Digital Identity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 75.23 Billion |

| Market Size (2031) | USD 168.75 Billion |

| Growth Rate (2026 - 2031) | 17.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Identity Market Analysis by Mordor Intelligence

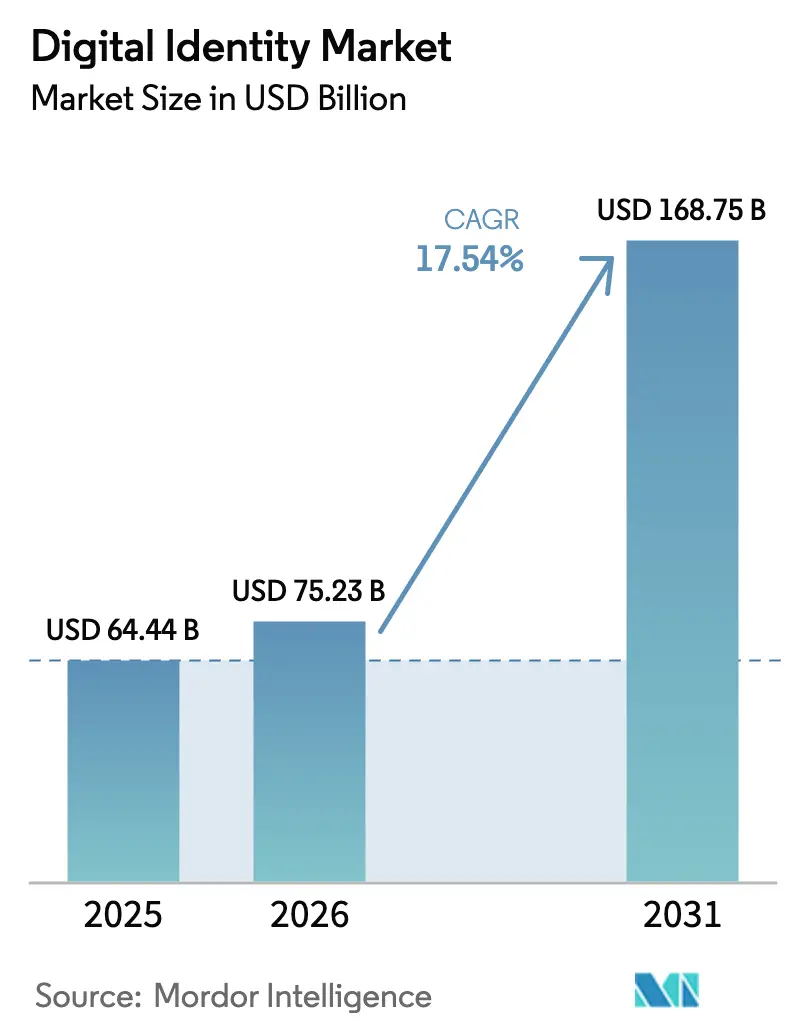

The digital identity market size is expected to grow from USD 64.44 billion in 2025 to USD 75.23 billion in 2026 and is forecast to reach USD 168.75 billion by 2031 at 17.54% CAGR over 2026-2031. Rising wallet mandates under eIDAS 2.0, record anti-money-laundering penalties, and zero-trust security frameworks have combined to accelerate the adoption curve far beyond voluntary uptake cycles. Enterprises now view identity verification as a frontline control, directing budget from perimeter hardware toward policy-as-code orchestration that scales across cloud workloads. Biometric liveness detection, continuous behavioral analytics, and verifiable-credential exchange are converging into unified customer-identity platforms, reducing vendor lock-in while heightening competition on fraud-prevention accuracy. Parallel shifts in merchant fraud economics, government service delivery, and gig-work onboarding continue to expand the addressable base for the digital identity market, ensuring that growth momentum shows no sign of plateauing.

Key Report Takeaways

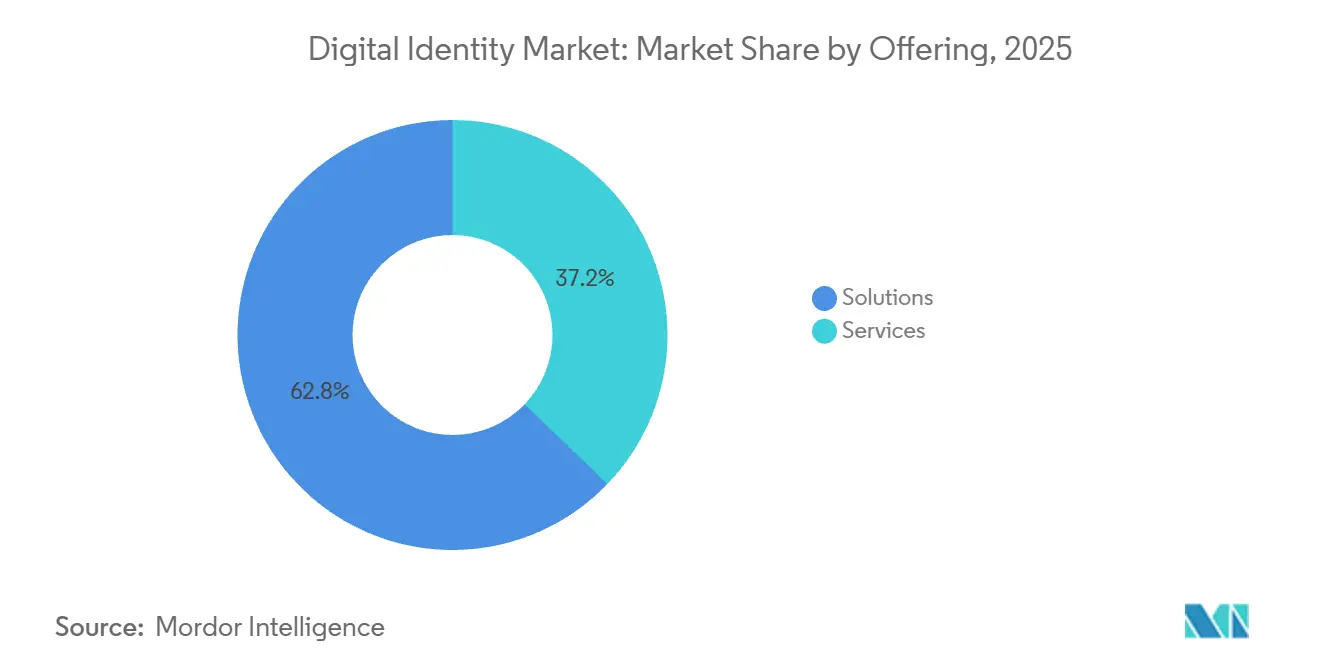

- By offering solutions, the company commanded 62.81% of the market share in 2025, while services are advancing at an 18.36% CAGR through 2031.

- By deployment mode, cloud captured 71.55% of the market share in 2025 and is forecast to expand at an 18.28% CAGR between 2026-2031.

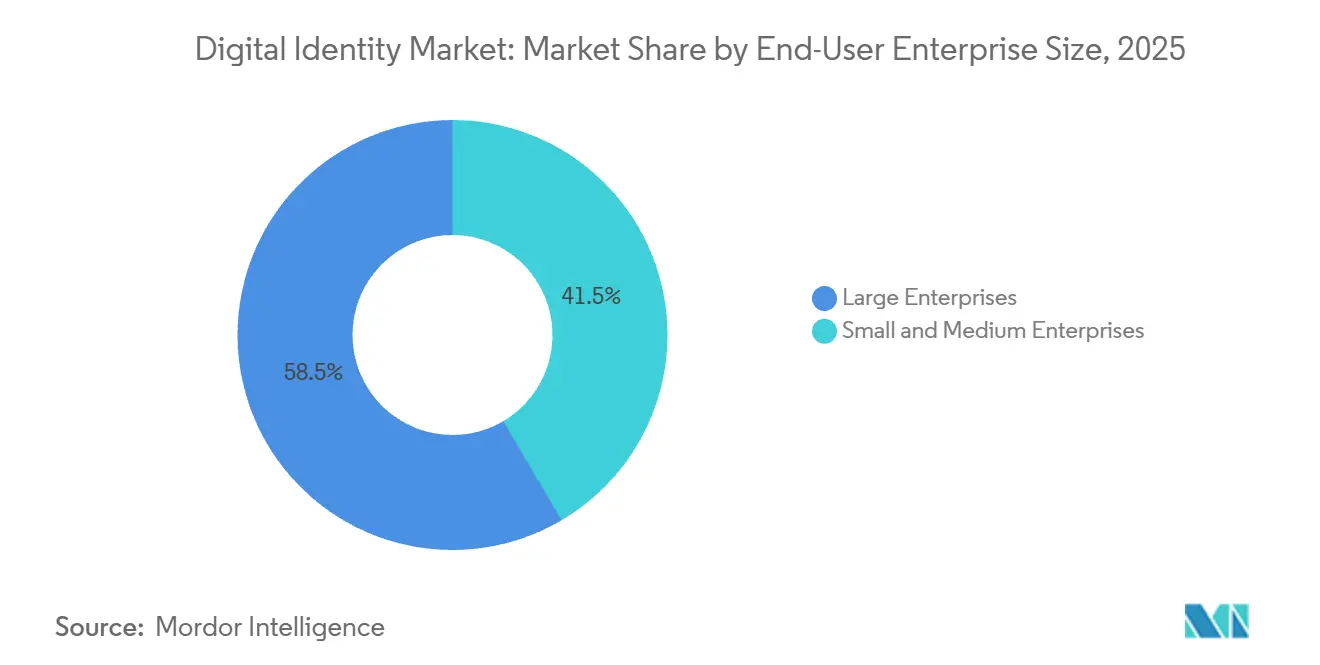

- By enterprise size, large enterprises held 58.48% of the market share in 2025, whereas small and medium enterprises are growing at a 18.49% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance led with 28.86% share in 2025, while retail and e-commerce is projected to rise at a 19.17% CAGR through 2031.

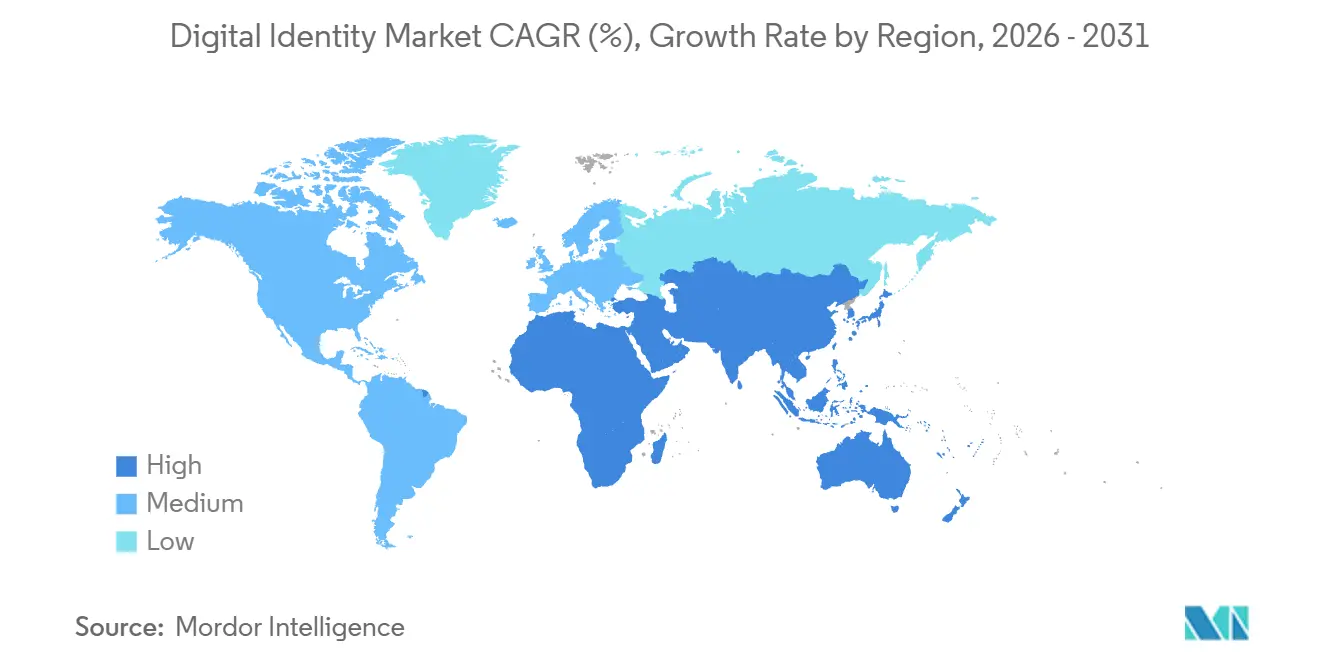

- By geography, North America accounted for 39.84% of rket share in 2025, yet Asia-Pacific is expected to record a 19.02% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Identity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of National ID-Wallet Programs | +3.5% | Europe, spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Heightened KYC and AML Compliance | +3.2% | Global, acute in financial hubs | Short term (≤ 2 years) |

| Cloud-First CIAM Adoption | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of Mobile Biometrics | +2.5% | Asia-Pacific core, accelerating globally | Short term (≤ 2 years) |

| Government Push for Digitised G2P Rails | +2.0% | Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Verifiable-Credential Demand in Supply Chains | +1.5% | Europe and North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of National ID-Wallet Programs

Mandated wallet rollouts are compressing adoption timelines, turning identity infrastructure from an optional enhancement into a regulatory requirement across the digital identity market. The eIDAS 2.0 deadline obliges every European Union member state to issue citizen wallets by December 2026, then enforces private-sector acceptance one year later, eliminating opt-out pathways for banks, telcos, and retailers. United States states are moving in parallel, with mobile driver’s licenses accepted at Transportation Security Administration checkpoints in 30 airports, even as technical formats still diverge. Japan’s MyNumber Card added health insurance functionality in 2024 and targets driver’s-license convergence by 2027, indicating that Asia-Pacific programs increasingly mirror European mandates. Platform vendors capable of ingesting multiple government-issued credentials without re-tooling core code gain a decisive advantage as enterprises recalibrate roadmaps around wallet interoperability.[1]EUROPEAN COMMISSION, “eIDAS Regulation,” digital-strategy.ec.europa.eu

Heightened KYC and AML Compliance amid Record Online Fraud

Global fraud losses and new supervisory guidelines are compelling financial institutions to abandon point-in-time checks. Continuous behavioral analytics and real-time biometric re-authentication are replacing legacy credential snapshots to satisfy updated Financial Action Task Force guidance that stresses ongoing monitoring. United Kingdom banks now bear reimbursement liability for authorized push-payment scams, pushing them to deploy live biometric step-ups on high-value transfers. Crypto-to-fiat rails face similar pressure as illicit cross-border flows top USD 40.9 billion, anchoring investment in shared-signal intelligence that flags device fingerprints and geolocation anomalies within 200 milliseconds. These dynamics strongly reinforce demand for scalable, cloud-native know-your-customer engines across the digital identity market.[2]FATF, “Updated Guidance on Digital Identity,” fatf-gafi.org

Cloud-First CIAM Adoption under Zero-Trust Architectures

Zero-trust policies, codified by NIST SP 800-207A, require identity verification for every resource request, making identity the primary control plane and relegating network perimeters to outdated status. Enterprises adopting conditional-access policies report steep declines in credential-stuffing incidents while avoiding the cost of over-provisioned on-premise appliances. Retailers handling flash-sale traffic spikes illustrate the elasticity gain; compute scales instantly, billing aligns to volume, and fraud-detection models retrain on anonymized multi-tenant telemetry. Vendors offering policy-as-code toolkits that map user, device, and application context into granular decisions are now central to procurement, solidifying cloud leadership inside the digital identity market.[3]NIST, “Special Publication 800-207A,” nist.gov

Expansion of Mobile Biometrics in Payment and Fintech Apps

Biometrics previously confined to airports are now embedded in everyday commerce. Visa’s passkey checkout cut abandonment by 23%, India’s face-match alternative reduced fingerprint failure rates, and Brazil’s Pix system lowered fraud 34% after mandating biometrics above transaction thresholds. Passkey adoption across Google, Apple, and PayPal jumped 180% in one year, even if cross-platform portability still needs maturation. Fintech startups, unburdened by hardware token logistics, prefer software development kits that tap native device sensors, facilitating rapid rollout across the digital identity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Privacy and Data-Breach Concerns | -2.8% | Global, acute in Europe, rising Asia-Pacific | Short term (≤ 2 years) |

| Regulatory and Standards Fragmentation | -2.2% | Global cross-border operations | Medium term (2-4 years) |

| Deep-Fake Driven Synthetic-ID False-Rejects | -1.8% | North America and Europe, spreading Asia-Pacific | Medium term (2-4 years) |

| Scarcity of Decentralised-ID Cryptography Talent | -1.3% | North America and Europe tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Privacy and Data-Breach Concerns

Biometric data cannot be re-issued once leaked, intensifying consumer anxiety and elevating compliance costs. Nearly 40% of European vendors still process templates in non-EU regions contrary to GDPR special-category safeguards, exposing clients to penalties that can reach 4% of global revenue. A 2024 breach that compromised 12 million facial templates drove legislative proposals to ban remote biometrics in several European countries, signaling that public trust remains fragile. Enterprises now run dual authentication tracks biometric and legacy because almost half of surveyed consumers refuse to share biometrics with private firms, capping the theoretical ceiling of the digital identity market. Vendors must therefore integrate privacy-enhancing cryptography, even at the expense of latency, to unlock the next adoption wave.[4]EDPB, “Biometric Data Processing Guidelines,” edpb.europa.eu

Regulatory and Standards Fragmentation across Regions

Conflicting data-localization mandates force multinational platforms to maintain parallel identity stacks, draining 15%–25% of budget that might otherwise fuel innovation. European algorithms specified by eIDAS 2.0 collide with China’s encryption-backdoor requirements, while India’s extraterritorial consent clauses complicate telemetry aggregation. Limited mutual-recognition prevents Japanese or Australian credentials from flowing seamlessly into European relying parties, obliging businesses to contract multiple verification providers with proprietary application programming interfaces. These discrepancies slow commercial rollout and raise the total cost of ownership for every newly launched geography, dampening the overall CAGR potential for the digital identity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Surge as Integration Complexity Escalates

In 2025, solutions accounted for 62.81% of the market share, while services are projected to grow at an impressive CAGR of 18.36% through 2031. Professional and managed services are expanding faster than packaged software because legacy core-banking and enterprise resource planning environments require protocol translation, schema alignment, and role-mapping that internal teams rarely master. Implementation partners build bridges between Security Assertion Markup Language, OAuth 2.0, and verifiable-credential protocols, reducing project risk even as they raise operating expenditure. Identity-verification solutions still dominate revenue, yet clients now demand bundled advisory, integration, and ongoing tuning rather than static license seats. Managed service providers guarantee real-time monitoring and incident response, a compelling proposition for regional banks authenticating half a million customers monthly without operating a 24/7 security operations center. This shift reallocates value toward outcome-based contracts that promise fraud-loss reduction, reinforcing the service trajectory across the digital identity market.

Frictionless onboarding and audit-ready governance further draw enterprises toward specialists who can operationalize compliance playbooks for SOC 2, ISO 27001, and sector-specific mandates. Decentralized-identity pilots, with their key-rotation and schema-design intricacies, represent fresh revenue streams for consulting partners now packaging starter kits and accelerator templates. The gravitation to services does not negate demand for solutions, but it reframes the purchasing logic; software must now arrive pre-integrated with analytics dashboards, case-management workflows, and flexible application programming interfaces, otherwise adopters default to vendors whose professional-services arms deliver an end-to-end stack. Accordingly, rising integration complexity cements the services uptrend inside the digital identity market.

By Deployment Mode: Cloud Dominance Reflects Zero-Trust Imperatives

The surge toward the cloud reflects both economic and security considerations. Real-time policy engines processing millions of authorization calls per hour demand elastic scaling, which on-prem hardware cannot match without costly headroom. Cloud platforms pool anonymized attack telemetry from thousands of tenants, training defensive models that single-tenant deployments would never accumulate. Organizations migrating to conditional-access policies report double-digit reductions in breach frequency, validating the cloud’s security posture. These attributes gave cloud a 71.55% market share of the digital identity market in 2025, and the category is forecast to grow at an 18.28% rate over 2026-2031.

On-premises retains a foothold wherever air-gaps, defense-grade resilience, or sovereign-cloud statutes apply, yet the total cost of ownership remains 40%-60% higher due to patching, hardware refreshes, and disaster recovery obligations. Hybrid strategies provide transitional relief, but they introduce synchronization latency between cloud directories and on-premise replicas that can stall session tokens or misalign privileges. Vendors that deliver migration toolkits, encryption key escrow, and point-and-click policy mapping find receptive audiences looking to modernize without jeopardizing uptime. In aggregate, cloud’s architectural strengths ensure its leadership trajectory inside the digital identity market, with on-premise increasingly relegated to niche regulatory enclaves.

By Enterprise Size: SMEs Leapfrog Legacy Constraints

Small and medium enterprises once lagged due to capital constraints and a scarcity of cryptographic talent. Cloud subscription models now invert that dynamic, letting startups embed enterprise-grade multifactor authentication through application programming interfaces configured in hours, not months. Consumption-based pricing aligns with the volatile transaction volumes common to gig-economy platforms, enabling them to pay only for authentications processed rather than for licensing dormant user seats. As a result, SMEs show an 18.49% compound annual growth through 2031, eclipsing large-enterprise momentum and broadening the addressable base for the digital identity market.

Large organizations accounted for 58.48% of the market share in 2025, thanks to their sheer scale and stringent oversight that mandates robust audit trails. Yet migration drag tied to legacy mainframes, jurisdictional overlaps, and unionized workforce retraining slows deployment. Talent scarcity compounds the hurdle; global openings for identity architects outpace qualified candidates three-to-one, inflating salaries and project durations. SMEs sidestep the constraint by offloading operations to managed service providers whose multi-tenant models embed expertise into platform logic. Consequently, fresh demand skews toward lightweight, self-service identity layers that unlock rapid launch cycles and feed the expansion of the digital identity market.

By End-User Industry: Retail Overtakes BFSI in Growth Velocity

The banking, financial services, and insurance sector dominates with a 28.86% share in 2025, yet retail and e-commerce are now the fastest climbers at a 19.17% CAGR through 2031. Synthetic-identity rings cost United States merchants USD 6 billion in 2025, fueling investment in behavioral biometrics and device-intelligence signals that profile typing cadence and touchscreen pressure. Retailers also face razor-thin margins, making false-decline avoidance paramount; Mastercard’s biometric card raised approval rates by 31%, proving that better authentication drives top-line conversion. This 19.17% forecast CAGR emphasizes why merchants are emerging as aggressive adopters within the digital identity market.

Government, healthcare, manufacturing, and telecommunications also increase demand, but through domain-specific pain points. Welfare-transfer digitization, Health Insurance Portability and Accountability Act audit stipulations, and low-latency factory access requirements each necessitate tailored identity governance patterns. Vendors now ship vertical templates that pre-configure data-retention windows, consent flows, and liveness thresholds, accelerating deployment while lowering compliance risk. Still, maintaining many vertical roadmaps strains engineering bandwidth, pushing providers to choose between deep specialization and horizontal platform breadth. Regardless, aggregate cross-vertical momentum continues to widen the digital identity market size through the forecast horizon.

Geography Analysis

North America remains the largest regional contributor, accounting for 39.84% of market share in 2025, but its growth arc has flattened as federal zero-trust mandates transition from rollout to optimization. Public-sector spending tilts toward license renewals and fine-tuning conditional-access policies rather than net-new seat expansion. Private-sector enterprises similarly shift budget away from first-time digital identity implementations toward analytics add-ons that reduce authentication friction. State-level fragmentation of mobile driver’s licenses persists, forcing residents to carry physical credentials and limiting wallet network effects. Canada’s trust framework is operational yet partial, while Mexico’s legislative vacuum introduces compliance uncertainty that tempers full-scale deployments. Overall, maturing infrastructure means incremental growth slows, even as replacement cycles stabilize regional revenue inside the digital identity market.

Asia-Pacific delivers the fastest trajectory, poised for a 19.02% CAGR between 2026-2031. India’s Aadhaar ecosystem authenticates billions of payment events monthly, and the introduction of face match cut failure rates for manual laborers whose fingerprints degrade. Japan’s MyNumber convergence targets a 2027 driver’s-license merge, trimming national administrative overhead and providing private lenders a standardized credential for credit-scoring. China’s pervasive facial-recognition rails process daily retail transactions at huge scale, though strict data-residency laws deter Western vendors. Australia’s nationwide digital identity scheme, federating government and private providers, underscores regional appetite for interoperable credentials that facilitate cross-border e-commerce. Taken together, the sheer volume of new enrollees cements Asia-Pacific as the growth engine of the digital identity market.

Europe, South America, and the Middle East and Africa form the next tranche of opportunity, each colored by unique catalysts and constraints. eIDAS 2.0 imposes a compliance countdown that should translate into rapid private-sector acceptance once wallets launch; however, fiscal variation among member states risks staggered readiness. Brazil’s Pix system, with biometric thresholds tied to transaction caps, spotlights consumer trust gains achievable when authentication improves without extra hardware. Gulf Cooperation Council nations leapfrog legacy by embedding biometrics in national portals, yet cross-border integration remains aspirational. African initiatives like Nigeria’s national ID confront rural connectivity gaps, resulting in urban-centric rollouts that risk digital exclusion. Across these theaters, vendors that localize swiftly and offer offline-capable modalities are best positioned to capitalize on the expanding digital identity market.

Competitive Landscape

The market is moderately fragmented. Thales and IDEMIA leverage decades of passport issuance experience to secure government contracts, embedding cryptographic elements that withstand advanced cloning attacks. Yet their hardware-heavy models encounter margin squeeze in consumer sectors where smartphones provide secure enclaves that eliminate standalone tokens. Microsoft’s Entra suite weaponizes its Azure Active Directory installed base, cross-selling conditional access and privileged identity functions inside enterprise license bundles. Okta positions as a neutral orchestrator across multi-cloud estates, appealing to organizations wary of single-vendor dominance in the digital identity market.

Startups focus on niche proficiency such as deep-fake resilience or rapid developer onboarding. iProov’s liveness analytics detect pixel-level spoofing, a differentiator as generative-AI tools democratize face-swap capabilities. Jumio combines document verification with sanction-screening in one workflow, reducing hand-offs and compliance gaps for fintech players. Private-equity consolidation has also reshaped the field; Ping Identity’s merger with ForgeRock under Thoma Bravo integrates workforce and customer modules, promising cost-reduction through product line rationalization. Meanwhile, standards bodies have elevated interoperability to a deciding factor. The World Wide Web Consortium’s verifiable-credential model, ratified in 2024, renders proprietary schemas less defensible, nudging vendors toward open frameworks that simplify wallet portability within the digital identity market.

Technology differentiation now hinges on adaptive fraud models trained on globally diversified datasets, privacy-enhancing computation that satisfies regional rules without compromising latency, and developer experience scored by software development kit integration simplicity. Certifications such as ISO 27001 and SOC 2 once conferred differentiation but are increasingly commoditized, pushing providers to obtain jurisdiction-specific attestations like Brazil’s LGPD or India’s Digital Personal Data Protection compliance. Given these crosscurrents, no individual company appears poised to dominate outright, and the digital identity market maintains its moderate concentration profile even as alliances and acquisitions continue to reshape boundaries.

Digital Identity Industry Leaders

IDEMIA Group

NEC Corporation

Thales Group

Experian plc

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft broadened Entra Verified ID to let clients anchor decentralized identifiers on Ethereum, Hyperledger Fabric, or private chains, accommodating jurisdictions that disallow public-ledger storage.

- December 2025: Thales aligned its Digital Identity Wallet with the European Blockchain Services Infrastructure conformance suite, setting the stage for cross-border credential presentation under eIDAS 2.0.

- September 2025: Okta embedded generative-AI policy drafting into Workforce Identity Cloud, automating least-privilege recommendations and cutting quarterly audit labor by hundreds of hours.

- February 2025: Thales launched FIDO Key Lifecycle Management, allowing organizations to rotate or revoke hardware-token keys remotely, eliminating multi-day downtime when devices are lost.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital identity market as every software platform, hosted service, and supporting consultancy that captures, verifies, federates, and governs a digital record of a person, entity, or connected device across cloud, on-premise, and hybrid environments. According to Mordor Intelligence, value is tracked only where identity creation or verification is the primary revenue driver, expressed in USD.

Scope exclusion: single-purpose password managers, stand-alone physical access badges, and hardware tokens shipped without identity-orchestration logic are not counted.

Segmentation Overview

- By Offering

- Solutions

- Identity Verification

- Authentication

- Credential Management

- Identity and Access Management (IAM)

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By End-User Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-User Industry

- BFSI

- Government and Public Services

- IT and Telecom

- Retail and E-Commerce

- Manufacturing

- Healthcare

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed senior architects in banks, national ID program officers, telecom identity heads, and SaaS CISOs across North America, Europe, the Gulf, and ASEAN. These conversations clarified average verification fees, adoption timelines, and post-implementation churn, allowing us to reconcile gaps spotted in public data.

Desk Research

We began with policy and statistical repositories such as NIST Digital Identity Guidelines, the World Bank ID4D Atlas, EU eIDAS 2.0 regulatory dossiers, ITU ICT penetration data, and BIS cyber-risk bulletins, followed by company 10-Ks, investor decks, and association portals (FIDO Alliance, EuroSmart, OpenID Foundation). Subscription feeds from D&B Hoovers and Dow Jones Factiva helped us capture vendor-level revenue shifts and contract wins. These references illustrate, not exhaust, the evidence base that grounds our desk work.

Market-Sizing & Forecasting

We start top-down by reconstructing spend from verified-user pools: active e-government IDs, digital banking customers, and remote-KYC onboarding volumes, filtered through typical price-per-check and wallet-maintenance fees. Supplier roll-ups and sampled ASP × transaction counts provide bottom-up cross-checks before totals are locked. Key variables modeled include national ID-wallet rollout deadlines, fraud-loss ratios, biometric sensor attach rates, cloud CIAM seat growth, and regulatory audit frequency. A multivariate regression blended with ARIMA handles the five-year outlook; scenario pivots adjust for compliance lags or macro-credit shocks. Where bottom-up evidence is thin, weightings are prorated using nearest proxy markets validated by our respondents.

Data Validation & Update Cycle

Outputs pass variance screens versus payment-fraud losses, smartphone shipments, and vendor bookings. Senior reviewers rerun anomaly flags, and we refresh every twelve months or sooner if material events, such as new eID mandates, shift baselines. A final pre-publication sweep ensures clients receive the most current view.

Why Mordor's Digital Identity Baseline Commands Confidence

Published estimates often diverge because each firm picks a different mix of solutions, pricing ladders, and refresh cadences.

Key gap drivers include: some studies focus only on software subscriptions, others bundle hardware readers; a few rely on historical CAGR extrapolation without primary validation; currency conversions vary, and refresh cycles stretch to three years, whereas Mordor revisits data annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 64.44 B (2025) | Mordor Intelligence | |

| USD 47.02 B (2025) | Global Consultancy A | Excludes on-premise services, limited expert interviews |

| USD 42.12 B (2024) | Industry Association B | Earlier base year, hardware weighting diluted, top-down only |

| USD 33.36 B (2025) | Regional Consultancy C | Conservative adoption scenario, revenue roll-ups by broad ICT buckets |

The comparison shows that when scope, price points, and validation depth are fully aligned, our figures sit mid-band, offering decision-makers a balanced, traceable baseline they can defend in board discussions and budget cycles.

Key Questions Answered in the Report

What is the current value of the digital identity market?

The digital identity market size reached USD 64.44 billion in 2025 and is projected to grow rapidly through 2031.

Which region is expanding the fastest?

Asia-Pacific is forecast to advance at a 19.02% CAGR between 2026-2031, fueled by large-scale national ID programs and booming mobile payments.

Why are services growing faster than software in this space?

Integration complexity, protocol translation, and compliance demands are driving organizations to purchase professional and managed services rather than standalone licenses.

How does zero-trust architecture influence identity spending?

Zero-trust policies require continuous verification of user, device, and application context, steering budgets toward cloud customer-identity platforms with elastic policy engines.

Which industry vertical currently leads adoption?

Banking, financial services, and insurance dominate overall spend, holding 28.86% share in 2025 due to stringent regulatory mandates.

What authentication trend is reducing checkout abandonment?

Passkey and biometric checkout, championed by payment networks and wallet providers, cut cart abandonment by over 20% for early adopter merchants.

Page last updated on: