Identity Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

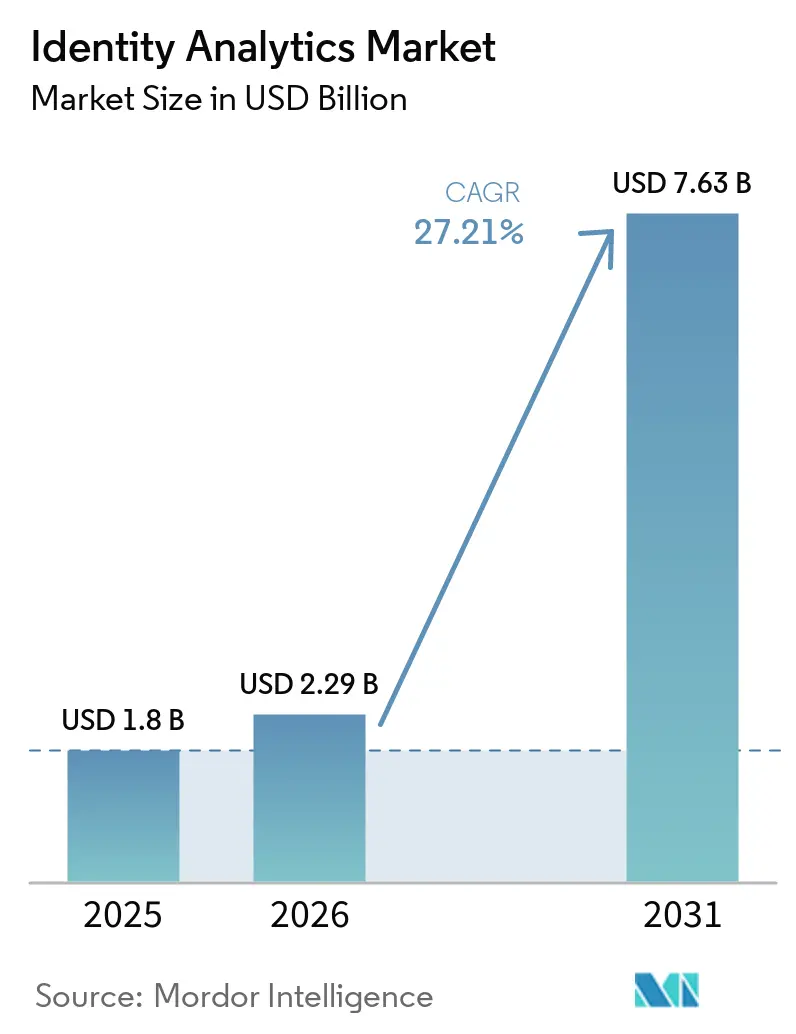

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 7.63 Billion |

| Growth Rate (2026 - 2031) | 27.21% CAGR |

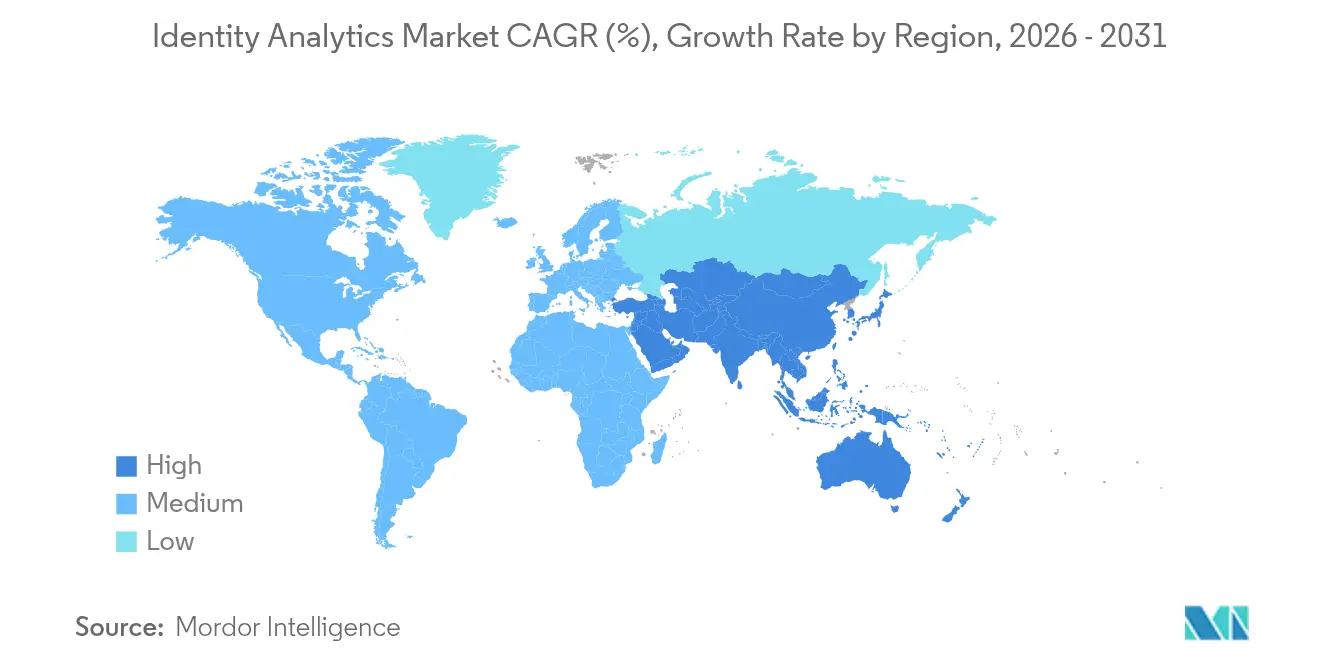

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Analytics Market Analysis by Mordor Intelligence

The identity analytics market size is expected to grow from USD 1.8 billion in 2025 to USD 2.29 billion in 2026 and is forecast to reach USD 7.63 billion by 2031 at 27.21% CAGR over 2026-2031. Surging deepfake attacks, zero-trust compliance deadlines and rapid migration toward cloud-native identity fabrics are steering enterprise budgets toward analytics-driven verification solutions. Executive Order 14144’s phishing-resistant authentication mandate is accelerating public-sector demand and triggering parallel adoption waves across highly regulated private industries. The combination of generative-AI-enabled fraud detection and cyber-insurance incentives is creating measurable return-on-investment arguments, while machine-identity governance requirements extend platform scope far beyond human users. As vendors integrate behavioural biometrics, graph analytics and cryptographic credentialing, the identity analytics market is shifting from optional enhancement to core security infrastructure. [1]Pomerium Team, “Executive Order 14144 Summary,” pomerium.com

Key Report Takeaways

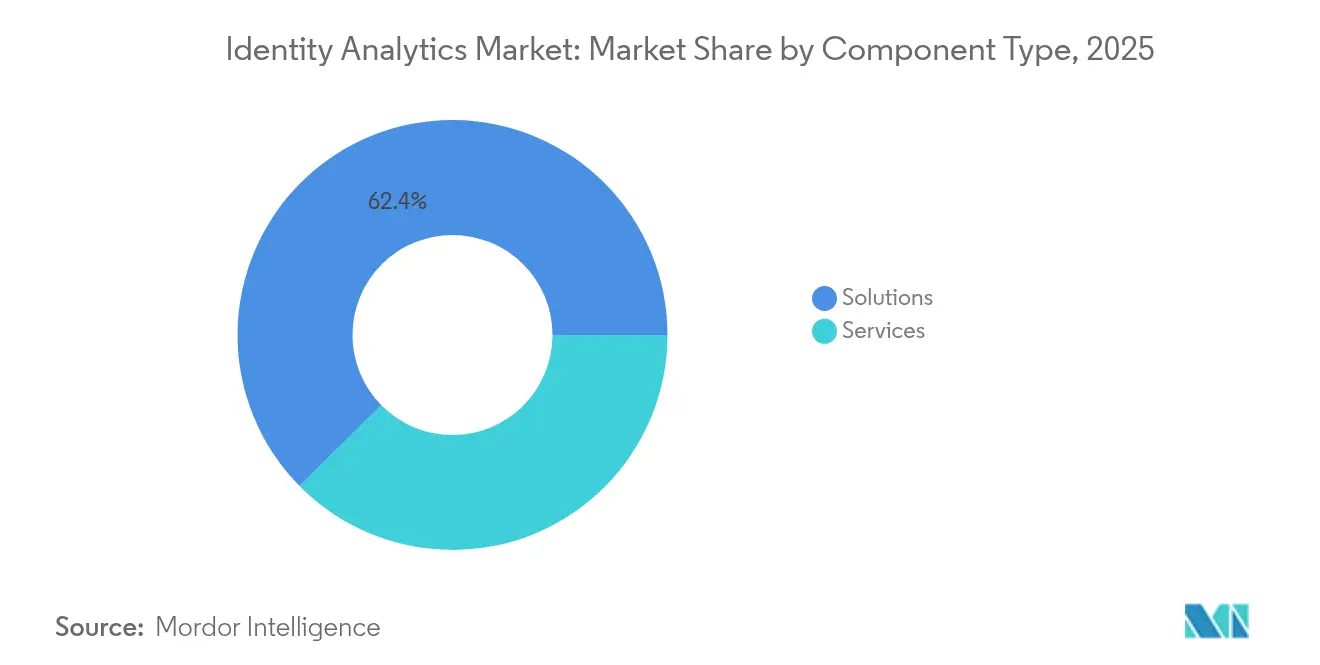

- By component type, solutions led with 62.40% revenue share in 2025, while services are projected to expand at a 33.17% CAGR through 2031.

- By deployment model, cloud held 70.30% of the identity analytics market share in 2025 and is forecast to grow at a 30.62% CAGR.

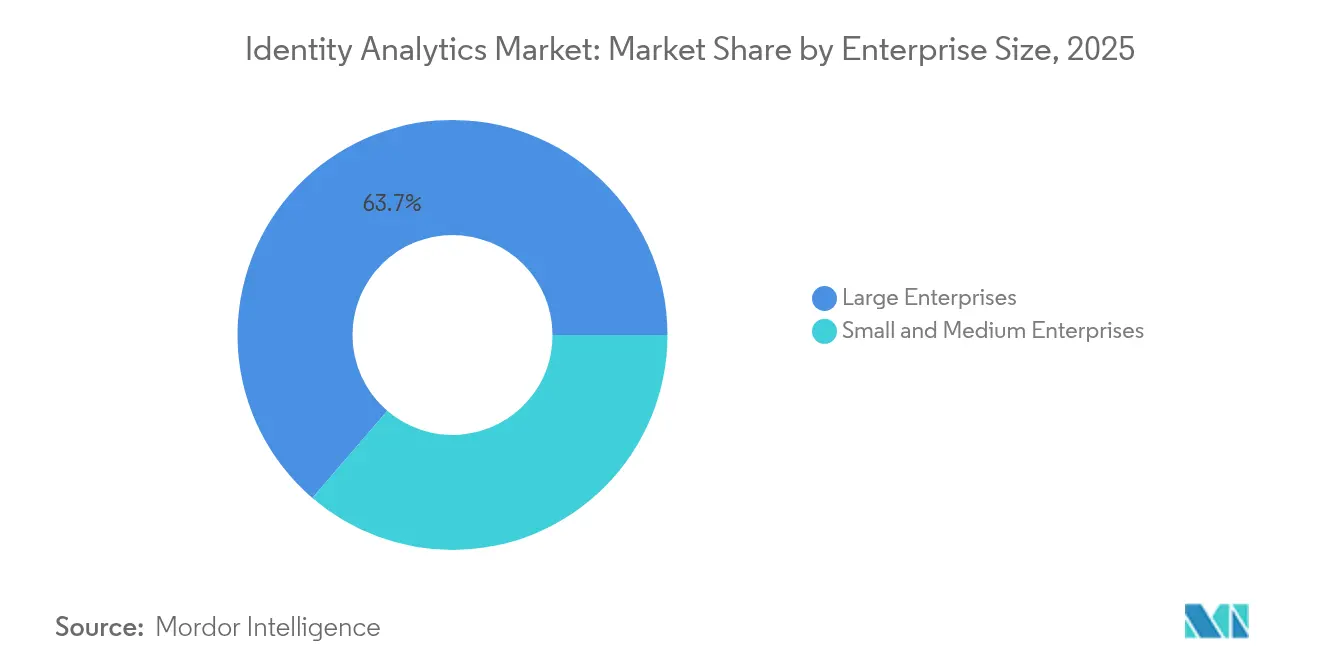

- By enterprise size, large enterprises accounted for 63.70% of the identity analytics market size in 2025; small and medium enterprises record the fastest growth at 31.87% CAGR.

- By end-user industry, the BFSI sector captured 26.60% of the identity analytics market share in 2025, whereas retail and consumer applications are advancing at a 31.28% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Identity Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in deep-fake-driven identity attacks | 6.20% | Global, with concentrated impact in North America & EU | Short term (≤ 2 years) |

| Zero-Trust and machine-identity governance mandates | 5.80% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Migration to cloud-native identity fabric | 4.90% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Gen-AI-based fraud-detection performance gains | 4.10% | Global, with early adoption in BFSI sectors | Short term (≤ 2 years) |

| Cyber-insurance premium discounts tied to analytics | 3.70% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Government-backed eID program roll-outs | 3.40% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Deep-fake-driven Identity Attacks

Deepfake-enabled impersonation skyrocketed 3,000% in 2024, now representing 6.5% of global fraud attempts. Synthetic identities account for 85% of total identity fraud cases, according to the U.S. Department of Homeland Security. The democratization of generative-AI tooling means threat actors can bypass static biometric checks, compelling enterprises to deploy multilayered analytics that fuse behavioural, device and cryptographic signals. Vendors able to detect AI-generated content in real time are winning proof-of-concept trials, and deepfake mitigation is rapidly becoming a core evaluation criterion in competitive tenders. The urgency of this threat elevates identity analytics investments from discretionary spending to board-level risk mitigation. [2]U.S. Department of Homeland Security, “Synthetic Identity Fraud Report,” dhs.gov

Zero-Trust and Machine-Identity Governance Mandates

Executive Order 14144 requires U.S. federal agencies to implement phishing-resistant authentication by December 2025, catalysing broader enterprise zero-trust adoption. Machine-to-machine identities already outnumber human accounts, and unmanaged service credentials expose cloud workloads to lateral-movement attacks. IBM’s integration of HashiCorp technology illustrates a shift toward unified identity fabrics that discover, classify and govern millions of API keys and certificates. Compliance deadlines translate into time-boxed procurement cycles, pushing organizations to favour analytics platforms that ship with embedded governance policies. The resulting demand uplift spans public and private sectors, embedding identity analytics market growth into multi-year budget roadmaps.

Migration to Cloud-native Identity Fabric

Legacy IAM stacks struggle to process high-velocity identity telemetry or support policy-as-code models. SailPoint reports that 60% of its annual recurring revenue now originates from SaaS subscriptions, underscoring the architectural transition. Microsoft’s Entra ID migration guidance highlights the operational intricacies of running on-premises and cloud directories in parallel during multi-year cutovers. Organizations lean on analytics platforms that normalize log formats, reconcile identities across hybrid estates and provide policy insight in real time. This requirement places cloud-native analytics at the center of modernization programs, sustaining double-digit growth even as macro IT spending softens.

Gen-AI-based Fraud-detection Performance Gains

AI-enhanced detection engines are achieving step-change accuracy improvements. Turkish bank Yapı Kredi cut fraud losses by 98.7% across 40 million daily transactions after deploying FICO’s AI models. Vector embeddings and graph analytics surface cross-channel anomalies that rule-based systems miss, reducing false positives and investigation costs. Large language models extend identity verification to unstructured communications, enabling contextual risk scoring for email, chat and voice interactions. Early adopters report measurable ROI, accelerating board approval for analytics refresh budgets. Continuous model training pipelines, delivered through managed services, address in-house talent shortages and sustain performance gains. [3]FICO Communications, “Yapı Kredi Fraud Loss Reduction Case Study,” fico.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO of real-time analytics at petabyte scale | -4.30% | Global, particularly impacting mid-market enterprises | Medium term (2-4 years) |

| Shortage of identity-centric data-science talent | -3.80% | North America & EU, with spillover to APAC | Long term (≥ 4 years) |

| Inter-operability gaps across legacy IAM stacks | -3.20% | Global, concentrated in enterprises with complex IT environments | Medium term (2-4 years) |

| Privacy-by-design regulatory hurdles for UEBA | -2.90% | EU core, expanding to North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO of Real-time Analytics at Petabyte Scale

Processing petabyte-level identity data can push annual infrastructure outlays above USD 10 million for large enterprises, and unexpected query spikes during security incidents aggravate cost volatility. Cloud billing models often lack price predictability when customers ingest streaming logs at sustained throughput. Mid-size organizations therefore delay advanced analytics deployments or limit telemetry retention windows, trading visibility for budget certainty. Managed SaaS models that amortize compute across tenants are gaining traction, but margins remain sensitive to cloud egress and GPU leasing rates. Until cost-management tooling matures, procurement cycles may lengthen for budget-constrained buyers.

Shortage of Identity-centric Data-science Talent

Identity analytics requires professionals versed in adversarial-resilient machine learning, behavioural biometrics and IAM integration. Academic pipelines have been slow to incorporate such interdisciplinary curricula, and global demand far exceeds current supply. Organizations compete for a limited talent pool, inflating salary benchmarks and elongating hiring timelines. Vendors respond by productizing model-development workflows and offering outcome-based managed services. Nevertheless, the scarcity of specialized practitioners remains a structural brake on widespread deployment, particularly for mid-market enterprises lacking brand recognition to attract niche expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Services Scale Despite Solutions Dominance

Solutions retained a 62.40% revenue share in 2025, anchoring the identity analytics market with integrated platforms that deliver governance, risk scoring and orchestration. Yet services revenue is advancing at a 33.17% CAGR, reflecting enterprises' dependence on vendor expertise for migration roadmaps, regulatory alignment and model optimization. The services contribution to the identity analytics market size is forecast to surpass USD 3.54 billion by 2031, underscoring professional consultancies’ role in translating platform capabilities into operational outcomes. Ongoing shortages of identity-centric data scientists further fuel services demand, compelling organizations to engage success-acceleration packages from vendors like SailPoint.

Professional services also address post-implementation challenges such as continuous model tuning and attack-surface reassessment. As executive leadership demands evidence of risk reduction, service teams benchmark fraud metrics, refine detection thresholds and structure remediation workflows. This lifecycle support converts one-time projects into recurring revenue. Conversely, the solutions segment is evolving toward modular micro-services, allowing enterprises to activate analytics functions on demand and pay only for utilized capacity. The interplay between packaged software and high-touch services positions full-stack providers to capture larger wallet share across the identity analytics market.

By Deployment Model: Cloud Accelerates Legacy Modernization

Cloud deployments represented 70.30% of 2025 revenue and are projected to grow at 30.62% over the forecast horizon, driven in part by enterprise legacy modernization initiatives. Demand is fuelled by elastic compute, API-first integration and built-in high availability. Many organizations, however, operate hybrid estates during multiyear transitions, with parallel on-premises and SaaS directories. This coexistence phase elevates analytics workloads because data must be collected across both environments and correlated in real time. Cloud platforms therefore emphasize connector breadth and policy reconciliation engines that interpret legacy attribute structures.

Identity analytics market share is shifting decisively toward consumption-based pricing, and insurers such as AIG now link premium discounts to customers that evidence continuous monitoring via cloud platforms. Migration roadmaps are informed by Microsoft’s published Entra ID playbooks and reference architectures, setting de-facto industry implementation patterns. While total cost of ownership can rise during dual-running periods, long-term economics favour cloud models once on-premises hardware refresh cycles are avoided. Vendors offering granular usage billing and cross-tenant data isolation are positioned to win procurement rounds, especially within multinational enterprises subject to data-residency regulations.

By Enterprise Size: SMEs Drive Democratization Through MSPs

Large enterprises controlled 63.70% of 2025 spending, leveraging scale to deploy bespoke analytics layers and run cross-border governance programs. Yet SMEs are forecast to grow at 31.87% annually through 2031. Managed service providers (MSPs) are central to SME adoption, bundling identity analytics with endpoint management, help desk and compliance audits. JumpCloud notes that 42% of SMEs outsource full-stack IT operations, illustrating the distribution channel’s relevance. As insurance underwriters extend cyber-risk coverage only to customers demonstrating continuous identity monitoring, many SMEs perceive analytics not as optional but as a prerequisite for affordable protection.

Cloud-native design lowers entry barriers by removing high up-front licensing and infrastructure commitments. Vendors are packaging use-case-specific starter tiers that analyse authentication flows, privilege escalations and anomalous device fingerprints. Automated model-training pipelines address skills gaps, while intuitive dashboards guide MSP technicians who may lack deep data-science backgrounds. These dynamics expand the addressable base of the identity analytics market and reinforce its role in levelling security capabilities between large and small organizations.

By End-user Industry: BFSI Leadership Faces Retail Disruption

The BFSI sector captured 26.60% of 2025 revenue, anchored by stringent anti-money-laundering regulations and high financial exposure to account-takeover fraud. Banks deploy behavior analytics to evaluate transaction velocity, geolocation anomalies and device parity. Yet retail and consumer applications are projected to grow the fastest at a 31.28% CAGR on the back of e-commerce fraud losses that exceeded USD 48 billion in 2024. Mass-market platforms adopt passive biometrics to minimize shopper friction while detecting bots, credential stuffing and synthetic personas.

Outside these two verticals, healthcare providers accelerate deployment after breaches such as Blue Shield of California’s inadvertent PHI exposure, which underscored gaps in consent management. The public sector faces immovable zero-trust deadlines, while energy utilities expand analytics to operational technology layers where compromised identities can trigger physical safety incidents. Collectively, these dynamics diversify revenue streams and reduce concentration risk within the identity analytics market, supporting its long-run growth trajectory.

Geography Analysis

North America retained a 41.60% revenue share in 2025, buoyed by the Executive Order 14144 mandate and a dense concentration of analytics vendors. Federal deadlines drive near-term spending spikes, while U.S. enterprises leverage favourable cyber-insurance economics tied to advanced identity postures. Canada’s digital credential framework and Mexico’s burgeoning fintech ecosystem contribute incremental growth, reinforcing regional leadership. Compliance alignment with NIST SP-800-63 guidelines further stimulates platform upgrades and positions North America as the reference market for zero-trust maturity.

Europe follows closely, propelled by the European Digital Identity Regulation that requires interoperable wallet solutions by 2027. The United Kingdom already hosts 270 digital-identity companies, generating USD 2.05 billion in annual revenue. Germany and France emphasize privacy-by-design, obliging vendors to embed consent orchestration and policy versioning into analytics workflows. Data-sovereignty clauses and cross-border transfer rules drive demand for regional data centers and encryption-in-use capabilities. As a result, cloud providers expand European availability zones to accommodate localized processing and maintain competitive parity.

Asia-Pacific represents the fastest-growing region with a 32.86% CAGR forecast through 2031. Government-backed eID schemes, such as Indonesia’s USD 1.2 billion digital-transformation partnership and Australia’s Digital ID Act 2024, establish mandatory verification layers that require analytics at scale. India’s Aadhaar success and China’s vast volume of digital transactions provide proof points for neighbouring economies, catalysing uptake across ASEAN. The region’s investment in 5G infrastructure and mobile-money adoption creates high-velocity identity telemetry that demands cloud-based analytic performance. Vendors offering language-agnostic interfaces and regionally hosted data options are well placed to gain share as cross-border digital-commerce expands.

Competitive Landscape

The identity analytics market exhibits moderate fragmentation, yet consolidation is accelerating. CyberArk’s USD 1.66 billion acquisition of Venafi integrates machine-identity protection with privileged access management, expanding detection breadth across human and non-human entities. SailPoint’s USD 1.05 billion IPO at an USD 11.5 billion valuation signals investor belief that unified identity platforms will command premium multiples. IBM’s alliance with HashiCorp underscores the shift toward end-to-end identity fabrics and managed secrets engines, responding to enterprise preference for single-vendor accountability.

Incumbents and disruptors compete intensely on AI competencies. Vendors incorporating synthetic-media detection algorithms and adversarial-trained models differentiate in procurement scorecards. Patent filings in quantitative document-image analysis and behavioural-sequence clustering highlight ongoing intellectual-property races. Customer references that quantify fraud-loss reductions, such as Yapı Kredi’s 98.7% improvement, carry high persuasive value in RFP cycles.

Niche white-space opportunities remain. Healthcare identity analytics remains underpenetrated despite regulatory imperatives and reputational risk. Manufacturing, energy and utilities confront IT-OT convergence challenges that expose industrial controllers to identity attacks, yet few analytics suites currently integrate operational-technology telemetry. Vendors offering tailored connectors and low-code policy design are positioned to capture these segments. Overall rivalry is intensifying, and convergence of analytics, governance and secrets management is steering the market toward platform plays.

Identity Analytics Industry Leaders

Okta Inc.

SailPoint Technologies Holdings Inc.

Oracle Corporation (Security & Identity Analytics sub-segment)

International Business Machines Corporation

IBM Security

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SailPoint announced pricing of its upsized IPO of 60 million shares at USD 23.00, targeting an USD 11.5 billion valuation.

- January 2025: Executive Order 14144 mandated phishing-resistant authentication for U.S. federal agencies, setting December 2025 deadlines.

- December 2024: SailPoint and Imprivata completed a strategic partnership focused on healthcare identity governance.

- November 2025: CyberArk closed the USD 1.66 billion acquisition of Venafi, merging human and machine identity security.

Global Identity Analytics Market Report Scope

Identity analytics solutions allow businesses to define and manage roles and automate vital identity-based controls. Once the roles are certified and assigned, the software solutions continue to deliver scalable identity governance. The market scope of identity analytics tracks the adoption of different solutions and services used by several end-use industries across major regions. The study also focuses on the impact of COVID-19 on the identity analytics market ecosystem.

The identity analytics market is segmented into component type (solutions, services), deployment (on-premise, cloud), enterprise size (small & medium enterprises, large enterprises), end-users (IT & telecommunication, BFSI, government, retail & consumer, healthcare), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| On-Premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Information Technology and Telecommunication |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| Retail and Consumer |

| Healthcare and Life Sciences |

| Manufacturing, Energy and Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component Type | Solutions | |

| Services | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Industry | Information Technology and Telecommunication | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Public Sector | ||

| Retail and Consumer | ||

| Healthcare and Life Sciences | ||

| Manufacturing, Energy and Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the identity analytics market and how fast is it growing?

The market is valued at USD 2.29 billion in 2026 and is forecast to expand to USD 7.63 billion by 2031, advancing at a 27.21% CAGR.

Which component segment is expanding the fastest?

Services are growing the quickest, recording a 33.17% CAGR through 2031 as enterprises seek implementation expertise and continuous model tuning.

Why is cloud deployment preferred for identity analytics platforms?

Cloud models provide elastic compute, API-first integration and built-in availability, enabling real-time analysis of high-volume identity telemetry while cutting long-term infrastructure costs.

How are deepfake attacks influencing spending decisions?

A 3,000% surge in deepfake-enabled fraud during 2024 has pushed organizations to prioritize analytics platforms capable of detecting AI-generated content in real time, turning mitigation into a board-level imperative.

Which region is projected to grow the fastest and why?

Asia-Pacific is forecast to grow at a 32.86% CAGR to 2031, fueled by large-scale government eID programs, rapid digital-commerce adoption and substantial cloud-infrastructure investments.

What sectors outside BFSI are showing strong momentum for identity analytics adoption?

Retail & consumer sectors are advancing at a 31.28% CAGR due to rising e-commerce fraud losses, while healthcare, manufacturing and utilities are accelerating deployments to counter data-privacy, IT/OT convergence and safety risks.

Page last updated on: