HR Document Management and ESignature Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.07 Billion |

| Market Size (2031) | USD 13.89 Billion |

| Growth Rate (2026 - 2031) | 11.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Document Management and ESignature Market Analysis by Mordor Intelligence

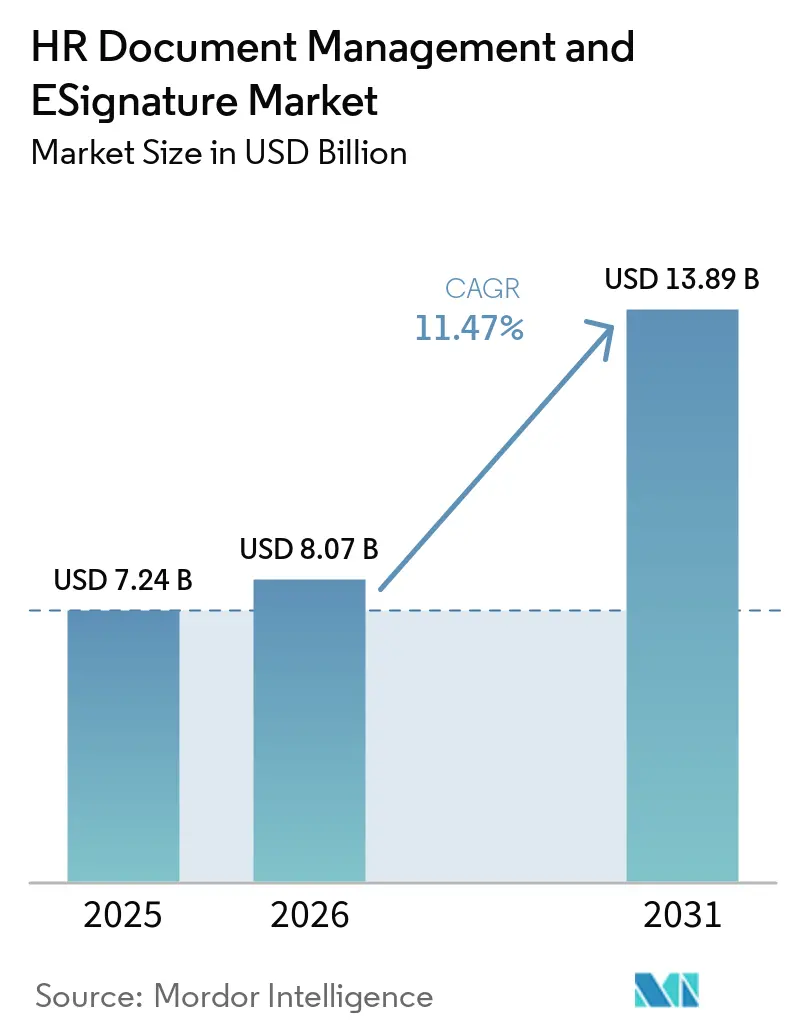

The HR document management and eSignature market size is expected to increase from USD 7.24 billion in 2025 to USD 8.07 billion in 2026 and reach USD 13.89 billion by 2031, growing at a CAGR of 11.47% over 2026-2031. The market is moving from paper-heavy personnel file handling toward connected digital systems that combine document creation, e-signing, archiving, and audit support in a single workflow. This shift is tied to day-to-day HR efficiency because delays in onboarding, contract completion, and record retrieval can now affect both workforce productivity and compliance exposure. Cross-border hiring, higher volumes of digital employment documentation, and broader cloud adoption are also pushing buyers toward platforms that can manage templates, signatures, and retention rules across multiple jurisdictions. Growth still faces friction from fragmented privacy rules, country-level labor consultation requirements, and the technical work needed to align new systems with existing HR platforms. Competition remains balanced between a dominant global vendor and a wide range of regional and specialized providers, keeping the market open to differentiation through depth of compliance, identity assurance, and integration strength.

Key Report Takeaways

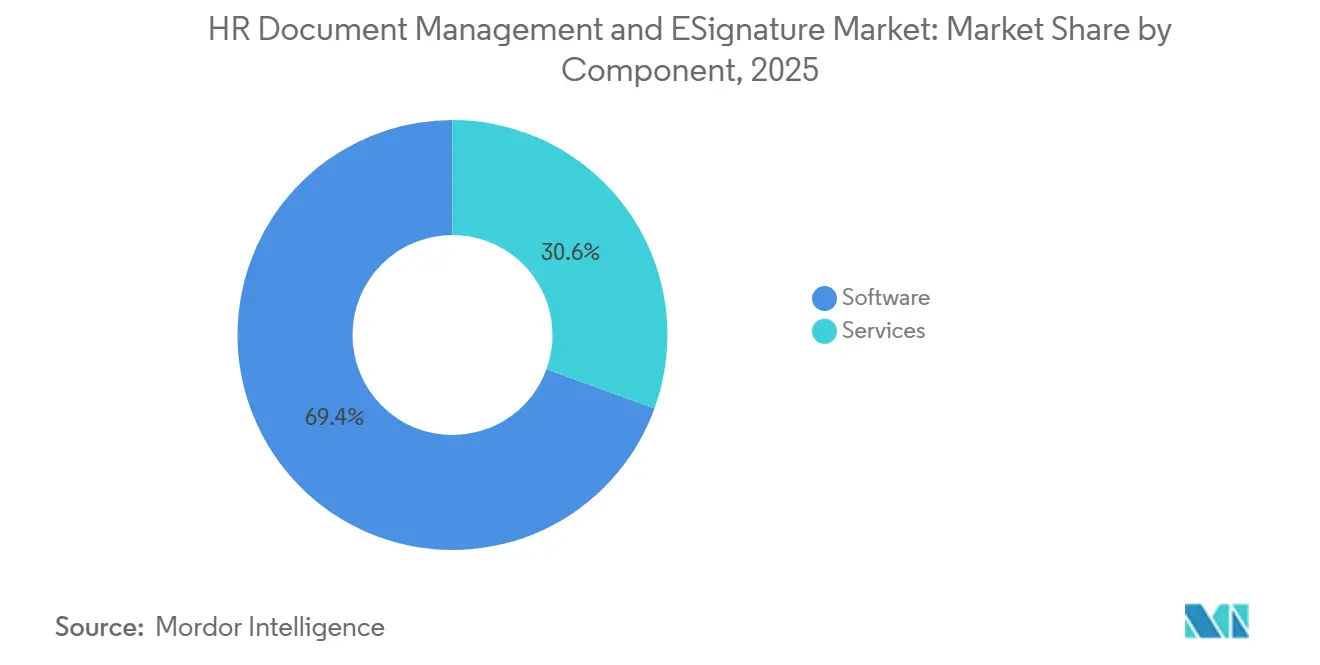

- By component, software held 69.44% of the HR document management and eSignature market share in 2025, while services are projected to expand at 13.65% CAGR through 2031.

- By deployment mode, cloud accounted for 68.16% of the total revenue in 2025, while hybrid deployment is projected to grow at 12.78% CAGR through 2031.

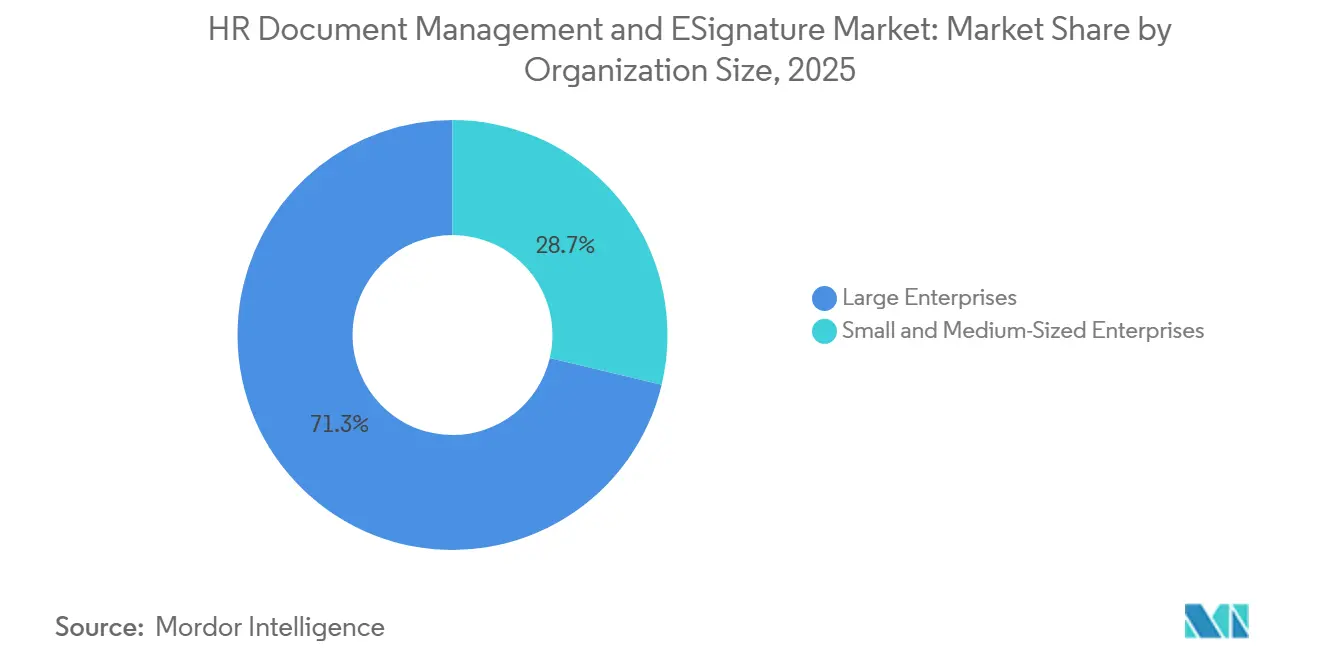

- By organization size, large enterprises accounted for 71.29% of revenue in 2025, while SMEs are expected to expand at a 13.29% CAGR through 2031.

- By industry vertical, IT and telecommunications accounted for 30.29% of revenue in 2025, while healthcare and life sciences are projected to advance at 11.86% CAGR through 2031.

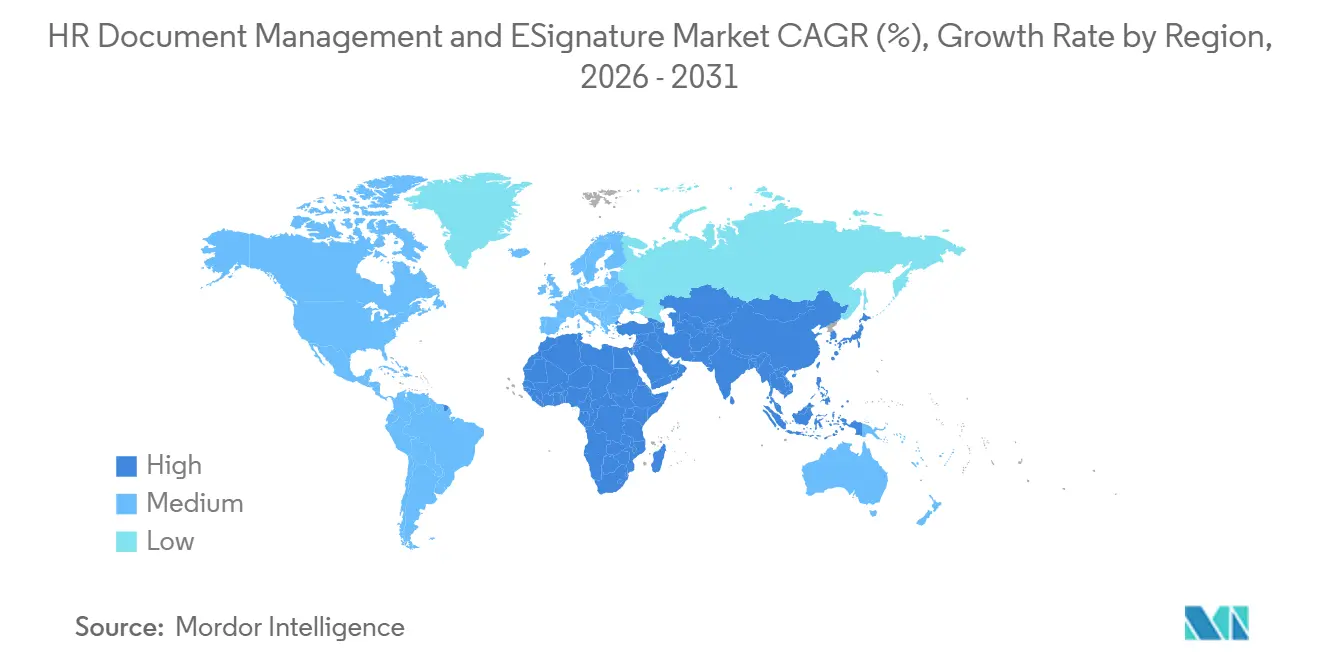

- By geography, North America held 36.41% of the HR document management and eSignature market in 2025, while Asia-Pacific is projected to record the highest regional CAGR of 12.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Document Management and ESignature Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Paperless HR Workflows | +2.9% | Global | Short term (≤ 2 years) |

| Cloud-Native HR Tech Modernization | +2.4% | Global, with APAC acceleration | Medium term (2-4 years) |

| Tightening Audit and Records Retention Requirements | +1.8% | North America and EU, expanding globally | Medium term (2-4 years) |

| Growing Demand for Compliant Global Hiring and Onboarding | +1.5% | Global, with focus on APAC and MEA | Medium term (2-4 years) |

| Expansion of Remote I-9 and Digital Identity Verification Workflows | +1.0% | North America | Short term (≤ 2 years) |

| EIDAS 2.0 Wallet Readiness for Cross-Border Employment Signing | +0.7% | EU and EEA, with spillover to Switzerland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Paperless HR Workflows

The shift to paperless HR administration remains the clearest demand driver for the HR document management and eSignature market. Organizations are replacing paper files because digital workflows reduce delays in onboarding, policy acknowledgment, and contract handling, and they also make records easier to find and review. Avature reported that 60% of survey respondents identified streamlining HR processes through automation and AI as their top organizational priority in 2025, which supports the strong focus on document workflow digitization. The effect goes beyond efficiency, as a smoother onboarding experience at the start of employment reduces administrative friction for new hires and supports better early engagement. Once a company builds searchable digital files and auditable document trails, the operating model of the HR document management and eSignature market becomes much harder to reverse.

Cloud-Native HR Tech Modernization

Cloud modernization is reshaping how buyers evaluate the HR document management and eSignature market. Employers increasingly want document platforms that integrate with cloud HR environments, support remote access, and enable updates to templates or compliance controls without long internal release cycles. This demand is even stronger when organizations manage employees across several jurisdictions and cannot rely on slow manual patching after local regulatory changes. aconso’s March 2026 update on HR document management in the AWS European Sovereign Cloud showed how vendors are responding to data residency and sovereignty concerns while still keeping cloud delivery at the center of the offering. As a result, the HR document management and eSignature market is rewarding vendors that pair cloud delivery with deep system integration rather than those that offer only basic signature functions.

Tightening Audit and Records Retention Requirements

Audit readiness and records retention are pushing the HR document management and eSignature market further into compliance-critical territory. Employers now need personnel records that are not only stored securely but also timestamped, traceable, and retrievable in a format that withstands investigations and disputes. The Court of Justice of the European Union clarified in Case C-65/23 that works agreements cannot override GDPR necessity requirements, thereby increasing scrutiny of how HR systems process and retain employee information. In the United States, USCIS maintained the remote document examination alternative for eligible employers while also reinforcing procedural expectations for Form I-9 completion, thereby increasing the value of structured digital workflows.[1]U.S. Citizenship and Immigration Services, “Minor Changes to Form I-9 and E-Verify Updates,” U.S. Citizenship and Immigration Services, uscis.gov This is why the HR document management and eSignature market is benefiting from demand for immutable audit trails, retention policies, and role-based controls over employment documents.

Growing Demand for Compliant Global Hiring and Onboarding

Global hiring is expanding the need for jurisdiction-aware workflows across the HR document management and eSignature market. Employers with distributed workforces cannot rely on uniform offer letters, consent forms, and signature processes, as document requirements vary across labor systems and privacy regimes. The European Commission’s Regulation (EU) 2024/1183 requires each EU member state to make at least 1 certified digital identity wallet available by December 2026, which is raising the baseline for identity-backed employment signing workflows. Avature also found that 68% of respondents ranked effective onboarding processes as a priority, indicating that document execution remains central to workforce activation rather than a secondary admin task. These conditions are creating sustained demand in the HR document management and eSignature market for tools that can move hiring data across ATS, HRIS, and signing workflows without breaking local compliance rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Employee Consent Requirements | -1.6% | EU and GDPR-aligned markets globally | Long term (≥ 4 years) |

| Integration Complexity Across HRIS, Payroll, and Identity Systems | -1.2% | Global | Medium term (2-4 years) |

| Works Council and Cross-Border Data Transfer Constraints | -0.8% | EU, primarily Germany, France, and Benelux | Long term (≥ 4 years) |

| Identity Friction for Deskless and Shared-Device Workforces | -0.5% | APAC, MEA, and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Employee Consent Requirements

Privacy regulation remains a long-running restraint on the HR document management and eSignature market because employee data touches recruitment, onboarding, daily administration, and offboarding. The difficulty is not only storage security, but also lawful processing, retention discipline, and local variation in how employee data rules are applied. The CJEU ruling in Case C-65/23 added further legal weight to the requirement that HR data processing must meet the GDPR's necessity standards, thereby raising the compliance burden for both employers and platform vendors. Multinational employers, therefore, need country-specific configuration models, and smaller firms often struggle to assess whether a vendor’s privacy posture is strong enough for their risk profile. This keeps the HR document management and eSignature market growing, but it also raises the cost of product maintenance and slows adoption in more complex regulatory settings.

Integration Complexity across HRIS, Payroll, and Identity Systems

Integration complexity is a practical brake on the HR document management and eSignature market, especially for organizations with layered HR technology stacks. Many employers already run separate systems for recruiting, core HR, payroll, identity management, and document storage, so the document platform must connect across multiple environments simultaneously. The problem becomes more serious when authentication and signing occur across different identity contexts, as even a small mismatch can require manual intervention and delay completion. aconso’s May 2026 Workday partnership is one example of how vendors are trying to reduce this friction by embedding document creation, management, and archiving into core HCM workflows. Until more buyers can rely on low-friction connectors and clean data exchange, the HR document management and eSignature market will continue to experience slower rollouts in large, highly customized enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds the Lead While Services Gain Speed

Software accounted for 69.44% of total revenue in 2025, indicating that the core buying priority in the HR document management and eSignature market still lies in the application layer. Buyers continue to favor platforms that cover document creation, template management, digital file handling, secure storage, archiving, and signing in a single operating environment. This reflects the need to standardize routine HR workflows before companies add broader advisory or transformation support. The HR document management and eSignature market also benefits from demand for employee record systems that can keep documents accessible, auditable, and aligned with local retention expectations.

Services are projected to grow at a 13.65% CAGR through 2031, faster than software, pointing to a changing commercial mix in the HR document management and eSignature market. Implementation and integration work is expanding because organizations rarely deploy HR document tools in isolation; instead, they connect them to HCM, payroll, and workflow systems already in place. Advisory work is also gaining weight as employers need help translating regulatory requirements into document design, storage rules, and process controls. aconso stated that it manages more than 1 billion HR documents for over 600 HR teams globally, which shows why scale, deployment expertise, and compliance support are becoming stronger differentiators across the HR document management and eSignature market.

By Deployment Mode: Cloud Leads While Hybrid Supports Compliance Needs

Cloud commanded 68.16% of the market in 2025, making it the largest contributor to the HR document management and eSignature market size among deployment options. The preference for cloud in the HR document management and eSignature market is driven by scalability, remote access, and vendor-managed updates, which are difficult to match in isolated on-premises environments. This matters more as employers operate across multiple locations and need consistent workflows for signing, retrieval, and policy distribution. The cloud position is therefore not only a cost decision, but also a response to speed, administrative simplicity, and regulatory change.

Hybrid deployment is projected to grow at a 12.78% CAGR through 2031, making it the fastest-growing model in the HR document management and eSignature market. Many enterprises are keeping historical personnel archives on-premises while routing active workflows, such as offers, onboarding packets, and policy acknowledgments, through cloud systems. That structure is becoming a deliberate long-term design choice rather than a temporary migration stage, especially in regulated settings. aconso’s work on AWS's European Sovereign Cloud highlights why the HR document management and eSignature market is increasingly linking deployment choice to sovereignty, residency, and operational control rather than a simple cloud-versus-on-premises debate.

By Organization Size: Large Enterprises Provide Scale While SMEs Expand Faster

Large enterprises accounted for 71.29% of revenue in 2025, giving them the leading market share by organization size in the HR document management and eSignature market. This reflects the fact that large employers manage higher hiring volumes, more countries, more document classes, and deeper integration needs than smaller firms. Their HR teams often require role-based access, jurisdiction-specific retention, audit trails, and automated purge controls, all of which support premium platform spending. In the HR document management and eSignature market, these needs also make vendor switching more difficult once the platform is embedded in daily HR operations.

SMEs are projected to grow at a 13.29% CAGR through 2031, making them the fastest-expanding buyer group in the HR document management and eSignature market. Lower SaaS entry costs are making purpose-built document tools more accessible to smaller companies that previously relied on email attachments, paper records, or generic cloud drives. PandaDoc said in December 2025 that it serves more than 60,000 organizations globally, underscoring the scale to which value-oriented automation platforms are reaching smaller and mid-sized employers.[2]PandaDoc, “What’s New in PandaDoc, December 2025,” PandaDoc, pandadoc.com The growth path for this part of the HR document management and eSignature market is also supported by the fact that smaller firms face meaningful risk from even a single compliance failure and therefore have growing reasons to adopt structured HR document workflows.

By Industry Vertical: IT and Telecom Leads While Healthcare Moves Up

Information technology and telecommunications accounted for 30.29% of revenue in 2025, making it the largest vertical in the HR document management and eSignature market. The sector adopted early because its employers are already comfortable with cloud-native systems, API-based connectivity, and remote work structures that depend on digital documentation. Frequent hiring cycles, large volumes of employment contracts, and widespread use of non-disclosure agreements also support stronger recurring demand. Within the HR document management and eSignature industry, this vertical remains important because it sets the pace for integration expectations and workflow design.

Healthcare and life sciences are projected to grow at 11.86% CAGR through 2031, the fastest rate among industry verticals in the HR document management and eSignature market. Growth requires managing clinical credentialing, employee records, and regulated signatures within a single workflow environment. This creates a more complex operational need than standard employment paperwork and favors vendors that can manage identity, documentation, and compliance together. The HR document management and eSignature market is therefore seeing stronger demand from healthcare buyers who want purpose-built controls rather than generic signing tools.

Geography Analysis

North America accounted for 36.41% of global revenue in 2025, making it the largest regional contributor to the HR document management and eSignature market. The region benefits from mature cloud HR infrastructure, high familiarity with e-signature workflows, and strong adoption of integrated talent management platforms. In the United States, changes to Form I-9 preserved the remote document examination option for eligible employers while imposing tighter procedural requirements, which directly support demand for structured digital document workflows. USCIS also continues to detail the optional alternative procedure for remote document examination, which reinforces the need for verifiable digital processes rather than informal manual workarounds. Canada is seeing demand driven by provincial employment variations and documentation complexity, while Mexico is seeing adoption rise among multinational subsidiaries that need stronger cross-border workforce compliance.

Europe was the second-largest regional market by revenue in 2025 and remains the most regulation-heavy environment in the HR document management and eSignature market. Regulation (EU) 2024/1183 established a firm timetable for the availability of national digital identity wallets, pushing vendors to align employment signing workflows with the new framework.[3]European Commission, “Regulation (EU) 2024/1183, European Digital Identity Framework,” European Commission, ec.europa.eu Commission Implementing Regulation (EU) 2026/248 added technical specificity to the formats that public-sector bodies must recognize for advanced electronic signatures and seals, thereby increasing the precision required of platform providers. Germany’s works council approval requirements and similar labor governance structures in other European markets continue to slow deployment speed even as demand remains solid.

Asia-Pacific is projected to grow at 12.33% CAGR through 2031, the fastest regional pace in the HR document management and eSignature market. The region is benefiting from workforce expansion, stronger multinational hiring activity, and national digital identity systems that support online verification and signing. India is particularly important because its eSign environment gives HR platforms a practical way to reduce onboarding cycle time at scale, while South Korea and other digitally active economies continue to support cloud-based HR administration. The Middle East and Africa are still smaller in revenue terms, but sovereign digital transformation programs in markets such as the UAE and Saudi Arabia are opening new demand paths for workforce documentation tools. South America remains centered on Brazil and Argentina, where large enterprise adoption in banking and retail supports revenue, though inflationary pressures and uneven digital identity infrastructure continue to limit broader acceleration.

Competitive Landscape

The global HR document management and eSignature market remains moderately fragmented, with DocuSign holding the strongest enterprise visibility while mid-tier vendors and regional specialists compete through integration, compliance design, and local trust capabilities. The competitive landscape shows a clear split between broad-agreement platforms and more HR-focused providers that emphasize employee records, retention logic, and jurisdiction-specific workflows. This structure leaves room for leaders to scale through brand and ecosystem reach, while also allowing smaller specialists to defend positions in tightly regulated use cases. In 2026, the main point of competition in the HR document management and eSignature market is moving toward AI-assisted workflow handling, identity assurance, and deeper embedding inside HR systems. Buyers are increasingly comparing vendors on how well they support the full employment lifecycle rather than just the signing process.

DocuSign strengthened that position in May 2026 when it unveiled its AI Assistant and Agents suite together with IAM for HR, which added mobile I-9 verification and deeper HCM workflow support. OneSpan also moved to reinforce its trust and security position when it reported the acquisition of Build38 in its first-quarter 2026 financial results, a step aimed at stronger mobile protection and in-app defense.[4]OneSpan Inc., “OneSpan Reports First Quarter 2026 Financial Results,” OneSpan, investors.onespan.com aconso added another competitive marker in May 2026 when it became a Workday partner, extending automated document creation, management, and archiving across core Workday HCM modules. These moves show that the HR document management and eSignature market is no longer competing only on signature execution, but is instead competing on how deeply the platform integrates into hiring, onboarding, and document governance workflows.

A second line of competition is developing around regional compliance and digital identity infrastructure in Europe, where local trust services and hosting expectations carry greater weight. That benefits providers built around eIDAS-aligned workflows and national eID integrations, because those features are harder for foreign incumbents to replicate quickly. At the same time, the HR document management and eSignature market still has visible white space in SME-focused multi-jurisdiction compliance and in identity-first workflows for deskless and shared-device workers. The result is a market where leadership is clear at the top, but differentiation remains strong enough for specialized vendors to grow without directly matching the scale of the largest platform.

HR Document Management and ESignature Industry Leaders

DocuSign, Inc.

PandaDoc, Inc.

OneSpan Inc.

Nitro Software, Inc.

Scrive AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DocuSign unveiled its AI Assistant and Agents suite alongside IAM for HR, a product that integrates AI-powered mobile I-9 verification, automated field population from HCM data, and direct synchronization with HR systems. IAM for HR entered early access in the United States beginning June 2026, targeting the full employee lifecycle from hiring through offboarding.

- May 2026: aconso AG was named a Workday Partner, enabling organizations to create, manage, and archive personnel documents across Workday HCM modules, including Core HCM, Talent Management, and Experience and Engagement. The partnership addressed a known gap in Workday's native document management capabilities, particularly for EU GDPR-compliant retention workflows.

- March 2026: DocuSign introduced an AI-powered contract review assistant built on its Iris agreement AI engine and IAM platform, enabling legal teams to review and surface key terms across HR, sales, and procurement agreements within a single workflow.

- February 2026: The European Commission adopted Implementing Regulation (EU) 2026/248, standardizing the formats of advanced electronic signatures and seals that EU public-sector bodies must recognize for cross-border administrative and employment workflows, with full technical specification applicability from February 2027.

Global HR Document Management and ESignature Market Report Scope

The HR Document Management and eSignature Market encompasses software solutions that enable organizations to create, store, manage, and securely sign HR-related documents in digital formats. These platforms support document lifecycle management, workflow automation, audit trails, and legally compliant electronic signatures. They facilitate paperless HR operations and improve efficiency in processes such as onboarding, contract management, and policy documentation. The market addresses the need for secure, scalable, and compliant document handling within HR environments.

The HR Document Management and eSignature Market Report is Segmented by Component (Software [Document Creation and Template Management Systems, Employee Records and Digital File Management Platforms, Document Storage, Retrieval and Archiving Systems, Secure Document Signing and Encryption Solutions, and Other Software], and Services [Implementation and Integration Services, and Consulting and Advisory Services]), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Banking, Financial Services and Insurance, Information Technology and Telecommunications, Healthcare and Life Sciences, Government and Public Sector, Retail and E-commerce, Manufacturing, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Document Creation and Template Management Systems |

| Employee Records and Digital File Management Platforms | |

| Document Storage, Retrieval and Archiving Systems | |

| Secure Document Signing and Encryption Solutions | |

| Other Software | |

| Services | Implementation and Integration Services |

| Consulting and Advisory Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Retail and E-commerce |

| Manufacturing |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Document Creation and Template Management Systems |

| Employee Records and Digital File Management Platforms | ||

| Document Storage, Retrieval and Archiving Systems | ||

| Secure Document Signing and Encryption Solutions | ||

| Other Software | ||

| Services | Implementation and Integration Services | |

| Consulting and Advisory Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Industry Vertical | Banking, Financial Services and Insurance | |

| Information Technology and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the HR document management and eSignature space?

The HR document management and eSignature market is valued at USD 8.07 billion in 2026 and is forecast to reach USD 13.89 billion by 2031 at an 11.47% CAGR.

Which component currently leads revenue generation?

Software led the revenue mix with 69.44% in 2025, reflecting the strong role of document creation, file management, storage, and signing platforms.

Which deployment model is growing the fastest?

Hybrid deployment is projected to expand at 12.78% CAGR through 2031 because many employers are keeping legacy archives on premises while shifting active workflows to cloud systems.

Why are large enterprises still the biggest buyers?

Large enterprises held 71.29% of revenue in 2025 because they manage more hiring volume, more countries, more retention rules, and more integration points than smaller employers.

Which region is expanding the quickest through 2031?

Asia-Pacific is forecast to grow at 12.33% CAGR through 2031, supported by workforce expansion, multinational hiring, and digital identity infrastructure.

Which end-user vertical is showing the strongest growth outlook?

Healthcare and life sciences is expected to advance at 11.86% CAGR through 2031 as employers in this vertical manage both workforce records and clinical credentialing requirements.

Page last updated on: