Data Management Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

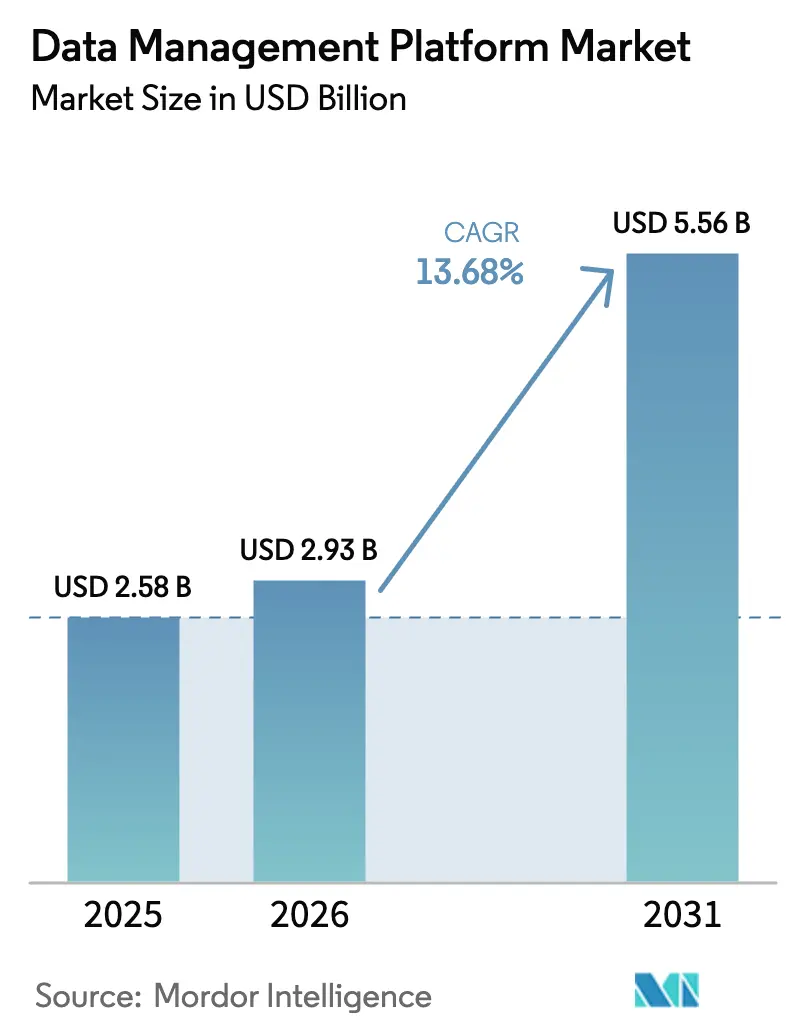

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 13.68% CAGR |

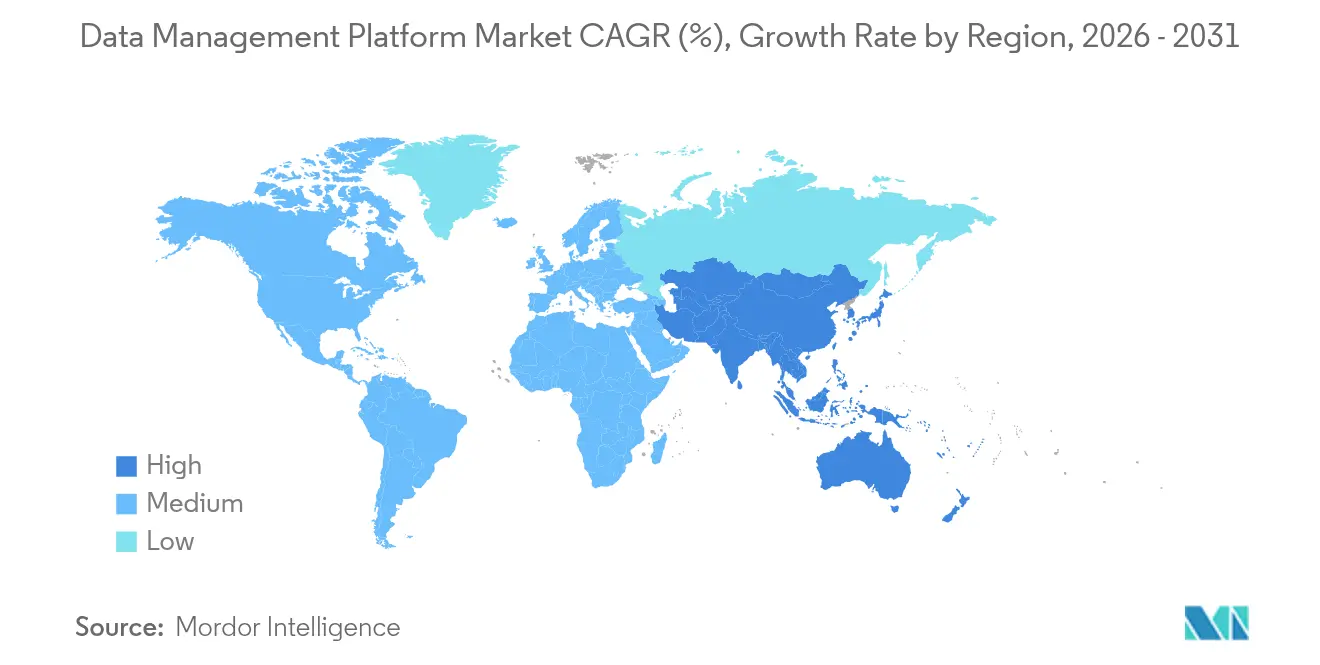

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

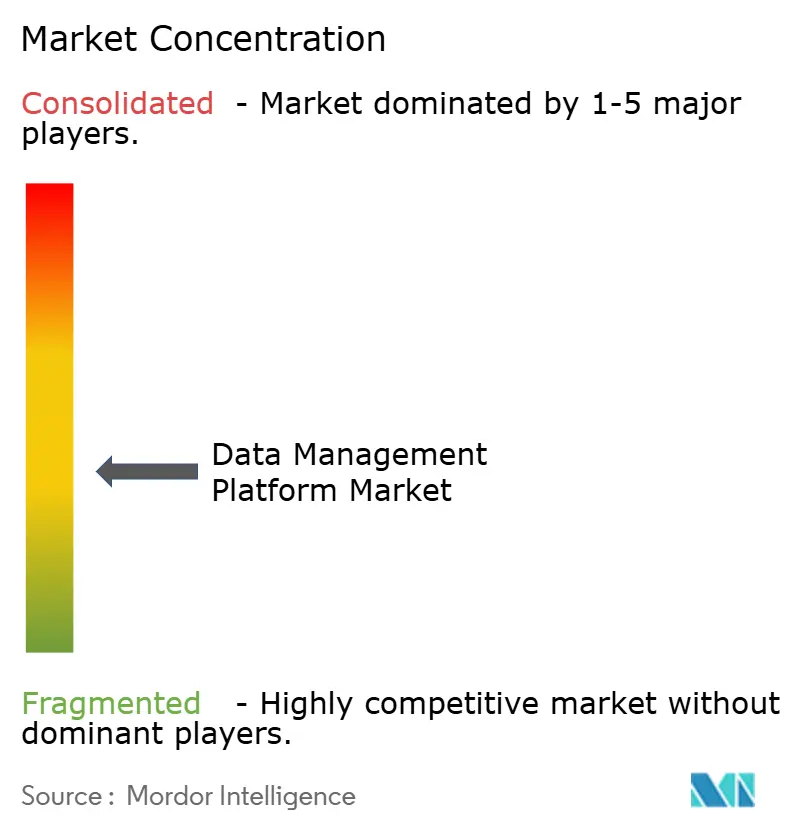

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Management Platform Market Analysis by Mordor Intelligence

The data management platform market size was valued at USD 2.58 billion in 2025 and estimated to grow from USD 2.93 billion in 2026 to reach USD 5.56 billion by 2031, at a CAGR of 13.68% during the forecast period (2026-2031). Intensifying privacy regulations and the retirement of third-party cookies are compelling enterprises to unify disparate customer data within privacy-first architectures that support AI-driven personalization at scale. Retail media networks, now monetizing first-party insights as an independent revenue stream, further accelerate platform adoption. Cloud elasticity, embedded machine-learning services, and composable APIs allow organizations to consolidate point tools into a single orchestration layer capable of real-time decisioning. The data management platform market also benefits from widening 5G coverage and edge computing investments that raise ingestion volumes and lower latency thresholds for activation. Competitive dynamics remain fluid as vendors race to embed predictive analytics, consent management, and secure collaboration features directly into their core offerings.

Key Report Takeaways

- By deployment, cloud delivery captured 69.87% of the data management platform market share in 2025 while holding the highest 14.31% CAGR through 2031.

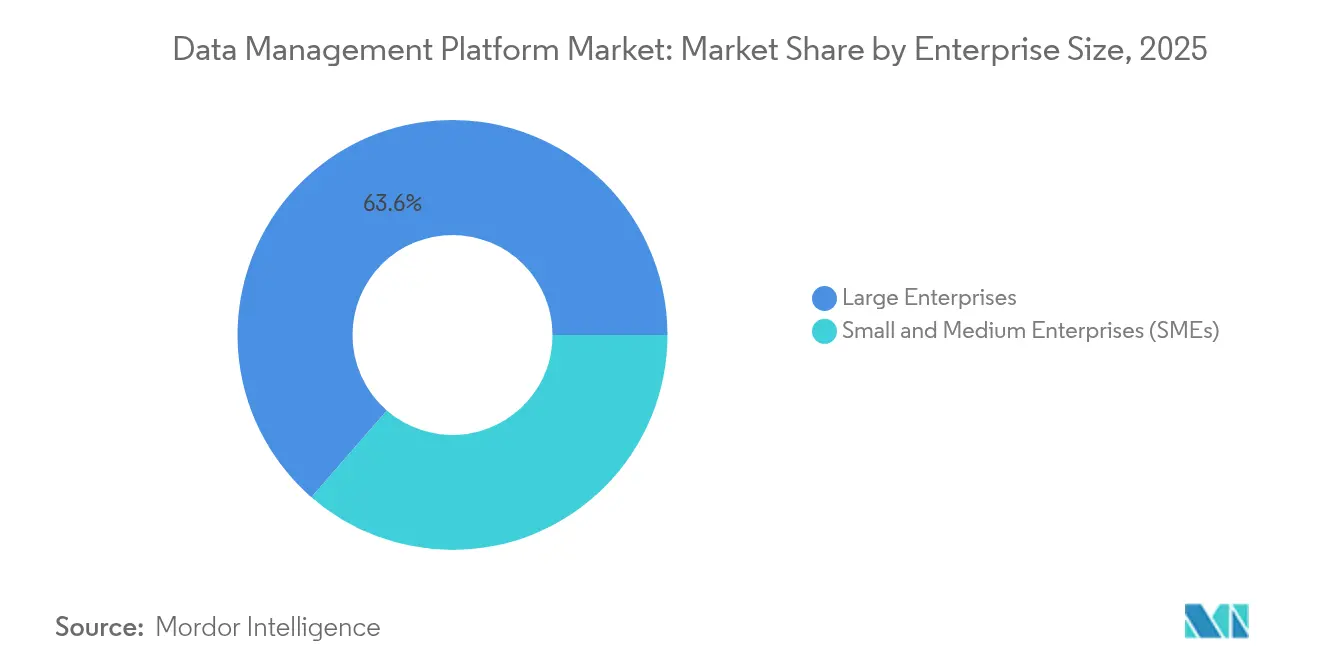

- By enterprise size, SMEs posted the briskest 15.25% CAGR, even though large enterprises retained 63.60% revenue share of the data management platform market size in 2025.

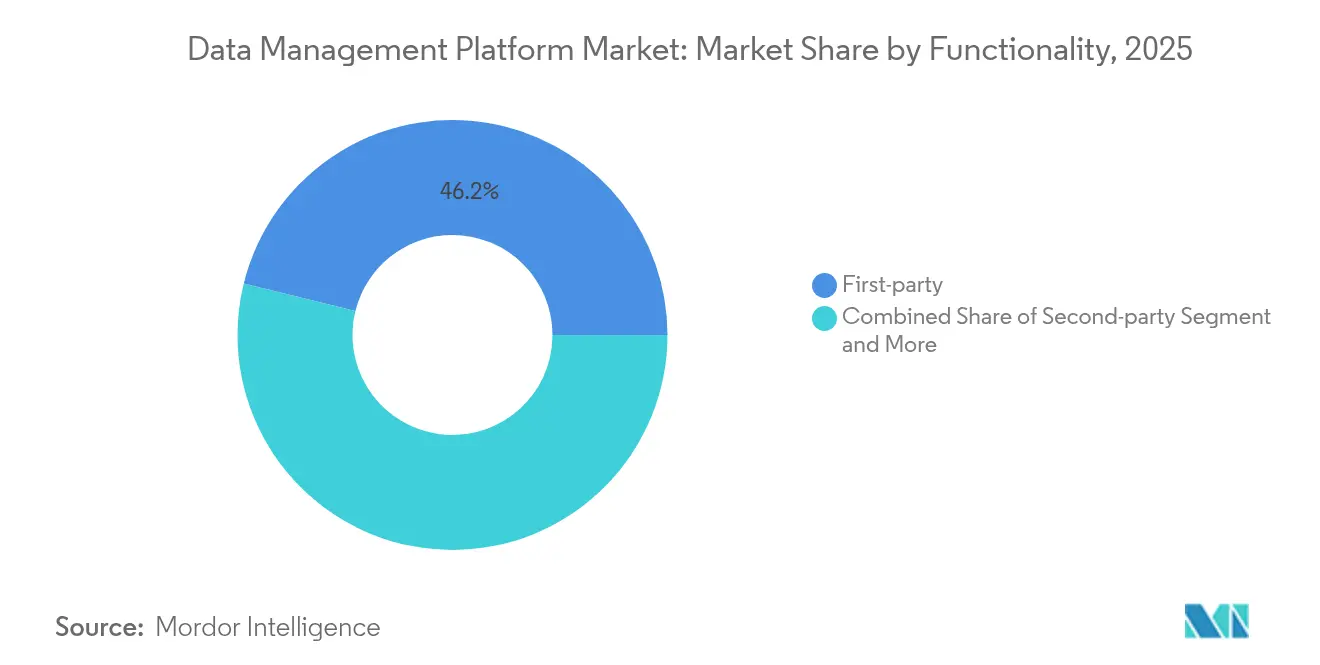

- By functionality, first-party data modules led with 46.15% of 2025 revenue, whereas second-party data recorded the quickest 16.92% CAGR to 2031.

- By data source, mobile web and apps climbed at a 15.77% CAGR, outpacing web analytics tools that held 30.78% of the data management platform market share in 2025.

- By industry vertical, healthcare and pharma advanced at an 17.85% CAGR to 2031, although retail and e-commerce commanded 26.18% of the 2025 data management platform market size.

- By geography, North America generated 38.92% of 2025 revenue, while Asia-Pacific is poised for a 26.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Data Management Platform Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investments in AI-driven audience analytics | +3.2% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising privacy-compliant first-party data strategies | +2.8% | Global, led by Europe and North America | Short term (≤2 years) |

| Omnichannel customer-journey orchestration needs | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Retail media networks’ surge in first-party data monetization | +1.9% | North America and Europe, emerging in Asia-Pacific | Short term (≤2 years) |

| De-siloing martech stacks through unified IDs | +1.5% | Global, early rollout in North America | Long term (≥4 years) |

| Edge-enabled real-time governance* | +1.1% | Asia-Pacific and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing investments in AI-driven audience analytics

Enterprises now embed machine-learning models that parse real-time behavioral signals across web, mobile, and connected devices to build adaptive segments within seconds. Adobe allocated USD 1 billion to expand its Experience Platform Agent Orchestrator, enabling brands to deploy autonomous agents that adjust offers on the fly.[1]Adobe Inc., “Introducing Experience Platform Agent Orchestrator,” adobe.com Sophisticated churn-prediction algorithms then trigger retention pathways, improving subscription lifetime value.

Rising privacy-compliant first-party data strategies

Annual compliance outlays range from USD 7.7 million to USD 30.9 million for large organizations, while penalties average 2.71 times higher than proactive spending. Firms therefore favor zero-party surveys, data clean rooms, and consent solutions that update permissions instantaneously across every connected channel.[2]Snowflake Inc., “What Is a Data Clean Room?,” snowflake.com

Omnichannel customer-journey orchestration needs

Eighty-nine percent of marketers cite cross-channel data stitching as a perennial hurdle.[3]Martech, “89% of Marketers Still Struggle With Cross-Channel Data,” martech.org Consumers interact across six to eight brand touchpoints per purchase, obliging platforms to ingest event streams and activate bespoke messages within milliseconds. IoT telemetry enriches these models by feeding product-usage signals back into acquisition and upsell workflows.

Retail media networks’ surge in first-party data monetization

Retail media spend rose from USD 20 billion to USD 40 billion and is projected to eclipse USD 75.1 billion as merchants convert shopper data into high-margin advertising inventory. Amazon alone generated USD 46.9 billion in ad revenue in 2023, highlighting the profit potential.

Restraints Impact Analysis of Data Management Platform Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-party cookie deprecation uncertainty | -2.1% | North America and Europe | Short term (≤2 years) |

| Fragmented global privacy regulations | -1.8% | Global, higher complexity for multinationals | Medium term (2-4 years) |

| High total cost of ownership for bespoke on-premise deployments | -1.3% | Regulated industries worldwide | Long term (≥4 years) |

| Scarcity of skilled CDP/DMP integration talent | -1.1% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Third-party cookie deprecation uncertainty

Seventy-five percent of marketers still rely on cookies as Google prolongs its phase-out, prompting parallel investments in both legacy IDs and emerging alternatives that double infrastructure costs. Divergent browser policies further erode attribution accuracy and complicate ROI measurement.

Fragmented global privacy regulations

Data-localization statutes now touch 75% of countries, obliging multinational enterprises to engineer region-specific storage, processing, and consent flows. Smaller firms struggle to fund these parallel stacks, amplifying competitive gaps and delaying market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Data Management Platform Market Segment Analysis

By Functionality – First-party data dominance accelerates

First-party modules secured 46.15% of 2025 revenue within the data management platform market and remain central to privacy-first personalization strategies. Second-party partnerships expand at a 16.92% CAGR as allied brands co-model insights without breaching regulations. Third-party enrichment continues but loses budget share amid quality concerns. Progressive profiling and zero-party interactions deepen preference graphs, raising predictive accuracy beyond demographic segmentation. Organizations also exploit proprietary engagement channels to refine psychographic clusters, proving that data quality now outweighs raw volume.

Expanding progressive profiling means brands incrementally earn trust while compiling granular customer history. This cadence fuels stronger lifetime value projections and heightens return on ad spend through more precise bid modifiers. The trend confirms maturing expectations in the data management platform market, where customer trust becomes the primary performance currency.

By Data Source – Mobile analytics drives growth

Web analytics tools still account for 30.78% of 2025 revenue, yet mobile web and apps grow fastest at 15.77% CAGR as smartphone sessions exceed 60% of digital media time. Mobile applications emit rich sensor data, enabling contextual offers tied to location or device state. CRM and point-of-sale feeds enrich lifetime value models, while social network inputs fall as API restrictions tighten.

Edge processing pushes select mobile events to the cloud in under 30 milliseconds, meeting sub-second personalization thresholds. Mobile session authentication reduces bot interference, elevating attribution fidelity. Consequently, leading adopters report lower acquisition costs and greater incremental revenue per engaged user.

By Deployment – Cloud infrastructure dominates

Cloud models command 69.87% of 2025 revenue and expand at 14.31% CAGR, benefiting from elastic compute, embedded AI services, and certifications that satisfy regional privacy acts. On-premise estates persist where sovereignty rules mandate local processing, but hybrid bridges now offload compute-intensive analytics to the cloud while keeping sensitive datasets on site. This blend answers scalability and compliance in a single architecture.

Cloud interoperability accelerates time-to-value for SMEs by exposing low-code APIs and pre-built connectors. Advanced encryption, confidential computing, and zero-trust blueprints have assuaged earlier security reservations. With cost-per-terabyte declining annually, more enterprises shift batch workloads and real-time inference pipelines alike to multi-cloud clusters.

By Enterprise Size – SME adoption accelerates

Large companies still hold 63.60% of 2025 spending, yet SMEs log the swiftest 15.25% CAGR as pay-as-you-go licenses shrink barriers to entry. Typical SME analytics budgets fall between USD 10,000 and USD 100,000, or 2–6% of annual expenditure. Cloud-native starters supply turnkey templates and automated governance that offset limited technical staff. OECD now reports that 72% of SMEs use data to inform daily decisions.

Outcome-based pricing models resonate with resource-scarce firms that demand provable gains in conversion or retention before committing bigger allocations. Success stories drive peer adoption, spreading the data management platform market beyond Fortune 500 cohorts.

By Industry Vertical – Healthcare leads innovation

Retail and e-commerce retained 26.18% of 2025 revenue, but healthcare and pharmaceuticals pace the field with an 17.85% CAGR through 2031. Innovaccer’s Health Cloud already supports 39 million patient records across 1,600 locations while scoring 93.6 for customer relationship functionality. Strict HIPAA rules force specialized consent modules and audit trails that generic stacks rarely supply out of the box.

Financial services rely on real-time fraud classification and regulatory reporting, whereas media companies monetize content through audience segmentation and frequency controls. Travel and hospitality platforms ingest dynamic inventory variables to power revenue-management algorithms. Vertical-specific extensions demonstrate that one-size-fits-all offerings no longer satisfy nuanced compliance and workflow demands inside the data management platform market.

Geography Analysis

North America Data Management Platform Market

North America generated 38.92% of 2025 revenue behind mature martech ecosystems and state-level privacy laws that push enterprises toward first-party conversion paths. Average monthly compliance costs range from USD 1,125 for basic CCPA coverage to USD 2,275 for broad privacy programs. Retail media pioneers further lift spending by reinvesting ad revenue into richer identity graphs.

APAC Data Management Platform Market

Asia-Pacific advances at a 26.85% CAGR due to 5G rollout, AI commercialization, and supportive digital-economy agendas. Regional data-center capacity reached 12,206 MW active with 14,338 MW planned, underpinning hyperscale deployments. Nevertheless, localization statutes in China and Vietnam complicate cross-border flows, compelling vendors to offer region-specific hosting and federated analytics.

Europe Data Management Platform Market

Europe sustains moderate growth through GDPR-driven best practices that elevate consent orchestration and data minimization. German, UK, and French enterprises lead investment, while smaller markets lean on cloud-based subscriptions to bridge capability gaps. European governance frameworks increasingly influence global product roadmaps as multinational clients request unified compliance layers that mirror EU rigor.

Competitive Landscape

The data management platform market features moderate fragmentation, with platform giants and niche specialists vying for share across horizontal and vertical use cases. Adobe, Oracle, and Salesforce bundle orchestration, identity, and AI under expansive cloud suites, whereas BlueConic, Permutive, and Lotame concentrate on publisher analytics, privacy-safe activation, or cookieless identity. Consolidation continues: Salesforce moved to acquire Informatica for USD 8 billion, Publicis secured Lotame, and Rokt obtained mParticle for USD 300 million.

Differentiation now hinges on privacy-preserving computation such as secure multi-party analytics, differential privacy, and federated machine learning. Vendors also cultivate vertical accelerators—healthcare-ready templates, banking-grade risk modules, or retail media monetization toolkits—to sidestep one-size-fits-none pitfalls. Open APIs and event routers further arm clients seeking composable stacks rather than monoliths.

Data Management Platform Industry Leaders

Adobe Inc.

Oracle Corp.

Salesforce Inc.

SAP SE

Lotame Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Data Management Platform Market Companies Covered in this Report

- Adobe Inc.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Lotame Solutions Inc.

- Neustar (TransUnion)

- SAS Institute Inc.

- Cloudera Inc.

- The Trade Desk

- Treasure Data (Arm)

- OnAudience.com

- Snowflake Inc.

- Nielsen Holdings

- Experian plc

- BlueConic

- Permutive

- Amobee

- Krux Digital (Salesforce)

- Dun and Bradstreet

- Epsilon (Publicis Groupe)

Recent Industry Developments in Data Management Platform Market

- May 2025: Salesforce agreed to buy Informatica for USD 8 billion, adding large-scale data integration and governance capabilities.

- May 2025: SAS unveiled custom AI models that tackle entity resolution and document parsing under a USD 1 billion industry-solution fund.

- March 2025: Adobe launched Experience Platform Agent Orchestrator, enabling real-time activation of AI agents across omnichannel journeys.

- January 2025: Rokt acquired mParticle for USD 300 million to fuse commerce optimization with first-party data platform technology.

Global Data Management Platform Market Report Scope

A data management platform (DMP) centralizes the collection, organization, and management of vast data volumes from diverse sources. This enables organizations to efficiently store, process, and analyze data, leveraging it for purposes like marketing, customer insights, decision-making, and analytics.

The study tracks the revenue accrued through the sale of data management platforms by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The data management platform market is segmented by data types (first party, second party, and third party), data source (web analytics tool, mobile web, mobile apps, CRM data, POS data, and social network), end-user (Ad agencies, marketers and publishers), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

Segmentation Overview

| First-party |

| Second-party |

| Third-party |

| Web Analytics Tools |

| Mobile Web and Apps |

| CRM Data |

| POS Data |

| Social Networks |

| Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Retail and e-Commerce |

| Media and Entertainment |

| BFSI |

| Healthcare and Pharma |

| Travel and Hospitality |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Functionality | First-party | ||

| Second-party | |||

| Third-party | |||

| By Data Source | Web Analytics Tools | ||

| Mobile Web and Apps | |||

| CRM Data | |||

| POS Data | |||

| Social Networks | |||

| By Deployment | Cloud | ||

| On-premise | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | Retail and e-Commerce | ||

| Media and Entertainment | |||

| BFSI | |||

| Healthcare and Pharma | |||

| Travel and Hospitality | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving revenue growth in the data management platform market between 2025 and 2031?

Growth stems from stricter privacy laws, third-party cookie deprecation, and the need for AI-ready first-party data that improves personalization efficiency.

Which deployment model dominates the data management platform market?

Cloud deployment holds 69.87% of 2025 revenue, due to elastic compute and built-in compliance frameworks.

Why are healthcare organizations adopting data management platforms rapidly?

HIPAA compliance and patient-centric personalization push healthcare and pharma toward specialized platforms, yielding an 17.85% CAGR.

How significant is Asia-Pacific’s role in future market expansion?

Asia-Pacific posts the fastest 26.85% CAGR, supported by 5G rollout and new data-center capacity that underpins large-scale deployments.

Page last updated on: