Cyber Threat Intelligence Sharing Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

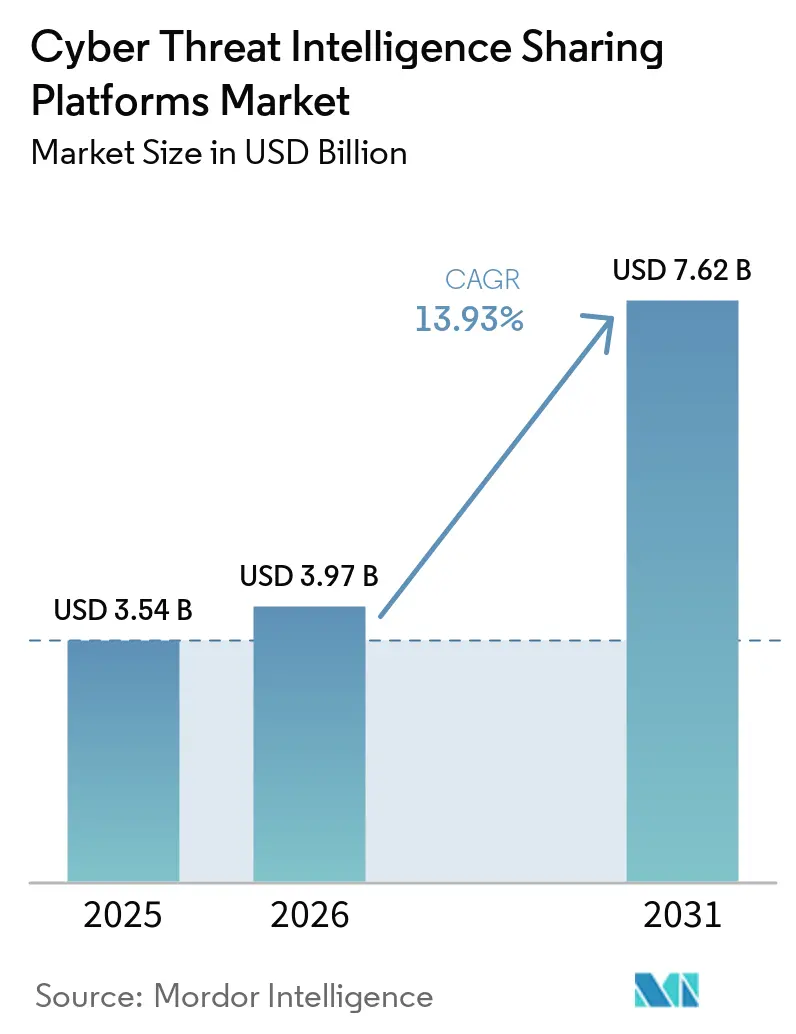

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 13.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyber Threat Intelligence Sharing Platforms Market Analysis by Mordor Intelligence

The cyber threat intelligence sharing platforms market size is projected to be USD 3.54 billion in 2025, USD 3.97 billion in 2026, and reach USD 7.62 billion by 2031, growing at a CAGR of 13.93% from 2026 to 2031. The cyber threat intelligence sharing platforms market is gaining momentum because regulatory frameworks now require faster reporting, documented intelligence exchange, and more formal cyber resilience processes, especially in financial services and other regulated sectors. The same shift is shortening evaluation timelines because many enterprises now treat shared intelligence workflows as part of operating compliance rather than as an optional enhancement to security tooling. The cyber threat intelligence sharing platforms market is also benefiting from the wider use of sector communities and shared feeds, which increases the need for platforms that can normalize and distribute intelligence at scale across many teams and tools. Competitive activity is moving toward integrated platforms, managed delivery, and acquisitions that connect external intelligence with broader fraud, cloud, and security operations workflows. A major constraint remains the gap between data volume and analyst capacity, which keeps automation, enrichment, and filtering central to product positioning in the cyber threat intelligence sharing platforms market.

Key Report Takeaways

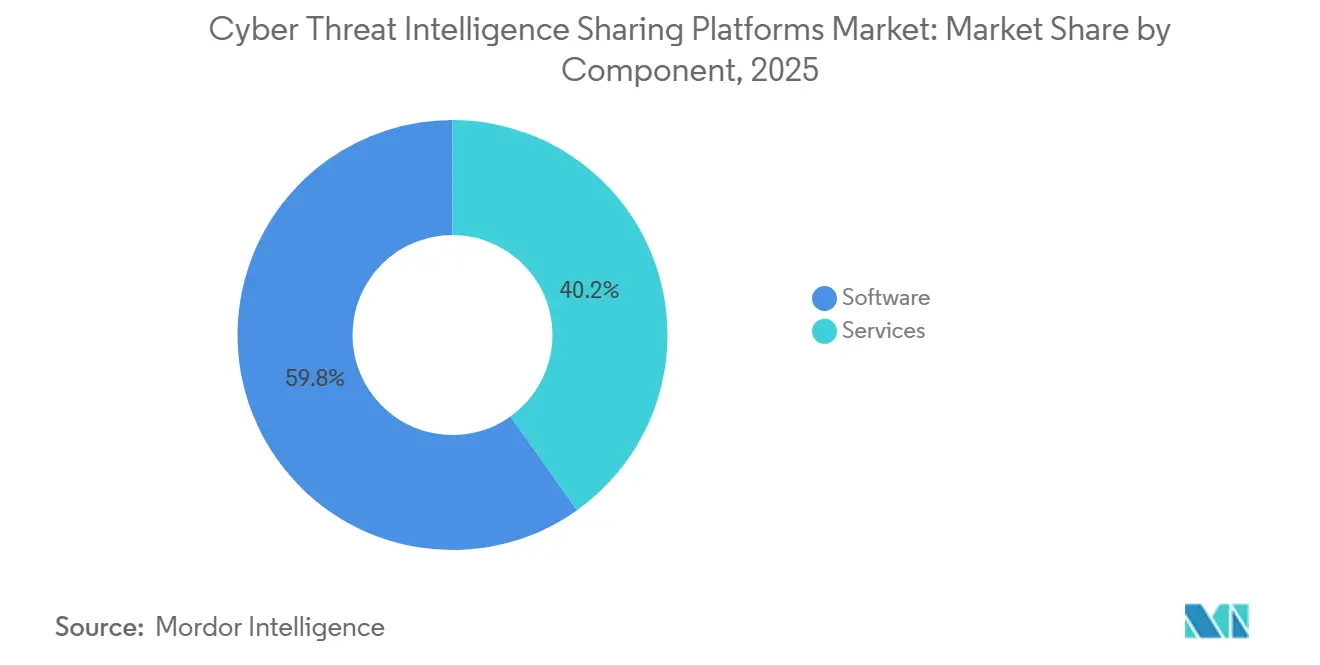

- By component, software led with 59.84% revenue share in the cyber threat intelligence sharing platforms market in 2025, while services are forecast to expand at a 14.98% CAGR through 2031.

- By deployment, cloud held 52.91% share in 2025, while hybrid recorded the highest projected 15.09% CAGR through 2031.

- By enterprise size, large enterprises accounted for 58.07% of the market share in 2025, while small and medium enterprises are projected to grow at a 15.20% CAGR through 2031.

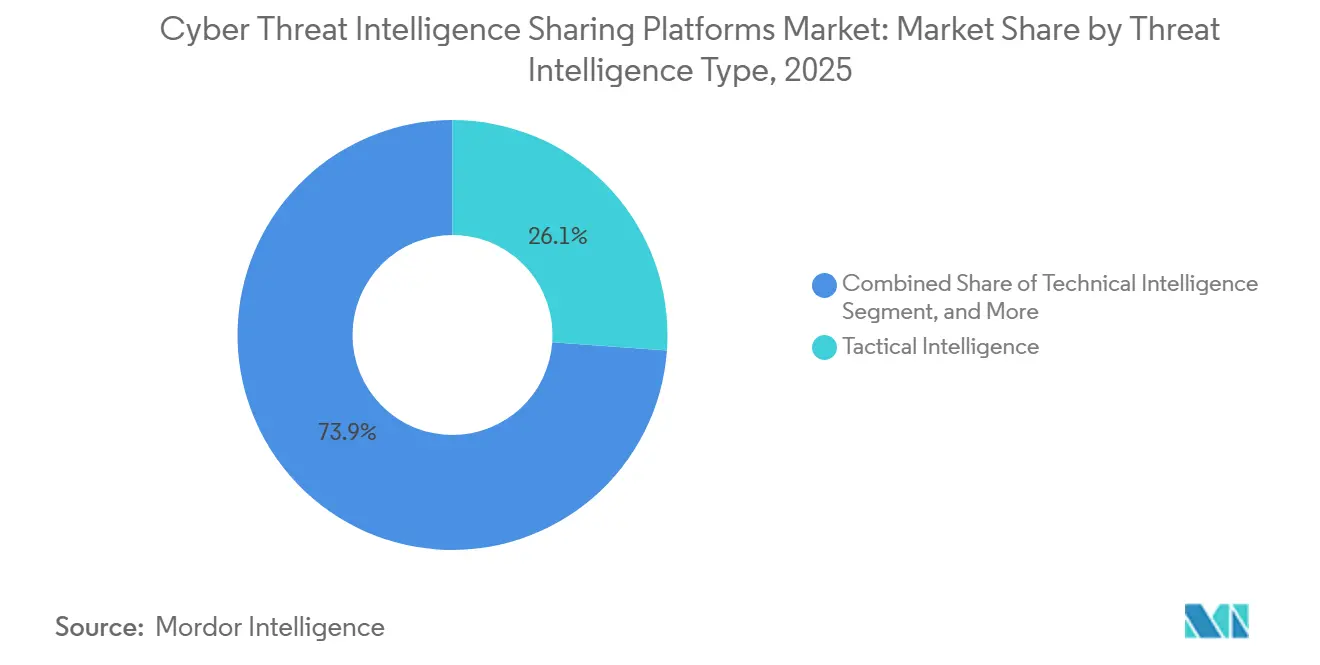

- By threat intelligence type, tactical intelligence captured 26.14% of the market in 2025, while technical intelligence is forecast to grow at a 15.31% CAGR through 2031.

- By end-user industry, BFSI held 16.11% share in 2025, while healthcare and life sciences are projected to expand at a 15.42% CAGR through 2031.

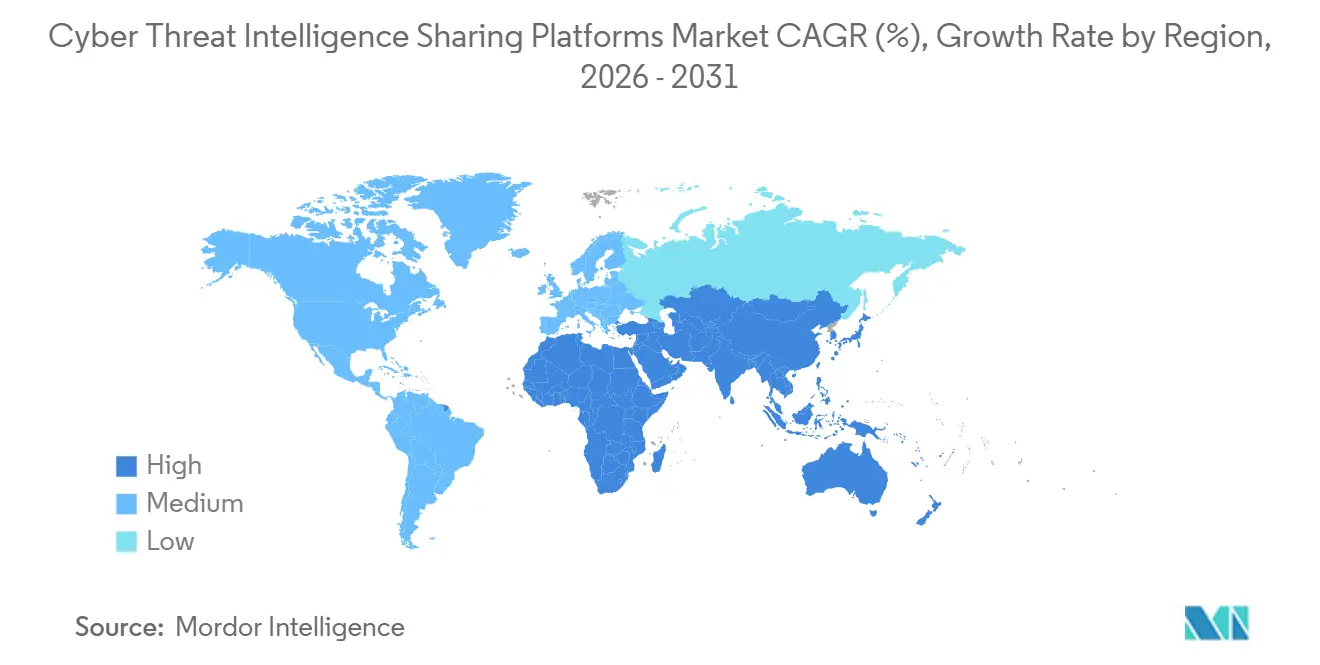

- By geography, North America led with 31.09% share in 2025, while Asia-Pacific is forecast to grow at a 15.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cyber Threat Intelligence Sharing Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure for Timely Incident Disclosure and Information Sharing | +3.0% | Global, with the strongest pull in Europe and North America | Short term (≤ 2 years) |

| Rising Frequency of Multi-Party Threat Intelligence Collaboration | +2.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Automation of IOC Normalization Across Disparate Security Stacks | +2.2% | Global, with Asia-Pacific acceleration | Medium term (2-4 years) |

| Expansion of Sectoral ISAC and ISAO Participation | +1.8% | North America core, with spillover to Europe, the Middle East, and Africa | Long term (≥ 4 years) |

| Cross-Enterprise Exposure From Third-Party and Fourth-Party Risk | +1.5% | Global, concentrated in BFSI and manufacturing | Medium term (2-4 years) |

| Demand for Shared Detection Content in Cloud and Identity-Centric Environments | +1.2% | Global, with North America and Asia-Pacific leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure for Timely Incident Disclosure and Information Sharing

Regulatory mandates are the clearest near-term growth engine for the cyber threat intelligence sharing platforms market because they turn intelligence sharing into a documented control rather than a discretionary security practice. DORA has required financial entities and their ICT third-party providers to maintain formal cyber resilience and reporting processes since January 17, 2025, which raises the need for structured evidence and repeatable intelligence workflows.[1]European Union, “Regulation (EU) 2022/2554 of the European Parliament and of the Council,” EUR-Lex, eur-lex.europa.eu The source draft also notes that NIS2 expanded cyber reporting and information-sharing expectations across a much broader set of European organizations, which materially widened the addressable base for platforms that can automate intake, classification, and distribution. This regulatory shift matters because generic security logs do not provide the same exchange structure, enrichment context, or documentation trail that formal CTI platforms can provide during reviews and incident follow-up. It also affects multinational enterprises outside Europe, as suppliers and service partners supporting European customers increasingly need common workflows that meet these compliance expectations. In practice, the cyber threat intelligence sharing platforms market is seeing regulation shape both product design and purchasing urgency.

Rising Frequency of Multi-Party Threat Intelligence Collaboration

The cyber threat intelligence sharing platforms market is also expanding as collaborative sharing models handle more data, more participants, and more sector-specific use cases than before. RH-ISAC closed 2025 with 333 core member organizations, added 52 new members during the year, reached 96% member engagement, and recorded nearly 20,000 total intelligence shares across platforms.[2]RH-ISAC, “RH-ISAC Unveils 2025 Year in Review,” RH-ISAC, rhisac.org FS-ISAC reported that its 2025 work reflected the needs of more than 5,000 financial firm members across 75 countries, with GenAI-enabled fraud and supply chain attacks ranking among the most important threats facing the sector. As the number of contributors and the volume of shared indicators rise, buyers place greater value on platforms that can merge community feeds with commercial intelligence into a single operating view. This is raising the relevance of ingestion, enrichment, confidence scoring, and workflow routing in the cyber threat intelligence sharing platforms market. Vendors that reduce the manual burden of collaboration are better placed because shared intelligence only creates value when it is easy to operationalize.

Automation of IOC Normalization Across Disparate Security Stacks

Automation has become a central buying factor in the cyber threat intelligence sharing platforms market, as most organizations still struggle to turn raw indicators into actionable detection and response steps. The source draft notes that STIX 2.1 and TAXII 2.1 are now the dominant exchange standards for machine-readable threat objects across SIEM, EDR, and SOAR environments, which supports wider interoperability in 2026.[3]Cyware Team, “What Is the Role of STIX/TAXII in Threat Intelligence Sharing,” Cyware, cyware.com The same source set states that 92% of practitioners view threat intelligence as critical, but many teams still cannot operationalize it effectively because feeds are fragmented and analyst capacity remains constrained. That gap pushes the cyber threat intelligence sharing platforms market toward solutions with embedded normalization, contextual enrichment, and stronger confidence scoring. It also shifts competition away from basic format compatibility and toward the practical ability to move intelligence into existing detection content without delay. Buyers with mixed vendor environments feel this pain most strongly, so they often favor centralized platforms that reduce manual conversion work across the stack.

Expansion of Sectoral ISAC and ISAO Participation

Sector communities continue to expand the use cases for the cyber threat intelligence sharing platforms market by bringing more organizations into formal exchange models. Health-ISAC stated that AI-enabled attacks ranked as the top concern for member executives in 2026, and its Targeted Alert program distributed more than 1,200 warnings during 2025.[4]Health-ISAC, “Annual Threat Report, Health Sector 2026,” Health-ISAC, health-isac.org That activity matters because many members rely on platforms to distribute alerts, preserve context, and connect shared warnings to local controls. The source draft also shows that NIS2 encourages member states to facilitate cybersecurity information-sharing arrangements, which supports the longer-term expansion of structured sharing ecosystems across Europe. As more sector groups formalize processes, the cyber threat intelligence sharing platforms market benefits from demand for bidirectional exchange, access control, and evidence retention. Commercial platforms gain additional relevance when organizations want the continuity of a self-sustaining operating model alongside community participation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intelligence Overload and Low Signal-to-Noise Ratio | -2.5% | Global | Short term (≤ 2 years) |

| Trust Deficits Around Data Sensitivity and Source Attribution | -2.0% | Global, more acute in Europe and Asia-Pacific because of data protection regimes | Medium term (2-4 years) |

| Integration Complexity With Legacy SIEM, SOAR, and EDR Workflows | -1.7% | Global, highest friction in large enterprise environments | Medium term (2-4 years) |

| Uneven Monetization of Shared Intelligence Across Smaller Buyers | -1.3% | Emerging markets and SME segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intelligence Overload and Low Signal-to-Noise Ratio

A major restraint in the cyber threat intelligence sharing platforms market is that feed volume is rising faster than the human capacity to review, enrich, and act on it. Google Cloud found that 82% of security practitioners worried about missing critical threats due to alert volume, 61% cited too many feeds as the main obstacle to effective operationalization of threat intelligence, and 60% pointed to insufficient analyst capacity. This means buyers are not only asking for more intelligence, but also for better filtering, ranking, and workflow automation. The problem becomes more serious when community sharing expands, because contribution volume can rise faster than an organization’s ability to score indicators and decide which ones matter. As a result, the cyber threat intelligence sharing platforms market does not benefit equally from raw volume growth, since low-quality or poorly prioritized signals can reduce practical value. Vendors that offer pre-investigation, deduplication, and alert reduction are therefore better aligned with buyer needs than vendors that mainly add new feeds.

Trust Deficits Around Data Sensitivity and Source Attribution

Trust remains a structural brake on the market for cyber threat intelligence sharing platforms, as many organizations hesitate to share telemetry that could reveal internal weaknesses, ongoing investigations, or business processes. A 2025 systematic review of cyber threat intelligence identified trust deficits, privacy breach risk, and compliance constraints as core barriers to cross-organizational sharing, while also highlighting anonymization and federated approaches as key mitigation paths. This hesitation is especially relevant where indicators may be linked to personal or sensitive operational data, since legal and governance teams often favor narrow sharing rules. The result is that some of the most operationally valuable intelligence stays within proprietary commercial collections rather than moving freely through community channels. That pattern strengthens vendors with independent collection infrastructure, but it also limits the depth and consistency of community-only models in the cyber threat intelligence sharing platforms market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Delivery Rising as Analyst Scarcity Widens

Software dominated the cyber threat intelligence sharing platforms market with a 59.84% share in 2025, which shows that buyers still prefer licensed platforms that centralize feed ingestion, scoring, enrichment, and dissemination. This leadership stems from the practical need for a common system that connects intelligence to existing security workflows without creating new silos. In the cyber threat intelligence sharing platforms market, software also benefits from deeper integration with enterprise detection and response tools. Those integrations make software the default foundation for organizations that need broad visibility, standardized workflows, and consistent handling of internal and external data.

Services is projected to grow at a 14.98% CAGR from 2026 to 2031, making it the fastest-growing component in the cyber threat intelligence sharing platforms market. Growth in services reflects the fact that many organizations need intelligence outcomes quickly but still lack enough dedicated analysts to manage the entire process in-house. The source draft points to SOCRadar’s AI Agent Marketplace as an example of how vendors are automating tasks such as phishing detection, dark web monitoring, and brand abuse protection through modular delivery models. The cyber threat intelligence sharing platforms market is, therefore, keeping software as the core layer while services expand access for buyers that want faster deployment and lower staffing pressure.

By Deployment: Hybrid Models Gaining Ground in Regulated Environments

Cloud captured 52.91% of the cyber threat intelligence sharing platforms market in 2025, supported by scalability, faster feed updates, and lower infrastructure overhead for teams that do not want to manage everything on premises. Many buyers prefer this model because it shortens setup time and makes it easier to distribute intelligence across many users and locations. In the cyber threat intelligence sharing platforms market, cloud deployment also works well for mid-sized organizations that want broad functionality without a large local operations footprint. This keeps cloud as the leading deployment model by current revenue share.

Hybrid deployment is projected to grow at a 15.09% CAGR from 2026 to 2031, making it the fastest-growing deployment type in the cyber threat intelligence sharing platforms market. The growth case is strongest in regulated sectors that want to keep sensitive telemetry or local evidence under direct control while still using cloud-scale enrichment and collaboration for less sensitive indicators. DORA and related governance pressures support this architecture by increasing the need for documented handling, resilient workflows, and clear separation of sensitive processes where needed. The cyber threat intelligence sharing platforms market is not moving away from cloud, but it is adapting to buyers who need more controlled operating models.

By Enterprise Size: SME Adoption Accelerating Through Modular and Managed CTI Models

Large enterprises accounted for 58.07% of revenue in 2025, making them the largest customer segment in the cyber threat intelligence sharing platforms market. This lead reflects earlier platform adoption, stronger compliance structures, broader attack surfaces, and larger security budgets. Large organizations also gain more from centralized intelligence because they usually operate many tools, business units, and regional security teams that need common workflows. That combination keeps enterprise demand at the center of commercial activity.

Small and medium enterprises are projected to grow at a 15.20% CAGR from 2026 to 2031, making them the fastest-growing customer segment in the cyber threat intelligence sharing platforms market. The source draft links this shift to subscription delivery, modular pricing, AI-assisted cost reduction, and the availability of open-source entry points such as OpenCTI and MISP. Kaspersky reported that cyberattacks disguised as AI tools targeting SMBs grew nearly 5 times in the first 4 months of 2026 compared with 2025, raising urgency among smaller firms. The cyber threat intelligence sharing platforms market is therefore expanding among smaller buyers as intelligence becomes easier to access through bundled, managed models.

By Threat Intelligence Type: Technical Intelligence Growing Fastest as Detection Engineering Matures

Tactical intelligence retained the largest share among intelligence types at 26.14% in 2025, showing that machine-readable indicators still anchor day-to-day SOC operations in the cyber threat intelligence sharing platforms market. IP addresses, domains, hashes, and similar artifacts remain useful because they can be directly incorporated into automated detection and blocking rules. This gives tactical content a durable role, even as buyers ask for more context and a richer understanding of threats. The segment remains closely tied to operational workflows that require speed and repeatability.

Technical intelligence is forecast to grow at a 15.31% CAGR from 2026 to 2031, making it the fastest-growing intelligence type in the cyber threat intelligence sharing platforms market. This expansion reflects rising interest in malware behavior, exploitation techniques, and adversary tactics, techniques, and procedures that can improve detection engineering and control validation. MITRE’s Center for Threat-Informed Defense published financial sector-specific ATT&CK mappings in June 2025 with support from Citigroup, JPMorgan Chase, and FS-ISAC, which helps link CTI content to defensive action in a more structured way. The cyber threat intelligence sharing platforms market is therefore moving beyond simple indicator blocking toward broader use of technique-based intelligence.

By End-user Industry: BFSI Anchors Share While Healthcare Accelerates

BFSI maintained the largest end-user industry share at 16.11% in 2025, which keeps it at the center of the cyber threat intelligence sharing platforms market. This position reflects a mix of regulatory maturity, high-value assets, and steady exposure to financially motivated threat actors. The sector also has a long history of formal information sharing and governance, which supports continued platform spending. In practical terms, BFSI remains one of the clearest examples of how CTI platforms are used as both an operational and compliance tool.

Healthcare and life sciences lead vertical growth at a 15.42% CAGR from 2026 to 2031, making it the fastest-growing end-user segment in the cyber threat intelligence sharing platforms market. SonicWall stated in its 2026 Healthcare Protect Brief that healthcare remained the most persistently targeted industry in its telemetry base, which was drawn from more than 1 million global security sensors. Health-ISAC reported that AI-enabled attacks ranked as the top concern for healthcare executives in 2026, following its Targeted Alert program, which distributed more than 1,200 warnings in 2025. The cyber threat intelligence sharing platforms market is benefiting because healthcare now treats intelligence more directly as part of operational continuity and patient safety.

Geography Analysis

North America commanded 31.09% of the cyber threat intelligence sharing platforms market in 2025, making it the largest regional segment in the source draft. The region benefits from a large base of enterprise security operations, a mature ISAC ecosystem, and established usage across BFSI, energy, healthcare, and retail. In the cyber threat intelligence sharing platforms market, these conditions support strong demand for platforms that can connect internal teams with community sharing bodies and commercial intelligence sources. The United States remains the main engine of regional demand because it combines deep enterprise spending with a broad set of sector-specific collaboration models. This gives vendors a mature environment for cross-sell opportunities, workflow integration, and managed intelligence delivery.

Europe remained a major part of the cyber threat intelligence sharing platforms market in 2025, as regulatory obligations expanded sharply following the implementation phase of NIS2 and the operational phase of DORA. The source draft states that NIS2 widened the relevant compliance coverage from approximately 20,000 to 300,000 European entities, thereby materially expanding the potential user base for structured sharing and reporting workflows. DORA has added further pressure in 2026 because financial entities and related ICT providers now need stronger documentation and resilience procedures. Europe, therefore, stands out in the cyber threat intelligence sharing platforms market as a region where buying decisions are increasingly tied to audit readiness and formal operating controls.

Asia-Pacific leads all regions in projected growth with a 15.53% CAGR from 2026 to 2031. The source draft attributes this rise to stronger nation-state activity and continued regulatory modernization across Japan, India, and South Korea. That combination is lifting demand for tools that can connect local operations with broader threat context and collaborative defense workflows. The cyber threat intelligence sharing platforms market also has room to expand across South America, the Middle East, and Africa as digital financial systems scale and formal sharing frameworks mature.

Competitive Landscape

The cyber threat intelligence sharing platforms market is moderately concentrated, with broad platform vendors such as CrowdStrike Holdings, Inc., Microsoft Corporation, Palo Alto Networks, Inc., and IBM Corporation competing alongside specialized providers such as Anomali, Inc., EclecticIQ B.V., SOCRadar Teknoloji A.Ş., and Flashpoint, Inc. This structure supports innovation because buyers can choose between large integrated ecosystems and more specialized intelligence-focused offerings. It also creates steady pricing pressure because specialized vendors must prove workflow depth, while larger vendors rely on platform breadth and installed relationships. The cyber threat intelligence sharing platforms market is, therefore, active rather than locked into a single competitive model. Large vendors have scale advantages, but smaller providers can still win by solving specific operational problems more directly.

Recent deal activity shows how competitive positioning is changing inside the cyber threat intelligence sharing platforms market. Mastercard completed its USD 2.65 billion acquisition of Recorded Future, Inc. in December 2024, which showed that CTI assets now carry strategic value for payment networks, identity services, and fraud workflows. Dataminr announced a definitive agreement in October 2025 to acquire ThreatConnect, Inc. for USD 290 million, linking real-time public signal analysis with internal threat contextualization and more adaptive client workflows. These transactions show that vendors are trying to more tightly integrate intelligence collection, contextual analysis, and action workflows. They also suggest that threat intelligence is now being treated as a core layer in broader cyber and fraud infrastructure.

Ecosystem alliances and AI-led product moves are also shaping the market for cyber threat intelligence sharing platforms. Microsoft and CrowdStrike expanded their alliance in February 2026 so the Falcon platform could be purchased through Microsoft Azure Consumption Commitments, which lowers procurement friction for enterprises already aligned with Microsoft infrastructure. CrowdStrike followed this in May 2026 with Falcon OverWatch for Defender, extending managed hunting support to Microsoft Defender for Endpoint users. SOCRadar launched its AI Agent Marketplace in March 2026, offering a more modular approach to phishing detection, dark web monitoring, and identity-related CTI tasks. Open-source platforms such as OpenCTI and MISP continue to influence the lower end of the cyber threat intelligence sharing market by providing smaller buyers a functional entry point, limiting pricing power for commercial vendors.

Cyber Threat Intelligence Sharing Platforms Industry Leaders

Recorded Future, Inc.

Anomali, Inc.

ThreatConnect, Inc.

Cisco Systems, Inc.

Palo Alto Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Anomali, Inc. launched Anomali Underground Threat Intelligence powered by RedSense, integrating five high-fidelity intelligence feeds into ThreatStream Next-Gen covering crimeware networks, nation-state actor profiles, C2 infrastructure detection, and automated credential monitoring. The product closes pre-compromise alerting gaps that conventional CTI feeds leave open, extending platform coverage to dark web and underground forum intelligence

- May 2026: CrowdStrike Holdings, Inc. announced Falcon OverWatch for Defender, extending its managed threat hunting service to Microsoft Defender for Endpoint customers. The launch completes a three-step CrowdStrike-Microsoft integration arc following the February 2026 Marketplace expansion and March 2026 Falcon Next-Gen SIEM support for Defender telemetry

- May 2026: Palo Alto Networks, Inc. completed its acquisition of Portkey, integrating Portkey's AI gateway processing trillions of tokens monthly into Prisma AIRS as a centralized control plane governing autonomous AI agent interactions. The acquisition extends Palo Alto's CTI surface to AI-native attack vectors emerging as enterprises deploy agentic AI at scale

- April 2026: Palo Alto Networks, Inc. completed its acquisition of Koi, a pioneer in Agentic Endpoint Security, establishing a new product category targeting vibe coding agents and autonomous endpoint tools that bypass traditional security controls

Global Cyber Threat Intelligence Sharing Platforms Market Report Scope

The Cyber Threat Intelligence Sharing Platforms market refers to solutions and services that enable organizations to collect, analyze, and securely share actionable cyber threat intelligence across enterprises, industries, and government ecosystems. These platforms provide strategic, tactical, operational, and technical intelligence to enhance situational awareness, strengthen cyber defenses, and foster collaboration against evolving threats. Driven by the increasing sophistication of cyberattacks, regulatory mandates for information sharing, and the need for collective resilience, industries such as BFSI, healthcare, IT, manufacturing, retail, and government are adopting these platforms to improve detection, response, and prevention capabilities. The core objective of this market is to build secure, collaborative, and intelligence-driven ecosystems that reduce risk exposure and enhance resilience against advanced cyber adversaries.

The Cyber Threat Intelligence Sharing Platforms market report is segmented by Component (Software and Services), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Threat Intelligence Type (Strategic Intelligence, Tactical Intelligence, Operational Intelligence, Technical Intelligence), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Strategic Intelligence |

| Tactical Intelligence |

| Operational Intelligence |

| Technical Intelligence |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Threat Intelligence Type | Strategic Intelligence | ||

| Tactical Intelligence | |||

| Operational Intelligence | |||

| Technical Intelligence | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected size of the cyber threat intelligence sharing platforms market by 2031?

The cyber threat intelligence sharing platforms market is projected to reach USD 7.62 billion by 2031, rising from USD 3.97 billion in 2026 at a CAGR of 13.93%.

Which region currently leads spending on cyber threat intelligence sharing platforms?

North America led the cyber threat intelligence sharing platforms market in 2025 with a 31.09% share.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 15.53% during 2026 to 2031.

Which deployment model is growing the fastest?

Hybrid is the fastest-growing deployment model in the cyber threat intelligence sharing platforms market, with a 15.09% CAGR during 2026 to 2031.

Which buyer group is creating the biggest new growth opportunity?

Small and medium enterprises are the fastest-growing customer segment, with a projected CAGR of 15.20% through 2031.

Which end-user vertical is most important today and which is growing fastest?

BFSI held the largest 2025 share at 16.11%, while healthcare and life sciences is growing the fastest at a 15.42% CAGR through 2031.

Page last updated on: