HR Data And Reporting Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.65 Billion |

| Market Size (2031) | USD 11.07 Billion |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

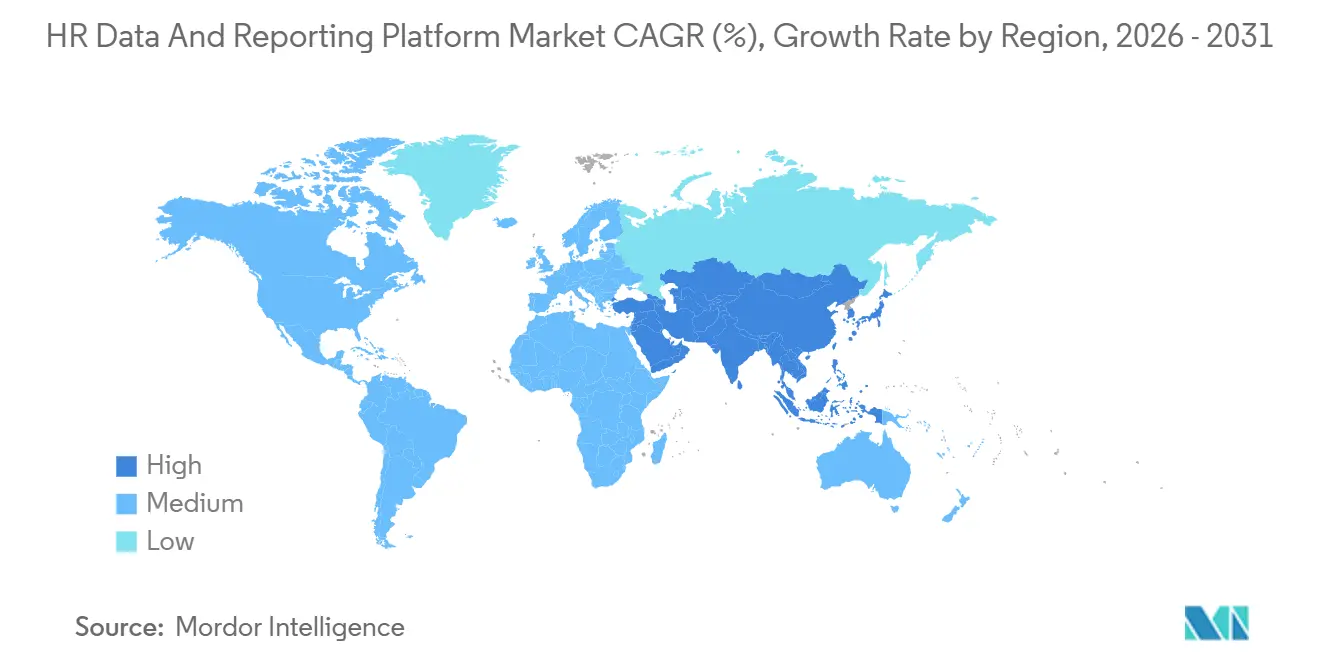

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

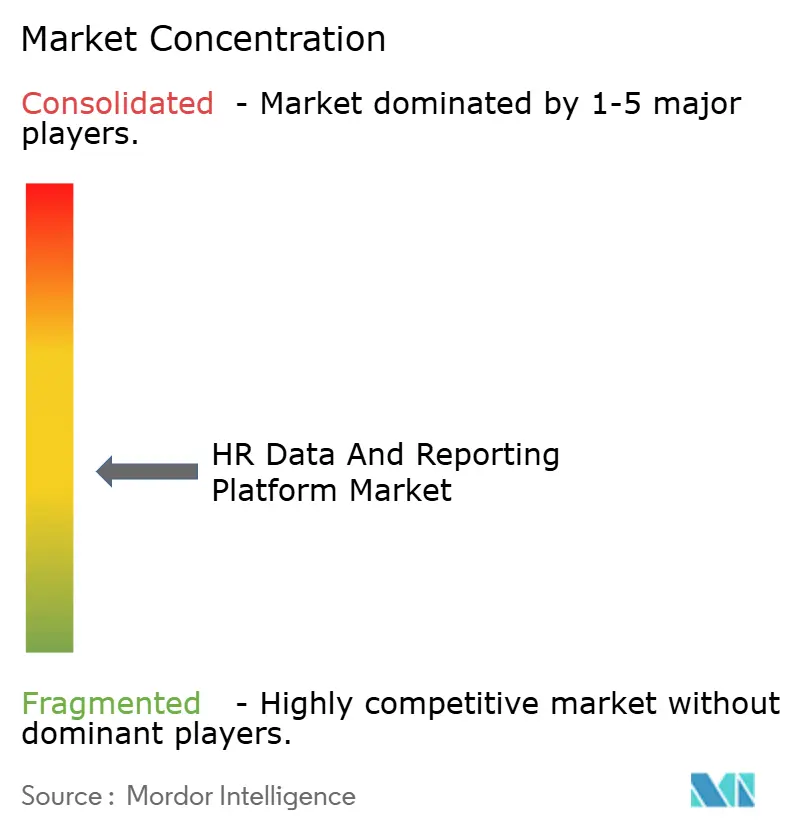

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Data And Reporting Platform Market Analysis by Mordor Intelligence

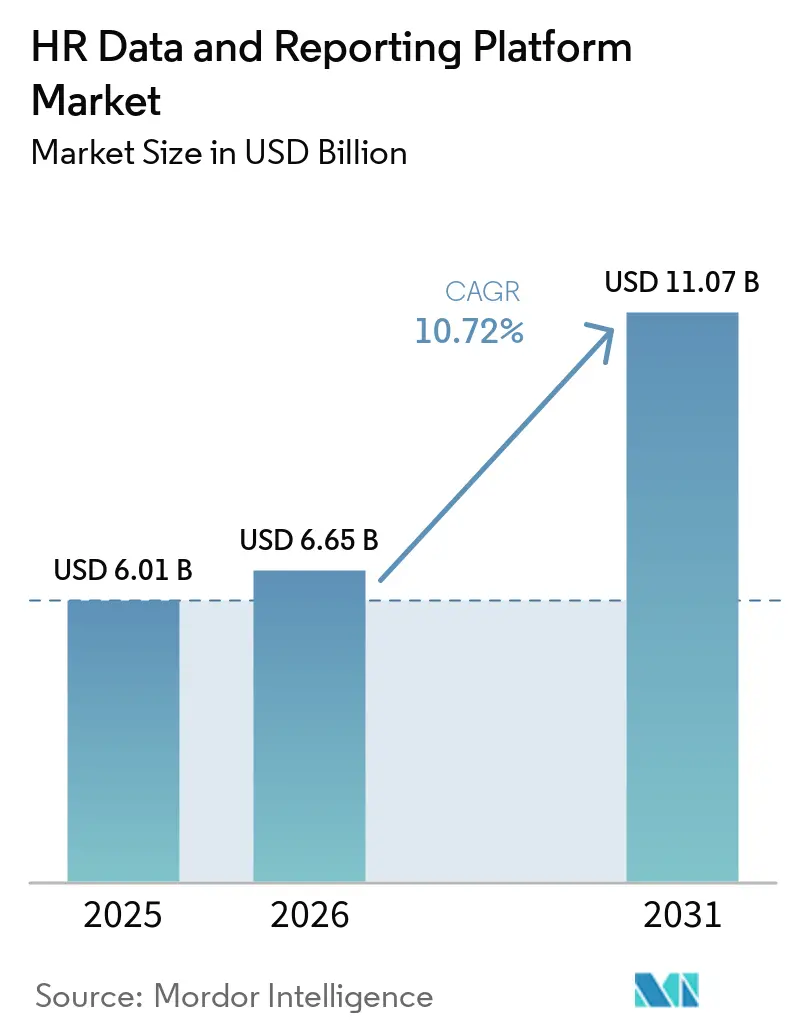

The HR data and reporting platform market size is expected to increase from USD 6.01 billion in 2025 to USD 6.65 billion in 2026 and reach USD 11.07 billion by 2031, growing at a CAGR of 10.72% over 2026-2031. Demand is being shaped by the overlap of stricter workforce disclosure requirements, broader AI use in people decisions, and greater board attention to labor data as a measurable business asset. Enterprises are moving spending toward platforms that combine reporting, governance, and forecasting into a single operating layer, because disconnected tools no longer meet the needs of finance, HR, and compliance simultaneously. Competitive pressure is also shifting toward integration quality, regulatory coverage, and the ability to place analytics directly inside daily manager workflows. Vendors that can shorten deployment time through cloud delivery, prebuilt models, and cleaner data pipelines are gaining stronger consideration across both large and mid-sized accounts. The HR data and reporting platform market is therefore growing on the back of structural demand rather than short-term software replacement alone.

Key Report Takeaways

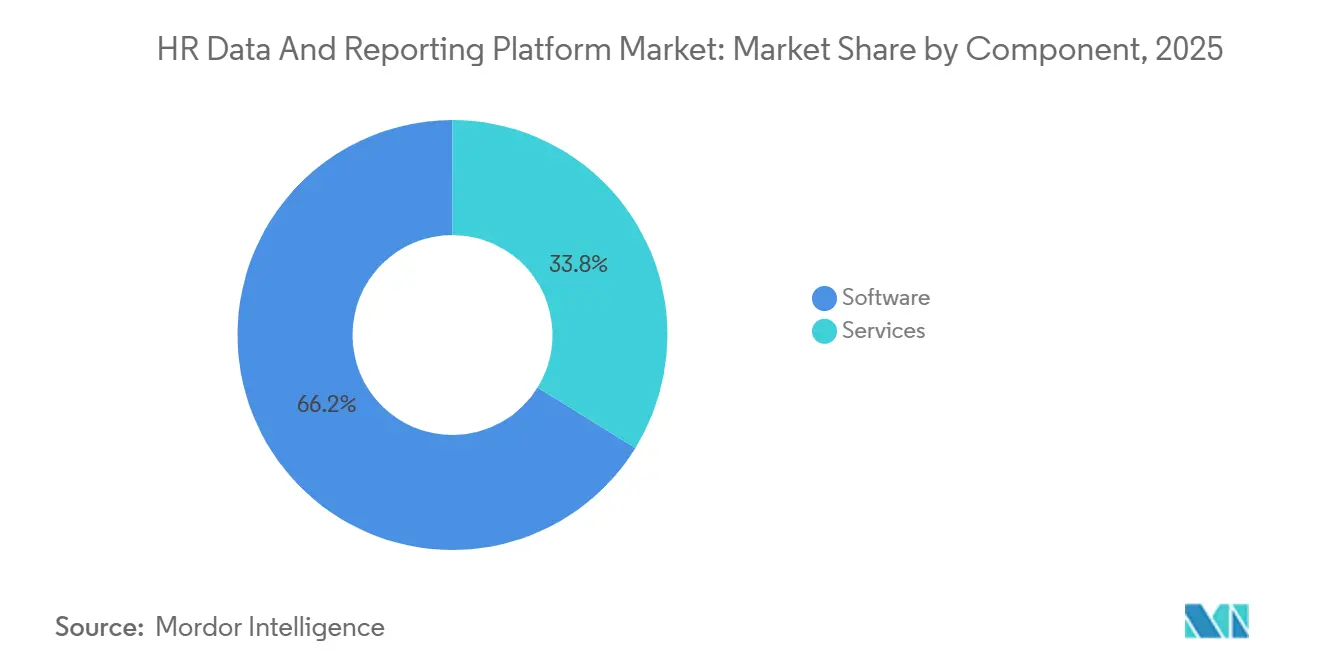

- By component, software led with 66.19% share in 2025, while services are projected to expand at a 12.75% CAGR through 2031 in the HR data and reporting platform market.

- By deployment mode, on-premises held 71.26% share in 2025, while cloud is expected to grow at a 13.01% CAGR through 2031.

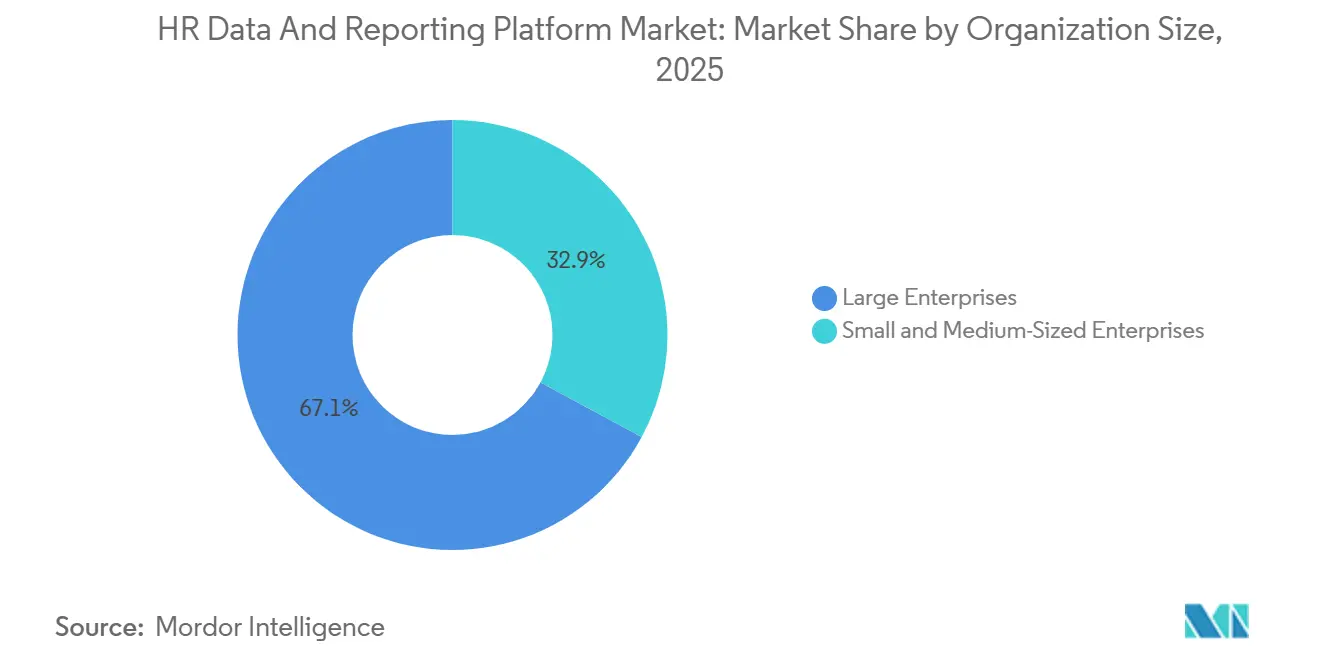

- By organization size, large enterprises accounted for 67.14% of the HR data and reporting platform market share in 2025, while SMEs are projected to record the fastest CAGR of 12.31% through 2031.

- By application, workforce analytics and dashboarding accounted for 36.32% share in 2025, while predictive analytics is projected to expand at an 11.49% CAGR through 2031.

- By end-user industry, information technology and telecommunications held 28.56% share of the HR data and reporting platform market in 2025, while healthcare and life sciences are expected to advance at an 11.12% CAGR through 2031.

- By geography, North America held 34.14% share in 2025, while Asia-Pacific is projected to grow at an 11.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Data And Reporting Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Data-Driven Workforce Planning | +2.8% | Global, with concentrated early gains in North America and Western Europe | Medium term (2-4 years) |

| Accelerating Shift Toward Cloud-Based HR Analytics | +2.3% | Global, strongest in Asia-Pacific, South America, and SME segments in North America | Short term (≤ 2 years) |

| Growing Use of AI for Attrition, Skills, and Capacity Forecasting | +2.1% | Global, with highest intensity in IT and telecommunications and healthcare and life sciences verticals | Medium term (2-4 years) |

| Increasing Focus on Retention, Engagement, and Productivity Outcomes | +1.5% | Global, with strong adoption in large enterprises across North America and Europe | Short term (≤ 2 years) |

| Pay Transparency Readiness and Job Architecture Standardization | +0.9% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Board-Level Human Capital Disclosure and Workforce Risk Reporting | +0.7% | North America and Europe, with growing presence in Middle East and Australia and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Data-Driven Workforce Planning

The HR data and reporting platform market is benefiting from a clear shift away from intuition-led headcount decisions and toward structured scenario planning. Enterprises now want labor costs, skills supply, and future capacity reviewed together, because isolated HR reports do not support board or finance decisions well enough anymore.[1]Workday, Inc., “Workday Introduces Workday Data Cloud to Unlock the Power of People This is making shared data environments and zero-copy access more important, since delayed data feeds reduce the value of planning models when organizations need faster responses. Adoption remains strongest in sectors where labor is both a major cost and a major source of competitive advantage, especially in information technology and financial services, while manufacturing is increasingly active as automation changes role design and redeployment needs. The vendor focus has therefore moved toward integrated workforce planning tools that connect people data with broader business data rather than leaving HR analytics as a stand-alone reporting layer. This pattern creates a durable demand base for the HR data and reporting platform market by treating planning as an operating capability rather than a periodic HR exercise.

Accelerating Shift Toward Cloud-Based HR Analytics

The broader shift toward cloud delivery across core HR systems is also boosting the HR data and reporting platform market. The most important change is architectural rather than cosmetic, because cloud-native analytics can now access live or near-live data without the long pipeline delays that used to slow and outdated people's reporting. Oracle has taken a similar direction in Fusion Data Intelligence, where natural language access and expanded analytical features are designed to shorten the path between a business question and a usable workforce answer. In the Asia-Pacific region, the cloud shift is accelerating because digital filing rules, growing SaaS adoption, and improved infrastructure are making hosted models easier to justify within expanding organizations. In Europe, centralized cloud controls are also attractive because vendors can build audit logs, lineage tracking, and governance tools into the platform layer rather than leaving those tasks to local IT teams. As a result, the HR data and reporting platform market is seeing cloud demand rise fastest, as buyers seek both speed and lower compliance effort from a single deployment model.

Growing Use of AI for Attrition, Skills, and Capacity Forecasting

The HR data and reporting platform market is moving beyond historical dashboarding and into predictive workflows that surface likely attrition, skill shortages, and capacity gaps earlier in the decision cycle. Peer-reviewed research showed that ensemble machine learning models can exceed 98% accuracy in attrition classification when training data is enriched and balanced, raising confidence in using predictions more directly in workforce management. At the same time, model explainability has become a practical buying criterion, because HR leaders and compliance teams want interpretable factors behind each risk score rather than opaque outputs. IBM reported that its AskHR deployment across 270,000 employees reduced HR operating costs by 40% and support tickets by 75%, demonstrating how embedded AI can transform the operating economics of service delivery at scale. Gloat has pushed the same movement on the skills side through a knowledge graph covering 2.4 million skill nodes and 18.7 million relationships, allowing enterprises to check talent supply and demand in real time. This combination of prediction, explainability, and workflow integration is making AI one of the clearest growth drivers for the HR data and reporting platform market.

Increasing Focus on Retention, Engagement, and Productivity Outcomes

The HR data and reporting platform market is also gaining from the need to reduce turnover costs and improve workforce productivity with clearer evidence. Recent academic work has placed replacement costs at 50% to 200% of annual salary, depending on role complexity, providing finance leaders with a direct cost framework for evaluating analytics spending. This has changed the language of platform buying, as employers now connect regrettable departures, bench strength, and engagement patterns to revenue pressure and execution risk rather than treating them as soft HR issues. Platform design is changing with that shift, and many vendors are linking performance, meeting patterns, compensation, and feedback data into a single interface so managers can see a fuller retention picture. In Europe, those broader models still need careful boundaries because privacy and proportionality rules limit how far individual behavioral monitoring can go in employee settings. Even with those limits, the HR data and reporting platform market continues to benefit, as retention and productivity are now managed with the same discipline that companies apply to other operating costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented HR Data Estates and Integration Complexity | -1.5% | Global, most acute in large enterprises with legacy on-premises ERP installations in Europe and North America | Medium term (2-4 years) |

| Employee Data Privacy and Cross-Border Compliance Burden | -1.2% | Europe, Asia-Pacific, and North America | Short term (≤ 2 years) |

| Works Council Scrutiny of Monitoring-Oriented Analytics Deployments | -0.8% | Europe, with spillover to pan-EU governance requirements | Medium term (2-4 years) |

| Explainability and Bias Audit Burden for High-Risk HR AI | -0.5% | Global, with strongest regulatory pressure in Europe and voluntary compliance emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented HR Data Estates and Integration Complexity

The HR data and reporting platform market still faces a fundamental architecture problem because workforce data is often spread across recruiting, payroll, learning, benefits, and time systems that were never built to work as a single record. Different schemas, refresh cycles, permissions, and ownership rules make it difficult to create a trusted employee view, even before analytics work begins. This is why buyers now look closely at native connectors, data normalization, and lineage controls when comparing vendors, rather than judging products solely on dashboard quality. When integration work expands, or data quality remains weak, decision-makers lose confidence in the platform, and the time to measurable value exceeds the plan. In Europe, this issue is even harder because data transfers and system connections must meet both legal requirements and technical compatibility, especially following court scrutiny of employee data processing arrangements. The result is that the HR data and reporting platform market keeps growing, but implementation cycles remain longer, and service demand stays elevated because integration work remains central to success.

Employee Data Privacy and Cross-Border Compliance Burden

Privacy and cross-border compliance are acting as a real brake on the HR data and reporting platform market, especially for multinational employers with shared data models across many countries. A European court ruling in late 2024 clarified that works agreements cannot override GDPR limits on employee data processing, removing an argument some employers had used to support broader handling practices. The EU AI Act is adding another layer by requiring stronger oversight, logging, and risk management for employment-related AI systems, even though key high-risk rules have been deferred to 2027. In China, PIPL-related localization obligations continue to favor vendors that can offer dedicated hosting and region-aware compliance design, which is one reason local providers are strengthening their position. In the United States, pay data reporting rules are also becoming more detailed, requiring analytics platforms to be frequently reconfigured for classifications, submission logic, and audit trails. These requirements do not stop adoption, but they do raise deployment cost and lengthen buying decisions across the HR data and reporting platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Emerging as the Value-Capture Layer

Software held 66.19% of the HR data and reporting platform market share in 2025, while services are forecast to expand at a 12.75% CAGR through 2031. The software segment remained the largest because recurring SaaS licenses and embedded analytics modules continue to be the primary commercial base for both pure-play vendors and large HCM suite providers. Buyers continue to start with software because they need a stable reporting engine, governed data structures, and a common interface for workforce dashboards before they can scale more advanced use cases. Standard dashboarding has also become easier to replicate across vendors, which means software leadership now depends less on basic visualization and more on data depth, governance controls, and integration quality. This keeps the software layer central to the HR data and reporting platform market, even as the value conversation broadens beyond license revenue.

Services are growing faster because platform value depends more heavily on integration, model governance, change management, and adoption support than it did in earlier reporting deployments. This is especially true when enterprises add AI features, because explainability, workflow redesign, and policy alignment require more hands-on configuration than a simple reporting rollout. Mid-sized organizations are also leaning toward managed analytics offerings because they often lack in-house data engineering and workforce science skills, even when they want predictive insights. SAP highlighted this shift in its 2H 2025 release, positioning People Intelligence on SAP Business Data Cloud as a separately licensed analytics layer with prebuilt use cases across compensation, skills, succession, and learning.[2]SAP SE, “Leading HR with Confidence, Unlocking AI, Skills, and People Insights in the SAP SuccessFactors 2H 2025 Release,” SAP News Center, news.sap.com The HR data and reporting platform market is therefore seeing more value captured through recurring advisory, implementation, and managed intelligence work, rather than solely through software subscriptions.

By Application: Predictive Analytics Reshaping the Value Proposition

Workforce analytics and dashboarding accounted for a 36.32% share of the HR data and reporting platform market size in 2025, while predictive analytics is projected to expand at an 11.49% CAGR through 2031. Dashboarding remained the largest application because it remains the first step for most buyers seeking common reporting on headcount, turnover, diversity, compensation, and leadership metrics. It also aligns naturally with executive reporting, disclosure support, and self-service manager queries, making adoption easier across organizations with varying analytical maturity. Many enterprises still need clean descriptive reporting before they can trust more advanced forecasting or automated recommendations, so dashboarding continues to anchor early deployments. For that reason, the HR data and reporting platform market continues to treat workforce analytics and dashboarding as the entry point for broader adoption rather than a fading legacy function.

Predictive analytics is growing faster as employers increasingly seek forward-looking insights into attrition risk, skills shortages, hiring bottlenecks, and labor capacity. Research published in 2026 showed that advanced ensemble models can achieve very high precision in employee attrition classification when data quality and balance improve, supporting broader production use in HR settings. The same movement is expanding compliance reporting, since the EU Pay Transparency Directive requires employers to prepare more structured pay gap reporting by work category and maintain stronger reporting discipline. Real-time workforce monitoring is also advancing, but more carefully, because GDPR proportionality and consultation rules in several European countries continue to limit person-level monitoring practices. Across these use cases, the HR data and reporting platform market is shifting from periodic historical reporting toward continuous analysis that sits closer to daily operating decisions.

By Deployment Mode: Cloud Momentum Outpacing On-Premises Share

On-premises deployment held 71.26% share in 2025, while cloud deployment is expected to grow at a 13.01% CAGR through 2031 in the HR data and reporting platform market. On-premises remained dominant because large enterprises still run legacy ERP-centric environments, and many prefer direct control over security, certifications, and sensitive employee records. This was particularly visible in Europe, where data residency concerns and GDPR sensitivity kept self-managed or tightly controlled architectures in place across established enterprises. On-premises systems also stayed relevant where analytics had to fit into long-standing internal integration patterns that could not be replaced quickly without operational disruption. That legacy base explains why the HR data and reporting platform market still carried a strong on-premises share in 2025, even as newer demand moved elsewhere.

Cloud is growing faster because it fits the need for shorter deployments, easier upgrades, and broader access to AI features without local infrastructure rebuilds. Zero-copy or low-friction data architectures are reducing the latency between transactions and analysis, making cloud analytics more useful for real-time workforce decisions than older batch-oriented models. Compliance pressure is also helping the cloud case, because providers can build audit logs, lineage, and governance controls into the platform layer more efficiently than many enterprises can do on their own. ChartHop’s 2025 platform internationalization, with added French, German, and Spanish support plus AI-powered translation for custom fields, shows how cloud-native products are lowering localization barriers for multinational use. The HR data and reporting platform market is therefore likely to see hybrid models expand, especially in Asia-Pacific, where organizations want cloud analytics with localized data control.

By Organization Size: SME Adoption Unlocking The Next Growth Tier

Large enterprises held a 67.14% share in 2025, reflecting that organizations led the HR data and reporting platform market with the deepest integration needs and the strongest reporting pressures. These employers manage multi-country workforces, larger compliance exposure, and more complex data relationships across payroll, finance, talent, and operations. They also have stronger budgets for specialized analytics teams, advisory support, and long transformation programs, which makes adoption easier at scale. Board-level scrutiny of labor productivity, workforce risk, and disclosure quality has also been much stronger in this group, reinforcing the need for dedicated platforms. As a result, large enterprises remained the main revenue base for the HR data and reporting platform market in 2025.

SMEs are growing faster, at a 12.31% CAGR, because vendors are removing many of the entry barriers that previously kept advanced analytics out of the mid-market. Pre-configured templates, tiered pricing, bundled support, and embedded AI are helping smaller employers adopt forecasting and reporting functions without building full internal analytics teams. This change matters because many mid-sized organizations now face the same retention pressure, pay transparency preparation, and skills visibility needs as larger companies, even if their budgets are lower. Vendors such as Leapsome and other newer platforms have helped normalize predictive and engagement tools for smaller workforces by packaging them in easier operating models. The HR data and reporting platform market is therefore opening a new growth tier in which analytical sophistication no longer depends solely on enterprise scale.

By End-User Industry: Healthcare Overtaking Technology Sector Growth Rate

Information technology and telecommunications accounted for 28.56% of the market in 2025, underscoring the strong link between the HR data and reporting platform market and talent-intensive sectors with high salary exposure and constant skills competition. This vertical has long invested in people analytics because labor is a core driver of both operating cost and product delivery capacity. High turnover risk, rapid skill obsolescence, and the need for workforce planning to align with project demand make analytics a routine management tool in this segment. IT and telecommunications buyers also tend to adopt cloud and AI capabilities earlier, further reinforcing their role as lead users of advanced platform functions. That combination kept this vertical in the top position during 2025.

Healthcare and life sciences are the fastest-growing verticals, with a 11.12% CAGR through 2031, because staffing complexity is rising faster than generic HR tools can handle. Credential tracking, shift optimization, compliance with role-specific regulations, and workforce safety requirements create structured data needs that favor specialized analytical models. BFSI remains important as well because auditability, access control, and model governance are essential in regulated environments, which makes vendor trust and documentation a major buying factor. Manufacturing is also becoming more active as automation changes role structures and raises demand for skills mapping, redeployment analysis, and labor cost scenario planning. Oracle’s Fusion HCM Analytics 26R1 release, including a workforce scheduling module for early adopters in January 2026, reflects how vendors are tailoring product design to these operationally complex verticals.

Geography Analysis

North America accounted for a 34.14% share of the HR data and reporting platform market size in 2025, making it the largest regional market. The region led because people analytics adoption was already mature, turnover costs remained high, and employers had been operating under disclosure and pay reporting expectations for longer than most other markets. In the United States, the disclosure environment changed in 2025 when anticipated prescriptive SEC human capital rules were removed from the near-term agenda, and S&P 100 companies narrowed the scope of DEI wording in Form 10-K filings. That shift is moving demand toward productivity, skills, and compensation analytics rather than pushing another round of diversity-reporting expansion. Canada remains an important secondary market due to local analytics talent and pay equity requirements, while Mexico is gaining relevance as nearshoring increases the need for cross-border workforce planning.

Europe remains one of the most regulation-driven regions in the HR data and reporting platform market, and buying decisions there are heavily shaped by compliance deadlines. The EU Pay Transparency Directive, with a June 7, 2026, transposition deadline, is forcing employers to build stronger job architecture, pay gap reporting, and salary range disclosure processes into their HR data workflows.[3]Altays SIRH, “Transparence Des Salaires, Ce Que Les DRH Doivent Anticiper,” Altays, altays.com Works council involvement adds another layer in countries such as Germany, France, the Netherlands, and Belgium, where consultation on high-risk HR AI can extend procurement and deployment timelines. The United Kingdom, Germany, and France continue to account for most regional demand, while sanctions and geopolitical limits keep Russia far more dependent on domestic solutions.

Asia-Pacific is projected to grow at an 11.88% CAGR through 2031, making it the fastest-growing region in the HR data and reporting platform market. Growth is being supported by a broad workforce scale, rising cloud infrastructure, and a stronger domestic vendor base that can respond to local language, compliance, and pricing needs. China is central to that story, and Yonyou’s May 2026 launch of an AI-driven global HCM solution for Chinese enterprises expanding abroad shows how local vendors are moving beyond domestic reporting into multinational capability. India and Southeast Asia are driving steady demand for mobile-first and multilingual platforms, while Japan’s aging workforce is strengthening the case for succession and skills-continuity analytics. Australia and New Zealand remain smaller in scale but advanced in compliance-oriented deployment, while the Middle East and South America are growing from lower bases as workforce nationalization programs, labor compliance needs, and formal digital reporting requirements become more important.

Competitive Landscape

The HR data and reporting platform market has a layered structure with large HCM suite providers on one side and focused analytics specialists on the other. Workday, SAP SuccessFactors, and Oracle compete through broad workforce management suites that include analytics as part of a larger platform relationship, while vendors such as Visier, Nakisa, Orgvue, ChartHop, Gloat, Eightfold AI, and Syndio compete more directly on analytical depth, workforce design logic, and targeted AI capabilities. This creates a market where the broader suite layer carries meaningful concentration, but the specialist layer remains fragmented enough for partnerships and category shifts to change positioning quickly. Buyers usually separate vendors less by dashboard design now and more by integration quality, compliance readiness, AI explainability, and how well insights can be placed into daily workflows. That balance keeps the HR data and reporting platform market moderately fragmented rather than tightly consolidated.

A major strategic move in this market has been the push to place governed people data within wider enterprise AI environments rather than keeping analytics in isolated portals. Visier moved in that direction with its MCP server launch in November 2025, allowing governed workforce data to feed enterprise AI agents across broader software environments. Gloat made a similar move with its March 2026 Agentic HR Platform, which sits above systems such as Workday, SAP SuccessFactors, and Oracle HCM as a reasoning layer for redeployment, career development, and succession use cases. Eightfold AI extended the same competitive logic in May 2026 through TalentForge, which allows enterprises to build custom HR applications on its talent intelligence platform rather than buying fixed modules alone.

Specialists are also creating narrower categories with strong commercial appeal, which helps them avoid direct price competition with the largest suite vendors. Syndio’s May 2026 launch of a decision intelligence category for pay is a clear example, as it reframed pay governance as an ongoing operational discipline rather than a compliance tool. Nakisa has pursued a related path by combining natural language and voice access with predictive what-if simulations across HR, finance, and real estate, broadening its relevance beyond classic HR reporting.[4]Nakisa, “Nakisa Launches Enterprise Agentic Decision Intelligence Platform,” Nakisa, nakisa.com At the same time, incumbent vendors continue to defend their position by expanding data access and AI tooling, as seen in Workday Data Cloud and Oracle’s Fusion Data Intelligence enhancements. The clearest white space remains in mid-market accounts and in verticals such as healthcare scheduling, manufacturing skills redeployment, and public sector compliance reporting, where templates and domain-specific data models still offer defensible differentiation. For that reason, the HR data and reporting platform market is likely to remain active in alliances, ecosystem expansion, and selective category creation rather than moving quickly toward winner-take-all concentration.

HR Data And Reporting Platform Industry Leaders

Visier, Inc.

Lattice HQ, Inc.

Gloat Ltd.

Eightfold AI Inc.

Fuel50 Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Syndio launched "Decision Intelligence for Pay" as a new market category, introducing its Decisions AI product that provides real-time pay governance across the employee lifecycle. The company's research indicates ungoverned pay decisions cost enterprises with 60,000 employees USD 31 million to USD 62 million annually. Syndio was simultaneously named a Workday Design Approved partner and expanded alliances with Kognitiv, Strada, and Mercer, processing over 10 million pay decisions on its platform.

- May 2026: Eightfold AI introduced TalentForge, a platform that enables enterprises to build custom-fit HR applications powered by Eightfold's talent intelligence, trained on 1.6 billion career trajectories and 1.6 million skills. TalentForge inherits enterprise security architecture, including SOC 2, ISO 27001, and ISO 42001 certifications, and allows organizations to build production HRIS-level systems in weeks.

- May 2026: IBM Consulting launched Context Studio and previewed Process Studio at Think 2026, enabling enterprises to ground AI agents in organizational data. A joint IBM-Providence Healthcare deployment using IBM watsonx Orchestrate reduced manager time on hiring steps by 90%, improved job request accuracy by 70%, and cut internal transfer time by 12 days.

- May 2026: Yonyou launched its BIP Global HCM solution, targeting Chinese enterprises expanding internationally. The platform generates country-specific compliance reports within 10 minutes via AI agents, supports payroll across 40+ countries, and complies with GDPR and China's PIPL through a Singapore-based data center and zero-trust architecture.

Global HR Data And Reporting Platform Market Report Scope

The HR Data and Reporting Platform Market encompasses data-centric platforms that are revolutionizing the HR landscape by aggregating, processing, and analyzing workforce data from diverse sources. These platforms not only generate actionable insights but also offer reporting, visualization, and predictive analytics capabilities. Acting as an intelligence layer across HR systems, they facilitate data-driven planning, compliance reporting, and performance tracking. Emphasis in this market lies in transforming raw HR data into structured insights, catering to both operational and strategic needs.

The HR Data and Reporting Platform Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, Managed Services / Analytics-as-a-Service, and Advisory and Consulting Services]), Application (Workforce Analytics and Dashboarding, HR Performance and KPI Reporting, Predictive Analytics, Compliance and Regulatory Reporting, Real-time Workforce Monitoring, and Other Applications), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Information Technology and Telecommunications, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Manufacturing, Retail and Consumer Goods, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Managed Services / Analytics-as-a-Service | |

| Advisory and Consulting Services |

| Workforce Analytics and Dashboarding |

| HR Performance and KPI Reporting |

| Predictive Analytics |

| Compliance and Regulatory Reporting |

| Real-time Workforce Monitoring |

| Other Applications |

| Cloud |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Information Technology and Telecommunications |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and Consumer Goods |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Managed Services / Analytics-as-a-Service | ||

| Advisory and Consulting Services | ||

| By Application | Workforce Analytics and Dashboarding | |

| HR Performance and KPI Reporting | ||

| Predictive Analytics | ||

| Compliance and Regulatory Reporting | ||

| Real-time Workforce Monitoring | ||

| Other Applications | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Information Technology and Telecommunications | |

| Banking, Financial Services, and Insurance | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Retail and Consumer Goods | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the HR data and reporting platform market in 2026?

The HR data and reporting platform market stands at USD 6.65 billion in 2026 and is forecast to reach USD 11.07 billion by 2031 at a CAGR of 10.72%.

Which region leads current demand for HR data and reporting platforms?

North America leads with 34.14% share in 2025, supported by mature people analytics use, high turnover costs, and established disclosure and pay reporting requirements.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region with an 11.88% CAGR, driven by cloud adoption, workforce scale, and a stronger domestic HR technology ecosystem.

Which application is expanding most quickly?

Predictive analytics is the fastest-growing application at an 11.49% CAGR, as employers move from historical reporting toward attrition, skills, and capacity forecasting.

Why are services growing faster than software?

Services is projected to expand at a 12.75% CAGR because integration, change management, model governance, and managed analytics support are becoming more important as AI deployments rise.

Which buyer group is opening the next growth tier?

SMEs are growing at a 12.31% CAGR as vendors offer tiered pricing, pre-configured deployments, and embedded AI that reduce the need for large internal analytics teams.

Page last updated on: