HR Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

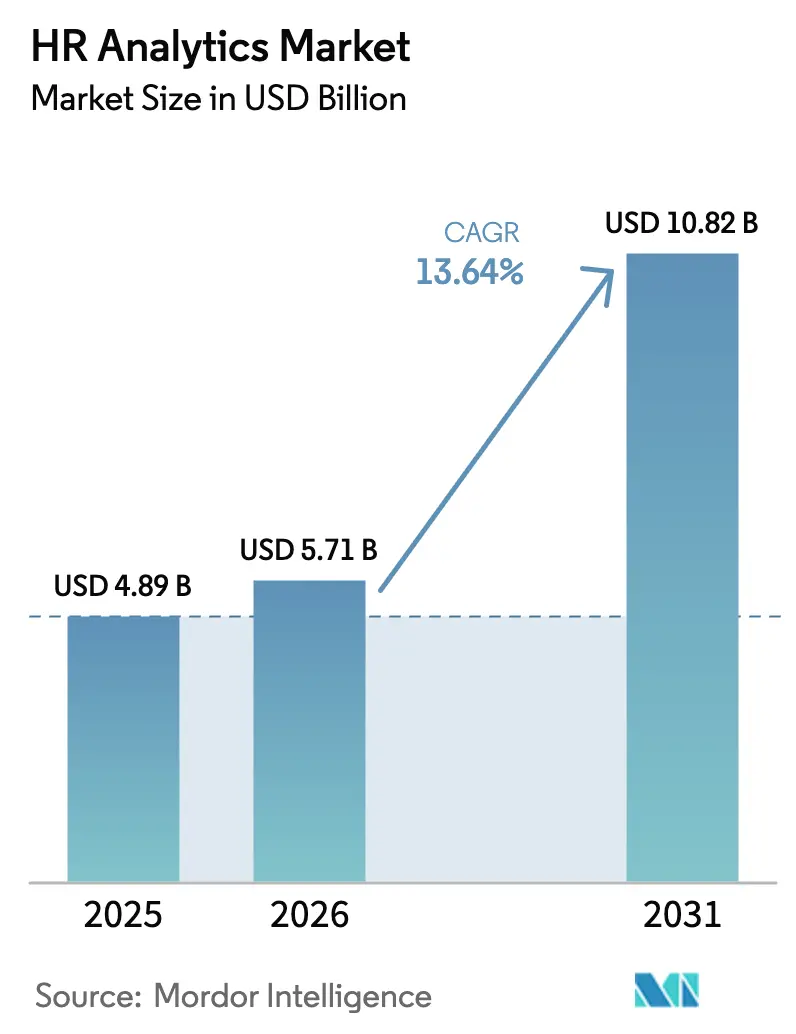

| Market Size (2026) | USD 5.71 Billion |

| Market Size (2031) | USD 10.82 Billion |

| Growth Rate (2026 - 2031) | 13.64% CAGR |

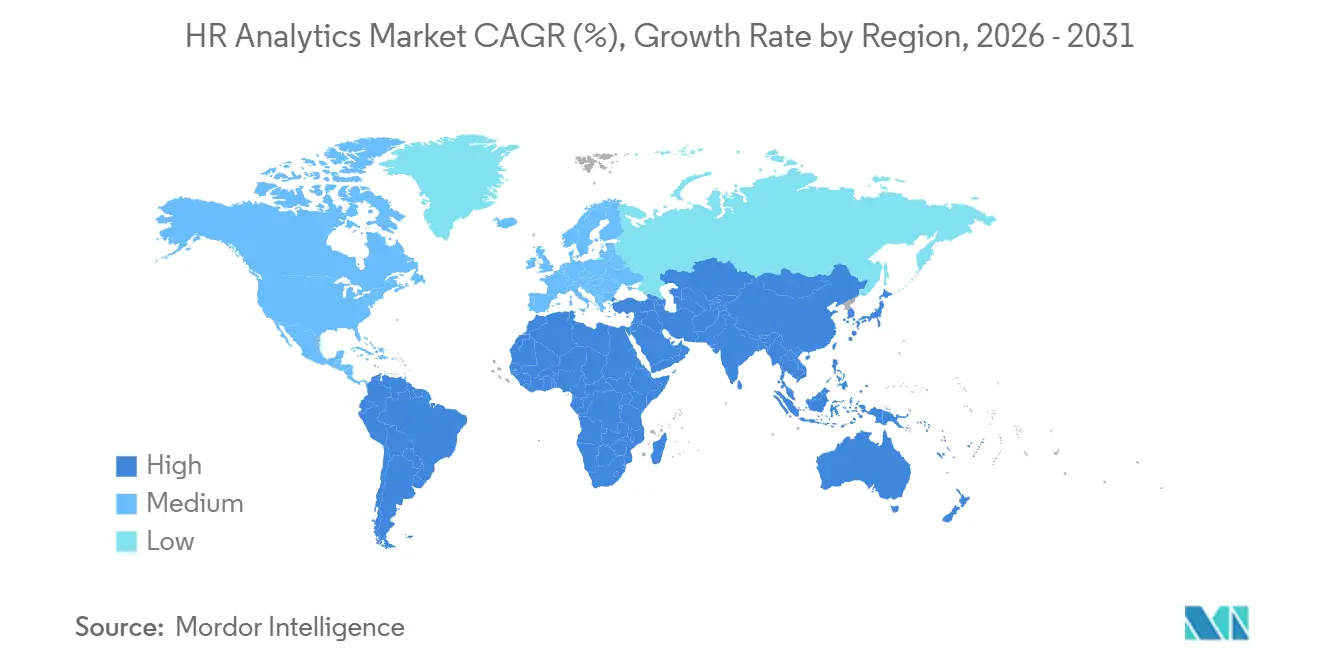

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Analytics Market Analysis by Mordor Intelligence

The HR analytics market size is projected to be USD 4.89 billion in 2025, USD 5.71 billion in 2026, and reach USD 10.82 billion by 2031, growing at a CAGR of 13.64% from 2026 to 2031. Cloud subscription economics, the pivot from descriptive to predictive workforce intelligence, and new ESG-driven disclosure duties together explain the sustained double-digit trajectory. Demand is rising fastest where generative-AI copilots compress labor-intensive recruiting and reporting cycles, while widening pay-equity mandates push diversity analytics from optional to required software. Competitive intensity is growing as pure-play analytics layers integrate with multiple HR and payroll systems, challenging incumbent HCM suites that bundle analytics as an add-on. Enterprises of every size now evaluate people-analytics platforms not only for dashboards but also for built-in bias controls, data-privacy tooling, and regulatory-ready audit trails.

Key Report Takeaways

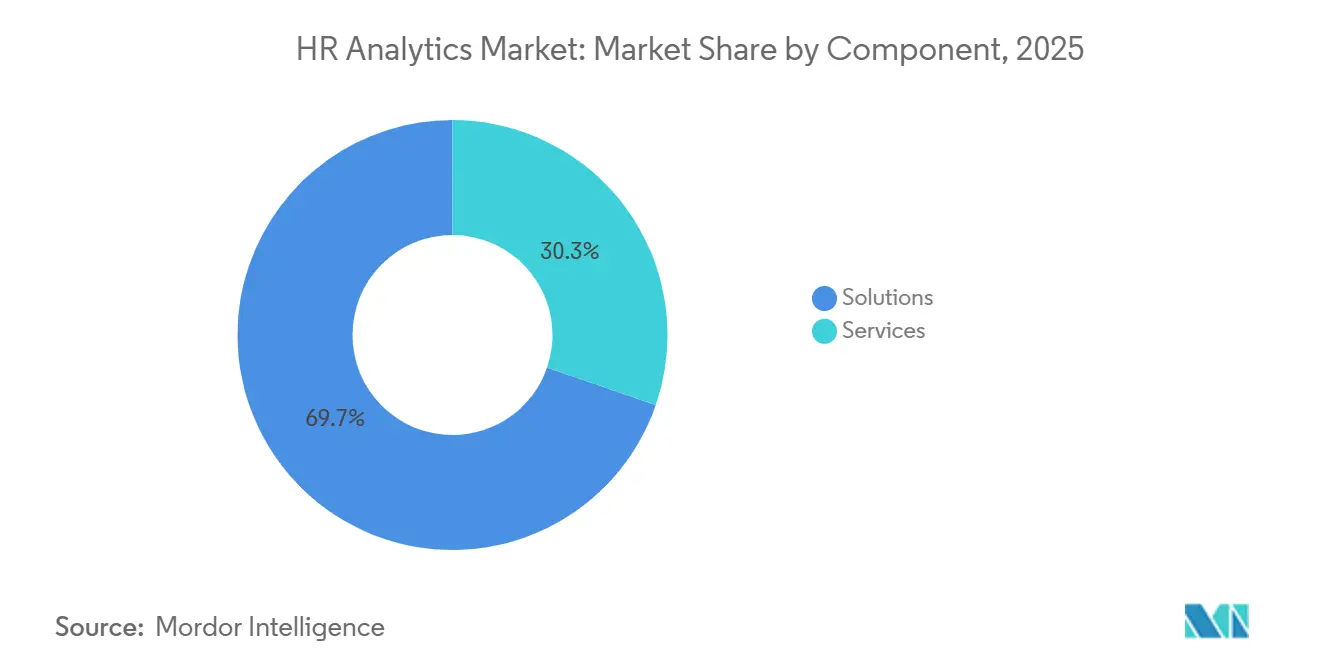

- By component, solutions led with 69.73% of the HR analytics market share in 2025, while services are projected to expand at a 13.89% CAGR through 2031.

- By deployment mode, cloud installations captured 75.67% of 2025 revenue and are forecast to grow at a 13.96% CAGR through 2031.

- By organization size, large enterprises held 62.33% of the HR analytics market share in 2025, whereas small and medium enterprises are advancing at a 13.92% CAGR through 2031.

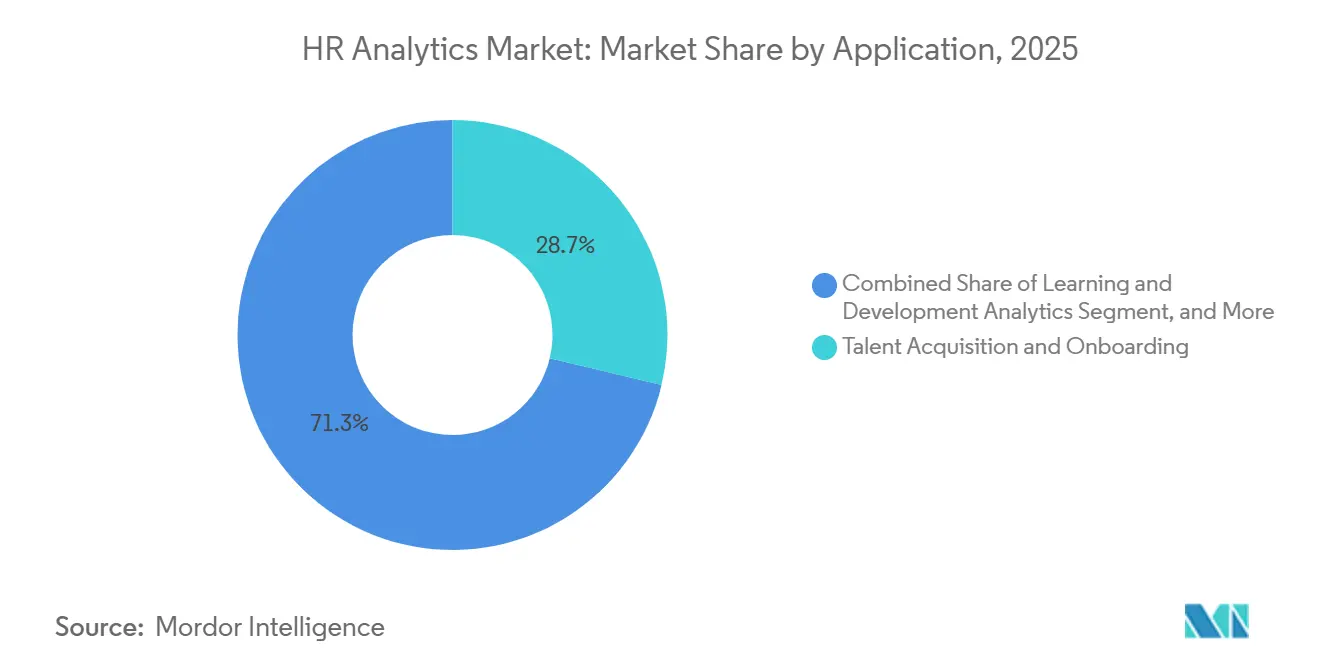

- By application, talent acquisition and onboarding accounted for 28.74% of 2025 revenue, and diversity, equity, and inclusion analytics are expected to rise at a 14.83% CAGR through 2031.

- By end-user industry, IT and telecom generated 23.62% of the HR analytics market share in 2025, while healthcare and life sciences are poised to grow at a 14.11% CAGR through 2031.

- By geography, North America retained 39.48% revenue share in 2025, and the Asia-Pacific is projected to register the fastest growth at a 14.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Based HR Analytics Adoption Surge | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Need to Cut Attrition and Optimize Workforce Cost | +2.5% | Global, acute in healthcare and IT services | Short term (≤ 2 years) |

| Hybrid and Remote Work Accelerating Data-Driven HR | +2.1% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Generative-AI Copilots Embedded in HR Suites | +2.3% | North America and Europe early adopters | Long term (≥ 4 years) |

| ESG-Linked Human-Capital Disclosure Mandates | +1.7% | North America and Europe, spillover to Asia-Pacific multinationals | Medium term (2-4 years) |

| Wearable and Biometric Data for Wellbeing Analytics | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Based HR Analytics Adoption Surge

Moving HR analytics to the cloud has eliminated the upfront hardware and licensing costs that once limited adoption to very large companies. An ISG poll of 1,200 organizations showed that 69% were already running at least one HR module in software-as-a-service form by the close of 2025, a steep jump from 52% in 2023.[1]Information Services Group, “2025 ISG Provider Lens HR Technology,” isg-one.com Oracle added 1,400 Fusion Cloud HCM clients during fiscal 2025 as modular, per-employee pricing appealed to budget-sensitive buyers. Workday shipped three major releases in 2025, versus the single annual update common in legacy on-premises deployments, underscoring the feature-velocity advantage of a multi-tenant design. The same architecture, however, channels data through hyperscale centers that can clash with EU cross-border rules, a tension highlighted by Amazon's EUR 746 million (USD 843 million) GDPR fine for employee data processing.

Need to Cut Attrition and Optimize Workforce Cost

Voluntary turnover costs U.S. employers USD 1 trillion in 2025, prompting firms to lean on predictive models that flag flight risk months before a resignation. IBM’s Watson Analytics reached 95% accuracy in predicting which workers would exit within a year by blending tenure, promotion history, and external labor-market signals. Hospitals that paired these insights with targeted retention bonuses and shift-pattern tweaks trimmed registered-nurse attrition by 22%, saving an average of USD 52,100 per avoided departure. Pay-compression dashboards also reveal cases where new hires out-earn long-serving colleagues, a trigger for “quiet quitting” that companies address through mid-cycle salary corrections. As CHROs quantify such savings, finance teams increasingly treat people analytics as a cost-containment lever rather than a discretionary tool.

Hybrid and Remote Work Accelerating Data-Driven HR

The shift to hybrid schedules removed hallway conversations that once signaled disengagement, so managers now study digital traces instead. Microsoft Viva Insights aggregates meeting loads, after-hours email counts, and collaboration networks to flag burnout or isolation risk before it shows up in exit interviews.[2]Microsoft Corporation, “Microsoft Viva Insights Product Page,” microsoft.com Qualtrics found that 63% of hybrid firms issued pulse surveys in 2025, up from 41% two years earlier, because annual engagement polls miss short-cycle sentiment swings. Regulators warn that excessive monitoring can violate privacy laws; the European Data Protection Board requires explicit consent for employers to capture keystrokes or webcam feeds under GDPR Article 88. Analytics also expose labor-cost arbitrage, as Deloitte noted 40% savings when U.S. software teams hired engineers in tier-2 Indian cities without productivity loss.

Generative-AI Copilots Embedded in HR Suites

Large language models now automate tasks that once consumed a third of HR-business-partner bandwidth. SAP’s Joule assistant drafts interview questions and proposes learning paths by mapping competency gaps to course catalogs.[3]SAP, “SAP Artificial Intelligence Joule Overview,” sap.com Workday’s Illuminate parses free-text feedback to uncover attrition themes in days rather than weeks. Oracle’s AI agents, rolled out in January 2025, shortened time-to-hire by 30% in pilot programs by pre-screening résumés against role-specific ontology maps. Yet a 2024 class-action lawsuit alleges that automated screening penalized applicants with résumé gaps, spotlighting litigation risk if training sets mirror historical bias. Vendors, therefore, rush to embed bias-detection layers and explainability dashboards to reassure risk officers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of HR Data-Science Talent | -1.8% | Global, pronounced in mid-market firms | Medium term (2-4 years) |

| Data-Privacy and Compliance Complexity | -1.5% | Europe, North America, fragmented Asia-Pacific | Short term (≤ 2 years) |

| Algorithmic-Bias Litigation Risk | -0.9% | North America and Europe | Medium term (2-4 years) |

| Legacy Siloed HR Data Architectures | -1.3% | Government, healthcare, manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of HR Data-Science Talent

People analytics roles blend SQL, Python, statistics, and HR policy knowledge, a skill cocktail still rare in labor markets worldwide. LinkedIn’s 2025 Emerging Jobs Report ranked people analytics specialist seventh by growth rate, yet the median position sat unfilled for more than 90 days and carried salary premiums of 25-35% over standard HR analyst positions. Deloitte observes that many mid-market firms stall at descriptive dashboards because they lack the staff to build predictive models. Drag-and-drop tools from vendors such as Visier reduce entry barriers, but interpreting model output and steering interventions still call for seasoned analysts. Until universities and in-house academies expand pipelines, talent scarcity will cap analytics ROI for small to midsize employers.

Data-Privacy and Compliance Complexity

HR files store health data, union affiliation, and disciplinary records, all granted heightened protection under global privacy statutes. The EU fined H&M EUR 35.3 million (USD 39.9 million) in 2020 for monitoring employees’ personal lives too closely. California’s Consumer Privacy Act, fully extended to employee records in 2023, obliges companies to deliver access, deletion, and correction rights on request. China’s Personal Information Protection Law blocks cross-border transfers without regulator-approved security assessments. GDPR Article 22 lets workers contest automated decisions that materially affect them, such as promotion denials, forcing firms to layer explainability and manual-review checkpoints into analytics workflows. Legal reviews and data-protection impact assessments can add six to 12 months to deployment timelines, squeezing smaller IT budgets and slowing innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead While Services Accelerate

Solutions captured 69.73% of 2025 revenue, underscoring enterprises’ preference for packaged dashboards, prebuilt connectors, and embedded predictive models that can be activated with minimal configuration. Services such as implementation consulting, custom model development, and managed analytics are advancing at a 13.89% CAGR, as firms without in-house data talent rely on partners for data migration, change management, and bias-testing. The HR analytics market share advantage enjoyed by software vendors is likely to narrow as regulatory requirements for explainability and privacy drive demand for specialized advisory projects.

Subscription pricing lets buyers add modules over time, compressing deployment cycles from months to weeks. Oracle recorded a 23% jump in cloud-services fees in fiscal-2025 because clients needed mapping of complex org structures to standardized metric libraries. Accenture and IBM both expanded workforce analytics practices by double digits, pairing data scientists with industrial-organizational psychologists to turn raw insights into retention or reskilling programs. This advisory uptick signals that services will continue to gain ground, even though software remains the spine of the HR analytics market.

By Deployment Mode: Cloud Defines New Default

Cloud installations accounted for 75.67% of 2025 spending and are growing at a 13.96% CAGR, outpacing all other deployment options. Multi-tenant design accelerates feature releases, evidenced by Workday’s three major updates in 2025 versus annual patches on legacy stacks. Consumption-based pricing also aligns vendor revenue with customer headcount, easing CFO concerns about shelf-ware during hiring freezes.

On-premises platforms persist in government and highly regulated banking, where data residency or mainframe entanglements slow migration. SAP reported that SuccessFactors added 2,100 cloud customers in 2025, while on-premises ECC licenses fell 9%. Hybrid architectures, a cloud analytics layer combined with in-country mirrors for sensitive records, are an interim fix in Russia, Indonesia, and Vietnam, but overhead costs may eventually push holdouts toward full SaaS adoption.

By Organization Size: SMEs Close the Capability Gap

Large enterprises accounted for 62.33% of 2025 spending, reflecting dedicated people-analytics centers that run complex succession, scenario, and skills-adjacency models. Small and medium enterprises are experiencing significant growth, advancing at a compound annual growth rate (CAGR) of 13.92%. This represents the fastest pace within this segment, driven by the adoption of no-code dashboards and per-employee licensing models, which effectively lower the barriers to entry for these businesses.

Visier’s Essentials plan, priced at USD 15,000 a year for 500–1,000-employee firms, bundles turnover prediction and diversity dashboards without demanding SQL expertise. BambooHR and HiBob added thousands of sub-500-staff customers in 2025 by embedding out-of-the-box reports on offer acceptance and time-to-fill. Quick, eight-week implementations and ROI calculators that convert attrition reductions into dollar savings help SMEs justify investments against lean budgets, further expanding the HR analytics market among mid-market buyers.

By Application: DEI Analytics Surges Ahead

Talent acquisition and onboarding retained a 28.74% slice of 2025 revenue, powered by ATS integrations that score candidate pipelines and cut time-to-hire. Driven by the implementation of California SB 1162, New York City Local Law 144, and the EU Pay Transparency Directive, which transform voluntary reporting into mandatory disclosure, the diversity, equity, and inclusion analytics market is experiencing significant growth. It is projected to expand at a compound annual growth rate (CAGR) of 14.83%, representing the steepest growth trajectory within this domain.

DEI modules now calculate adjusted pay gaps, track promotion velocity by demographic cohort, and issue audit-ready files for regulators. Compensation analytics remain vital to reveal pay compression, while learning analytics link certification completions to future performance ratings. Employee-wellbeing dashboards, which fuse pulse-survey sentiment with benefits use, flag burnout clusters that correlate with turnover risk. Together, these use cases support a rising share of the HR analytics market.

By End-User Industry: Healthcare Tops the Growth Charts

IT and telecom generated 23.62% of 2025 revenue, reflecting tech firms’ early embrace of skills graphs that map competencies to project needs. The healthcare and life sciences sector is projected to grow at a significant compound annual growth rate (CAGR) of 14.11%, making it the fastest-growing vertical. This growth is primarily driven by hospitals adopting comprehensive retention strategies to address the issue of registered-nurse turnover. The average turnover rate for registered nurses is anticipated to reach 18.4% in 2025, underscoring the importance of these retention efforts in stabilizing the workforce and ensuring operational efficiency.

BFSI institutions apply analytics to branch-network staffing and risk-compliance workloads, while retailers model seasonal labor spikes to trim overtime bills. Manufacturers track safety incidents and skills adjacency to support cross-training, shielding production lines against absenteeism. Government agencies, facing budget caps but mounting pension liabilities, lean on cloud platforms for succession planning and cost forecasting. Collectively, diverse vertical needs keep the HR analytics market share widely distributed, reinforcing the importance of sector-specific content libraries within vendor roadmaps.

Geography Analysis

North America accounted for 39.48% of 2025 revenue, supported by SEC rules mandating human-capital disclosures for listed companies and robust venture investment in HR tech startups. U.S. enterprises spent an average of USD 1.6 million each on AI-powered HR tooling during 2025. Canada’s Pay Equity Act further boosts demand for compensation analytics, while Mexico’s manufacturing nearshoring boom drives the need for headcount-planning dashboards that keep pace with plant expansions.

Asia-Pacific is the fastest-growing region, with a 14.69% CAGR. India’s IT majors adopted skills graphs to redeploy staff as generative-AI automation reshapes delivery models. China’s state-owned enterprises digitize HR processes under government modernization mandates, and Japan’s shrinking labor pool forces manufacturers to maximize productivity per worker. Australia’s 2024 Fair Work amendments extend leave entitlements to gig-economy workers, opening new analytics use cases in contingent labor management.

Europe’s Corporate Sustainability Reporting Directive embeds diversity and training metrics into audited statements, pushing HR analytics into CFO territory. Germany’s works council co-determination rules require consent layers for employee monitoring, thereby influencing product roadmaps. In the Middle East, Saudi Arabia’s Saudization quotas create a compliance-driven need for dashboards that track citizen-to-expat ratios. South America lags in spending, yet Brazil’s labor-law modernization is nudging employers toward cloud analytics for hybrid scheduling compliance.

Competitive Landscape

The HR analytics market is moderately fragmented. The top five vendors, SAP, Oracle, Workday, ADP, and IBM, accounted for around 45% of combined revenue in 2025, leaving ample room for niche specialists. Incumbent HCM suites embed analytics into existing payroll and recruiting workflows, monetizing installed bases. SAP SuccessFactors People Analytics links workforce-cost data with SAP ERP financials, letting users model cost-to-revenue ratios that point solutions cannot match. Oracle ships 200+ prebuilt metrics and industry benchmarks to reduce the custom report backlog.

Pure-play vendors differentiate on integration breadth and time-to-value. Visier connects to 200+ HR apps, serving as an agnostic insights layer across heterogeneous tech stacks. ChartHop targets org design visualizations for growth-stage firms, while Culture Amp combines engagement surveys with DEI analytics. Eightfold AI and Gloat specialize in talent marketplaces that match employees to gigs, projects, and mentors, driving internal mobility. Syndio owns the pay-equity niche, releasing templates that meet EU Pay Transparency requirements. Patent filings reveal roadmap priorities; Workday filed 14 patents related to federated learning in 2024, indicating a push toward privacy-preserving model training.

M&A and funding activity underline competitive ferment. ADP bought Workforce Software for USD 1.2 billion in August 2025 to add advanced scheduling analytics. Workday acquired HiredScore for USD 450 million in December 2024, sharpening its AI recruiting stack. Visier’s USD 154 million Series E underscores investor confidence, while Eightfold AI’s USD 220 million Series F bankrolls expansion into Latin America and Southeast Asia.

HR Analytics Industry Leaders

SAP SE

Oracle Corporation

Workday Inc.

IBM Corporation

ADP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Workday launched Illuminate Talent Intelligence, reducing regrettable attrition by 18% within six months.

- September 2025: SAP extended its Joule AI assistant to SuccessFactors for automated job-description drafting.

- August 2025: ADP acquired Workforce Software for USD 1.2 billion, adding labor-scheduling analytics.

- June 2025: Visier raised USD 154 million in Series E funding to accelerate DEI-analytics development.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the HR analytics market as the aggregated annual spend on software and related services that collect, integrate, and analyze workforce data to guide decisions across recruitment, engagement, compensation, compliance, and retention. These solutions sit on top of core HR information systems and pull structured and unstructured data to deliver descriptive, predictive, and prescriptive insights.

Scope Exclusion: Payroll processing and generic business intelligence tools not purpose-built for HR decision-making are left outside the baseline.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- On-Premise

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Talent Acquisition and Onboarding

- Workforce Planning and Optimization

- Compensation and Payroll Analytics

- Learning and Development Analytics

- Employee Engagement and Wellbeing Analytics

- Diversity, Equity and Inclusion Analytics

- By End-User Industry

- IT and Telecom

- Banking, financial services and insurance (BFSI)

- Retail and Consumer Goods

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview HR technology buyers, implementation partners, and product managers across North America, Europe, Asia-Pacific, and the Middle East to validate spend brackets, seat-based pricing, and deployment mix. Short online surveys with mid-market HR leaders refine penetration assumptions among small and medium enterprises, while follow-up calls with analysts of regional systems integrators clarify implementation revenue splits.

Desk Research

Mordor analysts begin with public datasets from organizations such as the International Labour Organization, US Bureau of Labor Statistics, Eurostat, and the World Bank, which give reliable employee head-count, wage, and enterprise-size distributions across regions. Trade associations like the Society for Human Resource Management and CIPD offer adoption ratios and functional benchmarks, which are then cross-checked with patent filings and product release notes captured through Dow Jones Factiva. D&B Hoovers supplies revenue ranges for major vendors, helping us sense-check average selling prices. Company 10-Ks, investor decks, and reputable business press provide further context on pricing shifts, customer wins, and macro signals. The sources cited above are illustrative; many additional references inform the desk work.

Market-Sizing & Forecasting

A top-down demand pool is first built from enterprise counts and employee totals, segmented by organization size and region, before being filtered through published SaaS adoption rates and per-employee license fees. Select bottom-up checks, vendor revenue roll-ups, sampled cloud contract values, and channel partner views are layered in to balance outliers. Key drivers modeled include average HR IT spend per employee, shift from on-premise to cloud, attrition-linked analytics uptake, hybrid-work prevalence, and data-privacy regulation milestones. Multivariate regression, tuned with three scenario assumptions agreed during primary research, projects each driver to 2030. Where vendor disclosures are missing, regional seat multiples derived from comparable deployments bridge the gaps.

Data Validation & Update Cycle

Outputs pass through variance checks against third-party labor indicators, peer model comparison, and a two-step analyst review. Reports refresh every twelve months, with interim updates triggered by material funding rounds, regulatory changes, or ≥10 % deviation in quarterly vendor bookings. An additional pre-publication sweep ensures clients receive the latest reconciled view.

Why Mordor's HR Analytics Baseline Earns Executive Trust

Published estimates often diverge because firms choose different functional scopes, price cuts, and refresh cadences.

Key gap drivers include whether implementation services are bundled, how on-premise upgrades are treated, and the currency-conversion date each publisher locks in, along with refresh frequency that can lag fast-moving SaaS price dynamics.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.03 Bn (2025) | Mordor Intelligence | - |

| USD 3.70 Bn (2023) | Global Consultancy A | Excludes service revenues and uses static seat pricing from 2022 |

| USD 3.28 Bn (2023) | Industry Journal B | Captures only solution revenue and omits mid-market cloud migration in Asia |

| USD 3.73 Bn (2024) | Research House C | Relies solely on vendor press releases; refresh cadence biennial |

In summary, by unifying labor statistics, live vendor data, and practitioner insight within a transparent model that updates annually, Mordor Intelligence delivers a balanced, traceable baseline that decision-makers can depend on for strategic planning.

Key Questions Answered in the Report

What CAGR is forecast for the HR analytics market through 2031?

The market is expected to grow at a 13.64% CAGR between 2026 and 2031.

Which deployment model is expanding the quickest?

Cloud deployments show the fastest growth, projected at a 13.96% CAGR.

Which application segment is forecast to outpace all others?

Diversity, equity and inclusion analytics is projected to advance at a 14.83% CAGR.

Why is Asia Pacific considered the fastest-growing region?

Digital-HR mandates in China, India’s IT-services expansion, and supportive regulation push Asia Pacific growth to a 14.69% CAGR.

How concentrated is vendor competition?

The top five providers account for roughly 45% of revenue, yielding a moderate market concentration score of 6.

Which industry vertical is set to record the highest growth rate?

Healthcare and life sciences is forecast to grow at a 14.11% CAGR as analytics tackle nurse turnover and staffing costs.

Page last updated on: