Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

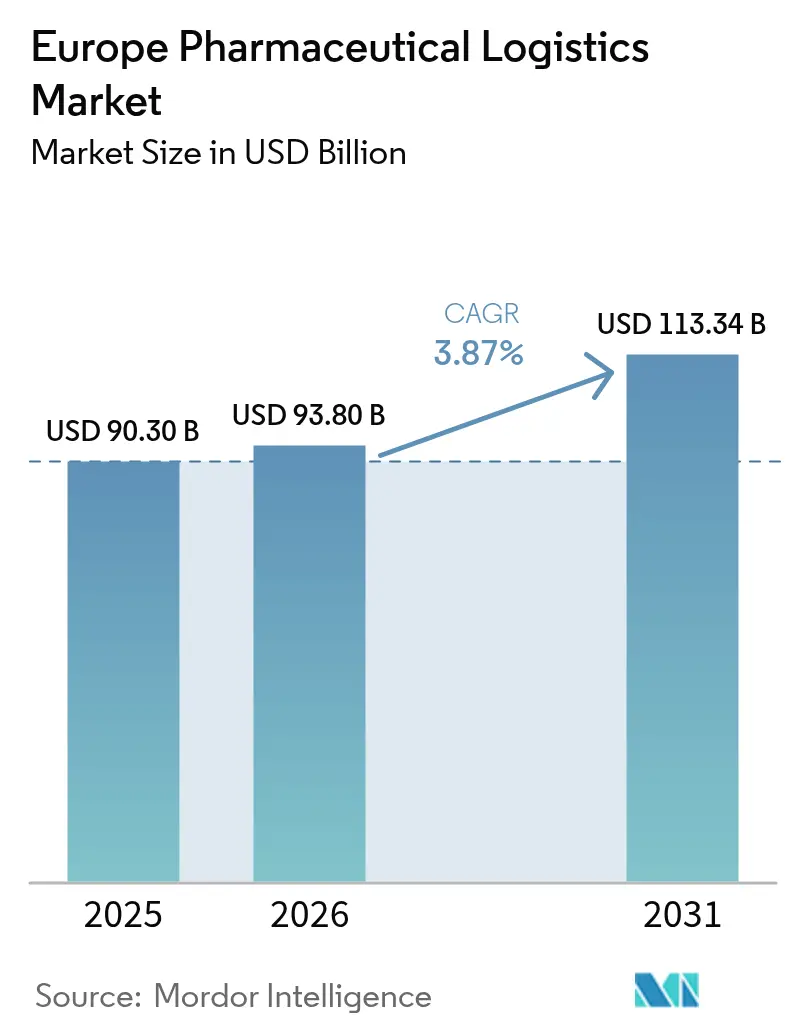

| Base Year Market Size (2025) | USD 90.30 Billion |

| Market Size (2026) | USD 93.8 Billion |

| Market Size (2031) | USD 113.34 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

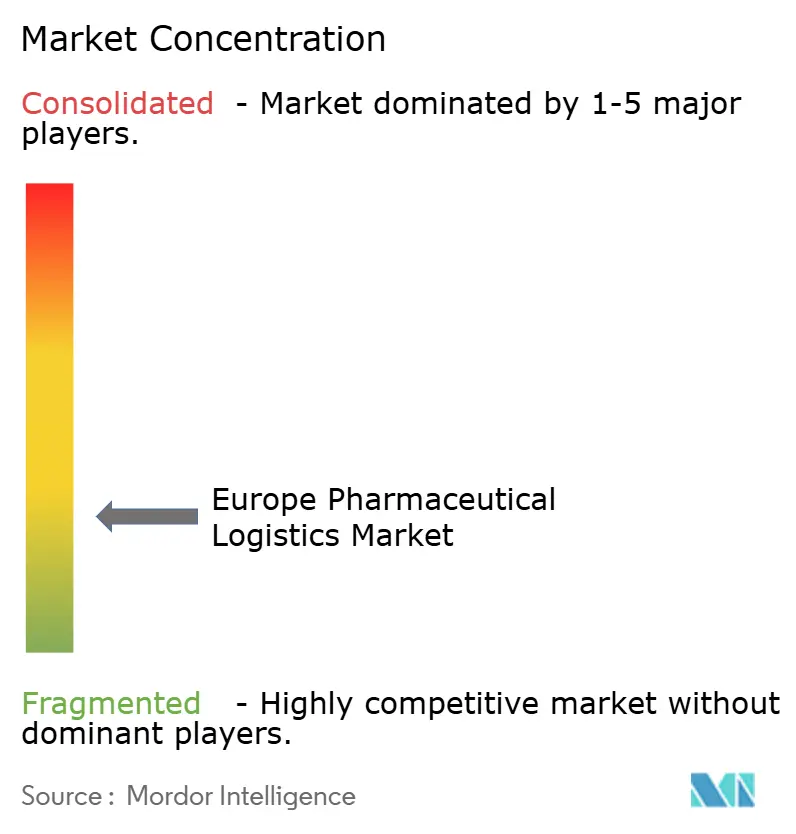

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pharmaceutical Logistics Market Analysis by Mordor Intelligence

Europe Pharmaceutical Logistics Market size in 2026 is estimated at USD 93.8 billion, growing from 2025 value of USD 90.30 billion with 2031 projections showing USD 113.34 billion, growing at 3.87% CAGR over 2026-2031.

Heightened EU Good Distribution Practice (GDP) enforcement, Brexit-related border friction, and the accelerating demand for temperature-controlled supply chains for biologics are reshaping service models, while record public investment in rail freight and inland waterways is reshuffling modal choices. Consolidation among third-party logistics providers (3PLs) is intensifying, led by DSV’s EUR 14.3 billion (USD 15.78 billion) purchase of DB Schenker in April 2025, which signals the emergence of mega-scale providers with global reach. At the same time, a region-wide driver shortage exceeding 500,000 professionals and escalating energy costs for refrigerants are diluting operating margins and encouraging automation investments[1]“Freight transport activity,” European Environment Agency, eea.europa.eu . Demand for value-added services such as end-to-end visibility, regulatory documentation, and reverse logistics is surging as pharmaceutical shippers seek risk mitigation and quality assurance.

Key Report Takeaways

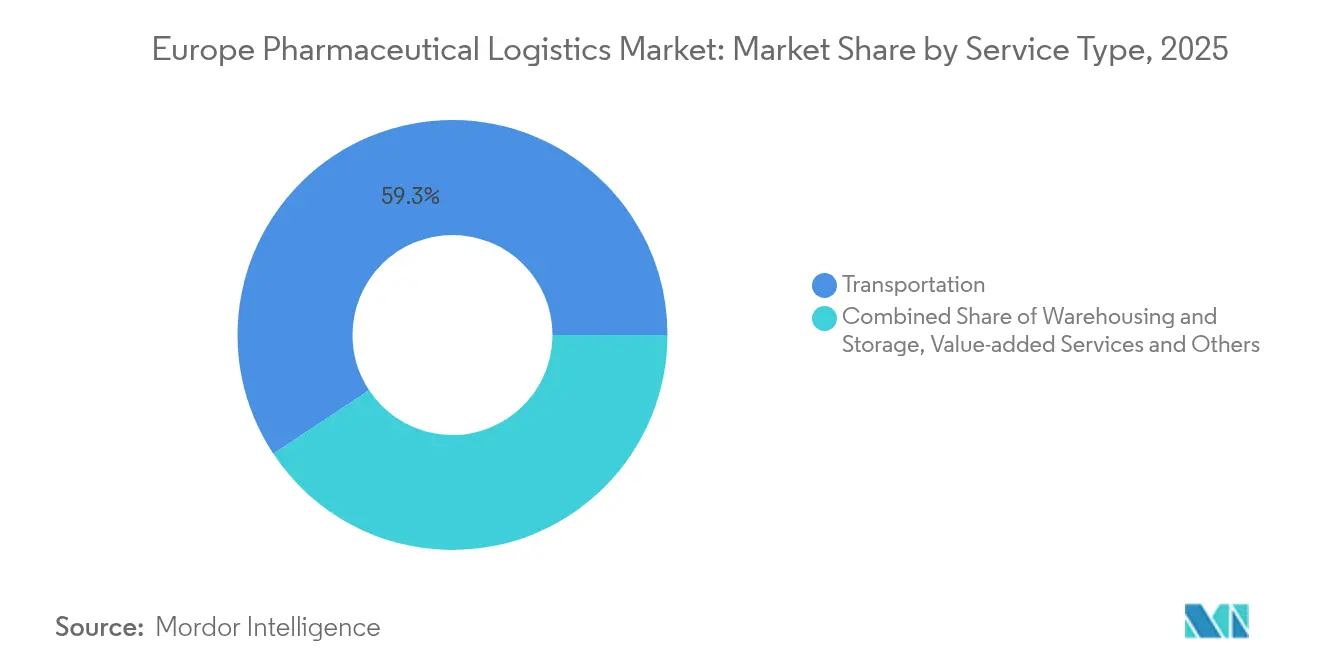

- By service type, transportation held 59.32% of Europe pharmaceutical logistics market share in 2025, while value-added services are forecast to grow at a 4.88% CAGR to 2031.

- By mode of operation, cold-chain logistics led with a 57.42% share of the Europe pharmaceutical logistics market size in 2025; non-cold-chain operations are expected to expand at a 4.44% CAGR through 2031.

- By product type, prescription drugs accounted for 31.35% of Europe pharmaceutical logistics market share in 2025, whereas vaccines and blood products are advancing at a 5.53% CAGR between 2026-2031.

- By geography, Germany captured 16.62% of Europe pharmaceutical logistics market size in 2025, and Poland is projected to record the fastest 4.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of biologics & temperature-sensitive drugs | +1.2% | Germany, Netherlands, Denmark | Long term (≥4 years) |

| Surge in e-commerce/OTC fulfillment volumes | +0.8% | Western Europe and CEE | Medium term (2-4 years) |

| Stricter EU GDP & serialization enforcement | +0.6% | EU-27 and UK | Short term (≤2 years) |

| Outsourcing to 3PL/4PL pharma-specialists | +0.7% | Pan-European | Medium term (2-4 years) |

| Green Deal modal-shift incentives | +0.3% | TEN-T corridors | Long term (≥4 years) |

| Rise of cell & gene therapy requiring ultra-cold chain | +0.4% | Nordics and Germany | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth of Biologics & Temperature-Sensitive Drugs

Biologics, cell, and gene therapies are expanding faster than the broader life-sciences sector, with biopharma volumes growing at double-digit rates and pushing the share of cold-stored medicines to 35% of total pharmaceutical value in 2022. Nordic manufacturers such as Novo Nordisk and Fujifilm Diosynth are investing over DKK 70 billion (USD 10.36 billion) in capacity, creating fresh demand for GDP-certified storage and -80°C transport lanes. To curb cost and emission pressures, shippers are pivoting from air to ocean freight when lead-time and product risk profiles allow. Advanced therapy medicinal products (ATMPs) now drive ultra-cold packaging innovations, while Sweden’s 146 CAR-T treatments in 2024 highlight the scale-up of personalized medicine workflows.

Surge in E-commerce/OTC Fulfillment Volumes

Europe’s e-pharmacy sector is projected to expand by 65% by 2028 as Germany, the UK, and France roll out e-prescription networks and AI-based order routing. Growth in home health services for an aging population requires time-defined, temperature-controlled last-mile deliveries. Logistics specialists such as Eurotranspharma have launched dedicated line-haul and city-distribution fleets to ensure GDP compliance down to the patient doorstep. Counterfeit risk and patchwork rules for controlled substances continue to constrain cross-border volume flows, but harmonized data-sharing platforms are mitigating compliance burdens.

Stricter EU GDP & Serialization Enforcement

Updated GDP guidelines effective January 1 2025 eliminate pandemic-era certificate extensions and restore on-site audits, forcing operators to modernize quality-management systems GMP[2]“Half of European truck operators can’t expand due to driver shortages,” IRU, iru.org . Italy’s February 9 2025 serialization deadline is galvanizing late-stage system upgrades across Southern Europe. The UK’s Windsor Framework introduces “UK Only” labels, adding cross-border documentation layers that ripple through warehousing and transport contracts.

Outsourcing to 3PL/4PL Pharma-Specialists

Rising product complexity is nudging shippers toward external logistics partnerships. Major 3PLs have responded with GDP-certified mega-hubs, predictive control-tower platforms, and GDP-trained cold chain crews. Providers such as DHL and CEVA have committed multi-billion-euro capex programs to upgrade European health-care networks, while clinical-trial sponsors rely on niche specialists for “vein-to-vein” traceability in cell-therapy programs.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy & refrigerant costs for cold-chain assets | −0.9% | EU-wide, notably Germany, Netherlands | Short term (≤2 years) |

| Driver shortages and road-capacity constraints | −1.1% | Germany, France, Benelux, CEE | Medium term (2-4 years) |

| Brexit-related border friction & paperwork | −0.4% | UK-EU corridors | Medium term (2-4 years) |

| Limited ultra-cold infrastructure in CEE & Nordics | −0.3% | CEE, Nordic periphery | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Energy & Refrigerant Costs for Cold-Chain Assets

EU F-gas quota curbs and a multi-year surge in R452A prices up to 1,000% since 2014 are inflating operating outlays for reefer fleets[3]“Guidelines on Good Distribution Practice,” European Commission, gmp-compliance.org. OEMs such as Carrier Transicold have levied surcharges from January 2025 and plan lower-GWP blends later in the year. Power-price volatility, despite stabilizing LNG imports, is still eroding margins, spurring investments in solar-assisted depots and hydrocarbon refrigerants[4]“High GWP refrigerants face soaring prices,” Green Cooling Initiative, green-cooling-initiative.org.

Driver Shortages and Road-Capacity Constraints

Europe lacks more than 500,000 qualified heavy-vehicle drivers today, a gap projected to widen to 745,000 by 2028, limiting fleet utilization and inflating wages. Germany faces the steepest deficit, with only 2.6% of its driver cohort younger than 25 years. Congestion on aging motorway corridors and rising tolls linked to CO₂ classes further curb productivity. Modal diversification can alleviate but not fully offset the labor crunch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Drives Infrastructure Investment

Transportation services accounted for 59.32% of Europe pharmaceutical logistics market share in 2025, underscoring the sector’s dependence on road, air, ocean, and rail capacity. Value-added services, though a smaller pool, are forecast to contribute USD 14.79 billion to Europe pharmaceutical logistics market size by 2031, expanding at 4.88% CAGR as shippers seek batch-level tracking, regulatory documentation, and kitting support. Road haulage moves the lion’s share of medicines, yet EU toll hikes pegged to CO₂ classes are tightening margins and accelerating fleet renewal toward battery-electric and hydrogen drivelines. Airfreight operators are retrofitting unit-load devices to meet ReFuelEU mandates for 2% sustainable aviation fuels from 2025, while ocean carriers leverage FuelEU Maritime rules to pitch lower-carbon temperature-controlled containers.

Automation and digitalization define future warehousing value creation. Fully robotized Nordic depots can move 1,000 pallets per hour, reducing human error and improving batch traceability. Meanwhile, the EUR 7 billion EU infrastructure package is expanding rail freight capacity, with the Lyon-Turin tunnel slated to boost inter-alpine pharmaceutical flows once operational. Overall, the service mix is shifting from pure transport toward integrated, temperature-controlled orchestration, allowing operators to lock-in multi-year contracts and stabilize revenue.

By Mode of Operation: Cold-Chain Complexity Reshapes Service Models

Cold-chain solutions held 57.42% of Europe pharmaceutical logistics market size in 2025 due to the proliferation of biologics, vaccines, and precision therapies. However, non-cold-chain lanes will register a 4.44% CAGR to 2031 as reformulated room-temperature-stable biologics and OTC categories gain traction. Heatwaves and storms in 2024 exposed vulnerabilities in older reefer fleets, prompting accelerated rollout of solar-powered depots and next-generation eutectic plates. Logistics leaders such as CEVA project reusable packaging penetration to reach 70% by 2030, lowering waste and carbon budgets.

Ultra-cold shipments for cell and gene therapies remain capacity-constrained east of Germany. Cold Chain Technologies’ new Breda plant adds multi-format shipper production and cuts lead times across the Benelux and CEE by two days. Non-cold-chain services, while operationally less complex, must still meet GDP traceability mandates, leading to increased adoption of IoT sensors even for ambient cargo.

By Product Type: Prescription Drugs Anchor Growth While Vaccines Accelerate

Prescription medicines retained the largest 31.35% tranche of Europe pharmaceutical logistics market share in 2025, reflecting high chronic-care volumes and established procurement channels. Vaccines and blood products, stewarded by expanding immunization programs and pandemic-preparedness stockpiling, will outpace all other categories at 5.53% CAGR through 2031. Biologics and biosimilars demand specialized handling, driving cold-chain capex throughout Western Europe. Germany’s pharmaceutical market is forecast to add USD 28 billion between 2024 and 2032 on the back of biopharmaceutical plant expansions and personalized therapy adoption.

Clinical trial materials face new labeling freedoms under the Clinical Trial Regulation, which allows hospital relabeling to cut waste but raises chain-of-custody complexity. Cell and gene therapies require vein-to-vein orchestration, and medical centers are ramping cryopreservation and RFID-tagging capacity to manage donor-patient pairings. Medical devices, spurred by EUDAMED rollout in 2026, will call for harmonized UDI data flows that integrate with logistics control towers.

Geography Analysis

Germany generated 16.62% of Europe pharmaceutical logistics market size in 2025, leveraging its 13,000 km motorway grid and status as a manufacturing nucleus. Toll extensions to vehicles over 3.5 tons from July 2024 add cost pressure but accelerate efficiency drives in fleet telematics and alternative fuels. The United Kingdom contends with chronic drug shortages and higher import paperwork despite Windsor Framework mitigations, which streamline licensing yet impose UK-only labeling for mainland trade. The Netherlands exploits Rotterdam’s cold-chain port cluster and Schiphol’s Pharma Gateway corridor to attract high-value biologic traffic.

Poland, the fastest growing geography at a 4.73% CAGR to 2031 is modernizing motorway and rail hubs to become a CEE consolidation point. Italy, facing its February 2025 serialization deadline, channels capex into track-and-trace IT ahead of regulatory cut-offs. Spain links GDP-compliant logistics incentives to CO₂-indexed toll reform, while Sweden leads in battery-electric truck adoption, supported by Eurovignette tariffs pegged to emissions from March 2025. Rest-of-Europe markets, particularly Hungary and Romania, offer greenfield opportunities for ultra-cold storage networks where incumbents are scarce.

Regulatory Landscape

Pharmaceutical logistics in Europe is governed by the EU quality framework for medicinal products, with mandatory Good Distribution Practice (GDP) as the core operating standard for storage, handling, and transport under the EU GDP guidelines (2013/C 343/01). Wholesale distributors operating in the EEA must hold a wholesale distribution authorization issued by the national competent authority in the country of activity, and GDP compliance is central to maintaining these authorizations. This shapes audit readiness, documentation, and the qualification of transport lanes and subcontractors.

In 2026, the EU advanced a major legislative reset via the pharmaceutical reform package published on 6 March 2026, setting a transition period of about 24 months (2026-2028) for Member States to update national laws and for EMA and national authorities to develop implementing guidance. In July 2026, the European Medicines Agency (EMA) updated its Q&A guidance covering GMP and GDP topics (EMA/INS/GMP/161750/2026), reinforcing that operators must keep quality systems current as interpretations and expectations evolve alongside the reform agenda.

Value Chain Analysis

The European pharmaceutical logistics value chain typically runs from manufacturers (biopharma, vaccines, medical technology) through wholesalers and specialized logistics providers to hospitals, pharmacies, and increasingly patient-direct channels. Execution relies on freight forwarders and carriers (road, air, ocean, and rail), airport and ground-handling operators for temperature-controlled air cargo, and packaging, data, and monitoring technology providers (thermal packaging, IoT sensors, track-and-trace, and quality management systems) to maintain GDP compliance across multi-country movements.

GDP requirements and cross-border complexity drive a layered services structure where warehousing and distribution centers integrate secondary packaging, labeling, kitting, returns, and compliance documentation alongside storage. Network-led models are expanding to combine local execution with harmonized standards, illustrated by LOXXESS establishing PharmaXnet Europe GmbH in April 2026 as a GDP-certified pharmaceutical logistics network using qualified local partners. Capacity is concentrating in multi-temperature hubs to serve biologics and advanced therapies, with DHL Group expanding its Florstadt Health Logistics campus in Germany in May 2025 by 100,000 square meters and adding capacity for over 140,000 pallets.

Competitive Landscape

Market consolidation is rising as scale and specialized capabilities become critical. DSV’s integration of DB Schenker in April 2025 created a logistics conglomerate with 160,000 employees and anticipated DKK 9 billion (USD 1.33 billion) in synergies by 2028. DHL pledged EUR 2 billion to build Pharma Hubs and double healthcare revenue to EUR 10.8 billion (USD 11.91 billion) by 2030, signaling a shift toward vertically integrated, GDP-certified ecosystems. UPS deepened its European cold-chain strength by acquiring Frigo-Trans and BPL, noting that 80% of regional pharmaceutical flows are temperature sensitive.

Digitalization differentiates leaders: DHL Supply Chain’s generative-AI pilots streamline RFP data cleansing, while CEVA unites under a single brand post-Bolloré integration, deploying “FORPLANET” low-carbon services. White-space entrants in ultra-cold storage and AI-powered risk analytics compete by offering hyper-niche expertise rather than broad networks. EU antitrust scrutiny remains high, with an average of five pharma-logistics decisions annually and EUR 773 million (USD 853.11 million) in fines between 2018-2022.

Long-term competitive intensity will center on sustainable fleet transitions, clinical-trial supply visibility, and secure capacity on emerging rail corridors. Players with balanced modal portfolios, robust GDP certifications, and AI-enabled forecasting stand to capture premium contracts as regulatory oversight tightens.

Europe Pharmaceutical Logistics Industry Leaders

DHL

FedEx

Kuehne + Nagel International AG

United Parcel Service

C. H. Robinson

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multi-temperature and ultra-cold infrastructure remains a visible whitespace, particularly where therapy mix is shifting toward biologics and advanced therapies while capacity is uneven across countries. Recent capacity adds show where investment is flowing and where adjacent nodes can be built out: Movianto expanded its Aalst, Belgium site in June 2026, doubling temperature-controlled pallet positions from 14,000 to 25,000 across ambient, chilled, frozen, and ultra-cold, and Frankfurt Cargo Services opened a new CEIV- and GDP-certified Pharma Center at Frankfurt Airport in May 2026, quadrupling temperature-controlled handling capacity. These moves support opportunities for additional GDP-certified satellite depots, qualified lane development (including ultra-cold packaging and validation services), and control-tower orchestration tied to major hubs.

Policy initiatives aimed at supply resilience create further whitespace in Central and Eastern Europe for compliant storage, distribution, and value-added services close to reshoring and regional manufacturing programs. The European Commission proposed the Critical Medicines Act in March 2025 to incentivize manufacturing relocation to the EU, and the EU reached political agreement in December 2025 to modernize pharmaceutical legislation with measures targeting shortages and supply chain functioning. Operators that can combine GDP-grade execution with regulatory documentation, serialization-ready processes, and cross-border customs capabilities are positioned to capture incremental outsourcing as shippers rebalance networks toward resilience-focused footprints.

Recent Industry Developments

- June 2026: UPS invested USD 48 million in 27 temperature-controlled freight cross-dock facilities globally, including sites in Europe, to strengthen handling for medicines in 2-8 degrees Celsius and 15-25 degrees Celsius ranges. The added cross-dock footprint improves time-definite routing and reduces temperature-excursion risk during transfers. It also raises the capability baseline for mid-mile pharma networks beyond traditional hub-and-spoke models.

- June 2025: DHL Global Forwarding opened a 24,500 sq m air hub at Frankfurt Airport with capacity to handle 300,000 tons annually and a rooftop solar array supporting operations. The site increases controlled handling throughput at one of Europe’s key air cargo gateways, supporting pharma shippers that depend on high-frequency uplift. The investment also aligns air-side infrastructure with tighter GDP audit expectations for temperature management and documentation.

- July 2024: Germany extended tolling to vehicles over 3.5 tons, adding a new cost layer across road-based pharmaceutical distribution in one of the region’s largest logistics markets. This change accelerated attention to route optimization, fleet utilization, and shifts toward lower-emission equipment where commercially feasible. For pharma logistics providers, the policy sharpened the trade-off between service-level requirements and total landed cost on domestic and cross-border lanes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market means paid logistics services used to move, store, and manage pharmaceutical and adjacent healthcare products across Europe, including temperature-controlled and ambient flows, plus supporting handling and compliance activities.

Scope exclusions: In-house distribution done fully by drug manufacturers or hospitals (without a paid third-party logistics service) is excluded.

Segmentation Overview

- By Service Type

- Transportation

- Road Freight

- Air Freight

- Sea Freight

- Rail Freight

- Warehousing and Storage

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Geography

- Germany

- United Kingdom

- Netherlands

- France

- Italy

- Spain

- Poland

- Belgium

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outside limits of demand and the operational context for pharma distribution in Europe, and then to build clean assumptions that can be tested in interviews. We reviewed public statistics and regulatory references that influence how products can be stored and moved, since compliance often drives service mix and pricing.

Common reference points included sources such as Eurostat trade and transport series, European Commission publications on medicines policy and supply resilience, the European Medicines Agency guidance and safety communications, World Health Organization materials on good distribution practices, and customs or border-trade summaries released by national authorities. We also used annual reports and investor presentations of logistics providers, plus reputable press coverage on capacity additions, temperature-controlled networks, and major route disruptions. Where needed, a paid subscription for company financials and intelligence, and a shipment-level import export database, helped validate revenue ranges and cross-check trade-linked volume signals. The sources listed above are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with logistics operators, cold-chain specialists, warehousing managers, and pharma supply chain teams, since they can confirm service splits and real pricing movement. We covered major European corridors and hubs, and then used these inputs to close gaps from public data, especially on value-added services, compliance-driven handling, and temperature-control penetration.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 58% | Functional/Unit leaders: 42% | |

| Smaller Players: 16% | Managers: 45% |

Market-Sizing & Forecasting

Market sizing starts from a Europe demand pool view where healthcare and pharmaceutical distribution activity is reconstructed using trade and production indicators, and then converted into logistics spend using service mix and pricing logic. In practice, we first estimate addressable flows that require compliant handling, then apply splits for transport, warehousing, and value-added services, followed by checks on cold-chain versus non-cold-chain intensity.

To keep the model traceable, we used a mix of inputs such as pharma output and trade values by country, the share of products requiring controlled temperatures, warehousing throughput linked to GMP/GDP compliant space, modal mix for time-sensitive shipments, and practical assumptions on average service rates for storage and transport. When the model became too reliant on a single macro series, it was rebalanced using selective bottom-up approximations, such as sampled provider revenue ranges, route-level channel checks, and volume times average price checks for representative lanes. Gaps that remain in smaller countries were handled by applying validated proxy ratios from similar markets (like export intensity and biologics weight) and then stress-testing the impact.

For forecasting, scenario analysis was used to reflect different outlooks for biologics growth, vaccine and specialty-drug distribution needs, and policy-driven supply resilience investments, and then these scenarios were translated into yearly service demand. The final path was selected after our expert inputs converged on realistic growth ranges for volumes and pricing rather than a single aggressive or conservative case.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, followed by targeted checks on any outliers before figures are finalized. We compare outputs against country-level trade movement direction, reported capacity additions in temperature-controlled logistics, and public pharma production and export trends, which helps catch timing mismatches and currency effects.

If large variances show up by country or service line, analysts re-check assumptions, review interview notes, and re-contact respondents when a specific driver needs confirmation. Before sign-off, the model is reviewed in multiple steps by another analyst to ensure inputs, units, and conversion factors are consistent. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Pharmaceutical Logistics Market Sizing Compared With Other Published Estimates

Different published market numbers can look far apart because the market can be counted from different starting points, such as logistics spend, product trade value, or a narrower cold-chain-only view. Timing also matters, since some sources publish one year earlier or use a different currency conversion point.

Inclusions and exclusions are usually the biggest gap drivers, and they show up quickly in Europe where compliance services and temperature control are not evenly used across countries. Cosmetics and some healthcare-adjacent items are included within Mordor Intelligence's scope, which lifts the total versus estimates that restrict the market to prescription medicines only and exclude these adjacent flows. A second driver is how value-added services are treated, because some estimates count only transport and storage, while others also add packaging, labeling, and serialization-related handling as part of logistics spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 90.30 B (2025) | |

| Trade Journal A | USD 41.67 B (2023) | Often anchored to EU-27 turnover style indicators tied to transport and trade flows, which can undercount broader third-party logistics spend and may not capture warehousing and value-added services consistently across Europe. |

| Industry Publisher B | USD 24.61 B (2025) | Typically narrows the scope to a smaller set of pharma logistics activities, which can exclude adjacent healthcare handling and reduce coverage of specialized services like compliant packaging, monitoring, and cross-border GDP documentation support. |

The spread is mainly explained by what each source counts as logistics spend and how widely the service basket is defined across countries. By tying the totals back to observable distribution signals, and then confirming key splits with interviews, we keep the estimate easy to follow and repeat with clear inputs.

Key Questions Answered in the Report

What CAGR is forecast for Europe pharmaceutical logistics from 2026 to 2031?

The sector is projected to expand at a 3.87% CAGR over the period.

Which service type holds the largest share of pharmaceutical shipments in Europe?

Transportation services lead with 59.32% share in 2025 due to the region’s reliance on road, air, ocean, and rail capacity.

Why is cold-chain infrastructure critical for pharmaceutical distribution?

Biologics, vaccines, and cell- and gene-therapy products dominate the pipeline, requiring controlled temperatures and comprehensive GDP compliance.

How is Brexit affecting medicine flows between the UK and the EU?

Extra customs steps and new “UK Only” labeling rules add lead time and cost, contributing to higher drug shortage alerts and procurement spending.

What sustainability measures are logistics providers adopting?

Companies are investing in electric trucks, reusable packaging, rail and inland-waterway lanes, and shifting to sustainable aviation and marine fuels to cut emissions.

Which European country is expected to grow fastest in pharmaceutical logistics?

Poland is forecast to post the highest growth, with a 4.73% CAGR through 2031 as infrastructure modernization attracts new distribution hubs.

Page last updated on: