Unified Threat Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

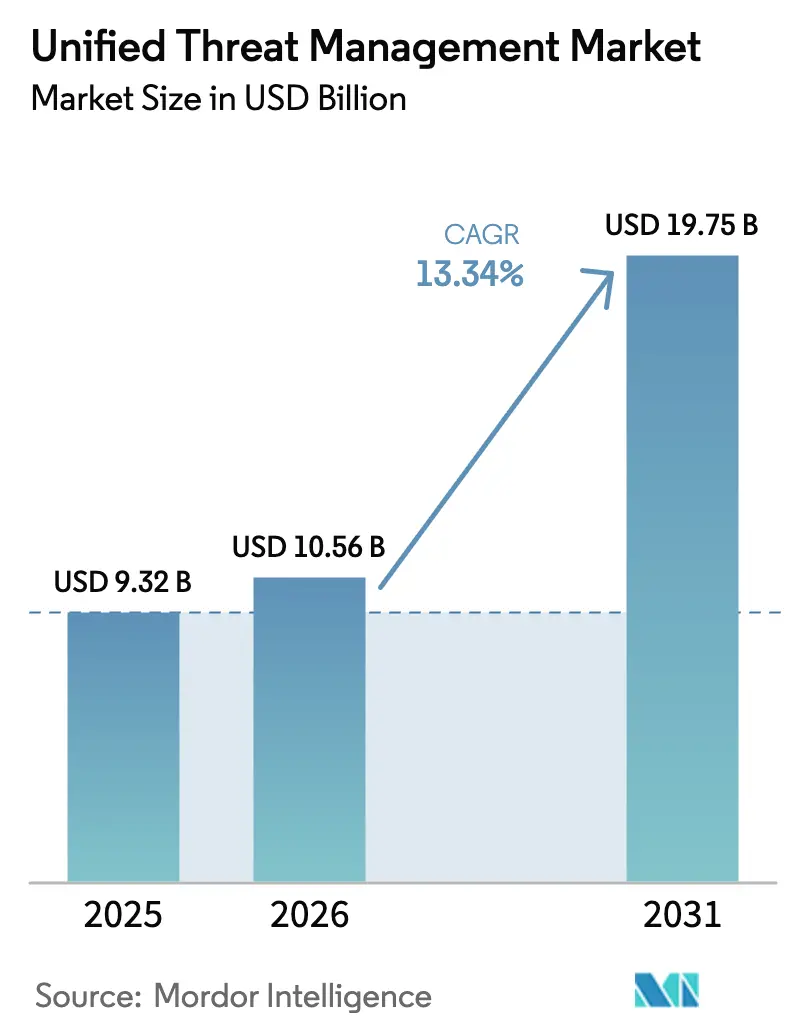

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 19.75 Billion |

| Growth Rate (2026 - 2031) | 13.34% CAGR |

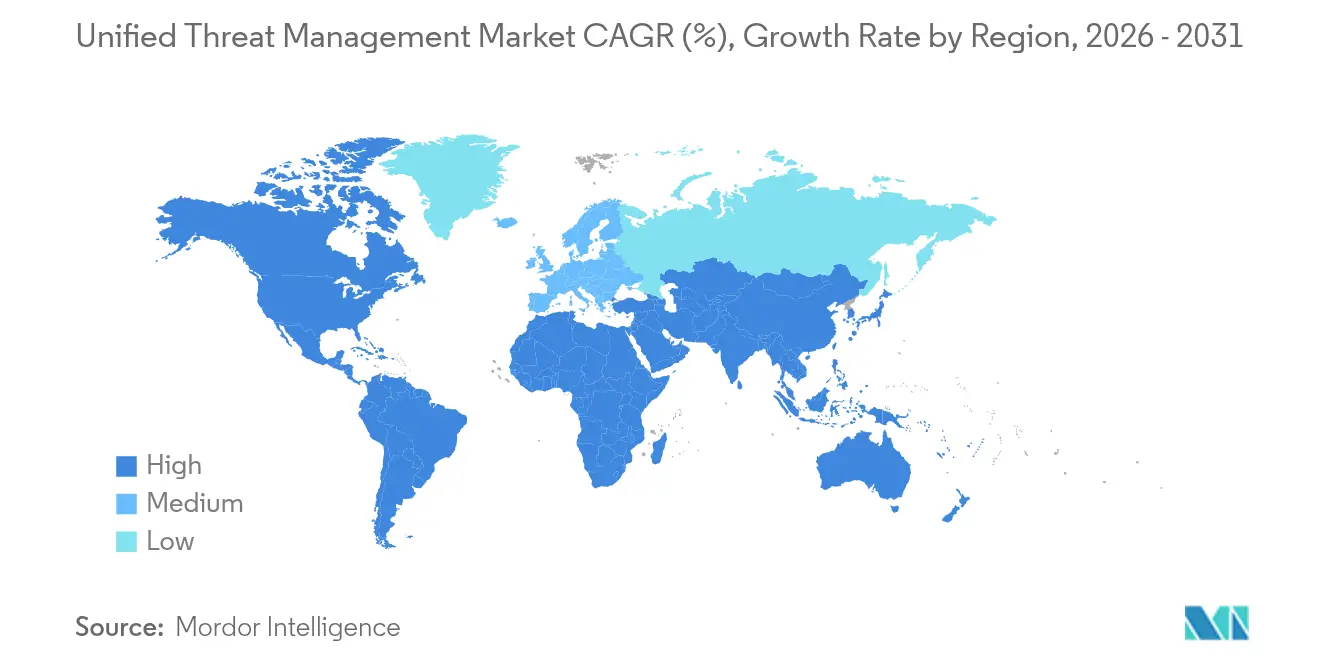

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

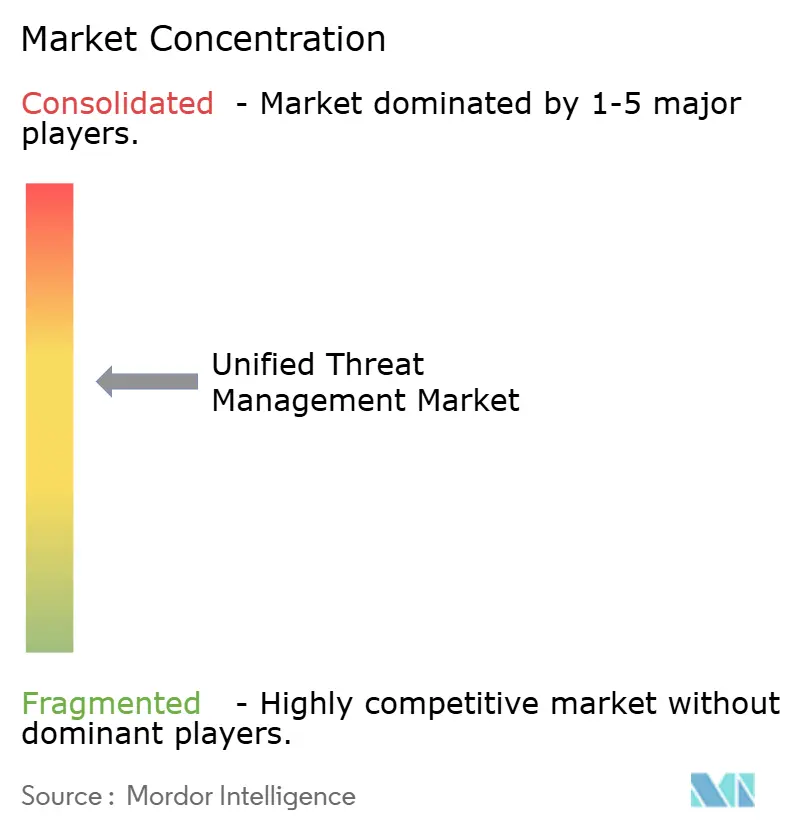

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unified Threat Management Market Analysis by Mordor Intelligence

The Unified Threat Management market size was valued at USD 9.32 billion in 2025 and estimated to grow from USD 10.56 billion in 2026 to reach USD 19.75 billion by 2031, at a CAGR of 13.34% during the forecast period (2026-2031). This expansion reflects how enterprises are retiring siloed appliances in favor of cloud-delivered and software-defined protection that adapts to remote work and edge computing. Software components lead adoption because updates arrive instantly without hardware swaps, while cloud deployments remove the throughput constraints that once hampered fully enabled appliances. Large enterprises sustain spending power, yet the accelerating demand from small and medium businesses signals wider democratization of advanced security. Geographically, North America supplies the core revenue base, but Asia-Pacific is moving faster on the back of data-sovereignty laws, manufacturing digitalization, and new maritime cybersecurity rules.

Key Report Takeaways

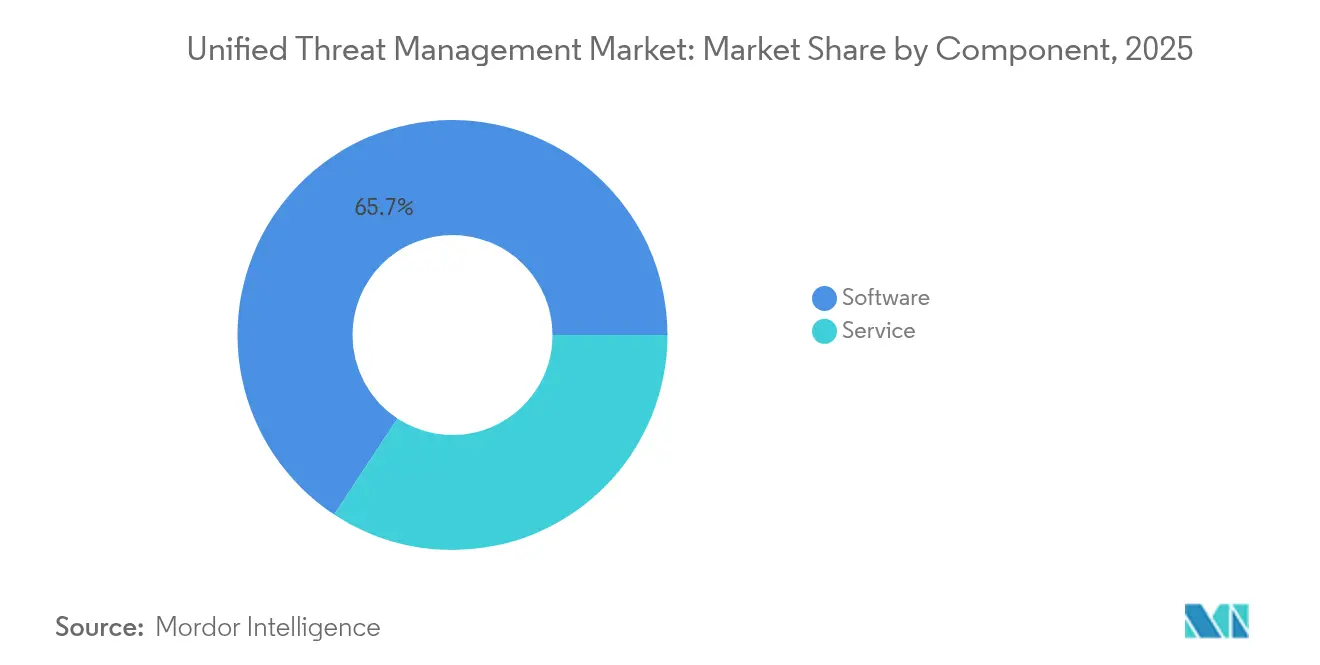

- By component, software captured 65.72% of Unified Threat Management market share in 2025.

- By deployment model, cloud held 57.65% of the Unified Threat Management market size in 2025 and is set to expand at a 13.92% CAGR to 2031.

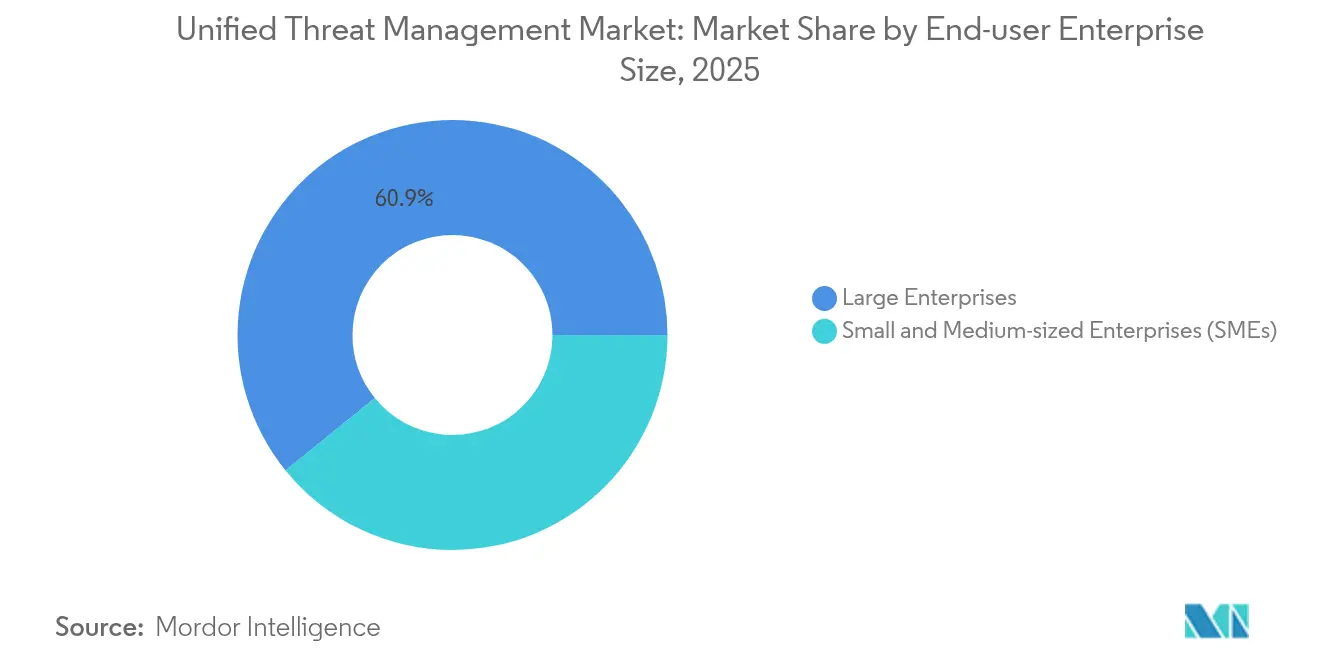

- By organization size, small and medium enterprises are advancing at a 14.48% CAGR through 2031, while large enterprises retained 60.85% revenue share in 2025.

- By end-user industry, financial services led with 24.21% revenue share in 2025; IT and telecommunications is projected to grow at a 14.55% CAGR to 2031.

- By geography, North America accounted for 36.62% of revenue in 2025, whereas Asia-Pacific is forecast to grow at an 18.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Unified Threat Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid SMB adoption of cost-effective integrated security appliances | +2.1% | Global with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Convergence with SD-WAN / SASE architectures | +2.8% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Surge in AI-driven polymorphic malware and need for unified analytics | +2.4% | Global | Short term (≤ 2 years) |

| Regulatory push for consolidated audit trails | +1.9% | EU and Asia-Pacific core with spill-over to Americas | Medium term (2-4 years) |

| Edge-cloud proliferation in Industry 4.0 networks | +1.7% | Asia-Pacific core, North America and EU manufacturing hubs | Long term (≥ 4 years) |

| Maritime and fleet-secure mandates creating niche UTM demand | +0.8% | Global maritime routes concentrated in Singapore, Rotterdam, Long Beach | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid SMB adoption of cost-effective integrated security appliances

Small and medium businesses increasingly pivot toward UTM boxes because separate firewalls, intrusion prevention, and content filters strain limited budgets and staff. Forty-three percent of SMBs faced attacks in 2024, yet many run with lean IT teams. An all-in-one unit trims capital outlay and day-to-day management while still meeting regulatory basics. Managed service providers now bundle UTM devices into fixed-price packages, doubling recurring revenue in some cases. Vendors that package enterprise-grade controls in simplified appliances are capturing loyalty in a price-sensitive segment.[1]American Bureau of Shipping, “Cybersecurity Requirements for Machinery and Control Systems,” eagle.org

Convergence with SD-WAN / SASE architectures

Networking and security teams want a single control pane that steers traffic and inspects it at once. Cisco has blended Catalyst SD-WAN with Microsoft Security Service Edge so users gain policy-based routing plus threat prevention on the same cloud edge.[2]Cisco Systems, “Catalyst SD-WAN and Microsoft SSE Integration,” cisco.com Seventy-nine percent of enterprises surveyed intend to fold web, cloud service, and private-app access under converged SASE by 2025, forcing legacy UTM suppliers to extend beyond appliance footprints. Fortinet’s Unified SASE annual recurring revenue rose 25.7% to USD 1.15 billion in 2025, underscoring momentum toward integrated cloud delivery Fortinet.[3]Fortinet, “2025 Investor Presentation,” fortinet.com

Surge in AI-driven polymorphic malware and need for unified analytics

Threat actors now automate code mutation to sidestep signature detection. Unified platforms that ingest firewall logs, intrusion alerts, and user behavior in one stream can apply machine-learning models for faster correlation. Palo Alto Networks added real-time controls for generative AI app usage inside its Prisma stack in 2025.[4]Palo Alto Networks, “Prisma SASE Enhancements,” paloaltonetworks.com Check Point shipped six AI-powered functions within Infinity to counter evasive threats. Organizations conclude that piecemeal tools cannot pivot quickly enough, so the Unified Threat Management market benefits from consolidated analytical depth.

Regulatory push for consolidated audit trails

NIS2 in the EU, Singapore’s strengthened Cybersecurity Act, and incoming US Coast Guard rules all raise the bar for log retention and incident reporting. UTM platforms automate collection from multiple engines and generate standardized reports, cutting compliance labor. Ship operators moving cargo through European and US ports must store cybersecurity event logs beginning July 2025, steering vessel owners toward purpose-built maritime UTM appliances. Vendors able to certify out-of-the-box audit functions gain an edge with regulated sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance bottlenecks when all services enabled | -2.3% | Global, especially high-bandwidth sites | Short term (≤ 2 years) |

| Migration to cloud-native SSE reducing on-prem UTM refresh cycles | -1.8% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Channel conflict between direct vendors and VAR ecosystems | -1.2% | Global | Short term (≤ 2 years) |

| Skills shortage to fine-tune multi-function policies | -0.9% | Global, acute in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance bottlenecks when all services enabled

Hardware UTM boxes often throttle throughput once intrusion prevention, SSL inspection, and sandboxing are switched on. Lab tests show some devices losing 20-30% of rated speed when every feature is active. For example, an 850 Mbps gateway can dip to 600 Mbps after deep-packet inspection is engaged. High-bandwidth enterprises then weigh speed against full protection and sometimes offload inspection tasks to cloud proxies, curbing appliance upgrades.

Migration to cloud-native SSE reducing on-prem UTM refresh cycles

Security Service Edge platforms deliver firewall-as-a-service, secure web gateway, and zero trust access from distributed cloud points. Enterprises that adopt SSE no longer replace rack-mounted UTMs every five years; they renew software subscriptions instead. Deakin University reports faster response times since moving inspection to the cloud, illustrating how hardware sales shrink for traditional vendors while recurring revenue models expand

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Accelerates Platform Shift

Software captured 65.72% of 2025 revenue, and this slice is climbing at 14.93% CAGR. The Unified Threat Management market size for software reached USD 6.13 billion in 2025 and is forecast to double by 2031. Organizations prefer downloadable images or virtual appliances that spin up in minutes across data centers and edge nodes. Continuous patching guards against zero-day exploits without a truck-roll. Services remain the minority today, yet managed detection and response revenues are outpacing product sales as skills shortages worsen. Vendors bundle onboarding, policy optimization, and 24 × 7 monitoring to lock in sticky, subscription-based income. Professional services teams also guide compliance mapping, especially for NIS2 and maritime mandates. The Unified Threat Management market continues to reward suppliers that anchor innovations in software while layering optional service wrap-arounds, assuring buyers of both agility and expertise.

A second wave of innovation is pushing software-defined engines into container form factors that auto-scale with application demand. Check Point’s Infinity architecture now spans on-premise, cloud, and branch edges through a single code base, lowering total cost of ownership because IT staff manage one console. The approach aligns with broader enterprise preference for platform unification rather than separate point products. In effect, the software surge redefines the benchmark for integrated security, setting expectations for one-click deployment, frictionless upgrades, and synchronized analytics. Such dynamics keep the Unified Threat Management market vibrant as subscription economics supplant box resell margins.

By Deployment Mode: Cloud Adoption Reshapes Security Architecture

Cloud models accounted for 57.65% of 2025 shipments on revenue terms and are tracking a 13.92% CAGR through 2031. Enterprises cite lower latency to SaaS destinations, infinite scalability, and simplified global policy enforcement as key motivations. The Unified Threat Management market share for on-premise appliances is slipping where bandwidth demands exceed embedded CPU limits. Still, air-gapped utilities and defense sites continue to favor local inspection. Hybrid designs therefore proliferate. Policies reside in the cloud, yet enforcement points can be virtual or physical, depending on compliance needs.

Cloud adoption also mitigates the earlier restraint of performance degradation. Inspection takes place in massive data centers engineered for multi-core processing. Organizations such as Marine Credit Union report smoother user experiences after migrating to secure web gateways that sit closer to productivity workloads. Vendors that originated in hardware now offer identical rule sets in cloud nodes to preserve policy continuity. Over time, billing flips from capital expenditure to operational expenditure, reinforcing predictable revenue streams for suppliers and lowering entry thresholds for buyers. These factors feed the forward momentum of the Unified Threat Management market.

By Organization Size: SME Growth Drives Market Expansion

Large enterprises held 60.85% of 2025 turnover, yet the small and medium enterprise segment is increasing at 14.48% CAGR, more than a full percentage point above the overall Unified Threat Management market. Cybercriminals view SMEs as soft targets, prompting boards to approve security upgrades despite tight cash flow. A single console that governs firewall, intrusion prevention, and web filtering minimizes staffing headaches. Channel partners capitalize by selling UTM-as-a-service bundles with flat monthly fees.

Managed service providers leverage repeatable UTM deployments to scale profitably without adding headcount. WatchGuard exemplifies the playbook, arming partners with centralized dashboards that handle thousands of tenant instances. As SMBs modernize networks for hybrid work, they often skip legacy point solutions and adopt unified platforms from day one. This greenfield demand boosts license volumes and encourages vendors to build tiered offerings that balance price and feature depth. The Unified Threat Management market thus benefits from dual-engine growth: entrenched renewal cycles in large accounts and first-time adoption in smaller firms.

By End-User Industry: Financial Services Lead, Technology Accelerates

Financial institutions commanded 24.21% revenue share in 2025 because regulators scrutinize transaction integrity and audit capabilities. Integrated logging streamlines proofs of compliance across firewalls, IPS, and antivirus, making UTM the default perimeter for branches and data centers. Insurers and asset managers likewise centralize controls to lower mean time to detect attacks.

Information technology and telecommunications providers show the quickest uptake, advancing at a 14.55% CAGR. Cloud hosting firms embed virtual UTM instances within multi-tenant overlays to shield customer workloads, while telecom carriers fold UTM engines into managed SD-WAN packages. Healthcare also intensifies spending after ransomware incidents locked access to records for 14 million patients in 2024. Manufacturers invoke unified inspection to safeguard industrial control systems, especially as Industry 4.0 links factory sensors to corporate networks. Across sectors, the market is buoyed by common requirements for simplified oversight, demonstrable compliance, and cost control.

Geography Analysis

North America generated 36.62% of 2025 revenue, driven by mature cyber insurance mandates and early adoption of integrated platforms. Federal rules compel shipping companies to install documented controls by July 2025, keeping demand steady for maritime-ready appliances. Canada’s critical infrastructure guidelines similarly favor centralized log management. Stable budgets and dense partner networks continue to underpin upgrades and subscription renewals.

Asia-Pacific is the growth engine, posting an 18.14% CAGR through 2031. Singapore extends the Cybersecurity Act to overseas systems, pushing multinational headquarters to adopt unified logging before fines begin. India’s Digital Personal Data Protection Act requires breach alerts within strict timelines, encouraging businesses to pick turnkey UTM bundles that handle incident reporting automatically. Japanese and South Korean manufacturers deploy UTM to watch industrial robots as they push for smart-factory productivity. The cumulative effect propels the Unified Threat Management market across the region.

Europe records steady expansion as NIS2 broadens incident-reporting duties for energy, transport, and digital-services operators. Ports in Rotterdam and Hamburg now require vessels to certify UTM deployment that aligns with IACS UR E26/E27 standards from July 2024. Organizations subject to DORA in financial services invest in unified controls that feed real-time dashboards to supervisors. Although the continent favors privacy and open standards, the complexity of overlapping regulations reinforces the appeal of single-pane solutions.

Competitive Landscape

Vendor presence is moderately fragmented, yet platform players wield clear scale advantages. Cisco and Broadcom together hold more than 70% revenue, leveraging entrenched switching and routing portfolios to embed security licenses during refresh cycles. SonicWall, Check Point, and Fortinet compete aggressively on feature breadth and AI-assisted analytics. Each rolled out cloud-native inspection nodes to combat the appliance-only stigma. SonicWall’s 2024 acquisitions of Solutions Granted and Banyan Security expanded managed services and zero-trust capabilities. Check Point’s January 2025 injection of AI functions boosted detection accuracy across its Infinity stack.

Broadcom bundles Symantec engines with its semiconductor footprint to cross-sell endpoint and network protection. Cisco stitched UTM firewalls into Meraki edge devices, creating an intuitive cloud dashboard attractive to branch offices. At the specialist end, providers chase maritime and operational-technology niches where compliance and ruggedization are critical. The field is primed for more mergers as vendors race to add SASE and AI threat-hunting features. Buyers favor suppliers that guarantee performance consistency when every inspection module is turned on.

Channel strategies also matter. More than 90% of sales in North America flow through resellers that package UTM subscriptions with SD-WAN circuits. Disintermediation risks emerge when vendors court direct cloud subscriptions, occasionally clashing with value-added resellers. Those that preserve partner margins and offer multi-tenant consoles retain loyalty. The competitive storyline therefore mixes scale, innovation cadence, and channel diplomacy as determinants of long-term share.

Unified Threat Management Industry Leaders

Cisco Systems, Inc

Fortified Networks

Sophos

Palo Alto Networks

Check Point Software

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SonicWall introduced new firewalls and managed cybersecurity services to bolster partner offerings.

- May 2025: T-Mobile and Palo Alto Networks launched T-Mobile SASE with Prisma SASE 5G for secure, high-speed enterprise connectivity.

- January 2025: HUB Cyber Security announced acquisition of BlackSwan Technologies in a stock-for-stock deal targeting a USD 500 million data-fabric opportunity.

- November 2024: Trustwave and Cybereason merged to create an expanded managed detection and response provider.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the unified threat management (UTM) market as all revenue earned from purpose-built or virtual security platforms that combine firewalling, intrusion prevention, gateway antivirus, web filtering, VPN, and related controls under a single management console, whether deployed as on-premise appliances or cloud-hosted gateways. Appliances folded into wider secure-access platforms are counted when the threat-inspection layer remains integral to the offer.

Scope exclusion: stand-alone next-generation firewalls, single-function secure web gateways, and fully outsourced managed security services are excluded.

Segmentation Overview

- By Component

- Software

- Service

- Professional Services

- Managed Services

- By Deployment Mode

- On-premise

- Cloud

- By End-user Enterprise Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare

- Retail and e-Commerce

- Manufacturing

- Utilities and Energy

- Transport and Logistics

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Switzerland

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Vietnam

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with chief information security officers, managed service providers, and value-added resellers across North America, Europe, Asia-Pacific, and the Gulf. These interviews clarified real-world ASPs, refresh cycles, cloud-migration ratios, and the hardware-versus-virtual mix, letting us fine-tune assumptions surfaced during desk work.

Desk Research

We drew on tier-one public sources such as NIST's National Vulnerability Database, US-CERT alert tallies, ENISA threat yearbooks, WTO customs data for HS 851762 devices, ITU ICT statistics, and Eurostat enterprise counts. Company 10-Ks, investor day decks, and distributor price books supplied shipment and pricing markers, while paid libraries like D&B Hoovers and Dow Jones Factiva helped us cross-check supplier revenues. The sources named are illustrative; many additional records were referenced to validate and enrich the dataset.

Market-Sizing & Forecasting

We start with a top-down reconstruction of global network-security spend using enterprise IT budget benchmarks, then apply adoption shares that link active business sites to UTM penetration by organization size. Supplier roll-ups of appliance shipments and sampled ASP × volume checks provide a bottom-up reasonableness screen. Key variables include fresh IPv4/IPv6 allocations, the SME digitization index, regulatory milestones such as NIS2, average firewall replacement cadence, and cloud workload share. An ARIMA regression fed by these drivers yields annual forecasts, with scenario analysis layering upside or downside for sudden regulatory shifts. Gaps in shipment disclosure are bridged by benchmarking against import values in customs data.

Data Validation & Update Cycle

Outputs undergo anomaly checks against independent appliance revenue, breach-trend divergence, and currency swings. Reports refresh every twelve months, with mid-cycle updates when major cyber regulations or material vendor mergers emerge; a final analyst review ensures clients receive the latest view.

Why Mordor's Unified Threat Management Baseline Commands Reliability

Published UTM estimates often diverge because firms vary functional baskets, price points, and refresh dates. Our team locks scope first, folds cloud-delivered UTM in from 2023 onward, and updates FX annually, reducing stale-currency bias.

Key gap drivers surfaced include hardware-only counting by some publishers, conservative list-price discounting, and instances where future-year figures are labeled as current. Mordor's mixed modeling approach, verifiable inputs, and live refresh cadence mitigate these issues.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.32 B (2025) | Mordor Intelligence | - |

| USD 6.78 B (2024) | Global Publisher A | Excludes cloud subscriptions and SME virtual licenses |

| USD 7.35 B (2024) | Industry Journal B | Fixed 18-month refresh; discounts unverified with channels |

| USD 9.60 B (2024) | Regional Consultancy C | Derives share from broad security appliance pool |

The comparison shows that Mordor's disciplined scope setting, blended modeling, and timely updates deliver a balanced, transparent baseline that decision-makers can trace back to clear, reproducible metrics.

Key Questions Answered in the Report

What is the current size of the unified threat management market and how fast is it growing?

The market stands at USD 10.56 billion in 2026 and is projected to reach USD 19.75 billion by 2031, reflecting a 13.34% CAGR.

Which component contributes the largest share to the unified threat management market?

Software components lead with 65.72% revenue share in 2025, owing to their flexible deployment and rapid update capabilities.

Which deployment model is expanding the fastest?

Cloud-based deployments hold 57.65% of 2025 revenue and are advancing at a 13.92% CAGR through 2031 as enterprises shift away from hardware-bound appliances.

Which geographic region is expected to record the highest growth rate?

Asia-Pacific is forecast to expand at an 18.14% CAGR to 2031, driven by stricter regulations and rapid digitalization across manufacturing and services.

What years does this Unified Threat Management Market cover?

The report covers the Unified Threat Management Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Unified Threat Management Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: