HR Service Delivery Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.45 Billion |

| Market Size (2031) | USD 38.88 Billion |

| Growth Rate (2026 - 2031) | 10.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Service Delivery Platform Market Analysis by Mordor Intelligence

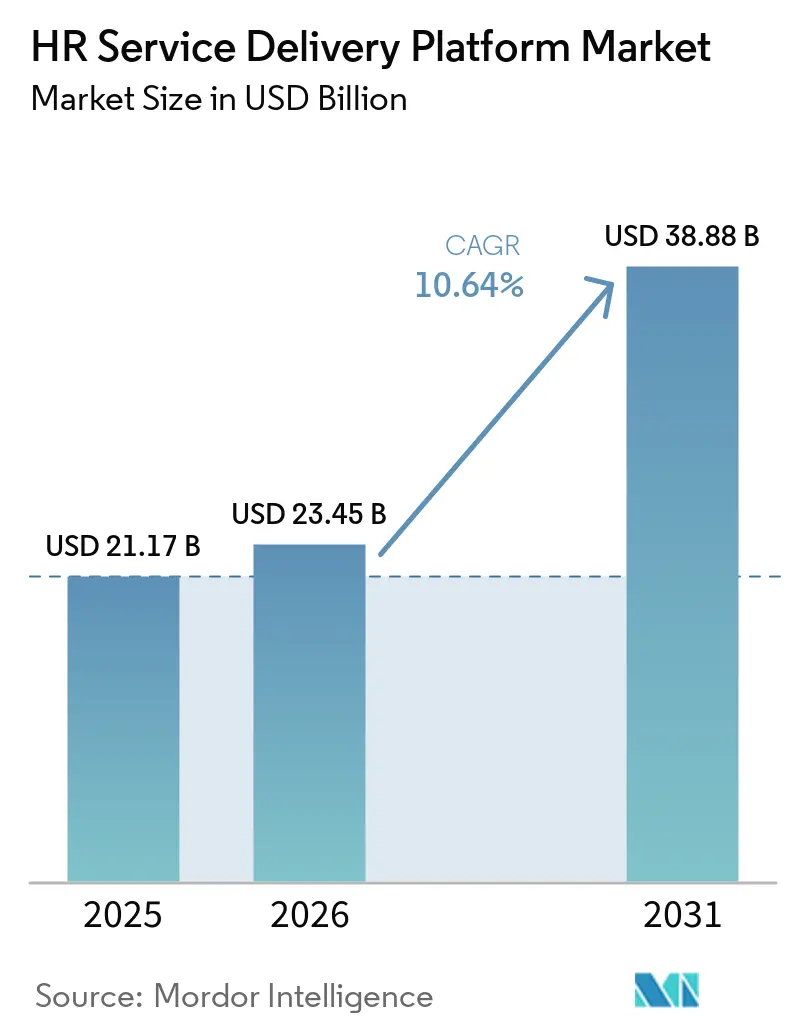

The HR service delivery platform market size is expected to increase from USD 21.27 billion in 2025 to USD 23.45 billion in 2026 and reach USD 38.88 billion by 2031, growing at a CAGR of 10.64% over 2026-2031. The HR service delivery platform market is expanding as employers move away from separate tools for personnel administration, case management, payroll, workforce analytics, and talent workflows, and adopt unified systems that support AI-enabled processes and tighter operational control. Regulatory pressure is also making platform adoption more durable, especially as employers prepare for pay transparency reporting, tighter AI governance in employment decisions, and stronger auditability expectations across regions. Cloud migration remains central to this shift because aging HR and ERP environments now expose security, integration, and compliance gaps that modern platforms are built to address. Competitive behavior in the HR service delivery platform market is increasingly shaped by platform expansion, AI feature releases, sovereign cloud investments, and acquisitions that help vendors widen their suite coverage or deepen workflow ownership. The strongest near-term opportunity lies where employers need both operational efficiency and regulatory readiness, particularly in large, multi-country workforces, healthcare settings, and growing mid-market organizations that want enterprise-grade capabilities without the enterprise-scale implementation complexity.

Key Report Takeaways

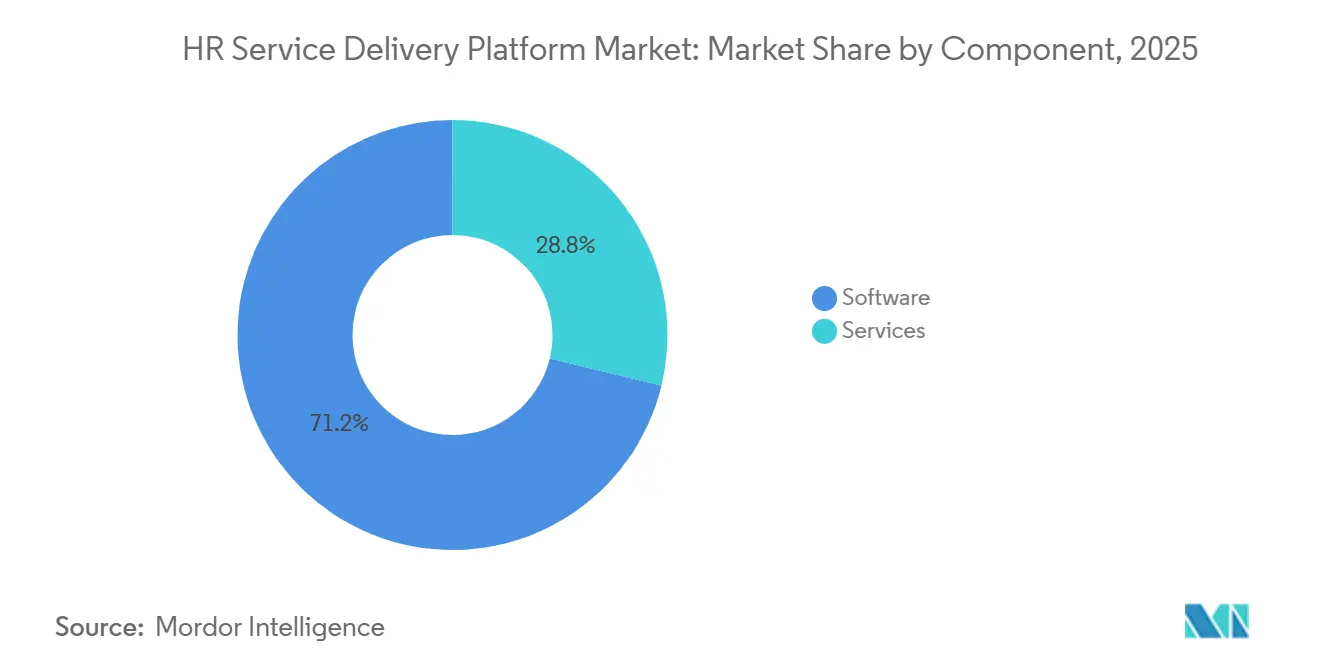

- By component, software accounted for 71.21% of the HR service delivery platform market size in 2025, while services are projected to expand at a 12.43% CAGR through 2031.

- By deployment model, cloud-based deployment held 64.90% share in 2025, while hybrid is expected to grow at an 11.87% CAGR through 2031.

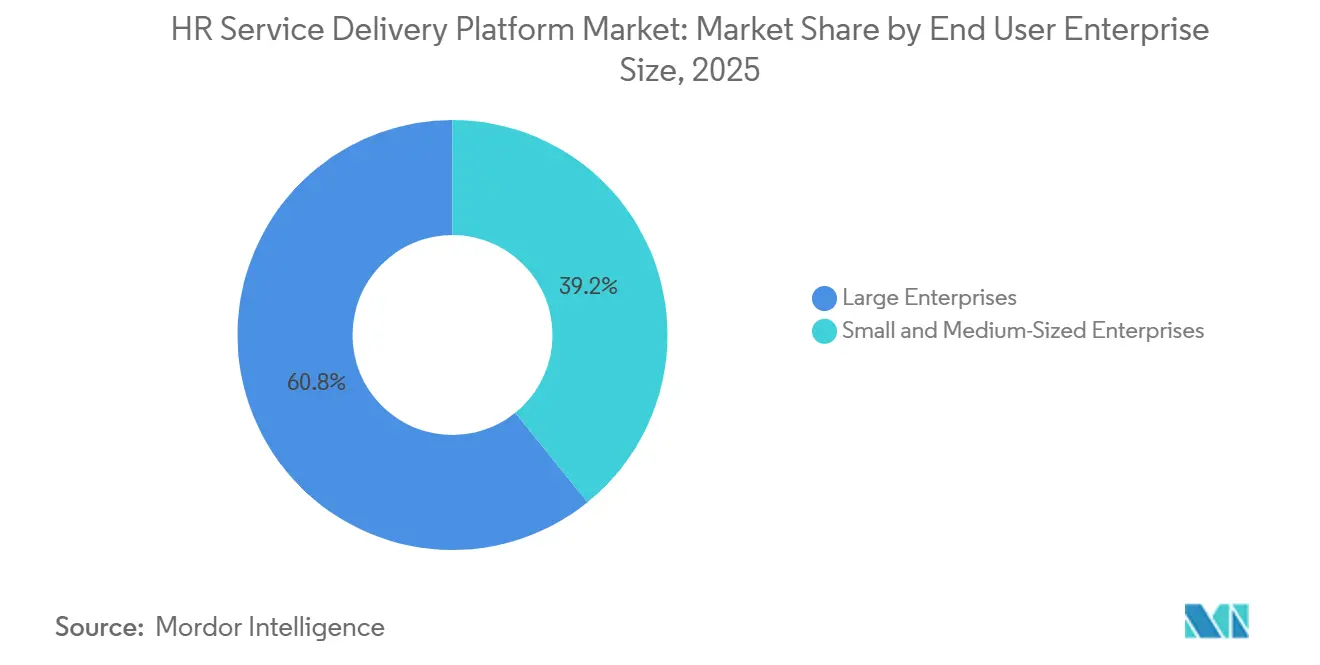

- By enterprise size, large enterprises held 60.81% of the HR service delivery platform market share in 2025, while SMEs are projected to advance at a 13.12% CAGR through 2031.

- By end-user industry, information technology and telecom accounted for 28.62% in 2025, while healthcare and life sciences are expected to expand at a 12.78% CAGR through 2031.

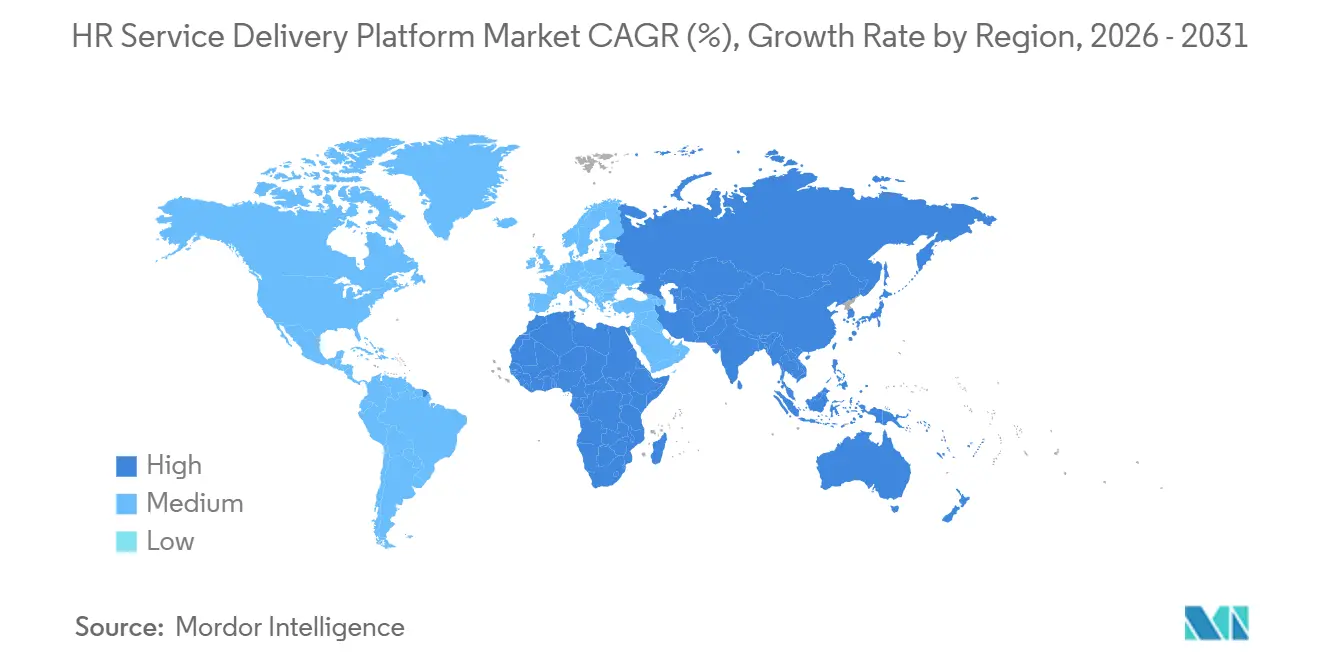

- By geography, North America held 41.71% of the HR service delivery platform market in 2025, while Asia-Pacific is projected to grow at a 15.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Service Delivery Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Migration from Legacy Human Resources Stacks | +2.8% | Global | Short term (≤ 2 years) |

| Rising Demand for Unified Employee Self-Service and Case Management | +2.4% | Global | Short term (≤ 2 years) |

| Need for Real-Time Workforce Analytics And Workflow Automation | +1.9% | Global | Medium term (2-4 years) |

| Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints | +1.5% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| European Union Pay Transparency Directive Forcing Harmonized Job and Pay Data | +0.9% | Europe, spill-over to North American and APAC multinationals | Short term (≤ 2 years) |

| Skills-Based Workforce Planning and Internal Talent Mobility | +0.7% | North America, Europe, APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration from Legacy Human Resources Stacks

Cloud migration in the HR service delivery platform market has moved beyond a cost discussion and now sits at the center of operating resilience. Strada reported in July 2025 that nearly 40% of businesses still ran aging on-premise HR and ERP systems, and that budget limits and integration complexity each affected 42% of transformation plans. That finding matters because delayed migration now carries a larger penalty, especially after SAP ECC reached end-of-life in December 2025 and Microsoft Dynamics GP moved toward support expiry in 2029, which raises security and capability risk for organizations that stay on older stacks. The U.S. federal government reinforced this direction when OPM and OMB announced Federal HR 2.0, a program that begins in fiscal 2026 and aims to consolidate more than 100 legacy HR systems onto a single commercial platform. ISG also projected that 83% of companies will have SaaS or hybrid cloud at the core of their HR technology by the end of 2027, suggesting that the migration window in the HR service delivery platform market is narrowing quickly. Vendors that can shorten deployment time and show operational gains, not just license savings, are therefore in a stronger position across the HR service delivery platform market.[1]Cisco, “Cisco Global Hybrid Work Study 2025,” Cisco Newsroom, cisco.com

Rising Demand for Unified Employee Self-Service And Case Management

The HR service delivery platform market is also being pushed by frustration with fragmented HR helpdesk models and slow employee support workflows. McKinsey reported in 2025 that only 19% of core HR processes in Europe had been enhanced with generative AI, while another 32% remained in pilot stages, leaving a large room for platforms that can automate routing, search, and resolution at scale. The same demand is evident in service organization design, where specialized HR shared-services centers remain underused, meaning many companies have not yet captured the efficiency gains from centralizing service delivery on a common platform. UKG showed the value of this model in healthcare, where its Rapid Hire capability automated up to 90% of repetitive hiring tasks, reduced time-to-hire by 10 days, and tripled apply-to-hire conversion rates for customers operating under acute staffing pressure. As a result, the HR service delivery platform market is seeing stronger demand for platforms that combine employee self-service, case management, knowledge access, and workflow automation into a single operating layer.

Need For Real-Time Workforce Analytics And Workflow Automation

Real-time analytics and workflow automation are turning into baseline buying criteria in the HR service delivery platform market. ISG reported that average HR-AI budgets stood at USD 1.6 million in 2026, which was 10 times the 2023 level, and that production HR AI use cases had doubled to more than 30%, led by onboarding automation, HR document creation, and AI-assisted job postings. Value now depends less on isolated dashboards and more on how well analytics are linked to actions inside workflows, because integrated ecosystems delivered twice the ROI of siloed setups in the same survey. Finch added another sign of the same problem in early 2025 when it found that 1 in 8 employers still spent more than 4 hours each week on manual HR data entry because systems were not properly connected. BCG later argued that HR and shared services are among the earliest and most productive settings for agentic AI, especially when employers first remove spreadsheet workarounds, disconnected systems, and poor data hygiene, thereby strengthening the long-term demand path for the HR service delivery platform market.

Hybrid And Distributed Work Models Expanding Digital Human Resources Touchpoints

The HR service delivery platform market continues to benefit from the permanent expansion of digital HR touchpoints created by hybrid and distributed work. Cisco found in 2025 that only 49% of employees felt workflows were seamless across locations, while 93% of employers were investing in AI and collaboration technologies to close that gap. That operating model increases compliance complexity because teams spread across many jurisdictions create payroll tax, labor law, and data transfer obligations that older, centralized systems were not designed to manage effectively. Employers, therefore, need platforms that can handle local rules, policy updates, and cross-border controls natively, rather than through layers of middleware or manual workarounds. CIPD also reported in 2025 that 15% of organizations planned to invest more in technology specifically to support hybrid or home working within 12 months, with technology quality and quantity ranked as the top spending priorities. This keeps the HR service delivery platform market closely tied to broader workforce digitalization programs across North America, Europe, and, increasingly, Asia-Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cross-Border Employee Data Controls | -1.5% | Global, peak severity in EU and EEA | Short term (≤ 2 years) and Medium term (2-4 years) |

| Integration Complexity with Legacy Enterprise Resource Planning and Payroll Systems | -1.3% | Global, concentrated in large enterprise and public sector | Medium term (2-4 years) |

| European Union Artificial Intelligence Act and Algorithmic Accountability for Employment Decisions | -0.8% | Europe, spill-over to global multinationals with EU workforces | Medium term (2-4 years) |

| Data Sovereignty and Regional Hosting Requirements | -0.6% | Europe, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Cross-Border Employee Data Controls

Privacy and cross-border transfer rules remain one of the clearest brakes on the HR service delivery platform market. The challenge is no longer limited to legal review because multinational employers now need standard contractual clauses, transfer impact assessments, and sub-processor governance embedded directly into platform operations.[2]European Data Protection Board, “Europrivacy as a Data Transfer Mechanism,” iGDPR, igdpr.eu The EDPB approved Europrivacy in April 2026 as the first certification-based mechanism for international data transfers under Articles 42 and 46 of the GDPR, creating a new compliance path that vendors must support alongside older transfer frameworks. Procurement effects are already visible because buyers in healthcare, financial services, and the public sector increasingly favor vendors with EU-based infrastructure and stronger local residency controls. In markets such as Germany, France, and the Benelux, due diligence under GDPR Article 28 is also pushing evaluations toward vendors that can demonstrate local hosting and clearer accountability across data-handling chains, narrowing the flexibility of globally standardized platforms in the HR service delivery market.

Integration Complexity with Legacy Enterprise Resource Planning and Payroll Systems

Integration with legacy ERP and payroll systems continues to slow adoption across the HR service delivery platform market, especially in large enterprises and the public sector. Reported in March 2025, integration capability was identified as the single most influential factor in HR software buying decisions, ahead of pricing, and disconnected HR systems were estimated to create more than USD 8 billion in annual operating costs for employers. The same issue is hard to solve structurally because the top 10 payroll providers covered only 62% of the U.S. market, so each unsupported provider can still block or delay a deal for a platform that lacks broad connector coverage. Findings also showed that both budget constraints and integration complexity affected 42% of large enterprises planning an HCM transformation, demonstrating that technical friction and change management pressure often go hand in hand. In this setting, vendors in the HR service delivery platform market gain an advantage by offering pre-built connectors for SAP, Oracle, and Microsoft environments rather than relying on custom middleware projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leadership Holds While Services Scale With Deployment Complexity

Software accounted for 71.21% of the HR service delivery platform market in 2025, which shows that recurring licenses remain the core commercial engine for the category. In the HR service delivery platform industry, buyers increasingly want core HR, employee service management, payroll, workforce management, talent tools, analytics, and learning, all connected within one suite rather than stitched together as separate products. That preference supports a model where continuous AI releases, compliance updates, and module expansion reinforce renewal and cross-sell activity over time. The result is that software continues to dominate the HR service delivery platform market, even as customers debate how far they should consolidate under a single vendor.

Services are projected to grow at a 12.43% CAGR through 2031, making it the faster-growing component, even though it starts from a smaller base. This does not weaken the software case because implementation, managed services, and compliance advisory demand tend to rise as platforms become broader and more embedded in daily operations. Vendor support, client success programs, and managed services are becoming central to value realization for SMB HCM buyers, which aligns with this direction. The HR service delivery platform market size for software remains larger, but the services layer is becoming more durable because customers need help with rollout, integration, and policy alignment as the operating model grows more complex.

By Deployment Model: Cloud Remains The Core Choice While Hybrid Gains In Regulated Settings

Cloud-based deployment accounted for 64.90% of the HR service delivery platform market in 2025, reflecting lower infrastructure costs, faster feature delivery, and easier policy updates across distributed workforces. That position aligns with the wider shift in the HR service delivery platform market toward hosted environments that support analytics, self-service, and continuous configuration change without on-premises overhead. Workday reinforced this direction in November 2025 when it launched Workday EU Sovereign Cloud with full EU data residency and EU-based operations, showing that vendors are addressing regulatory concerns inside the cloud model rather than stepping away from it. OPM and OMB also signaled the same transition when Federal HR 2.0 set out to move more than 100 legacy federal systems onto a commercial platform by fiscal 2028.

Hybrid deployment is forecast to grow at a 11.87% CAGR through 2031, indicating that some employers still need a mixed architecture for compliance and control. Financial services, healthcare, and government buyers often want cloud agility for self-service and analytics while keeping selected payroll or personnel data in locally controlled environments. That pattern means hybrid growth in the HR service delivery platform market is not a sign of cloud hesitation, but a response to residency rules and internal risk policy. The HR service delivery platform industry, therefore, continues to favor cloud-first design, while hybrid architecture expands where legal and operating conditions require more segmented deployment choices.[3]Workday, “Workday Launches Workday EU Sovereign Cloud to Unlock Enterprise AI With Full EU Data Residency and Control,” Workday Newsroom, workday.com

By End User Enterprise Size: Large Enterprises Lead Revenue While SMEs Gain Speed

Large enterprises held 60.81% of the HR service delivery platform market share in 2025, reflecting the weight of global workforces, higher process complexity, and deeper HCM integration into ERP environments. These customers usually have longer buying cycles and heavier governance requirements, but they also create stable multi-module contracts that shape the enterprise tier of the HR service delivery platform market. Demand in this group remains tied to case management, payroll coordination, analytics, and compliance control across many jurisdictions. That keeps large enterprises at the center of spending even as growth shifts elsewhere.

SMEs are projected to grow at a 13.12% CAGR through 2031, making them the fastest-growing segment in the HR service delivery platform market. HR and shared services were noted in late 2025 as among the earliest productive settings for agentic AI, a point that matters strongly for smaller companies that must automate because HR headcount is limited. A 2026 peer-reviewed study found that cloud-based HRM platforms improved data accuracy, appraisal reliability, and operational responsiveness in SME environments. Research also highlighted that unifying payroll, HR, and talent processes in a single system was the leading SMB priority, supporting modular, usage-based platforms with short deployment cycles. The HR service delivery platform market for SMEs is therefore gaining momentum, as buyers seek enterprise-grade analytics and automation without the time and cost profile of large-scale transformation programs.

By End-User Industry: IT And Telecom Leads While Healthcare And Life Sciences Accelerates

Information technology and telecom accounted for 28.62% of the HR service delivery platform market size in 2025, supported by large digital workforces, mature SaaS usage, and steady demand for advanced analytics and skills-based management. This vertical has been an early adopter in the HR service delivery platform market because buyers already operate in cloud-centered environments and are more willing to expand into AI-enabled planning and service workflows. Current demand is concentrated on organizational analytics, talent visibility, and automation that improves speed without creating more administrative layers. That combination helps IT and telecom remain the largest end-user industry by revenue.

Healthcare and life sciences are forecast to grow at a 12.78% CAGR through 2031, which makes it the fastest-growing vertical in the HR service delivery platform market. The growth path is tied to credential complexity, shift-based scheduling, mobile access needs, and higher burnout-driven turnover, all of which stretch the limits of generic HCM designs. In 2026, 83% of healthcare workers in acute settings and 82% in non-acute settings reported feeling burnt out at least sometimes, indicating a clear operating pain point tied to staffing and scheduling. A major public system also selected a workforce management solution covering the full employee lifecycle, showing how large healthcare organizations are moving from custom HR tools toward commercial platforms with stronger compliance support. Across the HR service delivery platform market, healthcare stands out because workflow design and compliance depth matter as much as broad HCM coverage.

Geography Analysis

North America held 41.71% of the HR service delivery platform market share in 2025, which made it the leading regional revenue base. The United States accounted for most of that demand because enterprise SaaS adoption remained above global averages and large employers continued to modernize workforce systems at scale. Federal HR 2.0 became the clearest public signal of this trend when OPM and OMB set out to consolidate more than 100 agency HR systems onto a single commercial HCM platform, with a 10-year contract expected to exceed USD 1 billion. Canada introduces a new source of demand, as 13 provinces and territories create a multi-jurisdictional compliance burden that favors platforms with automated legislative updates and stronger payroll alignment. Mexico also supports the HR service delivery platform market through manufacturing growth and cross-border workforce administration needs, especially in high-volume hourly labor settings.

Europe remains one of the most regulation-heavy parts of the HR service delivery platform market, and that complexity is also becoming a strong commercial driver. Directive (EU) 2023/970 required member states to transpose the Pay Transparency Directive by June 7, 2026, which pushed employers to harmonize job structures and combine HR and payroll data for reporting. Employers with 250 or more workers will begin annual gender pay gap reporting in 2027 based on 2026 data, which tightened the system-readiness window for platform deployment. Germany, the United Kingdom, France, and the Netherlands remain the largest revenue markets in the region, while local hosting and GDPR readiness increasingly shape vendor selection. Russia also maintains a more restricted profile because Federal Law No. 242-FZ mandates data localization as a core requirement, limiting the scope for global cloud deployment models.

Asia-Pacific is projected to grow at a 15.21% CAGR through 2031, making it the fastest-growing geography in the HR service delivery platform market. Growth in this region comes from multinational expansion, faster digitization among mid-sized employers, and the rise of local vendors that handle country-specific rules better than global suites in some use cases. China illustrates that pattern through platforms such as Kingdee AI HR and Yonyou, which are built around local labor, tax, and social insurance requirements. India has also become more important after Darwinbox raised USD 140 million in March 2025 and shifted its headquarters to Singapore as part of a broader international scale-up. Japan added another clear signal in April 2026 when SmartHR passed 80,000 registered companies and secured its seventh consecutive year as the leading labor-management cloud vendor, which shows that the HR service delivery platform market in Asia-Pacific is not defined by global incumbents alone.[4]SmartHR, “SmartHR Achieves 7 Consecutive Years as Market Share No. 1, Surpassing 80,000 Registered Companies,” SmartHR, smarthr.jp

Competitive Landscape

The HR service delivery platform market is fragmented in the enterprise tier, where Workday, Oracle, ADP, SAP SuccessFactors, and UKG remain the most visible names in large-account evaluations. At the same time, the market stays fragmented in the mid-market and SME layers, where HiBob, Rippling, Personio, Darwinbox, and Deel each hold narrower positions by geography, use case, or customer size. This split structure matters because leadership in Fortune 500 procurement does not automatically convert into control of the broader revenue pool. It also explains why the market keeps showing both platform consolidation and new specialist entry at the same time.

Product strategy has shifted from pure feature competition toward broader workflow control. Workday moved early in this cycle when it launched Sana in March 2026 and then expanded its Google Cloud partnership in May 2026 to embed Sana in daily employee workflows, extending Workday beyond a stand-alone HR system into a broader enterprise intelligence layer. Oracle followed with Fusion Agentic Applications for HR in April 2026, embedding 8 specialized AI agents and a Workforce Operations Command Center into Oracle Fusion Cloud HCM. UKG also sharpened its positioning in May 2026 by launching UKG Pro Pay with Workforce AI, which uses agentic AI to detect and resolve payroll anomalies in real time. These moves show that vendors are trying to own decision support, not just transaction processing, and they raise the competitive bar for smaller vendors that still rely on narrow module differentiation.

M&A and adjacent platform expansion remain important because buyers increasingly prefer fewer systems with broader native coverage. Paylocity added to that pattern in April 2026 by acquiring Grayscale Labs to strengthen AI-driven recruiting automation for high-volume hiring. Dayforce also pushed deeper into workforce planning through its Agentnoon acquisition and product integration, turning skills-based planning into an operational capability within its broader platform. White-space demand remains strongest in vertical workflows such as healthcare, manufacturing, and government, as well as in global payroll infrastructure, where ownership of underlying payroll rails is becoming strategically valuable. That leaves the market open to further consolidation, even though regional and workflow specialists still have room to grow where localization or industry depth matters more than full-suite breadth.

HR Service Delivery Platform Industry Leaders

Workday, Inc.

Ultimate Kronos Group, Inc.

Automatic Data Processing, Inc.

Paycom Software, Inc.

Dayforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Workday and Google Cloud expanded their strategic partnership to embed Workday's Sana Self-Service Agent in Gemini Enterprise, enabling employees to complete HR and finance tasks without switching applications. The partnership creates a zero-copy data integration between Workday Data Cloud and Google Cloud Lakehouse, enabling deeper cross-system workforce analytics.

- May 2026: SAP announced that Tata Consultancy Services (TCS) had successfully migrated its global payroll operations to SAP S/4HANA Cloud on AWS, consolidating multi-country payroll through more than 20 high-volume interfaces and establishing a scalable digital foundation for adaptive workforce operations.

- May 2026: UKG launched UKG Pro Pay with Workforce AI at Payroll Congress 2026, embedding Payroll Auditing AI, Anomaly Detection AI, and an AI Payroll Analyst Agent to detect and resolve payroll errors in real time, targeting the 2-4% payroll leakage.

- May 2026: Paychex launched the WISE AI Platform, an agentic intelligence layer spanning Paychex Flex, Paycor, and SurePayroll, providing AI agents, expert advisory, embedded intelligence, and personal assistants across the full HR and payroll lifecycle for SMB customers.

Global HR Service Delivery Platform Market Report Scope

The HR Service Delivery Platform market refers to integrated software and service solutions that centralize and streamline human resource operations across organizations. These platforms encompass core HR functions, employee service management and helpdesk, payroll and compensation, workforce management, talent management, people analytics and reporting, and learning and development. Delivered through cloud-based, on-premises, and hybrid deployment models, they serve both large enterprises and SMEs across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The primary purpose of this market is to enhance HR efficiency, reduce administrative overhead, improve employee engagement, ensure compliance, and provide data-driven insights that support workforce productivity and organizational growth.

The HR Service Delivery Platform market report is segmented by Component (Software, [Core Human Resources, Employee Service Management and Helpdesk, Payroll and Compensation, Workforce Management, Talent Management, People Analytics and Reporting, Learning and Development] and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa), The Market Forecasts are Provided in Terms of Value (USD).

| Software | Core Human Resources |

| Employee Service Management and Helpdesk | |

| Payroll and Compensation | |

| Workforce Management | |

| Talent Management | |

| People Analytics and Reporting | |

| Learning and Development | |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Core Human Resources |

| Employee Service Management and Helpdesk | ||

| Payroll and Compensation | ||

| Workforce Management | ||

| Talent Management | ||

| People Analytics and Reporting | ||

| Learning and Development | ||

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future size of the HR service delivery platform space?

The HR service delivery platform market was valued at USD 21.27 billion in 2025, reached USD 23.45 billion in 2026, and is forecast to reach USD 38.88 billion by 2031 at a 10.64% CAGR.

Which deployment model is most widely used today?

Cloud-based deployment led with a 64.90% share in 2025 because employers want faster feature delivery, lower infrastructure burden, and easier compliance updates.

Which customer segment is growing the fastest?

SMEs are projected to grow at a 13.12% CAGR through 2031 as modular, usage-based platforms make advanced HR tools more accessible to smaller organizations.

Which end-user vertical creates the strongest demand right now?

Information technology and telecom led with 28.62% in 2025, while healthcare and life sciences is growing faster at a 12.78% CAGR because of staffing, scheduling, and credentialing pressure.

Why is Asia-Pacific expanding faster than other regions?

Asia-Pacific is forecast to grow at a 15.21% CAGR through 2031 due to mid-market digitization, multinational expansion, and strong local vendors such as SmartHR and regional HR SaaS providers.

What are the main barriers that slow platform adoption?

Data privacy controls and integration complexity remain the largest barriers because multinational employers need stronger transfer compliance, while many organizations still struggle to connect legacy ERP and payroll systems.

Page last updated on: