De-oiled Lecithin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

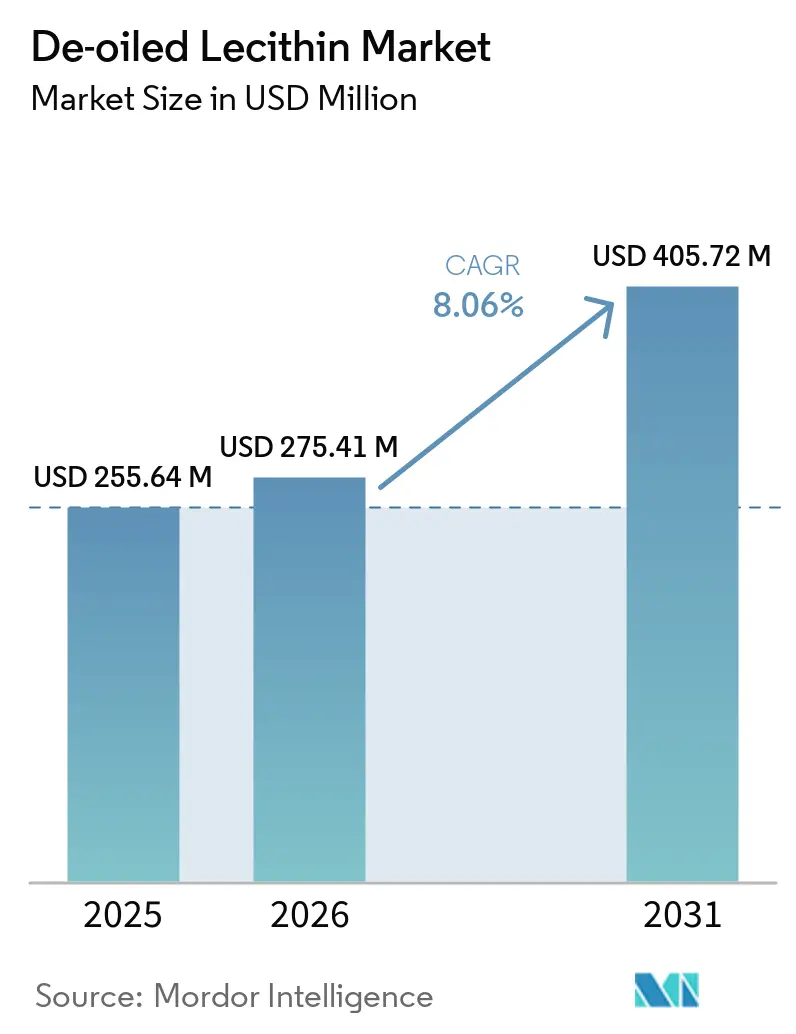

| Market Size (2026) | USD 275.41 Million |

| Market Size (2031) | USD 405.72 Million |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

De-oiled Lecithin Market Analysis by Mordor Intelligence

The de-oiled lecithin market size is expected to grow from USD 255.64 million in 2025 to USD 275.41 million in 2026 and is forecast to reach USD 405.72 million by 2031 at a 8.06% CAGR over 2026-2031. The global de-oiled lecithin market is driven by the increasing demand for clean-label, non-GMO, and allergen-conscious food ingredients, as manufacturers shift from synthetic emulsifiers to naturally derived alternatives. The growing consumption of convenience foods, bakery products, confectionery, dairy alternatives, and plant-based foods has boosted the use of de-oiled lecithin due to its effective emulsification, dispersibility, and extended shelf-life properties. Additionally, the expanding nutraceutical and pharmaceutical industries contribute to market growth, as de-oiled lecithin is widely used in dietary supplements, instant powders, capsules, and drug formulations for its flowability and phospholipid content. The rising adoption of organic and soy-free variants, such as sunflower-derived de-oiled lecithin, is expanding its applications among health-conscious consumers and manufacturers targeting premium product segments. Furthermore, advancements in extraction and processing technologies have enhanced product purity, functionality, and stability, supporting its use in high-performance food, feed, cosmetic, and industrial applications. The growing emphasis on sustainable, naturally sourced ingredients continues to drive long-term market demand.

Key Report Takeaways

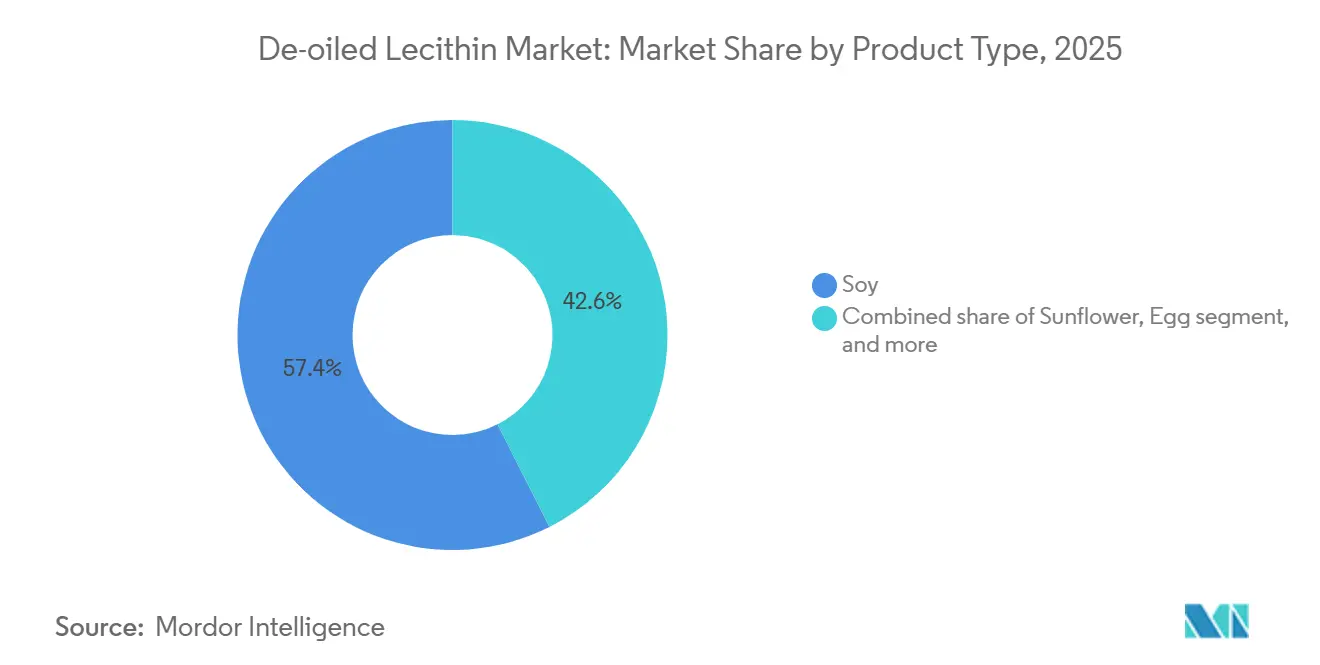

- By source, soy held 57.44% share in 2025, while sunflower is forecast to expand at 8.84% CAGR through 2031.

- By form, powder accounted for 51.76% share in 2025, while granules are projected to grow at 8.65% CAGR through 2031.

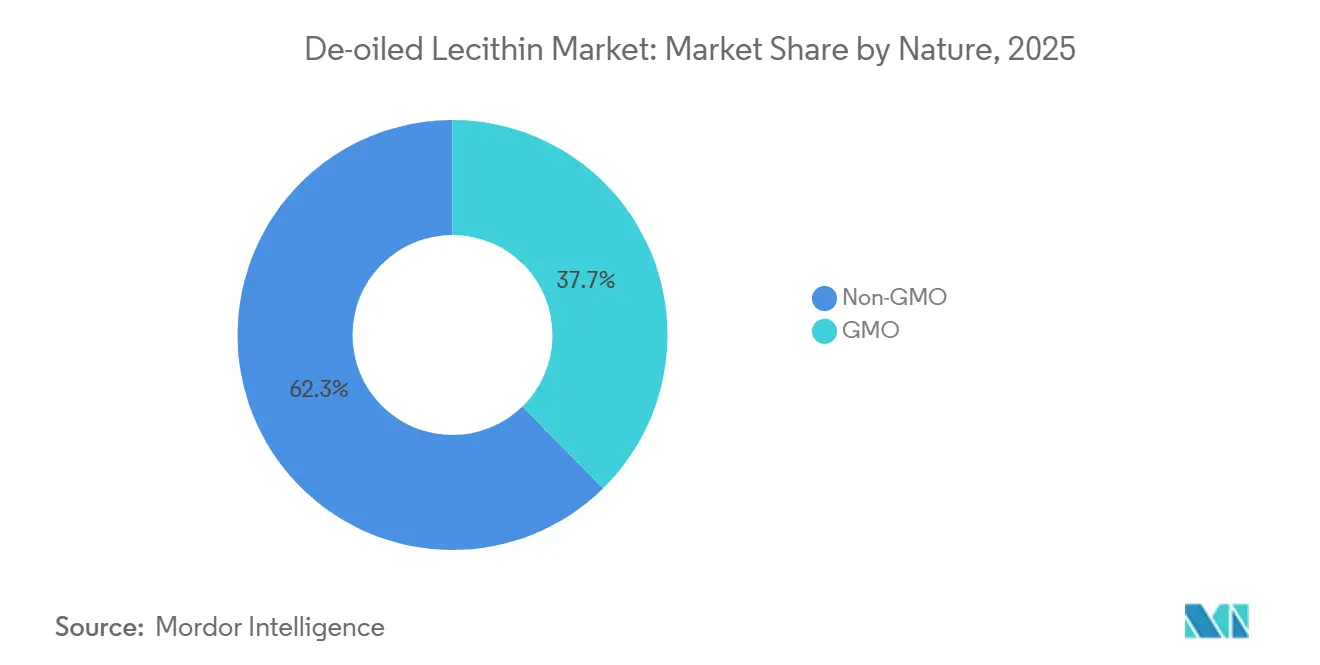

- By nature, non-GMO held 62.34% share in 2025 and is also the fastest-growing segment at 8.75% CAGR through 2031.

- By application, food and beverages captured 54.55% share in 2025, while nutraceuticals and pharmaceuticals are forecast to expand at 9.01% CAGR through 2031.

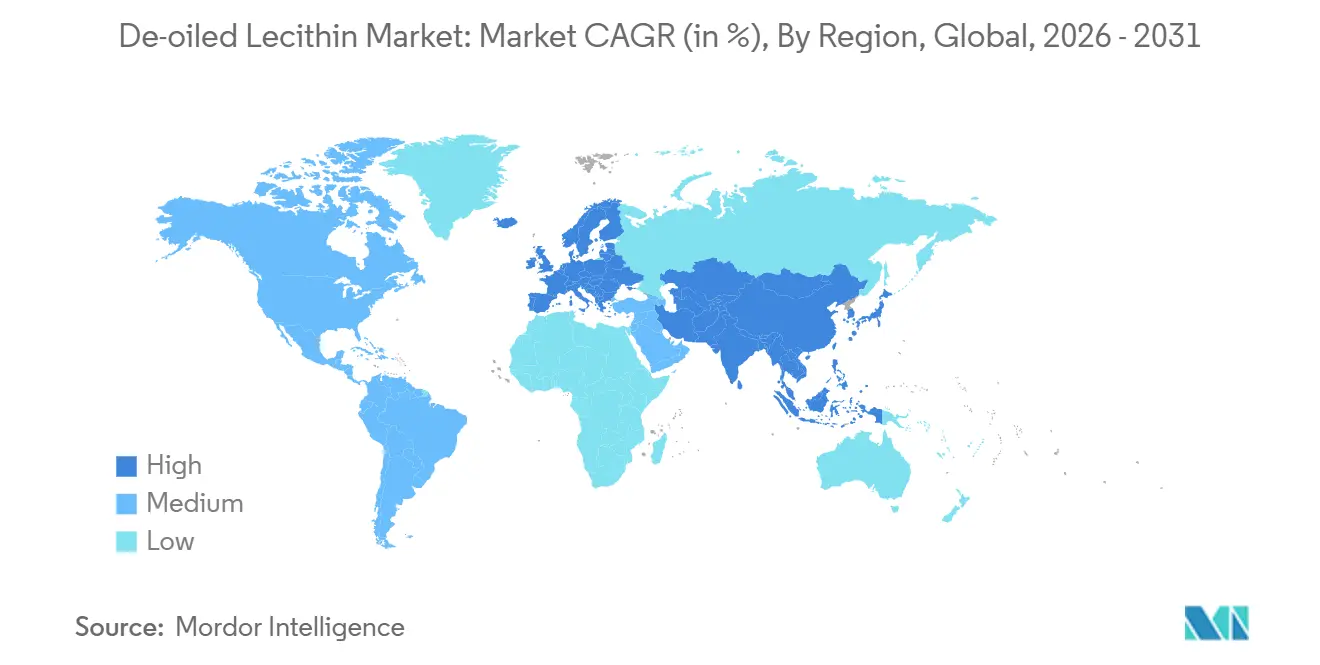

- By geography, Asia-Pacific represented 34.13% share in 2025 and is projected to record the highest CAGR at 8.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global De-oiled Lecithin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label food ingredients | +1.6% | Global, with premium markets in North America and Europe leading adoption | Short term (≤ 2 years) |

| Expansion of plant-based food and beverage formulations | +1.4% | North America and Europe core, extending to Asia-Pacific | Medium term (2-4 years) |

| Rising demand for allergen-free and specialty lecithin variants | +0.9% | North America and Europe, with spill-over to Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements in lecithin extraction and purification | +0.8% | Global, concentrated in Europe and North America R&D centres | Long term (≥ 4 years) |

| Increasing adoption of organic and non-GMO food manufacturing | +1.1% | Europe and North America core; growing in Asia-Pacific and South America | Medium term (2-4 years) |

| Growing applications across nutraceuticals, pharmaceuticals, cosmetics, and instant food products | +1.3% | North America and Europe leading; Asia-Pacific emerging rapidly | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label food ingredients

The increasing demand for clean-label food ingredients is a significant factor driving the growth of the global de-oiled lecithin market. Food and beverage manufacturers are progressively replacing synthetic additives with naturally derived ingredients that consumers recognize and trust. De-oiled lecithin is highly preferred due to its role as a natural emulsifier, while also enabling simplified ingredient lists, non-GMO formulations, and greater transparency in product labeling. This trend is particularly prominent in bakery, confectionery, dairy alternatives, nutritional beverages, and convenience foods, where clean-label positioning has become a competitive advantage. Consumer willingness to pay a premium for products with familiar ingredients is motivating manufacturers to reformulate existing products and develop new clean-label offerings incorporating de-oiled lecithin. According to Ingredion, in 2024, 56% of consumers expressed a willingness to pay more for products with recognizable ingredients, while 38% of new food and beverage product launches in the United States and Canada featured clean-label claims[1]Source: Ingredion, "Clean label ingredients: From buzzword to business driver," ingredion.com. This underscores the strong market momentum driving the adoption of de-oiled lecithin across various food applications.

Expansion of plant-based food and beverage formulations

The growth of plant-based food and beverage formulations is driving the global de-oiled lecithin market, as manufacturers increasingly seek natural emulsifiers and stabilizers to enhance the texture, consistency, and shelf life of dairy alternatives, meat substitutes, protein beverages, and vegan bakery products. De-oiled lecithin is extensively utilized in these applications due to its excellent dispersibility, ability to improve ingredient blending, and alignment with clean-label and plant-derived product preferences. As consumer interest in sustainable and plant-based nutrition continues to shape product innovation, food companies are incorporating de-oiled lecithin into a wider range of formulations to achieve desired functional performance without relying on synthetic additives. This trend is further supported by the 2025 IFIC Food & Health Survey, which indicates that 3% of Americans followed a plant-based diet in 2025[2]Source: International Food Information Council, "2025 Food & Health Survey," ific.org. This stable consumer base continues to drive investment and product development in the plant-based food and beverage market, thereby sustaining demand for de-oiled lecithin.

Technological advancements in lecithin extraction and purification

Technological advancements in lecithin extraction and purification are driving the growth of the global de-oiled lecithin market by enabling manufacturers to produce higher-purity ingredients with improved functional performance and consistency. Techniques such as enzyme-assisted processing, membrane filtration, low-temperature drying, and solvent optimization have increased phospholipid concentration while reducing residual oil content. This has resulted in products with enhanced dispersibility, flowability, and storage stability. These advancements enable de-oiled lecithin to meet the stringent quality standards required in food, nutraceutical, pharmaceutical, and cosmetic applications, where precision and uniformity are critical. Additionally, advanced processing technologies enable the production of non-GMO, organic, and allergen-free lecithin variants while improving production efficiency and reducing waste. As manufacturers continue to invest in modern extraction and refining methods, the availability of high-performance de-oiled lecithin is increasing, supporting its adoption across a broader range of value-added applications.

Increasing adoption of organic and non-GMO food manufacturing

The growing adoption of organic and non-GMO food production is driving the global de-oiled lecithin market, as food manufacturers prioritize naturally sourced ingredients that align with strict labeling standards and evolving consumer preferences. De-oiled lecithin, particularly derived from organic or identity-preserved non-GMO soy and sunflower, is extensively used as a natural emulsifier in bakery products, dairy alternatives, confectionery, infant nutrition, and nutritional supplements. Manufacturers are increasingly utilizing these specialty ingredients to enhance product transparency, meet certification standards, and differentiate premium product offerings. The rising demand for organic foods is highlighted in the 2025 IFIC Food & Health Survey, which indicates that 30% of Americans consider organic labels when purchasing food and beverages under food production-related claims[3]Source: International Food Information Council, "2025 Food & Health Survey," ific.org. This growing consumer emphasis on organic and non-GMO products is prompting manufacturers to expand certified ingredient sourcing, thereby driving sustained demand for de-oiled lecithin in global food and beverage applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock volatility in soy, sunflower, and canola | -1.5% | Global; most acute in Europe and South Asia | Short term (≤ 2 years) |

| Competition from alternative natural emulsifiers | -0.7% | North America and Europe; emerging in Asia-Pacific premium markets | Medium term (2-4 years) |

| Stringent quality and regulatory compliance requirements | -0.5% | Europe and North America primarily; extending to Asia-Pacific | Long term (≥ 4 years) |

| Limited processing capacity and technical limitations for high-purity de-oiled grades | -0.6% | Global; particularly acute in South Asia and emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock volatility in soy, sunflower, and canola

Feedstock volatility in soy, sunflower, and canola poses a significant restraint on the global de-oiled lecithin market, as these oilseeds are the primary raw materials for lecithin production. Fluctuations in crop yields, driven by adverse weather conditions, pest outbreaks, geopolitical conflicts, trade restrictions, and changing agricultural policies, can disrupt raw material availability and result in unpredictable price movements. These supply chain uncertainties increase production costs for lecithin manufacturers and complicate long-term procurement planning. Additionally, higher feedstock prices often reduce profit margins or compel manufacturers to pass increased costs to end users, impacting the competitiveness of de-oiled lecithin in price-sensitive markets. This challenge is particularly significant for producers of organic, non-GMO, and specialty lecithin grades, where certified raw material supplies are more limited, making the market more susceptible to fluctuations in agricultural production and global commodity prices.

Competition from alternative natural emulsifiers

Competition from alternative natural emulsifiers poses a significant restraint on the global de-oiled lecithin market. Manufacturers in the food, beverage, pharmaceutical, and cosmetic industries now have access to a wider range of ingredients that offer comparable functional properties. Alternatives such as gum arabic, acacia gum, guar gum, xanthan gum, pectin, mono- and diglycerides of plant origin, and modified starches are increasingly utilized for emulsification, stabilization, and texture enhancement in various formulations. These alternatives enable manufacturers to choose ingredients based on factors such as application requirements, cost, allergen considerations, regulatory compliance, and formulation compatibility, rather than relying exclusively on de-oiled lecithin. Furthermore, ongoing innovation in hydrocolloids and other plant-derived functional ingredients is enhancing their performance in clean-label and specialty food applications. This expanding competitive landscape limits the pricing power of de-oiled lecithin manufacturers and may reduce its adoption in cases where substitute emulsifiers provide similar functionality at a lower cost or offer greater formulation flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sunflower Demand Reshaping Soy's Long-Term Hold

Soy lecithin accounted for 57.44% of the market in 2025, driven by the abundant global availability of soybeans, a well-established oilseed processing infrastructure, and cost-efficient large-scale production. As a by-product of soybean oil refining, soy lecithin provides a reliable and economical source of high-quality phospholipids for applications in food, feed, pharmaceuticals, and industrial products. Its excellent emulsifying, dispersing, and instantizing properties make it widely utilized in bakery products, chocolate, confectionery, instant beverages, nutritional supplements, animal feed, and pharmaceutical formulations. The increasing demand for functional ingredients in processed foods, along with the availability of identity-preserved and non-GMO soybean varieties, has further reinforced its market position. Advancements in soybean processing technologies have improved product purity and functionality, enabling manufacturers to meet the growing demand for clean-label, high-performance, and value-added formulations while maintaining competitive production costs.

Sunflower lecithin is projected to be the fastest-growing source, with a CAGR of 8.84% between 2026 and 2031. Sunflower-derived de-oiled lecithin is gaining traction as manufacturers increasingly prioritize allergen-friendly, non-GMO, and clean-label ingredient solutions. Unlike soy lecithin, sunflower lecithin is naturally free from major soy allergens, making it suitable for products targeting consumers with dietary restrictions or preferences for soy-free formulations. It is extensively used in premium bakery products, plant-based foods, infant nutrition, dietary supplements, chocolate, cosmetics, and pharmaceutical applications, where ingredient transparency and natural sourcing are critical purchasing factors. Rising consumer demand for organic and minimally processed foods has encouraged food manufacturers to incorporate sunflower-derived lecithin into premium formulations, particularly in North America and Europe. Additionally, advancements in sunflower cultivation, oil extraction, and lecithin purification technologies have increased the availability of high-purity de-oiled sunflower lecithin, enabling manufacturers to deliver products with superior functionality while adhering to stringent regulatory and clean-label standards.

By Form: Powder Commands Share, Granules on the Rise

Powder lecithin accounted for 51.76% of the market value in 2025. Powder de-oiled lecithin is experiencing strong demand due to its excellent dispersibility, uniform particle size, extended shelf life, and ease of incorporation into dry formulations. Its low oil content enhances flowability and minimizes clumping, making it ideal for applications such as instant beverage mixes, bakery premixes, confectionery, dairy powders, protein supplements, infant nutrition, and pharmaceutical formulations. Manufacturers prefer the powdered form for its precise dosing, consistent blending, and compatibility with automated production systems, which improve manufacturing efficiency and product quality. The growing popularity of convenience foods, sports nutrition products, and functional ingredients has further driven the adoption of powder de-oiled lecithin. Additionally, its compatibility with clean-label, non-GMO, and organic formulations makes it a preferred ingredient for premium food and nutraceutical products, supporting market growth across various end-use industries.

Granule de-oiled lecithin is expected to grow at a CAGR of 8.65% between 2026 and 2031, driven by its superior handling characteristics, reduced dust formation, and controlled dissolution properties. These features make it suitable for both industrial processing and direct consumer use. The granular format offers improved storage stability and simplifies transportation and packaging, reducing material loss during handling. Increasing consumer demand for convenient nutritional ingredients and ready-to-mix health products has encouraged manufacturers to expand the use of granulated lecithin in retail and foodservice applications. Advances in granulation technology have further improved product consistency and functional performance, enabling granule de-oiled lecithin to meet the quality standards of food, pharmaceutical, and nutraceutical manufacturers while supporting efficient production processes.

By Nature: Non-GMO Commands Scale and Growth Simultaneously

Non-GMO lecithin accounted for 62.34% of the market in 2025 and is projected to be the fastest-growing nature sub-segment, with a CAGR of 8.75% through 2031. The strong growth of non-GMO de-oiled lecithin is driven by increasing demand from food manufacturers prioritizing ingredient transparency, clean-label positioning, and compliance with evolving consumer preferences and regulatory standards. It is extensively used in premium bakery products, confectionery, dairy alternatives, infant nutrition, dietary supplements, and plant-based foods, where non-GMO claims enhance brand value and consumer trust. Retailers and multinational food companies are expanding their certified non-GMO product portfolios to cater to health-conscious consumers, particularly in North America and Europe. Additionally, the growing adoption of organic and identity-preserved agricultural supply chains has improved the availability of certified non-GMO soy and sunflower lecithin. The ability of non-GMO de-oiled lecithin to provide effective emulsification while supporting premium labeling and export compliance is driving its adoption in high-value food, nutraceutical, and pharmaceutical applications.

GMO de-oiled lecithin continues to hold an accountable share of the global market due to its cost-effectiveness, consistent raw material supply, and large-scale production capabilities. The widespread cultivation of genetically modified soybeans ensures a stable and abundant feedstock for lecithin manufacturers, reducing procurement costs and minimizing supply chain disruptions. This reliable availability allows manufacturers to produce de-oiled lecithin at competitive prices, making it a preferred choice for high-volume applications. The well-established infrastructure for GMO soybean cultivation, crushing, and oil refining further supports efficient production and global distribution. In regions where GMO ingredients are widely accepted and regulatory frameworks permit their use, manufacturers favor GMO-derived de-oiled lecithin for its dependable functionality, scalable production, and cost advantages in mass-market formulations.

By Application: Food & Beverages Anchors Volumes, Pharmaceuticals Define the Next Margin Frontier

Food and beverages accounted for 54.55% of the application-segment value in 2025. This industry represents the largest application segment for de-oiled lecithin due to its multifunctional properties as a natural emulsifier, dispersing agent, instantizing agent, and release aid. Manufacturers widely use de-oiled lecithin in bakery products, chocolate, confectionery, dairy alternatives, instant beverages, powdered mixes, sauces, margarine, and processed foods to enhance texture, improve ingredient dispersion, extend shelf life, and maintain product consistency. The rising demand for clean-label, non-GMO, allergen-friendly, and plant-based foods has further driven its adoption as a substitute for synthetic emulsifiers. Its low oil content and excellent flowability make it particularly suitable for dry formulations and automated manufacturing processes. Additionally, ongoing innovation in functional foods, convenience products, and premium food formulations is expanding the use of de-oiled lecithin as manufacturers prioritize ingredients that combine processing efficiency with consumer-preferred natural labeling.

The nutraceutical and pharmaceutical sectors are the fastest-growing application areas for de-oiled lecithin, with a projected CAGR of 9.01% between 2026 and 2031. These sectors are emerging as significant growth drivers due to de-oiled lecithin's high phospholipid content, superior dispersibility, and compatibility with a wide range of active ingredients. It is extensively used in dietary supplements, protein powders, capsules, tablets, infant nutrition products, and pharmaceutical formulations to enhance ingredient blending, improve powder flow, stabilize formulations, and support efficient manufacturing processes. As global demand for preventive healthcare, personalized nutrition, and functional supplements continues to rise, manufacturers are increasingly seeking high-purity excipients that ensure consistent quality and regulatory compliance. De-oiled lecithin also plays a critical role in lipid-based drug delivery systems by enabling the formulation of stable and bioavailable products. Advances in purification technologies and the growing preference for natural, non-GMO, and allergen-friendly excipients are further accelerating its adoption in nutraceutical and pharmaceutical applications globally.

Geography Analysis

Asia-Pacific accounted for 34.13% of the global lecithin market value in 2025, with the fastest regional growth at a CAGR of 8.91% through 2031. The region's rapid growth in de-oiled lecithin sales is driven by expanding food manufacturing capacity, rising disposable incomes, and increasing consumption of processed, convenience, and functional foods. Key markets such as China, India, Japan, South Korea, and Australia are experiencing strong demand for bakery products, confectionery, instant beverages, infant nutrition, and dietary supplements, all of which extensively utilize de-oiled lecithin for its emulsifying and instantizing properties. Factors such as growing urbanization, the expansion of organized retail, and heightened awareness of clean-label and plant-based products are encouraging manufacturers to incorporate natural ingredients into new product formulations. Additionally, the region's large soybean production base, improving oilseed processing capabilities, and investments in pharmaceutical and nutraceutical manufacturing are expanding the application of de-oiled lecithin across various industries.

In North America, sales of de-oiled lecithin are driven by strong demand for clean-label, non-GMO, and plant-based food products. This trend is supported by a mature food processing industry and high consumer awareness of ingredient transparency. Food and beverage manufacturers are increasingly using de-oiled lecithin in bakery products, confectionery, dairy alternatives, nutritional beverages, and convenience foods to replace synthetic emulsifiers while enhancing product stability and texture. The region's expanding nutraceutical and pharmaceutical industries also contribute to demand, with high-purity lecithin being utilized in dietary supplements, protein powders, capsules, and drug formulations. Furthermore, the widespread availability of soybean processing infrastructure, growing adoption of organic-certified ingredients, and continuous investment in food innovation and functional nutrition products further bolster regional consumption of de-oiled lecithin.

Sales of de-oiled lecithin across Europe, South America, and the Middle East & Africa are supported by distinct regional demand patterns that collectively drive market growth. In Europe, stringent food quality regulations, strong consumer preference for organic, non-GMO, and allergen-friendly ingredients, and a well-established functional food industry are key factors driving the adoption of high-purity de-oiled lecithin. South America benefits from abundant soybean production and a robust edible oil processing sector, ensuring cost-effective raw material availability while supporting exports and expanding domestic food manufacturing. In the Middle East & Africa, rising urbanization, population growth, increasing consumption of packaged and convenience foods, and ongoing investments in food processing, bakery, confectionery, and nutritional products are creating new opportunities for de-oiled lecithin. Across all three regions, growing demand for natural emulsifiers, clean-label formulations, and value-added food and pharmaceutical products continues to support sustained market expansion.

Competitive Landscape

The global de-oiled lecithin market is characterized by a moderately concentrated competitive landscape. A few vertically integrated oilseed processors hold a significant share of global production capacity, while numerous specialty manufacturers compete in premium market segments. Large integrated producers benefit from control over oilseed sourcing, crushing, refining, and lecithin processing, ensuring a stable raw material supply, economies of scale, and cost-efficient production. In contrast, specialized manufacturers focus on high-purity de-oiled lecithin, customized phospholipid compositions, application-specific formulations, and certifications tailored for food, nutraceutical, pharmaceutical, and cosmetic applications. Recent industry consolidation and portfolio expansions have enhanced the capabilities of leading suppliers, enabling them to offer a broader range of soy-, sunflower-, and rapeseed-derived liquid, powdered, fractionated, and de-oiled lecithin products.

Competition in the de-oiled lecithin market is increasingly moving away from price-based strategies toward value-added differentiation. Large-scale manufacturers prioritize vertical integration, feedstock diversification, and supply chain resilience to mitigate the effects of agricultural price volatility. Meanwhile, specialty suppliers emphasize regulatory compliance, technical support, formulation expertise, and certified ingredient portfolios. Certifications such as non-GMO, organic, identity-preserved, ProTerra, and adherence to evolving environmental regulations have become critical competitive advantages, particularly for customers in premium food, infant nutrition, and pharmaceutical markets. Multi-feedstock sourcing strategies, including soy, sunflower, and rapeseed, enhance supply security, enabling manufacturers to maintain consistent product availability despite fluctuations in individual oilseed markets.

Growth prospects in the de-oiled lecithin market are concentrated in high-value specialty segments, particularly pharmaceutical-grade, sustainability-certified, and specialty phospholipid-based products. Investments in new processing facilities dedicated to premium sunflower lecithin production signal a gradual expansion of manufacturing capacity beyond traditional oilseed-processing regions. Additionally, advancements in enzymatic phospholipid modification technologies are facilitating the production of high-value compounds with enhanced functional and bioactive properties for pharmaceutical and nutraceutical applications. Strict pharmacopeial standards and quality specifications create significant barriers to entry in these premium segments, allowing manufacturers with advanced purification capabilities, regulatory expertise, and certified supply chains to achieve higher margins compared to those competing in commodity-grade de-oiled lecithin markets.

De-oiled Lecithin Industry Leaders

-

Cargill, Incorporated

-

Stern-Wywiol Gruppe GmbH and Co. KG

-

Archer-Daniels-Midland Company

-

American Lecithin Company

-

Bunge Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EBRD extended a EUR 13.5 million (approximately USD 15.78 million) loan to LeciForce, a newly established Polish company, to construct the first premium sunflower lecithin manufacturing facility in Poland, located in Lublin, and only the second such facility in Europe. Backed by an InvestEU guarantee, the plant transforms crude lecithin, a byproduct of vegetable oil processing, into higher-grade non-GMO lecithin for food, pharmaceutical, and cosmetic applications, strengthening European supply chain resilience and demonstrating scalable circular economy principles

- March 2026: Bunge completed its acquisition of International Flavors & Fragrances' (IFF) soy protein concentrate, lecithin, and soy crush businesses, incorporating IFF's Solec™ brand and a complete line of liquid, powdered, and fractionated lecithins from soy, sunflower, and rapeseed.

- August 2024: Bunge expanded its North American lecithin product portfolio by launching de-oiled soybean lecithin, complementing its existing range of crude, standard, and specialty lecithins sourced from soybean, sunflower, and rapeseed. The new offerings include de-oiled soybean lecithin in powder and granulated forms, offering customers more formulation options for various food and industrial applications.

Global De-oiled Lecithin Market Report Scope

| Soy |

| Sunflower |

| Rapeseed and Canola |

| Egg |

| Other Sources |

| Powder |

| Granules |

| GMO |

| Non-GMO |

| Food and Beverages |

| Animal Feed |

| Nutraceuticals and Pharmaceuticals |

| Personal Care and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Source | Soy | |

| Sunflower | ||

| Rapeseed and Canola | ||

| Egg | ||

| Other Sources | ||

| By Form | Powder | |

| Granules | ||

| By Nature | GMO | |

| Non-GMO | ||

| By Application | Food and Beverages | |

| Animal Feed | ||

| Nutraceuticals and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the de-oiled lecithin market?

The de-oiled lecithin market was valued at USD 255.64 million in 2025 and is expected to reach USD 275.41 million in 2026.

How fast is the de-oiled lecithin market expected to grow by 2031?

The de-oiled lecithin market is forecast to reach USD 405.72 million by 2031, growing at a CAGR of 8.06% during 2026-2031.

Which source segment leads de-oiled lecithin demand?

Soy led the de-oiled lecithin market by source with a 57.44% share in 2025, supported by its cost advantage and broad processing base.

Which de-oiled lecithin type is seeing the strongest momentum?

Non-GMO de-oiled lecithin held the largest share at 62.34% in 2025 and is also projected to be the fastest-growing nature segment at 8.75% CAGR through 2031.

Page last updated on: