Germany Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

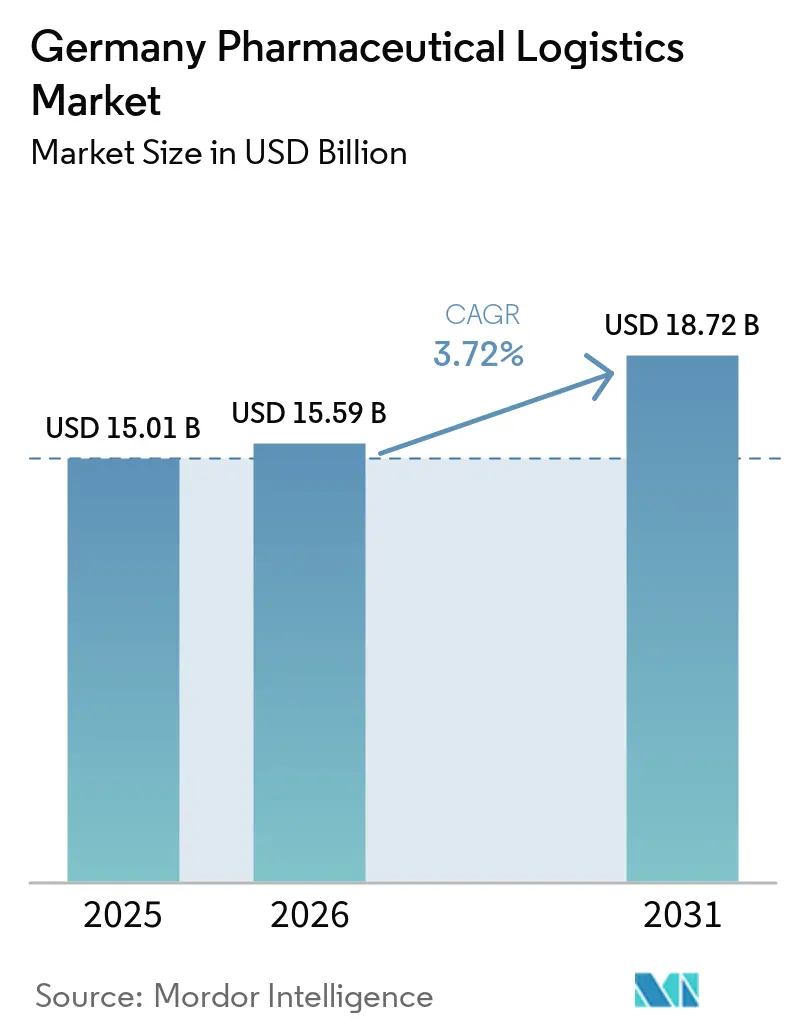

| Base Year Market Size (2025) | USD 15.01 Billion |

| Market Size (2026) | USD 15.59 Billion |

| Market Size (2031) | USD 18.72 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

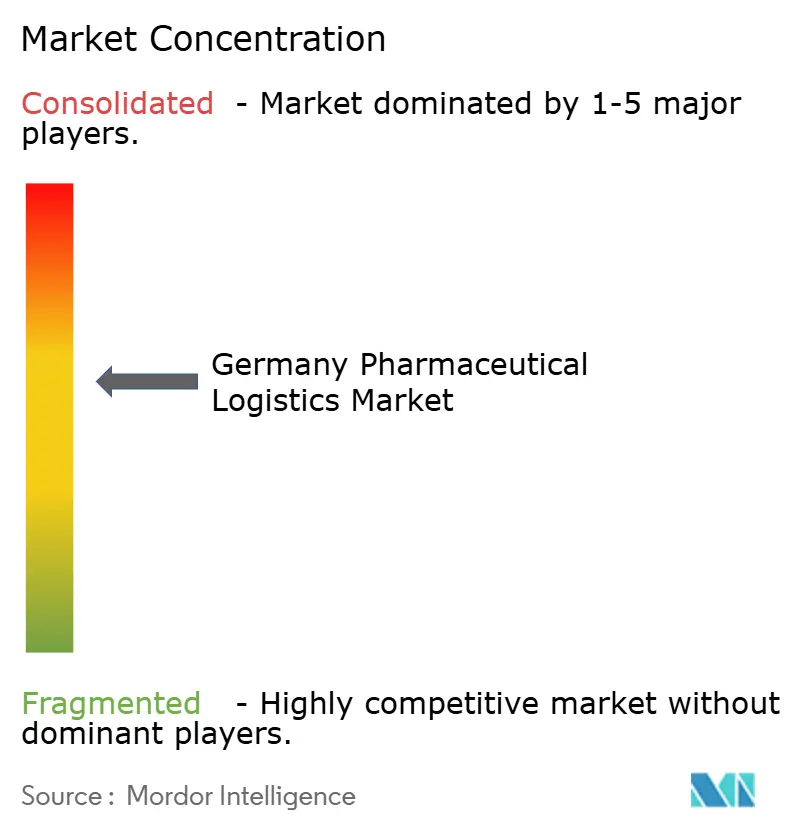

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The Germany pharmaceutical logistics market size is expected to increase from USD 15.01 billion in 2025 to USD 15.59 billion in 2026 and reach USD 18.72 billion by 2031, growing at a CAGR of 3.72% over 2026-2031.

The Germany pharmaceutical logistics market is expanding in a period when Germany’s wider economy remains subdued, with GDP rising only 0.2% in 2025 and energy price risks still weighing on near-term industrial output. Demand remains steady because pharmaceutical distribution is tied more closely to healthcare consumption and regulated supply needs than to the freight cycles seen in automotive and industrial chains. The Germany pharmaceutical logistics market is also benefiting from the nationwide shift toward digital prescription fulfillment, which is increasing parcel-scale pharmacy distribution and tightening the link between prescription data, replenishment planning, and last-mile delivery. Growth opportunities are moving toward compliant cold-chain handling, patient-specific logistics, serialization support, and specialized flows linked to biosimilars and advanced therapies, while contract awards increasingly reflect certification depth rather than price alone. The main pressure points for the market are still structural, with high cold-chain energy costs and shortages of GDP-qualified drivers and technicians limiting capacity expansion for operators that lack scale, training systems, and multi-temperature infrastructure.

Key Report Takeaways

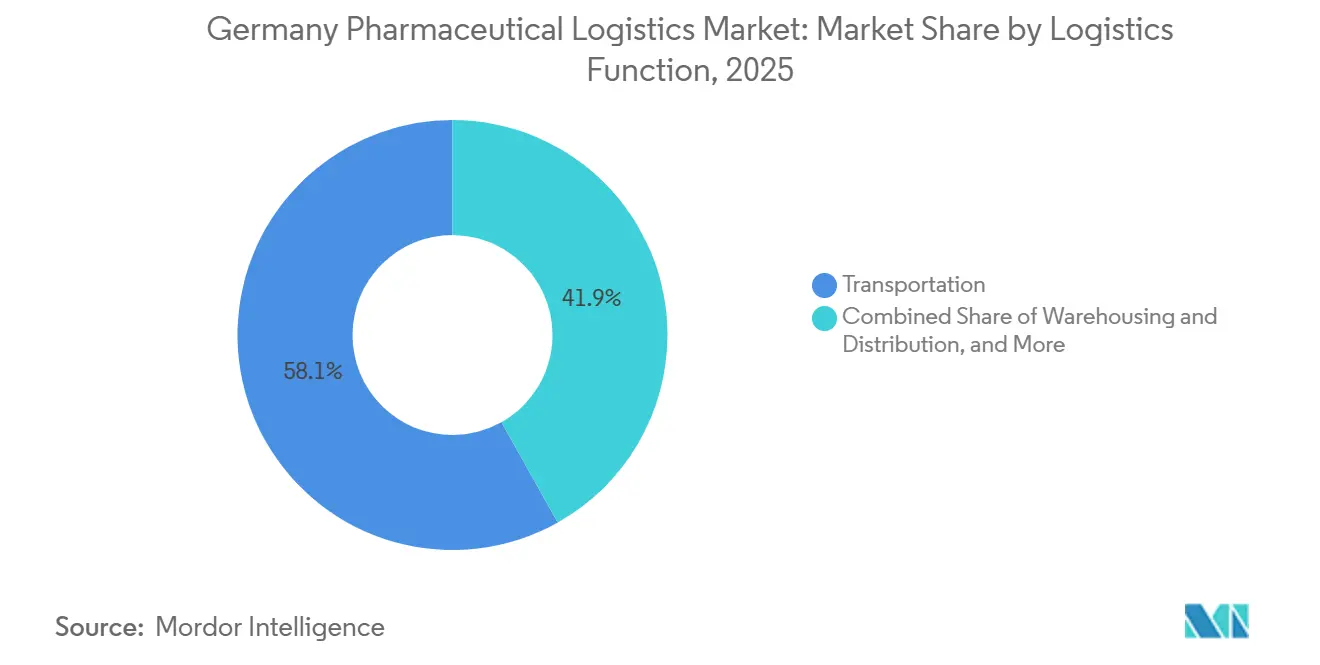

- By logistics function, transportation held 58.14% of the Germany pharmaceutical logistics market size in 2025, while value-added services recorded the highest projected CAGR at 6.55% through 2031.

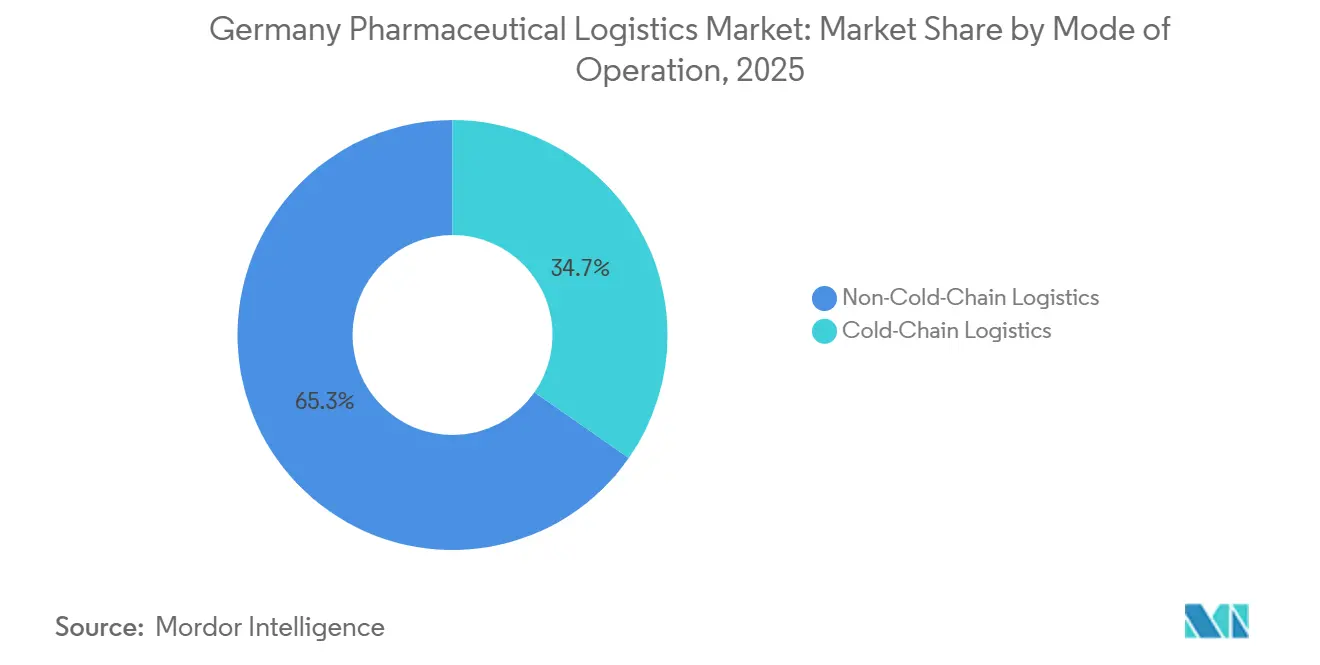

- By mode of operation, non-cold-chain logistics accounted for 65.30% of the Germany pharmaceutical logistics market share in 2025, while cold-chain logistics is forecast to expand at a 5.72% CAGR through 2031.

- By product type, prescription drugs captured 42.89% of the Germany pharmaceutical logistics market share in 2025, while cell and gene therapies are projected to grow at a 6.86% CAGR through 2031.

- By geography, North Rhine-Westphalia represented 34.29% of the Germany pharmaceutical logistics market size in 2025, while Bavaria is expected to post the fastest CAGR at 5.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding biologics and biosimilars pipeline adoption | +1.2% | National, concentrated in Bavaria and Baden-Württemberg pharma clusters | Medium term (2-4 years) |

| Nation-wide roll-out of Germany's e-prescription system | +0.8% | National, with early gains in Hamburg, Berlin, Munich | Short term (≤ 2 years) |

| Stringent enforcement of EU GDP 2022/993 compliance audits | +0.5% | EU-wide, enforced by Germany's state-level competent authorities | Medium term (2-4 years) |

| Growth of specialty pharmacies pushing same-day delivery models | +0.6% | National, concentrated in major urban centers including Berlin, Hamburg, Munich, and Cologne | Short term (≤ 2 years) |

| Hydrogen-powered temperature-controlled truck pilots on autobahn | +0.3% | North Rhine-Westphalia, Baden-Württemberg, Bavaria | Long term (≥ 4 years) |

| Blockchain-enabled serialization pilots beyond fmd mandates | +0.2% | EU-wide, with active piloting activity in Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Biologics and Biosimilars Pipeline Adoption

The Germany pharmaceutical logistics market is seeing a sharper shift toward cold-chain complexity as biologics and biosimilars move deeper into routine dispensing. Germany’s pharmacy substitution framework for biosimilars took effect from April 1, 2026, which increased the need for precise lot tracking, controlled handovers, and clear chain-of-custody records at the pharmacy level. That change matters because it does not simply add volume to established wholesale lanes, it shifts more shipments into smaller and more frequent pharmacy-level consignments that are harder to manage with standard networks. The Germany pharmaceutical logistics market is therefore rewarding providers that can manage +2 °C to +8 °C, frozen, and cryogenic ranges inside one validated operating model. This is especially relevant in Bavaria and Baden-Wurttemberg, where biologics production, plasma handling, and specialty manufacturing are pushing demand for more specialized storage and transport. The commercial pipeline for advanced therapies is also raising the bar, as operators must demonstrate they can document every handoff and maintain temperature integrity throughout the full route in line with EU GDP requirements[1]“Germany 2025 Energy Policy Review,” International Energy Agency, iea.org .

Nation-Wide Roll-Out of Germany's E-Prescription System (eRezept)

The Germany pharmaceutical logistics market is being reshaped by eRezept because prescription fulfillment is now more digital, faster, and easier to route into home delivery and mail-order channels. Germany crossed 1 billion cumulative eRezept redemptions on October 17, 2025, demonstrating how quickly the digital prescription system had scaled since the mandatory rollout began in 2024. This shift is changing the mix of shipments from larger scheduled wholesale drops toward higher-frequency parcel flows that still need GDP-compliant handling. It is also improving demand visibility because pharmacy and prescription data are now available much earlier in the ordering cycle than they were in the paper-based model. That earlier signal allows logistics operators and specialty pharmacies to pre-position stock nearer to high-demand urban districts and reduce replenishment lead times. The Germany pharmaceutical logistics market is therefore seeing stronger value in warehouse management systems that can connect prescription data with stock planning, route scheduling, and temperature-specific inventory allocation.

Stringent Enforcement of EU GDP 2022/993 Compliance Audits

The Germany pharmaceutical logistics market is becoming harder to enter because GDP compliance is once again being enforced through full on-site inspection activity across the EEA. The blanket extensions that had kept some certificates alive are no longer in place, and inspection focus has returned to physical storage conditions, temperature continuity, documentation quality, and data integrity. Non-compliance reporting in 2025 showed recurring failures in cold-chain storage and responsible person oversight, including a suspension in Germany tied to inadequate storage controls. The Germany pharmaceutical logistics market is therefore treating GDP authorization as a legal access requirement rather than a quality badge. Larger integrators have an advantage because they can support recurring audits, cross-site harmonization, and data integrity controls across a wider network. Smaller carriers and warehouse operators face a tougher path because any documentation gap can now limit access to prescription pharmaceutical contracts[2]“Questions and Answers from the ECA Webinar GDP Update 2026 Part 1,” European GDP Association, gmp-compliance.org.

Growth of Specialty Pharmacies Pushing Same-Day Delivery Models

The Germany pharmaceutical logistics market is also gaining support from the growth of specialty pharmacies that need same-day delivery for therapies with short handling windows and patient-specific dispensing requirements. These flows are concentrated in oncology, immunology, and rare disease treatment pathways, where speed matters but GDP compliance still cannot be relaxed. The move to eRezept has removed paper delays that once slowed this channel, pushing some urgent orders into less structured courier models[3]“GDP Update 2025/2026,” GMP Journal, gmp-journal.com. Eurotranspharma’s expansion to 13 German locations, with a target of 30 sites, demonstrates the network density required to meet this demand with dual-temperature transport and compliant timing. The real limit is workforce availability, because same-day GDP distribution needs trained drivers who can manage deviations, documentation, and patient-facing delivery steps on short routes. This means the Germany pharmaceutical logistics market favors providers that build their own trained delivery base rather than relying fully on subcontractors for hyperlocal specialty distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating energy costs for cold-chain warehousing | -0.5% | National, most acute in North Rhine-Westphalia and Bavaria logistics hubs | Short term (≤ 2 years) |

| Complex multi-agency permitting for last-mile urban deliveries | -0.3% | Berlin, Hamburg, Munich, Frankfurt, Cologne | Medium term (2-4 years) |

| Shortage of GDP-certified drivers and warehouse technicians | -0.4% | National, critical in major pharmaceutical distribution corridors | Short term (≤ 2 years) |

| Limited regulatory pathways for medical-grade drone corridors | -0.2% | National, experimental corridors only | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Energy Costs for Cold-Chain Warehousing

The Germany pharmaceutical logistics market remains exposed to high energy prices because cold-chain warehouses consume far more electricity than ambient facilities. Germany continues to have some of the highest industrial power costs in Europe, placing a direct burden on operators of refrigerated and frozen pharmaceutical sites. This cost issue is becoming more serious as facilities also prepare for refrigerant transition requirements, which add capital spending for low-GWP systems and related equipment upgrades. A reported example from the sector showed that switching to a blended power procurement model with wind PPA exposure reduced costs and avoided 1,900 tons of CO₂ in one reporting period. Even so, hedging and energy transition programs compete for the same capital that operators need for GDP upgrades, monitoring systems, and new cold rooms. The Germany pharmaceutical logistics market, therefore, gives a clear edge to providers with stronger balance sheets, because they can fund energy adaptation and compliance investment at the same time.

Shortage of GDP-Certified Drivers and Warehouse Technicians

The Germany pharmaceutical logistics market faces a structural labor shortage that is more restrictive than the weakness seen in some other freight segments. The sector was reported to be missing 176,000 qualified logistics workers in 2025, including 70,000 truck drivers with the competencies needed for GDP-compliant pharmaceutical handling. This matters because GDP work is not standard freight labor, and personnel must be trained to manage deviations, temperature events, chain-of-custody controls, and emergency documentation. Training cycles are lengthy, and the retirement of experienced staff is still outpacing the number of newly qualified workers entering the system. Large operators can spread these certification costs across national networks, but regional carriers cannot do so as easily. As a result, the Germany pharmaceutical logistics market is becoming more concentrated in the most sensitive lanes, especially where audited cold-chain performance and trained last-mile execution are both required.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Value-Added Services Outpace Core Transportation

Transportation held 58.14% of Germany pharmaceutical logistics market share in 2025, which kept it as the largest logistics function in the Germany pharmaceutical logistics market. Road distribution remained the core because Germany’s pharmacy, hospital, wholesale, and manufacturing networks require dense domestic coverage and frequent replenishment runs. Air freight kept its role in high-value and time-critical shipments such as advanced therapies, clinical trial materials, and short-stability biologics that need rapid airport-to-care-site movement. Rail and sea-linked flows remained more relevant for import-side handling of bulk materials and selected upstream pharmaceutical inputs.

Warehousing and distribution continued to hold a stable middle position because GDP-certified multi-temperature sites near Autobahn corridors are still central to national service design. The fastest shift came from value-added services, which are projected to expand at a 6.55% CAGR and therefore show the fastest growth in the Germany pharmaceutical logistics market through 2031. Pharmaceutical shippers are increasingly outsourcing serialization aggregation, returns control, deviation handling, artwork support, and patient-specific kitting to providers that can combine compliance systems with physical handling[4]“GDP Update for 2024/2025,” GMP Journal, gmp-journal.com. DHL’s EUR 2 billion (USD 2.35 billion) investment in the health logistics underlined how strongly large operators are backing clinical, biopharma, and advanced therapy support services inside the Germany pharmaceutical logistics market.

By Mode of Operation: Cold-Chain Momentum Accelerates Against a Non-Cold-Chain Base

Non-cold-chain logistics accounted for 65.30% of the Germany pharmaceutical logistics market share in 2025, supported by high volumes of ambient prescription medicines, OTC products, and standard medical device shipments. This mode remains the economic backbone of the Germany pharmaceutical logistics industry because it uses less energy, simpler documentation, and more standard fleet deployment than temperature-sensitive lanes. The rise in parcel-scale prescription fulfillment is also supporting ambient flows, especially where mail-order and direct-to-home volumes include OTC products and standard-temperature prescriptions. Those advantages keep non-cold-chain networks central to daily replenishment across national pharmacy and hospital channels.

Cold-chain logistics is forecast to expand at a 5.72% CAGR, which means this part of the Germany pharmaceutical logistics market size is growing faster than the overall market. That premium reflects the increasing commercial weight of biosimilars, biologics, and advanced therapies that need validated +2 °C to +8 °C, frozen, or cryogenic conditions across handoffs. The biosimilar substitution framework that took effect in April 2026 adds more temperature-sensitive pharmacy-level movements and tighter requirements for documented continuity. Operators now need validated packaging, calibrated monitoring, and documented deviation response systems that many smaller firms still struggle to maintain. DHL’s Florstadt expansion, with capability down to −70 °C, showed the level of infrastructure that customers now use as a benchmark in the Germany pharmaceutical logistics industry.

By Product Type: Cell and Gene Therapies Lead Fastest Product Growth

Prescription drugs accounted for 42.89% of the Germany pharmaceutical logistics market share in 2025, making them the largest product category by revenue. This position reflects Germany’s scale in ethical pharmaceutical dispensing and the steady need for recurring prescription distribution across retail, hospital, and wholesale networks. Their logistics profile is still defined by frequent movement, broad domestic reach, and dependable compliance rather than extreme handling complexity in most cases. OTC drugs, veterinary products, and medical devices added steady volumes, while clinical trial materials remained smaller in volume but higher in handling intensity.

Cell and gene therapies are projected to grow at a 6.86% CAGR, making them the fastest-growing product group in the German pharmaceutical logistics market through 2031. These therapies require patient-specific scheduling, very short timing windows, and uninterrupted cryogenic handling, so the value of per-shipment logistics is much higher than in standard pharmaceutical flows. Germany’s university hospital network is becoming increasingly important in administrative pathways, shifting logistics requirements toward precise point-of-care coordination rather than bulk distribution. Specialized operators such as Marken and World Courier have built ATMP capabilities in Germany, while DHL has positioned Florstadt as a major European anchor for advanced therapy handling with clean-room support and deep temperature control.

Geography Analysis

North Rhine-Westphalia led with 34.29% of the Germany pharmaceutical logistics market share in 2025, which reflects the region’s role as the main logistics and manufacturing anchor inside the Germany pharmaceutical logistics market. The Rhine-Ruhr corridor combines dense motorway links, major wholesale activity, and a concentration of GDP-certified sites that support both high-frequency domestic delivery and international transit. This gives NRW an advantage in network efficiency because providers can serve pharmacies, hospitals, and industrial customers from closely linked nodes rather than from scattered facilities. FedEx’s CEIV Pharma certification for Cologne and Frankfurt further supported western Germany’s position in temperature-sensitive air cargo handling and added credibility for globally integrated providers working across the region.

Bavaria is the fastest-growing regional part of the Germany pharmaceutical logistics market, with a projected CAGR of 5.10% through 2031. The region’s growth is tied to the expansion of southern Germany’s biopharma base, especially around Munich and Ingolstadt, where commercial-stage biologics and advanced therapies are creating demand for closer cold-chain support. Munich Airport is gaining from this pattern because it reduces exposure to long inland transfer times for imported temperature-sensitive products. Lufthansa Cargo’s CEIV Pharma recertification, valid through April 2029, supports Bavaria’s role as a reliable international gateway for these flows. Cross-border infrastructure is also strengthening the southern corridor, with CEVA’s new Strasbourg-Entzheim pharmaceutical facility supporting GDP-compliant flows into Baden-Württemberg and Bavaria from the French side of the border.

Baden-Württemberg remains important because its specialty pharma and medtech footprint generates regular demand for controlled warehousing, domestic distribution, and cross-border handling within the Germany pharmaceutical logistics market. The rest of the states are smaller as a group, but they still add meaningful incremental demand through Hamburg’s temperature-controlled sea freight role, Hessen’s large 3PL campus ecosystem, and Berlin’s home-delivery pharmacy activity. Frankfurt continues to matter for air cargo, customs clearance, and access to surrounding temperature-controlled campus infrastructure, which supports nationwide distribution after international arrival. Geography is therefore not only a question of local demand, it is also a question of where operators can combine certified warehousing, airport access, road density, and specialized labor. That is why the Germany pharmaceutical logistics market continues to reward providers with balanced coverage across western, southern, and gateway regions rather than relying on a single cluster.

Competitive Landscape

The Germany pharmaceutical logistics market has a layered competitive structure rather than a winner-takes-most pattern. Global integrators such as DHL Group, DSV, Kuehne+Nagel, UPS Healthcare, and FedEx operate at the top end by combining multimodal reach with audited GDP processes and multi-temperature assets. A second group, including CEVA Logistics, GEODIS, DACHSER, Hellmann, and Fiege, competes through sector specialization, depth of compliance, and selected network strengths. Below them, Germany-focused specialists such as Pharmaserv, PharmLog, LOXXESS, UNITAX, and Transpharm hold defensible positions in regional distribution and narrower specialty flows. No single provider holds a majority share in the Germany pharmaceutical logistics market, so contract wins depend more on certification records, cold-chain performance, and advanced therapy capability than on simple price competition.

Recent consolidation has raised the competitive bar in the Germany pharmaceutical logistics market. DSV completed the acquisition of DB Schenker in April 2025, and the combined business began operative integration in Germany in January 2026, making this the most consequential consolidation move in the sector for years. DHL responded with continued infrastructure investment, including the expansion of its Florstadt campus and a broader Health Logistics spending plan aimed at biopharma, clinical, and cell and gene therapy support. UPS also moved to strengthen its position through acquisitions tied to cold-chain scale and end-to-end healthcare visibility. Together, these moves show that scale is becoming more important, but only where it is matched by audited handling quality.

Technology and process control are now central to retention and pricing in the Germany pharmaceutical logistics market. Providers are investing in real-time temperature monitoring, serialization support, and stronger data integration because pharmaceutical shippers now expect visibility at the shipment and batch level. Kuehne+Nagel’s healthcare expansion in Hamburg and its broader HealthChain quality positioning show how operators are using certification-backed service models to protect premium accounts. FedEx is doing the same through network-wide healthcare certification, while specialists still compete effectively where they offer deep local knowledge or focused therapy expertise. There is still open space in ATMP point-of-care logistics for smaller university hospitals and in GDP-certified same-day delivery for rural specialty pharmacy routes, which means the Germany pharmaceutical logistics market remains competitive even as entry barriers rise.

Germany Pharmaceutical Logistics Industry Leaders

DHL Group

FedEx

DSV A/S

United Parcel Service of America, Inc. (UPS)

Kuehne+Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group expands airfreight cold-chain network with dedicated Boeing 777 freighter on Brussels–Cincinnati route. As part of its EUR 2 billion DHL Health Logistics investment, DHL deployed a dedicated Boeing 777 freighter to provide predictable temperature-controlled capacity for pharmaceuticals, vaccines, and advanced therapies including cell and gene therapy products, reinforcing its end-to-end cold-chain offering across the Atlantic corridor.

- November 2025: UPS Healthcare completes USD 1.60 billion acquisition of Andlauer Healthcare Group, adding 31 temperature-controlled facilities. UPS finalized the acquisition of Andlauer Healthcare Group for USD 1.60 billion, adding a specialized North American cold-chain network to UPS Healthcare's global pharmaceutical logistics footprint and strengthening end-to-end visibility and quality assurance for trans-Atlantic pharmaceutical flows.

- November 2025: Daimler Truck GenH2 hydrogen truck entered the second customer trial phase with Teva Germany for pharmaceutical transport. Daimler Truck launched the second customer testing phase of its Mercedes-Benz GenH2 hydrogen fuel-cell truck, with Teva Germany deploying the 40-tonne vehicle for long-haul temperature-controlled pharmaceutical deliveries to hospitals, wholesalers, and pharmacies across Germany, and Rhenus Logistics integrating a GenH2 unit at its Duisburg site for pharmaceutical and general cargo routes.

- September 2025: Kuehne+Nagel opens 10,000 sqm dedicated healthcare distribution center for Sysmex in Hamburg. Kuehne+Nagel inaugurated a multi-temperature-zone healthcare distribution center in Hamburg for Sysmex Europe SE and Sysmex Deutschland GmbH, providing direct-to-customer delivery across parts of Europe, EMEA region supply, and same-day urgent air freight export dispatch for diagnostic instruments and reagents.

Germany Pharmaceutical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States |

Key Questions Answered in the Report

What is the size of Germany pharmaceutical logistics in 2026 and where will it reach by 2031?

The Germany pharmaceutical logistics market stands at USD 15.59 billion in 2026 and is projected to reach USD 18.72 billion by 2031, growing at a CAGR of 3.72% over 2026-2031.

Which logistics function leads revenue in Germany pharmaceutical logistics?

Transportation is the largest function, holding 58.14% of 2025 revenue, because the country depends on dense road-based distribution across pharmacies, hospitals, and wholesale networks.

Which logistics function of the market is growing the fastest?

Value-added services are growing the fastest by logistics function at a 6.55% CAGR, while cell and gene therapies lead product growth at a 6.86% CAGR through 2031.

Why is cold-chain becoming more important in Germany?

Cold-chain logistics is forecast to grow at a 5.72% CAGR, faster than the overall market, because biologics, biosimilars, and advanced therapies need stricter temperature control and traceability.

Which German region is the largest and which is growing the fastest?

North Rhine-Westphalia is the largest regional market with a 34.29% share in 2025, while Bavaria is the fastest-growing region with a 5.10% CAGR through 2031.

What are the main risks for pharmaceutical logistics providers in Germany?

The main risks are high cold-chain energy costs and shortages of GDP-qualified drivers and warehouse technicians, which raise operating costs and limit network expansion.

Page last updated on: