Managed HR Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

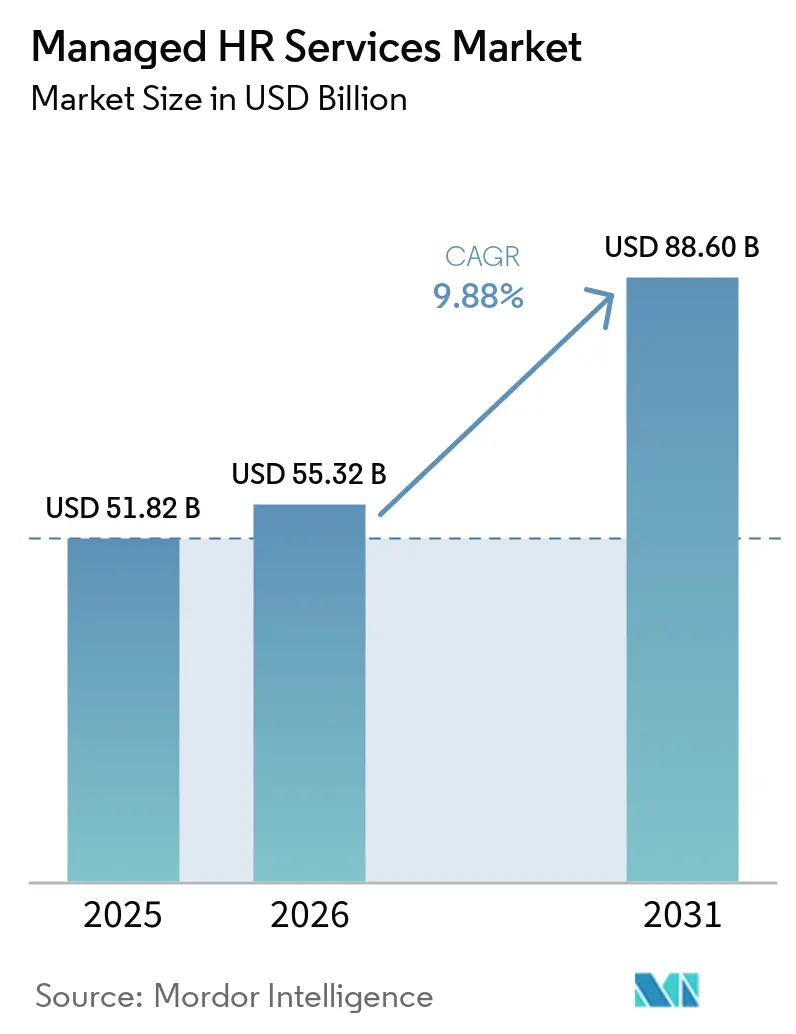

| Market Size (2026) | USD 55.32 Billion |

| Market Size (2031) | USD 88.60 Billion |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

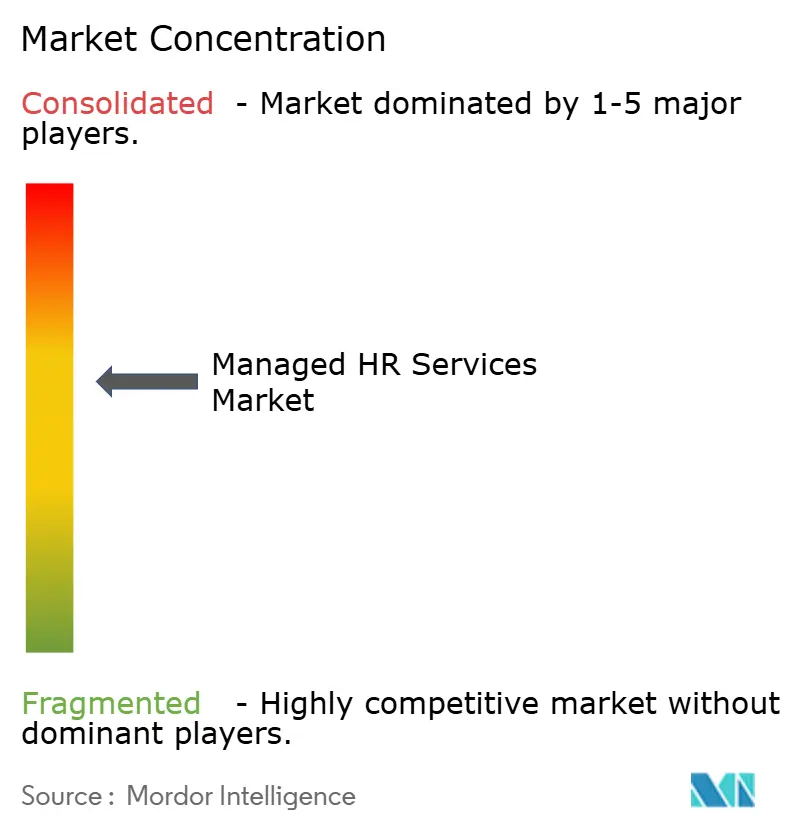

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed HR Services Market Analysis by Mordor Intelligence

The managed HR services market size is projected to expand from USD 51.82 billion in 2025, USD 55.32 billion to USD 88.60 billion by 2031, registering a CAGR of 9.88% during 2026-2031. Growth is being supported by multinational companies outsourcing non-core HR work while internal teams focus more on talent planning, workforce policy, and business support. Labor compliance has become harder to manage across multiple countries, which keeps demand firm for providers that can standardize payroll, benefits, and employee administration at scale. AI-led automation is also changing how the managed HR services market operates, because providers can now reduce manual effort in payroll checks, leave administration, employee service requests, and exception handling. Competition is shifting as buyers place greater weight on measurable outcomes, reliability of compliance, and workforce insight than on labor costs alone. Security incidents and difficult migrations from legacy platforms remain important risks, which means vendors that can offer stronger data protection and cleaner transition paths are better placed to win renewals.

Key Report Takeaways

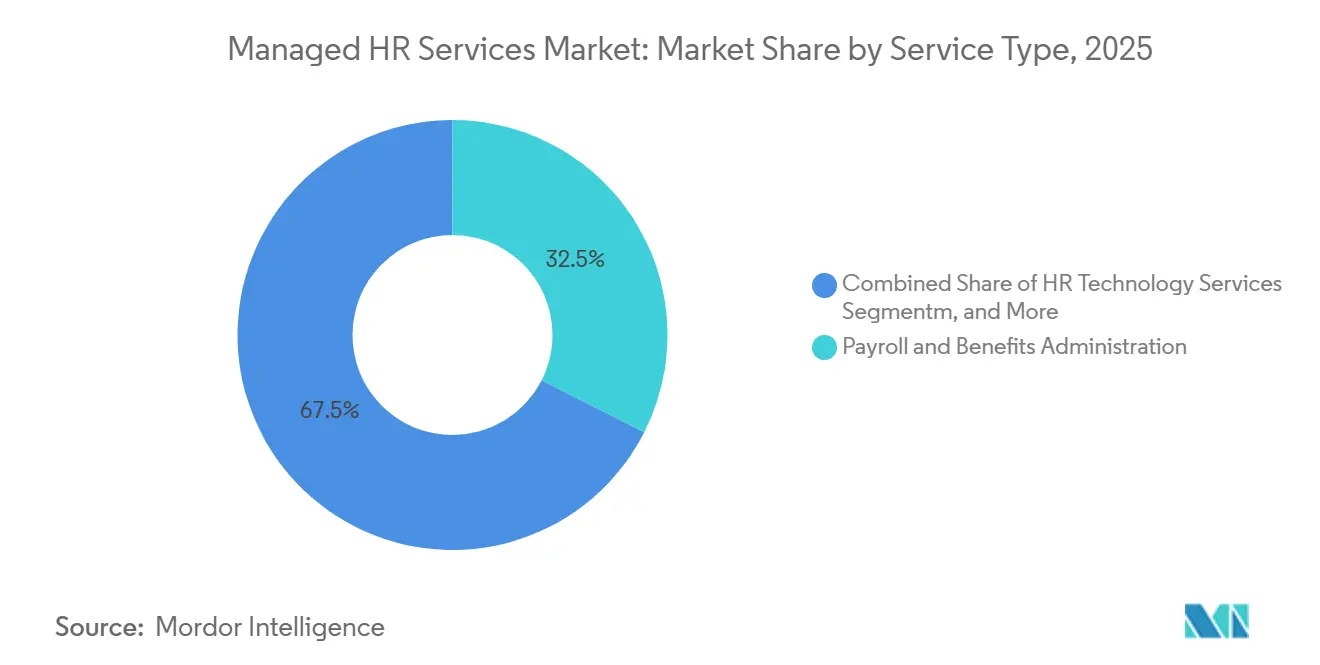

- By service type, payroll and benefits administration led with a 32.47% revenue share in the managed HR services market in 2025, while HR technology managed services is projected to expand at a 12.86% CAGR through 2031.

- By deployment model, cloud-enabled managed services held 63.29% share in 2025, while hybrid delivery is expected to record the highest CAGR at 11.72% through 2031.

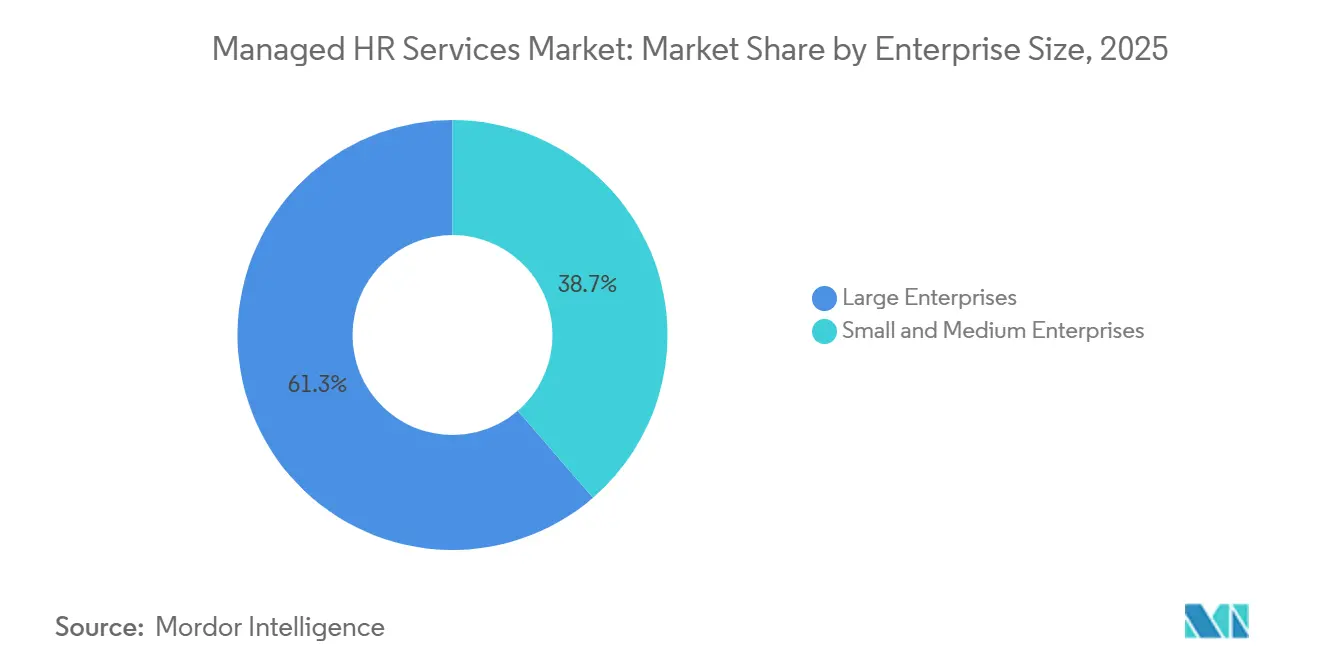

- By enterprise size, large enterprises accounted for 61.34% of revenue in 2025, while SMEs are projected to advance at a 13.41% CAGR through 2031.

- By end-user industry, information technology and telecom captured 27.63% of the managed HR services market share in 2025, while healthcare and life sciences are projected to grow at a 14.28% CAGR through 2031.

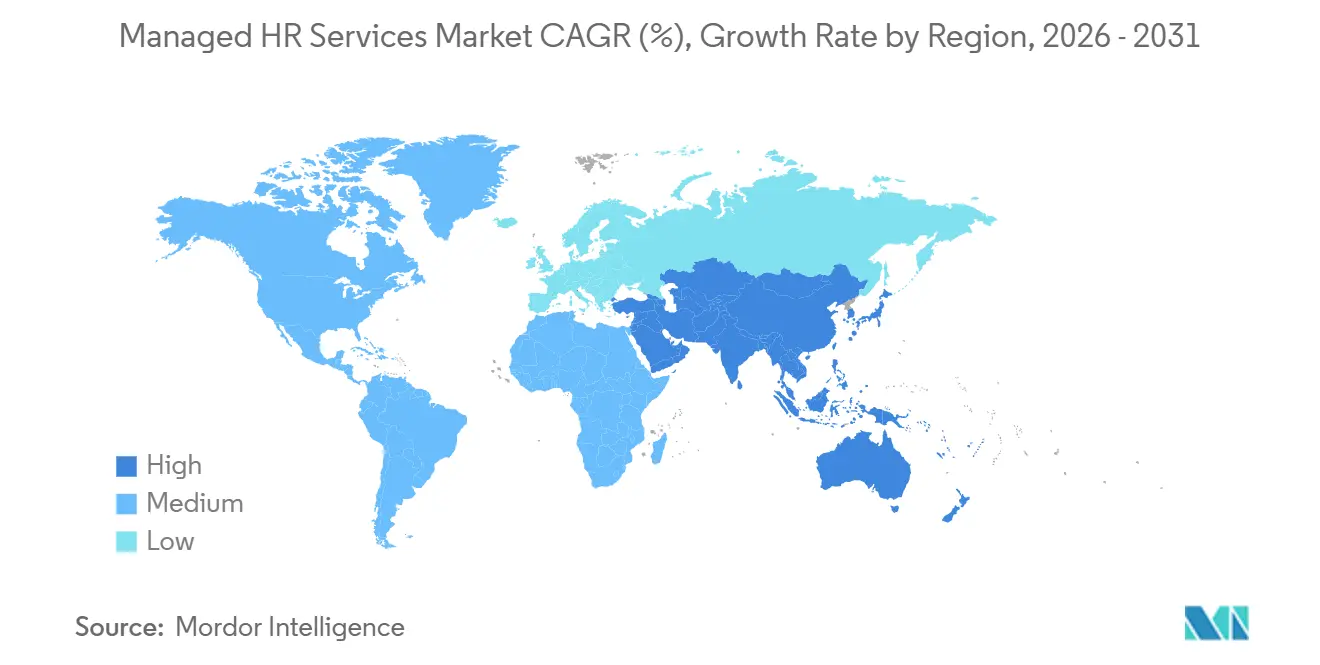

- By geography, North America represented 38.92% of the managed HR services market in 2025, while Asia-Pacific is expected to expand at a 15.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Managed HR Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Outsourcing of Core HR Operations | +2.5% | Global, concentrated impact in North America and Europe | Short term (≤ 2 years) |

| Need for Multi-Country Payroll Standardization | +1.8% | Global, concentrated in APAC, Europe, and multinational corridors | Medium term (2-4 years) |

| Rising Compliance Burden Across Labor Jurisdictions | +1.5% | Global, with early intensification in EU, North America, and APAC | Medium term (2-4 years) |

| Expansion of AI-Enabled HR Workflow Automation | +1.3% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Shift Toward Employee Experience-Led Service Models | +0.8% | Global, with stronger traction in North America and APAC | Medium term (2-4 years) |

| Growth of Distributed and Remote Workforces | +0.6% | Global, strongest in North America, EU, and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing of Core HR Operations

The managed HR services market is moving further toward full-process outsourcing as enterprises combine payroll, benefits, HR operations, and technology support under fewer vendors. Buyers now treat external HR delivery as an operating model choice rather than a short-term cost program, because HR has become more data-intensive and more exposed to compliance failures. Service levels are increasingly tied to payroll accuracy, compliance pass rates, and employee experience, thereby reducing the appeal of providers that rely solely on labor arbitrage. More than 1.1 million clients across 140-plus countries relied on a major HR and payroll platform as of April 2026, which shows the scale advantage large platform providers hold in the managed HR services market.[1]ADP, “Third Quarter Fiscal 2026 Financial Results,” SEC, sec.gov This scale matters because mid-sized buyers can access analytics such as attrition monitoring, pay benchmarking, and workforce planning through outsourced contracts rather than building those tools internally. As a result, the managed HR services market is seeing more demand for multi-tower relationships and fewer buyers willing to manage separate point vendors across core HR tasks.

Need for Multi-Country Payroll Standardization

The managed HR services market is also being shaped by the difficulty of running payroll across multiple tax, filing, and benefits systems. More than 36% of organizations handled payroll in 6 or more countries, and 7% operated across 51 or more territories in 2025.[2]PayrollOrg, “Navigating Compliance, Strategy in a Complex Global Market, Global Payroll Week 2025 Survey Results in Review,” PayrollOrg, payroll.org That level of spread makes internal payroll standardization hard to manage, especially when payroll data is also needed for headcount, turnover, and compensation analysis. A payroll platform with Workforce AI launched in May 2026 was designed to cut payroll processing from days to hours while keeping human review for exceptions, which reflects where buyer expectations are moving. Real-time filing rules, wage transparency mandates, and social contribution changes have continued to add complexity across countries. In the managed HR services market, providers with native multi-country capability have a clear advantage because they reduce latency, cut handoffs, and improve data consistency across payroll operations.

Rising Compliance Burden Across Labor Jurisdictions

The managed HR services market continues to benefit from expanding labor rules across states and countries. Employers now face more moving parts in paid leave administration, worker classification, remote work tax exposure, and recordkeeping obligations than they did a few years ago. These changes matter because HR teams must update benefit rules, tax logic, worker documents, and audit trails every time a law changes. In the managed HR services market, providers that build regulatory change management into the base contract are in a better position than vendors that treat each update as a separate project. The result is a stronger demand for services that combine execution with interpretation, especially for multinational employers that cannot monitor each jurisdiction in real time. This pressure also raises switching barriers, because once a provider's compliance workflows are embedded, buyers are less willing to restart the process with a new vendor.

Expansion of AI-Enabled HR Workflow Automation

AI deployment is changing the cost and operating structure of the managed HR services market. A workflow layer introduced in March 2026 was designed to automate HR and finance tasks across enterprise applications and third-party systems.[3]Workday, “Introducing Sana from Workday, Superintelligence for Work That Finds Answers, Takes Action, and Automates Workflows,” Workday Newsroom, workday.com In April 2026, specialized AI agents were embedded into leave management, contract compliance, and benefits enrollment workflows. Another major HR platform reported that its employee support system had already handled more than 11.5 million employee interactions before transitioning to an agentic AI platform. These moves show that the managed HR services market is shifting routine processing away from human teams and toward exception handling, governance, and data supervision. Providers that combine AI tools with proprietary payroll, attrition, and skills data are therefore building stronger differentiation than firms that rely solely on generic automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Employee Information Security Risks | -1.2% | Global, heightened exposure in regulated markets, EU, North America, and APAC | Short term (≤ 2 years) |

| Fragmented Country-Specific Labor Regulation Complexity | -0.8% | Global, most pronounced in high-regulatory-velocity markets, India, EU member states, Southeast Asia | Medium term (2-4 years) |

| High Switching Costs During Legacy HR Transformation | -0.6% | North America and Europe, higher legacy system concentration | Medium term (2-4 years) |

| Under-Reported Risk, Dependence on Clean Master Data and HR Record Quality | -0.4% | Global, concentrated in high-complexity multi-entity enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Employee Information Security Risks

Data protection remains one of the clearest limits on faster expansion in the managed HR services market. Outsourced HR environments store payroll records, bank details, benefits data, and personal identifiers for large employee groups, making them attractive targets for ransomware and data theft. Buyers now evaluate vendors not only on service scope but also on access controls, audit readiness, incident response, and breach notification commitments. Changing privacy rules during 2025-2026 affected how outsourcing contracts allocate responsibility and manage risk.[4]NAPEO PEO Insider, “Data Privacy and the PEO Role, Managing Risk in a Changing Compliance Landscape,” NAPEO, peoinsider.org This adds cost and time to vendor selection, especially in regulated sectors and cross-border engagements. The managed HR services market is therefore favoring providers that can show mature security controls, shared-processor compliance, and repeatable governance rather than broad service menus alone.

Fragmented Country-Specific Labor Regulation Complexity

Fragmented labor regulation also limits how far and how fast providers can scale the managed HR services market across countries. Shortages in local payroll and compliance expertise remained a major challenge in multi-country delivery during 2025. The issue is most visible in mid-tier markets where rules change quickly, but contract values do not always justify deep in-country staffing. When providers must reconfigure local logic by hand after each change, the risk of payroll errors and service delays increases. That makes some buyers question the economics of outsourcing at renewal, even when the broader case for external support remains strong. As a result, the managed HR services market continues to reward firms with durable country coverage, local knowledge, and standardized update processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Payroll Administration Anchors Revenue While Technology Services Accelerate

Payroll and benefits administration accounted for 32.47% of the managed HR services market in 2025, making it the revenue anchor for the category. The segment stays essential because payroll cannot be delayed, and compliance errors can create direct financial and legal exposure for employers. This makes enterprises less willing to rebuild payroll operations internally, even when they review other service towers for savings or simplification. Recruitment process outsourcing maintained steady demand in BFSI and technology settings, where hiring volumes fluctuate and time-to-fill remains commercially important. HR operations outsourcing also remained important for buyers seeking standardized workflows for employee records, service requests, document handling, and routine administration.

HR technology managed services are projected to grow at a 12.86% CAGR from 2026 to 2031, making it the fastest-moving service category in the managed HR services market. Growth is being pulled by companies that prefer outcome-based management with Workday, SAP SuccessFactors, and Oracle HCM Cloud rather than large internal support teams. Advanced technology solutions revenue rose 17% in full-year 2025, supported by data, AI, and agentic solutions across HR and finance process management work. The launch of an AI-led workforce platform in May 2026 also showed how payroll, HR workflows, time tracking, and benefits administration are being combined into a single offering for smaller businesses. Learning and talent management services, along with advisory and compliance support, gained importance as buyers sought reskilling, policy assurance, and cleaner data flows across the broader managed HR services industry.

By Deployment Model: Cloud Delivery Dominates While Hybrid Models Gain Strategic Ground

Cloud-enabled managed services held 63.29% of revenue in 2025, giving this model the largest share of the managed HR services market. The lead reflects a long migration toward cloud-native HR platforms that support automatic updates, elastic capacity, and faster reporting. Buyers also value the ability to unify data from payroll, benefits, time, and case management into a single operating model rather than across disconnected tools. Cloud delivery often improves rollout speed for new capabilities, especially in analytics, employee self-service, and workflow automation. Even so, not every enterprise can move all sensitive employee data into a fully public cloud setup.

Hybrid delivery is projected to expand at an 11.72% CAGR through 2031, making it the fastest-growing deployment path in the managed HR services market. Financial services and healthcare buyers are major drivers because they often need cloud flexibility without losing control over sensitive records or legacy systems. An Autonomous HCM framework presented in May 2026, with support for AI orchestration across cloud and on-premise layers, signaled that hybrid persistence is now a design assumption rather than a temporary stage. On-premise support still serves governments and state-linked organizations in parts of South America and the Middle East where sovereign storage rules and long contracts remain in place. Providers that can bridge all 3 models are better positioned to retain spend as the managed HR services market navigates uneven modernization cycles.

By Enterprise Size: Large Enterprises Lead In Value While SMEs Drive New-Logo Growth

Large enterprises accounted for 61.34% of revenue in 2025, giving them a dominant share of spending in the managed HR services market. Their scale, multi-country payroll needs, complex benefits structures, and union or works council obligations make outsourcing economically necessary in many cases. These buyers also prefer providers that can integrate multiple service towers under a single governance model and reporting structure. Contract value is therefore still concentrated among large organizations even as sales activity spreads into smaller accounts. This keeps enterprise-grade breadth of service and depth of compliance central to competition in the managed HR services market.

SMEs are projected to grow at a 13.41% CAGR through 2031, making them the fastest-expanding buyer group in the managed HR services market. Providers have opened this segment by offering modular, usage-based pricing and lower minimum contract thresholds. A USD 4.1 billion acquisition completed in April 2025 strengthened one provider's reach in the mid-market and broadened its HCM offering for smaller organizations. Fractional HR and PEO-adjacent models have also lowered the entry cost for companies that once relied only on basic HR software subscriptions. Across the managed HR services industry, providers that can win SME volume without weakening enterprise margins hold a durable commercial advantage.

By End-User Industry: Technology Leads In Volume While Healthcare And Life Sciences Gain Pace

Information technology and telecom accounted for 27.63% of the managed HR services market share in 2025, making it the largest end-user group by revenue. The sector has a high level of outsourcing maturity and manages distributed project-based workforces across multiple delivery locations. Those conditions create a steady demand for coordinated payroll, onboarding, workforce mobility, and employee support services. BFSI also remained a major contributor because data handling obligations, screening requirements, and hiring cycles are harder to manage through basic internal systems. Retail and e-commerce spending grew as seasonal hiring and variable labor demand increased the need for flexible payroll and staffing support.

The healthcare and life sciences sector is projected to record a 14.28% CAGR through 2031, making it the fastest-growing end-user segment in the managed HR services market. Demand is being lifted by workforce expansion in the Asia-Pacific and by the need for accurate credential tracking, compliance records, and shift-heavy administration. Industrial manufacturing and public sector demand remained steadier because union rules, civil service structures, and function eligibility limits limit outsourcing in some cases. Learning, compliance, and workflow automation are becoming increasingly relevant in healthcare settings, where staff availability, documentation, and audit readiness carry direct operational consequences. This leaves the managed HR services market with growth that remains broad-based but increasingly tilted toward sectors where regulation and workforce complexity move in step.

Geography Analysis

North America accounted for 38.92% of the managed HR services market share in 2025, making it the largest regional contributor. The region benefits from a deep buyer base, large multinational headquarters, and a rule environment that makes self-managed HR harder to sustain at scale. More than 1.1 million clients across 140-plus countries relied on a major HR and payroll platform in April 2026, which highlights the scale and maturity of the U.S. core in the managed HR services market. A major acquisition expanded the mid-market's reach and strengthened HCM capabilities for smaller organizations, while Mexico and Canada add demand for unified payroll and compliance workflows required by cross-border employment, manufacturing, and logistics.

Europe remains a large part of the managed HR services market because the region combines substantial demand with dense labor regulation. Germany, the United Kingdom, France, and the Netherlands lead adoption, but buyer needs differ by country because works councils, outsourcing norms, and local employment rules are not uniform. The United Kingdom has moved away from pure cost-driven contracts and toward technology-enabled, outcome-based models, creating space for both global providers and regional specialists. AI-powered recruiting analytics and multi-country payroll delivery across Northern and Central Europe show how regionally embedded firms defend their position against larger platforms.

Asia-Pacific is projected to expand at a 15.36% CAGR through 2031, which makes it the fastest-growing regional segment in the managed HR services market. India plays a dual role: it is both a major delivery hub for global providers and a growing buyer market as Global Capability Center activity scales. China, Southeast Asia, Japan, South Korea, Australia, and New Zealand also support regional growth through modernization programs, aging workforces, and mature outsourcing ecosystems. The Middle East and Africa are smaller today, but Saudi Arabia's workforce nationalization policies and the formalization of employment practices in South Africa and Nigeria are supporting demand for specialist compliance and payroll services. South America remains an emerging opportunity where frequent labor rule changes, currency pressure, and multi-jurisdiction payroll needs keep the managed HR services market relevant even when technology budgets are tight

Competitive Landscape

The managed HR services market is moderately concentrated at the top, with ADP, Accenture, IBM, TCS, Strada, Infosys, and other large providers holding a disproportionate share of major contract value. Even so, the broader managed HR services market remains highly competitive because more than 100 regional and niche specialists serve mid-market, country-specific, and single-tower needs. This mix limits pricing power, especially where buyers can separate payroll, technology support, recruiting, or compliance work across different vendors. It also means that large incumbents must continue to add product depth and delivery flexibility to protect renewal rates.

Strategic moves in 2025 and 2026 show that competition is shifting toward platform breadth, AI enablement, and better coverage of adjacent HR workflows in the managed HR services market. The acquisition of a compensation software provider in October 2025 expanded capabilities in compensation planning for mid-size and enterprise buyers. Another major acquisition completed in April 2025 strengthened reach in the mid-market and widened talent management and embedded HCM capabilities. A multi-year partnership announced in fiscal 2026 to build AI-powered back-office solutions, including HR and employee services, reflects the alliance-based model many providers are using to move faster.

White-space demand is centered on 3 areas in the managed HR services market: SME accounts that remain hard to serve profitably, emerging-market corridors where local expertise is thin, and AI governance services within HR workflows. The last area is gaining weight because buyers want evidence on bias controls, human review, decision logging, and policy oversight when AI is used in employee-facing processes. The launch of an AI-powered workforce platform in May 2026 demonstrated how talent development, skills optimization, onboarding, and internal mobility are moving closer to mainstream managed service offers. Deeper expansion of agentic HR capabilities in 2026 also raised the competitive bar for service providers that rely on manual processing rather than platform-led execution. The managed HR services market is therefore likely to continue rewarding providers that combine country coverage, platform partnerships, AI governance, and measurable service outcomes within a single contract model.

Managed HR Services Industry Leaders

Automatic Data Processing, Inc.

Accenture plc

Randstad N.V.

Alight, Inc.

Ceridian HCM Holding Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Intuit unveiled QuickBooks Workforce, a unified AI-agent-driven HCM platform for small and mid-market businesses integrating payroll, HR workflows, time tracking, and benefits administration. The launch directly competes with managed HR service bundles previously limited to enterprise-scale providers, accelerating SME segment penetration.

- May 2026: Novaworks.ai launched its Core HR SuperAgent, Special Agents, and Policy Advisor on the ServiceNow enterprise AI infrastructure at Knowledge 2026, delivering agentic HR workflows covering onboarding, performance, benefits, and workforce transitions with built-in governance controls.

- May 2026: Cornerstone OnDemand launched Cornerstone Workforce AI, combining workforce readiness insights, skills development, and dynamic AI agents for internal mobility, goal alignment, and onboarding. The platform blurs the boundary between talent management outsourcing and learning managed services at the enterprise level.

- May 2026: UKG unveiled UKG Pro Pay with Workforce AI at the American Payroll Association's Payroll Congress 2026, deploying agentic AI to reduce payroll processing from days to hours while maintaining human oversight for compliance exception resolution.

Global Managed HR Services Market Report Scope

The Managed HR Services market refers to outsourced solutions and managed service models that support organizations in handling critical human resource functions. These services include recruitment process outsourcing, payroll and benefits administration, HR operations outsourcing, learning and talent management, HR technology managed services, and advisory and compliance support. Delivered through cloud-enabled, hybrid, and on-premise models, they cater to both large enterprises and SMEs across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The primary objective of this market is to optimize HR operations, reduce costs, ensure compliance, enhance employee experience, and enable organizations to focus on strategic workforce initiatives while leveraging specialized expertise and technology-driven service delivery.

The Managed HR Services market report is segmented by Service Type (Recruitment Process Outsourcing (RPO), Payroll and Benefits Administration Services, HR Operations Outsourcing (HRO), Learning and Talent Management Services, HR Technology Managed Services (AMS/MSP), Advisory and Compliance Services), Deployment Model (Cloud, Hybrid, and On-Premise), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Recruitment Process Outsourcing (RPO) |

| Payroll and Benefits Administration Services |

| HR Operations Outsourcing (HRO) |

| Learning and Talent Management Services |

| HR Technology Managed Services (AMS/MSP) |

| Advisory and Compliance Services |

| Cloud |

| Hybrid |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Service Type | Recruitment Process Outsourcing (RPO) | |

| Payroll and Benefits Administration Services | ||

| HR Operations Outsourcing (HRO) | ||

| Learning and Talent Management Services | ||

| HR Technology Managed Services (AMS/MSP) | ||

| Advisory and Compliance Services | ||

| By Deployment Model | Cloud | |

| Hybrid | ||

| On-Premise | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the managed HR services market?

The managed HR services market stood at USD 51.82 billion in 2025 and is projected to reach USD 88.60 billion by 2031, growing at a 9.88% CAGR during 2026-2031.

Which service category leads revenue in managed HR services?

Payroll and benefits administration led the market with a 32.47% revenue share in 2025, supported by the non-discretionary nature of payroll execution and high compliance risk.

Which deployment model is growing the fastest in HR managed services?

Hybrid delivery is the fastest-growing deployment model, with a projected CAGR of 11.72% through 2031, as enterprises balance cloud scale with tighter governance over sensitive employee data.

Why are SMEs becoming important buyers of outsourced HR services?

SMEs are projected to grow at a 13.41% CAGR through 2031 because providers now offer modular and usage-based services that lower contract barriers for smaller organizations.

Which end-user sector is expanding the fastest?

Healthcare and life sciences is forecast to grow at a 14.28% CAGR through 2031, driven by workforce expansion and stricter needs around credentialing, compliance, and workforce recordkeeping.

Which region shows the strongest growth outlook?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 15.36% through 2031, supported by outsourcing adoption in India, China, and Southeast Asia.

Page last updated on: