Identity Threat Detection and Response (ITDR) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

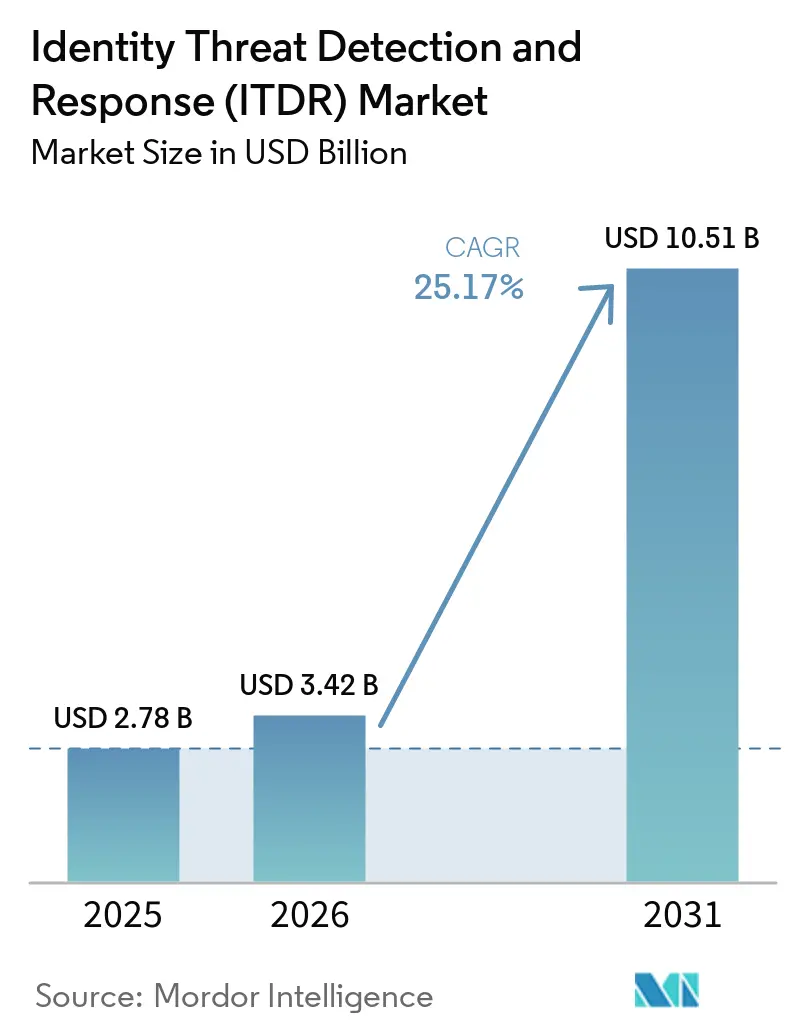

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 10.51 Billion |

| Growth Rate (2026 - 2031) | 25.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Threat Detection and Response (ITDR) Market Analysis by Mordor Intelligence

The identity threat detection and response (ITDR) market size is expected to increase from USD 2.78 billion in 2025 to USD 3.42 billion in 2026 and reach USD 10.51 billion by 2031, growing at a CAGR of 25.17% over 2026-2031. Stolen credentials now appear in 39% of breaches across the attack chain, which keeps identity protection at the center of enterprise security budgets in 2026. Microsoft reported a 32% rise in identity-based attacks in the first half of 2025, with more than 97% of those incidents driven by mass password-guessing activity, underscoring why the identity threat detection and response (ITDR) market is moving from optional tooling to a core control layer. Demand is also rising because remote work, SaaS expansion, and machine identities have increased the number of access points that security teams must monitor simultaneously. Europe is adding urgency, as Germany’s NIS2 implementation took effect in December 2025, pushing identity controls and multi-factor authentication into a broader set of regulated environments. The identity threat detection and response (ITDR) market is also being shaped by pressure to consolidate and integrate platforms, as enterprises seek stronger identity visibility without adding more disconnected tools to IAM, PAM, SIEM, and XDR environments.

Key Report Takeaways

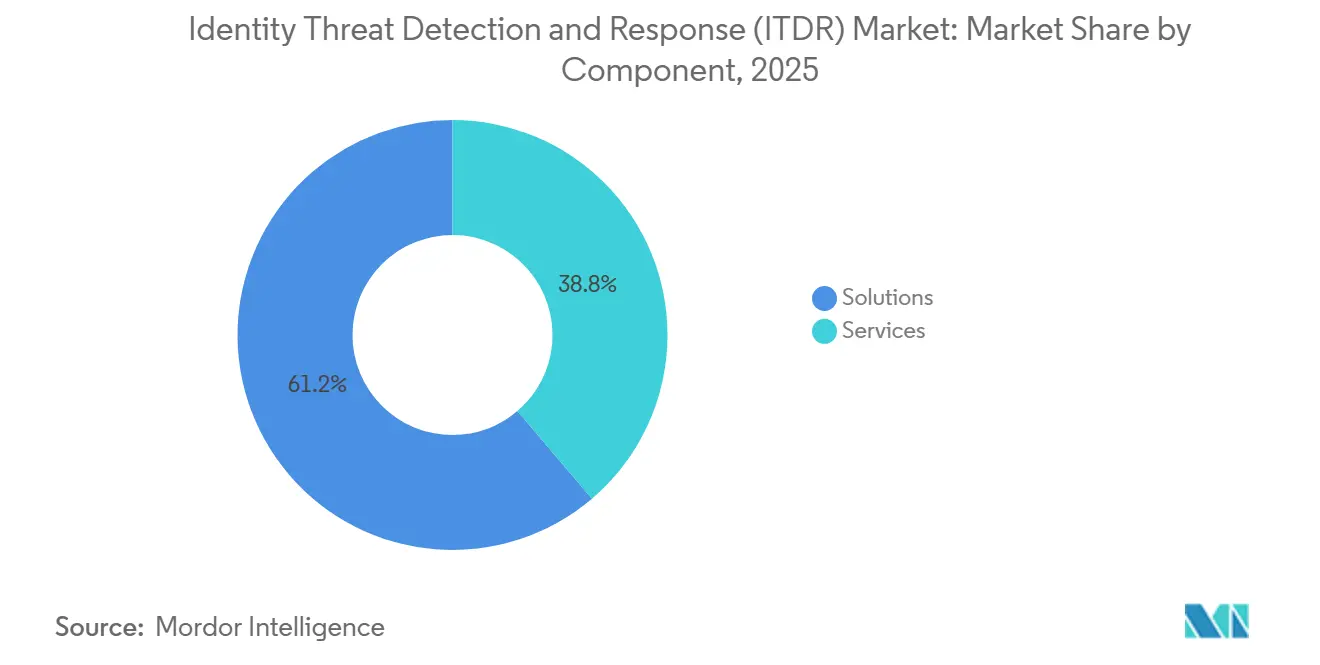

- By component, solutions held a 61.23% share of the identity threat detection and response (ITDR) market in 2025, while services are projected to grow at a 26.28% CAGR through 2031.

- By security type, identity threat detection led with 27.19% share of the identity threat detection and response market in 2025, while identity security posture management is forecast to expand at a 26.39% CAGR through 2031.

- By deployment, cloud accounted for 54.16% share of the identity threat detection and response (ITDR) market in 2025, while hybrid is projected to grow at a 26.50% CAGR through 2031.

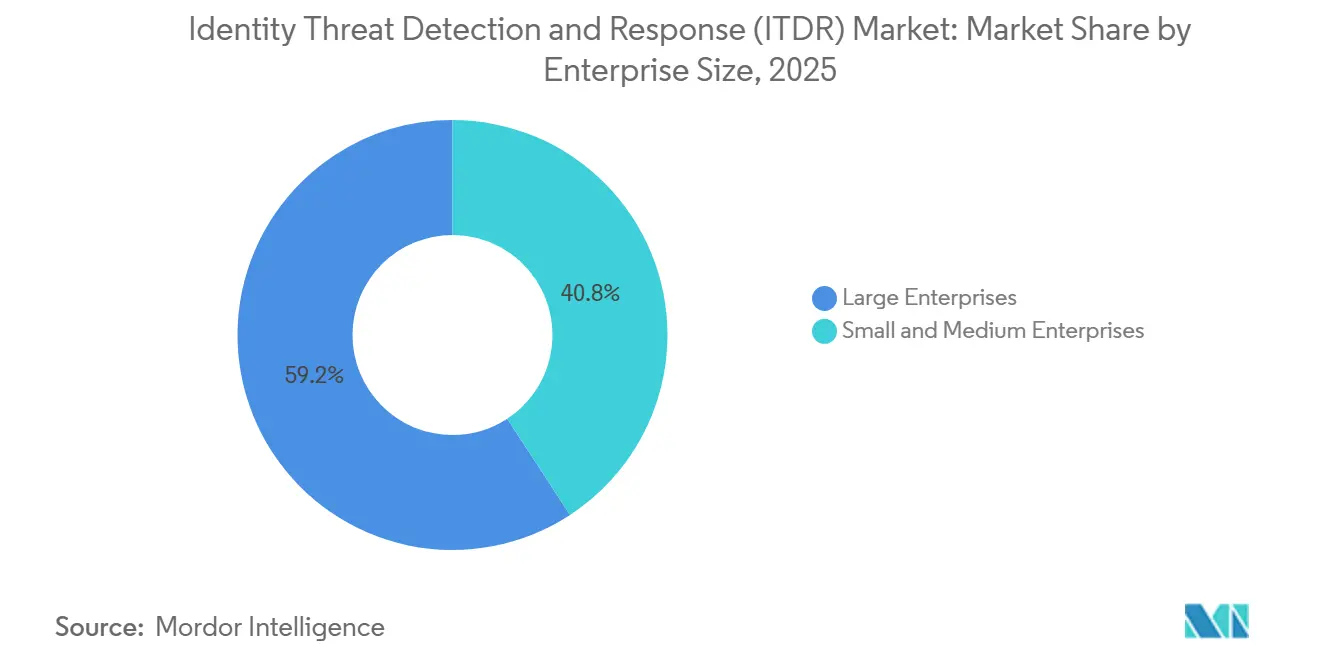

- By enterprise size, large enterprises held 59.21% share of the ITDR market in 2025, while SMEs are expected to advance at a 26.61% CAGR through 2031.

- By end-user industry, BFSI held 16.24% share of the identity threat detection and response market in 2025, while healthcare and life sciences are forecast to grow at a 26.72% CAGR through 2031.

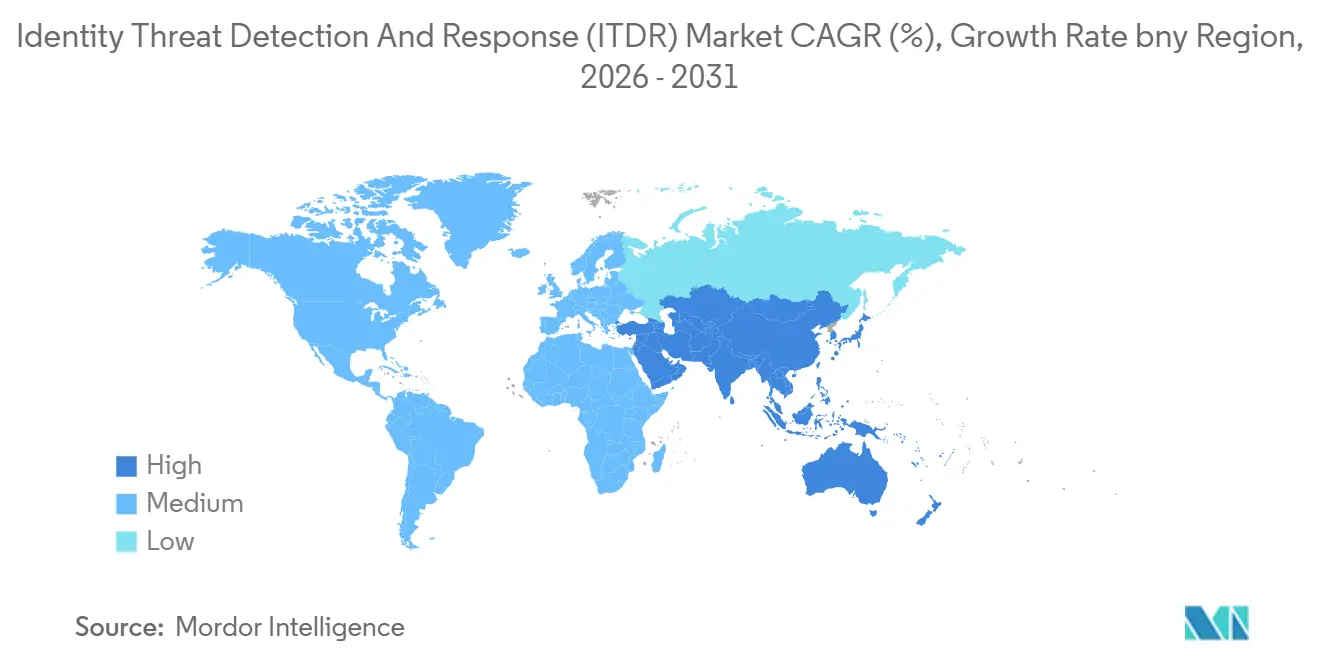

- By geography, North America accounted for 32.18% share of the ITDR market in 2025, while Asia-Pacific is projected to expand at a 26.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Identity Threat Detection and Response (ITDR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise In Identity-Based Attacks and Credential Abuse | +6.5% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Expansion of Remote and Hybrid Work Identity Sprawl | +5.5% | Global, with APAC and North America as primary markets | Medium term (2-4 years) |

| Cloud Identity Fragmentation Across SaaS and IaaS Environments | +4.8% | Global, especially North America, Europe, and APAC | Medium term (2-4 years) |

| Zero Trust Program Expansion across Large Enterprises | +4.2% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Board-Level Pressure for Identity Telemetry And Measurable Control Coverage | +2.8% | Global, skewed toward large-enterprise markets | Long term (≥ 4 years) |

| AI-Augmented Attack Simulation and Exposure Prioritization | +2.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Identity-Based Attacks and Credential Abuse

Credential abuse remains the most direct growth driver for the identity threat detection and response (ITDR) market, as attackers continue to use valid accounts to move through enterprise systems. Verizon reports that stolen credentials appear in 39% of breaches across the full attack chain in 2026, indicating that identity is often the initial entry point and the subsequent path of attack.[1]Verizon, “2026 Data Breach Investigations Report,” Verizon, verizon.com Sophos found in Q1 2026 that 71% of organizations experienced at least 1 identity-related breach in the prior 12 months, and the mean recovery cost per incident reached USD 1.64 million. The same study found that identity compromise was the primary delivery path in 67% of ransomware incidents, while API keys, service accounts, and orphaned credentials accounted for 41% of identity breaches. As automated attacks keep accelerating and non-human identities keep growing, buyers in the identity threat detection and response market are placing greater value on continuous monitoring, rapid validation, and automated response actions that act before a human analyst can review every alert.

Expansion of Remote and Hybrid Work Identity Sprawl

Remote and hybrid work have left the identity threat detection and response (ITDR) market with a much broader set of user accounts, devices, temporary permissions, and partner connections to monitor. In many enterprises, each onboarding cycle now creates tokens, cookies, and short-term access grants that remain active longer than intended, increasing the amount of identity noise defenders must sort through. Netwrix reported that 46% of organizations experienced cloud account compromise in 2025, up from 16% in 2020, which closely tracks the shift toward more distributed work and more cloud-dependent access patterns.[2]Netwrix, “2025 Hybrid Security Trends Report,” Netwrix, netwrix.com This change matters because remote work not only moved employees outside the office but also pushed identity checks across more directories, applications, and unmanaged sessions. That is why the identity threat detection and response (ITDR) market is seeing stronger demand for

Cloud Identity Fragmentation Across SaaS and IaaS Environments

The identity threat detection and response (ITDR) market is also expanding because SaaS and IaaS adoption has split enterprise identity across many separate control points. A single organization can now run cloud identity providers, legacy Active Directory, workload credentials, and application-level privilege models simultaneously, yet none of them provides a complete picture on its own. Netwrix data on cloud account compromise shows how quickly this exposure has grown over a five-year period, which helps explain why buyers are looking beyond directory-native tools. Germany’s NIS2 implementation adds another layer of pressure by bringing identity controls, authentication discipline, and audit readiness into a broader compliance perimeter. In practice, the ITDR market benefits because buyers need platforms that can read signals from multiple identity providers simultaneously and close blind spots that remain hidden within separate cloud tenants.

Zero Trust Program Expansion Across Large Enterprises

Zero Trust programs are giving the identity threat detection and response (ITDR) market a durable, long-term demand base because identity sits at the center of modern enforcement policy. CISA’s Zero Trust Maturity Model places identity as the first and highest-leverage pillar, which has made identity visibility and control a more formal part of both public-sector and private-sector security planning.[3]Cybersecurity and Infrastructure Security Agency, “Zero Trust Maturity Model,” CISA, cisa.gov Once enterprises move from Zero Trust planning to daily execution, they need to continuously verify users, devices, and access behavior rather than relying on one-time access reviews. That requirement aligns closely with ITDR tools, which connect identity policy with behavioral signals and response workflows in near real time. As large organizations scale Zero Trust programs across cloud, on-premises, and partner environments, the identity threat detection and response market benefits from spending now linked to broader architecture programs rather than stand-alone point-tool purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across IAM, PAM, SIEM, And XDR Stacks | -3.8% | Global, particularly pronounced in large enterprises with legacy IAM | Short term (≤ 2 years) |

| Identity Telemetry Privacy Concerns And Data Minimization Constraints | -2.5% | EU and APAC, with spillover to North America | Medium term (2-4 years) |

| False Positive Fatigue In Identity Signal Correlation | -1.9% | Global | Short term (≤ 2 years) |

| High Operational Skill Requirement For Tuning And Investigation | -1.4% | Global, especially acute in SME and mid-market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across IAM, PAM, SIEM, and XDR Stacks

Integration work remains the clearest adoption barrier in the identity threat detection and response (ITDR) market, as most enterprises already run multiple identity and security systems owned by different teams. Deployment becomes more difficult when organizations must integrate single sign-on, privileged access, endpoint telemetry, and incident workflows before the platform can deliver complete detection coverage. Partial integration creates another problem because the tool may appear effective within the data it sees, while remaining blind to access paths in other identity stores or unmanaged applications. That slows buying decisions because security leaders often need budget and approval from both security operations and IT teams before rollout can begin. Vendors that offer broader connector libraries can reduce this friction, but the ITDR market still faces slower adoption, as enterprises maintain older IAM estates and mixed-vendor architectures.

Identity Telemetry Privacy Concerns and Data Minimization Constraints

Privacy requirements are another restraint on the identity threat detection and response (ITDR) market, as these platforms depend on continuous collection of authentication data, behavioral signals, and access logs. In Europe, data minimization expectations under GDPR and the wider control obligations shaped by NIS2 can make organizations more cautious about how much workforce telemetry they collect and store.[4]Federal Office for Information Security, “NIS2 Implementation in Germany,” BSI, bsi.bund.de In healthcare, the issue becomes more sensitive because workforce authentication records can sit close to regulated data environments governed by HIPAA controls. As a result, regulated buyers often need legal review, data-flow mapping, and policy design before technical implementation starts, which extends deployment cycles. The burden falls more heavily on smaller organizations because they usually do not have dedicated privacy teams, which means the identity threat detection and response (ITDR) market can see strong interest but slower conversion in tightly regulated environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Hold the Revenue Base as Services Scale Rapidly

Solutions held 61.23% of the identity threat detection and response (ITDR) market share in 2025, which kept product revenue ahead of services as enterprises prioritized direct control over core detection, analytics, and directory protection layers. Demand for this part of the identity threat detection and response (ITDR) market remained centered on identity threat detection platforms, Active Directory security tools, cloud identity controls, and risk intelligence features that help teams see misuse earlier. Buyers have also moved beyond simple alerting, as security leaders increasingly want dashboards and evidence to show whether access controls are effective across complex environments. That makes solution spending easier to justify because the product is now tied to daily monitoring, policy validation, and audit support rather than a narrow breach response use case.

Services are projected to grow at a 26.28% CAGR through 2031, which makes them the faster-moving part of the component mix even though they start from a smaller base. This growth follows a practical pattern in the identity threat detection and response industry, as many organizations still lack internal specialists who can tune detections, map telemetry, and investigate identity signals at scale. Managed detection, implementation support, and advisory services therefore rise with product adoption instead of competing against it. Mid-market buyers are especially important here because they often want stronger identity monitoring without building a dedicated identity security team. Over time, the component mix suggests that the identity threat detection and response market will continue to reward vendors that can pair a usable platform with service depth, especially when deployments span multiple identity providers and response tools.

By Security Type: Posture Management Redefines the Investment Thesis

Identity threat detection held a 27.19% share in 2025, indicating that direct detection remains the starting point for many buyers entering the identity threat detection and response (ITDR) market. Most organizations first need to see suspicious logins, privilege misuse, and unusual authentication paths before they expand into more preventive identity programs. This keeps threat detection important because it delivers immediate visibility and gives security teams a clear operational case for investment. It also remains the easiest entry point for enterprises that already understand endpoint or network detection and now want equivalent coverage at the identity layer.

Identity security posture management is forecast to expand at a 26.39% CAGR through 2031, signaling the next phase of spending in the identity threat detection and response (ITDR) market. Buyers are no longer satisfied with finding misuse after it starts, and they increasingly want to identify over-permissioned accounts, orphaned credentials, and weak policy settings before those gaps are exploited. That shift changes the value story because posture management supports continuous review rather than isolated responses. Identity risk assessment and incident response also benefit from this pattern, as posture findings are easier to prioritize when they connect to live activity and access behavior. The direction of travel suggests that the ITDR market is broadening from a detection category into a broader identity risk management layer that supports governance, audit readiness, and operational control.

By Deployment: Cloud Dominates While Hybrid Bridges the Transition Gap

Cloud accounted for 54.16% of the identity threat detection and response (ITDR) market in 2025, reflecting how much enterprise access has already moved to SaaS and cloud-native identity environments. In the cloud model, buyers value speed of deployment, easier coverage across distributed users, and faster updates that keep pace with new attack methods. Cloud also aligns with the current structure of the identity threat detection and response (ITDR) market, as many organizations now rely on multiple online services that generate identity data far beyond traditional network boundaries. The result is a steady demand for tools that can monitor sign-ins, tokens, privilege changes, and unusual behavior across a wide range of cloud applications.

Hybrid deployment is set to grow at a 26.50% CAGR through 2031, indicating that many enterprises still need to protect both on-premises directories and cloud identity providers simultaneously. This matters because the hardest identity risks often reside in the connections between legacy Active Directory, modern cloud tenants, and federated trust relationships rather than in a single environment. CrowdStrike’s 2025 and 2026 launches of Falcon Identity Protection for Microsoft Entra ID highlight how vendors are building products that can follow identities across both on-premises AD and cloud systems. On-premises deployments remain relevant in regulated and sovereign environments, but the larger story is that mixed estates will stay common throughout the forecast period. That keeps hybrid demand strong and leaves the identity threat detection and response market with a continued need for deployment models that can unify policy and visibility across old and new identity infrastructure.

By Enterprise Size: Large Enterprises Lead as SME Adoption Accelerates

Large enterprises held a 59.21% share in 2025, making them the leading buyer group in the identity threat detection and response (ITDR) market. Their lead came from earlier spending on cloud security, broader attack surfaces, and larger security teams that could absorb new platforms and response processes. Large organizations are also more likely to run multi-cloud identity estates, privileged access programs, and cross-border operations, which increase the value of identity telemetry. As a result, they often moved ITDR forward earlier and used it to connect identity events with broader security operations.

SMEs are projected to grow at a 26.61% CAGR through 2031, making them the fastest-growing segment in the ITDR market. Germany’s NIS2 implementation widened the compliance burden to more entities across 18 critical sectors, helping push identity control spending beyond the traditional large-enterprise base. This matters because smaller organizations now face stronger expectations around multi-factor authentication, access discipline, and incident readiness, even when they do not have large internal teams. Many SMEs therefore prefer managed delivery, where monitoring, tuning, and response are integrated into the service model rather than handled fully in-house. The growth pattern shows that the identity threat detection and response industry is expanding its buyer base, but it also indicates that vendors will need simpler deployment paths and stronger services to convert SME demand into long-term recurring revenue.

By End-user Industry: BFSI Sets the Standard While Healthcare Accelerates

BFSI held a 16.24% share in 2025, making it the largest end-user segment in the identity threat detection and response (ITDR) market. Financial institutions have long managed sensitive customer identities, privileged access, fraud controls, and regulatory reporting, so identity-focused detection fits naturally into existing risk programs. FinCEN’s updated AML and CFT national priorities in 2025 also kept synthetic identity fraud in focus, supporting spending through compliance and fraud-prevention channels as well as cybersecurity budgets. This combination keeps BFSI steady because the sector already understands the cost of misuse of access and the operational value of stronger identity validation.

Healthcare and life sciences are forecast to grow at a 26.72% CAGR through 2031, making it the fastest-growing end-user segment in the identity threat detection and response (ITDR) market. HHS data shows that more than 275 million individuals were affected by reportable HIPAA breaches in 2024, and hacking and IT incidents made up more than 80% of those events. That scale changes buying behavior because identity misuse can now affect clinical continuity, operational trust, and legal exposure simultaneously. Healthcare organizations also work across employees, contractors, partner systems, and connected applications, which raises the value of continuous identity visibility. The broader end-user mix across IT and telecom, retail and e-commerce, industrial manufacturing, and government suggests that the identity threat detection and response (ITDR) market is no longer limited to early adopters and is moving into a wider set of operationally complex sectors.

Geography Analysis

North America held 32.18% of the identity threat detection and response (ITDR) market share in 2025, making it the largest regional contributor. The region benefits from a dense base of regulated enterprises, mature vendor presence, and a stronger willingness to fund identity controls as part of broader cyber programs. CISA’s Zero Trust Maturity Model gives identity the highest-leverage starting role, and that has helped turn identity visibility into a practical requirement for many large organizations and federal-facing suppliers. The identity threat detection and response market in North America also benefits from steady pressure created by credential abuse, ransomware delivery through identity compromise, and rising scrutiny of privileged access across complex enterprise estates. Buyers in the region are therefore more likely to treat ITDR as a permanent layer inside security operations rather than as a short-term procurement cycle.

Europe is entering a stronger, compliance-led phase of the identity threat detection and response (ITDR) market. Germany’s NIS2 implementation took effect in December 2025 and introduced stricter obligations on identity controls and authentication across a wider set of entities. This matters because spending is now linked not only to breach prevention but also to audit readiness and enforceable operating requirements. HID Global reported in 2026 that identity has become a key meeting point between physical security and cybersecurity, which fits the broader European push toward integrated control frameworks. South America remains earlier in the adoption cycle, but digital financial growth and tighter data protection expectations are helping the region build a clearer case for identity monitoring.

Asia-Pacific is projected to grow at a 26.83% CAGR through 2031, which makes it the fastest-growing region in the ITDR market. The region is seeing rapid expansion of digital services, heavy cloud use, and rising volumes of mobile-led authentication activity, all of which increase the number of identities and sessions that must be monitored. Government-backed digital identity programs in countries such as India, Japan, South Korea, and Australia also support a wider identity control agenda across public and private systems. That does not mean adoption is uniform, because local compliance demands, purchasing maturity, and staffing depth still vary widely by country. The Middle East and Africa remain at an earlier stage, yet sovereign digital infrastructure plans and public-sector identity programs are starting to create more structured demand. Across both Asia-Pacific and MEA, the identity threat detection and response (ITDR) market is likely to grow fastest where cloud adoption, regulatory attention, and machine-identity growth converge within the same buyer environment.

Competitive Landscape

The identity threat detection and response (ITDR) market remains moderately consolidated at the platform level, with a smaller set of large vendors holding the strongest position in enterprise-wide deployments. These vendors benefit from broader security portfolios, established channels, and the ability to combine identity signals with endpoint, cloud, and access data. That advantage matters because buyers increasingly want fewer tools that can work across several operating layers rather than more stand-alone products. At the same time, the identity threat detection and response (ITDR) market still leaves room for specialists in Active Directory protection, non-human identity control, hybrid access enforcement, and targeted identity analytics. The result is a market where scale matters, but detection depth and deployment fit still influence vendor choice.

Competition is also changing because identity detection is being folded into broader platform strategies rather than remaining a niche category. Palo Alto Networks’ completion of its USD 25 billion CyberArk acquisition in February 2026 is one of the clearest signs that identity security now sits close to the center of platform planning, even though specialist depth still matters in deployment decisions. CrowdStrike’s June 2026 launch of Continuous Identity for AI Agents demonstrates how major vendors are extending identity coverage across human, non-human, and AI-agent environments as the access model becomes more complex. Silverfort’s April 2026 acquisition of Fabrix Security points in the same direction because it adds AI-native runtime identity decisioning to an identity-focused security stack. These moves show that the identity threat detection and response (ITDR) market is being shaped less by basic visibility and more by who can deliver unified response, policy, and behavior-based decisions.

Specialist vendors still have a clear role because broad platform coverage does not automatically solve every identity problem inside mixed enterprise estates. Vendors focused on runtime identity control, hybrid governance, directory hardening, and service-led delivery can still win where buyers need specific outcomes without a full platform migration. CyberArk’s February 2025 integration with SentinelOne is a good example of this market logic, as it connects identity data to AI SIEM and XDR workflows rather than treating identity as a separate control stream. Proofpoint’s March 2026 launch of its AI security framework also shows that identity-adjacent vendors are widening into agent control and runtime trust models as enterprise AI use grows. The white space remains largest in managed delivery for mid-market and SME buyers, because many of them want stronger identity defense but still lack the internal staff to run raw detection platforms themselves. That balance between platform power and specialist execution is likely to remain a defining feature of the identity threat detection and response (ITDR) market through the forecast period.

Identity Threat Detection and Response (ITDR) Industry Leaders

CrowdStrike, Inc.

Microsoft Corporation

CyberArk Software Ltd.

Varonis Systems, Inc.

SentinelOne, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: CrowdStrike unveiled Continuous Identity for AI Agents at Identiverse 2026 on June 15, 2026. The new Falcon Next-Gen Identity Security capability, powered by technology from CrowdStrike's acquisition of SGNL, introduces real-time, risk-aware authorization across human, non-human, and AI agent identities, using the SPIFFE open standard for cryptographically verifiable agent identities and eliminating standing privileges through dynamic grant-and-revoke enforcement.

- June 2026: SailPoint announced its intent to acquire Tel Aviv-based Entro Security for approximately USD 200 million. The deal extends SailPoint's Agentic Fabric platform with Entro's non-human identity and credentials security capabilities, providing out-of-the-box coverage for over 1,000 NHI and agent types. The transaction is expected to close in Q3 2026.

- June 2026: Netwrix launched new AI Governance Capabilities within its 1Secure SaaS platform on June 23, 2026, adding over 200 PingCastle-powered checks across Active Directory and data sources, AI-powered guidance for closing identity exposure gaps, and extended monitoring across hybrid Microsoft environments including Copilot activity and identity risk assessment.

- June 2026: Silverfort launched runtime identity controls for Microsoft Copilot Studio agents on June 8, 2026, integrating its Runtime Access Protection technology to enforce least-privilege policies, block anomalous access attempts before execution, and maintain audit trails for agentic AI activity mapped to enterprise identity governance frameworks.

Global Identity Threat Detection and Response (ITDR) Market Report Scope

The Identity Threat Detection and Response (ITDR) market refers to platforms and services that protect digital identities by detecting, analyzing, and responding to identity-based threats across enterprise environments. These solutions include identity threat detection platforms, posture management tools, analytics and risk intelligence systems, Active Directory security, and cloud identity protection, all designed to safeguard user accounts, credentials, and access pathways. The market is driven by the surge in identity-related cyberattacks such as credential theft, privilege escalation, and account compromise, alongside the growing complexity of hybrid and cloud environments. Organizations across BFSI, healthcare, IT, manufacturing, retail, and government are adopting ITDR solutions to strengthen identity governance, ensure compliance, and reduce the risks of unauthorized access.

The Identity Threat Detection and Response (ITDR) market report is segmented by Component (Solutions [Identity Threat Detection Platforms, Identity Security Posture Management, Identity Analytics and Risk Intelligence, Active Directory Security, Cloud Identity Security], and Services), Security Type (Identity Threat Detection, Identity Risk Assessment, Identity Security Posture Management, Identity Incident Response, Governance and Compliance), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Identity Threat Detection Platforms |

| Identity Security Posture Management | |

| Identity Analytics and Risk Intelligence | |

| Active Directory Security | |

| Cloud Identity Security | |

| Services |

| Identity Threat Detection |

| Identity Risk Assessment |

| Identity Security Posture Management |

| Identity Incident Response |

| Governance and Compliance |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Identity Threat Detection Platforms | |

| Identity Security Posture Management | |||

| Identity Analytics and Risk Intelligence | |||

| Active Directory Security | |||

| Cloud Identity Security | |||

| Services | |||

| By Security Type | Identity Threat Detection | ||

| Identity Risk Assessment | |||

| Identity Security Posture Management | |||

| Identity Incident Response | |||

| Governance and Compliance | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current outlook for the identity threat detection and response (ITDR) market?

The identity threat detection and response (ITDR) market size is expected to rise from USD 3.42 billion in 2026 to USD 10.51 billion by 2031 at a 25.17% CAGR, showing strong multi-year demand.

Why are enterprises increasing spending on identity threat detection and response tools?

Spending is rising because stolen credentials appear in 39% of breaches, and Microsoft reported a 32% rise in identity-based attacks in the first half of 2025.

Which deployment model leads spending in identity threat detection and response?

Cloud led with 54.16% share in 2025, while hybrid is the fastest-growing deployment model at a 26.50% CAGR through 2031.

Which end-user sector is growing fastest in identity threat detection and response?

Healthcare and life sciences is growing fastest at a 26.72% CAGR through 2031, supported by the scale and severity of healthcare breach activity.

Which region offers the strongest near-term opportunity?

North America remains the largest region with 32.18% share in 2025, while Asia-Pacific offers the strongest growth outlook with a 26.83% CAGR through 2031.

What is the biggest challenge when deploying identity threat detection and response platforms?

The main challenge is integration across IAM, PAM, SIEM, and XDR environments, especially in enterprises with mixed vendors and legacy identity systems.

Page last updated on: