Threat Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

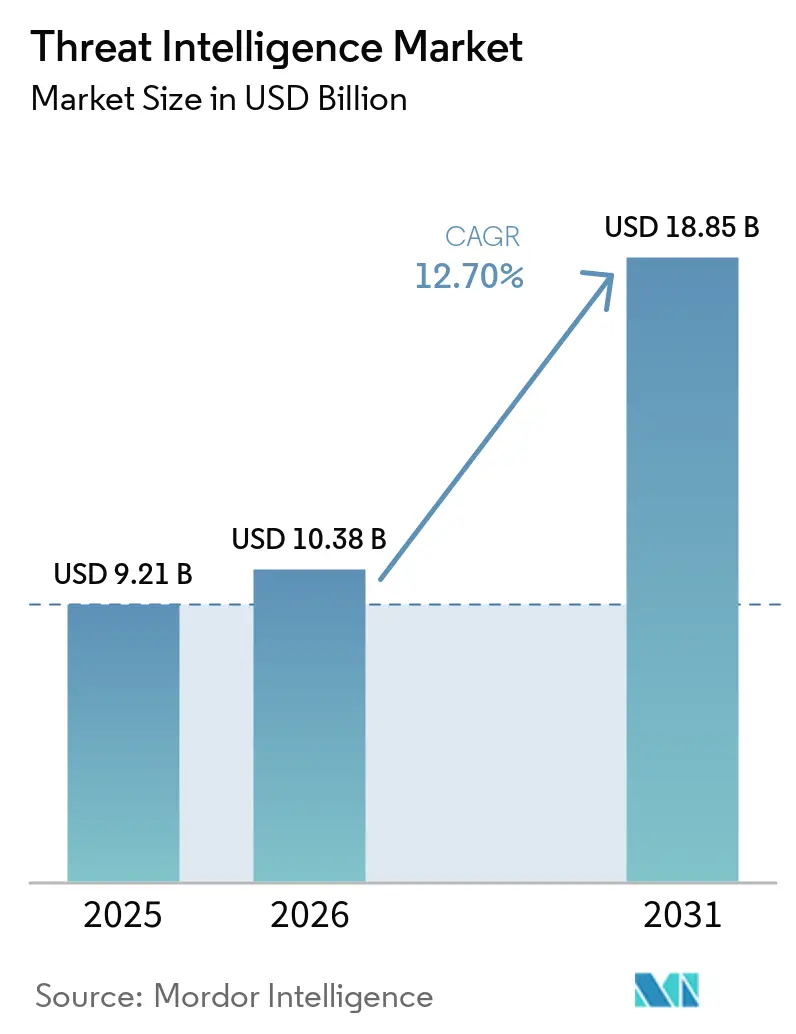

| Market Size (2026) | USD 10.38 Billion |

| Market Size (2031) | USD 18.85 Billion |

| Growth Rate (2026 - 2031) | 12.70% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

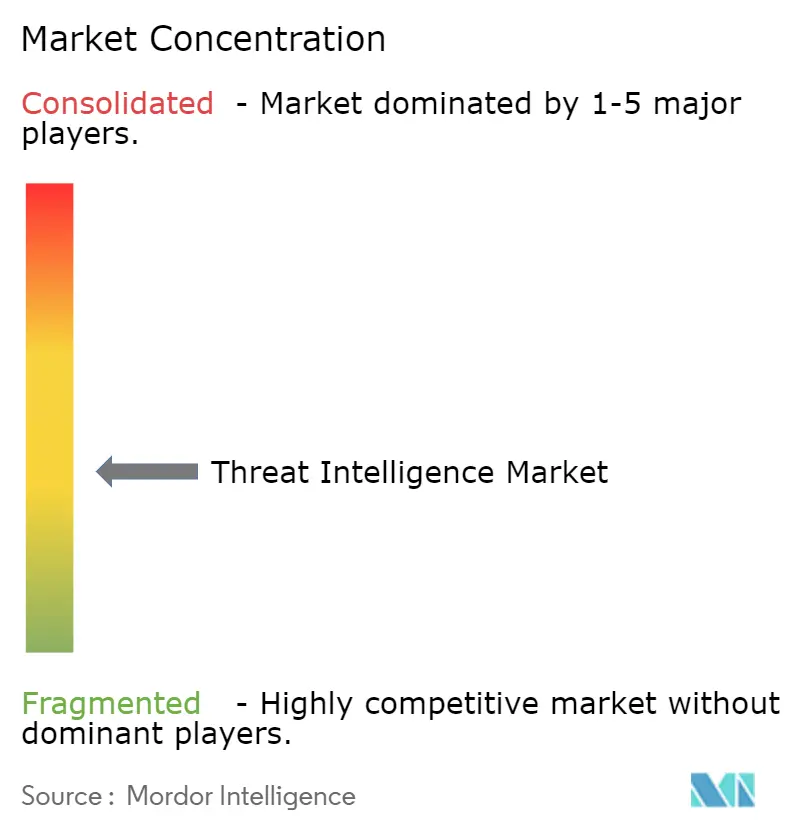

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Threat Intelligence Market Analysis by Mordor Intelligence

Threat intelligence market size in 2026 is estimated at USD 10.38 billion, growing from 2025 value of USD 9.21 billion with 2031 projections showing USD 18.85 billion, growing at 12.7% CAGR over 2026-2031. Expanding cloud adoption, rapid attacker use of AI, and tighter regulatory frameworks such as the EU-NIS2 directive are lifting spending on proactive intelligence platforms. Security leaders are prioritizing context-rich analytics that shorten response times and lower breach costs, while insurers and investors now examine live intelligence feeds before underwriting cyber risk. Consolidation among large vendors is accelerating platform breadth, yet specialist providers remain relevant where sector-specific intelligence is required. Heightened nation-state activity and ransomware cartel funding through cryptocurrencies are expected to keep the threat environment volatile, sustaining investment momentum across every major vertical.

Key Report Takeaways

- By component, Solutions captured 55.40% of the threat intelligence market share in 2025, whereas Services are projected to expand at a 14.12% CAGR through 2031.

- By deployment, on-premise held 54.30% of the market size in 2025; cloud is slated to grow at a 16.25% CAGR during 2026-2031.

- By threat-intelligence type, Strategic intelligence contributed 33.60% revenue in 2025, while Operational intelligence is tracking a 16.35% CAGR to 2031.

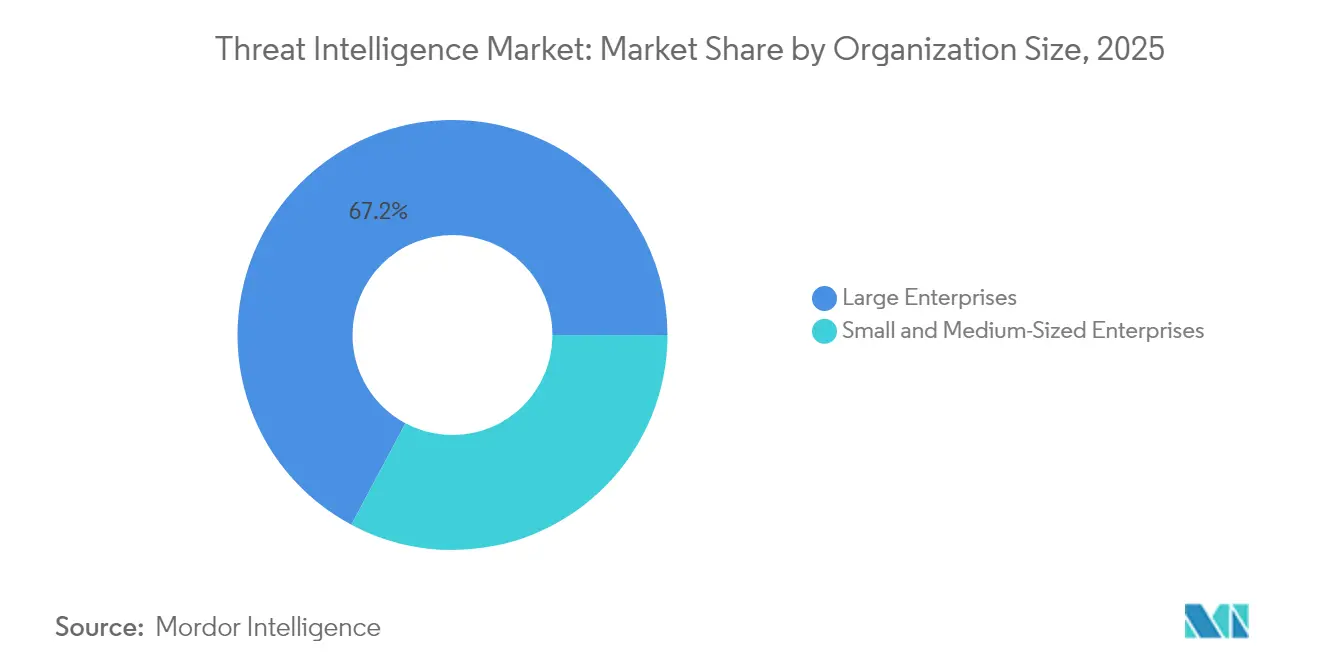

- By organization size, large enterprises accounted for 67.20% of the threat intelligence market size in 2025; the SME segment is advancing at a 14.95% CAGR.

- By end-user sector, IT and Telecommunications led with 20.60% of the market share in 2025; BFSI is the fastest-growing vertical at a 14.70% CAGR.

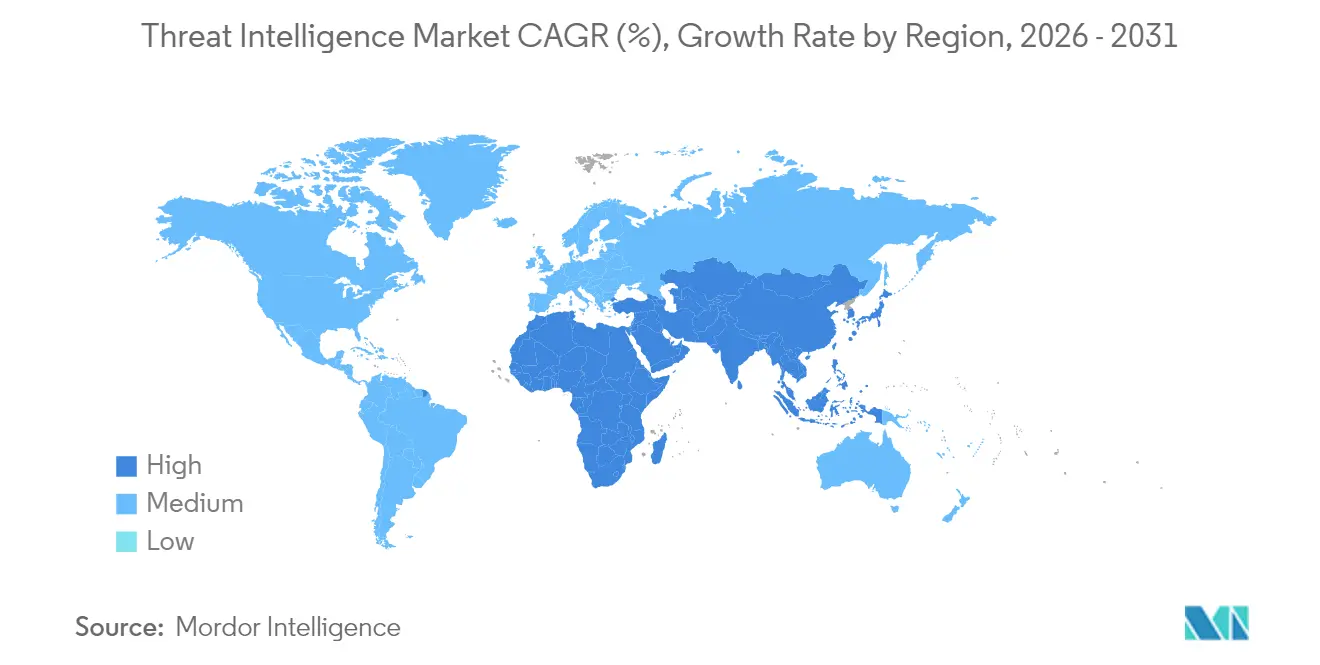

- By geography, North America commanded 37.50% of global revenue in 2025; the Middle East exhibits the quickest regional CAGR at 15.35% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Threat Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven polymorphic malware targeting cloud-native workloads | +3.5% | North America with spillover to Europe and APAC | Medium term (2-4 years) |

| EU-NIS2 compliance spend by critical infrastructure operators | +2.8% | European Union; global multinationals | Short term (≤2 years) |

| Zero Trust roll-outs in APAC large enterprises | +2.2% | Japan, South Korea, Australia | Medium term (2-4 years) |

| RaaS cartels fuelling crypto-wallet monitoring demand | +1.9% | North America and Europe | Short term (≤2 years) |

| Outsourced threat-hunting by South American mid-tier BFSI | +1.5% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Cyber-insurance premium discounts tied to live feeds in Middle East energy | +1.0% | UAE, Saudi Arabia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

AI-driven Polymorphic Malware Targeting Cloud-Native Workloads

AI-generated polymorphic malware can rewrite its code on the fly, defeating traditional signature tools and forcing defenders to rely on behavioural analytics. IBM research shows such malware now negotiates ransoms without human contact and pivots tactics based on cloud configuration, complicating incident response.[1]Matthew Kosinski, “How to Fight AI Malware,” ibm.com The U.S. Department of Justice recently dismantled a ring that stole USD 263 million in cryptocurrency through AI-enabled exploits, underscoring the financial risk.[2]U.S. Department of Justice, “Cryptocurrency Theft Conspiracy,” trmlabs.com North American enterprises are boosting budget for machine-learning detection, making the threat intelligence market essential for cloud workload protection.

EU-NIS2 Compliance Spend by Critical Infrastructure Operators

Effective October 2024, the NIS2 directive subjects roughly 300,000 European entities to mandatory risk assessments, incident reporting, and supply-chain scrutiny.[3]Skadden Arps, “Implications of the EU NIS2 Directive,” skadden.com Penalties can reach EUR 10 million or 2% of global turnover, pushing boards to prioritise real-time intelligence. Multinationals outside the bloc must also comply when serving EU customers, widening opportunity for vendors that package ready-to-audit intelligence feeds.

Zero Trust Roll-outs in APAC Large Enterprises

In APAC, in 2024, 97% of enterprises have begun Zero Trust projects, up from 16% in 2019 . Threat intelligence enriches these frameworks by adding adversary context to every access decision. Despite progress, only 2% of firms have reached mature Zero Trust status, so demand for turnkey intelligence-enabled solutions remains high.[4]Xiou Ann Lim, “25 on 2025: APAC Security Predictions,” csoonline.com

RaaS Cartels Fuelling Crypto-Wallet Monitoring Demand

Ransomware-as-a-Service groups collected USD 459.8 million in 2024 payments, laundering proceeds through obfuscated crypto routes. Exchanges and banks now invest in blockchain-aware intelligence that spots ransom wallets early to avoid sanctions violations, further expanding the threat intelligence market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| STIX/TAXII interoperability gaps in legacy SOCs | -1.2% | Global mature SOCs | Medium term (2-4 years) |

| Escalating subscription costs for actionable intel data | -0.8% | SMEs worldwide | Short term (≤2 years) |

| Data-sovereignty barriers in China CSL and India DPDP | -0.6% | China, India | Long term (≥4 years) |

| Analyst fatigue and alert overload | -0.5% | Regions with talent shortages | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

STIX/TAXII Interoperability Gaps in Legacy SOCs

Although STIX and TAXII became OASIS standards in 2021, many legacy platforms still process proprietary formats, preventing seamless data sharing. An exploratory study identified integration complexity and inconsistent notation as primary hurdles. As a result, organisations delay platform upgrades, restraining short-term spending.

Escalating Subscription Costs for Actionable Intel Data

Advanced feeds that bundle machine learning and analyst validation now command premium pricing. Security leaders worry that multi-feed strategies may outpace budget growth, particularly in small and medium enterprises. Vendors are experimenting with tiered access, yet cost-to-value concerns are likely to temper adoption among resource-constrained buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate While Services Accelerate

Solutions generated 55.40% of global revenue in 2025, giving platforms an outsized hold on the threat intelligence market. Microsoft Defender Threat Intelligence alone processes 78 trillion signals per day, highlighting scale advantages. This dominance underlines why the market size attached to platforms is expected to keep rising through 2031. Leading vendors incorporate AI for behaviour analytics, easing analyst workload and improving detection fidelity.

Managed and professional services are outpacing product growth with a 14.12% CAGR, reflecting talent shortages and rising complexity. SANS surveys show many enterprises outsource hunting duties to close skill gaps. Partnerships that wrap training around deployments allow buyers to derive quicker value, propelling service uptake, especially across the threat intelligence industry’s mid-market segment.

By Deployment: Cloud Adoption Accelerates Security Transformation

On-premise deployments held 54.30% of spending in 2025 as heavily regulated sectors prefer local data residency. Even so, cloud-hosted platforms are the fastest riser at 16.25% CAGR, signalling confidence in provider hardening and FedRAMP expansions such as Microsoft Defender Threat Intelligence gaining High attestation. Segment observers see the threat intelligence market size for cloud deliveries eclipsing on-premise totals late in the forecast window.

Hybrid approaches blend legacy sensors with SaaS analytics, appealing to organisations modernising at their own pace. Financial regulators now publish blueprints for secure cloud adoption that specifically mention continuous intelligence integration, accelerating momentum.

By Threat-Intelligence Type: Strategic Insights Drive Decision-Making

Strategic intelligence held 33.60% share in 2025 as boards rely on geopolitical context and adversary motivation to steer risk budgets. Documents such as the ENISA Threat Landscape give executives a high-level view of campaigns shaping the market. Operational feeds are surging at 16.35% CAGR because security operations centres need near real-time mapping between Indicators of Compromise and active incidents, making the threat intelligence market size tied to SOC workflows grow sharply.

Tactical and technical feeds remain vital for signature creation and malware reverse engineering. Vendors blend these perspectives into unified workspaces, enabling faster pivot from a single artefact to strategic context, a feature showcased in Microsoft Security Copilot.

By Organization Size: Large Enterprises Lead, SMEs Gain Momentum

Large enterprises captured 67.20% of 2025 spending, driven by broad attack surfaces and compliance mandates. Microsoft tracks over 1,500 unique threat groups, illustrating the barrage facing Fortune-class networks. Yet SMEs are advancing at a 14.95% CAGR because cloud delivery and freemium tiers lower entry barriers, bringing them into the threat intelligence market.

Service providers embed curated intelligence into managed offerings, allowing smaller firms to participate without hiring dedicated analysts. Microsoft’s Defender Threat Intelligence Standard Edition widens profile access, an example of democratisation underway.

By End-user Industry: IT and Telecommunications Leads, BFSI Accelerates

IT and Telecommunications held 20.60% revenue in 2025, mirroring its exposure to supply-chain breaches and DDoS attacks. Continuous monitoring of 5G core and edge assets keeps spending high, sustaining the overall threat intelligence market. BFSI is progressing at a 14.70% CAGR as regulators compel threat intelligence integration into fraud analytics and risk scoring. India’s 2025 BFSI Digital Threat Report outlines ransomware and third-party breaches as top exposures, spurring fresh investment.

Healthcare, energy, government, and manufacturing are also scaling programmes. For Middle East utilities, insurance premium rebates now hinge on live feed adoption, tightening links between operational continuity and intelligence quality.

Geography Analysis

North America commanded 37.50% of 2025 revenue owing to mature cloud uptake, joint public-private information sharing, and deep vendor presence. Legislators continue to refine disclosure laws, while federal bodies sponsor real-time data-exchange platforms that reinforce the threat intelligence market. AI-enabled malware against cloud workloads remains the top regional concern, keeping platform spending buoyant.

Europe’s outlook brightens under NIS2, which scales mandatory coverage from 20 000 to 300 000 entities, greatly enlarging the addressable threat intelligence market. Complementary legislation such as the Cyber Resilience Act furthers demand for continuous vulnerability context across supply chains. Vendors that package audit-ready reporting with multi-lingual threat data are well positioned.

The Middle East shows the fastest CAGR at 15.35% through 2031. National agencies in the UAE and Saudi Arabia invest in sector-focused fusion centres while energy majors receive cyber-insurance discounts tied to live feeds. Rising geopolitical tension in the region elevates the strategic value of the threat intelligence market for both public and private sectors.

Asia-Pacific sees a double-digit attack uptick, notably in Indonesia where weekly incidents top 3,300. Rapid digitalisation, paired with diverse sovereignty rules, produces fragmented demand. Japan, South Korea, and Australia lead Zero Trust pilots that embed live intelligence into access decisions, while China and India’s data-localisation laws create preferences for in-country cloud nodes.

South America’s adoption is spurred by mid-tier BFSI outsourcing threat-hunting to overcome skills shortages, adding to global revenue even if from a smaller base.

Competitive Landscape

Market concentration tightened in 2024 amid 362 cybersecurity acquisitions that combined advanced detection, response, and intelligence assets into broader portfolios. Mastercard’s USD 2.65 billion purchase of Recorded Future and Google’s impending USD 32 billion deal for Wiz typify moves to embed threat intelligence within cross-domain security stacks.

AI capability is the prime differentiator. Microsoft Security Copilot analyses 78 trillion daily signals to enrich investigation workflows, while CrowdStrike’s Charlotte AI automates response playbooks. Fortinet integrates FortiAI across its fabric, unifying network and endpoint context. Stand-alone vendors now specialise in niche areas such as firmware telemetry or crypto-asset tracing to remain competitive.

Open standards pressure vendors with proprietary schemas. Buyers value platforms that ingest STIX/TAXII without heavy customisation. Providers that deliver interoperability plus sector-specific enrichment are gaining favour as organisations expand coverage beyond traditional IT assets into OT and IoT.

Threat Intelligence Industry Leaders

Dell Inc.

IBM Corporation

Anomali, Inc.

Fortinet, Inc.

CrowdStrike, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Check Point agreed to acquire Veriti Cybersecurity to add automated exposure management to its Infinity suite.

- May 2025: Fortinet extended its Hybrid Mesh Firewall lineup with the AI-ready FortiGate 700G series.

- April 2025: Palo Alto Networks revealed plans to buy Protect AI for up to USD 700 million to fortify AI governance.

- April 2025: CrowdStrike launched Charlotte AI Agentic Response and Workflows at RSAC 2025.

- April 2025: Rapid7 introduced Intelligence Hub within its Command Platform, delivering curated insight.

- April 2025: Binarly released Transparency Platform v3.0 with exploitation-aware risk scores

- April 2025: CyberRisk Alliance bought Execweb to deepen CISO engagement capabilities.

- April 2025: Bitsight launched Pulse, consolidating open-source and dark-web intelligence into custom channels.

Global Threat Intelligence Market Report Scope

Threat intelligence collects and evaluates information relevant to protecting an organization from internal and external threats and analyzes that information to detect deceptions for accurate and relevant intelligence.

The threat intelligence market is segmented by type (solutions and services), deployment (on-premise and cloud), end user (banking, financial services, and insurance (BFSI), IT and telecom, retail, manufacturing, healthcare), and geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, Rest of Asia-Pacific), Latin America (Mexico, Brazil, Rest of Latin America), Middle East and Africa (United Arab Emirates, South Africa, Rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Threat Intelligence Platforms |

| Security Information and Event Management (SIEM) Feeds | |

| Threat Hunting/Analytics Tools | |

| Services | Managed/Outsourced Services |

| Professional and Consulting | |

| Training and Support |

| On-premise |

| Cloud |

| Hybrid |

| Strategic |

| Tactical |

| Operational |

| Technical |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| IT and Telecommunications |

| Retail and E-commerce |

| Manufacturing |

| Healthcare and Life Sciences |

| Government and Defense |

| Energy and Utilities |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Solutions | Threat Intelligence Platforms |

| Security Information and Event Management (SIEM) Feeds | ||

| Threat Hunting/Analytics Tools | ||

| Services | Managed/Outsourced Services | |

| Professional and Consulting | ||

| Training and Support | ||

| By Deployment | On-premise | |

| Cloud | ||

| Hybrid | ||

| By Threat-Intelligence Type | Strategic | |

| Tactical | ||

| Operational | ||

| Technical | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | BFSI | |

| IT and Telecommunications | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| Energy and Utilities | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the threat intelligence market?

The threat intelligence market is worth USD 10.38 billion in 2026 and is projected to reach USD 18.85 billion by 2031.

Which region leads global demand for threat intelligence solutions?

North America holds the largest regional share at 37.50% of 2025 revenue, supported by advanced cloud uptake and public–private information sharing alliances.

Why are services growing faster than products in this space?

Skills shortages and rising attack complexity drive organisations to outsource threat-hunting and analysis, resulting in a 14.12% CAGR for the Services segment.

How does EU-NIS2 impact corporate spending?

With fines of up to EUR 10 million or 2% of global turnover, the directive compels about 300,000 entities to invest in real-time intelligence for compliance and resilience.

What technologies differentiate leading vendors?

Embedded AI that automates detection and response, open STIX/TAXII interoperability, and integrated cloud-to-edge visibility are primary differentiators among market leaders.

Which vertical shows the fastest growth rate?

The BFSI sector is forecast to expand at a 14.70% CAGR through 2031 as financial institutions bolster defences against ransomware and digital payment fraud.

Page last updated on: