Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

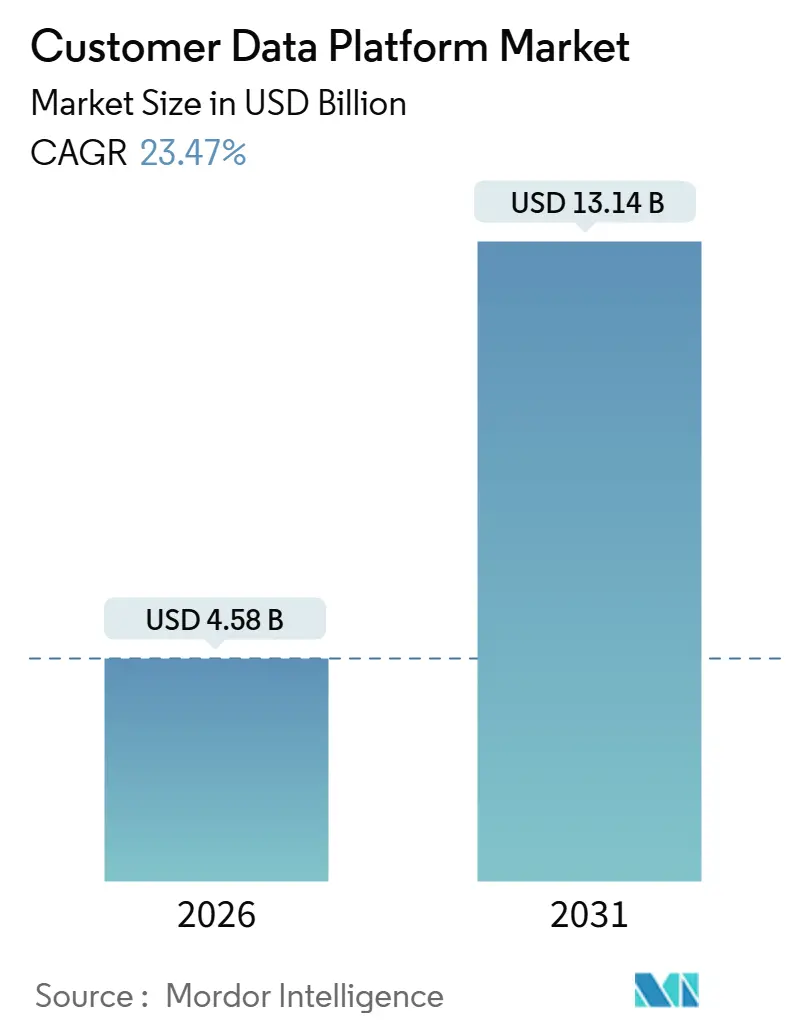

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 13.14 Billion |

| Growth Rate (2026 - 2031) | 23.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Data Platform Market Analysis by Mordor Intelligence

The customer data platform market size is valued at USD 4.58 billion in 2026 and is projected to reach USD 13.14 billion by 2031, advancing at a 23.47% CAGR over the forecast period. Intense regulatory pressure, the retirement of third-party cookies, and elastic cloud economics are collectively accelerating enterprise investment in unified first-party data layers that support privacy-safe personalization. Vendors that embed warehouse-native connectors and zero-copy pipelines are gaining share because they remove data egress fees while sustaining real-time identity graphs. Retailers, banks, and healthcare providers that deployed customer data platforms before 2025 are now reporting double-digit gains in conversion rates, reduced churn, and increased lifetime value, narrowing the adoption gap between early movers and laggards. Competitive intensity is increasing as reverse-ETL specialists challenge legacy marketing clouds on total cost of ownership, prompting incumbents to open their architectures and add warehouse-native features. At the same time, generative AI agents require sub-second access to unified profiles, pushing the market toward streaming topologies that favor vendors with event-driven ingestion pipelines.

Key Report Takeaways

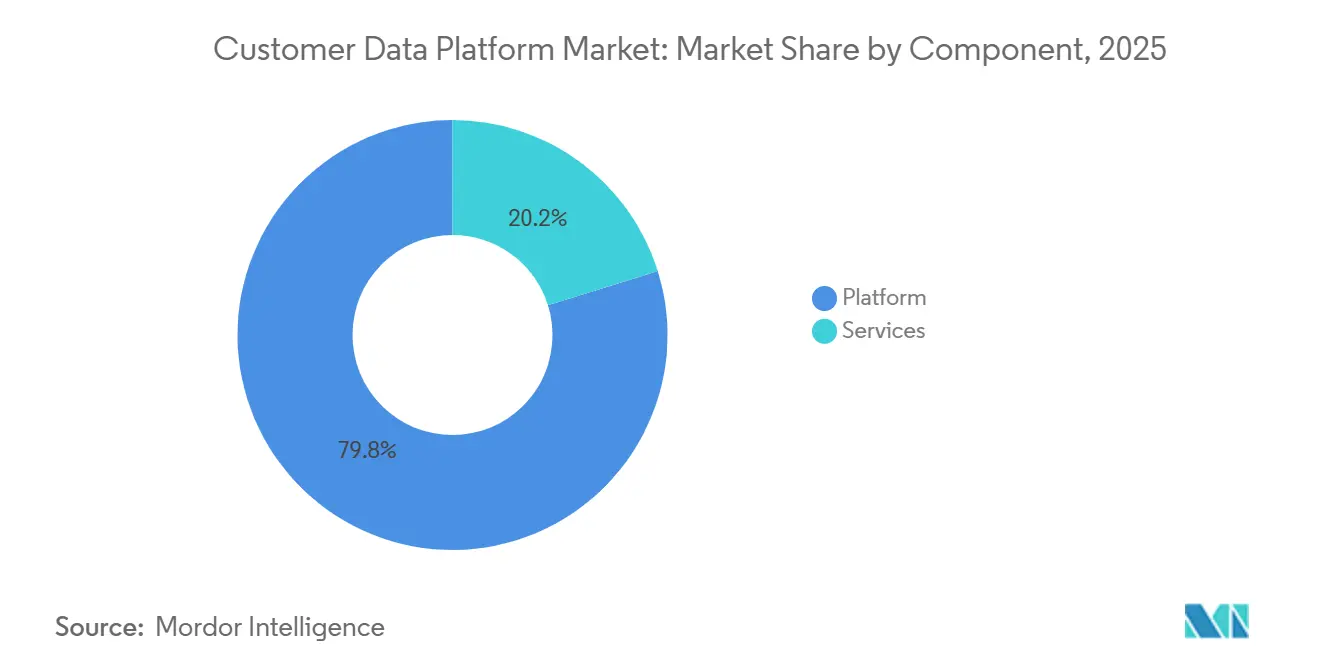

- By component, platforms led with 79.82% customer data platform market share in 2025, while services are advancing at a 23.82% CAGR through 2031.

- By deployment mode, cloud solutions accounted for 88.43% of the 2025 customer data platform market, and this segment is growing at a 23.89% CAGR through 2031.

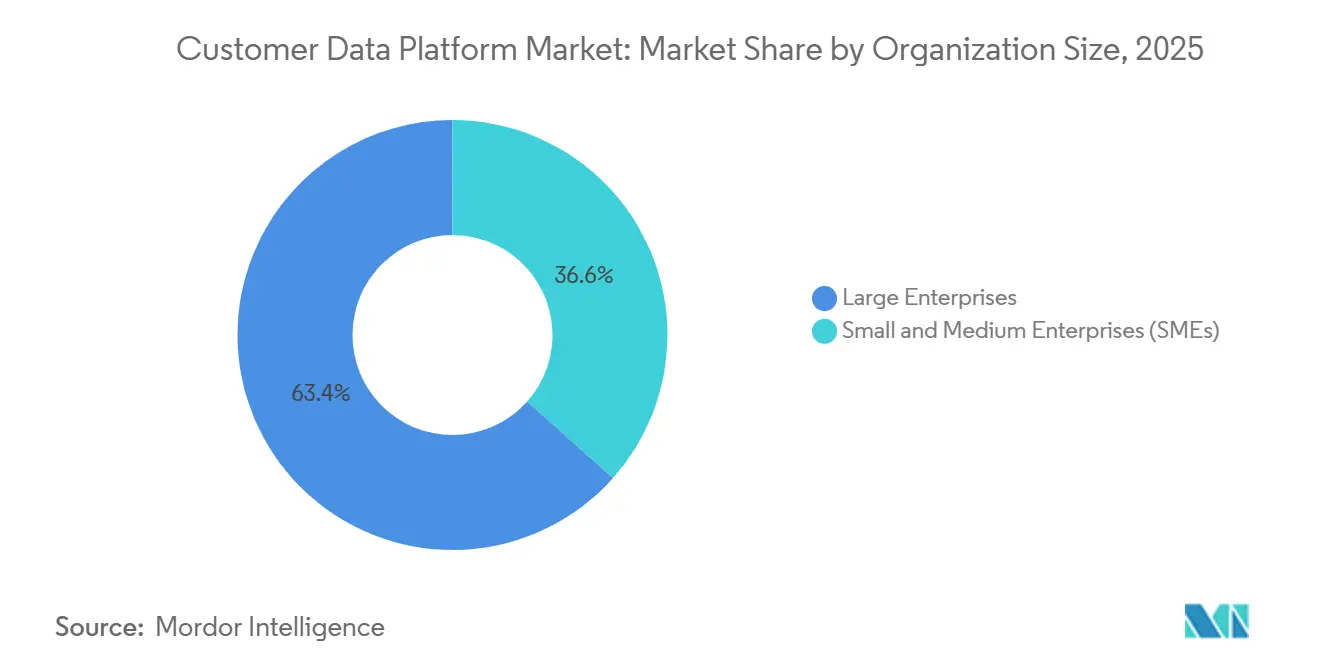

- By organization size, large enterprises accounted for 63.41% of 2025 revenue, yet small and medium enterprises are expanding at a 23.84% CAGR over the forecast period.

- By end-user industry, retail and e-commerce accounted for 35.67% of the customer data platform market share in 2025, whereas healthcare is projected to post the fastest CAGR of 24.68% through 2031.

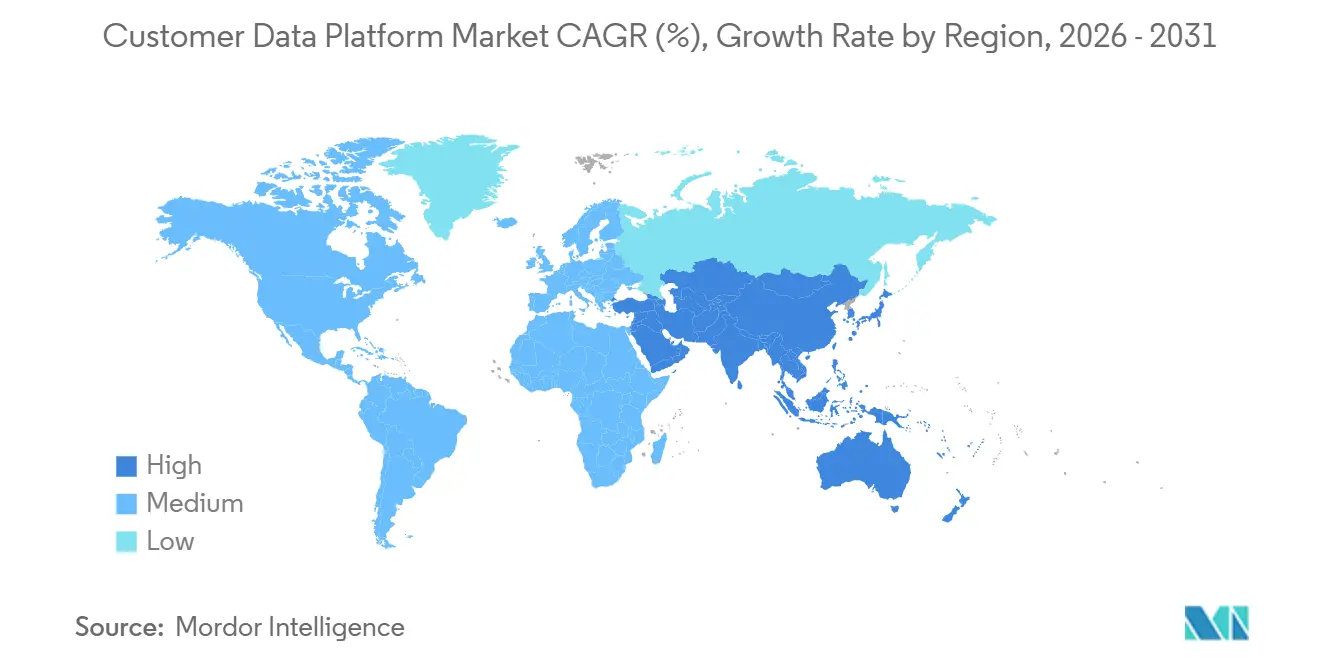

- By geography, North America captured 47.32% of global revenue in 2025, while Asia Pacific is forecast to accelerate at a 24.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Customer Data Platform Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phase-out of third-party cookies accelerating first-party data investments by European retailers | +4.2% | Europe, North America | Short term (≤ 2 years) |

| Headless and omnichannel commerce boom in Asia Pacific raising demand for event-driven data unification | +3.8% | Asia Pacific, Middle East and Africa | Medium term (2-4 years) |

| AI-powered predictive patient engagement driving healthcare CDP uptake in United States and Europe | +3.5% | North America, Europe | Medium term (2-4 years) |

| Generative AI agents requiring real-time customer graphs for next-best-action in North American retail banking | +4.1% | North America, expanding to Europe and Asia Pacific | Medium term (2-4 years) |

| 5G lifecycle monetization initiatives fueling CDP deployments by Middle East telcos | +2.9% | Middle East | Long term (≥ 4 years) |

| Zero-copy data warehouse integrations cutting data egress costs for global enterprises | +3.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Phase-Out of Third-Party Cookies Accelerating First-Party Data Investments by European Retailers

Google’s final removal of third-party cookies from Chrome eliminates cross-site identifiers that fueled programmatic advertising. European retailers are rebuilding their audience insights around loyalty programs, authenticated sessions, and progressive profiling to generate deterministic first-party data. Customer data platforms have therefore shifted from optional martech to foundational infrastructure that unifies consented signals across web, store, and call-center interactions. Platforms that provide integrated consent orchestration and deterministic identity stitching are winning deals because they simplify compliance with the General Data Protection Regulation. Early adopters that completed migration before 2025 cited 15-25% lifts in customer lifetime value and 10-12% improvements in media efficiency after reallocating spend toward owned channels.[1]Salesforce, “Data Cloud Overview,” salesforce.com Growing first-party addressability also enables these retailers to negotiate better audience-extension deals with walled-garden publishers, amplifying the economic upside of CDP projects.

Headless and Omnichannel Commerce Boom in Asia Pacific Raising Demand for Event-Driven Data Unification

Retailers in India, Indonesia, and Vietnam are decoupling front-end experiences from back-end engines to support mobile-first shopping journeys. Headless architecture generates thousands of behavioral events from progressive web apps, super-app mini-stores, and social commerce plug-ins, overwhelming batch-oriented marketing suites. Streaming customer data platforms that capture, transform, and join these event flows into real-time profiles allow marketers to trigger personalized offers within milliseconds of basket abandonment. Merchants using event-driven CDPs recorded 30-40% conversion uplifts compared to peers using daily batch workflows. Super-app ecosystems common in Southeast Asia further increase data complexity because a single user ID spans payments, ride-hailing, and marketplace verticals. CDP vendors that resolve identities across those domains without exporting data outside regional borders are therefore preferred as data-localization laws tighten in India and Indonesia.

AI-Powered Predictive Patient Engagement Driving Healthcare CDP Uptake in the United States and Europe

Hospitals and insurers are unifying electronic health records, wearable telemetry, and claims data to power early-warning models that flag care gaps. Real-time CDPs feed these models in real time, enabling outreach such as medication reminders or telehealth scheduling within hours of an anomaly. Platforms embed consent gateways and audit trails that map directly to Health Insurance Portability and Accountability Act and General Data Protection Regulation requirements, reducing compliance friction for clinical teams.[2]Onetrust, “CCPA and CPRA Enforcement: What You Need to Know,” onetrust.com Payers adopting unified data layers reported double-digit decreases in avoidable readmissions and 10-15% improvements in member retention through personalized wellness journeys. The shift toward value-based reimbursement amplifies urgency because revenue increasingly correlates with measurable patient outcomes. Vendors integrating Fast Healthcare Interoperability Resources endpoints and common electronic health record APIs are best positioned to capture this healthcare wave.

Generative AI Agents Requiring Real-Time Customer Graphs for Next-Best-Action in North American Retail Banking

Retail banks are piloting large language model agents that converse with customers through mobile apps and call centers. Those agents require sub-second retrieval of unified account, transaction, and intent signals to suggest the next best action. Customer data platforms that maintain streaming profiles and push vector embeddings into AI inference layers enable this latency goal. Banks deploying such stacks reported faster cross-sell conversion, with mortgage pre-qualification offers delivered during the same chat session that originated from a credit-card inquiry. Warehouse-native CDPs reduce total cost of ownership by eliminating data copies, an advantage that resonates with chief information officers pursuing cloud cost optimization. As consumer adoption of conversational banking rises, real-time CDP infrastructure is set to become as fundamental as core banking systems.

Restraints Impact Analysis of Customer Data Platform Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented legacy banking schemas limiting CDP ROI in Europe | -2.8% | Europe | Medium term (2-4 years) |

| High total cost of ownership of on-premise CDPs discouraging South American SMEs | -2.1% | South America | Short term (≤ 2 years) |

| Shortage of reverse-ETL talent hindering composable CDP rollouts in Asia Pacific | -1.9% | Asia Pacific | Medium term (2-4 years) |

| Data-localization mandates restricting multi-region CDPs | -2.5% | China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Banking Schemas Limiting CDP ROI in Europe

Most European banks still run mainframe cores where customer data is scattered across products, each with different identifiers in the customer data platform market. A CDP must reconcile checking, mortgage, and wealth attributes in a single profile, yet conflicting keys lead to 12-18-month engineering projects that inflate budgets by up to 60% compared to greenfield deployments.[3]Oracle, “Oracle Data Cloud and AI,” oracle.com Data-minimization clauses under the General Data Protection Regulation further constrain profile enrichment because banks must justify every persisted attribute. Several tier-one institutions that launched CDPs without first modernizing schemas realized minimal lift in email conversion because fragmented profiles could not trigger timely offers across channels. Interest is therefore shifting toward composable banking, which wraps legacy systems with application programming interfaces, but adoption remains slow due to migration risk.

High Total Cost of Ownership of On-Premise CDPs Discourages South American SMEs

Small and medium enterprises in Brazil and Argentina face price tags exceeding USD 500,000 over three years when deploying on-premises CDPs. Upfront hardware costs, perpetual licenses, and skilled-labor scarcity lengthen payback periods beyond the tolerance of firms operating in volatile macroeconomic climates. Cloud versions could ease the strain, yet many buyers hesitate because only a handful of providers operate in-country data centers needed to meet sovereignty requirements in the customer data platform industry. Implementation partners are limited, so companies often import talent from the United States or Europe at premium rates, adding 25-30% to project cost. A nascent ecosystem of regional cloud providers is emerging, but market penetration remained modest by the end of 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Customer Data Platform Market Segment Analysis

By Component:

Platforms Retain Dominance While Services AcceleratePlatform solutions accounted for 79.82% of total 2025 revenue of the customer data platform market, underscoring the importance of proprietary identity graphs that reconcile deterministic and probabilistic signals across every channel. This dominance is expected to persist because many buyers still prefer end-to-end functionality that combines unification, segmentation, and activation into a single vendor contract. The services segment, however, is on a 23.82% annual growth trajectory as organizations seek guidance on configuring composable stacks, instituting privacy governance, and training marketers on low-code orchestration.

Professional services teams are increasingly retained after go-live to monitor data quality and optimize campaigns, generating high-margin recurring revenue. Managed services appeal to firms that lack in-house data engineering talent, especially in regulated verticals where audit trails must be updated continuously. Implementation tasks are slowly being commoditized as offshore centers in India and Eastern Europe automate extract-transform-load mapping using reusable libraries. Consequently, consulting value is migrating toward strategic advisory, such as lifetime-value modeling and multi-touch attribution, areas where domain expertise rather than coding speed confers an advantage.

By Deployment Mode:

Cloud Architectures, Capture Elastic Compute PremiumCloud deployments accounted for 88.43% of the 2025 customer data platform market share, reflecting the appeal of elastic compute that absorbs Black Friday traffic without over-provisioning servers. The cloud segment is also the fastest-growing, with a 23.89% CAGR through 2031, as zero-copy integrations with Snowflake, Databricks, and Google BigQuery eliminate storage duplication. On-premises installations persist mainly in financial services and healthcare institutions that demand in-house control over sensitive records, yet their share is eroding as hybrid architectures route activation workloads to the public cloud while retaining restricted data locally.

Edge computing is creating a complementary layer where lightweight identity graphs sit close to point-of-sale terminals or connected vehicles in the customer data platform market. Vendors that synchronize these edge profiles with centralized cloud instances achieve latency below 200 milliseconds, meeting in-store personalization requirements without compromising cross-channel orchestration. Multi-cloud strategies are expanding as chief technology officers seek to avoid lock-in; this preference favors CDPs that remain agnostic by containerizing services or adopting open table formats such as Apache Iceberg. Subscription pricing converts capital expenses into operating expenses, improving vendor revenue visibility but requiring stronger cash management among growth-stage entrants.

By Organization Size:

Consumption-Based Pricing Unlocks SME GrowthLarge enterprises accounted for 63.41% of 2025 revenue share of the customer data platform market, thanks to scale economies that justify multimillion-dollar licensing fees. These buyers run hundreds of campaigns across dozens of channels, prompting them to prefer integrated platforms that centralize governance and reduce integration sprawl. Small and medium enterprises are forecast to grow at a 23.84% CAGR because warehouse-native vendors now unbundle identity resolution from activation and offer pay-as-you-go tiers starting below USD 50,000 for under 500,000 profiles.

SMEs leverage reverse-ETL pipelines that push modeled tables from Snowflake or BigQuery to email and advertising endpoints, reducing total cost of ownership by as much as 70% compared with traditional CDPs. Low-code interfaces let marketers configure identity rules without SQL, overcoming staffing shortages. Large organizations, by contrast, demand advanced entity resolution that links multiple individuals to complex buying committees, a scenario still nascent in SME-focused tools. Across both tiers, the maturation of generative AI assistants increases appetite for unified data because conversational interfaces surface data gaps instantly, driving additional seat expansion.

By End-User Industry:

Healthcare Emerges as Fastest-Growing VerticalRetail and e-commerce accounted for 35.67% of 2025 sales, benefiting from a decade of investment in personalized merchandising and high-velocity experimentation. Healthcare, however, is poised for the fastest 24.68% CAGR through 2031 as hospitals and insurers apply predictive models to chronic care, readmission prevention, and member retention. The customer data platform market size for healthcare use cases is on course to more than triple within the forecast horizon as value-based reimbursement intensifies the link between personalization and revenue.

Financial institutions are also migrating from product-centric to customer-centric engagement, using CDPs to assemble unified views of deposits, lending, and investments that feed financial wellness programs. Telecommunications operators tap CDPs to curb churn, which costs more than USD 200 per subscriber in saturated markets, and to cross-sell 5G value-added services such as cloud gaming. Media and entertainment players rely on sub-second identity graphs to recommend live-event content that maximizes watch time. Manufacturing and logistics firms use account-level resolution to accelerate B2B sales cycles spanning multiple stakeholders, demonstrating that CDP adoption is no longer confined to consumer retail.

Geography Analysis

North America Customer Data Platform Market

North America remained the single largest region, accounting for 47.32% of 2025 revenue of the customer data platform market, supported by widespread cloud adoption, strong digital ad budgets, and privacy statutes such as the California Consumer Privacy Act that reward transparent first-party data practices. The region also benefits from a dense ecosystem of system integrators and data-science talent that shortens deployment timelines. The customer data platform market is expanding here as banks, insurers, and healthcare providers integrate streaming telemetry into unified profiles for generative AI agents.

APAC Customer Data Platform Market

Asia Pacific is the fastest-growing region, with a 24.41% CAGR through 2031. Headless commerce in India, Indonesia, and Vietnam generates event streams that legacy marketing clouds cannot reconcile, pushing mid-market retailers toward event-driven CDPs. China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act require in-country storage, so vendors are launching geo-fenced instances to meet localization mandates. This fragmentation increases operational costs but expands the total addressable market, as every multinational now needs separate regional deployments.

EMEA and South America Customer Data Platform Market

Europe’s adoption curve remains healthy as General Data Protection Regulation enforcement intensifies, yet fragmented legacy cores in banking and telecom extend implementation cycles. The Middle East represents a high-growth pocket because 5G monetization drives telcos in Saudi Arabia and the United Arab Emirates to deploy CDPs that unify subscriber, network, and billing data. Africa and South America lag due to limited cloud infrastructure, macroeconomic volatility, and high on-premise costs, though regional cloud providers with local data centers are beginning to close the gap.

Competitive Landscape

The customer data platform market is moderately fragmented. The top five vendors collectively hold around 45% revenue share, while dozens of specialists cover composable architectures, vertical niches, or regional compliance gaps. Integrated platform providers such as Salesforce, Adobe, and Oracle differentiate through bundled identity, analytics, and activation modules that appeal to large enterprises seeking a single throat to choke. Composable challengers like Hightouch, RudderStack, and Census advocate a warehouse-first model, claiming 30-50% lower total cost and freedom from vendor lock-in.

Technology roadmaps converge on real-time streaming. Salesforce patented a distributed identity graph that shards profiles across edge nodes while preserving consistency, cutting in-store personalization latency to under 150 milliseconds. Adobe embedded natural-language AI assistants into its platform so marketers can build audiences by simply asking questions, lowering data-science barriers. Oracle launched zero-copy connectors that read directly from its lakehouse without exporting data, eliminating egress fees for highly regulated sectors.

Strategic alliances are forming around cloud warehouses. RudderStack and Snowflake released a native application that builds identity graphs inside the warehouse, while Amperity integrated directly with Azure Synapse to win retailers seeking Microsoft alignment. Venture capital remains active, highlighted by Hightouch’s USD 35 million Series C, although funding terms now emphasize efficient growth over pure top-line expansion. As generative AI elevates the need for millisecond context retrieval, vendors that master event ingestion, probabilistic stitching, and low-latency query processing are likely to consolidate leadership.

Customer Data Platform Industry Leaders

Salesforce.com, Inc.

Oracle Corporation

Adobe Inc.

SAP SE

Segment.io Inc.

- *Disclaimer: Major Players sorted in no particular order

Customer Data Platform Market Companies Covered in this Report

- Salesforce.com, Inc.

- Oracle Corporation

- Adobe Inc.

- SAP SE

- Twilio Inc.

- Segment.io Inc.

- Arm Ltd.

- Tealium Inc.

- Acquia Inc.

- BlueConic, Inc.

- mParticle Inc.

- Zeta Global Corp.

- Amperity Inc.

- ActionIQ, Inc.

- Klaviyo Inc.

- RedPoint Global Inc.

- Bloomreach, Inc.

- Lexer Pty Ltd

- RudderStack, Inc.

- Snowplow Analytics Ltd.

- Zeotap GmbH

- Optimove Inc.

- Leadspace, Inc.

- Ometria Ltd.

- Blueshift Labs, Inc.

- Simon Data, Inc

- Lytics, Inc.

Recent Industry Developments in Customer Data Platform Market

- October 2025: Adobe broadened its Real-Time Customer Data Platform with richer AI Assistant tools that let marketers pull audience segments through natural-language prompts and build predictive lists from propensity scores. The upgrade makes advanced data science accessible to non-technical teams, removing a key barrier to wider CDP use.

- August 2025: Twilio deepened the connection between Segment’s customer data layer and its communications suite, allowing businesses to launch personalized email, SMS, and WhatsApp messages in real time without custom code. The tighter coupling accelerates omnichannel deployments and shortens the path to measurable engagement gains.

- June 2025: Oracle added zero-copy links to Unity Customer Data Platform for its Cloud Infrastructure Data Lakehouse, enabling clients to craft unified profiles without duplicating data. The enhancement addresses sovereignty rules in regulated industries and eliminates the egress fees that once discouraged petabyte-scale cloud projects.

- January 2025: Salesforce introduced Agentforce within Data Cloud, opening the door for autonomous AI agents that draw on unified profiles to tailor conversations across sales, service, and marketing. By positioning Data Cloud as the real-time backbone for agent-led journeys, the release highlights the market’s shift toward generative-AI personalization.

Customer Data Platform Market Report Scope and Research Methodology

Market Definition and Coverage

Our study treats the customer data platform (CDP) market as all packaged software platforms that ingest primarily first-party customer data, resolve identities, maintain persistent unified profiles, and expose those profiles to external applications through real-time APIs and batch connectors. Revenue is counted at the point a license or subscription is booked, net of professional services and third-party data fees.

Scope exclusion: pure-play data-management platforms that traffic chiefly in anonymous third-party data are excluded.

Segments Covered in This Report

- By Component

- Platform

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- Retail and E-Commerce

- Banking, Financial Services, and Insurance

- IT and Telecommunication

- Media and Entertainment

- Healthcare

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with mar-tech architects, privacy officers, and regional system integrators across North America, Europe, and fast-growing Asia-Pacific helped verify average license sizes, deployment hurdles, and churn ratios that seldom appear in public filings. Short surveys of retail and BFSI digital leaders gauged penetration rates among mid-market firms, filling data gaps left by desk research.

Desk Research

Mordor analysts began with open datasets, including UN Comtrade shipment logs, U.S. Bureau of Economic Analysis ICT spend tables, Eurostat cloud-services turnover, and filings scraped from SEC 10-Ks to anchor baseline enterprise software spending. Specialist sources such as the Interactive Advertising Bureau, the CDP Institute annual census, and privacy-ruling repositories from EDPB and the FTC provided adoption signals and regulatory triggers. Company presentations, patent abstracts (via Questel), and press releases supplied price points and product mix clues. These examples illustrate, not exhaust, the secondary inputs consulted for trend mapping and sanity checks.

Market-Sizing & Forecasting

A top-down model scales global enterprise software outlays and applies industry-specific CDP penetration and average selling-price coefficients, which are then balanced against a sampled bottom-up roll-up of 60 public and private vendors. Key variables include e-commerce share of retail sales, marketing-cloud spending per employee, cloud-migration ratios, regional privacy-compliance costs, and the sunset timeline for third-party cookies. Multivariate regression, cross-validated with ARIMA for short-term shocks, projects each driver to 2030. Outliers flagged during expert callbacks are adjusted before finalization.

Data Validation & Update Cycle

Outputs run through variance thresholds versus external indices, after which senior reviewers sign off. Reports refresh annually, with interim updates triggered by material funding rounds, landmark privacy rulings, or mergers. A final analyst pass occurs just before delivery so clients always receive the latest calibrated view.

How Mordor Intelligence's Customer Data Platform Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different revenue buckets, embed services unevenly, or refresh at varying cadences.

Key gap drivers here include whether campaign-delivery add-ons are folded into scope, how aggressively future cookie deprecation uplifts are baked in, and the cadence at which foreign-exchange adjustments are applied. Mordor's study locks definitions early, triangulates price and volume from both buyers and sellers, and applies mid-cycle FX re-baselining, choices that temper extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.71 B (2025) | Mordor Intelligence | - |

| USD 9.72 B (2025) | Global Consultancy A | Bundles campaign and delivery CDPs, vendor-revenue list multiplied by aggressive forward ASP |

| USD 7.06 B (2024) | Trade Journal B | Derives share from total marketing-cloud spend, limited country splits, single-year FX rate |

These contrasts show that, by anchoring on clearly bounded software revenue and cross-checking both penetration and price, Mordor Intelligence delivers an even-handed, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the customer data platform market in 2026?

The market is valued at USD 4.58 billion in 2026 and is forecast to reach USD 13.14 billion by 2031.

Which region is expanding fastest for customer data platforms?

Asia Pacific is growing at a 24.41% CAGR, driven by headless commerce adoption and mobile-first engagement models.

What deployment model holds the largest customer data platform market share?

Cloud deployments dominate with 88.43% share in 2025 because zero-copy integrations eliminate data movement costs.

Why are healthcare organizations adopting customer data platforms?

Hospitals and insurers need unified real-time profiles to power predictive care models that improve outcomes and reimbursement.

How are composable CDP vendors challenging incumbents?

Warehouse-native platforms cut total cost of ownership by 30-50% and minimize vendor lock-in, attracting cost-conscious buyers.

What impact will generative AI have on CDP requirements?

Generative AI agents demand sub-second access to unified data, making real-time streaming and edge-aware identity graphs essential.

Page last updated on: