Mustard Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.53 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

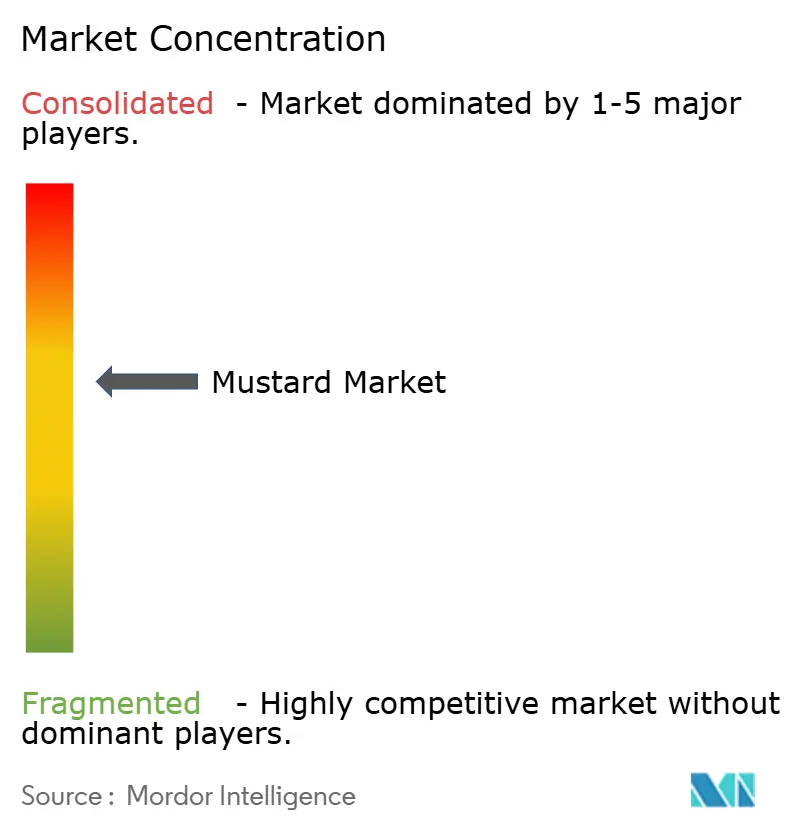

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mustard Market Analysis by Mordor Intelligence

Mustard market size in 2026 is estimated at USD 10.53 billion, growing from 2025 value of USD 10.01 billion with 2031 projections showing USD 13.55 billion, growing at 5.18% CAGR over 2026-2031. Consistent household use, growing interest in functional ingredients, and the spread of international cuisines position mustard products as a dependable yet dynamic category within global condiments. Manufacturers capitalize on wellness trends by highlighting mustard’s antioxidant profile, while quick-service restaurants rely on its thermal stability and natural preservative attributes to streamline menu costs. Premiumization is raising average selling prices, especially for region-specific Dijon, whole-grain, and organic lines, as consumers seek authentic flavor without artificial additives. Fast-expanding e-commerce platforms amplify visibility for smaller brands, broadening competitive intensity. Brand owners who integrate direct seed sourcing and regenerative agriculture already enjoy higher supply security and reputational benefits.

Key Report Takeaways

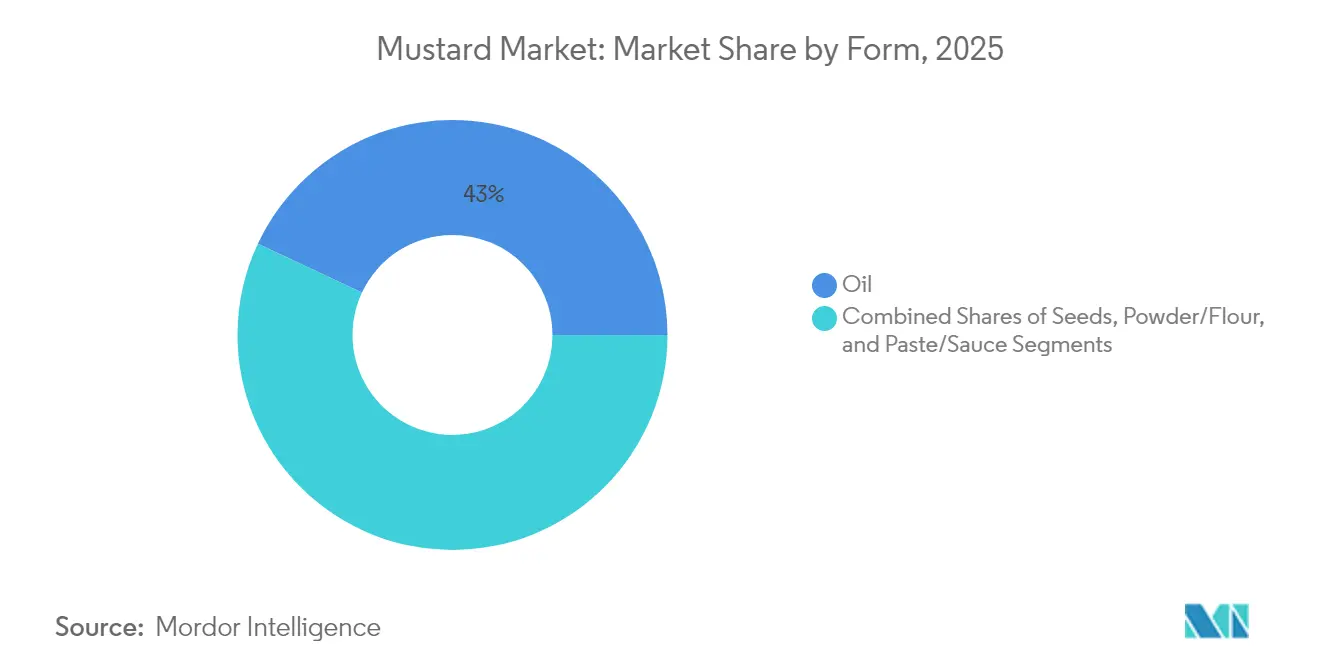

- By form, oil led with 43.02% shares of the mustard market in 2025; paste/sauce formats are expanding at a 6.12% CAGR through 2031.

- By nature, conventional products held 66.15% market share, while organic variants are growing at a 7.4% CAGR to 2031.

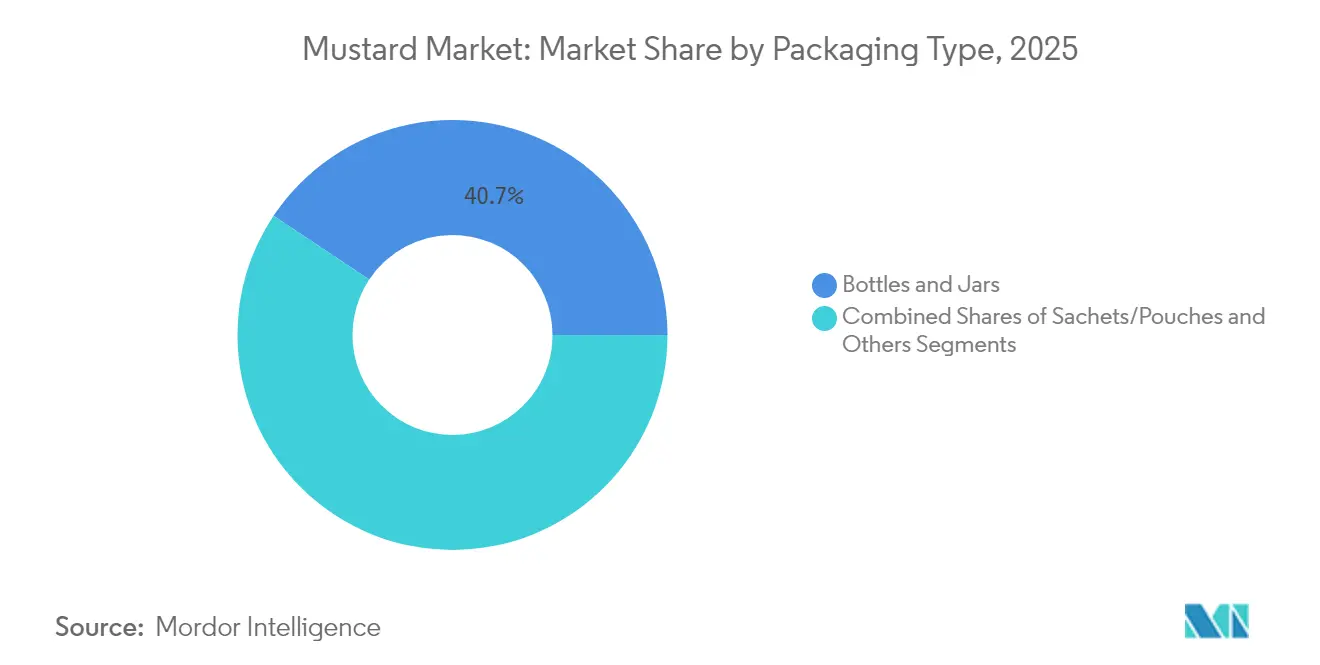

- By packaging type, bottles and jars retained 40.65% revenue share, whereas sachets and pouches are advancing at a 6.28% CAGR.

- By end-use channel, retail accounted for 72.15% share of sales in 2025; foodservice is projected to register a 4.55% CAGR as restaurant activity rebounds.

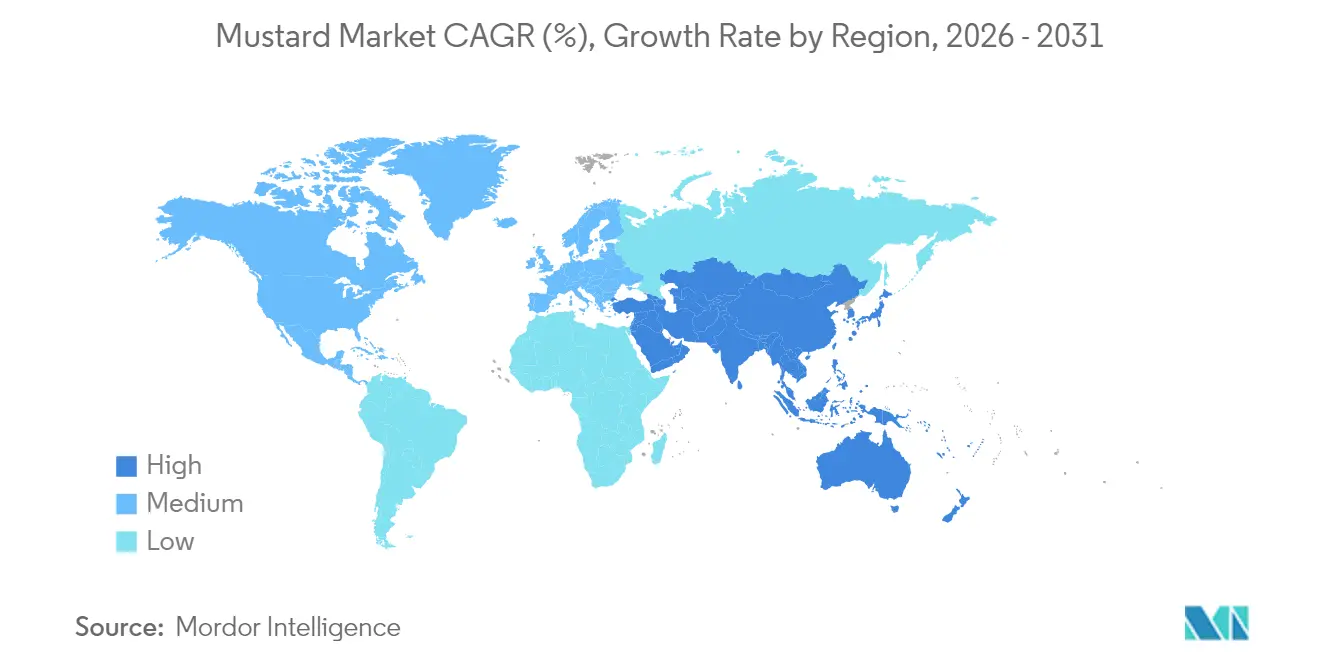

- By geography, Asia-Pacific captured 46.55% share of the mustard market in 2025 and is forecast to post the fastest 6.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mustard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for condiments and sauces | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Increasing popularity of fast food | +0.9% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Health awareness around antioxidant benefits | +1.1% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Expansion of international cuisines | +0.8% | Global metropolitan areas | Medium term (2–4 years) |

| Packaging and format innovation | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Growth in online grocery retail | +0.7% | Highest in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Condiments and Sauces Fuels Mustard Consumption Globally

The condiments sector's robust expansion creates a rising tide that elevates mustard products across multiple consumption occasions, from traditional table applications to industrial food processing. Restaurant industry sales projections of USD 1.5 trillion in 2025 demonstrate the scale of foodservice demand, where mustard serves as both a flavor enhancer and a cost-effective ingredient in menu diversification strategies[1]Source: National Restaurant Association, “State of the Restaurant Industry 2025,” restaurant.org. Mustard's versatility across a wide range of culinary applications serves as a key driver of its market growth, allowing food manufacturers to capitalize on single-ingredient platforms for the creation of diverse product portfolios. With the increasing consumer demand for mustard-based products, supply chain integration has emerged as a critical factor for success. To address this, companies are proactively investing in direct sourcing partnerships, ensuring a reliable supply of premium-quality raw materials and safeguarding product availability. These strategic initiatives not only enhance operational efficiency but also reinforce the competitive advantage of businesses operating in this market.

Increasing Popularity of Fast Food and Processed Meals Boosts Mustard Use

The expansion of the fast food sector is significantly driving the consumption of industrial mustard, primarily due to the adoption of standardized recipes and portion-controlled packaging. These practices create consistent and predictable demand streams, contributing to enhanced market stability. Additionally, the ongoing shift toward off-premises dining has been notable. This shift has amplified the demand for shelf-stable condiments that can maintain their flavor integrity during transportation. Mustard, with its natural preservation properties and extended shelf life, has emerged as a preferred choice over mayonnaise-based alternatives. Furthermore, processed food manufacturers are increasingly incorporating mustard as a clean-label ingredient. By leveraging its inherent antimicrobial properties, they are able to extend product shelf life while eliminating the need for synthetic preservatives, aligning with evolving consumer preferences for natural and sustainable food solutions.

Growing Health Awareness Supports Demand for Mustard Due to Its Antioxidant Properties

Increasing consumer health awareness is driving the transformation of mustard from a traditional condiment to a functional food with added value. Scientific research has validated this transition by highlighting the significant antioxidant properties found in mustard microgreens and seeds. These studies reveal that mustard microgreens are rich in chlorophyll, carotenoids, flavonoids, and phenolic compounds, which collectively enhance their antioxidant activity. This positions mustard microgreens as highly nutrient-dense functional foods, catering to the preferences of health-conscious consumers. Furthermore, the growing adoption of plant-based diets is amplifying the demand for mustard as a versatile flavor enhancer that provides complexity without the inclusion of animal-derived ingredients. Manufacturers are capitalizing on premium positioning opportunities by emphasizing mustard's inherent health benefits, such as its natural anti-inflammatory properties and selenium content. By leveraging health-focused marketing strategies, companies are effectively differentiating their products in an increasingly competitive condiment market.

Expansion of International Cuisines Promotes Mustard Use in Diverse Recipes

The globalization of food culture is driving consumer interest in mustard varieties beyond the traditional yellow, resulting in increased demand for premium options such as Dijon, whole grain, and specialty regional variants. The growing expatriate population in key metropolitan areas is accelerating the need for authentic ingredients. Middle Eastern markets, particularly the UAE and Saudi Arabia, are expanding their dietary preferences, showcasing a rising demand for diverse food products [2].Source: Food Export Association, "2025 UES Middle East Market Assessment", www.foodexport.org This trend creates growth opportunities for established players with extensive product portfolios while enabling market entry for specialty producers focusing on authentic regional offerings. The integration of Asian cuisine is significantly enhancing mustard oil consumption, where traditional culinary applications align with modern health trends to broaden its market appeal. Additionally, innovation in restaurant menus is driving product trials and adoption, as chefs leverage mustard-based sauces and marinades to differentiate their offerings and optimize food costs through strategic ingredient substitutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mustard seed production and price volatility | -0.8% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Competition from alternative condiments | -0.6% | North America and Europe | Medium term (2–4 years) |

| Short Shelf Life of Certain Mustard Products Can Lead to Inventory Challenges | -0.4% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Adulteration Risks and Quality Inconsistencies Reduce Consumer Trust | -0.4% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuations in Mustard Seed Production, Supply, and Pricing Create Market Volatility

Volatility in agricultural commodity prices significantly affects margins in the mustard products market. Studies indicate that mustard prices are most volatile during pre-harvest and harvest periods, creating cost unpredictability for manufacturers. To address this price risk, businesses are increasingly adopting forward contracting and vertical integration strategies, emphasizing the need for robust supply chain resilience. Government policies in major production regions further complicate the landscape. For example, India's National Mission on Oil Seeds and Oil Palm (NMOOP), aimed at increasing domestic production, has the potential to disrupt traditional trade flows[3]Source: United States Department of Agriculture, “Oilseeds: World Markets and Trade,” usda.gov. Additionally, climate variability exacerbates supply uncertainties, making advanced inventory management and pricing strategies critical for market players.

Competition from Alternative Condiments Limits Mustard's Market Growth Potential

The growing diversity within the condiments market is intensifying competitive dynamics as consumers increasingly explore global flavor profiles such as sriracha, harissa, and other offerings that deliver similar heat and complexity. Private-label brands are gaining market share by implementing aggressive pricing strategies, particularly within retail channels. These store brands capitalize on strong supplier relationships to provide products of comparable quality at reduced price points, thereby appealing to cost-conscious consumers. Additionally, innovation cycles in adjacent categories, notably hot sauces and specialty mayonnaises are capturing consumer interest and creating competition for wallet share, which may constrain mustard's position in household condiment purchases. The rising popularity of fusion cuisines is driving the development of hybrid products that combine mustard with other flavor profiles. While this trend risks commoditizing traditional mustard varieties, it simultaneously presents opportunities for premium positioning by emphasizing authenticity and leveraging heritage-focused marketing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Oil Dominance Faces Paste Innovation Challenge

Oil captured 43.02% share of the mustard market in 2025, owing to entrenched culinary habits in South Asia, whereas paste and sauce lines exhibit a 6.12% CAGR, the fastest within the form spectrum. Producers emphasize cold-pressed extraction, heart-healthy unsaturated fats, and clean-label claims to sustain oil demand. The mustard products market size for paste and sauce variants is forecast to broaden as busy households gravitate to ready-to-eat spreads and squeezable formats.

Consumer interest in diverse textures fosters extensions such as whole-grain spreads that pair with artisanal bread, while powdered mustard supports industrial seasoning blends. The market’s form diversity creates resilience against raw-material shocks; when seed prices rise, processors can shift emphasis toward higher-margin pastes that use smaller seed volumes.

By Nature: Organic Surge Challenges Conventional Dominance

Conventional offerings retained 66.15% share in 2025, but organic SKUs are advancing 7.4% annually, far outpacing category averages. The mustard products market size for organic lines benefits from transparent supply chains that satisfy consumers concerned about pesticide exposure and soil health. European retailers feature prominent organic store brands, promoting price competition that accelerates trial.

Certified supply remains limited, keeping input costs elevated; yet, scale advantages for large multinationals narrow the price gap versus conventional products. Processors cooperate with grower co-operatives to ensure non-GMO compliance, building marketing stories that reinforce premium positioning and defend margins.

By Packaging Type: Traditional Formats Meet Convenience Innovation

Bottles and jars dominated sales with a 40.65% contribution in 2025, validating their role in retail merchandising and family-size consumption. Still, sachets and pouches are moving ahead at a 6.28% CAGR because quick-service restaurants and delivery platforms demand portion-controlled units that curb waste. The mustard products market size for sachets aligns with the broader shift toward on-the-go snacks and meal kits.

Lightweight flexible materials reduce freight emissions and align with corporate carbon goals. In parallel, glass-jar makers explore weight-reduction techniques to retain premium cues while lowering transport costs. Across formats, tamper-evident closures and easy-pour spouts differentiate brand value propositions at the point of sale.

By End-Use: Retail Dominance Meets Foodservice Recovery

Retail generated 72.15% of 2025 revenue as households stocked pantries during economic uncertainty; nonetheless, foodservice is on track for a 4.55% CAGR through 2031. Chain restaurants standardize mustard flavor to maintain menu consistency, driving predictable bulk orders that stabilize plant utilization. Operators also push healthier condiment swaps, choosing mustard over sugar-heavy sauces to meet nutritional commitments.

Digital grocery platforms encourage brand experimentation via targeted promotions, while brick-and-mortar stores allocate more shelf facings to gourmet and regional labels. The mustard products market size within foodservice may accelerate further if hospitality-sector wage pressures spur ingredient substitution toward cost-efficient flavors such as mustard.

Geography Analysis

Asia-Pacific’s 46.55% share underscores its pivotal role in shaping the mustard products market. Regional growth of 6.85% CAGR reflects urban migration, rising disposable income, and the everyday use of mustard oil in Indian and Bangladeshi cooking. Policy support, including India’s Atmanirbhar oilseed program, bolsters domestic output and can temper raw-material cost swings over the long term.

North America remains a high-value market where per-capita spending surpasses global averages. The region favors premium Dijon and organic spreads, and online grocery penetration enhances shelf turn for niche brands. Restaurant chains leverage mustard’s clean-label status to satisfy calorie-conscious guests, supporting steady demand despite category maturity.

While Europe matches North America in product sophistication, there's a growing price sensitivity, largely due to the expansion of private labels. In 2024, EU regulators reported 248 compliance issues related to spice residue testing. This heightened scrutiny on imports has set stricter entry standards, posing challenges for budget-conscious exporters. On another front, both South America and the Middle East & Africa are witnessing a surge in imports, with growth rates in the double digits, driven by local processors broadening their flavor offerings.

Competitive Landscape

Global competition in the mustard market remains moderate, with heritage multinationals competing against agile artisanal labels and private retail brands. Prominent players in the global mustard market include Backwoods Mustard Company, Woeber Mustard Manufacturing Company, McCormick and Co., Conagra Brands Inc., and Unilever Plc. These companies are leveraging globalization to drive product innovation and engage in mergers and acquisitions, as leading global firms hold a significant share of the market. Mergers and acquisitions serve as a strategic approach for these players to strengthen their market position and maintain an edge over regional competitors.

Mid-size specialists, prioritizing regional authenticity and small-batch production, are successfully commanding premium prices in online channels. On the other hand, white-label producers, by offering lower-priced alternatives to branded SKUs, are pressuring established players to focus on attributes such as provenance, health benefits, and packaging convenience. The adoption of advanced technologies, including machine-vision seed grading, blockchain-based farm tracing, and AI-driven demand forecasting, is enabling companies to achieve operational efficiencies, enhance customer service, and safeguard profit margins.

Market share consolidation, particularly in segments requiring certification expertise, can be achieved through strategic mergers or minority investments in organic farming collectives. At the same time, the mustard products sector continues to provide opportunities for niche entrants, especially those exploring innovative flavor combinations or direct-to-consumer business models.

Mustard Industry Leaders

-

Backwoods Mustard Company

-

Woeber Mustard Manufacturing Company

-

Conagra Brands Inc.

-

Unilever Plc

-

McCormickand Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Heinz launched a limited-edition mustard, representing its first-ever collaborative sauce development in the United States.

- May 2024: Adani Wilmar has introduced 'Fortune Pehli Dhaar', a premium mustard oil crafted from the first pressing. This launch enhances the mustard oil market and caters to consumers seeking superior quality, purity, and traditional authenticity.

- February 2024: Unilever launched its first UK regenerative agriculture project focusing on mustard seeds and mint leaves for Colman's products, aiming to restore soil health and ensure crop resilience through partnerships with local farming cooperatives and academic institutions.

Global Mustard Market Report Scope

Mustard seeds are the tiny round seeds of various mustard plants. The seeds are usually about 1 to 2 millimeters in diameter and may be colored from yellowish-white to black. The global mustard market has been segmented by distribution channel into online Retailing, hypermarkets/ supermarkets, convenience stores/ grocery stores, and other Retailing. The market is also segmented by geography, including countries in North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on the value (in USD million).

| Seeds |

| Powder/Flour |

| Oil |

| Paste/Sauce |

| Conventional |

| Organic |

| Bottles and Jars |

| Sachets/Pouches |

| Others |

| Retail | Supermarkets / Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Seeds | |

| Powder/Flour | ||

| Oil | ||

| Paste/Sauce | ||

| By Nature | Conventional | |

| Organic | ||

| By Packaging Type | Bottles and Jars | |

| Sachets/Pouches | ||

| Others | ||

| By End-Use | Retail | Supermarkets / Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the mustard products market?

The mustard products market stands at USD 10.53 billion in 2026 and is expected to reach USD 13.55 billion by 2031.

Which region leads the market?

Asia-Pacific holds 46.55% of global revenue and is projected to grow at 6.85% CAGR through 2031, making it both the largest and fastest-growing region.

Which product form is most popular?

Mustard oil leads with 43.02% share, but paste and sauce formats are expanding faster at a 6.12% CAGR.

How significant is organic mustard demand?

Organic variants, though smaller today, are advancing at 7.4% CAGR, outperforming conventional products due to clean-label and wellness trends.

Page last updated on: