Hot Sauce Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

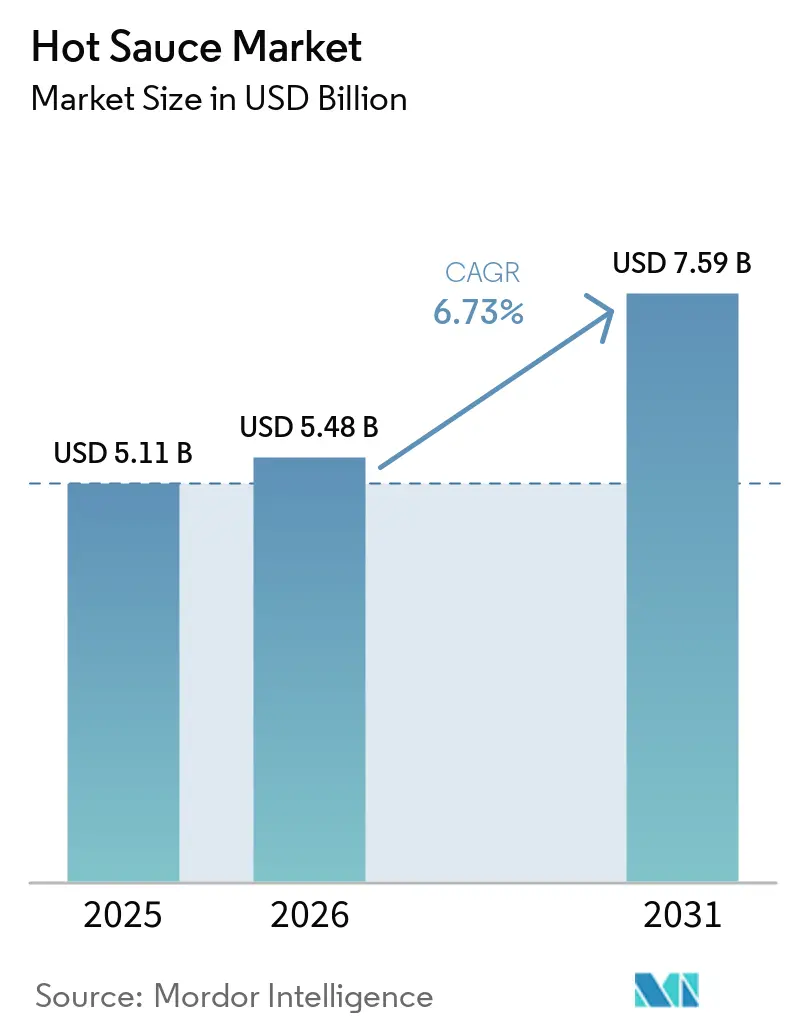

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 7.59 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

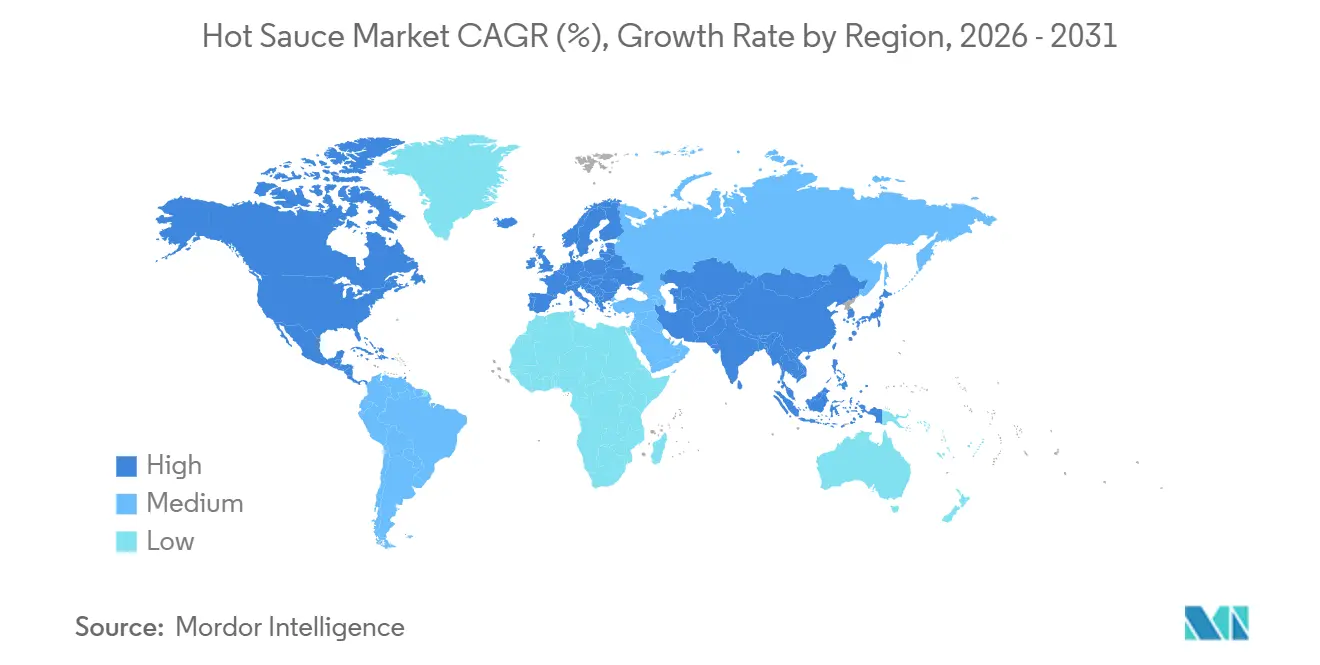

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hot Sauce Market Analysis by Mordor Intelligence

The hot sauce market size is expected to grow from USD 5.11 billion in 2025 to USD 5.48 billion in 2026 and is forecast to reach USD 7.59 billion by 2031 at a 6.73% CAGR over 2026-2031. As craft labels leverage limited-batch fermentation, direct-to-consumer subscriptions, and celebrity collaborations, they're not only securing shelf space but also capturing digital attention. In response, traditional manufacturers are turning to artificial intelligence, significantly shortening formulation cycles from 18 months to under six. This shift is exemplified by Symrise’s Symvision platform, which made its debut in November 2025. Today's consumers prioritize flavor complexity over mere heat, evident in the evolution from the “swicy” sweet-spicy trend to the newer “swangy,” which introduces tangy notes. Sustainability is also on the radar; with single-serve sachets and pouches gaining traction in foodservice, they're reducing sauce waste by up to 18% compared to traditional countertop pumps. Despite broader economic challenges, bold condiments remain a staple, enhancing the appeal of budget-friendly home-cooked meals and maintaining consumer spending even amidst cutbacks.

Key Report Takeaways

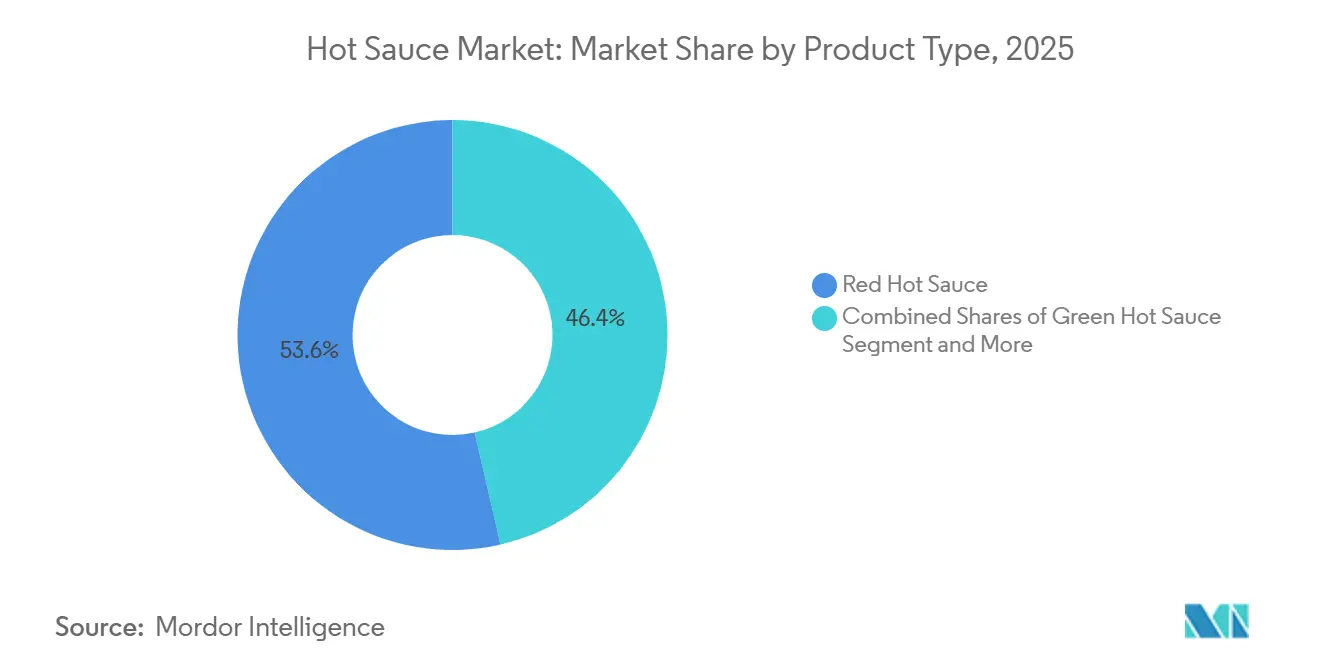

- By product type, red sauces held 53.59% of 2025 volume, while green sauces are projected to expand at a 7.48% CAGR through 2031.

- By flavor, plain variants commanded 65.69% revenue share in 2025, whereas flavored offerings are forecast to rise at a 7.97% CAGR to 2031.

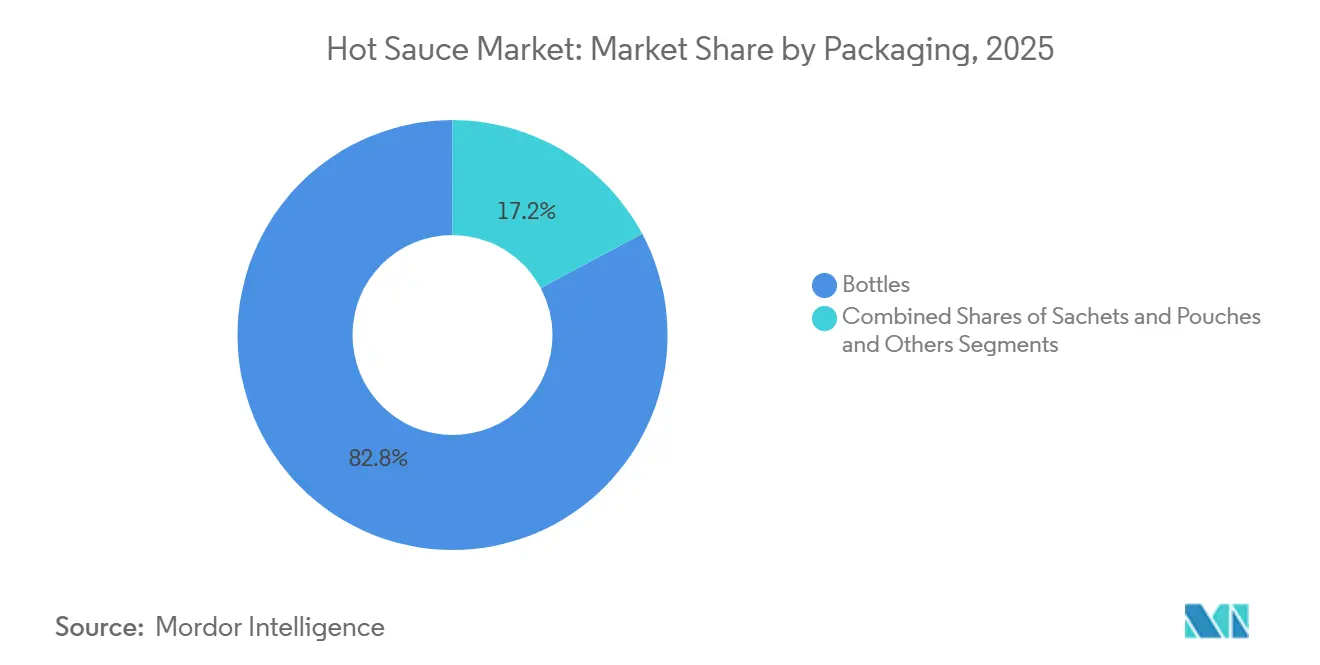

- By packaging, bottles led with 82.72% of the hot sauce market share in 2025; sachets and pouches represent the fastest pack format at a 6.98% CAGR through 2031.

- By distribution, retail channels controlled 67.12% of 2025 sales, but foodservice will record the highest growth at a 7.20% CAGR during 2026-2031.

- North America captured 37.40% of 2025 revenue, while Asia-Pacific is expected to post a regional high 7.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hot Sauce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Foodservice and Quick-Service Restaurants | +1.2% | Global, with concentration in North America, Asia-Pacific urban centers | Medium term (2-4 years) |

| Globalization of Ethnic and Spicy Cuisines | +1.0% | Global, led by North America and Europe, adoption of Asian and Latin American flavors | Long term (≥ 4 years) |

| Product Innovation and Premiumization | +1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Artificial Intelligence-Driven Flavor Personalization | +0.6% | North America, Europe | Medium term (2-4 years) |

| Growing Popularity of Home Cooking | +0.8% | Global, post-pandemic behavioral shift | Medium term (2-4 years) |

| Influencer-Led DTC Subscription Models | +0.5% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of foodservice and quick-service restaurants

Quick-service restaurants (QSRs) are now embedding proprietary hot sauces into their core menu items, elevating these condiments from mere optional add-ons to pivotal brand-defining elements. Yum! Brands revealed that sauces evoke 2.4 times more consumer excitement than other menu components. Notably, 71% of KFC's top-performing items now feature these signature sauces in 2025[1]Source: Yum! Brands, “2025 Annual Report,” yum.com. This integration goes beyond mere flavor differentiation. QSRs are harnessing the power of sauces not only to entice repeat visits but also to command premium pricing. Moreover, limited-time sauce offerings instill a sense of urgency, amplifying transaction frequency. The rise of ghost kitchens and delivery-only concepts further underscores this trend. Sauces, unlike fried items, travel better and retain their flavor integrity during transit. Additionally, the foodservice industry's pivot towards single-serve sachets, witnessing a robust 7.20% CAGR, underscores a quest for operational efficiency. These sachets allow for precise portion control, significantly reducing waste compared to traditional bulk dispensers[2]Source: Packaging Europe, “Single-Serve Sachets Cut Food Waste,” packagingeurope.com.

Product innovation and premiumization

Artisan producers are leveraging fermentation, small-batch aging, and single-origin chili sourcing to command price premiums 3 to 5 times higher than their mass-market counterparts. Truff, which secured around USD 79.87 million in funding, rolled out its inaugural mild hot sauce in 2026, catering to consumers who value truffle-infused nuances over mere heat. Frank's RedHot unveiled 10 new SKUs, such as Korean BBQ, Pineapple Hawaiian, and Ghost Pepper Ranch, between April 2025 and January 2026. This move underscores the necessity for even established brands to innovate at an artisan pace to maintain their shelf presence. The "swicy" trend, which melds sweet and spicy flavors, has now transitioned to "swangy," adding tangy notes. This evolution reflects consumers' desires for intricate flavor profiles that complement a variety of cuisines. Moreover, limited-edition releases and partnerships with celebrities are fueling this premiumization trend. Such products frequently sell out within hours, leading to secondary markets and bolstering brand value through their scarcity.

Artificial intelligence-driven flavor personalization

AI platforms are accelerating product development and facilitating large-scale mass customization. In November 2025, Symrise unveiled its Symvision AI tool, capable of analyzing consumer preferences, ingredient interactions, and regional taste profiles. This tool can produce optimized formulations in weeks, a process that previously took months. As a result, brands can now test micro-batches in select regions, minimizing the financial risks associated with flavor mismatches before committing to full production. Meanwhile, Kraft Heinz rolled out its Heinz Remix, a digital sauce dispenser that blends sauces in real-time based on user preferences. This innovation not only caters to individual tastes but also generates valuable data for future product launches. Furthermore, AI-driven personalization is tackling challenges from GLP-1 medications, known to dull taste perception in 12% of the U.S. population. Manufacturers are leveraging machine learning to pinpoint flavor compounds that remain detectable for these users, effectively broadening their market reach.

Growing popularity of home cooking

Cooking habits formed during the pandemic have become ingrained, with many consumers now eager to experiment with new condiments. This shift has propelled hot sauce from a once-niche status to a must-have pantry item, particularly in retail channels, which accounted for 67.12% of distribution in 2025. E-commerce platforms are capitalizing on this trend, introducing subscription models that deliver handpicked sauces monthly, alleviating decision fatigue and bolstering brand loyalty. Brands like HeatWave and Secret Aardvark are tapping into influencer collaborations to connect with home cooks; for instance, influencer Will Neff's endorsement of HeatWave led to a notable uptick in online orders, underscoring the power of social validation, especially among younger audiences. Furthermore, as more consumers dive into home cooking, there's a noticeable uptick in demand for premium and artisan condiments. Those dedicating time to meal prep are increasingly inclined to splurge on higher-end condiments, believing these elevate their culinary prowess.

Restraints Impact Analysis*

| Restraint | (!) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Over Sodium, Sugar, and Capsaicin | -0.9% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Concern Over Raw Material Quality | -0.7% | Global, acute in North America and the Asia-Pacific | Short term (≤ 2 years) |

| Stringent Food Safety and Labeling Regulations | -0.5% | North America, Europe, Gulf Cooperation Council | Medium term (2-4 years) |

| Supply Chain Disruptions | -0.8% | Global, concentrated in Mexico, India, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over sodium, sugar, and capsaicin

Manufacturers are under pressure to reformulate products, balancing the need to reduce sodium and sugar content with the desire to maintain flavor intensity. Starting in 2026, the FDA's revised definition of "healthy" will enforce stricter sodium limits, pushing brands to cut sodium levels by 10-15% or risk losing the "healthy" label[3]Source: U.S. FDA, “Definition of ‘Healthy’ Final Rule 2026,” fda.gov. Peer-reviewed research highlights the dual nature of capsaicin: while it provides cardiovascular and metabolic benefits in moderation, excessive consumption can lead to gastrointestinal issues and worsen conditions like irritable bowel syndrome. This nuanced perception complicates marketing strategies and restricts consumption among health-conscious consumers. Flavored variants, especially those riding the "swicy" trend, are facing criticism over their sugar content. Clean-label proponents advocate for natural sweeteners, but these come at a premium, often 2 to 3 times the cost of traditional options, and can change the product's taste profile.

Concern over raw material quality

Climate change is diminishing chili quality and weakening capsaicin potency, jeopardizing product consistency. Rising temperatures and unpredictable rainfall are further depleting capsaicin levels in peppers. As a result, manufacturers are compelled to boost chili content in each batch to uphold desired heat levels. In March 2026, Huy Fong Foods suspended production due to crop failures of red jalapeños in Mexico, where drought, heat stress, and pest pressures wreaked havoc on yields. The 2025-2026 season saw India's chili production plummet by 35-40%, constricting global supply and driving up prices. This surge rippled through supply chains, squeezing margins for mid-tier brands in India that couldn't transfer costs to their price-sensitive consumers. Highlighting the critical need for raw material access, McCormick acquired chili mash supplier Jurado Inc. for USD 38.1 million in March 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Red Dominance Faces Green Innovation

Red hot sauce maintains its commanding position with 53.59% market share in 2025, reflecting consumer familiarity and established brand loyalty, while green hot sauce emerges as the fastest-growing segment with 7.48% CAGR through 2031. Green hot sauce's acceleration is driven by its milder heat profile and broader culinary applications, particularly in fusion cuisines and health-conscious consumer segments seeking flavorful alternatives to traditional condiments. The competitive dynamics within product types reveal distinct positioning strategies, with red hot sauce manufacturers focusing on heat intensity differentiation and brand heritage, while green hot sauce producers emphasize flavor innovation and culinary versatility. McCormick's expansion of its crushed pepper portfolio with Thai Style Chili and Hatch Chile variants demonstrates the innovation trajectory within traditional red pepper products in May 2025.

Yellow hot sauce and other variants collectively represent the remaining market share, with yellow varieties gaining traction in specific regional markets and specialty applications. Yellow hot sauces, such as Yellowbird Habanero, often use habanero peppers as their main source of heat. These peppers provide a tropical, fruity heat that distinguishes yellow sauces from red or green varieties. The "other" category, including specialty blends and limited-edition variants, represents an emerging battleground for premium positioning and seasonal marketing campaigns that can command higher margins while testing consumer acceptance of new flavor profiles.

By Flavor: Plain Foundations Enable Flavored Growth

In 2025, plain hot sauce captured a dominant 65.69% market share, underscoring a deep-rooted consumer affinity for its pure chili essence, which allows for personal customization. Yet, flavored variants are set to surge at a 7.97% CAGR through 2031, driven by limited-edition launches, celebrity partnerships, and the rising "swicy" trend, which harmoniously melds sweet, spicy, and tangy flavors. Truff debuted its inaugural mild hot sauce in 2026, infusing truffle essence into a chili foundation, catering to upscale consumers who value flavor complexity over mere heat. The "swangy" trend, which introduces tangy nuances to sweet-spicy blends, took shape between 2025 and 2026. Brands began infusing citrus, vinegar, and fermented elements, crafting richer, multi-layered taste experiences.

Frank's RedHot rolled out 10 new SKUs, spanning from Korean BBQ to Ghost Pepper Ranch, between April 2025 and January 2026. This move underscores the rapid pace needed to thrive in the flavored segment, where novelty is key to both initial trials and repeat purchases. In a bold fusion, Jeremiah's Italian Ice teamed up with Hawaiian Hot T's to unveil "Island Fire." This innovative blend marries POG² (passion fruit, orange, guava) with ghost and scorpion peppers, straddling the line between dessert and condiment. It's a tantalizing offering for the adventurous palate, especially those chasing Instagram-worthy flavor profiles. Beyond traditional uses, brands are reimagining flavored sauces as versatile marinades, salad dressings, and pizza drizzles. This strategy not only broadens their appeal but also boosts per-capita consumption by introducing new usage occasions.

By Packaging: Bottles Yield to Convenience Innovation

Traditional bottles maintain market dominance with 82.72% share in 2025, reflecting established retail infrastructure and consumer purchasing habits, while sachets and pouches are experiencing rapid growth at 6.98% CAGR through 2031. This packaging evolution is driven by on-the-go consumption patterns, portion control preferences, and sustainability concerns that favor reduced packaging waste and improved recyclability. The growth of flexible packaging formats aligns with the "bring your own condiments" trend among younger consumers and the expansion of delivery and takeout food services that require portable condiment solutions.

Innovation in packaging technology is creating new opportunities for product differentiation and consumer engagement, with research into acidic sauce permeation on high-barrier packaging films revealing opportunities for improved product preservation and shelf life extension. The "other" packaging category, including cans and jars, represents niche applications and premium positioning opportunities, particularly for artisanal brands and specialty products that can command higher prices through distinctive packaging design. Sustainability trends are driving investment in eco-friendly packaging materials and refillable formats that appeal to environmentally conscious consumers while reducing long-term packaging costs.

By Distribution Channel: Retail Stability Meets Foodservice Dynamism

In 2025, retail channels dominated distribution with a 67.12% share. Supermarkets and hypermarkets led due to high foot traffic and impulse purchases. Online retail, a subset of retail, was the fastest-growing segment. E-commerce platforms like Amazon and brand-owned direct-to-consumer (DTC) sites reshaped shopping with curated selections, subscription models, and customer reviews that reduce purchase risks. Truff's USD 79.87 million funding in February 2026 highlighted confidence in DTC economics, where brands achieve 40-50% gross margins compared to 20-30% in traditional retail after slotting fees and promotional allowances. Influencer collaborations further drive DTC growth; for instance, Will Neff's promotion of HeatWave spurred significant online order spikes, showcasing the impact of social proof on digitally-savvy consumers.

Foodservice, holding 32.88% of the 2025 share, is projected to grow at a 7.20% CAGR through 2031, making it the fastest-growing distribution channel. Quick-service restaurants are driving this growth by integrating proprietary sauces into core offerings. Yum! Brands reported that sauces generate 2.4 times more consumer excitement than other menu items, with 71% of KFC's top-selling dishes featuring signature sauces. Licensing collaborations, such as Ginsters' Buffalo Chicken Pocket with Frank's RedHot in the UK, expand brand reach into new categories and generate royalty income without capital investment. Convenience and grocery stores act as intermediary channels, offering smaller pack sizes and impulse-buy opportunities to capture consumers between major shopping trips. As brands adopt omnichannel strategies, the distribution landscape will fragment further, balancing retail shelf presence, DTC margins, and foodservice growth.

Geography Analysis

North America maintains its market leadership with 37.40% share in 2025, driven by established consumer preferences for hot sauce consumption and the presence of major manufacturers like McCormick and Kraft Heinz. The region's mature market characteristics are reflected in the emphasis on premium positioning and flavor innovation, with companies investing heavily in brand differentiation and product line extensions. Regulatory pressures from FDA sodium reduction initiatives are forcing reformulation strategies that may create competitive advantages for companies that can maintain flavor integrity while meeting health guidelines. The region's foodservice sector strength, particularly in quick-service restaurants, provides stable volume demand while creating opportunities for bulk packaging and customizable flavor systems.

Asia-Pacific emerges as the fastest-growing region with 7.58% CAGR through 2031, reflecting urbanization trends, rising disposable incomes, and expanding middle-class consumption patterns. The region's growth is supported by cultural preferences for spicy foods and the integration of hot sauce into traditional cuisines, creating opportunities for both international brands and local manufacturers. Kikkoman's USD 560 million investment in a new Wisconsin production facility demonstrates the strategic importance of Asian companies in the global hot sauce market in June 2024.

Europe represents a significant growth opportunity driven by increasing consumer interest in international cuisines and spicy flavors. Germany leads European imports, followed by Spain and the United Kingdom, with strong demand for organic products and sustainable packaging solutions. The region's regulatory environment favors natural additives and clean-label products, creating opportunities for manufacturers who can meet these requirements while maintaining competitive pricing. South America and Middle East & Africa represent emerging markets with significant growth potential, driven by urbanization trends and expanding retail infrastructure, though these regions face challenges related to distribution networks and price sensitivity that may require adapted product formulations and packaging strategies.

Competitive Landscape

The hot sauce market is characterized by moderate competition among both established multinational corporations and a growing number of regional and artisanal brands. Major players such as McCormick & Company, Huy Fong Foods, Inc., McIlhenny Company (Tabasco), The Kraft Heinz Company, and Baumer Foods, Inc. dominate the global landscape, leveraging extensive distribution networks, diverse product portfolios, and strong brand recognition to maintain significant market shares. These companies often expand their reach through strategic acquisitions, such as McCormick & Company, Inc. purchase of Cholula, and invest in packaging innovations and influencer-driven marketing to attract younger consumers.

In addition to these industry giants, the market is witnessing a surge in smaller, niche brands that focus on organic, vegan, and fusion hot sauces. Artisanal producers differentiate themselves through unique flavor profiles, clean-label ingredients, and small-batch production methods, appealing to consumers seeking novel taste experiences and healthier options. The rise of e-commerce and the increasing globalization of cuisines have further lowered barriers to entry, enabling these emerging brands to reach broader audiences and carve out specialized market segments.

Success in the hot sauce sector increasingly depends on innovation, product quality, branding, and adaptability. Companies are responding to evolving consumer preferences by launching new flavors, emphasizing premiumization, and targeting health-conscious buyers. For instance, in June 2024 TRUFF, the truffle brand celebrated for its innovative take on pantry staples launched TRUFF Buffalo Sauce. This new hot sauce aligns with the refined allure of black truffle with zesty vinegar, a spicy cayenne punch, and the smooth richness of olive oil. The growing popularity of spicy foods, the influence of Asian and Latin American cuisines, and the expansion of fast food and foodservice industries continue to fuel demand. As the market expands, both established and emerging players must remain agile, monitor trends closely, and leverage digital platforms to sustain competitive advantage in this dynamic industry

Hot Sauce Industry Leaders

Huy Fong Foods, Inc.

McIlhenny Company

The Kraft Heinz Company.

McCormick & Company, Inc.

Baumer Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cholula, the Mexican Hot Sauce brand, brought its signature balanced heat to 11 new products, including cholula cooking sauces that made it easy to recreate a taco truck experience at home. Crafted with authenticity, convenience and versatility, the expansion celebrated the rich heritage of Cholula. With cooking sauces that offered premium, restaurant-level flavor, seasoning mixes based on popular Latin dishes, and fan-favorite toppings, they take any meal to the next level.

- March 2025: Truckee Hot Sauce, founded by long-time local residents Tray and Janai Shock, became available in stores across Truckee, Tahoe, Reno, and Northern California. After years of perfecting recipes and hand-selecting premium ingredients, the company launched its flagship sauces, On the Go Rojo and Everyday Verde, as well as its fiery new flavor, Happy Habañero.

- February 2025: With its Amarillo Hotish Sauce and Rocoto Hot Sauce enlivening mealtime one drizzle at a time, Tari launched three more vibrant and piquant flavors in 2025 - Zesty Verde, Tropical Kick, and Smoky Heat. For each vibrant bottle, Tari grew native Peruvian peppers in the Andean Mountains and used a longstanding grinding tradition that maximized taste and created a creamy texture.

- January 2025: Cholula announced the launch of "Cholula Extra Hot", an extra spicy version of the brand's generations-old family recipe. The Cholula lineup featured eight hot sauces with varying heat levels and flavor profiles. Since acquiring the brand in 2020, McCormick has also entered new categories, including Cholula Salsas, Cholula Taco Seasonings, and Cholula Frozen Bowls.

Global Hot Sauce Market Report Scope

Hot sauce is a pungent, spicy condiment or seasoning made primarily from chili peppers. The Hot Sauce Market is segmented by product type, flavor, packaging, and distribution channel. By product type, the market is segmented into red hot sauce, green hot sauce, yellow hot sauce, and others. By flavor, the market is segmented into plain and flavored. By packaging, the market is segmented into bottles, sachets and pouches, and others. By Distribution channel, the market is segmented into horeca/foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Red Hot Sauce |

| Green Hot Sauce |

| Yellow Hot Sauce |

| Others |

| Plain |

| Flavored |

| Bottles |

| Sachets and Pouches |

| Others |

| HoReCa/Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Red Hot Sauce | |

| Green Hot Sauce | ||

| Yellow Hot Sauce | ||

| Others | ||

| Flavor | Plain | |

| Flavored | ||

| Packaging | Bottles | |

| Sachets and Pouches | ||

| Others | ||

| Distribution Channels | HoReCa/Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the hot sauce market?

The Artisan hot sauce market size is USD 5.48 billion in 2026 and is projected to climb to USD 7.59 billion by 2031.

Which region will contribute the fastest growth?

Asia-Pacific is forecast to log a 7.58% CAGR through 2031, driven by Thailand’s sriracha export engine and increasing demand in Japan and Australia.

Which product type is expanding the quickest?

Green sauces, centered on jalapeño and serrano bases, are set to grow at a 7.48% CAGR through 2031.

Why are single-serve sachets gaining traction?

QSR chains adopt sachets to cut waste by up to 18%, improve portion control, and maintain flavor integrity during delivery, boosting 6.98% CAGR for the format.

Page last updated on: