Core HR Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

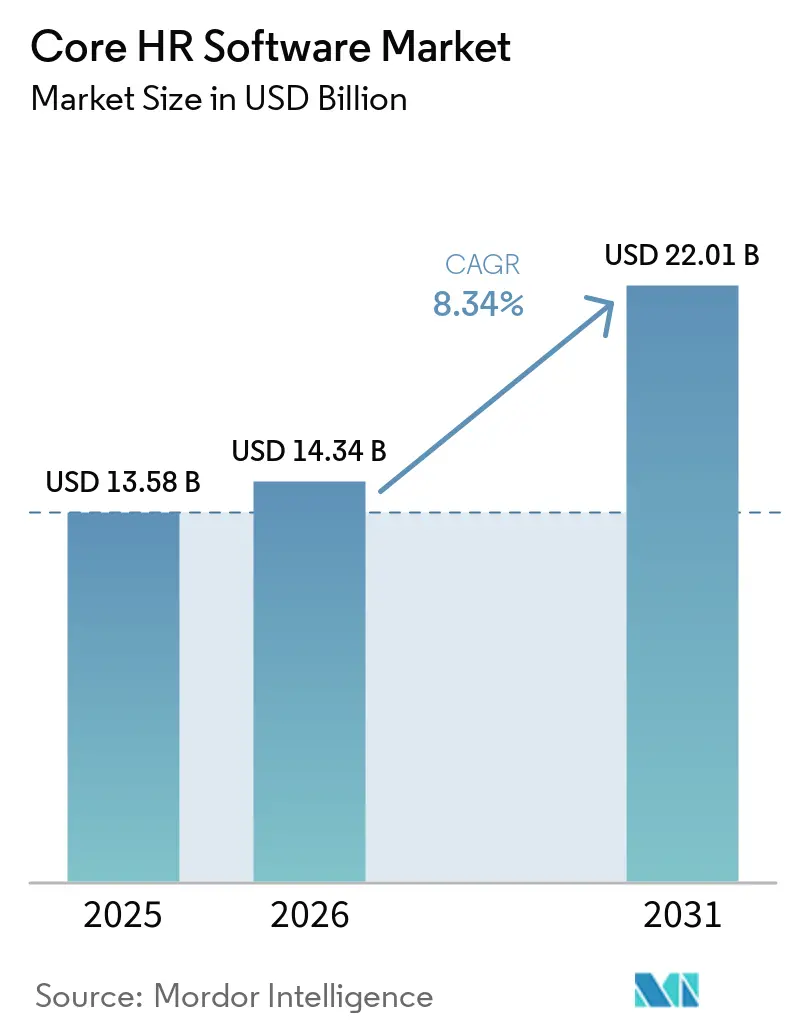

| Market Size (2026) | USD 14.34 Billion |

| Market Size (2031) | USD 22.01 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Core HR Software Market Analysis by Mordor Intelligence

The core HR software market size reached USD 13.58 billion in 2025 and is expected to reach USD 14.74 billion in 2026, growing to USD 22.01 billion by 2031, at a CAGR of 8.34% from 2026 to 2031. Rising investment in cloud-native human capital management platforms, the rapid infusion of generative AI into talent workflows, and stricter multi-jurisdictional reporting rules combined to lift spending in 2025. Vendors embedded agentic AI that writes job descriptions, flags pay equity gaps, and recommends learning pathways, raising the perceived return on new deployments. At the same time, data-sovereignty mandates pushed many multinational buyers toward hybrid architectures that keep sensitive payroll data local while permitting SaaS innovation elsewhere. Private-equity ownership of legacy providers, coupled with well-funded disruptors, has compressed innovation cycles, giving buyers more choice but increasing integration complexity.

Key Report Takeaways

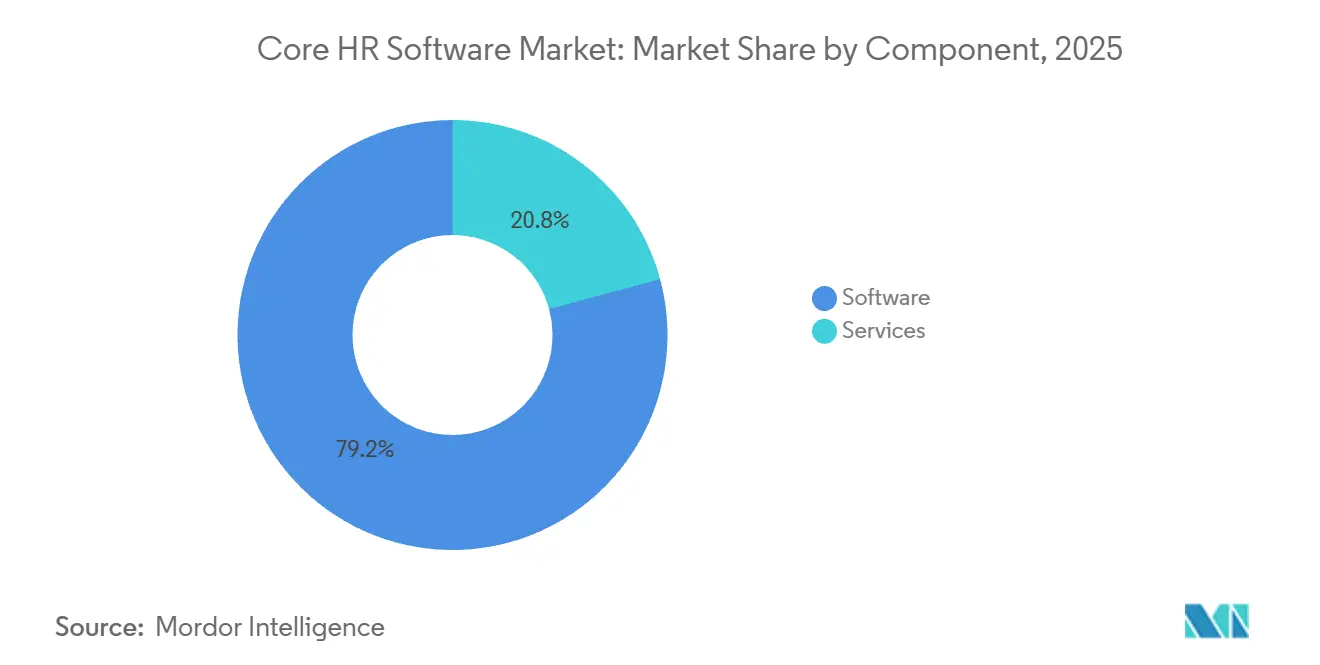

- By component, the software segment held 79.18% of revenue of the core HR software market in 2025, while services are forecast to expand at an 8.87% CAGR through 2031.

- By deployment, cloud models dominated with 72.46% share in 2025, whereas hybrid architectures represent the fastest trajectory at a 9.28% CAGR to 2031.

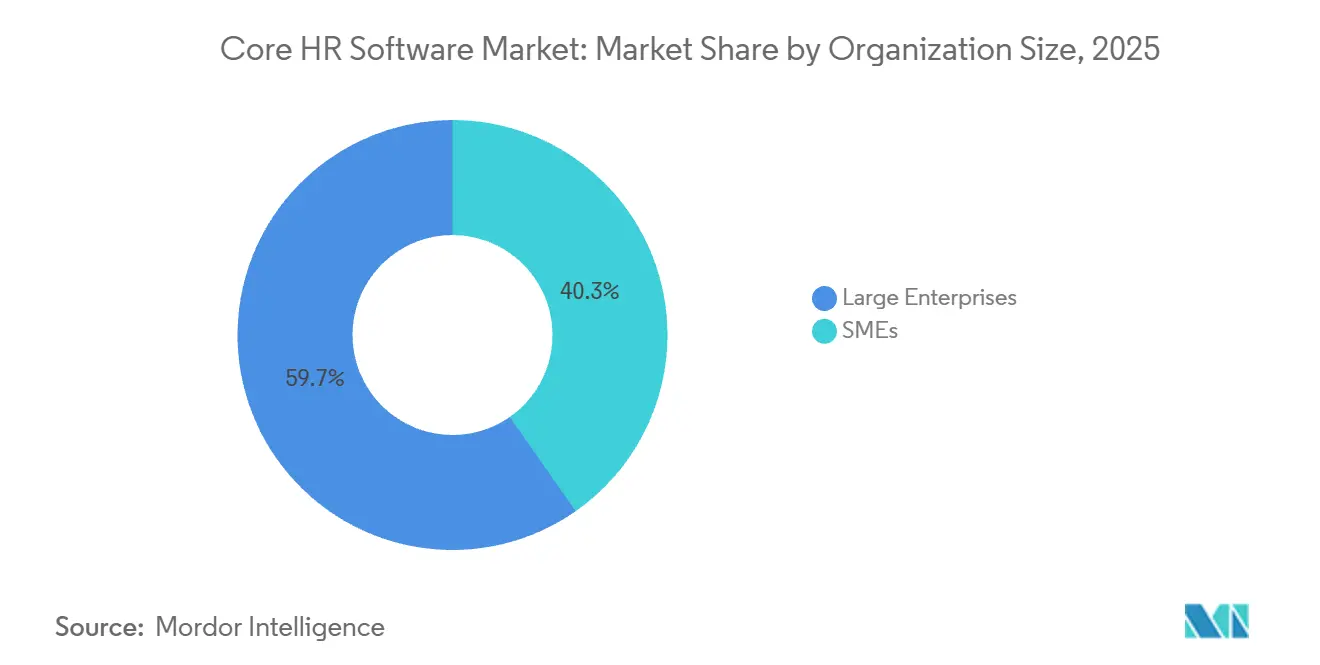

- By organization size, large enterprises commanded 59.72% of spending in 2025, yet small and medium-sized enterprises are projected to grow at a 9.41% CAGR during the forecast window.

- By industry vertical, IT and telecom accounted for 20.14% of 2025 revenue of the core HR software market, while healthcare and life sciences is set to advance at a 9.12% CAGR through 2031.

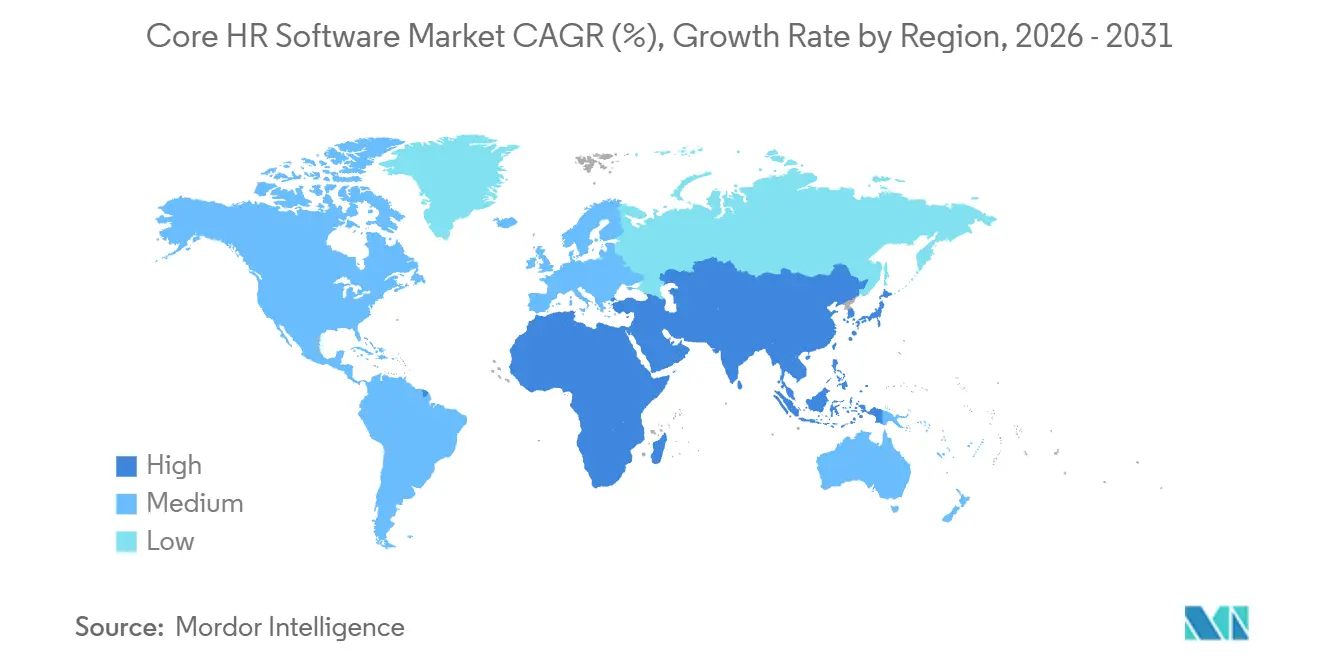

- By geography, North America contributed 38.96% of global revenue in 2025, whereas Asia-Pacific is expected to post a 10.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Core HR Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Adoption of HR Suites | +2.1% | Global, with North America and Europe leading, Asia-Pacific accelerating | Medium term (2-4 years) |

| AI-Driven Talent Analytics Integration | +1.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expansion of Remote and Hybrid Work Models | +1.3% | Global, particularly North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift to Skills-Based Workforce Planning | +1.1% | North America, Europe, early uptake in Asia-Pacific IT hubs | Long term (≥ 4 years) |

| Increasing Regulatory Reporting Complexity | +0.9% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Rising Mid-Market Demand in Emerging Economies | +1.0% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Adoption of HR Suites

Organizations continue to retire on-premises systems as quarterly SaaS releases deliver innovations that cannot be replicated behind the firewall. Vendor roadmaps increasingly couple cloud delivery with agentic AI, letting customers experiment with predictive attrition, automated compliance checks, and conversational self-service at minimal incremental cost. Multinational firms also lean on hyperscaler data centers to handle complex tax engines across dozens of jurisdictions. However, extracting and cleansing decades of payroll history before migration remains labor-intensive, reinforcing demand for implementation services.

AI-Driven Talent Analytics Integration

Large enterprises piloted AI-infused talent tools at scale in 2025, and corporate budgets for HR-focused AI climbed to a median of USD 1.6 million in 2026. Recent releases such as Workday’s Talent Optimization and SAP’s SuccessFactors agentic workflows move beyond descriptive dashboards, recommending promotions, surfacing succession risks, and drafting performance narratives automatically. Adoption is rapid in highly regulated sectors looking for audit trails, yet many mid-market firms still lack formal governance policies, slowing full deployment.

Expansion of Remote and Hybrid Work Models

With more than 70% of knowledge workers operating outside a single office in 2025, buyers now insist on mobile-first time tracking, geofenced payroll engines, and behavioral analytics that gauge engagement asynchronously. UKG partnered with Google Cloud to embed Gemini-based forecasting that balances employee preferences with labor plans, underscoring the premium placed on real-time insights for distributed teams.[1]UKG Newsroom, “UKG and Google Cloud Announce Strategic Partnership,” ukg.com The shift amplifies cross-border payroll complexity and spotlights privacy obligations when employee data moves between regions.

Shift to Skills-Based Workforce Planning

Enterprises, especially in technology and professional services, are dismantling title-based hierarchies in favor of skills taxonomies. AI inference engines automatically tag competencies from project repositories, external certificates, and peer endorsements, paving the way for internal talent marketplaces. Vendors able to bundle pre-built libraries and bias-detection tooling stand to benefit as firms tie compensation and advancement to verified capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Sovereignty Concerns | -1.2% | Europe, China, India, Russia, Middle East | Medium term (2-4 years) |

| High Switching Costs From Legacy Suites | -0.9% | Global, pronounced in North America and Europe | Long term (≥ 4 years) |

| Shortage of HR Tech Implementation Talent | -0.6% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Persistent Cybersecurity and Privacy Breaches | -0.8% | Global, heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Residency and Sovereignty Concerns

Rules such as the GDPR in the European Union, the Personal Information Protection Law in China, and India’s Digital Personal Data Protection Act mandate that certain employee attributes remain inside national borders. Vendors are therefore forced to maintain region-specific instances, which delays feature parity outside the United States and raises infrastructure costs. Buyers in defense, banking, and healthcare demand proof of local hosting, turning data residency into a primary evaluation criterion.[2]International Association of Privacy Professionals, “GDPR and Data Localization: A Global Map,” iapp.org

High Switching Costs From Legacy Suites

Deep customizations, intertwined finance links, and decades of historical payroll files make rip-and-replace strategies risky and expensive. Even the United States federal HR 2.0 program, which aims to converge more than 100 systems into a single hybrid HCM stack for two million employees, is budgeted as a multi-year endeavor that will run beyond fiscal 2028.[3]U.S. Office of Personnel Management, “Federal HR 2.0 Initiative,” opm.gov As a result, many enterprises layer modern talent modules on top of aging core HR records, slowing the flow of unified analytics and dampening short-term upgrade demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

The software segment captured 79.18% of the core HR software market share in 2025, thanks to large recurring subscriptions for payroll, benefits, and workforce analytics modules. Growth momentum is now tilting toward services because data migration, multi-country tax configuration, and AI governance demand specialized expertise. Managed payroll outsourcing, tier-1 help-desk support, and continuous optimization contracts are therefore widening the revenue base for systems integrators and vendor professional services teams.

The core HR software market size attributed to services is forecast to climb at an 8.87% CAGR between 2026 and 2031 as AI agents automate low-value tasks, freeing consultants to advise on skills frameworks and change management. SAP’s SmartRecruiters integration, which auto-maps legacy recruiting workflows into SuccessFactors, already trims professional services hours by about 30%, demonstrating how automation can shift billable effort from configuration to strategy.[4]SAP News, “SAP SuccessFactors SmartRecruiters Integration,” sap.com

By Deployment: Hybrid Architectures Bridge Sovereignty and Agility

Cloud installations represented 72.46% of spending in 2025, reflecting strong buyer confidence in vendor-managed security, rapid feature delivery, and lower upfront capital expenditure compared to traditional on-premises deployments. Organizations are increasingly favoring cloud-based core HR systems due to their scalability, automatic updates, and ability to support distributed workforces, while also reducing the burden on internal IT teams for infrastructure maintenance and system upgrades. Yet the hybrid model is on track for a 9.28% CAGR through 2031, the fastest within deployment types, because it allows sensitive payroll data to stay on-premises while newer talent modules run in SaaS.

Maintaining real-time data synchronization across two environments is technically demanding and often requires middleware orchestration. UKG’s early-2026 acquisition of Inova Payroll provides a hybrid-ready engine capable of operating inside air-gapped networks, a move aimed at regulated agencies that must balance sovereignty with modernization. Success will hinge on robust API governance, latency management, and clear division of security responsibilities between vendor and customer.

By Organization Size: SMEs Drive Growth as Vendors Unbundle

Large enterprises accounted for 59.72% of 2025 revenue due to complex multi-currency payroll, intricate benefits schemes, and expansive compliance obligations. This dominance is further supported by their need to manage large, geographically dispersed workforces and to adhere to diverse regulatory frameworks, which increases reliance on robust, scalable core HR systems. Their higher budgets and long-term vendor relationships also contribute to sustained spending on comprehensive HR platforms that integrate payroll, compliance, and workforce analytics.

Still, the small and medium-sized segment will outpace the overall core HR software market at a 9.41% CAGR to 2031 as vendors roll out consumption-based pricing and guided implementations that remove the need for large HR teams. This growth is driven by increasing digitization among SMEs, rising awareness of the benefits of HR automation, and the availability of modular solutions that lower entry barriers. Vendors are also simplifying onboarding and reducing implementation timelines, making it easier for smaller organizations to transition from manual or semi-digital systems to fully integrated HR platforms.

By Industry Vertical: Healthcare Leads Growth Amid Staffing Crisis

IT and telecom commanded the largest slice of spending at 20.14% in 2025, supported by high turnover, skills-based project staffing, and early AI adoption. In contrast, healthcare and life sciences are expected to post a 9.12% CAGR through 2031, the strongest across verticals, as providers confront nurse shortages, escalating credential verification, and overtime compliance obligations. This growth is further supported by the increasing digitization of workforce management and stricter regulatory requirements across healthcare systems. Additionally, the need for real-time staffing visibility and compliance tracking is accelerating the adoption of advanced core HR platforms in this sector.

The core HR software market size allocated to healthcare is climbing as organizations automate nurse scheduling, integrate with learning management for continuing education credits, and enforce complex labor ratios in real time. FinThrive’s 2025 survey found that more than half of healthcare finance leaders plan new AI investments by 2026 to reduce administrative costs per encounter. Vendors offering out-of-the-box clinical credential modules and secure mobile shift bidding stand to capture this upswing.

Geography Analysis

North America retained 38.96% of global revenue in 2025, benefiting from established consulting ecosystems, a concentration of large enterprise buyers, and relatively permissive data-transfer rules. Public-sector modernization remains a notable opportunity as the federal HR 2.0 initiative rolls out a hybrid core HCM to agencies such as the Department of Agriculture beginning in fiscal 2026, OPM.GOV. Growth is easing, however, because most Fortune 1000 organizations already run cloud or hybrid suites and are redirecting budgets toward skills marketplaces, employee experience layers, and analytics add-ons.

Asia-Pacific is forecast to register a 10.11% CAGR through 2031, outstripping every other region. Demand is strongest among mid-market firms in India, China, and Southeast Asia that are digitizing payroll for the first time, encouraged by government efforts to formalize employment contracts and improve tax compliance. Darwinbox raised USD 140 million in March 2025 to fund expansion beyond India, signaling investor belief in a sustained regional growth runway. Local data-protection laws in China and India favor domestic or regionally hosted platforms, giving vendors that maintain localized infrastructure a competitive edge.

Europe, South America, the Middle East and Africa collectively offer steady but fragmented demand patterns. GDPR-driven residency rules nudge multinational buyers toward hybrid or EU-specific cloud instances. Brazil leads South America on adoption because of its intricate e-social labor reporting, while Gulf Cooperation Council states mandate Wage Protection System payroll files, spurring specialized regional vendors. African markets are still nascent but exhibit high mobile use and interest in cloud payroll that leapfrogs on-premises deployments.

Competitive Landscape

Five vendors, Workday, Oracle, SAP, ADP, and UKG, holds major share, giving the sector a moderate concentration. These incumbents leverage comprehensive module suites, deep compliance libraries, and multi-decade customer relationships to defend share, layering agentic AI across recruiting, performance, and workforce planning to lock in renewals. Thoma Bravo’s USD 12.3 billion take-private of Ceridian in November 2025 exemplifies the private-equity thesis that operational control and bolt-on acquisitions can accelerate cross-module integration.

Disruptors are closing functional gaps by collapsing HR, finance, and IT workflows in a single tenancy. Rippling secured USD 450 million in fresh capital at a USD 16.8 billion valuation in May 2025 and now serves more than 20,000 customers, underscoring the appetite for unified platforms that simplify administration. Regional challengers such as Darwinbox capitalize on localized data hosting and language packs to edge global providers across Asia-Pacific.

Technology roadmaps emphasize explainable AI, secure integration fabric, and vertical depth. UKG added Inova Payroll early in 2026 to enhance air-gapped deployment options, while SAP continues to fold SmartRecruiters into SuccessFactors to deliver end-to-end talent acquisition. Vendors providing bias detection, SOC 2 Type II compliance, and auditable decision logs are emerging as preferred partners for risk-averse buyers in banking and healthcare.

Core HR Software Industry Leaders

Workday Inc.

Oracle Corporation

SAP SE

Automatic Data Processing Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SAP released the first-half 2026 SuccessFactors update that auto-drafts performance reviews, suggests learning paths and flags pay equity gaps, with Workforce Scheduling for manufacturing slated for the second half of the year.

- March 2026: SAP completed the integration of SmartRecruiters into SuccessFactors, introducing AI-powered migration utilities that reduce professional services hours by roughly 30%.

- November 2025: Thoma Bravo finalized the USD 12.3 billion acquisition of Ceridian, taking the Dayforce provider private to accelerate product expansion away from quarterly earnings pressure.

- November 2025: UKG purchased Mo, enhancing employee recognition and sentiment analytics within its experience platform.

Global Core HR Software Market Report Scope

The core HR software market refers to revenue generated from digital platforms that manage foundational human resource functions within organizations, including employee data management, payroll, benefits administration, time and attendance, compliance reporting, and workforce recordkeeping. These systems serve as the central system of record for employee information and are critical for ensuring operational efficiency, regulatory compliance, and workforce visibility across organizations.

The Core HR Software Market Report is Segmented by Component (Software, Services), Deployment (Cloud, On-premises, Hybrid), Organization Size (SMEs, Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, Retail and E-commerce, Manufacturing, Government and Public Sector, Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| SMEs |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment | Cloud | |

| On-premises | ||

| Hybrid | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By Industry Vertical | IT and Telecom | |

| BFSI | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the core HR software market expected to be by 2031?

Mordor Intelligence projects the core HR software market size to reach USD 22.01 billion by 2031, advancing at an 8.34% CAGR from 2026.

Which deployment model is growing fastest within core HR suites?

Hybrid architectures are forecast to expand at a 9.28% CAGR through 2031 as organizations balance data sovereignty with the agility of SaaS, according to Mordor Intelligence.

What segment currently holds the largest share of spending?

In 2025, software licenses accounted for 79.18% of global revenue, making them the largest contributor to overall spending.

Which region is expected to deliver the highest growth?

Asia-Pacific is set to grow at a 10.11% CAGR through 2031, outpacing all other regions owing to rapid mid-market digitization.

Why are services gaining momentum in the core HR software market?

Implementation complexity, data migration challenges and the need for AI governance are boosting demand for consulting, managed payroll and optimization services, which are projected to rise at an 8.87% CAGR.

Page last updated on: