HR and Finance Unified Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.78 Billion |

| Market Size (2031) | USD 27.38 Billion |

| Growth Rate (2026 - 2031) | 14.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR and Finance Unified Data Platform Market Analysis by Mordor Intelligence

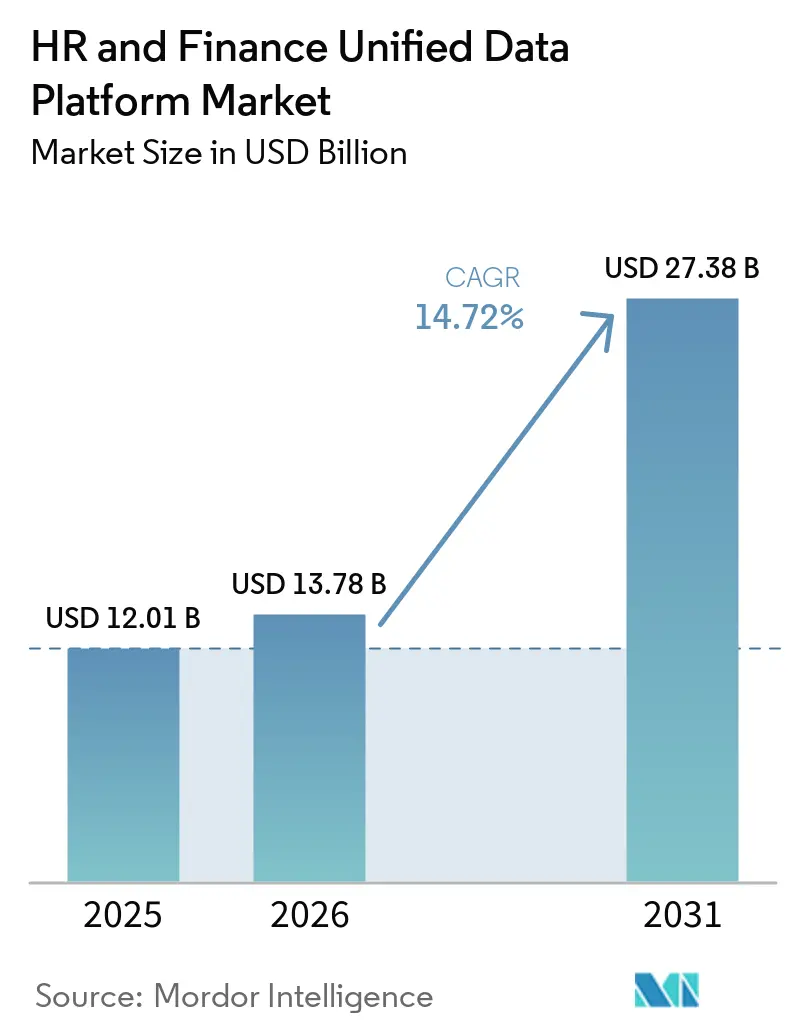

The HR and Finance Unified Data Platform market size is expected to increase from USD 12.01 billion in 2025 to USD 13.78 billion in 2026 and reach USD 27.38 billion by 2031, growing at a CAGR of 14.72% over 2026-2031. Growth is being shaped by the way finance and people leaders are now measured against the same operating goals, especially workforce cost efficiency, talent return, and skills readiness. That shift is pushing enterprises to move away from separate systems for headcount, payroll, and financial reporting, because the delay between those systems now affects planning quality and management accountability. Cloud migration is also changing the economics of adoption, as organizations replace siloed HR and finance software with platforms that can support a single data model and continuous updates. AI-enabled planning and decision support are strengthening demand because scenario modeling works better when workforce and financial records sit in one governed environment. The largest opportunity remains with enterprises that need one operating record across payroll, planning, compliance, and workforce analytics, even as migration complexity continues to slow conversion in older system estates.

Key Report Takeaways

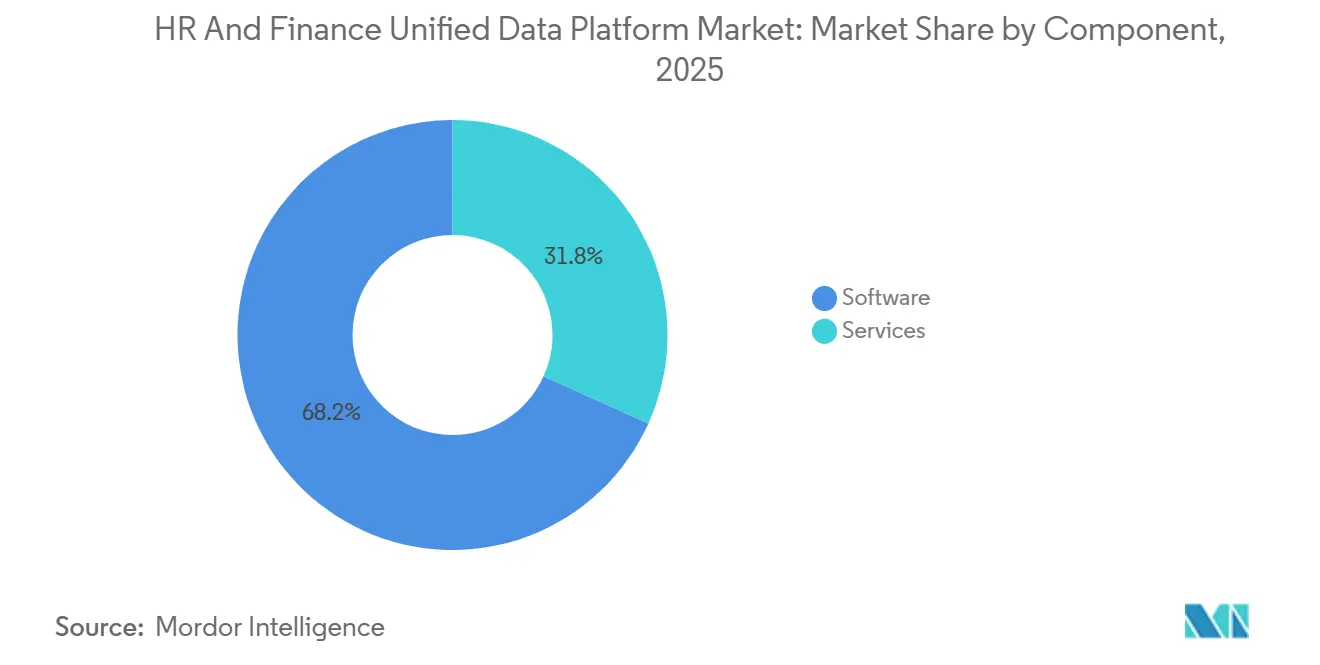

- By component, software accounted for 68.24% of revenue in the HR and Finance Unified Data Platform market in 2025, while services are projected to expand at a 15.58% CAGR through 2031.

- By deployment mode, cloud held 72.83% of the HR and Finance Unified Data Platform market share in 2025, while on-premises is projected to grow at a 14.97% CAGR through 2031.

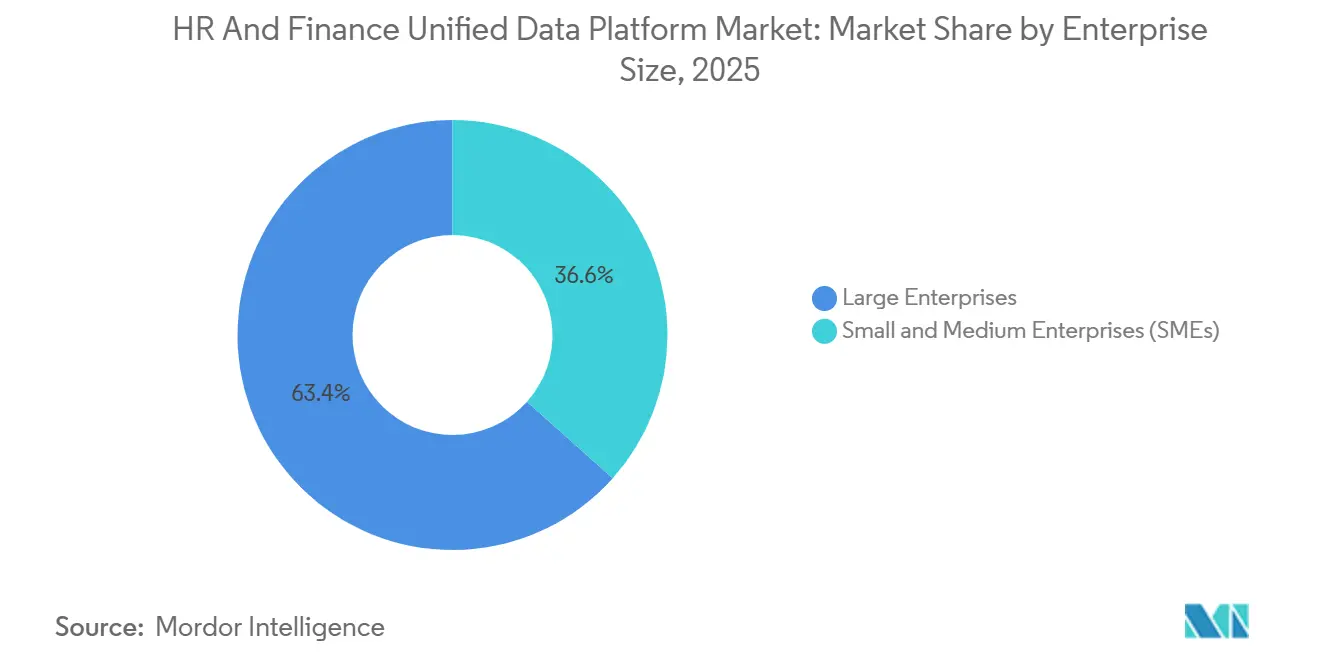

- By enterprise size, large enterprises accounted for 63.39% of revenue in 2025, while SMEs are expected to record the highest CAGR of 15.91% through 2031.

- By industry vertical, information technology and telecommunications held the largest share in 2025, while healthcare and life sciences are projected to expand at a 16.88% CAGR through 2031.

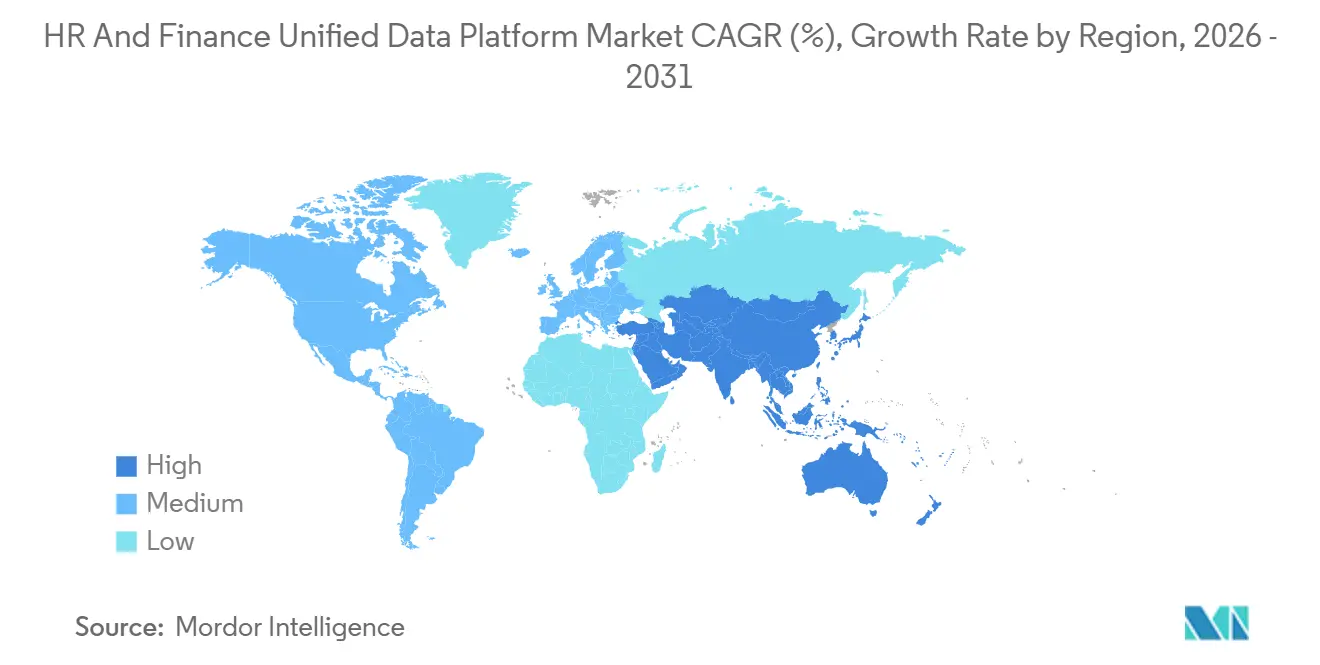

- By geography, North America accounted for 41.76% of global revenue in 2025, while Asia-Pacific is expected to grow at a 15.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR and Finance Unified Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Demand for Unified Workforce and Financial Truth Across the CFO and CHRO Office | +3.5% | Global | Short term (≤ 2 years) |

| Accelerating Cloud Migration Away From Siloed HR and Finance Systems | +3.0% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| AI-Enabled Planning, Forecasting, and Decision Support Across People and Money Data | +2.8% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Compliance Pressure From Multi-Jurisdiction Payroll, Labor, and Disclosure Rules | +2.2% | EU, North America, APAC (India, Japan, Australia) | Short term (≤ 2 years) |

| Employee Experience Expectations for Consumer-Grade Self-Service and Mobile Workflows | +1.8% | Global, with emphasis on Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of Skills-Based Workforce Planning and Internal Talent Mobility | +1.5% | North America, Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Unified Workforce and Financial Truth Across the CFO and CHRO Office

The HR and Finance Unified Data Platform market is being supported by a structural change in enterprise accountability, as CFOs and CHROs are increasingly judged on the same operating outcomes. Workforce cost per unit, headcount efficiency, retention quality, and skills readiness now sit closer to financial planning than they did in earlier software cycles. When those leaders work from separate systems, even routine planning becomes slower because the same decision needs to match employee, payroll, and cost-center records. That is why the demand driver is not simply a preference for modern software, but a need for one trusted operating record across people and money data. The HR and Finance Unified Data Platform market also benefits from joint buying decisions, because HR and finance teams are now more likely to evaluate vendors in the same procurement cycle. This shortens the distance between strategy, budgeting, and execution, and it makes platform unification easier to justify at the board level.

Accelerating Cloud Migration Away from Siloed HR and Finance Systems

The HR and Finance Unified Data Platform market is also being driven by the replacement of aging on-premises HRIS and ERP estates with cloud-based platforms. Nearly 40% of enterprises still relied on older on-premises HR and ERP environments in July 2025, indicating how much migration work remains in the installed base. SAP’s mainstream ECC support deadline has added urgency to those transition plans, because many organizations are already being pushed toward broader ERP renewal programs. The migration event matters because HR and finance data models are usually reviewed at the same time, creating a natural opening for vendors that offer unified platform architectures. Budget constraints, integration complexity, and internal resistance still slow large projects, especially in mature enterprises with many local systems. Even so, the HR and Finance Unified Data Platform market continues to benefit from this cycle, as cloud migration is now tied to compliance visibility, governance, and real-time access controls rather than simple infrastructure replacement.

AI-Enabled Planning, Forecasting, and Decision Support Across People and Money Data

The HR and Finance Unified Data Platform market is benefiting from enterprise demand for AI tools that can act on live transactional data rather than on disconnected extracts. That matters because planning for workforce cost, hiring, compensation, and productivity is much more useful when HR and finance data share the same structure. Workday made Sana globally available in March 2026, with more than 300 HR and finance workflow skills on a single AI layer for customers using the platform.[1]Workday, “Workday Launches Sana Globally,” Workday Newsroom, newsroom.workday.com Oracle also introduced 22 Fusion Agentic Applications in March 2026 across finance, HR, supply chain, and customer experience, with those tools operating natively inside Oracle Fusion Cloud Applications. Native deployment inside the transaction layer matters because it strengthens governance, reduces workflow friction, and supports auditability in sensitive processes such as payroll and compensation. As a result, the HR and Finance Unified Data Platform market is moving from basic reporting integration to platforms that support scenario planning, guided actions, and governed automation in a single environment.

Compliance Pressure from Multi-Jurisdiction Payroll, Labor, and Disclosure Rules

The HR and Finance Unified Data Platform market is also gaining support from tighter payroll, labor, and disclosure obligations across multiple jurisdictions. The EU Pay Transparency Directive requires member states to transpose salary range disclosure and pay equity reporting obligations into national law by June 7, 2026. Germany’s federal guidance has also highlighted the link between existing national pay transparency rules and the expanded obligations coming through the directive framework. In the United States, state-level pay-range disclosure requirements continue to spread, and Massachusetts is among the states that now require structured pay-range disclosure in job postings. These rule changes raise the cost of fragmented payroll architectures because multinationals cannot produce consistent compensation and workforce disclosures from disconnected systems. That is why the HR and Finance Unified Data Platform market is increasingly being selected on architecture quality, data structure, and reporting readiness, rather than on feature lists alone.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Data Reconciliation and Migration Complexity Between Legacy HRIS, ERP, and Payroll Stacks | -2.5% | Global, highest in North America and Europe (mature enterprise deployments) | Medium term (2-4 years) |

| Integration Risk From Fragmented Identity, Security, and Master Data Architectures | -2.0% | Global, with highest exposure in APAC and multi-entity European deployments | Medium term (2-4 years) |

| Elevated Total Cost of Ownership for Global, Multi-Entity Deployments | -1.5% | North America, Europe, APAC | Long term (≥ 4 years) |

| Resistance to Process Standardization in Mature Enterprises With Country-Specific Workflows | -1.2% | Europe (Germany, France), Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Data Reconciliation and Migration Complexity Between Legacy HRIS, ERP, and Payroll Stacks

The main restraint on the HR and Finance Unified Data Platform market is the effort required to clean, map, and reconcile data across legacy HRIS, ERP, and payroll stacks. Strada reported that nearly 40% of enterprises still relied on aging on-premises HR and ERP platforms in July 2025, and the same research identified budget limits, integration complexity, and resistance to change as major blockers.[2]Strada, “Research on Legacy HR and ERP Modernization Barriers,” Strada, stradaglobal.com In practical terms, many enterprises still hold duplicate employee records, inconsistent cost-center structures, and local job codes that do not align across systems. Those issues extend project timelines because vendors cannot automate migration until the underlying business rules are standardized. This slows large conversions even when the long-term business case remains strong, and it raises the service burden for providers working in mature enterprise environments. The HR and Finance Unified Data Platform market, therefore, keeps growing, but conversion speed remains lower where technical debt is deepest.

Integration Risk from Fragmented Identity, Security, and Master Data Architectures

A second restraint on the HR and Finance Unified Data Platform market comes from fragmented identity, security, and master data architectures. Many global organizations still operate separate identity tools, different employee identifiers, and inconsistent charts of accounts across business units. A unified platform cannot deliver reliable planning or reporting if those foundational records are not aligned before rollout. This risk is more visible in multi-entity deployments, where local payroll rules, local finance structures, and separate procurement histories create conflicting system logic. The result is a longer implementation cycle, more custom integration work, and greater audit exposure when exceptions surface during payroll runs or financial close. The HR and Finance Unified Data Platform market remains attractive under these conditions, but the path to value is slower when governance foundations are fragmented at the start.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth is Pulling Ahead of the Software Base

Software represented 68.24% of revenue in 2025, while services are projected to grow at a 15.58% CAGR from 2026 to 2031. That mix shows why the HR and Finance Unified Data Platform market still depends on software as its revenue base, even as services expand faster around complex deployments. Software remains central because buyers still need a unified data foundation, orchestration tools, analytics, and decision support applications that can sit on one operating model. At the same time, implementation demand rises whenever enterprises need to connect multiple HRIS, payroll, and finance environments across entities and jurisdictions. This is especially true in the HR and Finance Unified Data Platform market, where migrations often involve data cleansing, process redesign, role mapping, and change management at the same time.

The services category is expanding faster because unification is not a simple installation project, and many organizations need ongoing support after go-live to stabilize reporting, workflows, and controls. The September 2025 global payroll cloud partnership between ADP and SAP, which moved an initial wave of 50 multinational clients to SAP Cloud ERP in under 12 months, shows how recurring migration and support activity now sits alongside the software layer. In this setting, advisory and optimization work matters almost as much as technical integration because enterprises are trying to avoid carrying old processes into new systems. The software layer still anchors the HR and Finance Unified Data Platform market size, but the faster rise of services reflects the depth of transformation needed to make unified records useful in daily operations. This balance between recurring subscription revenue and recurring service engagement is likely to remain a defining trait of the component mix through 2031.

By Deployment Mode: Cloud Leads, While Hybrid and On-Premises Still Serve Complex Environments

Cloud held 72.83% of revenue in 2025, giving it the largest position in the deployment mix, while on-premises is projected to expand at a 14.97% CAGR through 2031. That share pattern shows that the HR and Finance Unified Data Platform market has already moved firmly toward SaaS delivery for most new demand. Cloud has the clearest advantage where organizations need regular compliance updates, faster release cycles, and easier access to analytics and AI services. A single cloud environment also makes it easier to manage global templates, shared controls, and centralized workforce reporting across multiple entities. For many buyers in the HR and Finance Unified Data Platform market, those benefits outweigh the flexibility of older local deployments.

Still, on-premises and hybrid models remain relevant because not every organization can move all people and finance records into a public cloud environment at the same pace. Strada’s 2025 research shows that a large installed base of aging on-premises systems remains active, which means many enterprises are still making gradual migration choices rather than full platform replacements. Regulated sectors such as financial services, government, and large healthcare systems often keep certain records closer to home because of data residency, security classification, or payroll validation requirements. Hybrid deployment therefore serves as a bridge, especially when cloud HR is paired with legacy ERP during a multi-year modernization program. This leaves the HR and Finance Unified Data Platform market with a clear cloud center of gravity, but not with a uniform migration path across all buyer groups.

By Enterprise Size: Large Enterprises Hold Revenue, While SMEs Set the Growth Pace

Large enterprises accounted for 63.39% of revenue in 2025, while SMEs are projected to grow at a 15.91% CAGR through 2031. That split explains how the HR and Finance Unified Data Platform market currently works, with the largest contracts still concentrated in organizations that run complex, multi-module, and multi-entity environments. Large enterprises drive current revenue because they process larger workforce volumes, carry wider payroll exposure, and have a stronger need to connect compensation, planning, and financial close processes. They also face greater pressure to align CFO and CHRO priorities across many countries, many legal entities, and many local compliance rules. In the HR and Finance Unified Data Platform market, these buyers often need broader deployment support, deeper governance controls, and more structured change programs than smaller firms.

SMEs, however, are moving faster because SaaS pricing, faster setup, and bundled functionality have lowered the threshold for adoption. Smaller organizations are more willing to start with one platform for HR, payroll, and finance instead of layering new tools onto legacy stacks over time. That gives them a structural advantage because they can establish unified records earlier, with fewer custom interfaces and fewer historical exceptions. Vendors are responding by packaging workforce administration, reporting, payroll services, and planning tools into simpler subscriptions that are easier to buy and easier to scale. As a result, the HR and Finance Unified Data Platform industry is seeing growth from two very different buyer groups, one that sustains revenue through scale and another that accelerates adoption through speed and lower entry friction.

By Industry Vertical: Healthcare and Life Sciences is Setting the Growth Curve

Healthcare and life sciences are projected to expand at a 16.88% CAGR through 2031, while information technology and telecommunications held the largest share in 2025. This reflects two different forms of demand inside the HR and Finance Unified Data Platform market. IT and telecommunications led early because these organizations adopted SaaS more quickly, operate distributed workforces, and place a high value on headcount analytics linked to financial planning. Healthcare and life sciences are growing faster because labor cost pressure, shift-based scheduling, credential tracking, and reimbursement-linked financial oversight all depend on better coordination between people and money data. Workday states that more than 850 healthcare organizations use its sector-focused ERP capabilities, which shows how strongly this vertical is already leaning toward integrated operational models.[3]Workday, “Healthcare Organizations Using Workday,” Workday, workday.com

The vertical mix is widening beyond those two leaders, but the intensity of need still varies by sector. Manufacturing, banking, financial services, insurance, and retail all have strong ERP and payroll integration needs, yet advanced analytics adoption is still less mature in many deployments. Government and public sector demand is also rising because modernization programs are pushing agencies toward greater workforce and budget visibility, even though procurement cycles remain long and rule-heavy. Professional services show notable momentum because resource allocation, skills visibility, and project financial performance are tightly connected in daily management. This makes healthcare and life sciences the fastest-growing engine, while IT and telecommunications remain the scale anchor for the HR and Finance Unified Data Platform market size across vertical demand.

Geography Analysis

North America held 41.76% of global revenue in 2025, giving the region the largest share of the HR and Finance Unified Data Platform market size. The United States remains the largest national market because it combines deep enterprise software penetration, heavy payroll complexity, and strong demand for connected planning across people and finance functions. The region also benefits from the presence of major platform vendors and a buyer base that is already familiar with SaaS-based ERP and HCM rollouts. Canada is building as a secondary growth area, supported by technology-sector expansion and rising adoption among mid-sized firms that want one operating record instead of separate administrative tools. Mexico adds another layer of demand because nearshore manufacturing expansion is increasing interest in payroll modernization and multi-entity workforce reporting across cross-border operations.

Europe is shaped by regulatory complexity, long-established enterprise software estates, and varied country-level payroll models. Germany remains central to regional demand, and IAB reported that the German labor market professional pool declined by around 40,000 people in 2026, which raises the importance of workforce planning efficiency for employers. SAP also notes that SuccessFactors is localized for more than 100 countries, which gives the company a strong structural position in European enterprise deployments that need broad country coverage.[4]SAP, “SuccessFactors Localization Coverage,” SAP, sap.com The EU Pay Transparency Directive created a near-term compliance catalyst across the region because member states must transpose the rules by June 7, 2026. The Middle East is also becoming more relevant, led by Saudi Arabia and the United Arab Emirates, where workforce nationalization programs are increasing demand for detailed HR-finance reporting on labor composition and employment policy outcomes.

Asia-Pacific is the fastest-growing region, with the HR and Finance Unified Data Platform market projected to advance at a 15.22% CAGR through 2031. India is a major driver because digital payroll modernization and data governance requirements are forcing both buyers and vendors to think more carefully about local hosting, control, and compliance. China is supported by domestic enterprise software suppliers, including Kingdee and Yonyou, both of which position finance, HR, and operations on broader unified platform models for business customers. Africa remains smaller in current revenue terms, but South Africa and Nigeria are showing early momentum as formalization needs and mobile-first payroll adoption create a stronger base for broader platform demand.

Competitive Landscape

The HR and Finance Unified Data Platform market is moderately concentrated at the enterprise tier, but it remains clearly contested in the mid-market. Workday, Oracle, SAP, ADP, and UKG all hold meaningful positions because they can link payroll, planning, reporting, and workforce administration more tightly than single-function software vendors. In the HR and Finance Unified Data Platform market, that integrated model matters because buyers increasingly want one governed data layer rather than a loose network of connectors between separate tools. The strongest vendors are also moving their AI capabilities into the transaction core, which increases both performance and switching costs for customers already using the platform. Workday’s Sana and Oracle’s Fusion Agentic Applications both show this shift toward native, governed automation inside the system of record. Strategic moves in 2025 and 2026 show how competition is changing from module breadth toward data intelligence, governance, and ecosystem control. Workday and Google Cloud expanded their partnership in May 2026 to integrate AI agents for HR and finance into employee workflows through Workday Data Cloud and Google Cloud services. Oracle introduced 22 Fusion Agentic Applications in March 2026, which strengthened its position around embedded automation, auditability, and execution within finance and workforce processes.[5]Oracle, “Oracle Introduces 22 Fusion Agentic Applications,” Oracle, oracle.com ADP’s October 2025 acquisition of Pequity added compensation planning depth to its HCM portfolio, especially for clients dealing with pay equity and scenario planning needs. ADP and SAP also deepened their global payroll cloud partnership in September 2025, reinforcing the value of payroll scale combined with cloud ERP infrastructure for multinational accounts.

The market still leaves room for challengers because no vendor has locked up every buyer tier or every vertical use case. In the mid-market, competition is sharper because customers want unified records, but they remain sensitive to implementation cost, service intensity, and product simplicity. Compliance expectations are also rising for AI-enabled platforms, and Cornerstone’s 2025 Workforce AI launch referenced ISO/IEC 42001 for AI management, which shows how governance standards are becoming part of the competitive bar for enterprise software providers. The HR and Finance Unified Data Platform market is therefore best described as enterprise-led in scale, but still open in structure, with the next phase of rivalry centered on automation quality, data governance, and fit for multi-entity operations.

HR and Finance Unified Data Platform Industry Leaders

Workday, Inc.

Oracle Corporation

SAP SE

Automatic Data Processing, Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Workday and Google Cloud strengthened their strategic partnership by integrating AI agents into daily HR and finance workflows. This collaboration combines Workday's Agent System of Record with Google Cloud's Gemini Enterprise and BigQuery.

- March 2026: Workday globally launched Sana, its enterprise AI platform designed to manage HR, finance, and agents. The Sana Self-Service Agent automates over 300 HR and finance workflow skills, now available to all Workday customers through Flex Credits.

- March 2026: Oracle introduced 22 Fusion Agentic Applications across HR, finance, supply chain, and customer experience. These applications operate natively within Oracle Fusion Cloud Applications, ensuring enterprise governance and auditability. The Workforce Operations and Collectors Workspace applications specifically address payroll accuracy and cash flow management, reflecting Oracle's transition from AI assistance to AI-driven outcome execution.

- October 2025: ADP acquired Pequity, a compensation management software provider established in 2019, to enhance its global compensation planning capabilities for mid-size, enterprise, and multinational clients. Pequity's AI-powered insights and scenario planning tools are being integrated into ADP's HCM ecosystem to address complex pay equity and compensation benchmarking needs.

- September 2025: ADP and SAP announced a global payroll cloud partnership, successfully migrating 50 multinational clients to SAP Cloud ERP within 12 months. This collaboration enables ADP Global Payroll, which supports millions of employees across more than 140 countries, to operate on SAP's cloud ERP backbone while incorporating AI-driven compliance and productivity tools.

Global HR and Finance Unified Data Platform Market Report Scope

An HR and Finance Unified Data Platform is a centralized system designed to integrate workforce and financial data into a unified framework. This platform connects key functions such as payroll, benefits, talent management, budgeting, and financial planning. By consolidating these datasets, it delivers real-time insights, enhances decision-making, and promotes collaboration between HR and finance teams. This integration enables organizations to improve operational efficiency, maintain compliance, and execute strategic workforce and financial planning effectively.

The HR and Finance Unified Data Platform Market Report is segmented by Component (Software, and Services), Deployment mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry Vertical (Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Information Technology and Telecommunications, Manufacturing, Retail and E-Commerce, Government and Public Sector, Professional Services, Energy and Utilities, and Other End-User Industry Verticals), and Geography, (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | HR and Finance Unified Data Foundation Layer |

| Data Integration and Orchestration Layer | |

| Workforce, Financial and Talent Analytics Layer | |

| Decision Intelligence Applications | |

| Services | Implementation and Integration Services |

| Data Architecture and Migration Services | |

| Managed Data Platform Services | |

| Advisory and Optimization Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Information Technology and Telecommunications |

| Manufacturing |

| Retail and E-Commerce |

| Government and Public Sector |

| Professional Services |

| Energy and Utilities |

| Other End-User Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | HR and Finance Unified Data Foundation Layer |

| Data Integration and Orchestration Layer | ||

| Workforce, Financial and Talent Analytics Layer | ||

| Decision Intelligence Applications | ||

| Services | Implementation and Integration Services | |

| Data Architecture and Migration Services | ||

| Managed Data Platform Services | ||

| Advisory and Optimization Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Industry Vertical | Banking, Financial Services, and Insurance | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecommunications | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Government and Public Sector | ||

| Professional Services | ||

| Energy and Utilities | ||

| Other End-User Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the HR and Finance Unified Data Platform market size through 2031?

The market was valued at USD 12.01 billion in 2025, stands at USD 13.78 billion in 2026, and is forecast to reach USD 27.38 billion by 2031 at a 14.72% CAGR.

Which deployment model leads current adoption?

Cloud leads adoption with 72.83% of revenue in 2025, supported by easier updates, centralized controls, and stronger fit for analytics and AI services.

Which buyer group is expanding the fastest?

SMEs are projected to grow at a 15.91% CAGR through 2031, while large enterprises still account for the biggest current revenue base at 63.39%.

Which vertical offers the strongest growth outlook?

Healthcare and life sciences is expected to grow fastest at a 16.88% CAGR, driven by labor-cost pressure, shift complexity, credential oversight, and tighter links between staffing and financial performance.

Which region has the strongest near-term momentum?

Asia-Pacific is the fastest-growing region with a projected 15.22% CAGR through 2031, while North America remains the largest current regional base with 41.76% of revenue in 2025.

What is the main obstacle slowing wider adoption?

The biggest hurdle is migration complexity across legacy HRIS, ERP, and payroll systems, especially where enterprises still carry fragmented employee records, cost centers, and security models.

Page last updated on: