Sauces, Condiments, And Dressings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

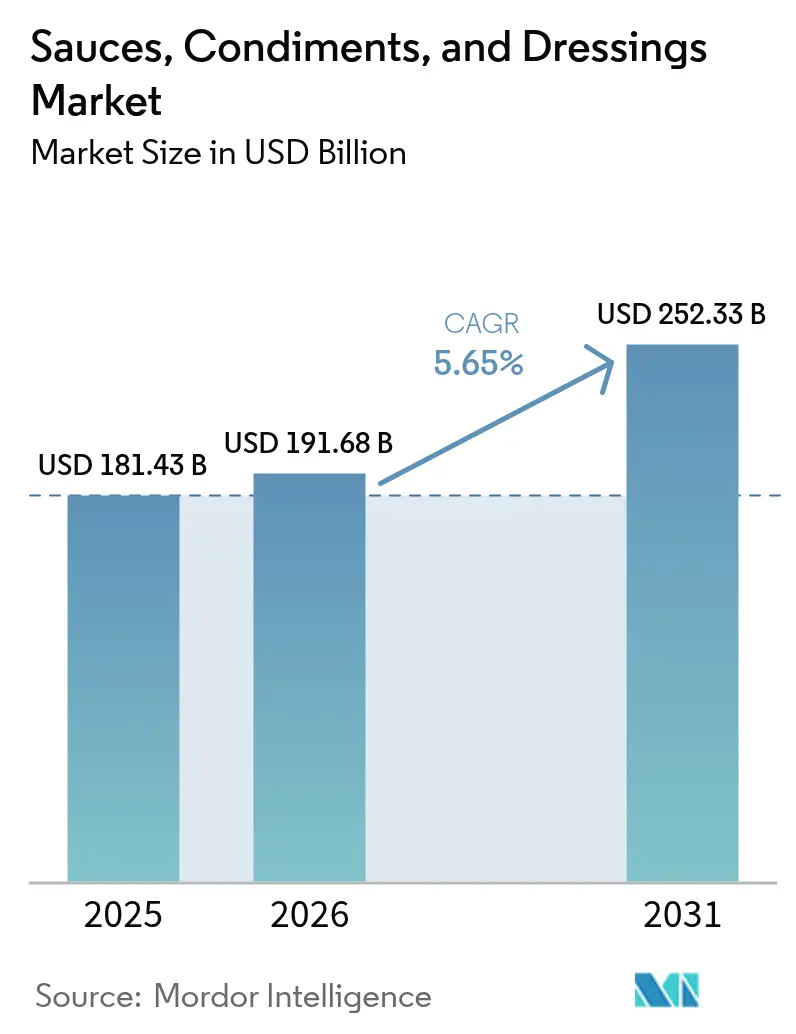

| Market Size (2026) | USD 191.68 Billion |

| Market Size (2031) | USD 252.33 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | Asia |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sauces, Condiments, And Dressings Market Analysis by Mordor Intelligence

The global sauces, dressings, and condiments market size in 2026 is estimated at USD 191.68 billion, growing from 2025 value of USD 181.43 billion with 2031 projections showing USD 252.33 billion, growing at 5.65% CAGR over 2026-2031. As consumers increasingly seek authentic flavors, premium clean-label recipes, and convenient meal solutions, value creation is surging across all channels. Modernization efforts, especially the U.S. Food and Drug Administration's decision to revoke 52 outdated standards in 2025, have eased reformulation challenges and expanded avenues for innovation. This regulatory change is expected to encourage manufacturers to experiment with new ingredients and formulations, fostering product differentiation and catering to evolving consumer preferences. Additionally, the growing emphasis on health-conscious eating habits has led to a surge in demand for low-sodium, organic, and gluten-free options within the sauces, dressings, and condiments category. Factors such as rapid urbanization in the Asia-Pacific, which is driving demand for ready-to-use condiments, a global rise in e-grocery adoption that enhances accessibility to diverse product offerings, and strategies for vertically integrated ingredient sourcing, which ensure cost efficiency and quality control, are bolstering the growth of the sauces, dressings, and condiments market[1]Source: Federal Register, "Proposal To Revoke 23 Standards of Identity for Foods", federalregister.gov. Furthermore, the increasing influence of international cuisines and the rising popularity of fusion flavors are creating new opportunities for market players to innovate and expand their product portfolios.

Key Report Takeaways

- By product type, sauces captured 49.25% of the sauces, dressings, and condiments market share in 2025, while dressings are forecast to post a 6.61% CAGR to 2031.

- By category, conventional offerings dominated with 82.10% revenue share in 2025; organic/clean-label alternatives are projected to climb at a 6.05% CAGR between 2026-2031.

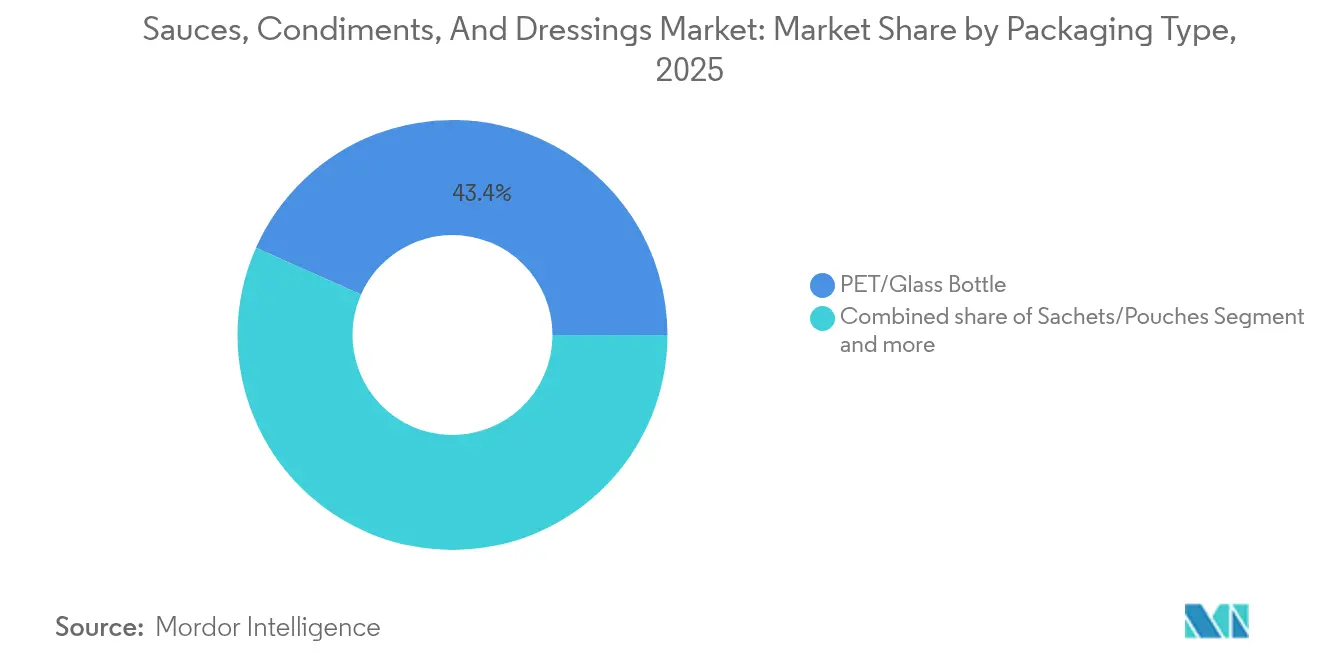

- By packaging format, PET/glass bottles accounted for 43.35% of 2025 sales, whereas sachets and pouches are expected to grow at a 5.86% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets controlled 58.75% of 2025 turnover, yet online retail is primed for the fastest expansion with a 6.71% CAGR over the forecast period.

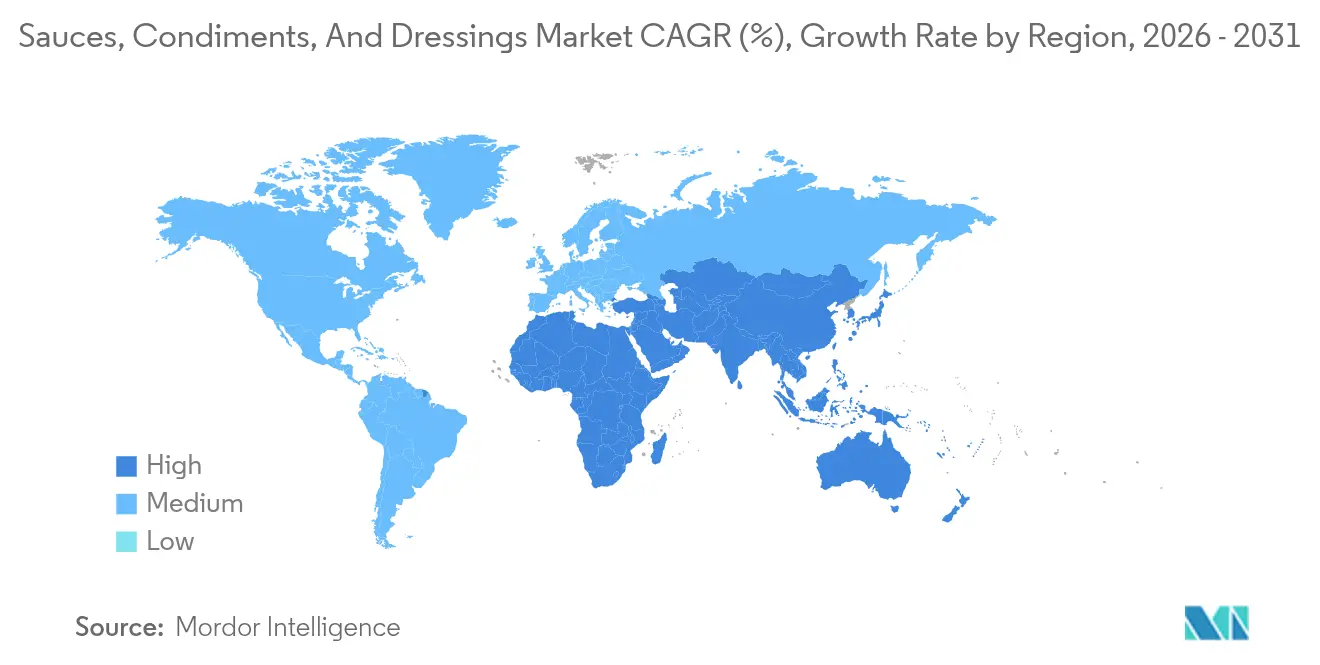

- By region, Asia-Pacific held 41.20% share in 2025; the Middle East and Africa region is projected to register the highest 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sauces, Condiments, And Dressings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product innovation and flavor diversification | +1.2% | Global (focus on North America and Asia-Pacific) | Medium term (2-4 years) |

| Rising popularity of ethnic and regional cuisines | +1.0% | Global (strongest in North America and Europe) | Long term (≥ 4 years) |

| Premium-priced clean-label formulations | +0.9% | North America and EU; rising in Asia-Pacific | Medium term (2-4 years) |

| Influence of food culture and social media | +0.8% | Global youth cohorts | Short term (≤ 2 years) |

| Rising home cooking and hybrid meal occasions | +0.7% | Developed markets worldwide | Medium term (2-4 years) |

| Fortification of condiments with functional ingredients | +0.6% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Innovation and Flavor Diversification

In a 2024 study published in Frontiers in Nutrition, researchers highlighted a breakthrough: brands can now reduce sodium in ketchup by up to 52% without compromising taste. This innovation is made possible through advanced encapsulation technologies, which ensure flavor retention while meeting health-focused reformulation goals. Multinational companies are leveraging these micro-delivery systems, integrating them with rapid prototyping kitchens. This integration enables pilot recipes to transition from concept to store shelves in under nine months, significantly accelerating product development timelines. With the FDA set to introduce new criteria for the "healthy" label in February 2028, there's a heightened push for nutrient-dense reformulations. These criteria are particularly impactful as condiments will no longer assist main dishes in qualifying for this label, prompting manufacturers to innovate independently. Consequently, flavor houses and branded manufacturers are collaborating to craft bolder and more diverse flavor profiles, such as gochujang barbecue, fermented yuzu aioli, and chipotle-lime crema. These flavors cater to both adventurous consumer palates and regulatory sodium limits, striking a balance between taste and compliance. Thus, the sauces, dressings, and condiments market is increasingly valuing research and development agility. Companies are also focusing on cross-regional flavor translation to meet the growing demand for globally inspired tastes, ensuring their products resonate with diverse consumer preferences while adhering to evolving regulatory standards.

Rising popularity of ethnic and regional cuisines

USDA data reveals that American households are increasingly embracing global spices, suggesting a trend where shoppers are recreating restaurant dishes at home. This shift reflects a growing consumer interest in diverse culinary experiences and a willingness to experiment with flavors beyond traditional American cuisine[2]Source: United States Department of Agriculture," Patterns of Global Food Consumption Expected to Shift in Next Quarter Century as Population, Incomes Rise", ers.usda.gov. Heritage products, once confined to local wet markets, are now making their way to mainstream grocery shelves. This shift, seen with items like Sichuan doubanjiang and Mexican mole negro, underscores a growing acceptance of international ingredients. In response, major players like Unilever are rolling out region-specific products, such as a guasacaca-inspired mayo tailored for South American consumers, to cater to this evolving demand. Meanwhile, smaller craft brands are carving out shelf space, aided by distributors who prioritize authentic narratives that resonate with consumers seeking genuine cultural connections. Authenticity, rooted in origin and traditional processing, has led to a surge in popularity for sauces, dressings, and condiments. The emphasis on native fermentation methods and single-estate pepper varietals has further enhanced the appeal of these products, particularly among flavor explorers who value unique and high-quality ingredients.

Premium-priced clean-label formulations

Consumers are increasingly willing to pay a premium for recognizable ingredients, leading to a surge in organic food demand. This trend highlights a growing preference for transparency and natural products in the food industry. In a related move, the European Commission, after conducting genotoxicity reviews, has started phasing out eight smoke flavorings[3]Source: European Commission,"Member States endorse withdrawal of smoke flavourings from EU market", ec.europa.eu. This regulatory action sets a significant precedent, encouraging many manufacturers to proactively reformulate their products to meet evolving safety standards. In response, condiment manufacturers are making strategic investments to align with these changes. These investments include establishing vertically integrated herb gardens to ensure a consistent supply of fresh ingredients, securing cage-free egg contracts to meet ethical and quality standards, and developing natural preservative blends to replace artificial additives. Furthermore, supply-chain transparency apps are playing a crucial role in enhancing premium positioning. These apps allow consumers to access detailed information about product origins by scanning farm-level QR codes displayed on bottle labels, fostering trust and brand loyalty. Collectively, these trends are not only expanding the value pool in the sauces, dressings, and condiments market but also tightening the industry's tolerance for artificial additives, signaling a shift toward more sustainable and consumer-focused practices.

Influence of food culture and social media

In just weeks, short-form recipe videos can ignite nationwide condiment crazes, as seen with the viral "pink sauce" sensation of 2024. This rapid pace shortens the go-to-market timelines for established players, while giving agile newcomers a significant spotlight. Hashtag analytics from major platforms reveal that in Q1 2025, the top 100 posts related to condiments amassed a staggering 2.4 billion views, highlighting the immense reach and influence of digital content in shaping consumer preferences. With such swift trend cycles, brands face heightened reputational risks for any missteps, as negative feedback can spread just as quickly as positive trends. In response, they've turned to real-time social listening tools to monitor consumer sentiment and micro-batch pilot releases to test new products in smaller, controlled environments. This immediacy not only influences product flavors but also redefines packaging designs, serving styles, and even marketing strategies. Brands are increasingly aligning their offerings with digital-first consumer rituals, focusing on visually appealing aesthetics, innovative formats, and convenience-driven solutions to capture attention in a highly competitive market. The sauces, dressings, and condiments market is evolving rapidly to meet these demands, ensuring relevance in an era where trends can shift overnight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar/salt and preservative concerns | –0.8% | Global (strictest in EU and North America) | Short term (≤ 2 years) |

| Volatile tomato/chili commodity prices | –0.6% | Global; acute in processing hubs | Medium term (2-4 years) |

| Regional labeling-compliance costs for exporters | –0.4% | EU-U.S.-China corridors | Long term (≥ 4 years) |

| Consumer skepticism toward additives | –0.5% | Developed markets, expanding worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High sugar/salt and preservative concerns

With the FDA setting a January 1, 2028 deadline for updated nutrition labels, global brands are being compelled to simultaneously adjust sodium and sugar levels across their entire portfolios. This regulatory shift aims to promote healthier consumer choices, but it presents significant challenges for manufacturers. Given that sauces and dressings can't help main dishes meet "healthy" standards, companies are tasked with revamping these products independently, requiring substantial reformulation efforts. As traditional preservatives come under scrutiny, challenges arise in preserving taste and ensuring product safety. Notably, benzoates and parabens, which were once widely used, have made their way onto several retailer avoidance lists due to growing consumer and regulatory concerns. To address these issues, manufacturers are increasingly relying on proprietary salt-taste enhancers and natural antimicrobial systems. However, these advanced ingredients come at a premium, increasing production costs and potentially altering established flavor profiles, which could impact brand loyalty. For smaller players in the sauces, dressings, and condiments market, these challenges are even more pronounced. Limited resources and tighter budgets restrict their ability to experiment with new formulations, making it harder to compete with larger companies that can absorb higher costs and invest in innovative solutions. As a result, the market dynamics are likely to shift, favoring well-resourced brands that can adapt to these regulatory and consumer-driven changes.

Volatile tomato/chili commodity prices

In 2024, California's processing tomato output fell by 12% due to extreme weather, while El Niño conditions wreaked havoc on Peruvian aji amarillo crops, significantly disrupting global supply chains and raw material availability. Despite improved global stock-to-use ratios, the World Bank has flagged ongoing volatility, emphasizing the challenges manufacturers face in managing costs and ensuring consistent supply. Manufacturers without futures hedging are particularly vulnerable, as they absorb immediate price spikes, which either erode profit margins or necessitate recipe re-specifications that could impact product quality and consumer satisfaction. To counteract these challenges, some manufacturers have diversified into alternative ingredients, such as carrot-based ketchup analogs or dehydrated pepper pastes. However, these substitutions carry the risk of consumer rejection, as changes in flavor, texture, or overall product experience may not align with consumer expectations. If the raw material squeeze persists, it could significantly temper the mid-term growth trajectory of the sauces, dressings, and condiments market, potentially leading to reduced innovation, higher prices, and constrained profitability for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Versatile Sauces Keep the Lead

In 2025, sauces raked in a retail value of USD 89.36 billion, commanding a robust 49.25% share of the global market for sauces, dressings, and condiments. They dominate the market, finding versatile applications in everything from meal kits and marinades to all-day dips. The rise of artisanal chili pastes and fermented soybean blends has propelled sauces into premium retail spaces, catering to consumers with a palate for authentic and bold flavors. Brand innovation shines through, with packaging like squeeze pouches for wok sauces and family-size jars for gravie,s enhancing convenience and relevance. This segment's allure extends into adjacent categories, notably ready-to-eat meals and snacks, broadening consumption avenues. While dressings and other condiments vie for attention, sauces firmly anchor the market, adeptly evolving with culinary trends while maintaining their essential role in homes and foodservice kitchens.

Dressings are emerging as the fastest-growing segment in the sauces, dressings, and condiments arena, projected to achieve a CAGR of 6.61% by 2031. Their ascent is driven by health-centric reformulations, such as reduced-oil emulsions and fermented bases, resonating with calorie-conscious consumers. Innovations like Greek yogurt and avocado oil dressings offer nutrient-rich profiles without sacrificing flavor. Enhanced packaging, like pour-over bottles with spice infusers, boosts at-home customization, allowing dressings to rival sauces. Dressings now complement a broader meal spectrum—from salads and grain bowls to sandwiches—expanding their usage. As brands delve into hybrid products merging features of both dressings and sauces, the lines blur. Yet, with a robust health-focused innovation pipeline, the dressings category is poised for sustained growth through the decade's close.

By Category: Clean-Label Ascends Under Cost Guardrails

In 2025, conventional recipes dominated the global sauces, dressings, and condiments market, commanding an impressive 82.10% share. Budget-conscious shoppers, particularly in price-sensitive regions, gravitate towards these value-driven brands, solidifying their market leadership. Yet, an inflation-adjusted basket analysis indicates a notable resilience in premium conventional condiments, with consumers showing a reluctance to downgrade to lesser alternatives. Retail channels prominently feature conventional products, occupying the lion's share of shelf space. While health trends usher in competition from cleaner formulations, many conventional brands are making subtle reformulations, such as reducing sodium or substituting synthetic emulsifiers with plant-based fibers to bridge the perception gap. These strategic moves not only safeguard their market share but also enhance their competitiveness against claims typically associated with clean-label brands.

Clean-label sauces, dressings, and condiments are on an upward trajectory, expanding at an estimated CAGR of 6.05%, making them the market's fastest-growing segment. This surge is fueled by a growing consumer appetite for transparency, with purchasing choices swayed by familiar ingredients and certifications like USDA Organic, EU Leaf, and Non-GMO Project Verified. In response, retailers are curating dedicated “natural” sections, placing no-additive ketchups alongside gluten-free soy sauces to promote cross-category exploration. Despite facing challenges, such as a 4% dip in organic tomato acreage in 2024, brands are innovating. They're blending certified-organic bases with conventionally grown spices, marketing them as “better-for-you” alternatives. This adaptability not only navigates supply constraints but also resonates with quality-conscious consumers. As conventional products gradually embrace clean-label traits, the emphasis on ingredient purity may wane, shifting the competitive focus towards branding, narrative, and pricing strategies.

By Packaging: Flexible Formats Accelerate Portion Control

In 2025, PET and glass bottles together accounted for 43.35% of the retail volume in the sauces, dressings, and condiments market, reinforcing their status as the leading packaging formats. PET bottles dominate high-volume categories like ketchup, where their squeeze-friendly design aids in portion accuracy, a crucial feature for calorie-conscious consumers. Conversely, glass bottles epitomize premium positioning, especially for heritage pasta sauces and fermented chili oils, where visual clarity and product appeal are paramount. This synergy enables the segment to cater to both mass-market demands and premium brand narratives, broadening its consumer reach. While carton-based formats are making inroads in specialty niches like broths and ready-to-serve gravies, they remain a minor player, ensuring PET and glass retain their pivotal roles in retail. Their established infrastructure, shelf recognition, and adaptability bolster their resilience against emerging formats.

Sachets and pouches are emerging as the fastest-growing packaging segment in the sauces, dressings, and condiments market, boasting a projected CAGR of 5.86%. Their growth is fueled by the surge in on-the-go consumption and the advantage of reduced plastic mass per serving compared to rigid formats. Brand owners emphasize that pouches boast up to a 60% lower carbon footprint than glass, aligning with stringent EU recyclability mandates and overarching sustainability objectives. Quick service restaurants (QSRs) are leading the charge, transitioning to laminated film sticks that optimize storage and boost operational efficiency. Flexible packaging not only offers branding versatility but also sees suppliers delving into paper-based barrier coatings and mono-material laminates to enhance recyclability. This blend of environmental advantages, consumer convenience, and adaptability to shifting regulations positions sachets and pouches as the dominant growth driver in the category through the decade's close.

By Distribution Channel: Online Retail Outpaces Brick-and-Mortar

In 2025, supermarkets and hypermarkets captured 58.75% of the market share in sauces, dressings, and condiments, solidifying their role as the leading sales channel. Their dominance stems from heightened product visibility, a diverse range of offerings, and the capability to stimulate impulse buys via sampling kiosks and live cooking demos. Such hands-on experiences promote the exploration of new flavors and formats, a feat challenging to achieve online. Ample shelf space accommodates various brands and packaging, catering to both premium and budget-conscious consumers. Moreover, physical stores offer the advantage of instant product access, free from shipping delays or costs. This blend of sensory interaction, diverse choices, and immediate satisfaction cements the position of supermarkets and hypermarkets as the cornerstone retail channel in this category, even as online platforms rise in prominence.

E-commerce is rapidly emerging as the leading distribution channel for sauces, dressings, and condiments, boasting a robust CAGR of 6.71%. This surge is fueled by subscription bundles, same-day delivery, and AI-driven flavor suggestions that tailor the shopping journey. Habits formed during the pandemic, like bulk digital purchases, have solidified. Marketplaces leverage algorithmic cross-selling, such as pairing sriracha with sushi rice kits, to boost average basket values. Direct-to-consumer platforms stand out with their storytelling approach and exclusive product drops, fostering brand loyalty. Yet, challenges loom with high last-mile delivery expenses, underscoring the importance of click-and-collect and hybrid models for expansion. Moving forward, the interplay of shipping costs, retailer data-sharing benefits, and shifting consumer preferences will shape the pace at which e-commerce captures more market share from traditional retail.

Geography Analysis

In 2025, Asia-Pacific commanded a dominant 41.20% share of the global market, with urban hubs seamlessly blending street-food traditions and contemporary safety measures. China's February 2025 introduction of unified additive limits, GB 2760-2024, is set to expedite export approvals for its chili bean pastes and soy-based dips. Meanwhile, Japan and South Korea are charting premium paths, leveraging cold-chain logistics to safeguard their kimchi and low-acid dressings. In contrast, India and Indonesia are focusing on volume, with mid-tier brands expanding their reach through cash-and-carry wholesalers and dark-store aggregators. The region's flavor fusion is evident, as Korean gochujang finds its way atop Thai rice bowls, boosting cross-border demand for these blended condiments.

Though the Middle East and Africa currently holds a modest mid-single-digit market share, it's on track to achieve the fastest growth rate of 7.09% CAGR from 2026 to 2031. The UAE boasts a robust USD 7.63 billion food-processing sector, adeptly repackaging imported tomato paste for local brands. In alignment with its Vision 2030, Saudi Arabia is backing its domestic sauce factories, aiming to curtail import dependencies and champion halal-certified products. South Africa's burgeoning quick-service chicken outlets are fueling a surge in peri-peri sauce consumption, while Nigeria's digital grocery platforms cater to the urban youth with convenient portion pouches. Free-trade zones in Jebel Ali and Tanger-Med are streamlining re-export processes, broadening the market's regional reach.

North America and Europe, while established, continue to be lucrative markets. Here, a focus on premiumization and regulatory-compliant reformulations is driving modest value growth rates in the low single digits. With a synchronized FDA label deadline set for January 2028, U.S. brands are proactively revamping recipes, aligning national updates with trends like shrinkflation and healthier perceptions. Europe is pushing for packaging circularity, driven by the PPWR initiative, leading to significant investments in innovations like tethered caps and monomaterial pouches, emphasizing differentiation beyond mere taste. South America's growth, spearheaded by Mexico and Brazil, is buoyed by local chili farming and craft-beer pairings, witnessing a rebound in expansion as GDPs rise. Furthermore, the bloc's harmonized Mercosur additive codes, set to take effect in late 2026, promise to simplify formulary designs, facilitating smoother cross-border innovations.

Regulatory Landscape

Regulation affecting sauces, condiments, and dressings is tightening around additives, contaminants, labeling, and packaging materials, while also moving toward harmonized limits that ease cross-border formulation. In the European Union, Regulation (EU) 2026/196 updated specifications for several commonly used texturizers and stabilizers (including guar gum, xanthan gum, and pectins), with transitional stock exhaustion ending on 18 August 2026. That timeline is likely to require manufacturers to re-check additive specifications and supplier documentation. In parallel, EU food-contact compliance continued to evolve in 2026 via updates to plastic food-contact material rules (Regulation (EU) 2026/245), raising the bar for bottle, cap, and liner materials used across ketchup, mayonnaise, and dressing formats.

Global and US frameworks also shape trade and operational systems. In July 2026, the Codex Alimentarius Commission adopted new and updated standards relevant to spice inputs, including maximum levels for lead in spices and culinary herbs, which can translate into tighter raw-material testing for spice-forward sauces and seasoning pastes. In the United States, the FDA kept the Food Traceability Rule compliance date of 20 July 2028 for covered foods. FY2026 appropriations language limited FDA enforcement spending before that date, which leaves brands and co-manufacturers building digital traceability capability ahead of the enforcement window.

Value Chain Analysis

The value chain for sauces, condiments, and dressings runs from agricultural and fermentation inputs (tomatoes, chilies, soy, herbs and spices, edible oils, eggs, sugar, and salt) through ingredient processing (purees, concentrates, oils, vinegar, emulsifiers, and hydrocolloids), and manufacturing (blending, emulsification, thermal processing such as hot-fill and aseptic, and fermentation where relevant). Packaging conversion covers PET and glass bottles, caps, pouches and sachets, and labels, followed by distribution across retail and foodservice. Large brand owners and co-manufacturers manage formulation, quality systems, and scale production, while flavor houses and specialty ingredient suppliers increasingly support rapid prototyping for clean-label and reduced-sodium and reduced-sugar recipes. Downstream, supermarkets and hypermarkets remain the dominant volume gatekeepers, while online retail and DTC mechanics amplify discovery through bundles and limited drops.

Pressure points in this category are concentrated upstream in commodity exposure and midstream in packaging and compliance. The report context highlights raw-material volatility, particularly for tomato and chili, alongside rising scrutiny of additives and preservatives. Together, these dynamics increase the importance of diversified sourcing, vertically integrated ingredient programs, and supplier qualification backed by documentation. Packaging is another constraint, as EU circularity and food-contact updates require tighter material selection and testing across closures and flexible formats, which elevates the role of converters and resin and film suppliers for brands scaling sachets and pouches.

Competitive Landscape

The global sauces, dressings, and condiments market exhibits moderate concentration, indicating balanced competition between established multinational corporations and emerging regional players that leverage authentic positioning and specialized distribution strategies. In 2024, the pace of consolidation quickened: Campbell Soup merged with Sovos Brands, amplifying Rao’s distribution and bolstering its premium pasta sauce platform. This strategic move allowed Campbell Soup to strengthen its foothold in the premium segment, catering to evolving consumer preferences for high-quality, authentic products. McCormick initiated discussions to acquire Sauer Brands for over USD 1 billion, underscoring its ambition to enhance its retail spice and hot sauce portfolio, which aligns with the growing demand for bold and diverse flavors. Meanwhile, Kraft Heinz, reaping USD 1.9 billion in operating cash flow for H1 2025 through operational efficiencies, is channeling these funds into digital shelf diagnostics and fully recyclable ketchup caps, reflecting its commitment to sustainability and innovation in packaging.

Regional players like Foshan Haitian from China and Mexico’s Herdez harness cultural authenticity to solidify their domestic market share while selectively venturing into exports. Foshan Haitian leverages its deep-rooted understanding of local tastes to maintain dominance in China, while Herdez capitalizes on Mexico’s rich culinary heritage to expand its footprint in international markets. Start-ups offering functional-fortified products like turmeric-infused ghee spreads and prebiotic miso dressings are drawing venture capital interest by marrying wellness themes with culinary artistry. These innovative products cater to health-conscious consumers seeking functional benefits alongside flavor, driving growth in this niche segment.

Investments in technology are leaning towards AI-driven demand forecasting, predictive maintenance for continuous pasteurizers, and blockchain for tracking tomato origins, all aimed at minimizing recall risks and streamlining compliance. These advancements not only enhance operational efficiency but also build consumer trust by ensuring transparency and traceability across the supply chain. Success in the sauces, dressings, and condiments sector will increasingly rely on research and development pipelines attuned to regulatory demands and robust omnichannel marketing, rather than solely on production capacity.

Sauces, Condiments, And Dressings Industry Leaders

-

McCormick & Company Inc.

-

The Kraft Heinz Company

-

Unilever PLC

-

Kikkoman Corporation

-

Mizkan Holdings Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Manufacturing automation and higher-throughput processing open room for both multinational brand owners and regional co-manufacturers to improve consistency, reduce changeover time, and support faster flavor rotation across sauces and dressings. The 2026 context shows capital and capability moving into scalable processing: The Campbell Company completed an 88,000-sq.-ft. aseptic manufacturing expansion at its Maxton, North Carolina facility. The expansion added new aseptic processing lines and supporting infrastructure, supporting higher-volume production needs as brands continue to broaden sauce and dressing formats.

Opportunities also cluster around reformulation, traceability readiness, and ingredient-system upgrades that protect taste while meeting tightening additive and contaminant requirements. The EU additive specification update (Regulation (EU) 2026/196) and Codex actions on heavy-metal maximum levels for spices raise the value of validated spice supply, stronger incoming QA, and documented clean-label stabilizer systems for emulsified dressings and premium sauces. Separately, the market evidence points to measurable gains from data-driven production approaches: AI-enabled autonomous manufacturing applied to a major sauce line in South Korea supports practical deployment of data-driven process control. That improves throughput and cost positions while supporting the faster innovation cycles tied to online discovery and limited-time launches.

Recent Industry Developments

- May 2026: The Kraft Heinz Company launched The United Tastes of America campaign with America250-branded, limited-time items across core lines such as Heinz Ketchup and Mustard. The activation refreshed visibility for staple condiments at shelf and in digital channels while using limited editions to stimulate trial without changing the long-run core assortment.

- March 2026: McCormick & Company Inc. and Unilever PLC announced a definitive agreement to combine McCormick with Unilever's Foods business (excluding India). The planned combination brings large-scale condiments, cooking aids, and flavor platforms under one umbrella, intensifying portfolio breadth and procurement leverage across sauces and seasonings.

- August 2024: Bachan's introduced Japanese Dipping Sauce in original and sweet-and-spicy variants, highlighting premium ingredients such as stone-ground sesame and white miso. The launch reinforced momentum for authentic, restaurant-inspired flavors migrating into mainstream retail condiment sets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of sauces, condiments, and dressings sold through retail and foodservice, counted at the point they are sold as packaged or prepared products for meal preparation or direct consumption.

Scope exclusions: We exclude fresh, unbranded homemade preparations and in-store prepared foods that are not sold as a distinct sauce, condiment, or dressing product.

Segmentation Overview

-

By Product Type

-

Sauces

- Condiment Sauces

- Cooking Sauces

- Herbs and Spices

- Dips

- Dressings

- Other Product Types

-

Sauces

-

By Category

- Conventional

- Organic/Clean-label

-

by Packaging

- PET/Glass Bottles

- Sachets/Pouches

- Others (Tetra packs, Jars, Cups, and others)

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context and the category boundaries for sauces, condiments, and dressings, then tying them to measurable signals that can be refreshed each year. We lean on public sources such as USDA and other national agriculture and food statistics, UN Comtrade trade flows for relevant food preparations, FAO food balance style indicators, and food safety and labeling references from regulators such as the FDA and EFSA.

To keep the model usable for a global report, company annual reports, investor decks, and earnings call notes are reviewed to understand category mixes, regional exposure, and pricing commentary. Reputed press and association websites are used to cross-check events like private label growth, packaging changes, and regulation-driven reformulation. Where needed, we also use paid subscriptions for company financials and intelligence, news and financials, import and export shipment-level checks, and patent activity scanning to validate innovation intensity. These examples are illustrative, and many other sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test category boundaries for sauces, condiments, and dressings and to confirm how volumes and prices behave across retail and foodservice. We spoke with a mix of manufacturers, ingredient and packaging participants, distributors, and large buying teams across APAC, EMEA, and the Americas so assumptions from desk work could be corrected where they did not match on-the-ground realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 16% | Managers: 48% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where food consumption and trade indicators help reconstruct the addressable pool, which is then adjusted using category penetration and spend behavior for sauces, condiments, and dressings. To keep it realistic, the totals are corroborated with selective bottom-up approximations like sampled brand and private label price points, typical pack sizes, and channel mix checks, and then the model is tuned when the two views do not line up.

Inputs that tend to matter most include household and away-from-home consumption trends, import and export movement for relevant prepared food categories, raw material and packaging cost direction that influences shelf pricing, the pace of premiumization and clean label switching, and the retail versus foodservice split (since pack formats and pricing differ). Forecasts are run using scenario analysis supported by expert views on pricing cycles, private label share movement, and regional demand resilience, and then translated into a single base case for the report. When bottom-up data is missing in smaller countries, gaps are handled using proxy indicators like comparable cuisine adoption, urbanization, and retail modern trade share, followed by a reasonableness check against trade flows.

Data Validation & Update Cycle

Outputs are checked against multiple independent signals for the sauces, condiments, and dressings category, and then the biggest variances are investigated before the numbers are finalized. If a country or product group shows an unusual jump, the drivers are re-tested and interview follow-ups are triggered so the assumption is not carried forward by mistake.

A multi-step analyst review is used so category scope, currency treatment, and price-volume logic are consistent across regions. The report is refreshed annually, and interim updates are made when a material event changes pricing, regulations, or channel structure. Before delivery, a final review pass is completed so clients receive the most current view available at the time of publication.

Mordor Intelligence's Sauces Condiments and Dressing Market Size Compared Against Other Published Estimates

It is common to see different market sizes for this category, even when the report titles look similar, because the boundaries and timing behind the numbers are not always the same. Differences usually come from what is counted inside the category, which year is treated as the anchor, and how pricing is carried forward in the forecast.

By tracking channel mix, pack-level pricing logic, and trade-linked supply signals, Mordor Intelligence keeps the estimate focused on packaged sauces, condiments, and dressings, rather than folding in adjacent prepared foods or broad seasonings that inflate totals in some publications.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 191.68 B (2026) | |

| Global Consultancy A | USD 165.81 B (2023) | Uses a different base year and starts the forecast window earlier, and the category cut can be narrower on what qualifies as sauces, dressings, and condiments, which lowers the reported total versus a later-year read. |

| Industry Research Group B | USD 173.43 B (2024) | Anchors the valuation in 2024 and applies a separate forecast window, and it can treat revenue coverage differently by mixing value and volume views, which changes how pricing progression is reflected in the market total. |

Looking across the three estimates, the spread is largely explained by base-year choice and category inclusions, followed by how price and channel mix are carried into the forward years. Using transparent inputs that can be checked each year helps keep the market size traceable to repeatable steps, which makes planning and benchmarking easier for decision-makers.

Key Questions Answered in the Report

What is the projected value of the global sauces, dressings, and condiments market by 2031?

The sector is forecast to hit USD 252.33 billion by 2031, expanding at a 5.65% CAGR.

Which product type currently holds the largest share?

Sauces, with 49.25% revenue share in 2025.

Why are sachets and pouches growing faster than bottles?

They align with portion control, lower plastic mass, and EU recyclability mandates, driving a 5.86% CAGR.

Which region is expected to see the fastest growth through 2031?

The Middle East & Africa, projected at a 7.09% CAGR thanks to processing investments and trade-hub logistics.

How will new FDA labeling rules affect manufacturers?

All brands must simultaneously reformulate for sodium and sugar limits by January 2028, increasing R&D and packaging costs.

What years does this Sauces, Condiments, And Dressings Market cover, and what was the market size in 2025?

In 2025, the Sauces, Condiments, And Dressings Market size was estimated at USD 191.68 billion. The report covers the Sauces, Condiments, And Dressings Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Sauces, Condiments, And Dressings Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: