Spain Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

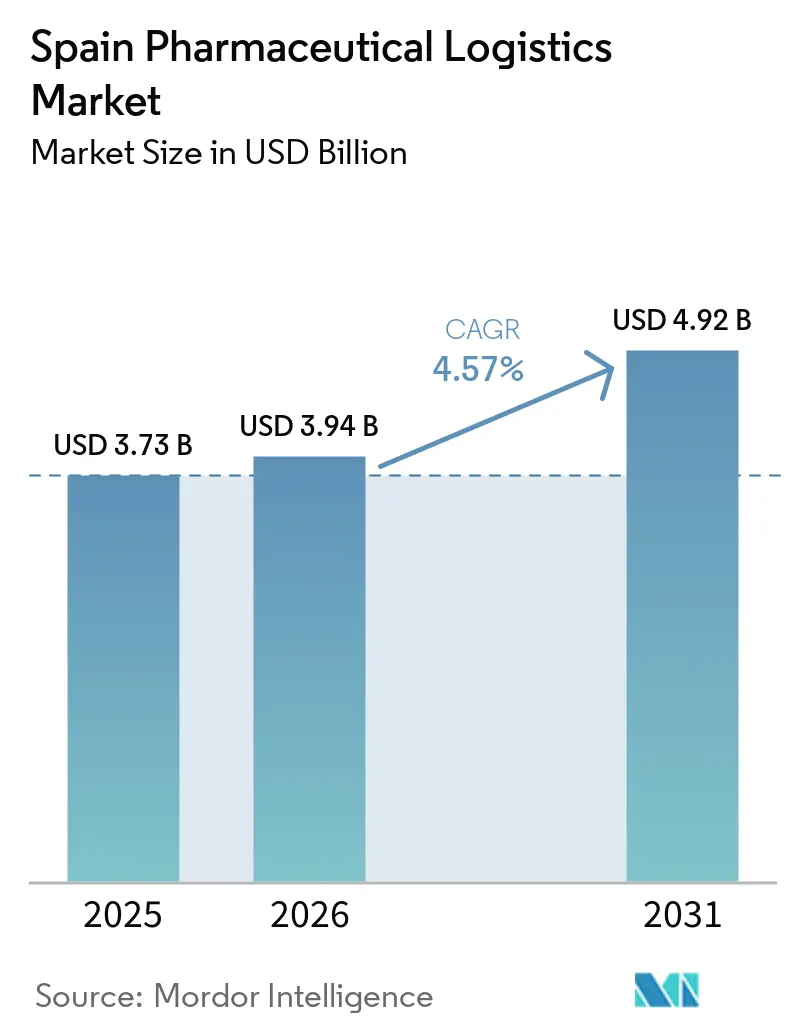

| Base Year Market Size (2025) | USD 3.73 Billion |

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

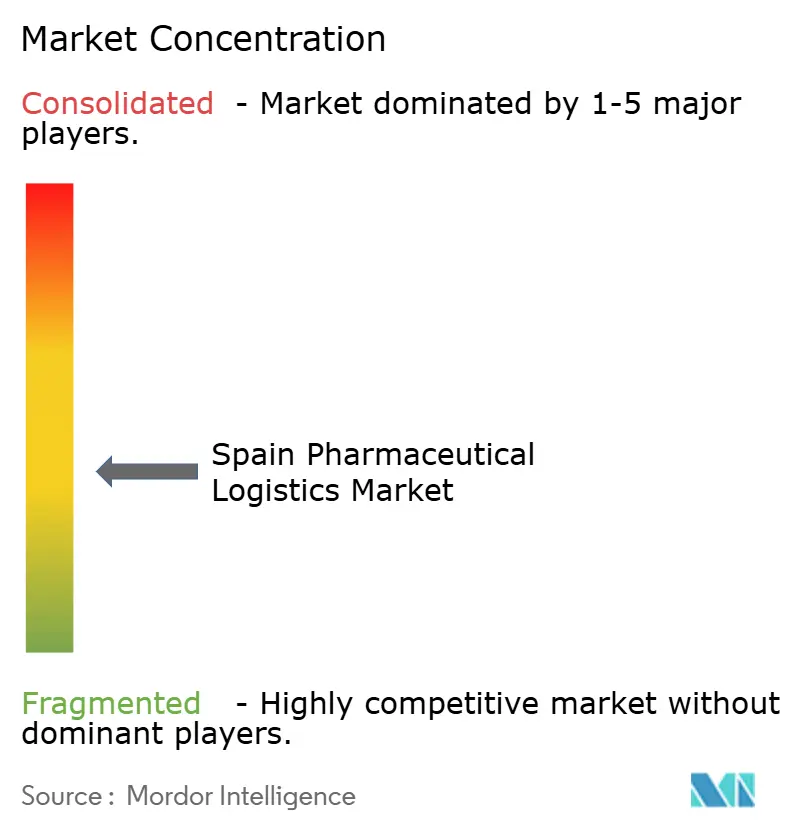

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The Spain Pharmaceutical Logistics Market size is expected to grow from USD 3.73 billion in 2025 to USD 3.94 billion in 2026 and is forecast to reach USD 4.92 billion by 2031 at 4.57% CAGR over 2026-2031. Sustained digital-health expansion and nationwide e-prescription uptake are funneling a rising share of medicines directly to patient homes, reshaping distribution networks that historically revolved around wholesale pharmacy replenishment. Urban micro-hubs equipped with Good Distribution Practice (GDP) controls are multiplying in secondary cities as operators race to cut last-mile transit times and uphold temperature integrity. Added compliance pressure from EU Annex 21 importer-accountability audits is rewarding players that hold robust quality management certificates, while capital-intensive investments in hydrogen-powered refrigerated fleets and blockchain-based traceability systems widen capability gaps between multinational integrators and smaller regional carriers. Together, these factors keep cost-to-serve high yet also unlock premium revenue streams around value-added services, serialization verification, and direct-to-patient clinical-trial support.

Key Report Takeaways

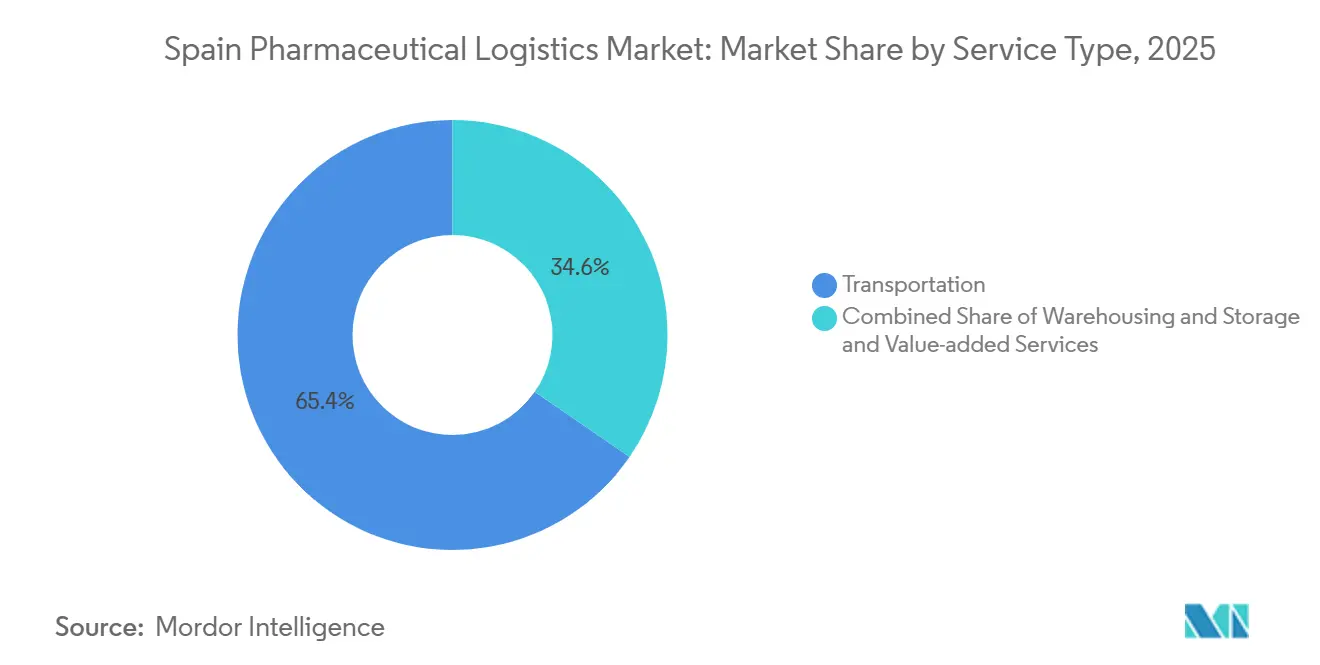

- By service type, transportation commanded 65.39% of the Spain pharmaceutical logistics market share in 2025, whereas value-added services are projected to advance at a 5.05% CAGR through 2031.

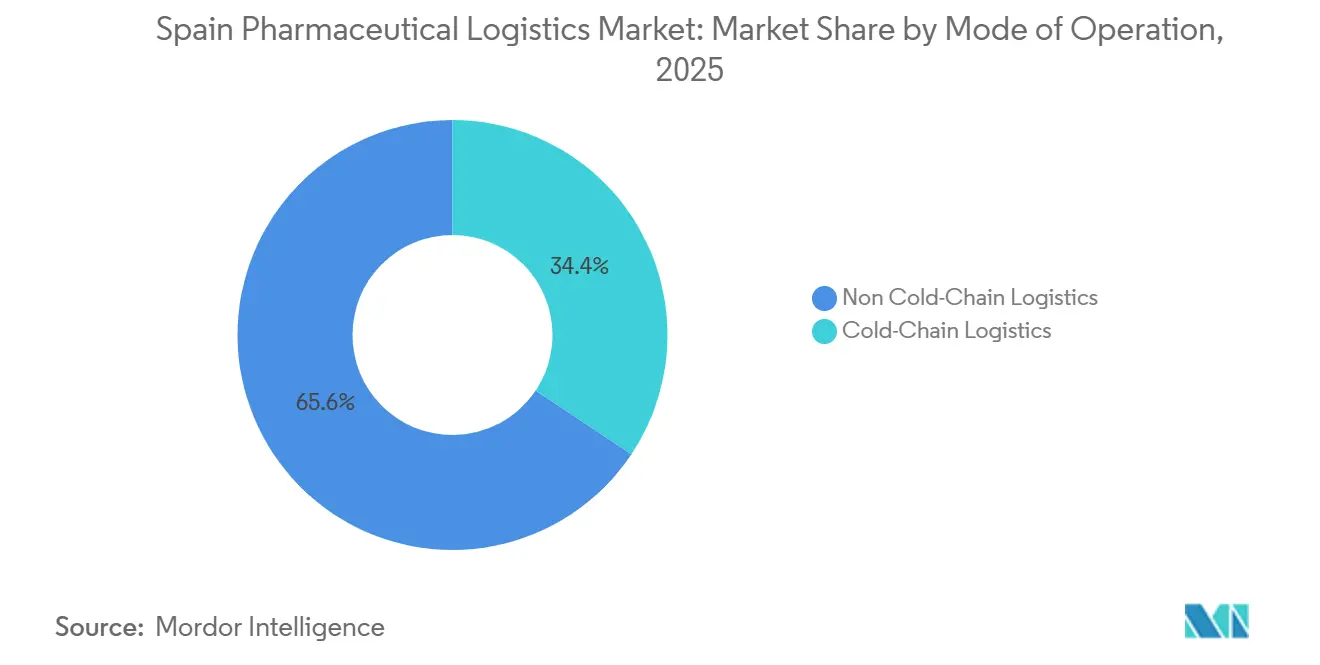

- By temperature control, non-cold-chain operations held 65.64% of the Spain pharmaceutical logistics market size in 2025, while cold-chain segments are set to expand at 5.22% CAGR to 2031.

- By product type, prescription drugs represented 56.22% share of the Spain pharmaceutical logistics market size in 2025, while cell and gene therapies are rising at 5.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in online-pharmacy and e-prescription parcel volumes | +1.1% | Madrid, Barcelona, Valencia, Seville | Short term (≤ 2 years) |

| Expansion of direct-to-patient clinical-trial logistics | +0.7% | Barcelona, Madrid biotech hubs | Medium term (2-4 years) |

| Stricter EU Annex 21 importer-accountability audits | +0.5% | National | Short term (≤ 2 years) |

| Regional subsidies for temperature-controlled urban micro-hubs | +0.6% | Secondary cities | Medium term (2-4 years) |

| Early adoption of hydrogen-powered refrigerated fleets | +0.4% | Industrial corridors | Long term (≥ 4 years) |

| Pilots of blockchain-enabled batch provenance | +0.5% | Major distribution centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Online-Pharmacy and E-Prescription Parcel Volumes

Spain’s online-pharmacy channel has been rising at 7.1% CAGR and now reaches consumers in every autonomous community, producing millions of individual prescription parcels each month. Digital prescribing fully integrates with the National Health System, bypassing brick-and-mortar hand-offs and demanding GDP-certified couriers able to maintain 2-8 °C conditions and real-time traceability. Logistics firms are responding with temperature-controlled micro-hubs positioned close to dense residential zones, enabling same-day drop-offs for chronic-care medicines. Secondary cities such as Zaragoza and Malaga, historically underserved, are priority build-out targets as parcel density now justifies fixed cold-room investments. The heightened visibility of chain-of-custody data also reduces counterfeit risk, a key compliance issue under EU Falsified Medicines Directive requirements.

Expansion of Direct-to-Patient Clinical-Trial Logistics

Decentralized clinical trials (DCTs) are displacing site-based models, with sponsors in Barcelona’s and Madrid’s biotech clusters already running hundreds of at-home studies. DCTs ship investigational medicines straight to participants, creating urgent demand for couriers trained in temperature-sensitive handling and patient-privacy compliance. Spanish regulators treat these study parcels as medicinal products, so GDP principles and chain-of-identity protocols apply. Providers that couple 24/7 control-tower visibility with remote-monitoring IoT devices gain a competitive advantage in winning sponsor contracts, especially for advanced therapies requiring cryogenic storage. As a result, contract logistics revenue linked to DCTs is projected to outpace conventional trial site resupply, reinforcing the importance of value-added services in the Spain pharmaceutical logistics market[1]“EudraLex Volume 4 – Good Manufacturing Practice Guidelines,” European Commission, EUROPA.EU.

Stricter EU Annex 21 Importer-Accountability Audits

Annex 21, adopted in 2022, strengthens oversight of medicinal-product importers, obliging Spanish wholesalers to verify supplier GDP status and keep exhaustive serialization records. Agencia Espanola de Medicamentos y Productos Sanitarios (AEMPS) has since doubled audit frequency, escalating penalties for deficiencies such as incomplete temperature logs or missing unique-identifier scans. Multinational 3PLs with EU-wide quality systems pass audits more easily, while smaller fleets lacking dedicated quality units face suspension risks or acquisition pressure. This regulatory tightening elevates compliance costs yet simultaneously filters out sub-scale players, nudging the Spain pharmaceutical logistics market toward higher concentration[2]“GDP Inspections and Certificates for Distributors,” AEMPS, AEMPS.GOB.ES.

Regional Subsidies for Temperature-Controlled Urban Micro-Hubs

Recover-and-Resilience-Facility (RRF) grants earmark EUR 163 billion (USD 191.73 billion) for digital and green infrastructure, with several regional calls offering up to 40% capex aid for GDP-certified cold rooms in logistics parks. Cities like Valladolid and Alicante now provide subsidy co-financing, reducing payback periods for operators installing 2-8 °C rooms below 1,000 m² dedicated to e-prescription fulfillment. Subsidies accelerate expansion beyond Madrid-Barcelona corridors, broadening parcel delivery coverage and lowering temperature-excursion risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of GDP-compliant last-mile carriers beyond tier-1 cities | -0.8% | Rural regions, secondary cities | Short term (≤ 2 years) |

| Port congestion and limited cold-storage slots at Valencia and Barcelona | -0.6% | Major port facilities | Medium term (2-4 years) |

| High capex for hydrogen/EV reefer fleet conversions | -0.7% | Nationwide | Long term (≥ 4 years) |

| Cyber-security vulnerabilities in IoT temperature devices | -0.5% | Digitally connected cold chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of GDP-Compliant Last-Mile Carriers Beyond Tier-1 Cities

In Spain, major hubs like Madrid, Barcelona, and Valencia dominate the last-mile cold-chain capacity compliant with GDP standards. Meanwhile, smaller provinces grapple with limited 2-8 °C delivery coverage. This disparity restricts online pharmacies in these regions, leaving them with fewer carrier options outside urban centers. As e-prescriptions and telepharmacy gain traction, regions like Castilla-La Mancha and Extremadura face potential service launch delays. The challenges stem from securing refrigerated deliveries, thinner competition, rising costs, and extended transit windows. These factors jeopardize refill reliability and adherence for chronic diseases[3]“Statistical Yearbook 2025,” Port of Valencia, VALENCIAPORT.COM .

Port Congestion and Limited Cold-Storage Slots at Valencia and Barcelona

Valenciaport processed 5.6 million TEU in 2024 and often reaches berth-utilization peaks above 90%, restricting off-load windows for refrigerated containers. Barcelona faces similar constraints and still lacks ample on-dock cool rooms, pushing high-value biologics into overflow yards where passive packaging struggles to hold target temperatures. Construction works to expand reefer plug capacity run through 2027, so congestion remains a mid-term risk[4]“Cargo Traffic Report 2025,” Port of Barcelona, PORTDEBARCELONA.CAT.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Capabilities Outpace Commodity Freight

Transportation retained 65.39% of the Spain pharmaceutical logistics market share in 2025 thanks to dense road and air networks connecting manufacturers with pharmacies and hospitals. Yet value-added services are projected to post a 5.05% CAGR through 2031 as manufacturers pay premiums for serialization checks, blockchain-verified provenance, and regulated-documentation management. This shift enlarges the Spain pharmaceutical logistics market size tied to compliance-critical workflows. Road transport remains the backbone, leveraging 15,825 km of motorways, while air freight covers high-urgency biologics routed through Madrid-Barajas and Barcelona-El Prat airports. Warehousing growth is fueled by e-prescription micro-hubs that convert former retail units into 2-8 °C cross-docks positioned near population centers.

Margin compression in basic freight accelerates diversification into consulting, regulatory advisory, and temperature-mapping audits, particularly among global integrators that bundle end-to-end services. Operators that integrate track-and-trace APIs with healthcare-provider portals capture new revenue streams by automating dispensation-confirmation messages back to prescribing doctors. These adjacent offerings deepen client stickiness, and their higher gross margins buttress overall profitability even as fuel-cost volatility squeezes road-line-haul yields.

By Temperature Control: Cold-Chain Infrastructure Gains Momentum

Non-cold-chain flows still accounted for 65.64% of the Spain pharmaceutical logistics market size in 2025, covering solid-dose forms and stable generics. Cold-chain volumes, however, are forecast to rise 5.22% CAGR from 2026 to 2031, reflecting Spain’s fast-growing biologics, vaccine, and cell-therapy segments. The Spain pharmaceutical logistics market, therefore, requires continuing investment in multi-range cold rooms, cryogenic shippers, and qualified packaging lines. National immunization drives following EU pandemic-preparedness guidelines have heightened visibility of cold-chain integrity, with regulators routinely inspecting temperature records.

IoT devices that generate real-time alerts on excursions underpin trust between drug makers and carriers. Yet each added sensor expands the cyber-risk surface, compelling operators to adopt layered security protocols that include encrypted data tunnels and device-authentication routines. Cold-chain intensity also accelerates modal shifts: shippers now book time-definite air charters for high-value biologics where road transit could exceed validated stability windows. Expanded cold-room shells at Madrid-Barajas’ cargo city and Valencia’s logistics park underscore investor confidence that temperature-controlled tonnage will keep outpacing ambient freight well beyond 2031.

By Product Type: Advanced Therapies Stretch Capability Limits

Prescription drugs made up 56.22% of the 2025 market share, but cell and gene therapies headline growth, advancing 5.78% CAGR through 2031. Such patient-specific medicines demand cryogenic storage at −150 °C, GPS-tracked hand-carry services, and chain-of-identity protocols that few operators master. Every successful shipment elevates service reputations and commands pricing multiples that enlarge the Spain pharmaceutical logistics market. Biologics and biosimilars also accelerate as blockbuster antibody patents expire, shifting volume into cost-sensitive cold-chain pipelines.

Vaccines and blood products retain stringent 2-8 °C requirements that spur continued refrigeration-capacity additions. Over-the-counter medicines, though less regulated, increasingly ship via e-commerce parcels, drawing last-mile players into the regulated ecosystem as they upgrade facilities for mixed ambient and cooled workloads. Veterinary medicines and diagnostics carve out niche demand streams that nonetheless reinforce network density, supporting utilization of specialized fleet assets across broader day-to-day routing.

Geography Analysis

Centralized around Madrid, Barcelona, and Valencia, the Spain pharmaceutical logistics market benefits from multimodal gateways that marry seaports, airports, and radial highway arteries. Madrid’s inland hub furnishes overnight truck access to nearly 60% of the population, supporting national e-prescription drop-off commitments. Barcelona leverages port proximity and cross-border ties with France, handling a growing share of inbound biologics. Valencia’s port acts as a Mediterranean entry point but suffers cold-store slot shortages that already spark demurrage and temperature-risk concerns.

Secondary cities are rapidly bridging infrastructure gaps thanks to European Connecting Europe Facility grants amounting to EUR 241 million (USD 283.49 million), including the Sagunto multimodal terminal that will relieve Valencia congestion. New GDP-compliant micro-hubs in Valladolid, Seville, and Malaga improve same-day delivery reach while creating employment in previously underserved logistics labor pools.

Rural zones still lag, with limited courier density hindering cold-chain parcel reliability; nonetheless, regional subsidy schemes now reimburse up to 40% of qualifying capex for temperature-controlled vans, incentivizing last-mile entrants. High-speed rail upgrades between Madrid and Galicia open future rail-based pharma corridors once specialized reefer wagons become commercially viable. Overall, geographic network expansion should cut average pharmaceutical parcel transit by nearly one full day by 2029, raising service levels nationwide.

Competitive Landscape

Competition intensifies as GDP audits and digital-traceability expectations escalate. DHL Supply Chain, UPS Healthcare, and FedEx already hold pan-European CEIV Pharma certificates, forming a quality moat that attracts biologic and cell-therapy shippers. Local specialists such as Movianto and Nacex compete on domestic network density and adaptive same-day services. Consolidation persists: UPS’s acquisition of Frigo-Trans and BPL deepened cold-chain reach across Iberia, while AD Ports’ purchase of Noatum inserted Middle-East capital into Spanish pharma corridors. Blockchain batch-provenance pilots with major wholesalers position early adopters to secure exclusive haulage lanes once nationwide serialization mandates fully roll out.

Strategic investments focus on capacity and compliance. DHL committed EUR 2 billion (USD 2.35 billion) by 2030 for global health-logistics hubs, allocating roughly one-quarter to EMEA nodes including Spain. FedEx added nearly USD 400 million in new European healthcare contracts in 2025, leveraging CEIV capabilities.

Competitive edges also hinge on sustainability; CEVA Logistics’ FORPLANET sub-brand already operates 1,000+ electric vehicles, aligning with pharmaceutical producers’ Scope 3 emission-reduction targets. Cybersecurity readiness is a rising differentiator as shippers audit IoT defense postures to safeguard patient data.

Spain Pharmaceutical Logistics Industry Leaders

DHL Group

Kuehne+Nagel

United Parcel Service of America, Inc. (UPS)

C.H. Robinson Worldwide, Inc.

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL expanded its Life Sciences & Healthcare (LSH) logistics capabilities with a dedicated Airfreight Cold Chain Network. It introduced a Boeing 777 freighter operating between Brussels and Cincinnati to support the network.

- May 2025: AEMPS launched MeQA, an AI tool that answers medication queries and streamlines logistics documentation.

- March 2025: FedEx announced USD 400 million in new European healthcare logistics wins.

- January 2025: UPS Healthcare completed the acquisitions of Frigo-Trans and BPL, doubling cold-chain capacity across Europe.

Spain Pharmaceutical Logistics Market Report Scope

| Transportation | Road Freight |

| Air Freight | |

| Sea Freight | |

| Rail Freight | |

| Warehousing and Storage | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| By Service Type | Transportation | Road Freight |

| Air Freight | ||

| Sea Freight | ||

| Rail Freight | ||

| Warehousing and Storage | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others |

Key Questions Answered in the Report

What is the forecast value of the Spain pharmaceutical logistics market in 2031?

It is projected to reach USD 4.92 billion by 2031.

How fast is the cold-chain segment growing within Spain’s pharmaceutical logistics?

Cold-chain logistics is forecast to expand at 5.22% CAGR during 2026-2031, faster than ambient flows.

Which service category is gaining the most revenue momentum?

Value-added services such as serialization verification and compliance documentation are rising at 5.05% CAGR, outpacing core transport.

Why are e-prescriptions critical for logistics providers?

Nationwide digital prescribing shifts fulfillment to home delivery, increasing parcel volume and driving demand for GDP-compliant last-mile networks.

How are sustainability goals influencing fleet investments?

Spain’s Climate Change Law pushes operators toward hydrogen and electric refrigerated trucks despite higher capex, positioning early adopters for future low-emission mandates.

Page last updated on: