Pasta Sauce Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

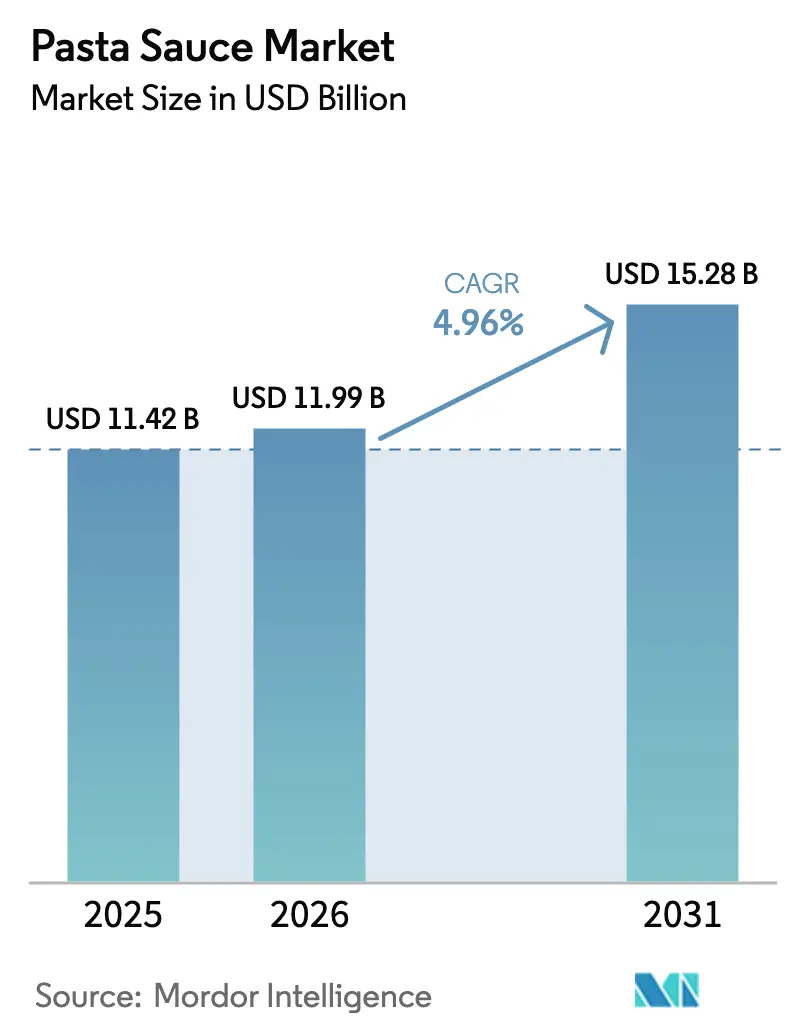

| Market Size (2026) | USD 11.99 Billion |

| Market Size (2031) | USD 15.28 Billion |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

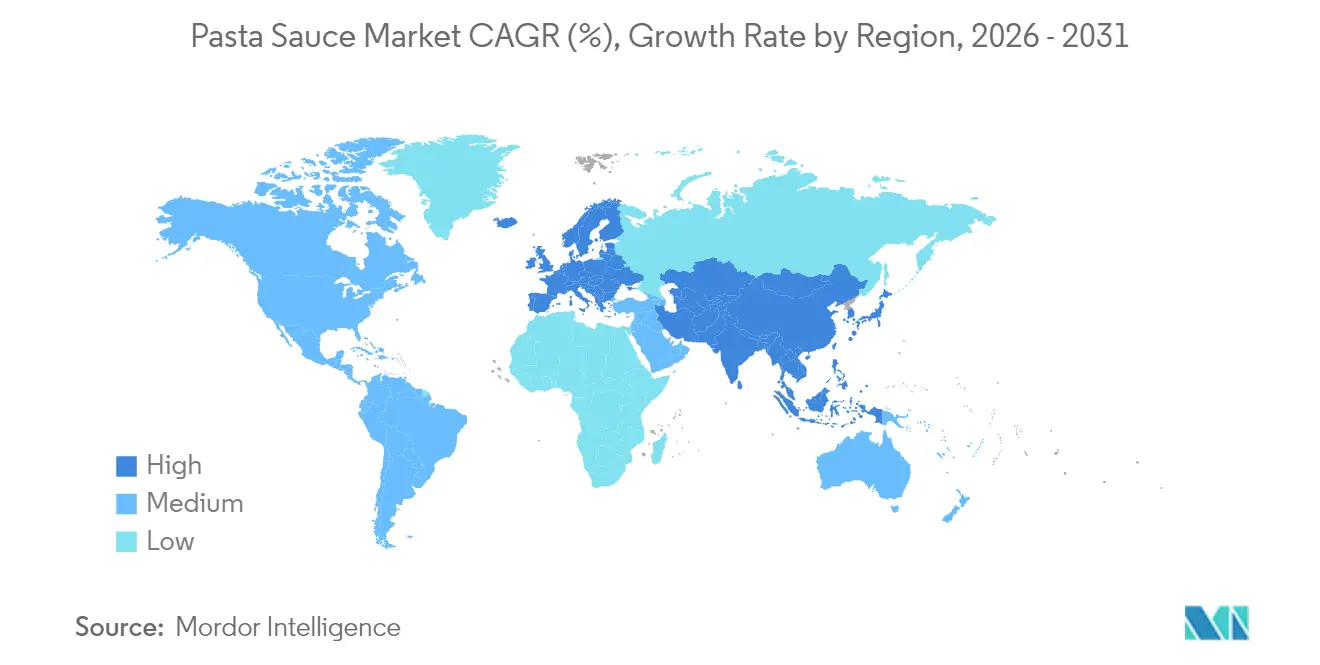

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

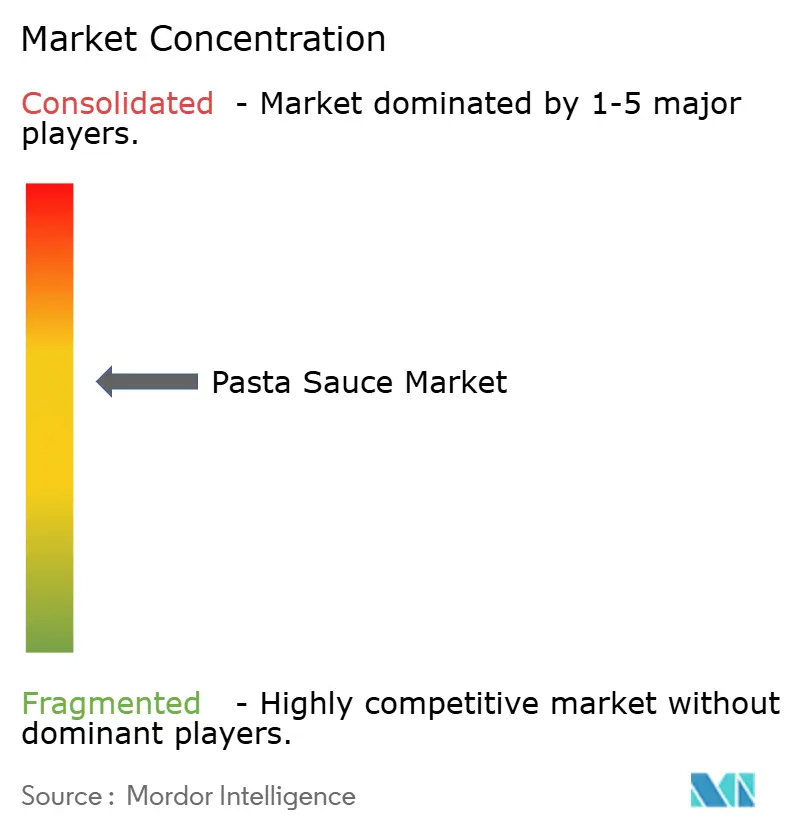

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pasta Sauce Market Analysis by Mordor Intelligence

pasta sauce market size in 2026 is estimated at USD 11.99 billion, growing from 2025 value of USD 11.42 billion with 2031 projections showing USD 15.28 billion, growing at 4.96% CAGR over 2026-2031. Consumer demand for convenient, high-quality meal solutions is driving the steady expansion of the global pasta sauce market, blending tradition with innovation. As home cooking gains popularity, there's a notable uptick in ready-to-use sauces that promise both authenticity and convenience. This trend is exemplified by Kraft Heinz's expansion of its Classico line to include plant-based variants. Europe, with its deep-rooted Italian culinary traditions, leads the market. Meanwhile, the Asia-Pacific region is rapidly embracing Western flavors, highlighted by Barilla's entry into India with offerings tailored to local tastes. While tomato-based sauces continue to dominate store shelves, there's a noticeable rise in creamy and cheese-based options. This shift mirrors the premiumization trend, with Rao's Alfredo and truffle-infused lines gaining popularity in the U.S. Health-conscious consumers are increasingly seeking organic and "free-from" products. A prime example is Whole Foods' 365 sauces, which boast no added sugar. Packaging is also transforming; brands like Prego are swapping out glass jars for flexible pouches, a move that aligns with broader sustainability goals. The introduction of new flavor formats, such as Sauz's Miso Garlic Marinara, underscores the influence of fusion trends on product offerings. In summary, the pasta sauce category is witnessing a dynamic evolution, driven by innovation, regional expansion, and shifting consumer values.

Key Report Takeaways

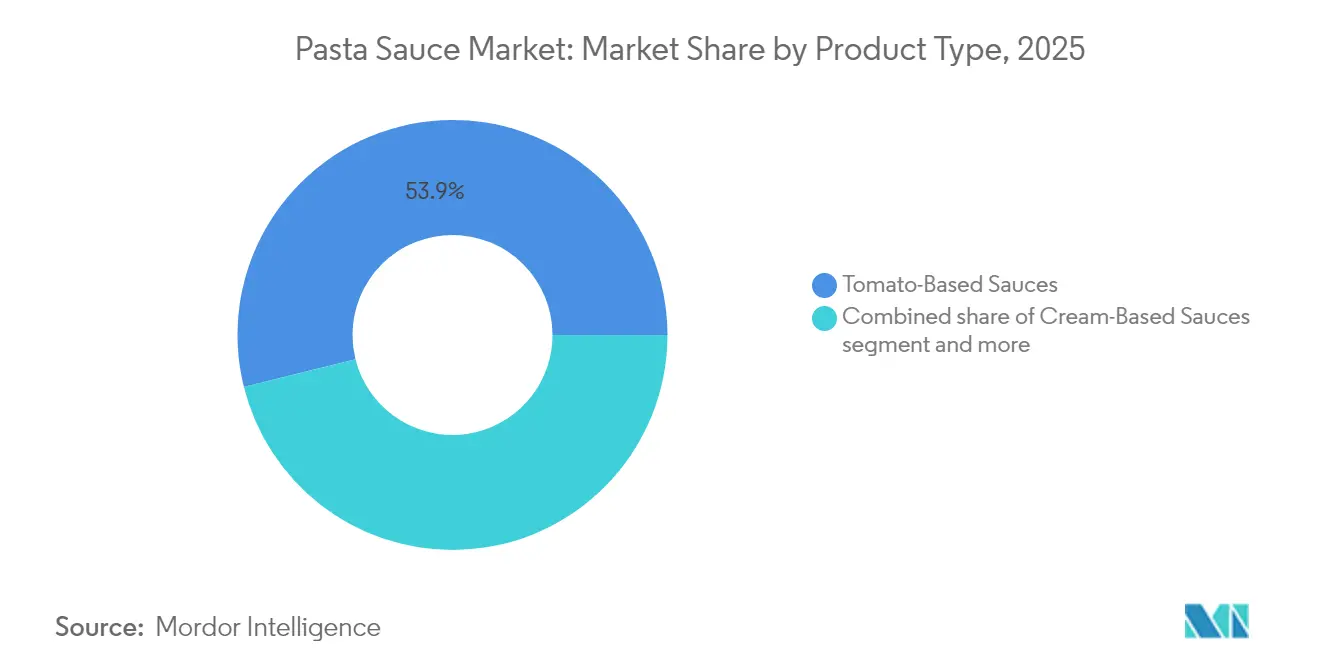

- By product type, tomato-based sauces held a 53.89% pasta sauce market share in 2025, while cream-based sauces are forecast to grow at a 7.01% CAGR to 2031.

- By packaging, glass jars retained 38.05% of the pasta sauce market size in 2025, whereas flexible pouches are expected to expand at a 6.51% CAGR through 2031.

- By distribution channel, retail commanded 71.88% of the pasta sauce market size in 2025, yet HoReCa channels are projected to record an 7.92% CAGR to 2031.

- By category, conventional products led with 80.75% revenue share in 2025; free-form alternatives are advancing at a 8.74% CAGR to 2031.

- By geography, Europe contributed a 38.10% pasta sauce market share in 2025, while Asia-Pacific is set to emerge as the fastest-growing region at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pasta Sauce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for convenient ready-to-cook options | +1.2% | Global, strongest in North America and urban Asia-Pacific | Medium term (2-4 years) |

| Rising global appetite for Italian cuisine | +0.9% | Global, notable in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Growth in the number of pasta foodservice outlets worldwide | +0.8% | Urban centers across developed markets | Medium term (2-4 years) |

| The shift toward clean-label ingredients in sauces | +0.7% | North America and Western Europe | Long term (≥ 4 years) |

| Innovation in packaging solutions for modern consumers | +0.6% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Artisanal and fusion pizza sauces see surge in demand | +0.5% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Convenient Ready-to-Cook Options

Modern consumers, prioritizing speed and simplicity in meal preparation, are driving the surge in the pasta sauce market, especially with their growing preference for convenient ready-to-cook options. The United Nations reported that in 2024, over 57% of the global population lived in urban areas, with projections suggesting this figure will exceed 60% by 2030 [1]Source: United Nations, “World Urbanization Prospects 2024,” un.org. This urban trend is intensifying the demand for quick culinary solutions. The International Food Information Council highlighted a generational shift in food habits, noting that 64% of younger consumers now favor quick meal options over traditional cooking [2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org . Responding to this trend, Nestlé introduced its new Maggi pasta sauces in ready-to-use formats across Southeast Asia, specifically targeting urban households. Del Monte India expanded its “Italian Kitchen” line, offering pre-cooked pasta paired with complementary sauces, allowing for meals in under 10 minutes. Rapid grocery platforms, including Swiggy Instamart and Zepto, have seen a spike in demand for shelf-stable pasta sauces, particularly among single-person households in metropolitan areas. Major brands, like Barilla, have rolled out new ready-to-cook sauce jars designed for quick heating and minimal prep. These trends underscore the impact of urbanization and shifting consumer behaviors on the pasta sauce market, driving product innovation and expanding market reach.

Rising Global Appetite for Italian Cuisine

As global enthusiasm for Italian cuisine surges, the pasta sauce market is reaping the benefits. Consumers are increasingly seeking authentic dining experiences at home, driving a wave of product launches that introduce regional Italian flavors to mainstream retail. In 2024, UK-based brand Sugo Tu rolled out its handcrafted pasta sauces, drawing inspiration from specific Italian regions like Sicilian cherry tomato and Calabrian chili, catering to the authenticity-seeking palate. Over in Japan, Nissin Foods debuted a premium line of Italian-style pasta sauces under its “La Cucina” label, aiming at urbanites with a taste for Western gourmet meals. Retail giants like Marks & Spencer have expanded their Italian repertoire, introducing rustic-style sauces such as tomato and mascarpone, tapping into the growing demand for restaurant-quality dining at home. In the Middle East, Spinney’s supermarkets are amplifying their imports of artisanal Italian pasta sauces, underscoring a wider cross-border enthusiasm. This global culinary shift transcends mere flavor; it's a lifestyle statement. Consumers now equate Italian cuisine with indulgence, comfort, and social dining, solidifying pasta sauces as a modern kitchen staple in today's internationally influenced homes.

Artisanal and Fusion Pizza Sauces See Surge in Demand

As demand surges for artisanal and specialty fusion pizza sauces, consumer expectations in the pasta sauce market are evolving, driving both innovation and a push towards premium offerings. Data from Symrise highlights a 38% uptick in consumer interest for cross-cultural pasta flavors in 2024 [3]Source: Symrise, “Cross-Cultural Flavor Trends 2024,” symrise.com , with North America and Asia-Pacific leading the charge. Here, culinary exploration is not just about taste but is intertwined with lifestyle identity and social media trends. In tune with this evolving palate, Sauz rolled out a Miso Garlic Marinara, merging Asian umami with Italian roots, and striking a chord with the younger, adventurous demographic. The Foraging Fox in the UK debuted a Harissa Tomato Pizza Sauce, targeting those with a penchant for bold, globally-inspired tastes. Meanwhile, Williams Sonoma in the U.S. catered to the gourmet crowd with sauces like Roasted Garlic Truffle and Thai Basil Tomato, underscoring the demand for upscale home dining. Not to be left out, Coles in Australia introduced a small-batch sauce line, featuring flavors like Chipotle Roma and Smoky Tomato. These diverse offerings underscore a broader trend: a move towards experimentation and personalization in food, enabling pasta sauce brands to resonate with shifting cultural tastes and a premium lifestyle ethos.

The Shift Toward Clean-Label Ingredients in Sauces

A shift toward clean-label ingredients is reshaping consumer behavior in the pasta sauce market. This trend is prompting both reformulations and the launch of premium products, as shoppers increasingly demand transparency and simplicity in ingredients. The 2024 IFIC Food & Health Survey reveals that 72% of consumers actively avoid artificial ingredients, and 63% scrutinize ingredient lists before making a purchase [4]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org . These statistics underscore the significant influence of clean-label cues on buying decisions. Responding to this trend, Rao’s Homemade has expanded its marinara line, now featuring non-GMO tomatoes and omitting added sugars and preservatives, specifically targeting ingredient-conscious consumers. Similarly, Otamot has rolled out vegetable-rich sauces boasting short, recognizable ingredient lists devoid of artificial additives, appealing to health-focused families. In Germany, Alnatura has launched a biodynamic tomato-basil sauce, highlighting its commitment to minimal processing and organic sourcing. Mainstream retailers, too, are taking note; Kroger is broadening its “Simple Truth” line of clean-label pasta sauces, underscoring the trend's resonance across various price points. These moves underscore the growing importance of ingredient integrity and label clarity in the market, spurring innovation and reformulation in the pasta sauce segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw-material prices | -0.8% | Global, with acute impact in tomato-producing regions | Short term (≤ 2 years) |

| Competition from homemade and fresh alternatives | -0.6% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Availability of diverse cuisines and exotic sauces | -0.5% | Global, strongest in multicultural urban markets | Medium term (2-4 years) |

| Regulatory and compliance challenges | -0.4% | Global, intensity varies by jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Homemade and Fresh Alternatives

Consumers increasingly favor homemade and fresh alternatives over packaged pasta sauces, driven by a desire for authenticity, freshness, and control over ingredients. As cooking evolves into a form of self-expression and wellness, many are opting for homemade sauces crafted from pantry staples like olive oil, garlic, and fresh herbs. Social media, from TikTok's viral Gigi Hadid vodka sauce to influencers touting "5-ingredient" clean pasta sauces, has made scratch-cooking not just common but aspirational. In 2023, meal kit services such as Blue Apron and HelloFresh pivoted from offering pre-made sauces to providing individual sauce components, emphasizing freshness and customization. This trend is especially evident among urban, label-conscious consumers who view store-bought sauces as overly processed and lacking in flavor depth. Consequently, brands that have traditionally relied on shelf-stable formats now face a pressing challenge: they must enhance ingredient quality and minimize additives or risk being dismissed as mere shortcuts in today's discerning kitchens. This shift towards personalization and freshness not only curbs category growth but also compels premium brands to reevaluate their market positioning.

Availability of Diverse Cuisines and Exotic Sauces

As diverse cuisines and exotic sauces become more accessible, consumer interest in traditional pasta sauces wanes, stunting the category's growth. With palates evolving and global flavors more accessible, many consumers, especially younger, urban ones, are turning to alternatives like Thai curry, Korean gochujang, Mexican mole, or Middle Eastern zhug, sidelining classics like marinara and alfredo. In 2023, brands such as Omsom and Fly By Jing made waves in Western markets, introducing bold, globally-inspired sauce kits that cater to adventurous eaters. Meanwhile, restaurants and food delivery giants like Zomato and Uber Eats have broadened their international menus, bringing dishes like ramen, birria tacos, and bibimbap into the mainstream. This heightened exposure has reshaped consumer expectations, casting traditional Italian sauces as less dynamic. Retail shelves, once dominated by pasta sauces, now showcase a mix of ethnic condiments and fusion marinades, underscoring the shift in demand. In this evolving landscape, pasta sauce brands face mounting pressure to innovate beyond their traditional offerings or risk stagnation, especially in premium food segments where novelty and global influences reign supreme.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tomato-Based Dominance Faces Cream Innovation

In 2025, tomato-based sauces command a dominant 53.89% share of the pasta sauce market, underscoring their universal appeal and pivotal role in Italian cuisine. Their adaptability to various pasta types and regional flavor preferences solidifies their status as the preferred choice for both casual and gourmet meals. Brands are innovating to keep this segment fresh; for instance, Sauz’s Hot Honey Marinara, introduced in 2024, marries sweetness with spice, catering to contemporary tastes. This knack for evolution, while staying true to their roots, has helped tomato-based sauces fend off rising competition from newer formats.

Meanwhile, cream-based sauces are on a rapid ascent, with projections indicating a 7.01% CAGR growth rate through 2031. This surge is largely attributed to consumers' growing penchant for indulgent, restaurant-style meals at home. Dishes like fettuccine alfredo and carbonara, both visually appealing and social media darlings, have further fueled this trend. Nestlé's recent expansion into creamy white sauce variants, alongside gourmet D2C brands rolling out truffle-infused and herb-forward alfredo jars, underscores the segment's premiumization. Pesto and herb-based sauces are also on the rise, bolstered by Barilla's 2024 introduction of Creamy Tomato Pesto and Vegan Pesto, catering to both traditionalists and the plant-based crowd. These trends highlight a pronounced consumer shift towards adventurous flavors, health-centric choices, and a desire for gourmet experiences at home, reshaping the competitive dynamics of the pasta sauce market.

By Packaging Type: Glass Heritage Meets Flexible Future

In 2025, glass jars command a leading 38.05% share of the pasta sauce market, primarily due to their strong association with quality, freshness, and visual appeal. These jars are particularly popular in the premium and specialty sauce segment, where the visibility of ingredients like herb flecks or olive oil separation boosts perceived authenticity. Brands such as Rao’s and Barilla capitalize on this trend, packaging their flagship sauces in glass. This choice not only aligns with an artisanal image but also taps into a deep-rooted consumer trust in glass's flavor-preserving attributes. Furthermore, the durability and prominent shelf presence of glass jars solidify their status as the go-to choice for both retail and gifting, even as sustainable alternatives emerge.

On the other hand, flexible pouches and squeeze packs are rapidly gaining traction, projected to grow at a 6.51% CAGR through 2031. A consumer shift towards eco-friendly, lightweight, and user-friendly packaging fuels this surge. Amcor's introduction of recyclable retort pouches for pasta sauces in 2024 underscores the industry's push to meld convenience with sustainability. Catering to eco-conscious families and individuals, Saucery Co. and Coles have rolled out refillable and squeezable pouches, emphasizing portability and waste reduction. While PET containers remain a staple for budget-conscious consumers, their dominance is increasingly challenged by a growing sustainability ethos. These evolving dynamics underscore a broader industry pivot towards circular packaging systems, aligning product design with a heightened consumer focus on environmental stewardship and usability.

By Distribution Channel: Retail Strength Meets Foodservice Recovery

In 2025, retail channels commanded a dominant 71.88% share of the pasta sauce market, buoyed by a surge in home cooking during the pandemic and the ongoing ascent of omnichannel shopping. Supermarkets and hypermarkets, with their vast selections and promotional prowess, continue to lead the pack. E-commerce, propelled by giants like Amazon in Italy, has broadened access, while artisanal brands' direct-to-consumer subscription models are winning over urbanites. These models resonate particularly with millennials and Gen Z, who prioritize personalization, authenticity, and convenience in their culinary pursuits.

The HoReCa segment, projected to grow at an 7.92% CAGR through 2031, is riding the wave of a post-pandemic dining resurgence and the allure of high-margin pasta dishes. For example, Barilla’s Foodservice division provides a variety of bulk-packaged sauces, designed for both quick-service and full-service restaurants. Similarly, Mutti offers foodservice-exclusive formats, such as 3kg tomato sauce tins, perfect for bustling kitchens. La San Marzano caters to upscale dining with its HoReCa line, featuring gourmet imported Italian sauces made with DOP ingredients. Such tailored offerings not only help restaurants stand out on menus but also ensure consistency and efficiency, underscoring HoReCa's pivotal role in driving pasta sauce demand.

By Category: Conventional Stability Versus Free-Form Innovation

In 2025, conventional pasta sauces commanded an 80.75% market share, buoyed by consumers' preference for familiar tastes and consistent quality. Ingrained purchasing habits and prominent national branding bolster their stronghold. Leading players, including Prego and Classico, provide a diverse array of flavor options, ensuring accessibility. These brands capitalize on widespread retail distribution, mainstream allure, and strategic promotions to nurture loyalty, especially among families and value-driven consumers who favor dependability over novelty.

On the other hand, free-form alternatives are on an upswing, boasting a 8.74% CAGR projected through 2031. A surging appetite for authenticity, clean-label assurances, and an artisanal touch fuel this growth. Brands like Monte's Fine Foods are carving a niche with their small-batch sauces, crafted from non-GMO tomatoes and minimal processing. Their transparent ingredient sourcing appeals to discerning consumers in pursuit of premium culinary experiences. The segment's growth trajectory also mirrors heightened health and sustainability concerns. Innovations are branching into organic, vegan, and functional subcategories. While these niche formats may be smaller in volume, they promise high margins, allowing brands to stand out in a market increasingly influenced by values-driven choices.

Geography Analysis

In 2025, Europe secures a commanding 38.10% share of the global pasta sauce market, a testament to its rich pasta heritage, a penchant for authentic flavors, and cutting-edge manufacturing prowess. Italy stands as a beacon of this dominance, with legacy brands like La Doria championing traditional recipes and boasting a robust export network. Meanwhile, Barilla, celebrated for its expansive production and sustainability efforts, epitomizes the region's fusion of tradition with modern efficiency. The UK's appetite for artisanal sauces has spurred the rise of regional players, emphasizing heritage and clean-label offerings. Concurrently, Germany's quest for authenticity and quality positions it as a prime market for premium Italian sauces.

Asia-Pacific emerges as the fastest-growing region, projected to accelerate at a 7.42% CAGR through 2031. Urbanization, a burgeoning middle class, and an increasing palate for Western cuisine propel this growth. In India, pasta sauces are gaining traction in home kitchens and quick-service restaurants. Brands like Del Monte and Veeba are leading the charge, offering variants tailored to regional preferences. Over in Japan, Kagome is at the forefront, diversifying its portfolio with innovative fusion sauces that resonate with local tastes. Such trends underscore the region's culinary experimentation, especially among the youth and in urban centers.

North America showcases robust consumption patterns, underscoring a commitment to flavor innovation. Established brands like Rao’s Homemade, Prego, and Classico dominate the shelves, while newcomers like Sauz highlight a pivot towards bold, contemporary flavors. South America's Italian culinary influence fosters a growing acceptance of pasta sauces, with local producers aligning their offerings to traditional meal customs. Meanwhile, in the Middle East and Africa, premium European brands such as Rummo and Barilla are broadening their footprint, appealing to urbanites and high-end dining venues.

Competitive Landscape

Pasta sauce manufacturers are employing diverse marketing strategies to capture and keep consumers in a moderately consolidated market. Established names like Kraft Heinz, Barilla, and Campbell’s leverage their broad brand recognition and heritage, marketing their sauces as trusted staples for all demographics. Meanwhile, premiumization trends have ushered in artisanal brands such as Monte’s Fine Foods and Sauz. These newcomers set themselves apart with clean-label offerings, bolder flavors, and narratives of small-batch production. By emphasizing transparency and authenticity, they resonate deeply with younger, health-conscious consumers. Moreover, through social media campaigns, influencer collaborations, and direct-to-consumer sales, these emerging brands sidestep traditional retail, captivating digitally savvy audiences with their compelling stories.

In the competitive pasta sauce arena, technology adoption stands out as a pivotal differentiator. Take Barilla, for example. They've harnessed Industrial Internet of Things (IIoT) technologies to oversee their supply chains, ensuring traceability and bolstering both sustainability and quality control. Packaging innovations are also making waves, with Amcor's recyclable retort pouches cutting carbon footprints by a notable 60%, a move that resonates with eco-conscious consumers. Beyond that, many manufacturers are tapping into data analytics for refined product development and inventory planning.

Strategic expansion is at the forefront of growth strategies, with many companies leaning into vertical integration and cross-category innovations. A notable trend sees sauce manufacturers branching into related areas like dried pasta and meal kits, crafting bundled offerings that not only elevate basket value but also bolster customer loyalty. The landscape has also been molded by mergers and acquisitions, with major players snapping up niche brands, diversifying their portfolios, and making inroads into lucrative premium segments. Furthermore, untapped opportunities like fusion flavors, regional Italian profiles, and the inclusion of functional ingredients present a fertile ground for both newcomers and established brands to carve out a unique growth trajectory.

Pasta Sauce Industry Leaders

Barilla G. e R. Fratelli S.p.A

The Campbell Soup Company

Mutti S.p.A

The Kraft Heinz Company

Del Monte Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sauz launched two new pasta sauce flavors, Miso Garlic Marinara and Brown Butter Alfredo, marking the first Asian-Italian fusion sauce commercially available and expanding distribution to Whole Foods and Sprouts nationwide. The launch represents significant category innovation by blending traditional Italian sauce bases with Asian flavor profiles, targeting adventurous consumers seeking unique culinary experiences while maintaining familiar pasta applications.

- January 2025: Filippo Berio introduced a premium pasta sauce line featuring eight varieties made with fresh, recognizable ingredients without preservatives or artificial additives, responding to consumer demand for clean-label products. The launch targets the growing segment of health-conscious consumers seeking authentic Italian flavors with transparent ingredient lists, positioning against mass-market alternatives through premium pricing and quality positioning.

- October 2024: Barilla expanded its pesto sauce line for fall with three new varieties including Creamy Tomato Pesto, Sweet and Spicy Pepper Pesto, and Vegan Pesto, available at Kroger and nationwide in 2025 at USD 3.99 per jar. The expansion addresses diverse dietary preferences while maintaining Italian authenticity, demonstrating how established brands adapt traditional recipes to accommodate contemporary consumer needs including plant-based alternatives.

- February 2024: TRUFF expanded its product line to include pasta sauce alongside hot sauce, mayonnaise, and truffle oil, leveraging pandemic-driven consumer interest in premium condiments. The expansion demonstrates how specialty condiment brands can successfully enter adjacent categories through brand extension strategies that maintain premium positioning and unique flavor profiles.

Global Pasta Sauce Market Report Scope

| Tomato-Based Sauces |

| Cream-Based Sauces |

| Pesto and Herb-Based Sauces |

| Others |

| Glass Jar |

| PET |

| Flexible Pouch/Squeeze Pack |

| Others |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores/Grocery Stores | |

| Others |

| Free- Form |

| Conventional |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tomato-Based Sauces | |

| Cream-Based Sauces | ||

| Pesto and Herb-Based Sauces | ||

| Others | ||

| By Packaging Type | Glass Jar | |

| PET | ||

| Flexible Pouch/Squeeze Pack | ||

| Others | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Online Retail Stores | ||

| Convenience Stores/Grocery Stores | ||

| Others | ||

| By Category | Free- Form | |

| Conventional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the pasta sauce market in 2026?

It is valued at USD 11.99 billion and is expected to grow to USD 15.28 billion by 2031.

Which region leads current sales?

Europe holds 38.10% of sales, driven by Italian culinary heritage and established manufacturing scale.

Which segment is expanding fastest?

Cream-based sauces are projected to post a 7.01% CAGR through 2031, outpacing tomato-based varieties.

What consumer trend most shapes new product development?

Clean-label demand drives reformulation toward recognizable ingredients and reduced additives.

Page last updated on: