Identity Theft Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

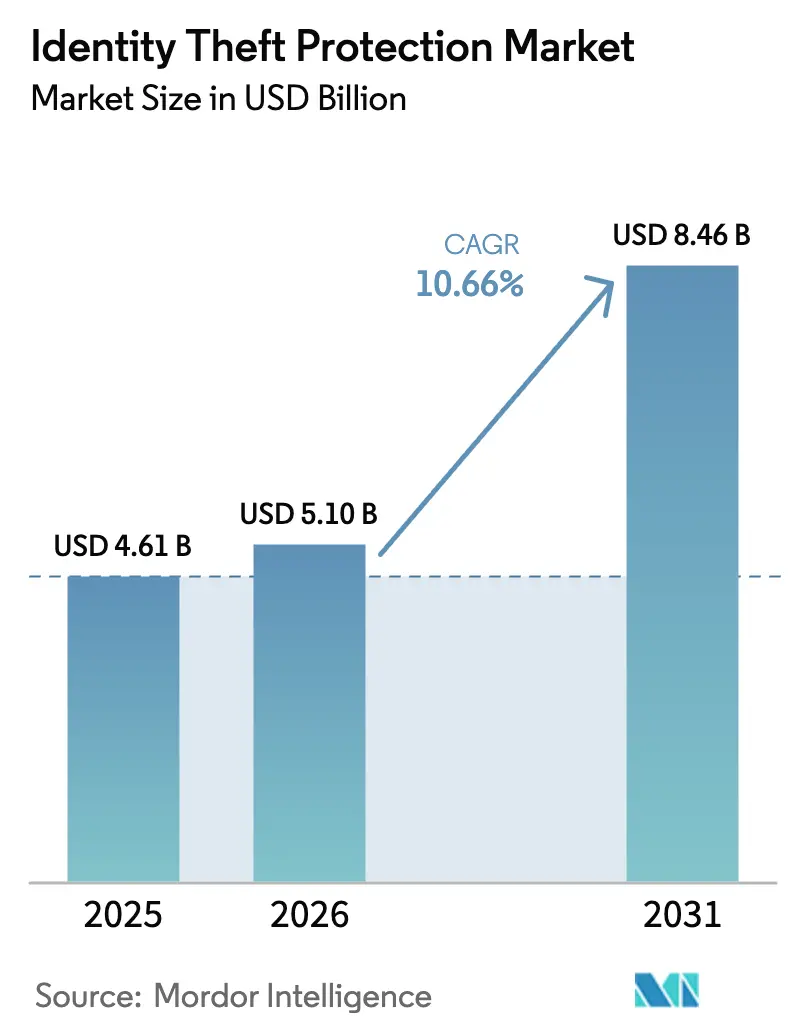

| Market Size (2026) | USD 5.1 Billion |

| Market Size (2031) | USD 8.46 Billion |

| Growth Rate (2026 - 2031) | 10.66% CAGR |

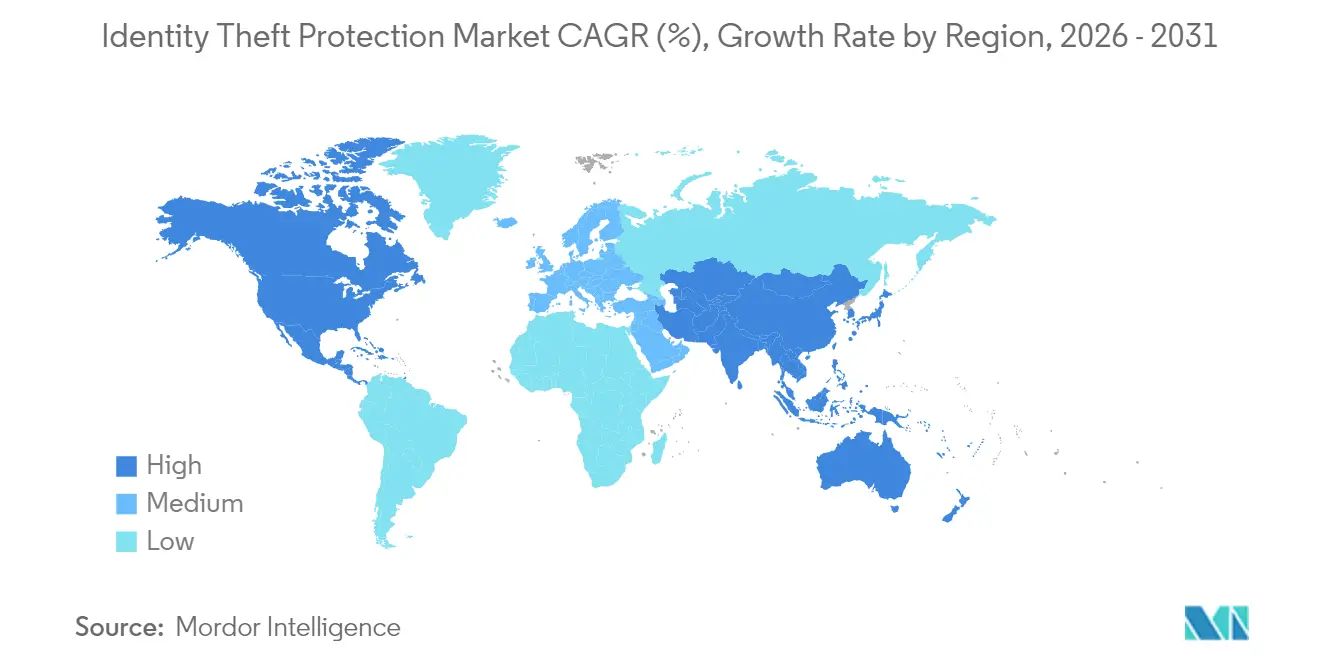

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Theft Protection Market Analysis by Mordor Intelligence

The identity theft protection market size is expected to grow from USD 4.61 billion in 2025 to USD 5.10 billion in 2026 and is forecast to reach USD 8.46 billion by 2031 at 10.66% CAGR over 2026-2031. Momentum stems from a sharp rise in sophisticated, AI-enabled fraud schemes, stricter global data-privacy mandates and growing enterprise spending on adaptive verification frameworks. Continuous cloud migration, the embedment of behavioral biometrics and employer-sponsored consumer plans are reshaping competitive playbooks. Asia posts the fastest trajectory, expanding at a 16.5% CAGR as Indian and Southeast Asian regulators tighten data-governance rules and mobile commerce explodes.

Key Report Takeaways

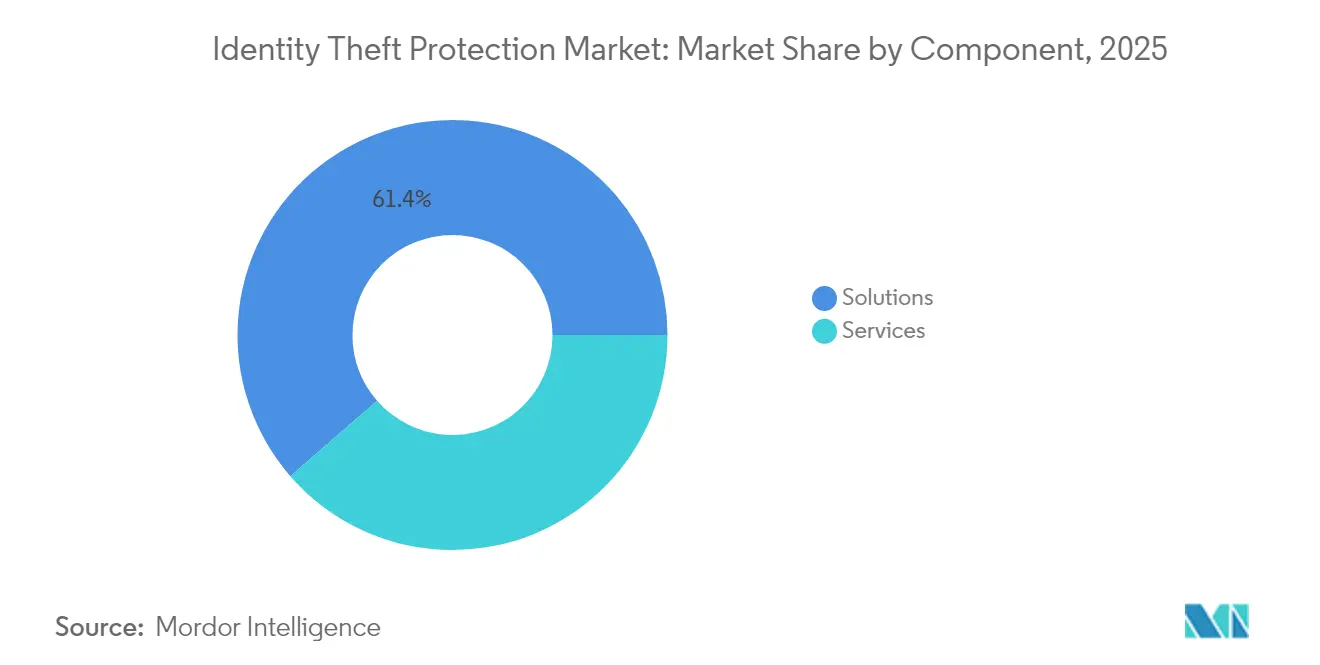

- By component, solutions led with 61.40% revenue share of the identity theft protection market in 2025; services are projected to grow at an 18.15% CAGR through 2031.

- By deployment, cloud captured 52.10% of the identity theft protection market share in 2025 and is slated to scale at an 18.70% CAGR to 2031.

- By end-user, enterprises held 61.55% of the identity theft protection market size in 2025, while the consumer segment records the fastest 14.90% CAGR to 2031.

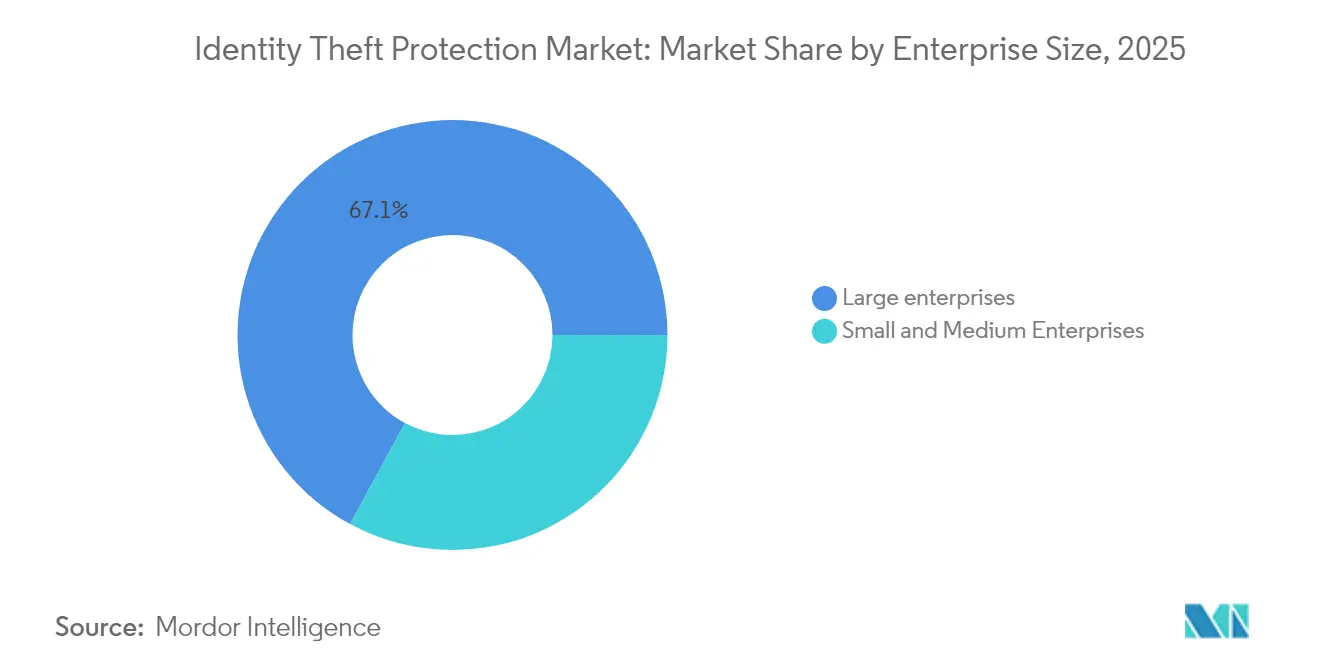

- By enterprise size, large companies commanded 67.10% of 2025 revenues; SMEs represent the highest-growing cohort at a 19.60% CAGR.

- By vertical, BFSI dominated with a 34.60% share in 2025; retail & e-commerce is advancing at a 21.40% CAGR through 2031.

- By geography, North America dominated with a 38.10% share in 2025: Asia is advancing at a 15.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Identity Theft Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deepfake-powered social-engineering attacks | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Synthetic-ID fraud in BNPL | +2.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| ‘KYC-for-All’ fintech roll-outs | +1.9% | Global | Medium term (2-4 years) |

| Employer-sponsored ID protection | +1.5% | North America, Europe | Short term (≤ 2 years) |

| Child-ID theft in high-income households | +1.2% | OECD countries | Medium term (2-4 years) |

| Generative-AI real-time scam tools | +2.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Deep-fake Powered Social-Engineering Attacks

Deepfake fraud attempts surged 2,137% over the past three years and now appear every five minutes, accounting for 40% of biometric fraud in 2024. Financial services remain prime targets; an Arup employee’s USD 25 million transfer under a spoofed video call underscores the stakes. Institutions are shifting to layered defenses that pair liveness checks with keystroke and mouse-dynamics analytics. Vendors integrating these controls report 80–90% drops in account-takeover incidents, reinforcing demand for behavior-centric verification suites.

Surge in Synthetic Identity Fraud in Buy-Now-Pay-Later (BNPL) Transactions

BNPL’s rapid checkout model lifted fraud values by 26% in early 2024 and pushed synthetic-ID attacks up 237% in 1H 2024. Merchants absorb losses once composite identities default, accelerating uptake of AI pattern-matching engines. Socure’s Sigma Synthetic captured 74% of synthetic fraud at onboarding, shrinking manual review queues by half. Retailers and payment fintechs are embedding similar models across Asia, Latin America and Europe as cross-border BNPL volume rises.

Mandatory ‘KYC-for-All’ Roll-outs by Neobanks and FinTechs

The UK alone hosts 266 digital-identity providers generating EUR 2.1 billion in 2023/2024 revenues, with 85% serving financial services. Competitive differentiation now hinges on journey-time orchestration that fuses documentary checks with passive biometrics. Adoption is spreading from Europe and North America to Middle-East neobanks, compressing onboarding friction while elevating security benchmarks.

Employer-Sponsored ID-Protection as an HR Benefit in North America

LegalShield found 77% of employees experienced identity theft or cybersecurity issues and 56% faced legal hurdles, fueling corporate demand for bundled protection plans. Texas Instruments offers free Experian monitoring and USD 1 million insurance on its medical plan [ti.com]; Leidos switched to MetLife + Aura at reduced premiums for staff. The channel unlocks scale for providers while enhancing workforce resilience.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited API integration with legacy core banking | -1.3% | Global | Medium term (2-4 years) |

| Fragmented regulations beyond OECD | -0.9% | LATAM, Africa, parts of Asia | Long term (≥ 4 years) |

| Scarcity of behavioral-bio data sets | -1.1% | Global | Short term (≤ 2 years) |

| Consumer price elasticity in emerging markets | -0.8% | Emerging Asia, LATAM, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited API-Level Integration Across Legacy Core-Banking Stacks

Many tier-one banks still run siloed COBOL-based ledgers that restrict real-time data access, delaying threat signals and inflating false-positive rates. Vendors must rely on batch file exchanges rather than streaming APIs, dampening efficacy of adaptive risk scoring engines.

Shortage of Behavioral-Bio Data Sets for Model Training

Experian discovered 48% of Indian firms lack the data depth to train effective ML models and 60% cite quality issues. Differential-privacy techniques are emerging to widen usable corpora without breaching confidentiality, yet algorithm accuracy remains uneven across demographic cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate While Services Accelerate

Solutions held 61.40% of identity theft protection market revenue in 2025, underscoring the foundational role of analytical engines, behavioral-biometric modules, and credential-monitoring feeds. Telecom giant AT&T realized an 80% drop in fraud attacks after integrating generative-AI algorithms atop its detection platform. Financial institutions, e-commerce gateways, and healthcare portals continue to prioritize solution licenses to meet audit and regulatory thresholds.

Services represent the fastest-advancing slice, growing at an 18.15% CAGR to 2031. Enterprises short on cyber talent subscribe to managed SOC, dark-web patrol, and breach-restoration bundles that deliver24×7 coverage. The consumer segment benefits as employers negotiate white-labeled service tiers that extend family protection, accelerating household uptake and improving brand stickiness for vendors.

By Deployment: Cloud Accelerates Security Innovation

Cloud accounted for 52.10% of the identity theft protection market in 2025 and posts a 18.70% CAGR through 2031. Elastic processing lets providers train larger behavior models, ingest real-time telemetry and push zero-day countermeasures without customer-side patches. Ninety-three percent of bank technology leaders expect ML in the cloud to transform fraud defens.

On-premise deployments remain for institutions bound by stringent data sovereignty or air-gap mandates. Yet roadmap momentum overwhelmingly favors multi-tenant SaaS. Providers highlight sub-hour provisioning, microservice upgrades and five-nines uptime as differentiators that legacy appliances struggle to match.

By End-User: Enterprises Lead, Consumers Gain Momentum

Enterprises directed 61.55% of spending in 2025, reflecting strict regulatory obligations and reputational risk. Verizon linked stolen credentials to over 60% of 2024 breaches, prompting board-level investment in continuous authentication layers. BFSI, telecom, and healthcare sectors reinforce identity-protection controls to satisfy regulatory audits and maintain service trust.

Consumers, however, log the briskest 14.90% CAGR. Notable offerings, such as Norton LifeLock’s Ultimate Plus with USD 3 million insurance and three-bureau monitoring, resonate amid high-profile breach headlines. The integration of these plans into payroll-deduct schemes and mobile-banking apps further simplifies subscription sign-up, shrinking the gap between corporate and personal adoption rates.

By Enterprise Size: Large Enterprises Invest While SMEs Catch Up

Large enterprises claimed 67.10% of the identity theft protection market share in 2025, leveraging deep budgets to implement endpoint-to-cloud identity mesh architectures and in-house threat-intel cells. Tier-one banks pilot keyboard-cadence profiling and device telemetry to cut synthetic-ID approvals, while insurers deploy liveness verification for claim portals.

SMEs, expanding at a 19.60% CAGR, gain from democratized security-as-a-service. Plug-and-play orchestration suites bundle device fingerprinting, IP reputation checks, and automated remediation at per-user price points suited to tight budgets. This shift reduces the average deployment window from several months to a few days, enabling cafés, logistics brokers, and online tutors alike to install enterprise-grade protection.

By Industry Vertical: BFSI Dominates While Retail Surges

BFSI captured 34.60% share in 2025, supported by stringent KYC/AML mandates and high fraud liability. Behavioral biometrics yields 60–80% fraud-reduction rates in digital-banking channels, reinforcing BFSI’s commitment to layered verification.

Retail and e-commerce accelerate at 21.40% CAGR. BNPL-driven synthetic IDs and account takeovers escalate cart-abandonment risk and chargebacks. Merchants counter with selfie liveness, document-authenticity scans, and risk-based step-ups at checkout, often delivered through API-first platforms that preserve user experience while reducing fraud

Geography Analysis

North America remains the most lucrative geography for the identity theft protection market, upheld by mature credit ecosystems and expansive employer-benefit programs. The Federal Trade Commission processed 5.39 million consumer reports in 2023, with identity-theft filings making up 19%. Vendors tap payroll-deduct channels, healthcare exchanges and affinity groups to deepen household penetration. U.S. insurance carriers now bundle digital-identity restoration alongside cyber-rider policies for small businesses, widening cross-sell lanes.

Asia delivers the sharpest 15.90% CAGR. India’s Digital Personal Data Protection Act mandates lawful processing, purpose limitation and secure retention, catalyzing spend on consent orchestration middleware. China combats credential-stuffing in its USD-trillion online retail sector, while Japan scales gait and palm-vein biometrics at ATMs. ASEAN central banks co-publish guidelines on biometric accuracy, spurring localized vendor solutions.

Europe prioritizes privacy and interoperability. The UK hosts a vibrant digital-ID cluster worth EUR 2.1 billion annually, with 71% of residents familiar with at least one digital-identity service. Nordic banks implement voice-analysis to flag deepfake-enabled phone fraud, whereas German retailers test passkeys under FIDO2 protocols to remove passwords altogether. Pan-European payment providers integrate reusable ID-vaults, satisfying regional travel and commerce flows. Middle East & Africa, South America and Oceania chart emerging-market opportunities. GCC governments embed face-match e-KYC in smart-city portals. Brazil’s LGPD pushes marketplaces toward liveness checks for seller onboarding, while regional fintechs adopt document fraud detection. South Africa’s mobile carriers trial SIM-swap-proof flows, and Nigeria’s payment licenses require face-matching. Australia and New Zealand enforce digital-identity interoperability for both public and private log-ins, positioning Oceania as a reference hub for verifiable-credential roll-outs.

Competitive Landscape

The identity theft protection market features moderate concentration anchored by credit-bureau incumbents Equifax, Experian and TransUnion. Each leverages expansive bureau files for risk scoring and extends into breach-resolution services, yet revenue growth now leans on AI upgrades and cloud orchestration. Entrust’s acquisition of Onfido blends document authentication with device intelligence, positioning the firm as an end-to-end identity-centric security platform capable of countering the 3,000% spike in deepfake attacks reported in 2024.

Disruptive entrants focus on behavioral analytics, synthetic ID prevention, and decisioning orchestration. Socure’s USD 136 million Effectiv buyout fuses transaction-risk scoring with identity graphs, opening doors to the USD 200 billion enterprise fraud-detection space. BioCatch, Sontiq, and Aura leverage specialized algorithms to detect cursor-drift, typing latency, or anomalous application navigation, promising 50–70% lifting accuracy over legacy static-credential checks.

White-space opportunities center on demographic niches such as child-ID monitoring, consumer micro-finance onboarding, and multilingual scam-coaching bots that demystify emerging AI scams for older adults. Pricing competition intensifies in employer-benefit channels, with group policies shaving 30–40% off individual subscription fees. Vendors also test usage-based billing where policy cost aligns with verified-identity query volume, appealing to gig-economy platforms that experience sporadic user spikes.

Identity Theft Protection Industry Leaders

Experian Plc

Equifax Inc.

TransUnion LLC

Gen Digital (NortonLifeLock)

Aura/Identity Guard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Jumio survey records steep decline in consumer digital trust, spotlighting demand for stronger verification,

- April 2025: Entrust’s report shows deepfake attempts every five minutes, forming 40% of biometric fraud.

- March 2025: Experian research finds 85% of fraud experts see generative AI reshaping threats, with social engineering topping the list.

- November 2024: Kingswood Capital Management acquires IDX, extending breach-response capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the identity-theft protection market as global sales of software and subscription plans that monitor, alert, and restore when personal or corporate identifiers are abused on any channel.

Scope exclusion: We leave out generic payment-fraud analytics or endpoint-security tools that never claim identity-theft protection.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment

- Cloud

- On-Premise

- By End-User

- Consumer

- Enterprise

- Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Industry Vertical

- BFSI

- Healthcare

- Retail and E-commerce

- IT and Telecommunications

- Government

- Other Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview product leads, bank and retail CISOs, insurance underwriters, and privacy advocates across North America, Europe, and Asia-Pacific. These talks confirm adoption ratios, price concessions, and churn triggers that desk work alone cannot surface.

Desk Research

We begin by lifting complaint counts and loss totals from the US FTC, FBI IC3, Europol, and the UK National Cyber Security Centre, then link them with World Bank payment volumes and OECD digital-ID surveys. Company 10-Ks, investor decks, and Dow Jones Factiva clips reveal average plan prices, while D&B Hoovers shows vendor splits. Volza customs data on multi-factor tokens, plus papers on synthetic IDs, round out the core spine. Mordor analysts consult many other public and paid databases; the list above is only illustrative.

Market-Sizing & Forecasting

We rebuild the base year through one top-down and bottom-up loop. Complaint volumes pair with verified plan penetration and weighted fees, then sample against supplier roll-ups from filings. Inputs such as card-not-present growth, breach severity, security spend per employee, penalty trends, and cloud uptake feed a multivariate regression out to 2030; scenario checks test upside from mandatory digital-ID laws and downside from price compression.

Data Validation & Update Cycle

We run variance checks against historic loss ratios, and peer review inside the analyst pod clears anomalies before sign-off. Mordor refreshes the model each year and issues interim updates when major breaches, mergers, or new rules shift the outlook.

Why Mordor Numbers Identity Theft Protection Baseline Give Decision Makers Confidence

We acknowledge that published estimates diverge because firms tweak service baskets, price lenses, or refresh rhythm, yet our disciplined scope helps buyers cut through the noise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.61 B | Mordor Intelligence | - |

| USD 14.41 B | Global Consultancy A | Bundles credit-bureau data and one-off breach projects |

| USD 7.94 B | Industry Data B | Uses one retail price worldwide, ignores low-income uptake |

| USD 25.00 B | Market Tracker C | Mixes broader anti-fraud platforms and IAM suites |

We believe this complaint-anchored, price-validated baseline, reviewed each year by us, offers planners a balanced starting point they can trust.

Key Questions Answered in the Report

What is the current size of the identity theft protection market?

The identity theft protection market is valued at USD 5.10 billion in 2026 and is expected to reach USD 8.46 billion by 2031.

Which region is expanding fastest?

Asia posts the steepest growth at a 15.90% CAGR, fueled by mobile-commerce adoption and emerging data-privacy laws such as India’s DPDPA.

Why are cloud deployments preferred?

Cloud platforms deliver elastic compute for AI-driven detection, faster updates and lower entry costs, supporting a 18.70% CAGR for cloud-hosted solutions.

How are employers influencing adoption?

U.S. companies bundle identity-protection plans into HR benefits, driving subscriptions at discounted group rates and widening consumer access.

Which threat vectors are most pressing?

Deepfake-enabled social engineering, BNPL synthetic identities and AI-orchestrated real-time scams propel investment in behavioral biometrics and continuous authentication.

Page last updated on: