Threat Intelligence Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

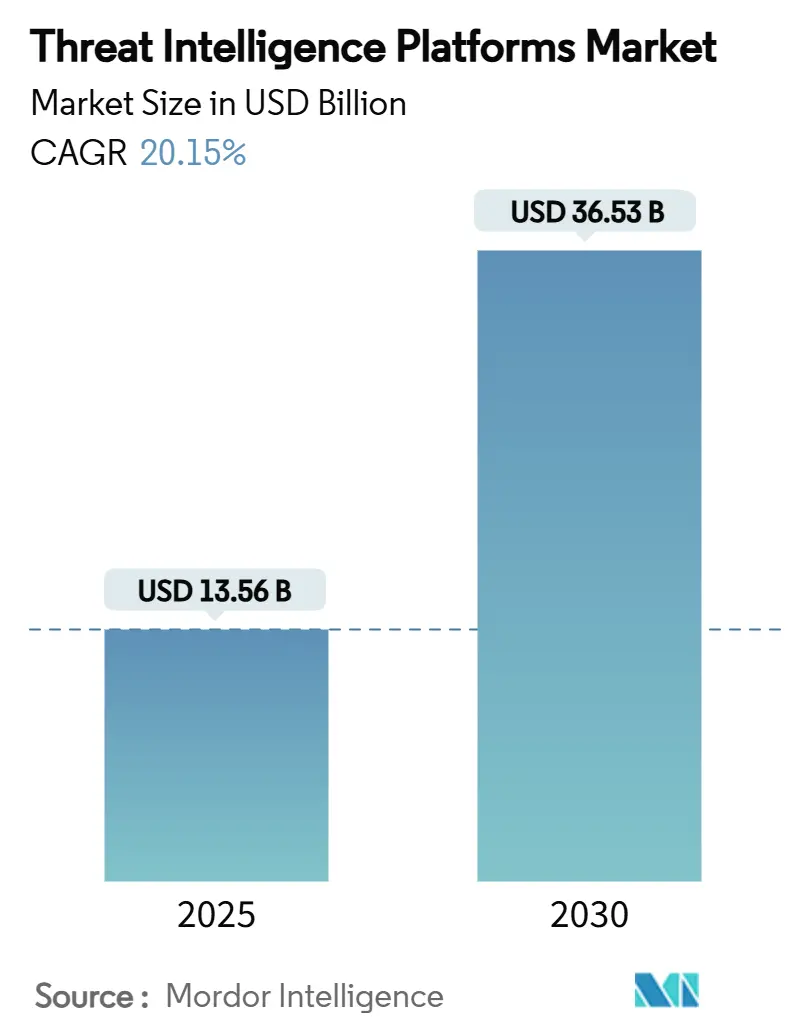

| Market Size (2025) | USD 13.56 Billion |

| Market Size (2030) | USD 36.53 Billion |

| Growth Rate (2025 - 2030) | 20.15% CAGR |

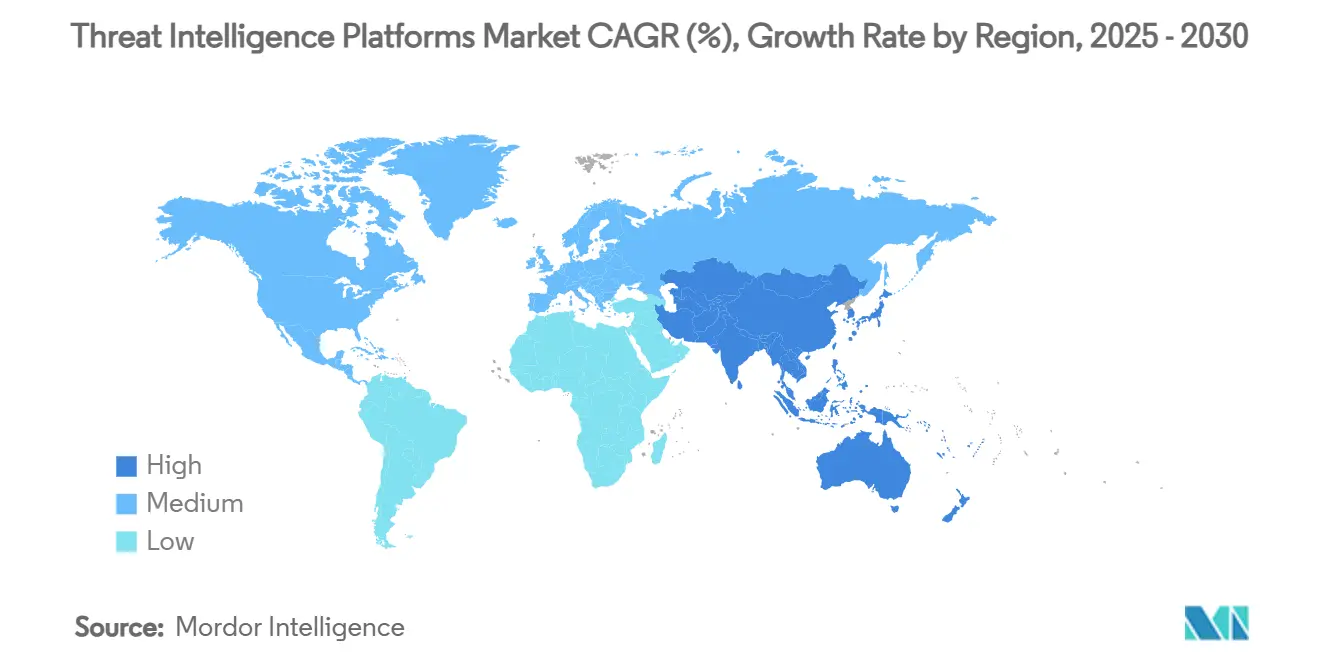

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Threat Intelligence Platforms Market Analysis by Mordor Intelligence

The threat intelligence platforms market size reached USD 13.56 billion in 2025 and is forecast to climb to USD 36.53 billion by 2030, registering a 20.15% CAGR. Heightened nation-state activity, real-time disclosure mandates, and the shift toward cloud-native security operations all accelerate spending on platforms that fuse telemetry, automation, and contextual analytics. Consolidation among technology majors, deeper use of AI for enrichment and triage, and the critical need to protect converged IT-OT environments are reshaping competitive dynamics. North America remains the largest buyer base, but rapid digitalization across Asia drives the fastest incremental growth. Vendors that combine sector-specific intelligence with scalable data pipelines see the strongest uptake as enterprises seek actionable, not voluminous, threat data.[1]Cloud Security Alliance, “Next-Gen AI Cybersecurity: Reshape Digital Defense,” cloudsecurityalliance.org

Key Report Takeaways

- By industry vertical, banking, financial services, and insurance accounted for 27.1% of the threat intelligence platforms market size in 2024; healthcare is advancing at a 24.3% CAGR to 2030.

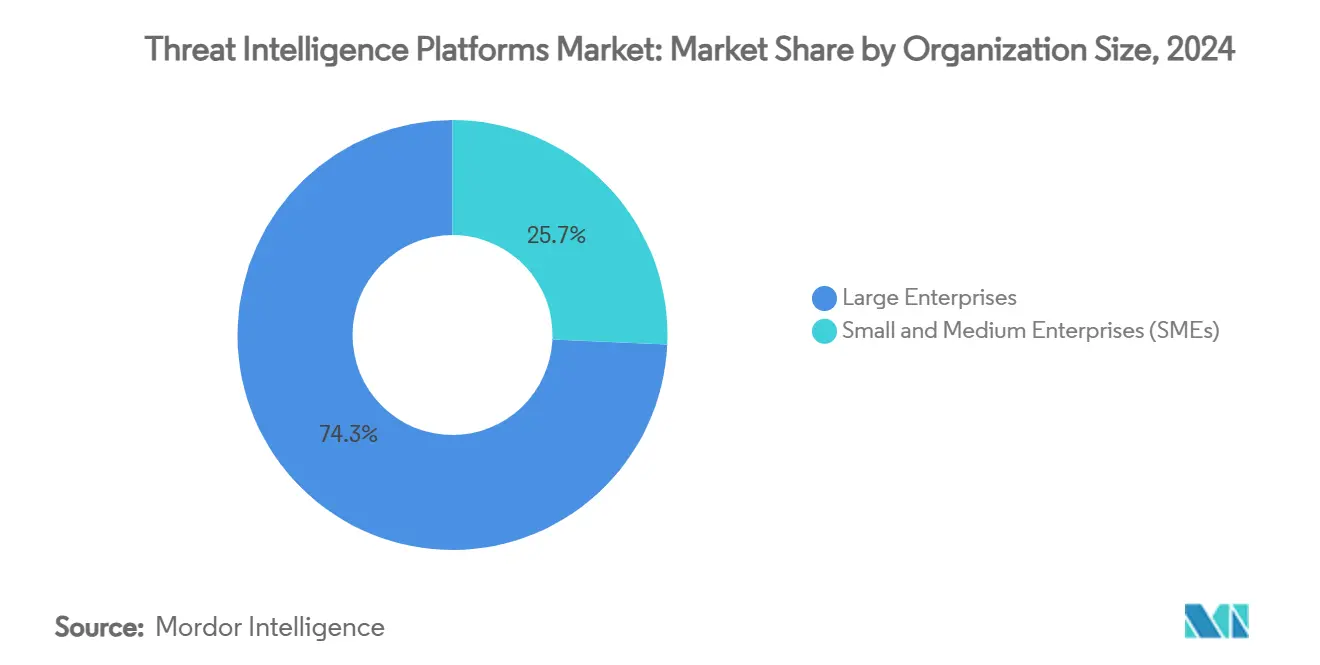

- By organization size, large enterprises controlled 74.3% of 2024 revenue; small and medium enterprises are expanding at a 24.2% CAGR.

- By deployment model, cloud-based platforms held 68.5% revenue share in 2024; hybrid architectures are forecast to grow at a 26.1% CAGR.

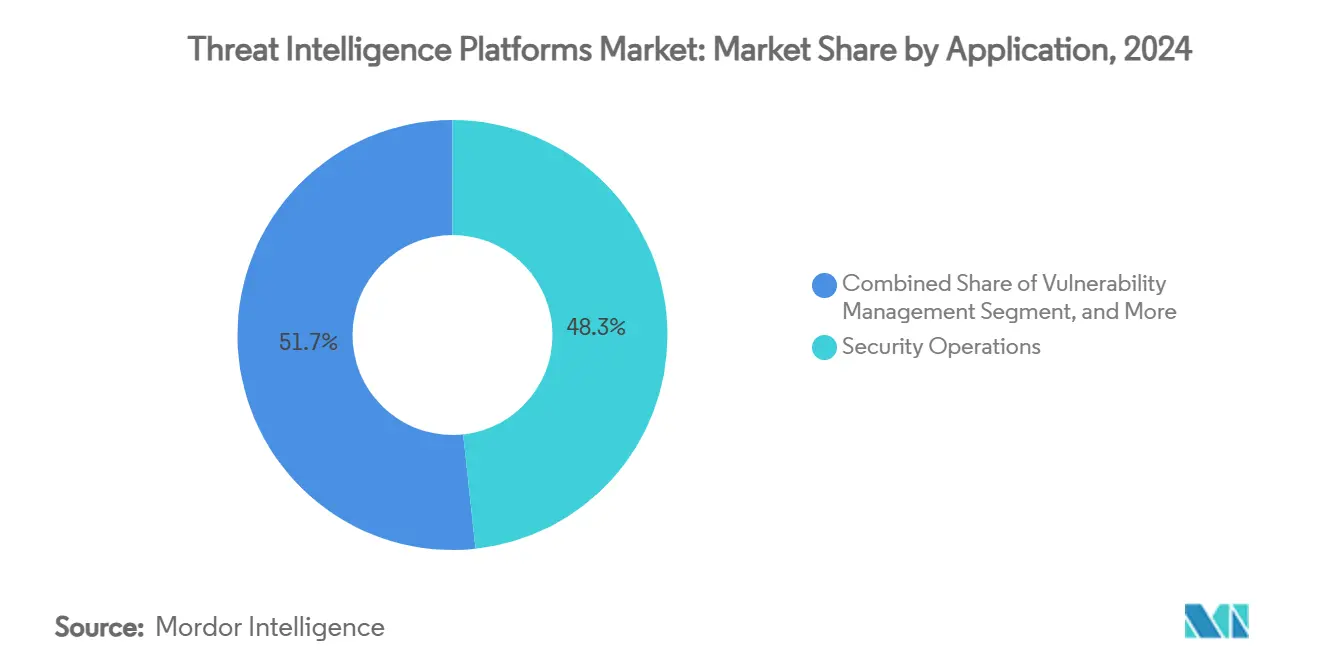

- By application, security operations represented 48.3% of spending in 2024, whereas incident response is rising at a 26.4% CAGR.

- By geography, North America led with a 44.6% threat intelligence platforms market share in 2024, while Asia-Pacific is projected to register a 25.6% CAGR through 2030.

Global Threat Intelligence Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of sophisticated OT and IoT-focused cyber threats | +4.2% | Global; strongest in North American and European industrial hubs | Medium term (2-4 years) |

| Surge in regulatory mandates for real-time threat reporting | +3.8% | North America and the EU first adopters, expanding across Asia | Short term (≤ 2 years) |

| Rapid adoption of cloud-based security analytics platforms | +3.5% | Global; early uptake in North America, fast acceleration in Asia | Short term (≤ 2 years) |

| Integration of AI/ML for automated threat enrichment and triage | +4.1% | Global; mature use cases in developed markets | Medium term (2-4 years) |

| Expansion of darknet marketplaces and cybercrime-as-a-service | +2.9% | Global; pronounced impact in emerging economies | Long term (≥ 4 years) |

| Growing demand for sector-specific threat-intelligence feeds | +2.7% | Global, pronounced in healthcare and financial services | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Sophisticated OT and IoT-Focused Cyber Threats

Attacks on operational technology grew sharply as adversaries discovered unprotected interfaces between factory-floor systems and enterprise networks. In 2024, 76% of organizations reported an intrusion in their OT stack, with 68 publicly confirmed incidents leading to physical consequences, a 19% jump from 2023. Discrete manufacturers endured outages costing tens to hundreds of millions of dollars per event. Legacy controllers designed without authentication safeguards remain in wide use, while the rapid rollout of IoT sensors multiplies entry points. The energy sector now tracks 60 new grid vulnerabilities daily, prompting utilities to embed continuous threat monitoring that flags malicious commands before they propagate through control rooms.[2]Resecurity, “Cyber Threats Against Energy Sector Surge as Global Tensions Mount,” resecurity.com As downtime risk elevates from data loss to physical harm, demand intensifies for threat intelligence enriched with device-level context.

Surge in Regulatory Mandates for Real-Time Threat Reporting

Legislators on both sides of the Atlantic compressed disclosure windows, making manual intelligence gathering impractical. In the United States, the SEC now requires public companies to file material-incident details within 4 business days, and CISA’s pending CIRCIA rule will oblige critical-infrastructure entities to notify within 72 hours and ransomware payments within 24 hours. Europe’s Digital Operational Resilience Act pushes banks to lodge an initial report in 4 hours and a comprehensive outline in 1 month. Such timelines force platforms to automate indicator correlation, provenance scoring, and narrative generation so that legal and executive teams can confirm facts swiftly. Financial firms face additional filing layers under new anti-money-laundering rules scheduled for 2026 that depend on rich intelligence to trace transaction anomalies.

Rapid Adoption of Cloud-Based Security Analytics Platforms

With 95% of enterprises already running workloads in public clouds, telemetry volumes have outstripped the capacity of on-premises collectors. Organizations now deploy security data pipelines that normalize logs before shipping them to lightweight correlation engines, sidestepping SIEM cost models tied to data ingest caps. Streaming frameworks built on Apache Kafka and Spark allow real-time matching of indicators against petabyte-scale repositories. Cloud elasticity lets defenders spin up compute clusters on demand during peak attack windows, then spin them down to manage spend. For regulated sectors that must store sensitive artifacts locally, hybrid patterns keep payloads on-premises yet tap cloud AI for enrichment.

Integration of AI/ML for Automated Threat Enrichment and Triage

AI augments every phase from collection to response. Agentic systems are projected to lift SOC efficiency 40% by 2026, mainly by clustering duplicative alerts, extracting entities from unstructured feeds, and proposing mitigation steps. Machine-learning models detect subtle behavioral shifts, while large language models summarize adversary chatter to shrink analyst review cycles. Nonetheless, adversarial inputs and model drift create new risk vectors, so many enterprises adopt human-in-the-loop controls. Mature programs couple AI scoring with expert override workflows, ensuring that automated block recommendations receive contextual validation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High volume of false positives is overwhelming SOC teams | -2.1% | Global, notably acute for resource-constrained organizations | Short term (≤ 2 years) |

| Shortage of skilled threat-intelligence analysts | -1.8% | Global; strongest in emerging markets | Long term (≥ 4 years) |

| Data-privacy barriers to cross-border intelligence sharing | -1.4% | EU and parts of the Asia-Pacific | Medium term (2-4 years) |

| Budget constraints among mid-sized enterprises | -1.2% | Emerging economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Volume of False Positives Overwhelming SOC Teams

SOC personnel wrestle with an alert tsunami as loosely tuned detection rules flood consoles. Studies isolate four root causes, from uninformed rule sets to poor context enrichment that leaves benign anomalies indistinguishable from genuine threats.[3]ACM Computing Surveys, “Alert Fatigue in Security Operations Centres: Research Challenges and Opportunities,” dl.acm.org Analysts forced to triage non-stop enter cognitive overload, heightening the risk of ignoring real intrusions. AI-powered prioritization engines are gaining traction, yet they depend on clean training data and regular validation—investments many mid-size firms cannot afford. Until tooling matures, high false-positive rates continue to sap productivity and elongate mean-time-to-detect.

Shortage of Skilled Threat-Intelligence Analysts

Even as platform usability improves, qualified human oversight remains indispensable for adversary attribution and risk framing. An estimated 89% of organizations plan to enlarge cyber staff just to satisfy new European resilience mandates, but the pipeline of practitioners versed in both technical forensics and intelligence tradecraft remains thin. The gap is wider in emerging regions where advanced institutes are scarce. Vendors respond by embedding workflows that hide analytic complexity, yet without seasoned professionals to interpret patterns, automation alone cannot deliver strategic guidance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Scale Spurs SME Catch-up

Large enterprises held 74.3% of the threat intelligence platforms market share in 2024, channeling multi-million-dollar budgets into global SOCs and proprietary correlation engines. Their layered control frameworks demand feeds covering endpoints, clouds, and industrial sites, generating vast telemetry that only high-end platforms can parse efficiently. At the same time, SMEs represent the fastest-growing cohort at a 24.2% CAGR, as SaaS pricing removes the capital hurdle and marketplaces offer plug-and-play intelligence bundles.

Vendors increasingly release tiered editions that map to SME maturity, pairing core detection with managed response options. The democratization trend is driven by soaring ransomware premiums on small businesses and legal exposure once reserved for large corporations. As a result, SME uptake enlarges the total addressable threat intelligence platforms market.

Cloud-native delivery is pivotal to SME traction. Lightweight agents stream essential events without overwhelming bandwidth, while multitenant back ends apply AI scoring that distills priorities into daily digest views. Partnerships with regional managed service providers further lower entry barriers, giving small customers analyst expertise at subscription levels aligned to their cash flow. Over the forecast horizon, SME demand is expected to narrow the adoption gap, although absolute spending will still favor Fortune-listed buyers.

By Deployment Model: Hybrid Becomes the Practical Default

Cloud deployments captured 68.5% of 2024 revenue thanks to elastic compute and reduced maintenance overheads. Enterprises ingest petabytes of telemetry, enrich it in the cloud, and expose curated indicators via APIs to downstream tools. However, compliance teams, especially in financial services and government, insist that raw evidence remain on servers they physically control. Hybrid architectures—local storage coupled with cloud analytics—therefore post the fastest trajectory at a 26.1% CAGR, signaling a structural shift rather than a passing trend.

Under the hybrid pattern, sensitive packet captures and legal holds stay inside corporate data centers, yet metadata and hashes traverse encrypted channels to cloud AI engines for wide-scale correlation. The architecture blends sovereignty with scale, a trade-off regulators increasingly endorse. Integration complexity remains the chief hurdle; vendors respond with reference blueprints and pre-tested connectors that trim deployment timelines.

Workload placement flexibility also mitigates cost exposure. Organizations route routine indicator matching to low-cost regional clouds, bursting to premium GPU lanes only when anomaly clusters emerge. This pay-as-needed model contrasts with the perpetual hardware refreshes inherent in purely on-premises stacks, reinforcing hybrid’s economic appeal. Consequently, hybrid adoption is set to redefine procurement criteria within the broader threat intelligence platforms market size allocations.

By Application: SOC-Centric Today, Incident Response Tomorrow

Security operations center use cases generated 48.3% of 2024 spending as teams embedded external intelligence into SIEM workflows for earlier detection. Correlating internal logs with external indicators accelerates kill-chain disruption and underpins zero-trust architectures. Yet incident response now records the steepest growth, posting a 26.4% CAGR as regulators compress disclosure windows and boards demand forensically defensible reporting.

Modern responders expect their platform to fetch historical context, map adversary infrastructure, and auto-generate narrative summaries within minutes of an alert. Integration with case-management tools and digital forensics suites positions threat intelligence as the central knowledge spine that drives containment playbooks.

In parallel, vulnerability management modules tap live exploit telemetry to prioritize patch cycles. Risk and compliance dashboards translate threat data into board-ready heat maps, while advanced threat hunting layers allow veteran analysts to pivot through graph databases and identify hidden relationships. These adjacent applications diversify revenue streams, yet SOC and incident-response scenarios will continue to dominate the near-term share of the threat intelligence platforms market size.

By Industry Vertical: Financial Stronghold, Healthcare Surge

Financial institutions accounted for 27.1% of 2024 spend, reflecting both asset attractiveness and stringent oversight. Payment networks, investment banks, and insurers distill threat feeds into fraud analytics, anomaly scoring, and anti-laundering surveillance, embedding intelligence into customer-facing workflows.

Healthcare, however, logs the briskest expansion at 24.3% CAGR. The 2024 ransomware strike on a leading claims processor, which disrupted 74% of U.S. hospitals, underlined patient-safety stakes, propelling boards to fund platform deployment. Medical records fetch up to USD 1,000 on illicit markets, incentivizing attackers and magnifying breach consequences.

Government, defense, and energy operators also rely heavily on sector-tuned feeds that spotlight nation-state tactics. Retail and e-commerce demand grows as card-skimming and credential stuffing push merchants toward proactive monitoring. Across verticals, the pivot from compliance-driven checkbox spending to risk-aligned intelligence consumption broadens use-case diversity within the threat intelligence platforms market.

Geography Analysis

North America maintained a 44.6% share in 2024, sustained by a mature vendor ecosystem and a dense fabric of information-sharing collectives such as ISACs. Federal rulemakings—SEC incident disclosure within 4 business days and imminent CIRCIA 72-hour reporting—cement intelligence platforms as compliance necessities. The United States also enforces sector-specific frameworks such as NERC CIP, which mandate threat mapping across utility control systems. Canada augments capability through cross-border data-exchange pacts, whereas Mexico’s financial regulator integrates platform output into systemic-risk dashboards.

Asia-Pacific delivers the fastest expansion at a 25.6% CAGR as digital-service adoption skyrockets and cyber adversaries intensify operations. Advanced persistent threat groups in the region increasingly weaponize generative AI, compelling Japan, South Korea, and Australia to subsidize commercial platform acquisition as part of critical-infrastructure defense. Government-backed CERTs in India and Singapore promote public-private intelligence flows, accelerating domestic vendor partnerships that localize language models for regional threats. Despite disparate legal regimes, market momentum outweighs interoperability frictions, making the Asia-Pacific central to the incremental threat intelligence platforms market growth.

Europe registers steady uptake anchored in the NIS 2 Directive and the Digital Operational Resilience Act. Banks must now deliver an initial cyber-incident notice in 4 hours, an obligation achievable only by integrating automated collection and correlation. France and Germany co-fund industry hubs that curate energy-sector indicators, while the United Kingdom’s National Cyber Security Centre pushes tailored feeds to small businesses. Eastern European states, facing heightened geopolitical tension, fast-track platform rollouts for grid and telecom operators. Overall, Europe’s policy-led demand stabilizes revenue despite data-sovereignty barriers that slow cross-border feed exchange.

Competitive Landscape

Market structure tightens as acquisitive giants fold threat intelligence into broader security clouds. Mastercard closed a USD 2.65 billion deal for Recorded Future in December 2024 to embed predictive feeds into payment fraud engines, echoing Google’s USD 5.4 billion purchase of Mandiant the year before.[4]Mastercard, “Mastercard Finalizes Acquisition of Recorded Future,” investor.mastercard.com Bitsight’s USD 115 million acquisition of Cybersixgill extended external-attack-surface mapping with dark-web reconnaissance, while Palo Alto Networks integrated IBM’s QRadar SaaS telemetry to boost Cortex XSIAM correlation throughput.

Leadership now clusters around Recorded Future, Google, and CrowdStrike, each coupling proprietary collections with machine-scale analytics. These three vendors collectively command a sizeable slice of the threat intelligence platforms market share and wield the R&D budgets to automate enrichment pipelines that small rivals struggle to match. Yet white-space opportunity persists in niche feeds—industrial control systems, healthcare device firmware, supply-chain visibility—where specialists offer depth over breadth.

Partner ecosystems gain strategic value. Managed security service providers' white-label platform results in offsetting analyst shortages among mid-market clients, while cloud hyperscalers bundle native threat feeds with compute credits. Competitive differentiation increasingly rests on delivery freshness, transparency of scoring algorithms, and the degree of workflow integration into ticketing, DevSecOps, and board-level risk portals. Vendors that marry timeliness with interpretability appear best positioned to capture upsell in the evolving threat intelligence platforms market.

Threat Intelligence Platforms Industry Leaders

Recorded Future, Inc.

Mandiant, Inc.

CrowdStrike Holdings, Inc.

Anomali, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: A widespread CrowdStrike outage underscored the need for diversified telemetry pipelines and rigorous change management.

- June 2025: Securonix agreed to acquire ThreatQuotient to fuse threat detection with AI-driven incident response.

- April 2025: Kevin Mandia stepped down as Mandiant CEO as Google integrated threat intelligence and incident-response units.

- January 2025: FinCEN’s anti-money-laundering program for investment advisers will require suspicious-activity reporting backed by real-time threat intelligence.

Global Threat Intelligence Platforms Market Report Scope

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Cloud-based |

| On-Premises |

| Hybrid |

| Security Operations |

| Incident Response |

| Risk and Compliance Management |

| Vulnerability Management |

| Others |

| BFSI |

| IT and Telecom |

| Government and Defense |

| Healthcare |

| Retail and E-commerce |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Deployment Model | Cloud-based | ||

| On-Premises | |||

| Hybrid | |||

| By Application | Security Operations | ||

| Incident Response | |||

| Risk and Compliance Management | |||

| Vulnerability Management | |||

| Others | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Government and Defense | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected value of the threat intelligence platforms market by 2030?

The server security solutions market size is USD 28.96 billion in 2025.

What growth rate is projected for server security solutions through 2030?

Revenue is forecast to advance at a 7.7% CAGR, reaching USD 41.95 billion by 2030.

Which segment holds the largest share of spending?

Services lead with 40.2% revenue share, driven by demand for managed and professional security offerings.

Which geography is expanding the fastest?

Asia-Pacific is projected to grow at a 11.2% CAGR, propelled by sovereign-cloud mandates and data-center expansion.

Why are SMEs increasing their security budgets?

SMEs face rising ransomware attacks and a stark gap between compliance costs and non-compliance penalties, encouraging new investment in managed and cloud-based protections.

How are vendors differentiating their server security platforms?

Providers integrate AI analytics, unified policy engines, and confidential-computing support while pursuing acquisitions to offer broad, end-to-end protection suites.

Page last updated on: