Information Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

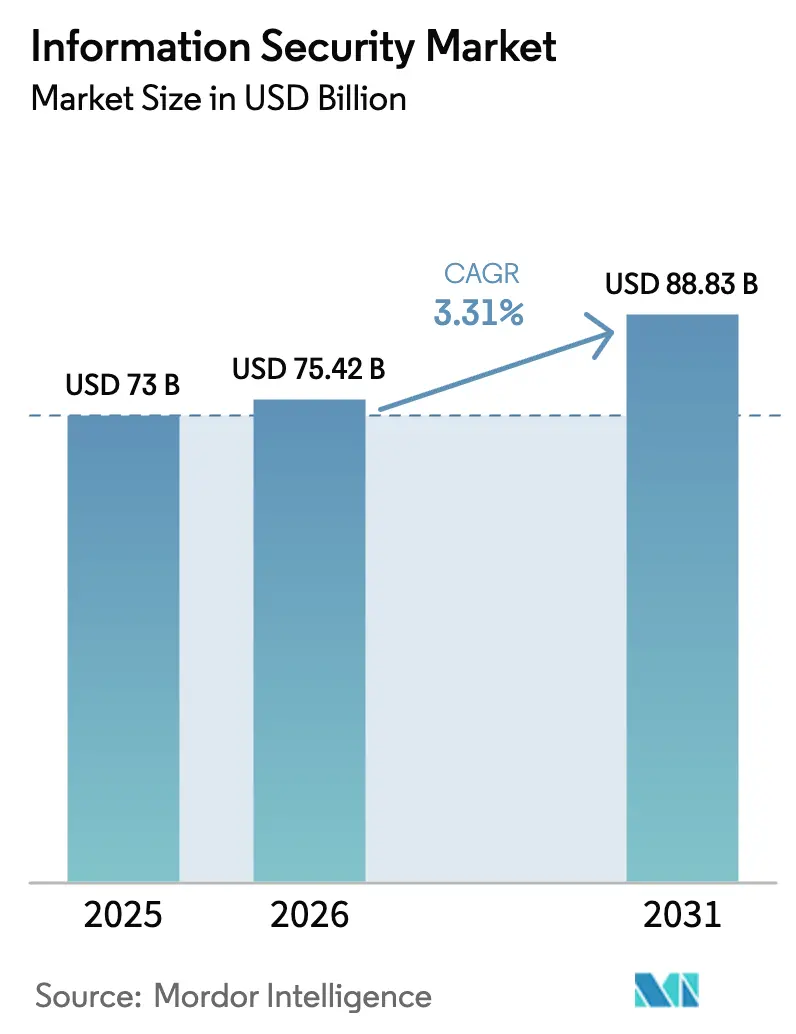

| Market Size (2026) | USD 75.42 Billion |

| Market Size (2031) | USD 88.83 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

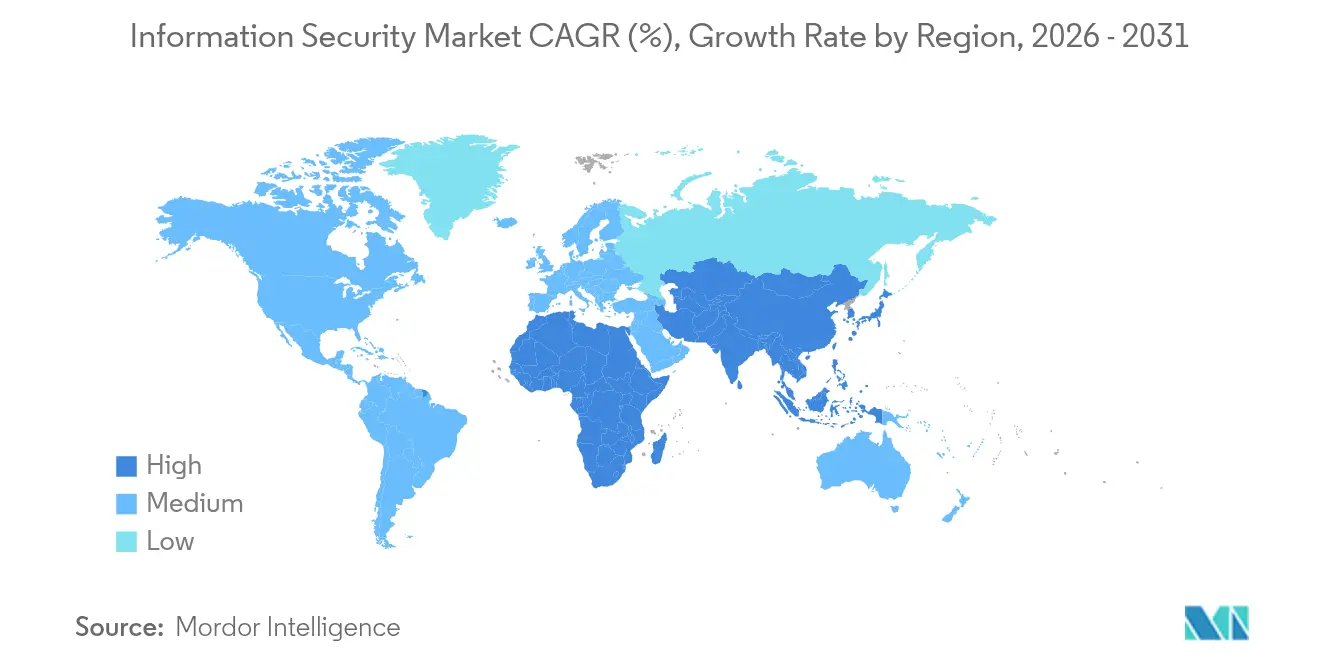

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

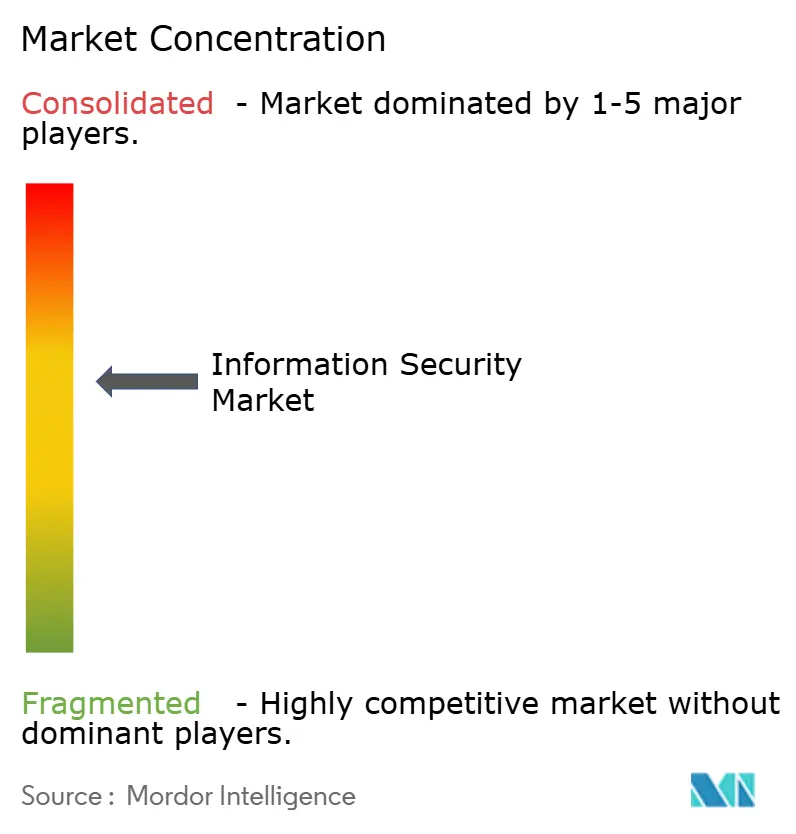

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Information Security Market Analysis by Mordor Intelligence

The information security market size is expected to grow from USD 73.00 billion in 2025 to USD 75.42 billion in 2026 and is forecast to reach USD 88.83 billion by 2031 at 3.31% CAGR over 2026-2031. Managed services, AI-enabled threat analytics and zero-trust roll-outs sustain revenue growth even as many enterprises rationalize the number of tools they operate. Vendor consolidation is reshaping competition, with integrated XDR platforms gradually displacing isolated point products. Rapid cloud-native application adoption and the spike in API-centric attacks are forcing organizations to modernize protection architectures. A persistent shortage of 4.8 million cyber professionals continues to channel spending toward outcome-based managed security services. Asia-Pacific delivers the fastest regional expansion, while North America preserves scale leadership amid heightened regulatory scrutiny.

Key Report Takeaways

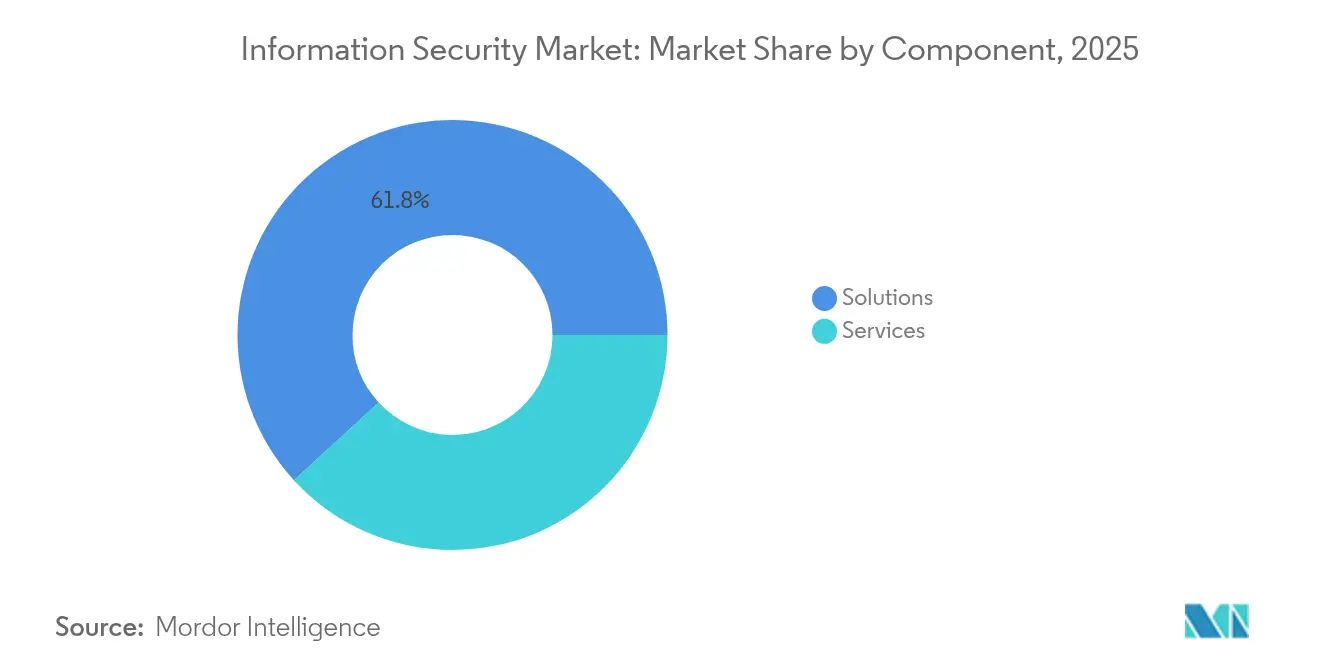

- By component, Solutions commanded 61.80% of the information security market share in 2025; Services are projected to expand at a 3.54% CAGR through 2031.

- By deployment model, Cloud captured 57.60% revenue share of the information security market size in 2025 and is forecast to grow at a 3.71% CAGR to 2031.

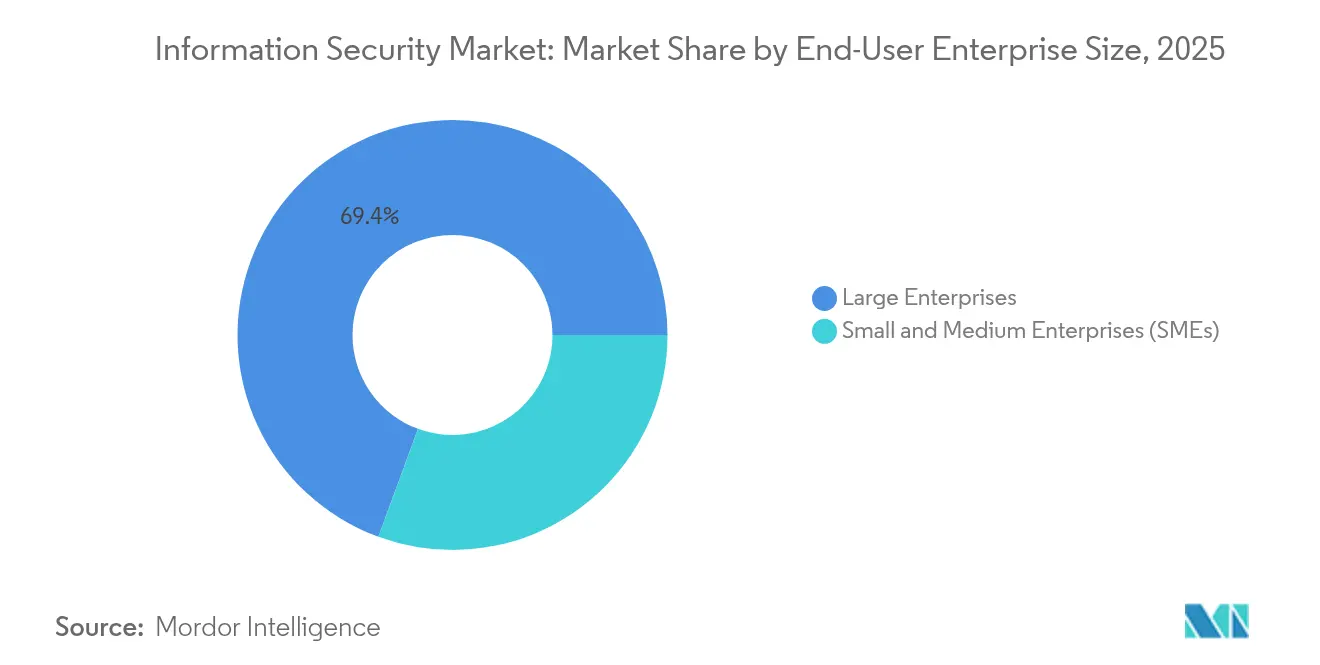

- By end-user enterprise size, Large Enterprises held 69.40% share of the information security market in 2025, whereas SMEs are set to grow at 3.9% CAGR.

- By end-user industry, BFSI led with 30.30% information security market share in 2025; Healthcare is advancing at a 4.7% CAGR through 2031.

- By geography, North America accounted for 39.00% of 2025 revenue, while Asia-Pacific is projected to post the fastest 4.17% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Information Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging cloud-native application adoption | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Growing zero-trust architecture mandates | +0.7% | North America and EU, rising in Asia-Pacific | Long term (≥ 4 years) |

| Explosion of API-centric attacks | +0.6% | Global, concentrated in financial hubs | Short term (≤ 2 years) |

| Expansion of 5G and edge computing footprints | +0.5% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Vendor consolidation to integrated XDR platforms | +0.4% | North America and EU enterprise markets | Medium term (2-4 years) |

| Quantum-ready cryptography investments | +0.3% | Government and critical infrastructure worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cloud-Native Application Adoption

Cloud-native architectures demand container security, service-mesh defense and runtime protection. Organizations running microservices maintain 40% more security tools than traditional estates, intensifying the need for unified platforms that span multi-cloud deployments. Eighty-four percent of enterprises admit to gaps in container protection, while spending on cloud-native security is rising 25% annually through 2027. DevSecOps pipelines that embed automated testing and compliance checks are becoming a baseline requirement as release cadences accelerate.

Growing Zero-Trust Architecture Mandates

Zero-trust has shifted from best practice to imposed standard. The U.S. federal roadmap requires agency-wide identity verification by 2026, opening a USD 7.1 billion procurement window for identity and access management vendors. Commercial deployments average 18-24 months, creating multi-year revenue visibility for suppliers. Firms completing zero-trust roll-outs record 45% lower breach costs, supporting premium license pricing. Continuous user and device validation stimulates demand for behavioral analytics that can evaluate risk in real time across hybrid environments.

Explosion of API-Centric Attacks

Financial institutions report APIs as their top vulnerability, with 95% facing an incident in 2024. Dynamic API inventories, runtime behavior analytics and automated response have turned into core purchase criteria. Regulatory pressure is mounting for documented API inventories and regular penetration testing, ensuring sustained investment in dedicated API security platforms.

Expansion of 5G and Edge Computing Footprints

Low-latency 5G services push processing to the edge, where localized protection is essential. Edge devices form vast, distributed attack surfaces that traditional perimeter models cannot defend. Manufacturing and healthcare use cases dominate early spending, driving demand for lightweight agents and edge-native zero-trust solutions [1]Eviden, “Securing the Edge in 5G Networks,” eviden.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global cyber-talent shortage | -0.5% | Global, acute in North America and EU | Long term (≥ 4 years) |

| Rising tool sprawl and alert fatigue | -0.4% | Enterprise markets worldwide | Medium term (2-4 years) |

| Data-sovereignty and cross-border transfer hurdles | -0.3% | EU and Asia-Pacific | Long term (≥ 4 years) |

| Escalating open-source software vulnerabilities | -0.2% | Global development ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global Cyber-Talent Shortage

A 4.8 million-person skills gap limits organizations’ capacity to install and manage defenses [2]ISC2, “Cybersecurity Workforce Study 2024,” isc2.org . Cyber roles stay open six months on average, with cloud security architects unfilled for 12 months. Salaries run 25-40% above comparable IT positions, inflating program costs. SMEs suffer most, steering demand toward managed security service providers that deliver expertise on subscription.

Rising Tool Sprawl and Alert Fatigue

Security operations teams juggle 60-75 tools, spending 40% of their time on integration and maintenance. Ninety percent report alert fatigue, and 62% ignore alerts because of false positives, eroding the value of existing investments. Consolidation onto integrated XDR or SIEM-plus-analytics platforms promises relief but migration entails legacy disentanglement that slows adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Reinforces Platform Shift

Solutions dominated with 61.80% revenue share in 2025, yet Services are expanding faster at 3.54% CAGR as enterprises outsource deployment and monitoring. Managed Security Services give customers 24×7 coverage without hiring scarce talent. The information security market size for Services is projected to reach USD 34.36 billion by 2031, reflecting growing reliance on outcome-based contracts. Platform vendors are embedding consulting and incident response to secure recurring revenue.

Solutions growth moderates as buyers favor fewer, broader platforms over isolated tools. Identity and Access Management retains pricing power because of zero-trust mandates, whereas standalone UTM devices face commoditization. Traditional SIEM products are evolving into AI-infused XDR suites that supply unified detection across endpoints, networks and cloud workloads. Vendors unable to demonstrate seamless orchestration risk displacement during refresh cycles.

By Deployment: Cloud Dominance Reshapes Architecture

Cloud models captured 57.60% share in 2025 and are on course for a 3.71% CAGR through 2031. Organizations adopting cloud-delivered controls report 30% lower total cost of ownership relative to comparable on-premise estates. The information security market size attached to cloud deployments is expected to climb to USD 52.34 billion by 2031. Zero-trust alignment, subscription pricing and simplified maintenance reinforce the preference for cloud.

On-premise solutions remain critical in regulated sectors such as defense and utilities where data residency is mandatory. Hybrid architectures that anchor sensitive workloads on-site while leveraging cloud analytics for scale are becoming standard. Vendors capable of policy consistency across hybrid footprints gain strategic advantage; legacy on-premise suppliers face margin compression as clients migrate.

By End-User Enterprise Size: SME Adoption Accelerates

Large Enterprises held 69.40% revenue share in 2025, propelled by expansive budgets and intricate risk profiles. These organizations prioritize platform consolidation, AI-augmented analytics and automated incident response. Average security budgets top USD 50 million among Fortune 500 companies, and they influence vendor roadmaps through demanding proof-of-value pilots.

SMEs post the steeper 3.9% CAGR because cloud-native solutions strip high upfront costs. Managed security offerings deliver enterprise-grade coverage without in-house SOCs, and outcome-based subscriptions convert capex into opex. The information security market share for SMEs is thus poised to expand as regulatory demands reach mid-market companies and cyber insurance policies require baseline controls.

By End-User Industry: Healthcare Leads Digital Transformation

BFSI contributed 30.30% of 2025 revenue, driven by stringent audit regimes and high-value data. Institutions prioritize continuous authentication, advanced fraud analytics and secure open-banking APIs. Their appetite for integrated threat-intel feeds and 24×7 managed detection keeps pressure on vendors to deliver low-latency incident response.

Healthcare is the fastest climber at 4.7% CAGR. Electronic health records, telemedicine and connected devices expand attack surfaces, pushing hospital cybersecurity budgets from 10% to 15% of IT spend by 2027. Vendors offering HIPAA-ready, cloud-native platforms with medical-device visibility secure competitive advantage. Manufacturing, energy and utilities follow with industrial IoT and SCADA security requirements that demand specialized OT-centric solutions.

Geography Analysis

North America sustained 39.00% revenue share in 2025 on the back of large enterprise budgets, aggressive zero-trust deadlines and federal investment programs. The region favors integrated XDR suites and identity platforms that streamline tool estates. Cloud adoption is mature, and spending emphasis is shifting to AI-driven analytics and managed detection services.

Asia-Pacific is the fastest-growing territory at 4.17% CAGR during 2026-2031. Government digital agendas in China, India and Japan, combined with rising data localization rules, fuel domestic cybersecurity investment. Local vendors that align with regulatory nuances gain traction, yet global suppliers remain influential where advanced analytics or specialized zero-trust solutions are required. Hybrid cloud adoption and 5G roll-outs further widen edge security demand.

Europe maintains steady uptake supported by GDPR and the incoming NIS 2 Directive. Data-sovereignty imperatives elevate interest in encryption, key-management and sovereign cloud solutions. Germany and the United Kingdom lead spending, while France and Italy accelerate migration toward cloud-delivered controls. Vendor consolidation is visible as enterprises streamline suppliers to ease compliance reporting and lower operational overhead.

Competitive Landscape

The information security market is moderately fragmented despite 362 acquisitions worth USD 49.9 billion in 2024. Strategic buyers pursue horizontal platform breadth and vertical specialization to control adjacent threat vectors. Hewlett Packard Enterprise paid USD 13.247 billion for Juniper to embed networking security into edge-to-cloud offerings. IBM’s USD 6.4 billion bid for HashiCorp adds infrastructure automation that tightens cloud-native posture management.

Mastercard acquired Recorded Future for USD 2.65 billion to integrate threat intelligence into payment-security services [3]Mastercard, “Mastercard to Acquire Recorded Future,” mastercard.com. These moves illustrate three dominant playbooks: platform consolidation, vertical depth in health or industrial sectors, and regional expansion with localized compliance capabilities. Differentiation centers on AI-assisted triage, automated remediation, and unified policy management across hybrid estates.

White-space opportunities persist in 5G edge security, quantum-ready encryption, and advanced API analytics. Vendors showcasing lightweight agents and machine-learning correlation gain mindshare. Pricing models shift toward usage-based subscriptions and managed bundles, aligning incentives with measurable security outcomes while smoothing revenue cycles for suppliers.

Information Security Industry Leaders

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cyble launched Cyble Titan, an endpoint platform integrated into its AI-Native Security Cloud for asset visibility, intelligence-led detection and automated response.

- May 2025: Cisco released Duo Identity and Access Management to combat identity-based attacks proliferating in the AI era.

- February 2025: Sophos completed its USD 859 million acquisition of Secureworks, adding managed services to the Taegis XDR platform.

- November 2024: Bitsight bought Cybersixgill for USD 115 million to enhance external attack-surface intelligence.

Global Information Security Market Report Scope

Information security (InfoSec) covers the tools and processes that organizations use to protect information. This includes policy settings that prevent unauthorized people from accessing business or personal information.

The information security market is segmented by type (solution, services), by deployment (cloud, on-premises), by enterprises (SMEs, large enterprises), by end-user (BFSI, IT and telecom, healthcare, retail and ecommerce, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Identity and Access Management (IAM) |

| Unified Threat Management (UTM) | |

| Security Information and Event Management (SIEM) | |

| Endpoint Protection Platforms (EPP) | |

| Extended Detection and Response (XDR) | |

| Data Loss Prevention (DLP) | |

| Services | Professional Services |

| Managed Security Services (MSS) |

| On-premise |

| Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Government and Defense |

| Manufacturing |

| Energy and Utilities |

| Others (Education, Hospitality, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | Identity and Access Management (IAM) | |

| Unified Threat Management (UTM) | |||

| Security Information and Event Management (SIEM) | |||

| Endpoint Protection Platforms (EPP) | |||

| Extended Detection and Response (XDR) | |||

| Data Loss Prevention (DLP) | |||

| Services | Professional Services | ||

| Managed Security Services (MSS) | |||

| By Deployment | On-premise | ||

| Cloud | |||

| By End-user Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Government and Defense | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Others (Education, Hospitality, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the information security market?

The information security market size reached USD 75.42 billion in 2026 and is forecast to attain USD 88.83 billion by 2031.

Which component segment is growing fastest?

Services, especially managed security services, are rising at a 3.54% CAGR as firms outsource skills they lack.

Why is Asia-Pacific the fastest-growing region?

Digital transformation initiatives, 5G deployments and tightening data-sovereignty rules are pushing Asia-Pacific growth at 4.17% CAGR.

How does zero-trust architecture influence spending?

Mandatory zero-trust deadlines, such as the U.S. federal 2026 target, are driving multi-year investments in identity, access management and behavioral analytics.

Page last updated on: