Non-Human Identity (NHI) Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

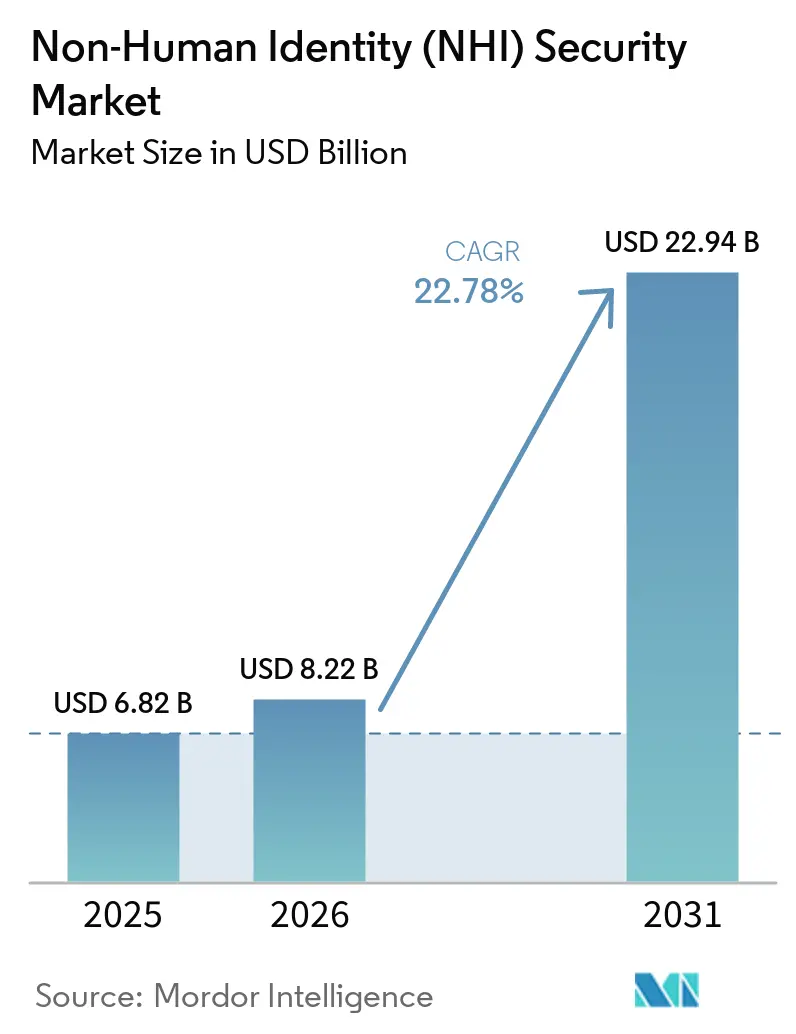

| Market Size (2026) | USD 8.22 Billion |

| Market Size (2031) | USD 22.94 Billion |

| Growth Rate (2026 - 2031) | 22.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

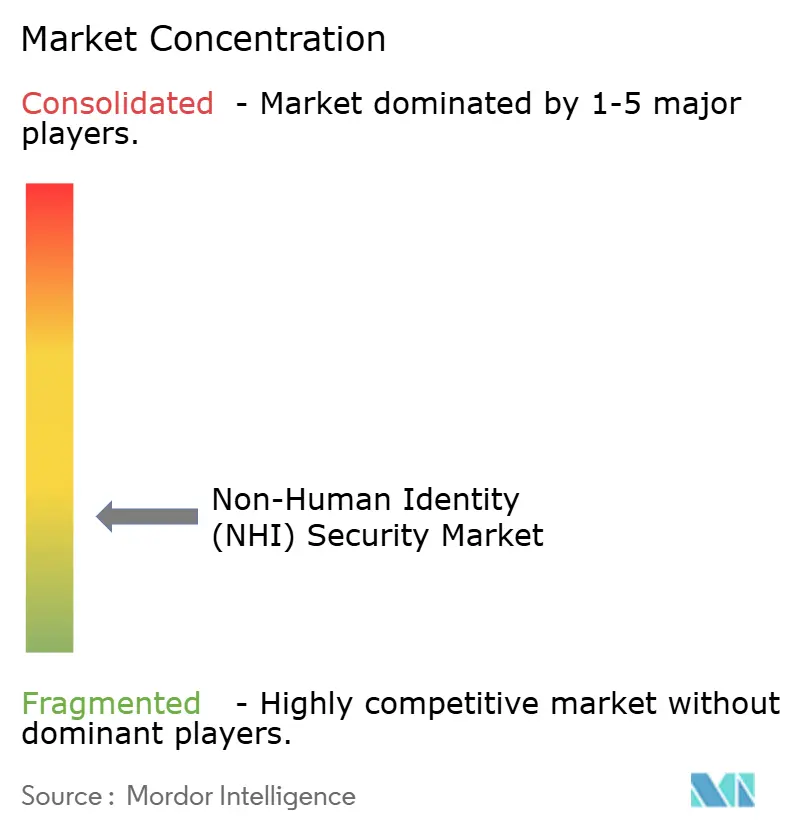

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Human Identity (NHI) Security Market Analysis by Mordor Intelligence

The Non-Human Identity (NHI) Security Market size is projected to expand from USD 6.82 billion in 2025 and USD 8.22 billion in 2026 to USD 22.94 billion by 2031, registering a CAGR of 22.78% between 2026 and 2031. This pace reflects a broad shift in enterprise security, as machine identities now span service accounts, API keys, AI agents, certificates, and workload tokens at a scale far beyond human identity volumes. The buying case is also strengthening because even small gains in discovery, governance, and rotation now apply across very large identity estates, expanding the commercial space for both incumbent platform vendors and NHI-focused specialists. Demand is rising as API growth, cloud workload expansion, and exposed secrets continue to increase the number of unmanaged credentials inside production environments. The risk is not only the number of identities, but also the way over-privileged service accounts keep access for long periods without strong review, which raises breach costs and widens the damage from misuse. Competitive activity has moved in the same direction, with larger security vendors using acquisitions, product expansion, and platform integration to secure a stronger position in the Non-Human Identity (NHI) Security Market.

Key Report Takeaways

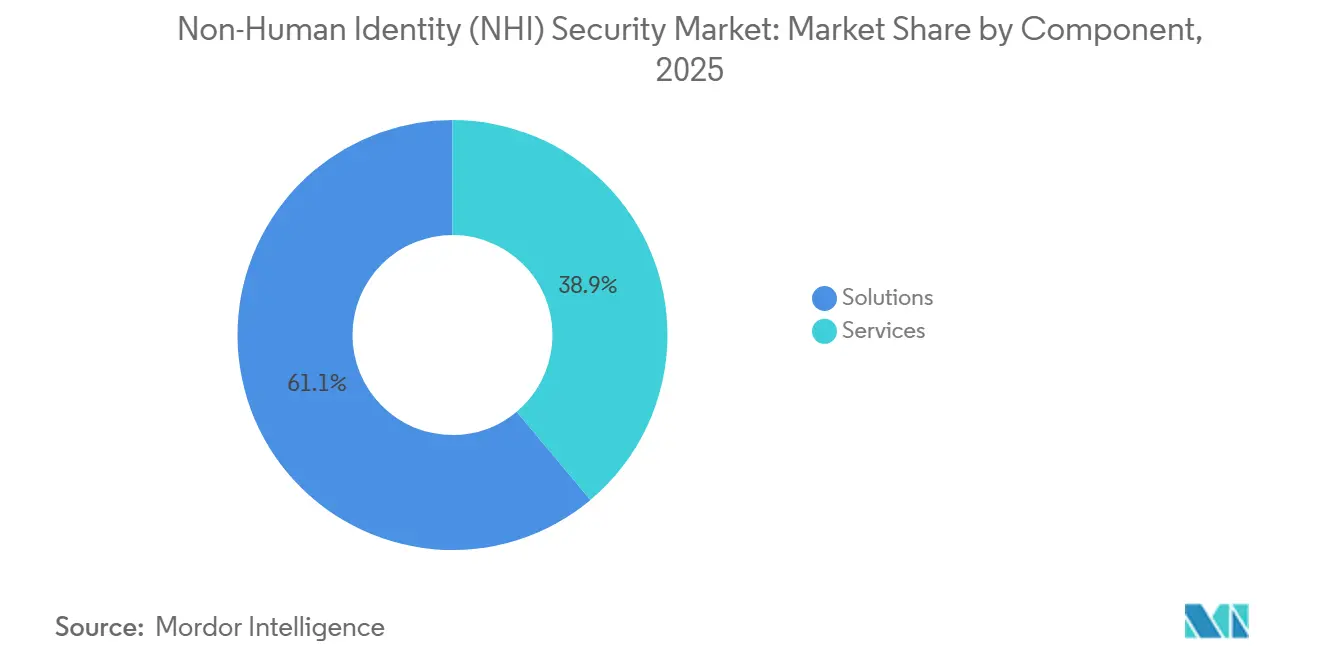

- By component, Solutions held 61.09% revenue share in the Non-Human Identity (NHI) Security market in 2025, while Services is projected to expand at a 23.84% CAGR through 2031.

- By identity type, Application and Service Identities accounted for 27.14% share of the NHI Security market in 2025, while Workload and Container Identities are projected to expand at a 23.95% CAGR through 2031.

- By deployment, Cloud accounted for 54.21% share of the Non-Human Identity Security market size in 2025, while Hybrid is projected to expand at a 24.06% CAGR through 2031.

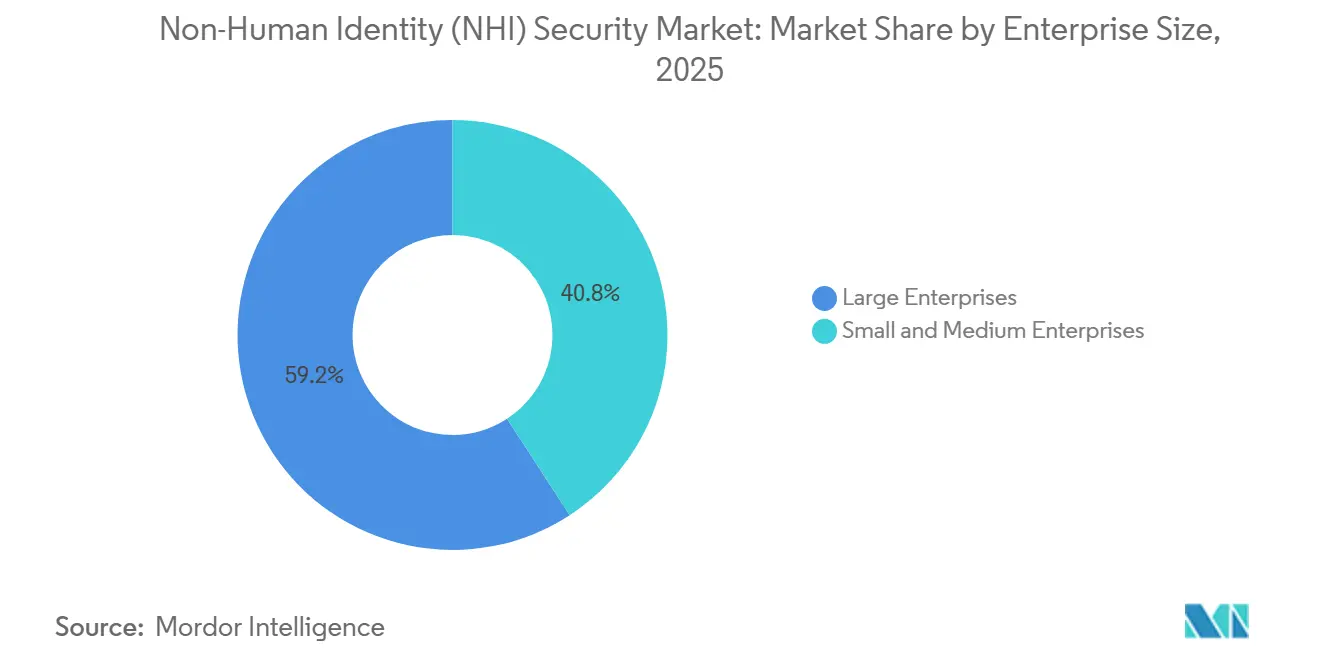

- By enterprise size, Large Enterprises held 59.18% share of the NHI Security market in 2025, while SMEs are projected to expand at a 24.17% CAGR through 2031.

- By end-user industry, BFSI held 16.22% share of the Non-Human Identity Security market in 2025, while Healthcare and Life Sciences are projected to expand at a 24.28% CAGR through 2031.

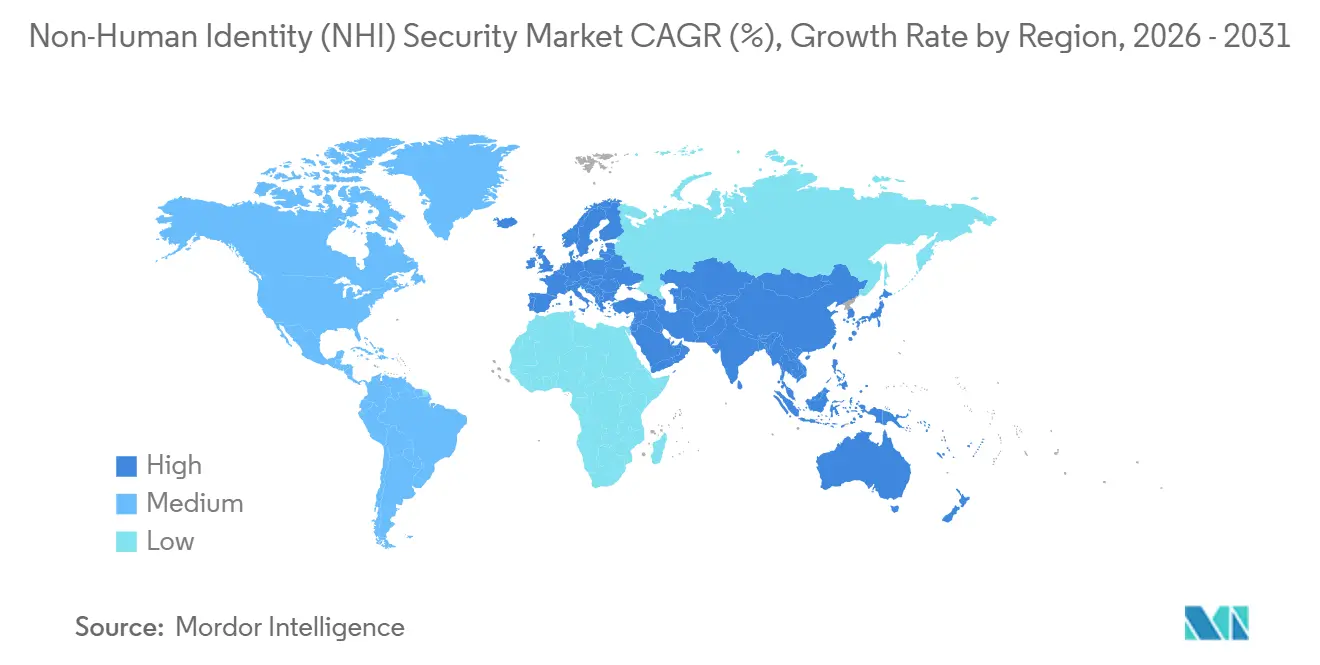

- By geography, North America held 32.15% share of the Non-Human Identity (NHI) Security market in 2025, while Asia-Pacific is projected to expand at a 24.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-Human Identity (NHI) Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion Of APIs, Cloud Workloads, and Machine-To-Machine Access | +6.0% | Global | Short term (≤ 2 years) |

| Rising Breach Costs from Over-Privileged Service Accounts | +4.5% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Cloud-Native and Kubernetes Identity Sprawl | +3.8% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Zero Trust Enforcement Across Non-Human Workloads | +3.2% | North America and EU | Medium term (2-4 years) |

| Under-Governed AI Agents and Automation Bots | +3.0% | Global | Short term (≤ 2 years) |

| Secretless and Ephemeral Credential Rotation Demand | +2.0% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of APIs, Cloud Workloads, and Machine-To-Machine Access

API-led architectures remain the strongest demand driver for the Non-Human Identity (NHI) Security Market because every cloud service, microservice, CI/CD workflow, and integration endpoint creates at least 1 machine identity. Modern enterprises therefore manage very large populations of service accounts, tokens, and keys, even before AI agents and automation bots are added to the environment. CyberArk reported in 2025 that machine identities outnumbered human identities by 82:1 in the average enterprise, underscoring how quickly machine credential populations have become the primary burden on security teams.[1]CyberArk, “Identity Security Landscape 2025,” CyberArk, cyberark.com New deployments also create new trust relationships between services, so identity growth is not linear and tends to spread across the application, cloud, and integration layers simultaneously. This pattern keeps discovery, rotation, and policy enforcement near the center of buying criteria across the Non-Human Identity Security Market. The standardization work under the IETF WIMSE effort also shows that workload identity attestation is moving from a niche topic toward a core infrastructure control for machine-to-machine security.

Rising Breach Costs from Over-Privileged Service Accounts

Over-privileged service accounts continue to drive spending in the Non-Human Identity (NHI) Security Market because they create a different risk profile from human account compromise. These accounts often operate without multi-factor authentication; they rarely trigger the same behavioral checks as employee accounts, and they tend to accumulate permissions over many years. IBM reported in 2025 that credential-based breaches took an average of 246 days to identify and contain, at an average cost of USD 4.67 million, highlighting the need to keep executive focus on identity exposure that remains hidden for long periods. BeyondTrust found dormant privileged service accounts in more than 70% of enterprise environments assessed in 2025, while Entro Security reported that 1 in 20 NHIs had full administrative privileges and many had remained inactive for more than 9 months.[2]BeyondTrust, “Privileged Dormant Service Accounts In 70% Of Enterprise Environments,” SC World, scworld.com The result is that the attack surface is not just a cleanup issue, because it stems from governance processes built for people rather than for machine-scale identities. That mismatch continues to support durable demand for discovery, policy, and least-privilege controls across the NHI Security Market.

Cloud-Native and Kubernetes Identity Sprawl

Cloud-native infrastructure is adding a sustained layer of demand to the Non-Human Identity (NHI) Security Market because Kubernetes and related platforms generate identities as part of normal system design. Each pod requires a service account, each deployment creates secrets, and many default settings still expose tokens more broadly than security teams would prefer. The Cloud Native Computing Foundation stated in 2026 that identity has become the primary security perimeter in cloud-native architectures, yet many Kubernetes environments still depend on permissive RBAC settings that grow faster than teams can review or revoke.[3]Cloud Native Computing Foundation, “Identity And Access Management Whitepaper,” CNCF, cncf.io That imbalance becomes more serious when organizations expand into edge environments and multi-cluster deployments, because the same identity model must operate across many locations and runtime conditions. It also means buyers want tools that can discover ownership, map privileges, and control credential lifecycles without slowing application delivery. As more enterprises move from early cloud adoption to scaled operations, this source of identity sprawl should remain a steady driver of growth in the Non-Human Identity (NHI) Security Market.

Zero Trust Enforcement Across Non-Human Workloads

Zero-trust adoption is also supporting the Non-Human Identity (NHI) Security Market, as many organizations have moved faster on human verification than on machine-to-machine access control. CISA's Zero Trust Maturity Model continued to place identity at the center of zero trust in 2025 and called for dynamic, risk-aware policies that apply to both human and non-human access. NIST stated in its 2026 concept paper on AI agent governance that AI agents must be known, trusted, and properly governed with the same discipline applied to other workloads. SANS also noted in 2026 that many NHIs still operate outside formal governance, leaving a clear control gap between zero-trust goals and day-to-day machine-identity practices. This has lifted demand for secretless access, just-in-time provisioning, and continuous attestation across the Non-Human Identity Security Market. It has also shifted buyer expectations, because machine identities are now being judged against the same access discipline once reserved for human users

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence Of Standardized Access Control Frameworks For NHIs | -1.2% | Global | Short term (≤ 2 years) |

| Integration Complexity Across Legacy and Hybrid IT Environments | -0.8% | North America and EU, with spill-over to APAC | Medium term (2-4 years) |

| Limited Discovery And Ownership Mapping for Ephemeral Identities | -0.6% | Global | Medium term (2-4 years) |

| Procurement Friction from IAM, PAM, CIEM, and Secrets Tool Overlap | -0.4% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Absence of Standardized Access Control Frameworks For NHIs

The lack of a widely adopted machine identity assurance framework continues to slow the Non-Human Identity (NHI) Security Market because buyers lack a single benchmark for policy design, maturity scoring, or budget justification. OWASP has published its Non-Human Identities Top 10, and industry groups have pushed workload identity standards, yet there is still no direct equivalent to long-established human identity assurance models. This leaves many organizations combining controls from several sources rather than implementing them in a single recognized structure. Cloud Security Alliance reported in 2026 that more than 16% of organizations did not track the creation of AI-related identities at all, indicating that policy coverage remains weak even as identity populations expand. The result is slower internal alignment between security, infrastructure, and application teams. Until standards move closer to common enterprise practice, this issue should remain a real drag on deployment speed in the NHI Security Market.

Integration Complexity Across Legacy and Hybrid IT Environments

Integration complexity remains a practical restraint on the Non-Human Identity (NHI) Security Market because many large organizations still run legacy systems alongside modern cloud-native workloads. Older batch systems and mainframe-linked applications often depend on static credentials that cannot easily support workload federation or short-lived credential issuance. Industry discussion in 2025 continued to show that these mixed estates require compensating controls, application changes, and long rollout cycles before consistent machine identity governance is possible. Oasis Security documented a healthcare environment in 2025 with more than 100,000 NHIs, including 50,000 certificates and 10,000 service accounts, where visibility alone did not solve the backlog of unused identities and unrotated secrets. That illustrates why buyers often move from discovery to remediation more slowly than they expected. It also explains why service demand is rising in the Non-Human Identity (NHI) Security Market, even though budget approval for the core platform has already been secured.[4]NHIMG, “Integration Complexity In Legacy And Hybrid NHI Environments,” NHIMG, nhimg.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Solutions Lead As Managed Services Accelerate

Solutions held 61.09% of the market in 2025, which showed that buyers first prioritized software platforms for discovery, posture management, and real-time policy control. The largest budgets still flowed to tooling that could identify machine identities across cloud, application, and infrastructure environments without relying on manual inventory work. This preference reflected the operational burden created by API keys, OAuth tokens, certificates, service accounts, and AI-related credentials that had spread across daily workflows. The Non-Human Identity (NHI) Security Market, therefore, favored solution vendors that could unify discovery with lifecycle actions instead of offering visibility alone. IBM's 2026 launch of Machine Identity Management also reinforced that enterprise demand had moved toward automated issuance, renewal, revocation, and governance rather than one-time assessment.

The Services segment is projected to grow at a 23.84% CAGR through 2031, indicating that implementation depth is becoming almost as important as platform selection. Many deployments require integration with existing PAM, CIEM, SIEM, and cloud identity stacks before policy outcomes become visible in production. Buyers also need support for credential rotation, ownership mapping, access reviews, and operating model design across teams that do not always share the same identity workflows. As NHI programs mature, consulting, managed operations, and remediation support should remain essential complements to product adoption in the Non-Human Identity (NHI) Security Market. The balance between platform spending and operational support suggests that the category is moving from early awareness into more structured enterprise execution.

By Identity Type: Application Identities Anchor Market, Workloads Surge

Application and Service Identities accounted for 27.14% of the market in 2025, making them the largest identity type inside the Non-Human Identity (NHI) Security Market. Their lead reflected the heavy use of OAuth tokens, API keys, SaaS integration credentials, and service accounts across ordinary business operations. These identities are also difficult to change because many are tightly linked to application performance, integration reliability, and release timelines. Entro Security reported in 2025 that 47% of NHIs had remained unchanged for more than 1 year, with many static credentials concentrated in application integration layers where rotation can break workflows. That mix of scale and operational sensitivity kept application identities at the center of buyer concern.

Workload and Container Identities are projected to expand at a 23.95% CAGR through 2031, which makes it the fastest-growing identity category. The Cloud Native Computing Foundation continued in 2026 to frame SPIFFE and SPIRE as important approaches to workload identity in Kubernetes environments, especially for organizations seeking cryptographic attestation without persistent secrets. This points to a broader platform shift within the Non-Human Identity (NHI) Security industry, as cloud-native environments move toward shorter-lived credentials and stronger runtime trust controls. Machine and Device Identities and Cryptographic Identities are also expanding as industrial IoT adoption, and the use of DevSecOps certificates expands the overall addressable base. Cloud Security Alliance's reference to Verizon's 2026 findings on higher supply chain and third-party breach exposure adds urgency to governing API and workload identities across external trust boundaries.

By Deployment: Cloud Dominates, Hybrid Gains Strategic Ground

Cloud accounted for 54.21% of the Non-Human Identity (NHI) Security market in 2025, confirming that SaaS delivery remained the preferred route for many deployments. Buyers wanted governance tools that could scale across AWS, Microsoft Azure, and Google Cloud without relying on local infrastructure or slow synchronization. This meets the operational needs of enterprises that already manage large machine identity populations via cloud APIs and distributed development environments. The lead for cloud deployment also reflected the broader move toward real-time monitoring and policy control in the Non-Human Identity Security Market. As a result, vendors with strong multi-cloud connectivity entered 2026 with a clear commercial advantage.

Hybrid deployment is projected to grow at a 24.06% CAGR through 2031, which shows that mixed environments remain the real operating model for many large organizations. Legacy applications, regulated workloads, and on-premises data constraints still require machine identity controls that span both cloud and on-premises systems. SUSE noted in 2025 that unified SSO and RBAC across hybrid Kubernetes clusters had become one of the most urgent security challenges for platform teams, which supports the need for broader cross-environment governance. This keeps hybrid delivery strategically important even as cloud remains the largest segment by revenue. On-premises deployment should still hold a role in regulated settings, but the longer-term momentum in the NHI Security Market continues to favor cloud and hybrid models.

By Enterprise Size: Large Enterprises Command Share, SMEs Drive Growth

Large Enterprises held 59.18% of the market in 2025, which reflected their much larger populations of machine identities and their stronger ability to fund broad governance programs. Cloud Security Alliance documented a 2025 Fortune 500 financial institution audit that found more than 4.2 million NHIs against around 50,000 human accounts, showing how quickly machine identity scale can create board-level urgency. These organizations also drive a significant share of services demand because they need custom integration across IAM, PAM, SIEM, and cloud security stacks. Large buyers, therefore, shaped the early commercial structure of the Non-Human Identity (NHI) Security Market through a bigger deployment scope and deeper remediation needs. Their spending profile still favors vendors that can support complex operating models across many teams and business units.

SMEs are projected to grow at a 24.17% CAGR through 2031, indicating a widening buyer base for the Non-Human Identity (NHI) Security Market. SaaS delivery is making machine identity governance more accessible for organizations that do not want to build heavy internal infrastructure. The adoption of AI-assisted workflows is also raising governance needs at smaller firms, because even modest automation programs can create material growth in service accounts, agent credentials, and application tokens. This is where the Non-Human Identity (NHI) Security industry can broaden beyond large enterprise deployments, especially as pricing becomes easier to justify and compliance requirements move downstream. As consolidation improves platform coverage and simplifies adoption, SME demand should continue to outpace large-enterprise growth throughout much of the forecast period.

By End-User Industry: BFSI Anchors Share, Healthcare And Life Sciences Leads Growth

BFSI represented the largest end-user segment at 16.22% in 2025, giving it the leading share in the Non-Human Identity (NHI) Security Market. The sector runs large volumes of automated transaction workflows, core banking integrations, and API-linked partner activity that depend on service accounts and application credentials. Compliance also supports demand because PCI DSS 4.0 explicitly treats service accounts and application accounts as in-scope identities that require unique identification, least-privilege access, and auditability. The Digital Operational Resilience Act also strengthened the case for traceable access controls for ICT across automated systems from January 2025. This combination of operational intensity and compliance pressure kept BFSI at the front of spending.

Healthcare and Life Sciences is projected to expand at a 24.28% CAGR through 2031, making it the fastest-growing end-user segment in the Non-Human Identity (NHI) Security Market. Growth is being supported by wider use of clinical AI tools, sensitive patient information workflows, and stronger expectations around automated system access control. Information Technology and Telecom remained another major demand center because CI/CD pipelines, cloud-native workloads, and software integration layers naturally create very large NHI populations. Government and Public Sector, Retail and E-commerce, and Industrial Manufacturing also broaden the addressable base through device identities, public service automation, and API-driven transactions. The result is a more diverse demand profile in which the same governance need appears across different operating environments, even though the underlying drivers vary by vertical.

Geography Analysis

North America accounted for 32.15% of the Non-Human Identity (NHI) Security Market in 2025, making it the largest regional contributor by revenue. The region benefits from a high concentration of cloud-native enterprises, strong zero-trust adoption, and a venture environment that has supported specialist NHI vendors. It also remains the most active region for platform consolidation, with Palo Alto Networks completing its acquisition of CyberArk in February 2026 and Cisco acquiring Astrix Security in May 2026 to strengthen identity and AI agent governance capabilities. Financial services and technology buyers remain the main demand centers because they run large machine identity estates and face higher governance expectations.

Europe remained the second-largest regional market, supported by strong data sovereignty priorities and the financial sector's focus on operational resilience. The United Kingdom, Germany, and France continued to lead adoption as regulated sectors favored on-premises and hybrid options that could integrate with established IAM estates. The Digital Operational Resilience Act has added a durable compliance layer for traceable ICT access control, which supports multi-year procurement for machine identity governance in financial institutions. GitGuardian's 2026 update on protecting more than 115,000 developers and monitoring more than 610,000 repositories also points to strong demand for secrets security across development-heavy organizations operating in Europe and other regions.

Asia-Pacific is projected to expand at a 24.39% CAGR through 2031, which makes it the fastest-growing regional segment in the Non-Human Identity (NHI) Security Market. China held the largest regional revenue share in 2025, supported by large-scale cloud infrastructure expansion and the presence of domestic technology providers that can support machine identity controls. India is expected to remain the fastest-growing country in the region as digital programs, fintech expansion, and IT services growth create larger volumes of service accounts and API credentials. Japan, South Korea, and Australia also support regional demand through continued enterprise cloud adoption and growing interest in stronger governance for automation and AI-linked workloads. The Middle East and Africa remained earlier-stage markets, but digital transformation programs in the Gulf and demand from BFSI and telecom in South Africa and Nigeria continued to create an entry point for future adoption.

Competitive Landscape

The Non-Human Identity (NHI) Security Market has been moving across 3 linked platform areas: discovery and posture management, dynamic credential issuance and vaulting, and lifecycle governance. Competition in 2026, therefore, reflected both category expansion and category overlap, because vendors from PAM, IGA, secrets management, and cloud security were all moving toward the same machine identity control space. Established providers such as BeyondTrust and Delinea have been expanding their reach into machine identity and AI agent governance through product expansions rather than relying solely on older privileged access models. At the same time, purpose-built vendors continued to compete on depth in AI agent discovery, ownership mapping, and ephemeral credential control, where specialist focus still matters.

Recent transactions showed how quickly consolidation had accelerated in the Non-Human Identity (NHI) Security Market. Palo Alto Networks completed its acquisition of CyberArk in February 2026 and tied privileged access management more closely to its broader platform strategy, centered on Cortex and Strata. Cisco acquired Astrix Security in May 2026 to strengthen AI agent discovery and NHI governance within its identity and secure access portfolio. SailPoint then acquired Entro Security in June 2026 to add coverage for more than 1,200 non-human identity types and strengthen lifecycle governance across cloud and SaaS environments. These moves suggest that large security vendors no longer treat machine identity as an adjacent feature set, but as a core control layer that needs tighter platform integration.

Product differentiation has also become more evidence-driven across the Non-Human Identity (NHI) Security Market. BeyondTrust expanded its Identity Security Risk Assessment in June 2026 with a 5-pillar framework that mapped findings to NIST 800-53 and MITRE ATT&CK, which raised the commercial value of framework-aligned remediation proof. Smaller vendors still retain room to compete, especially in hybrid-cloud governance for mid-market buyers and in workload identity federation for AI agent frameworks. Oasis Security's March 2026 funding round and GitGuardian's February 2026 Series C also showed that investor and customer interest continued to support focused category players even as consolidation intensified.

Non-Human Identity (NHI) Security Industry Leaders

CyberArk Software Ltd.

Delinea, Inc.

BeyondTrust Corporation

HashiCorp, Inc.

Keeper Security, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SailPoint Technologies acquired Entro Security for approximately USD 200 million, integrating Entro's coverage of over 1,200 non-human identity types into SailPoint's Agentic Fabric product. The acquisition extended SailPoint's NHI capabilities to AI agents, machine credentials, and secrets lifecycle governance across cloud and SaaS environments.

- June 2026: Saviynt expanded its Agent Access Gateway with intent-aware runtime authorization for AI agents, introducing step-up authentication, human-in-the-loop approvals, and biometric identity verification spanning over 4,000 government-issued document formats across 177 countries. The update operationalized just-in-time governance for AI agent interactions with applications, APIs, and infrastructure.

- May 2026: BeyondTrust launched an expanded Identity Security Risk Assessment with a new 5-pillar framework covering human, non-human, and AI identity attack surfaces, including a dedicated AI Security pillar for shadow AI agents and exposed secrets. Findings are mapped to NIST 800-53 and MITRE ATT&CK and delivered within 24 hours at no charge to enterprise customers.

- May 2026: Cisco acquired Astrix Security for approximately USD 300 million to bolster AI agent discovery and NHI governance. Cisco integrated Astrix's platform with its Identity Intelligence and Cisco Secure Access offerings, providing real-time inventory of AI agents, MCP servers, and NHIs, while extending zero-trust controls to agentic deployments.

Global Non-Human Identity (NHI) Security Market Report Scope

The Non-Human Identity (NHI) Security market focuses on platforms and services that protect digital identities tied to applications, workloads, containers, devices, and cryptographic keys rather than human users. These solutions provide secure authentication, authorization, monitoring, and governance for machine-to-machine interactions, automated processes, and AI-driven systems. The market is driven by the rapid growth of cloud-native architectures, IoT ecosystems, and AI/ML applications, which have expanded the number of non-human identities in enterprise environments. With cyber threats increasingly targeting machine credentials, APIs, and service accounts, industries such as BFSI, healthcare, IT, manufacturing, government, and retail are adopting NHI security to prevent breaches, ensure compliance, and strengthen resilience. Its primary goal is to deliver secure, scalable, and automated identity management for non-human entities, reducing risk exposure and safeguarding digital infrastructures in complex enterprise ecosystems.

The Non-Human Identity (NHI) Security market report is segmented by Component (Solutions and Services), Identity Type (Application and Service Identities, Workload and Container Identities, Machine and Device Identities, Cryptographic Identities), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Application and Service Identities |

| Workload and Container Identities |

| Machine and Device Identities |

| Cryptographic Identities |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Identity Type | Application and Service Identities | ||

| Workload and Container Identities | |||

| Machine and Device Identities | |||

| Cryptographic Identities | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the Non-Human Identity (NHI) Security Market?

The Non-Human Identity (NHI) Security Market is valued at USD 8.22 billion in 2026 and is projected to reach USD 22.94 billion by 2031 at a CAGR of 22.78%.

What is driving growth in non-human identity security spending?

Growth is being supported by API expansion, cloud workload growth, identity sprawl in Kubernetes, higher breach costs from over-privileged service accounts, and stronger zero trust enforcement across machine workloads.

Which component category leads spending today?

Solutions led the market in 2025 with 61.09% share, reflecting demand for automated discovery, posture management, lifecycle governance, and real-time policy enforcement.

Which deployment model is growing the fastest?

Hybrid deployment is projected to grow at a 24.06% CAGR through 2031, even though cloud remained the largest deployment segment in 2025 with 54.21% share.

Which end-user segment is expanding the fastest?

Healthcare and Life Sciences is projected to grow at a 24.28% CAGR through 2031, while BFSI remained the largest end-user segment in 2025 with 16.22% share.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is projected to post the fastest regional CAGR at 24.39% through 2031, while North America remained the largest regional market in 2025 with 32.15% share.

Page last updated on: