Salad Dressing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

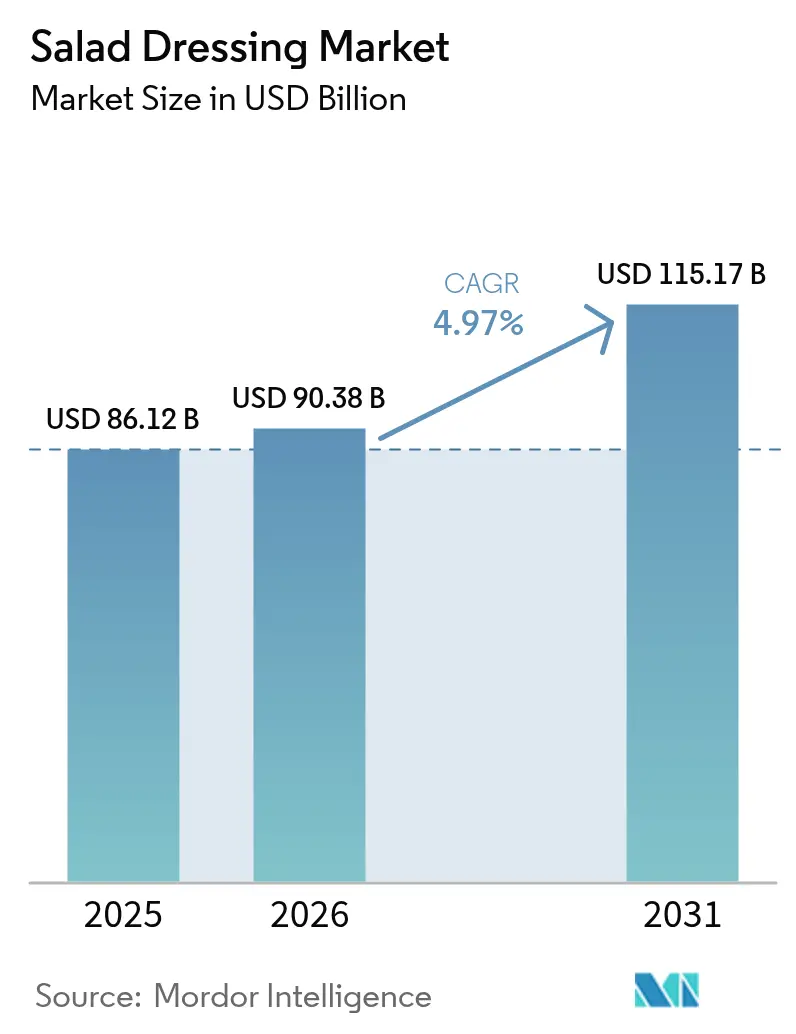

| Market Size (2026) | USD 90.38 Billion |

| Market Size (2031) | USD 115.17 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

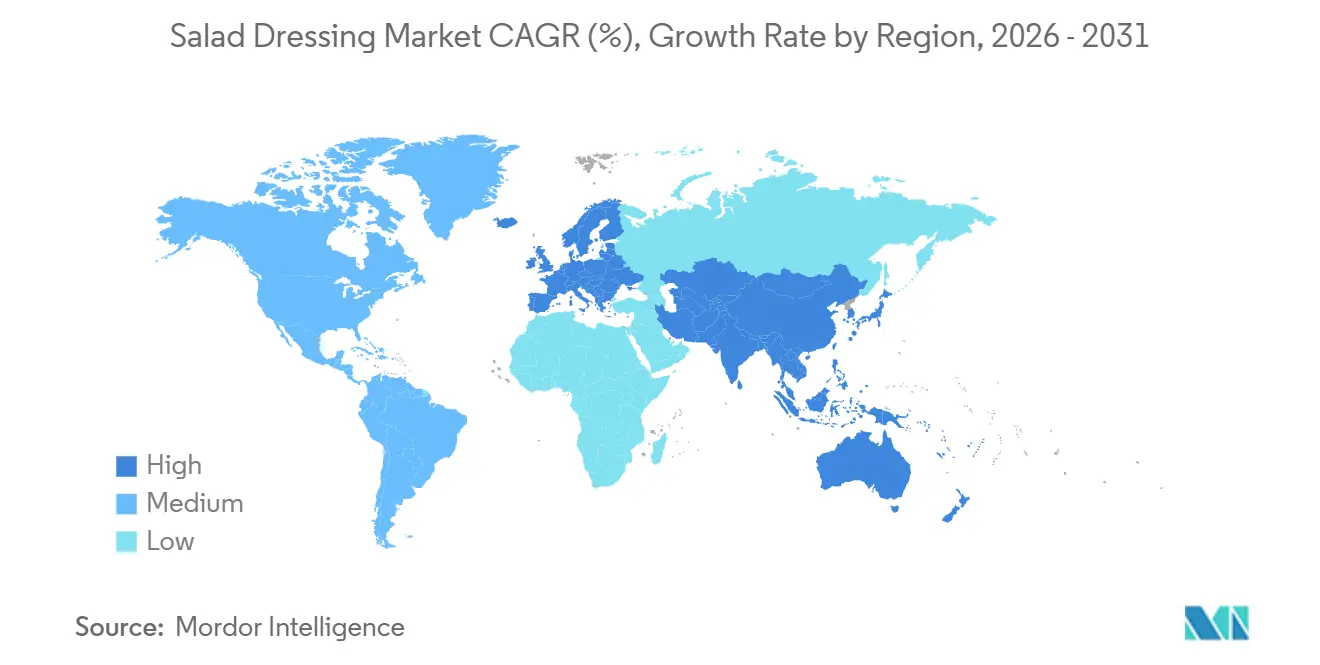

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Salad Dressing Market Analysis by Mordor Intelligence

The Salad Dressing Market size is projected to be USD 86.12 billion in 2025, USD 90.38 billion in 2026, and reach USD 115.17 billion by 2031, growing at a CAGR of 4.97% from 2026 to 2031. The market's growth is driven by premium clean-label launches, ethnic-fusion recipes, and plant-based formulations, which help stabilize prices despite fluctuations in soybean and palm oil costs. While private-label lines enhance retailer bargaining power, methods like high-pressure processing and cold-pressed oil extraction allow multinationals to sustain margins by extending shelf life without using synthetic preservatives. North America remains the primary revenue contributor, but the Asia-Pacific region, with a forecasted CAGR of 7.47%, shows significant growth potential as Western foodservice models expand in China, India, and Southeast Asia. Competition continues to rise, with organic dressings growing at an annual rate of 7.12%. Reflecting this trend, sales of organic groceries in Germany increased by 5.7% in 2024 compared to the previous year, according to Bund Ökologische Lebensmittelwirtschaft (BÖLW)[1]Source: Bund Ökologische Lebensmittelwirtschaft (BÖLW), "Ökologische Lebensmittelwirtschaft - Branchenreport 2025" boelw.de.

Key Report Takeaways

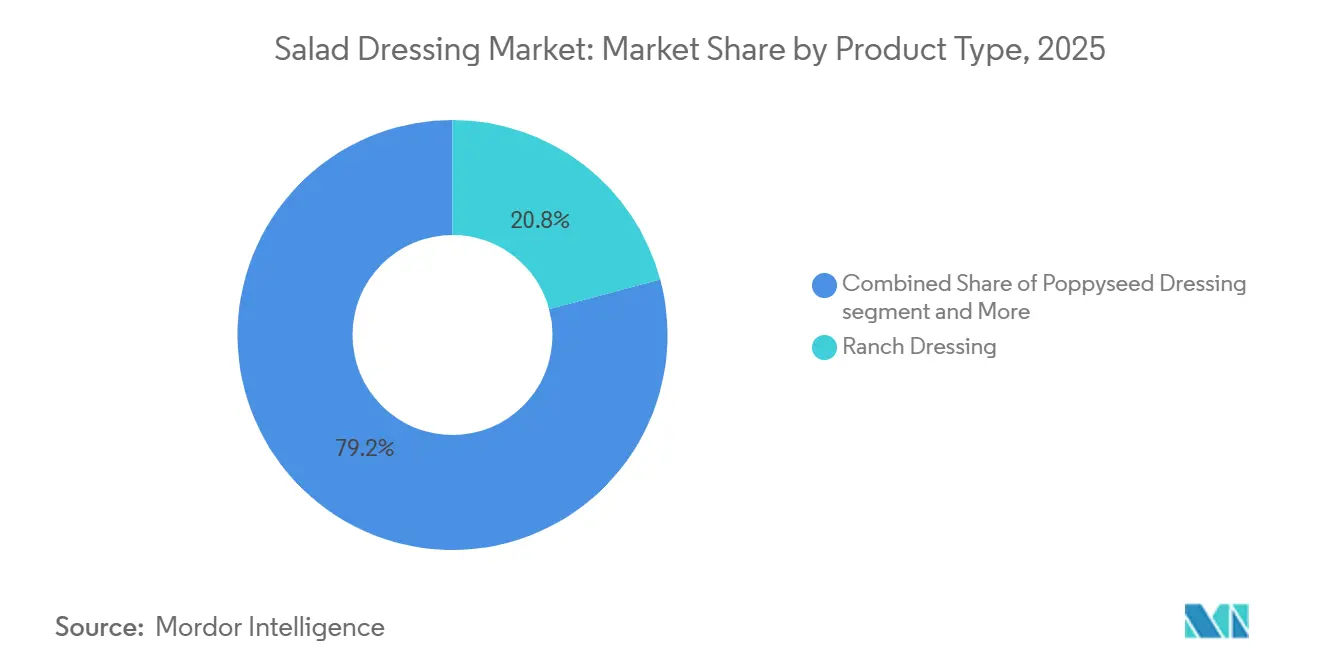

- By product type, ranch led with 20.84% of the salad dressing market share in 2025, whereas poppyseed is projected to post a 6.89% CAGR through 2031.

- By category, conventional dressings held 74.95% of the salad dressing market size in 2025, while organic lines are on track for 7.12% CAGR to 2031.

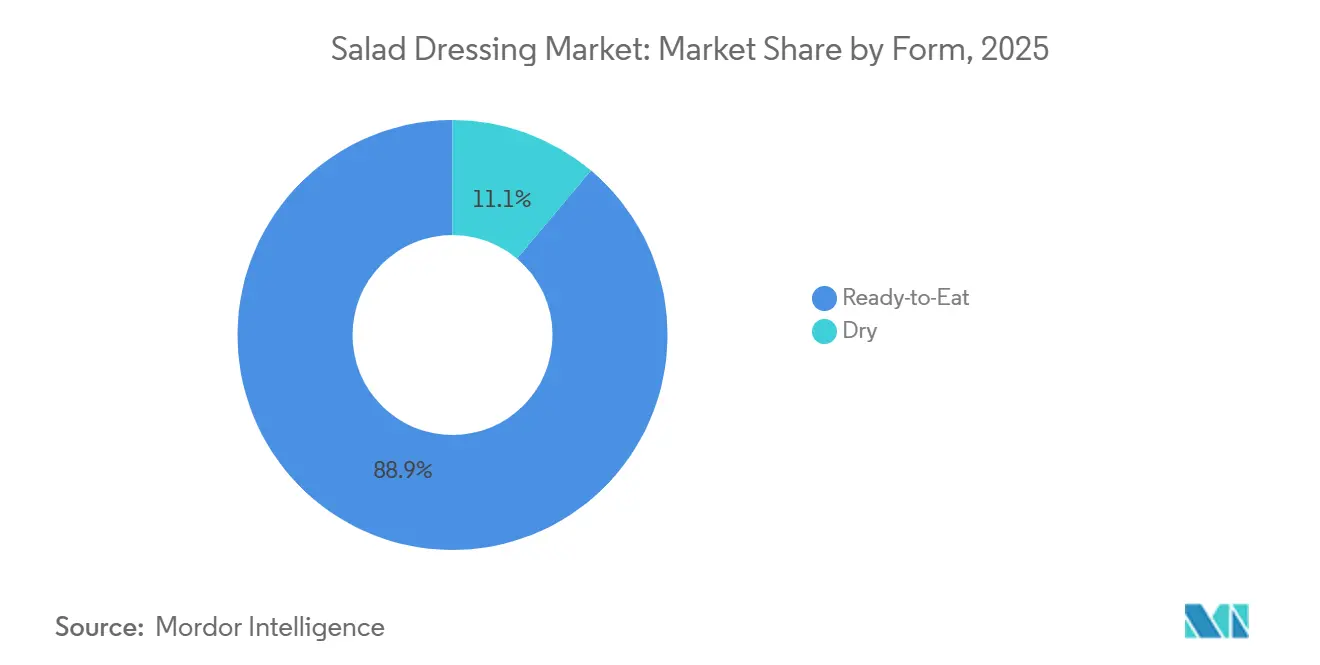

- By form, ready-to-eat accounted for 88.86% of the salad dressing market size in 2025; dry mixes are rebounding at a 6.38% CAGR.

- By distribution channel, retail captured 60.71% of the salad dressing market share in 2025; foodservice is recovering fastest at 6.46% CAGR.

- By geography, North America captured 43.02% of the salad dressing market share in 2025; Asia-Pacific is recovering fastest at 7.47% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Salad Dressing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of gourmet and artisanal salad dressings | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| Expansion of organic and plant-based salad dressing options | +1.2% | Global, with concentration in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for transparency and clean-label products | +1.0% | Global | Medium term (2-4 years) |

| Flavor innovation, including ethnic-inspired, gourmet, and fusion varieties | +0.8% | Global, early adoption in North America, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Technological advancements in product development and distribution | +0.6% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Growing consumer interest in global and regional flavor profiles | +0.7% | Global, strongest in North America, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing popularity of gourmet and artisanal salad dressings

In the premium tier, gourmet and artisanal positioning is taking center stage. Consumers are now willing to pay 20-30% more for craft-branded products. These products highlight small-batch production, heirloom ingredients, and compelling origin stories. This trend of premiumization is especially evident in North America and Western Europe. Here, specialty retailers and farmers' markets act as initial discovery platforms, paving the way for brands to transition into mainstream grocery outlets. Ingredient transparency has become a non-negotiable standard. Consumers are now meticulously examining product labels, favoring recognizable components like cold-pressed olive oil, aged balsamic vinegar, and hand-harvested herbs. They are quick to dismiss products containing modified starches or artificial emulsifiers. This shift is compelling mid-tier brands to either reformulate their offerings or face diminishing profit margins. Meanwhile, private-label premium lines from retailers such as Whole Foods and Trader Joe's are gaining traction. They achieve this by echoing artisanal qualities but at more accessible price points. While distribution initially leans towards direct-to-consumer and specialty channels, successful craft brands are increasingly entering co-packing agreements. This strategy allows them to secure supermarket shelf space without compromising their brand's integrity. The economic landscape is becoming polarized: ultra-premium craft SKUs are witnessing double-digit growth in niche markets, whereas mass-market conventional dressings are feeling the squeeze. These conventional brands are resorting to heightened promotions just to maintain their shelf presence.

Expansion of organic and plant-based salad dressing options

Organic and plant-based products have evolved from niche offerings into significant growth drivers. The organic market is expanding, driven by certifications such as USDA Organic and Non-GMO Project Verified, which appeal to health-conscious and environmentally aware consumers. For instance, a 2025 report from the India Brand Equity Foundation indicates that 60% of Indian consumers are willing to pay a premium for organic products[2]Source: India Brand Equity Foundation, "Future of Food Processing in India", ibef.org. Formulations using chickpea aquafaba, cashew cream, and avocado oil as emulsifiers meet both vegan demands and the growing preference for clean labels. Key product launches, such as Newman's Own's five-SKU organic line in January 2025 and Gotham Greens' Avocado Lime Ranch at Whole Foods, highlight retailers' dedication to these offerings. Regulatory frameworks, including USDA's National Organic Program and the EU's Organic Regulation 2018/848, mandate traceability and annual audits, creating entry barriers for smaller players lacking compliance capabilities. Additionally, plant-based products are increasingly tied to sustainability narratives, with brands emphasizing reduced water usage and lower greenhouse gas emissions compared to dairy-based dressings. This alignment supports corporate ESG objectives and attracts institutional buyers in foodservice channels. However, as organic products gain mainstream acceptance, the risk of commoditization grows. Differentiation is shifting from certifications alone to additional attributes such as regenerative agriculture sourcing, carbon-neutral logistics, and upcycled ingredients.

Rising demand for transparency and clean-label products

Consumer preferences for ingredient simplicity are driving changes in formulation strategies, with clean-label mandates playing a pivotal role. Consequently, manufacturers are limiting their ingredient options: they are replacing xanthan gum with chia or flax mucilage, opting for vinegar or citrus extracts instead of synthetic preservatives, and substituting titanium dioxide colorants with turmeric or beet powder. However, reformulating comes with significant challenges. For example, achieving shelf stability without potassium sorbate or calcium disodium EDTA requires investments in technologies like high-pressure processing or modified-atmosphere packaging, which can increase production costs by 5-8%. Regulatory developments further support this shift. The FDA's updated nutrition-facts-panel rules and voluntary front-of-pack guidelines promote simpler ingredient lists. Similarly, the EFSA's allergen-labeling directives emphasize the need for clear disclosure of potential cross-contaminants. Strategically, this creates a divided market: leading brands that invest in clean-label research and development gain access to premium pricing and prominent shelf placement. In contrast, brands that fail to adapt face the risk of delisting as retailers prioritize transparency. Smaller craft producers hold a competitive edge, as their batch-scale operations naturally align with minimal-processing claims. Meanwhile, multinational corporations face the challenge of retrofitting legacy facilities and managing complex SKU portfolios.

Flavor innovation, including ethnic-inspired, gourmet, and fusion varieties

Younger consumers' exposure to global cuisines through travel, social media, and multicultural urban environments is driving the rapid growth of ethnic and fusion flavor profiles as a key innovation trend. In May 2024, Kraft Heinz launched its Pure J.L. KRAFT line in Canada, offering 12 SKUs such as Pomegranate Zaatar, Miso Lime Ginger, and Moroccan Lemon. This initiative highlights a strategy to differentiate in a competitive market by blending influences from the Middle East, Asia, and North Africa. The commercial rationale is straightforward: ethnic dressings command a 15-20% price premium over traditional Italian or ranch variants, while ingredient costs increase only slightly when spices and aromatics are sourced from established commodity channels. Distribution patterns are also shifting. Specialty and natural-food retailers initially championed ethnic dressings, but mainstream grocers are now dedicating shelf space to meet growing demand from Hispanic, Asian, and Middle Eastern diaspora communities. However, the risk of authenticity dilution remains significant. Brands that adopt ethnic cues superficially, without ensuring ingredient integrity or cultural authenticity, risk consumer backlash. This has been evident in past controversies over "fusion" products perceived as inauthentic or culturally appropriative. Successful entrants collaborate with culinary experts, source region-specific ingredients, and focus on storytelling to educate consumers about flavor origins and traditional uses.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw material costs, especially vegetable oils and packaging | -0.8% | Global | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.4% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Increasing competition and market saturation | -0.5% | Global, most intense in North America and Western Europe | Long term (≥ 4 years) |

| High costs of sustainable and innovative packaging | -0.3% | Global, early impact in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile raw material costs, especially vegetable oils and packaging

Supply shortages and increasing demand are driving up vegetable oil prices. In 2024, U.S. olive oil imports soared to USD 3.28 billion, reflecting a significant 49.54% rise, primarily due to price inflation nearing USD 9,000 per ton, according to the World Integrated Trade Solution (WITS) database, a UN Comtrade initiative[3]Source: World Integrated Trade Solution (WITS) database, a UN Comtrade, "Import volume of olive oil worldwide", worldbank.org. Palm oil, a key ingredient in European and Asian formulations, traded between USD 1,050 and USD 1,200 per metric ton during the same period. Supply constraints were worsened by Indonesian export restrictions and Malaysian labor shortages. Canola oil, valued for its neutral taste and omega-3 content, experienced similar volatility. Canadian droughts reduced yields, while European rapeseed crops underperformed. Manufacturers with limited hedging options or short-term contracts faced margin compressions of 200-400 basis points during price spikes. This forced them to choose between absorbing costs, increasing retail prices, or switching to lower-cost alternatives that might compromise product quality. Glass bottles, though considered premium, are hindered by freight penalties and breakage risks, limiting their use to specialty channels. The industry's strategic response includes three key approaches: vertical integration into oil crushing or securing long-term supply agreements with crushers; adopting lightweight and alternative materials, such as flexible pouches instead of rigid bottles; and implementing dynamic pricing algorithms. These algorithms, initially used by private-label suppliers, adjust retail prices in near-real-time based on input-cost indices and are now being adopted by branded manufacturers.

Stringent food safety and labeling regulations

Compliance costs are increasing under the FDA's Food Safety Modernization Act, which requires condiment manufacturers to implement hazard-analysis documentation, preventive-controls plans, and supplier verification. Annual compliance costs range from USD 50,000 to 150,000 for mid-sized facilities, with multi-site operations incurring even higher expenses. Similarly, the EFSA's revised allergen-labeling directives mandate clear identification of 14 major allergens and precautionary statements for potential cross-contact. These changes often necessitate product reformulation or segregated production lines, raising manufacturing costs by 3-5%. Exporters face additional challenges. U.S. manufacturers targeting European markets must adhere to both FDA and EFSA standards, while those entering the Asia-Pacific region must comply with regulations such as China's GB 2760 food-additive standards and India's FSSAI labeling requirements. This complex regulatory environment drives consolidation pressures. Larger manufacturers can distribute compliance costs across extensive SKU portfolios and utilize in-house regulatory teams. In contrast, smaller players must either limit their distribution to domestic markets and select retail channels or seek acquisition by larger companies that can absorb compliance costs. Additionally, the regulatory framework hinders innovation. Introducing new ingredients or processing methods requires premarket notifications and safety assessments, delaying product launches by 6-12 months. This delay puts startups at a disadvantage compared to established brands with strong regulatory experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ranch Dominance Meets Poppyseed Momentum

In 2025, ranch dressing secured a dominant 20.84% share, solidifying its pivotal role in North America's foodservice and retail sectors. Beyond being a salad staple, ranch has become the go-to dipping sauce for chicken wings, pizza, and vegetables. Its enduring popularity can be attributed to its versatility and widespread appeal; ranch transcends age, income, and regional divides, making it a favored choice for cautious consumers. Retailers, keen on swift inventory turnover, have also made ranch a staple SKU. Yet, the segment grapples with commoditization. As private-label ranches close the taste gap with established brands, margins tighten. This has pushed market players to seek differentiation, turning to organic certifications, unique buttermilk sourcing claims, or even ethnic fusions like the Korean gochujang-ranch. Meanwhile, Italian dressing, once the second-largest segment, is losing ground. Consumers now view it as outdated and overly acidic, leading to a shift towards creamier, herb-centric profiles. French dressing, with its sweet-tangy taste, finds itself in a dwindling niche, primarily in institutional foodservice catering to children's menus. Balsamic dressing, while maintaining its foothold in premium channels thanks to the health benefits of aged balsamic vinegar and Mediterranean diet ties, faces stiff competition from balsamic glazes and reductions, which pack a more intense flavor punch.

Poppyseed dressing is emerging as the surprise success story, with projections of a 6.89% CAGR growth rate through 2031. Its ascent from a regional specialty to mainstream prominence is driven by gourmet repositioning and innovative ethnic fusions. A testament to this trend is Kraft Heinz's Pure J.L. KRAFT line, which has introduced an Orange Turmeric Poppyseed variant. This blend marries the traditional sweetness of poppyseed with the anti-inflammatory benefits of turmeric and a zesty citrus touch. The dressing's visual allure, especially its speckled look, resonates on social media, making it a hit among younger consumers who value Instagram-worthy presentations. This shift signals a strategic pivot for manufacturers: while they're trimming back on underperforming SKUs like French and Thousand Island, they're channeling investments into poppyseed, ethnic-inspired, and functional variants that not only command premium prices but also appeal to a younger, health-conscious demographic.

By Category: Conventional Scale Versus Organic Growth

In 2025, conventional dressings held a dominant 74.95% market share, supported by their affordability, extensive availability, and well-established taste profiles that appeal to mainstream consumers. These dressings benefit from significant scale advantages: major manufacturers use their purchasing power to secure favorable deals on oil and packaging, operate high-speed production lines to reduce per-unit costs, and negotiate prime shelf placements through strategic partnerships with leading retailers. Promotional efforts further enhance the appeal of conventional dressings: temporary price cuts and multi-buy deals encourage impulse purchases, particularly during the summer grilling season when salad consumption peaks. However, the segment faces challenges as younger consumers increasingly prioritize ingredient transparency and sustainability. They perceive conventional dressings, often containing synthetic preservatives, high-fructose corn syrup, and unclear “natural flavors”, as inconsistent with their wellness goals.

Organic dressings, while accounting for only 25.05% of the 2025 market volume, are growing at a strong 7.12% CAGR. This growth is driven by health-conscious and environmentally aware consumers who are influenced by USDA Organic and Non-GMO Project Verified certifications. The growth of organic dressings is concentrated in natural-food retailers such as Whole Foods and Sprouts, as well as in premium supermarket sections. In these spaces, organic dressings not only have dedicated shelf space but also command a 30-50% price premium over conventional options. In March 2025, Earthbound Farm launched three organic salad kits featuring avocado oil dressings, combining organic greens with dressings to boost margins and simplify meal preparation. However, producing organic dressings involves challenges: sourcing organic vegetable oils requires verified non-GMO feedstock and separate processing, increasing input costs by 15-25% compared to conventional oils. Manufacturers often absorb a significant portion of these costs to remain competitive. The competitive landscape is shifting: mainstream brands are introducing organic product lines to protect their market share, while dedicated organic brands face margin pressures due to rising competition and retailer demands for promotional support. A key opportunity lies in hybrid positioning: brands that combine organic certifications with additional features, such as plant-based formulations, ethnic flavors, or functional ingredients like probiotics and omega-3s, can stand out and justify premium pricing in the increasingly competitive organic market.

By Form: Ready-to-Eat Convenience Anchors Market

In 2025, ready-to-eat dressings held a commanding 88.86% market share, driven by consumers' increasing demand for convenience, consistent quality, and extended shelf life, which helps reduce waste. This segment includes both refrigerated and shelf-stable formats. Refrigerated dressings are often perceived as fresher and more premium due to their shorter ingredient lists and avoidance of high-temperature processing. In contrast, shelf-stable variants offer advantages in distribution and lower cold-chain costs. However, advancements in technology are narrowing the gap between the two. For example, high-pressure processing enables shelf-stable dressings to deliver refrigerated-quality flavor and nutrient retention without thermal pasteurization. Brands like Gotham Greens are leveraging this technology to distribute fresh-tasting dressings in ambient grocery aisles. Single-serve ready-to-eat formats are the fastest-growing subsegment, catering to on-the-go consumers and those seeking portion control in foodservice. The margin structure favors ready-to-eat formats, as they command per-ounce prices 2-3 times higher than bulk bottles. Despite rising input costs, the convenience premium remains largely intact, protecting manufacturers from raw material price volatility.

Although dry dressing mixes represented only 11.14% of the 2025 volume, they are experiencing a resurgence with a 6.38% CAGR. Foodservice operators are driving this growth, attracted by benefits such as portion control, reduced cold-chain logistics costs, and longer shelf life that minimizes spoilage. This growth is particularly evident in institutional settings, including healthcare facilities, schools, and corporate cafeterias. In these environments, centralized kitchens efficiently reconstitute dry mixes with oil and water, achieving cost savings of 30-40% compared to ready-to-eat alternatives. Additionally, dry mixes appeal to campers, emergency-preparedness consumers, and bulk-cooking enthusiasts who prioritize shelf stability and space efficiency over convenience. However, achieving sensory parity remains a challenge, as dry mixes have historically lagged behind ready-to-eat dressings in texture and flavor. Innovations in spray-drying and encapsulation technologies are helping to close this gap. The competitive landscape for dry formats is less crowded, as most innovation capital is directed toward the premiumization of ready-to-eat options. This creates opportunities for brands willing to invest in formulation research and development and foodservice distribution. Regulatory requirements are also simpler for dry mixes, as their lack of moisture reduces microbial risks and eliminates the need for preservatives. This aligns well with clean-label trends. Strategically, ready-to-eat formats are expected to maintain their dominance in retail due to consumer demand for convenience. Meanwhile, dry mixes are carving out niches in foodservice, bulk, and specialty channels, where cost and shelf stability take precedence over convenience.

By Distribution Channel: Retail Scale Meets Foodservice Recovery

In 2025, retail channels represented 60.71% of the volume, with supermarkets and hypermarkets leading the way, collectively holding an significant share in the U.S. market. This dominance provides mainstream brands with unmatched reach and frequency. Convenience stores are establishing a niche, particularly for single-serve formats aimed at on-the-go consumers, though their higher per-unit costs limit broader adoption. By 2024, online retail captured 13.5% of the U.S. retail volume, driven by the pandemic's acceleration of e-commerce and the convenience of home delivery. Specialty retailers, such as natural-foods stores and gourmet shops, play a significant role in the premium and organic segments. They serve as discovery platforms for craft brands, helping them scale into mainstream grocery. Margin dynamics vary: online channels achieve higher realized prices due to reduced promotional activity but face challenges like fulfillment costs and breakage risks. Supermarkets, while driving volume, operate on thinner margins due to promotional pressures and slotting fees.

Foodservice channels are recovering, with a 6.46% CAGR projected through 2031, outpacing retail growth. This recovery is supported by institutional segments like healthcare and education, which are experiencing 2.0% real growth, and the expansion of quick-service restaurants. Fast-casual chains, which are growing, play a key role in dressing innovations. They are at the forefront of introducing ethnic-inspired and premium dressings in grain bowls and vegetable-focused dishes, creating demand for retail equivalents. However, the foodservice recovery is uneven: full-service restaurants remain below pre-pandemic levels due to labor shortages and higher menu prices. Meanwhile, institutional channels benefit from return-to-office policies and the resumption of in-person education. This scenario underscores the need for a dual-channel strategy: manufacturers must balance retail scaling with foodservice innovation. Foodservice drives brand discovery and premiumization, which retail channels can then monetize. Packaging preferences differ significantly: foodservice prioritizes bulk formats like gallon jugs and bag-in-box to reduce per-serving costs, while retail focuses on consumer-friendly bottles and squeeze formats that command premium prices. Manufacturers with flexible production capabilities are well-positioned to serve both channels efficiently, avoiding capacity constraints or excessive SKU proliferation.

Geography Analysis

In 2025, North America accounted for a significant 43.02% market share, supported by established consumption patterns, a strong foodservice infrastructure, and its history as the origin of ranch dressing and other iconic formats. While Canada's salad dressing market is smaller, it is growing at a faster pace, driven by multicultural urban centers such as Toronto, Vancouver, and Montreal, where ethnic-inspired dressings appeal to diverse populations. Mexico's market is expanding due to the growth of Western foodservice chains and urbanization, which is increasing the demand for convenience foods. However, traditional lime-chili condiments continue to dominate home cooking. The regulatory environment is evolving, with the FDA's updated nutrition-facts-panel rules and voluntary front-of-pack guidelines promoting simplified ingredient lists. Additionally, state-level regulations like California's Proposition 65 require disclosure of trace chemicals, such as lead and cadmium, which may be present in certain spices and herbs.

Europe's market is defined by regional diversity, strong organic adoption, increasing salad consumption, and a shift toward premium products. Germany, France, Italy, and Spain collectively contribute a significant share of European volume, with each market showcasing distinct preferences: Germany favors yogurt-based and herb-focused dressings; France prefers vinaigrettes featuring Dijon mustard and shallots; Italy highlights the simplicity of balsamic vinegar and olive oil; and Spain is increasingly adopting Mediterranean-fusion styles. However, the regulatory framework is stringent. EFSA's allergen-labeling requirements and the EU's Single-Use Plastics Directive impose significant compliance costs, particularly for smaller manufacturers. Furthermore, the EU Organic Regulation 2018/848 enforces strict traceability and annual audits, creating barriers to entry for new players.

Asia-Pacific is the fastest-growing region, with a 7.47% CAGR projected through 2031. This growth is driven by urbanization, rising disposable incomes, and the increasing adoption of Western foodservice in countries such as China, India, Southeast Asia, and Australia. The online grocery sector is expanding rapidly, with a CAGR of approximately 30%. Platforms like Alibaba's Freshippo, JD.com, and India's Blinkit are leading this growth by offering fast delivery and curated selections that emphasize premium and imported dressings. Kewpie Corporation, Japan's leading producer of mayonnaise and dressings, opened its second U.S. production facility in Tennessee in May 2025. This expansion tripled its U.S. production capacity to serve both North and South America while also supporting growth in Thailand and Indonesia to meet rising demand in the Asia-Pacific region. Kewpie's strategy focuses on localization, including adapting products to local tastes in China, introducing region-specific offerings like fat-free dressings for noodle dishes, and obtaining halal certification for all products in Indonesia to cater to Muslim-majority markets. Although South America and the Middle East and Africa are smaller markets, they show considerable potential. Brazil and Argentina are gradually adopting Western salad consumption patterns as their urban middle classes grow. Meanwhile, the UAE and Saudi Arabia benefit from their expatriate populations and the expansion of foodservice in hospitality and quick-service sectors.

Competitive Landscape

The salad dressing market is moderately fragmented, with a blend of multinationals, regional specialists, and craft producers coexisting. Unilever Plc, The Kraft Heinz Company, and Ken’s Foods Inc. dominate a significant portion of the market, reflecting a moderate level of concentration. Hellmann’s is actively expanding its product portfolio by introducing flavored mayonnaise to enhance its visibility on retail shelves, while Hidden Valley Ranch is strategically strengthening its presence in the foodservice sector by forming co-branding partnerships with prominent pizza chains.

The mergers and acquisitions landscape is witnessing heightened activity, with flavor houses increasingly pursuing vertical integration to streamline operations and enhance supply chain efficiencies. A notable example is Advent International's planned acquisition of Sauer Brands in February 2025, a strategic initiative aimed at securing bottling capabilities and achieving synergies in spice supply. Simultaneously, private-equity firms are capitalizing on opportunities presented by distressed artisanal brands, attracted by their premium positioning in the market and their ability to cultivate dedicated customer bases. Technological advancements are also reshaping the competitive dynamics. For instance, McCormick’s AI-powered recipe generator has achieved a 33% reduction in research and development timelines, enabling the company to adapt more swiftly to evolving consumer preferences and emerging trends.

Regional players are gaining traction by emphasizing authenticity in their offerings and leveraging direct-to-consumer sales channels, thereby bypassing the costs associated with traditional slotting fees. On the other hand, larger companies are capitalizing on their extensive distribution networks and cost efficiencies to maintain a competitive edge. This evolving dynamic indicates a gradual consolidation of the competitive landscape, particularly in the saturated Western markets. However, there remains ample opportunity for niche innovators to carve out a space by focusing on unique flavor profiles and sustainability initiatives within the salad dressing sector.

Salad Dressing Industry Leaders

-

Unilever PLC

-

The Kraft Heinz Company

-

Ken’s Foods Inc.

-

T. Marzetti Company

-

Kewpie Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Lifeway Foods, a leader in promoting gut health in the U.S., has launched a new probiotic salad dressing, building on its success in popularizing kefir in the American market.

- August 2025: Dole launched its Apple Harvest Premium Salad Kit as part of Dole's seasonal fall product lineup. The kit featured a spring mix base, aged cheddar cheese, brown sugar pecans, and an apple cider vinaigrette. This product responded to the consumer's desire for unique, restaurant-inspired salad experiences at home. The launch was complemented by refreshed packaging across Dole's existing product lines.

- April 2025: Hidden Valley launched seven new ranch flavor varieties alongside a redesigned "Easy Squeeze" bottle with a new, more precise applicator. This release catered to consumer demand for flavor innovation and customization. The new offerings included both widely distributed flavors and retail exclusives to drive foot traffic for specific chains.

- January 2025: Stonewall Kitchen launched classic dressings, with an aim to expand the company's offerings beyond its gourmet, specialty items by providing everyday, familiar dressing flavors. The new dressings released were French, Blue Cheese, Ranch, and Thousand Island.

Global Salad Dressing Market Report Scope

Salad dressing is a sauce that combines mayonnaise or vinaigrette with other ingredients to make a topping or flavor that can be incorporated into salad greens or salad items being prepared. The salad dressing market is segmented by product type, category, form, distribution channels, and geography. By product type, the market is segmented into balsamic, ranch, Italian, poppyseed, French, and other. By category, the market is segmented into conventional and organic. By form, the market is segmented into dry and ready-to-eat. By distribution channel, the market is segmented into foodservice and retail. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD) and volume (tons).

| Balsamic Dressing |

| Ranch Dressing |

| Italian Dressing |

| Poppyseed Dressing |

| French Dressing |

| Other Product Types |

| Conventional |

| Organic |

| Dry |

| Ready-to-Eat |

| Foodservice | |

| Retail | Hypermarkets / Supermarkets |

| Convenience Stores | |

| Specialty Retailers | |

| Online Retail | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Balsamic Dressing | |

| Ranch Dressing | ||

| Italian Dressing | ||

| Poppyseed Dressing | ||

| French Dressing | ||

| Other Product Types | ||

| By Category | Conventional | |

| Organic | ||

| By Form | Dry | |

| Ready-to-Eat | ||

| By Distribution Channel | Foodservice | |

| Retail | Hypermarkets / Supermarkets | |

| Convenience Stores | ||

| Specialty Retailers | ||

| Online Retail | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Salad dressing market?

The Salad dressing market size stood at USD 90.38 billion in 2026.

How fast is global demand for salad dressings expected to grow?

Industry revenue is projected to rise at a 4.97% CAGR from 2026 to 2031.

Which product type leads category revenue today?

Ranch dressings command 20.84% Salad dressing market share thanks to broad menu versatility.

Which segment is expanding most quickly?

Poppyseed variants are forecast to achieve a 6.89% CAGR through 2031.

Page last updated on: