sun Belt metros | Medium term (2-4 years) |

| Qsr and fast-casual menu integration of signature hot sauces | +0.7% | National, strongest in regions with high QSR density in the Southeast and Midwest | Short term (≤ 2 years) |

| E-commerce and direct-to-consumer expansion for niche brands | +0.6% | National, with stronger D2C shipments into high-income suburban ZIP codes | Medium term (2-4 years) |

| Functional, clean-label, and low-calorie positioning | +0.5% | National, with stronger traction in the Northeast and West Coast | Medium term (2-4 years) |

| Social media, challenge culture, and influencer-led discovery | +0.4% | National, with stronger virality among Gen Z in urban and suburban clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mainstream Adoption of Spicy Condiments in Everyday Meals

In the U.S., hot sauce is evolving from an occasional condiment to a staple in meals, both at home and when dining out. Early 2025 disclosures from McCormick revealed a significant shift: Gen Z and millennials are now spending more on hot sauce than ketchup, indicating a lasting change in preferences rather than a fleeting trend. Restaurants further bolster this shift; diners who sample branded sauces in quick-service and casual settings often seek them out in retail stores, showcasing the growing influence of foodservice on retail demand. McCormick highlighted that Frank’s RedHot expanded its reach to over 6 million U.S. households in fiscal 2024, attributing the surge to partnerships with quick-service restaurants (QSRs) and heightened in-store visibility. These partnerships not only increased brand exposure but also encouraged trial among new consumers, converting them into repeat buyers. This underscores the trend of turning foodservice trials into consistent household demand in the U.S. hot sauce market, reflecting the category's growing integration into everyday consumption habits.

Premiumization Through Craft, Artisanal, and Small-Batch Formulations

As consumers in the U.S. increasingly scrutinize ingredient lists, pepper origins, and flavor complexity, the country's hot sauce market is witnessing a notable value uptick. Research from McIlhenny, highlighted in 2025, revealed that the Mexican-style hot sauce subcategory surged by 20% in the year ending June 2024. This trend underscores the notion that premium flavored variants are outpacing the broader hot sauce category. Instead of relying on mass advertising, this segment of the U.S. hot sauce market is being shaped by small-batch production, fermentation-driven profiles, and transparent ingredient labeling. TRUFF's leap to over 17,000 retail outlets underscores the potential of premium positioning, especially when bolstered by robust branding and widespread store access. The trend of premiumization is not only expanding price ranges within the U.S. hot sauce market but also providing established brands the opportunity to defend their market share through line extensions. Simultaneously, it paves the way for craft labels to cultivate loyalty via unique tastes and distinctive packaging.

QSR and Fast-Casual Menu Integration of Signature Hot Sauces

Restaurant chains are increasingly bolstering the U.S. hot sauce market by incorporating branded sauces into their menu launches and limited-time offers. These collaborations not only drive sales in the foodservice sector but also enhance in-store awareness of the sauces, creating a synergistic effect between foodservice and retail channels. In a notable move, KFC teamed up with Mike’s Hot Honey in February 2025, launching a limited-time spicy chicken in conjunction with major delivery platforms. This partnership highlights how restaurant distribution can rapidly expand product trials, reaching a broader audience through established foodservice networks. Similarly, Taco Bell introduced Frank’s RedHot Diablo Sauce in October 2025, integrating it into its Crispy Chicken platform. This launch reinforced the importance of co-branded sauces in menu strategies, as it not only attracted customers to the restaurant but also increased the sauce's visibility in retail stores. This approach streamlines customer acquisition for the U.S. hot sauce market: restaurants shoulder a portion of the trial costs, while sauce brands enjoy heightened visibility, increased consumer engagement, and improved retail traction.

E-Commerce and Direct-to-Consumer Expansion for Niche Brands

Owing to its low unit price, compact packaging, and high repeat-purchase rate among dedicated buyers, the U.S. hot sauce market is thriving on e-commerce platforms. These characteristics make it easier to implement strategies like subscriptions, online multipacks, and direct-to-consumer launch tactics that pose challenges in larger packaged food categories. Moreover, online platforms empower smaller hot sauce brands with direct access to invaluable customer data, enabling them to monitor flavor preferences, reorder timings, and regional demands. This data-driven approach enables brands to refine their offerings and better cater to evolving consumer needs. Highlighting this trend, Frank’s RedHot revealed in January 2026 that 41% of its U.S. enthusiasts experiment with new recipes for social events. This insight underscores the market's alignment with discovery-driven digital sales and the propensity for online replenishment. Consequently, online channels are emerging not just as revenue streams for the U.S. hot sauce market but also as experimental platforms for limited flavors, bundled formats, and region-specific campaigns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sodium, sugar, and capsaicin health concerns | -0.4% | National, with higher sensitivity in health-conscious segments in the Northeast and West Coast | Medium term (2-4 years) |

| Raw material volatility in peppers, vinegar, and specialty inputs | -0.5% | National supply impact, most acute for manufacturers dependent on Mexican pepper sourcing | Short term (≤ 2 years) |

| Shelf-space concentration and intensifying brand fragmentation | -0.3% | National, most constraining in the mid-tier between mass-market incumbents and premium craft brands | Long term (≥ 4 years) |

| Food safety, labeling, and traceability compliance burden | -0.3% | National, with disproportionate impact on smaller manufacturers with limited compliance infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sodium, Sugar, and Capsaicin Health Concerns

Nutrition labeling and health concerns are increasingly scrutinizing the U.S. hot sauce market. On January 16, 2025, the FDA proposed a front-of-package rule that could label many standard hot sauces as high in sodium. A typical teaspoon serving of these sauces contains between 100 mg to 210 mg of sodium, surpassing the 140 mg limit set for low-sodium claims under federal guidelines[2]Source: Federal Register, "Food Labeling: Front-of-Package Nutrition Information", federalregister.gov . While this labeling won't necessarily dampen overall demand, it may steer choices for consumers vigilant about their sodium intake. This regulatory shift could also prompt manufacturers to innovate and develop healthier alternatives to retain market share. Mid-tier brands feel the brunt of this pressure. Reformulating for lower sodium often means sourcing pricier ingredients, which can also shorten shelf life. This scenario poses a margin challenge in the U.S. hot sauce market, particularly for brands unable to command a premium yet needing to cater to health-conscious consumers.

Raw Material Volatility in Peppers, Vinegar, and Specialty Inputs

Due to concentrated sourcing and limited cultivar substitution, the U.S. hot sauce market faces volatility in pepper supply. According to the IFPA, 73% of the U.S.'s hot pepper volume comes from Mexico, underscoring the market's heavy reliance on this single cross-border supply chain. Data highlighted that in October and November 2024, jalapeño FOB prices in Pharr, Texas, surged to an average of USD 0.75 per pound, marking a 22% increase from the previous year[3]Source: United States Department of Agriculture, " National FOB Review", ams.usda.gov. Additionally, the report pointed out recurring supply-related production halts at Huy Fong Foods. The stakes are heightened as genuine hot sauce recipes often hinge on specific pepper varieties, whose unique taste and heat can't be substituted with generic alternatives. As a result, even amidst favorable demand conditions, the U.S. hot sauce market remains susceptible to weather fluctuations, crop quality challenges, and abrupt cost surges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Green Hot Sauce Gaining Ground on Legacy Red Formats

In 2025, red hot sauce captured 58.2% of the U.S. hot sauce market, solidifying its status as the top choice. This dominance stems from its household familiarity, extensive retail presence, and deep-rooted brand loyalty. Major U.S. hot sauce brands lean on red sauce as their primary draw, given its versatility across daily meals, restaurant tables, and cooking scenarios, all with minimal consumer education. In August 2024, TABASCO expanded its reach by introducing Salsa Picante at Walmart and Amazon. This move transitions its legacy pepper brand into a thicker, Tex-Mex style, underscoring the industry's strategy: evolving familiar brands into adjacent formats to bolster the leading red segment rather than relying solely on the original.

Green hot sauce is set to be the fastest-growing segment in the U.S. hot sauce market, with a projected CAGR of 6.5% from 2026 to 2031. This surge is attributed to jalapeño- and serrano-based formulations, which offer a fresher, herb-forward heat. Such profiles resonate with premium retailers, chef-driven menus, and younger consumers seeking nuanced flavors. The U.S. hot sauce market is increasingly accommodating this segment, as green sauces complement avocado-centric meals, bowls, tacos, and other dishes where consumers desire brightness alongside heat. McIlhenny’s January 2026 announcement, revealing a portfolio of over 20 core and extended SKUs, highlights how major manufacturers are diversifying to capture these swiftly rising subtypes, preempting smaller niche brands from seizing the opportunity.

By Flavor: Plain Dominance Conceals a Rapidly Compressing Flavored Subsegment

In 2025, plain hot sauce commanded a dominant 69.2% share of the U.S. hot sauce market, outpacing all other flavor segments. This stronghold is no accident; plain red sauce has cemented its status as a pantry essential, seamlessly complementing a wide array of meals. Moreover, its prominence in U.S. dining is underscored by its frequent appearance in restaurants, where many dishes lean towards the classic vinegar-pepper taste, eschewing more complex flavor profiles. While this entrenched position underscores the sauce's habitual purchase, it also highlights a reliance on routine buying, contrasting with the novelty trends capturing attention in other segments.

From 2026 to 2031, flavored hot sauces are projected to outpace their peers, with a robust 6.0% CAGR, making them the fastest-growing segment in the U.S. market. This surge is largely attributed to hybrid flavors like mango habanero, garlic chipotle, and sweet-spicy blends, which are redefining hot sauce's role from mere heat to a versatile flavor enhancer. Notably, Kraft Heinz's 2025 Flavor Tour line and Frank’s RedHot's quartet of new flavored sauces in January 2026 underscore the trend, highlighting major food corporations' pivot towards globally inspired and occasion-centric profiles. As a result, flavored hot sauces are not only claiming premium shelf space but also carving out new culinary uses, even if this expansion is partly at the expense of plain-sauce consumers trading up rather than increasing overall consumption.

By Packaging: Sachet and Pouch Formats Disrupting the Bottle-Centric Status Quo

In 2025, bottles commanded a dominant 63.3% share of the U.S. hot sauce market, solidifying their status as the preferred packaging format. Bottles play a pivotal role in the U.S. hot sauce landscape, enhancing shelf presentation, facilitating kitchen storage, serving on restaurant tabletops, and ensuring a familiar consumer experience. This format aligns with the visual recognition strategies major brands have cultivated over decades, making bottles crucial for impulse recognition in retail settings. Thus, while alternative formats are on the rise, the bottle remains entrenched, benefiting from consumer habits, display economics, and brand memory.

Sachets and pouches are projected to grow at a robust 6.2% CAGR from 2026 to 2031, emerging as the fastest-growing packaging format in the U.S. hot sauce arena. Their popularity is particularly pronounced in the foodservice sector, where operators prioritize portion control, waste reduction, sanitation, and streamlined back-of-house handling. According to Mordor Intelligence’s Argentina portal, single-use sachets in foodservice can curtail sauce waste by up to 18% compared to traditional dispensers, shedding light on the growing endorsement from procurement teams. Reinforcing this trend, McIlhenny unveiled TABASCO Salsa Picante in a portion-control packet format for foodservice in March 2025, underscoring the strategic significance of single-serve packs in the U.S. hot sauce market.

By Distribution Channel: Retail Incumbency Masks Foodservice’s Structural Ascent

In 2025, retail claimed a dominant 59.4% share, solidifying its position as the leading distribution channel in the U.S. hot sauce market. Supermarkets and hypermarkets serve as primary hubs for mass brands, offering extensive product selection, familiar product placement, and straightforward price comparisons. The U.S. hot sauce market continues to rely on retail for regular household restocking, particularly for established brands that thrive on repeat purchases and prominent shelf visibility. However, the retail landscape is intensifying, with private-label products and flavor extensions exerting pressure on mid-tier brands.

Between 2026 and 2031, HoReCa and foodservice channels are set to expand at a robust 6.3% CAGR, emerging as the fastest-growing segment in the U.S. hot sauce market. This growth underscores the dual role of restaurants: not only as revenue generators but also as platforms where branded sauces can swiftly transition from menu highlights to retail staples. Additionally, the U.S. hot sauce market is witnessing a surge in online retail, which is bolstering this trend. Smaller brands, after gaining traction through foodservice partnerships or social media buzz, are finding a national stage online. Highlighting the market's nuances, Grupo Herdez noted in its 2025 earnings call that a dip in spending among Hispanic consumers affected segments of its U.S. exports, underscoring the variability in channel performance driven by demographic and local demand dynamics.

Geography Analysis

In 2025, the South and Southwest emerged as the dominant regions for hot sauce consumption in the U.S., though the draft refrains from specifying their exact market share. These areas leverage Louisiana's rich hot sauce legacy and the prevalent influence of Mexican and Tex-Mex cuisines, especially in Texas, Arizona, and New Mexico. The U.S. hot sauce market finds a robust foothold here, as locals readily incorporate jalapeños, serranos, and habaneros into their cooking, eliminating the need for extensive consumer education. This positions the South and Southwest as primary hubs for both traditional red sauces and the swiftly gaining popularity of Mexican-style and green variants.

According to the draft, the Pacific Coast and Mountain West are the quickest to adopt trends in the U.S. hot sauce market, driven by a rising demand for fermented and function-oriented products. These regions are swiftly gravitating towards offerings that emphasize clean labels, probiotic benefits, ingredient transparency, and premium flavors. Research on capsaicin, published in 2025, bolsters this trend, shedding light on the growing popularity of wellness-focused products in these areas. Meanwhile, the Northeast and West Coast stand out as key premium markets, thanks to their affluent consumers, better access to specialty retailers, and a heightened appreciation for artisanal products.

The U.S. hot sauce landscape reveals a dichotomy: traditional regions dominate in volume, while premium markets drive higher-value growth. Coastal and Sun Belt retailers have been instrumental in propelling premium brands, and e-commerce has bridged gaps in areas lacking specialty stores. Even outside traditional strongholds, restaurants are reshaping demand. For instance, Jack in the Box's Nashville Hot launch has broadened the hot sauce trial in the Midwest. Regions with heightened sodium awareness, like parts of the Midwest and Southeast, might see a surge in demand for reduced-sodium variants, especially with the FDA's proposed front-of-package labeling rule. McCormick's fiscal 2024 move to integrate over 6 million U.S. households into Frank's RedHot underscores the untapped potential in suburban and mid-market areas, extending beyond established regional hubs.

Competitive Landscape

The United States hot sauce market is moderately fragmented; McIlhenny Company and McCormick & Company dominate with robust brand recognition, extensive distribution, and a prominent presence on store shelves. While these giants anchor the market's top tier, a diverse array of craft, premium, and regional brands occupies the remaining space. Highlighting the significance of hot sauce in its broader flavor portfolio, McCormick noted that its "heat platform" accounts for about 20% of company sales and is outpacing the growth of its other offerings. Today, success in the U.S. hot sauce market hinges not just on established shelf presence but also on product adjacency, foodservice outreach, and a continuous drive for innovation, all while maintaining brand familiarity.

In a decisive move, McCormick bolstered its foothold in the U.S. hot sauce market by acquiring an additional 25% stake in McCormick de Mexico for USD 750 million in January 2026, elevating its ownership to 75%. This strategic acquisition underscores McCormick's commitment to sauces and condiments that resonate with Mexican flavor profiles. Meanwhile, in March 2025, McIlhenny ventured further into the Mexican-style segment by introducing TABASCO Brand Salsa Picante for U.S. foodservice, emphasizing portion-control formats tailored for operators. Demonstrating the trend, Taco Bell collaborated with Frank’s RedHot in October 2025, highlighting how top brands leverage QSR partnerships to simultaneously boost awareness and demand. These strategic maneuvers indicate a shift in the U.S. hot sauce market, where competition is increasingly centered on platform building rather than mere shelf presence.

There's untapped potential at both the premium and value spectrums of the U.S. hot sauce market. At the premium end, there's ample growth opportunity for functional and fermented products, as few brands successfully merge scientific credibility with widespread distribution. Conversely, at the value end, mid-tier brands grapple with heightened competition from private labels, struggling to justify price or ingredient quality distinctions. As the U.S. hot sauce market gears up for the FDA’s Food Traceability Rule compliance deadline in July 2028, there's a noticeable shift towards heightened traceability expectations. This landscape suggests that while larger players can further solidify their stance through sourcing controls, scale, and retail access, smaller brands must either carve out sharper differentiations or hone in on specific channels to maintain their ground.

United States Hot Sauce Industry Leaders

-

McIlhenny Company

-

McCormick & Company, Incorporated

-

Huy Fong Foods, Inc.

-

The Kraft Heinz Company

-

B and G Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: McCormick & Company completed the USD 750 million acquisition of an additional 25% ownership interest in McCormick de México from Grupo Herdez, raising McCormick's stake to 75%. The deal, funded through cash and commercial paper, strengthens McCormick's hot sauce and condiments portfolio in Mexico and provides a platform for Latin American market expansion.

- January 2026: Frank's RedHot launched four new sauces on National Hot Sauce Day: Garlic Parmesan Wing Sauce and Dip, Pineapple Hawaiian Wing Sauce and Dip, Spicy Maple Wing Sauce and Dip, and Ghost Pepper Ranch Squeeze Sauce. The launch was paired with a new marketing campaign timed to the Super Bowl, reinforcing the brand's game-day consumption positioning.

- January 2026: McIlhenny Company and Absolut Vodka launched Absolut × TABASCO Chili Pepper Flavored Vodka across 50+ global markets, including the U.S. The product is made using TABASCO's fermented red pepper mash and contains no added sugar, positioning the launch as a premium spirits extension of the hot sauce brand.

- October 2025: Taco Bell launched Frank's RedHot Diablo Sauce as part of its Crispy Chicken platform, marking one of the hot sauce category's most prominent QSR co-branding integrations of the year. Frank's RedHot is the top-selling hot sauce in the U.S., according to market data, and the partnership is expected to extend the brand's penetration into younger, fast-food-native consumer segments.

United States Hot Sauce Market Report Scope

Hot sauce is a pungent, spicy condiment or seasoning made primarily from chili peppers. The United States Hot Sauce Market is segmented by product type, flavor, packaging, and distribution channel. By product type, the market is segmented into red hot sauce, green hot sauce, yellow hot sauce, and others. By flavor, the market is segmented into plain and flavored. By packaging, the market is segmented into bottles, sachets, pouches, and others. By Distribution channel, the market is segmented into horeca/foodservice and retail.

| Red Hot Sauce |

| Green Hot Sauce |

| Yellow Hot Sauce |

| Others |

| Plain |

| Flavored |

| Bottles |

| Sachets and Pouches |

| Others |

| HoReCa/Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Other Retail Stores |

| By Product Type | Red Hot Sauce | |

| Green Hot Sauce | ||

| Yellow Hot Sauce | ||

| Others | ||

| By Flavor | Plain | |

| Flavored | ||

| By Packaging | Bottles | |

| Sachets and Pouches | ||

| Others | ||

| By Distribution Channel | HoReCa/Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Other Retail Stores | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for hot sauce in the United States?

The United States hot sauce market is projected to grow from USD 1.29 billion in 2026 to USD 1.57 billion by 2031 at a 4.0% CAGR.

Which product type leads sales and which one is growing the fastest?

Red hot sauce led with 58.2% share in 2025, while green hot sauce is forecast to grow the fastest at a 6.5% CAGR through 2031.

Why are restaurant partnerships important for hot sauce brands?

QSR and foodservice tie-ins create trial at scale and often push the same sauces into retail demand, which is why HoReCa and foodservice are growing at a 6.3% CAGR.

What is changing in consumer flavor preference?

Plain hot sauce still led with 69.2% share in 2025, but flavored products are expanding faster at a 6.0% CAGR as consumers look for more layered and globally inspired profiles.

Page last updated on: