Germany Healthcare Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 26.97 Billion |

| Market Size (2026) | USD 28.63 Billion |

| Market Size (2031) | USD 38.10 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Healthcare Logistics Market Analysis by Mordor Intelligence

The Germany healthcare logistics market size is expected to increase from USD 26.97 billion in 2025 to USD 28.63 billion in 2026 and reach USD 38.10 billion by 2031, growing at a CAGR of 5.88% over 2026-2031.

The Germany healthcare logistics market is supported by Germany’s role as a central European pharmaceutical distribution base, where GDP-compliant warehousing, air cargo handling, and road connectivity support both domestic supply and cross-border drug flows across the European Union. Frankfurt Rhine-Main remains the clearest expression of this role, and DHL Group’s plan to invest EUR 2 billion (USD 2.2 billion) in DHL Health Logistics through 2030 has reinforced that position by adding additional pharmaceutical handling and cold chain capacity. DHL’s conversion of its Florstadt campus into a 100,000 m² pharmaceutical warehouse hub with more than 140,000 pallet spaces shows that large operators are concentrating capital where compliance, throughput, and multimodal reach can be combined in a single network. Frankfurt Airport’s position as a certified pharmaceutical cargo gateway with dedicated handling standards also favors providers that can offer validated temperature assurance rather than standard freight execution. The Germany healthcare logistics market is also benefiting from near-shoring of biopharma production in the south of the country, which is lifting demand for domestic GDP-compliant, temperature-controlled, and value-added logistics support.

Key Report Takeaways

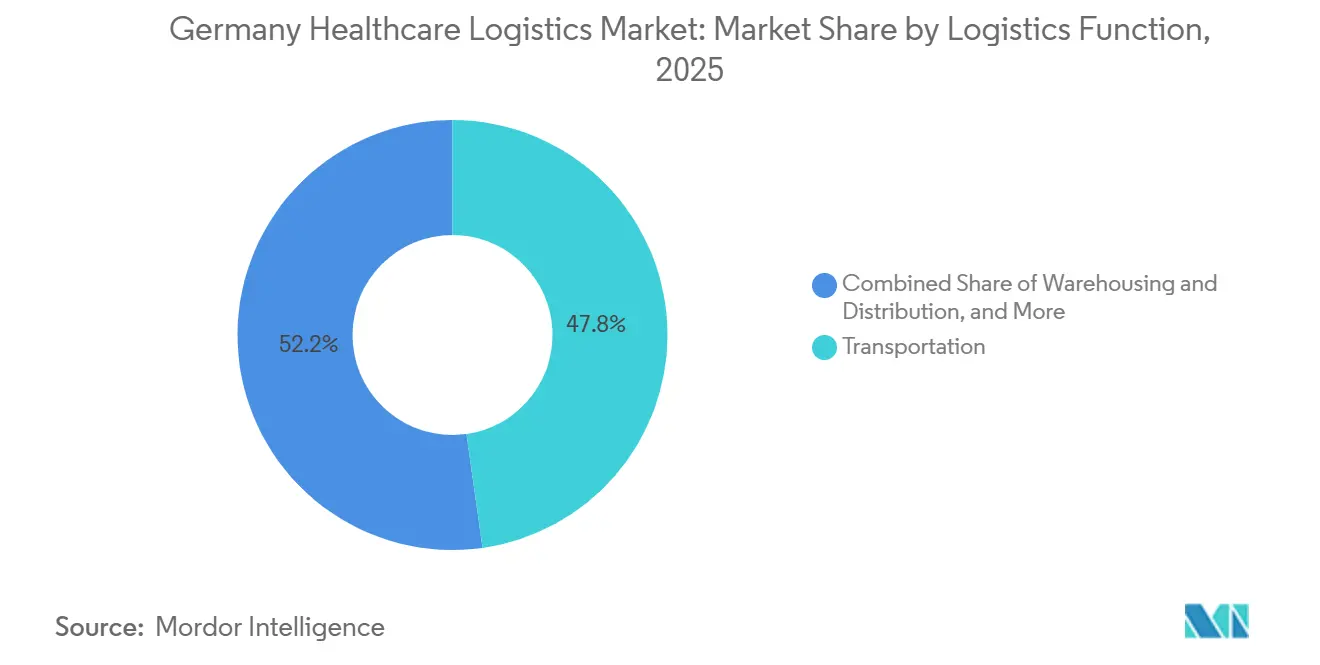

- By logistics function, transportation led with 47.78% of the Germany healthcare logistics market share in 2026, while value-added services and others are forecast to expand at a 7.64% CAGR through 2031.

- By temperature type, non-temperature-controlled logistics held 88.28% of the Germany healthcare logistics market size in 2025, while temperature-controlled logistics is projected to grow at a 7.46% CAGR through 2031.

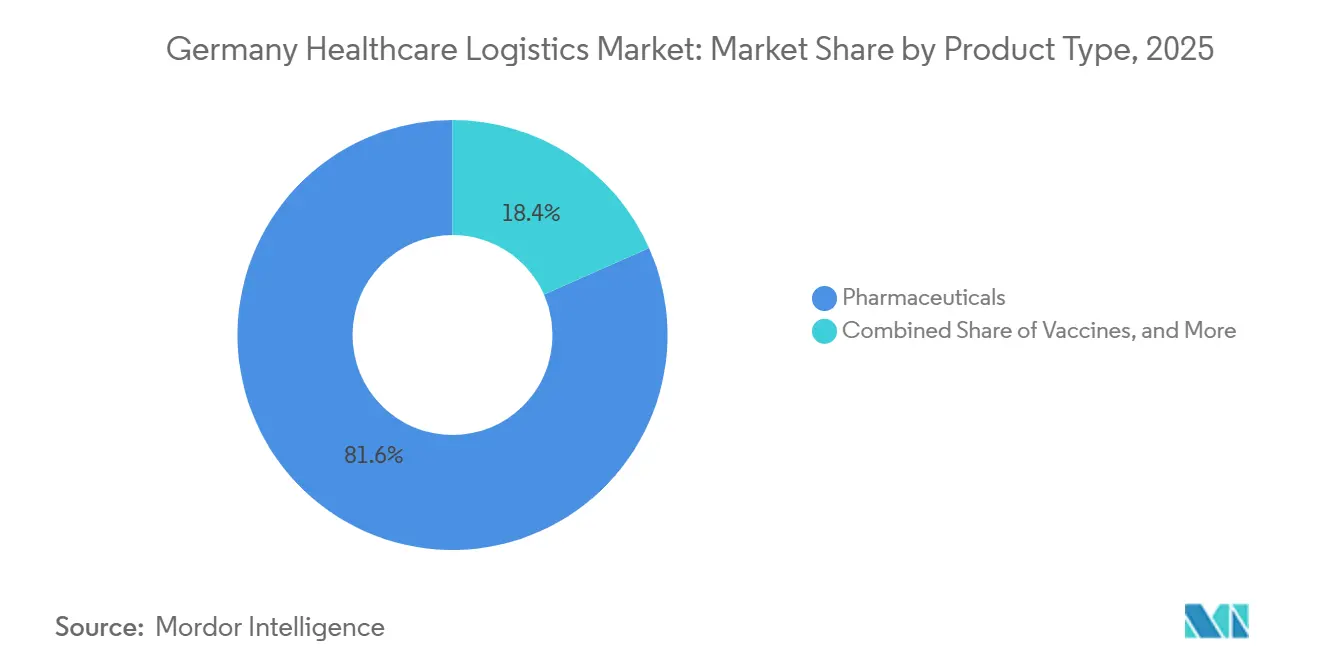

- By product type, pharmaceuticals accounted for 81.64% of the Germany healthcare logistics market share in 2025, while cell and gene therapies are forecast to grow at an 11.94% CAGR through 2031.

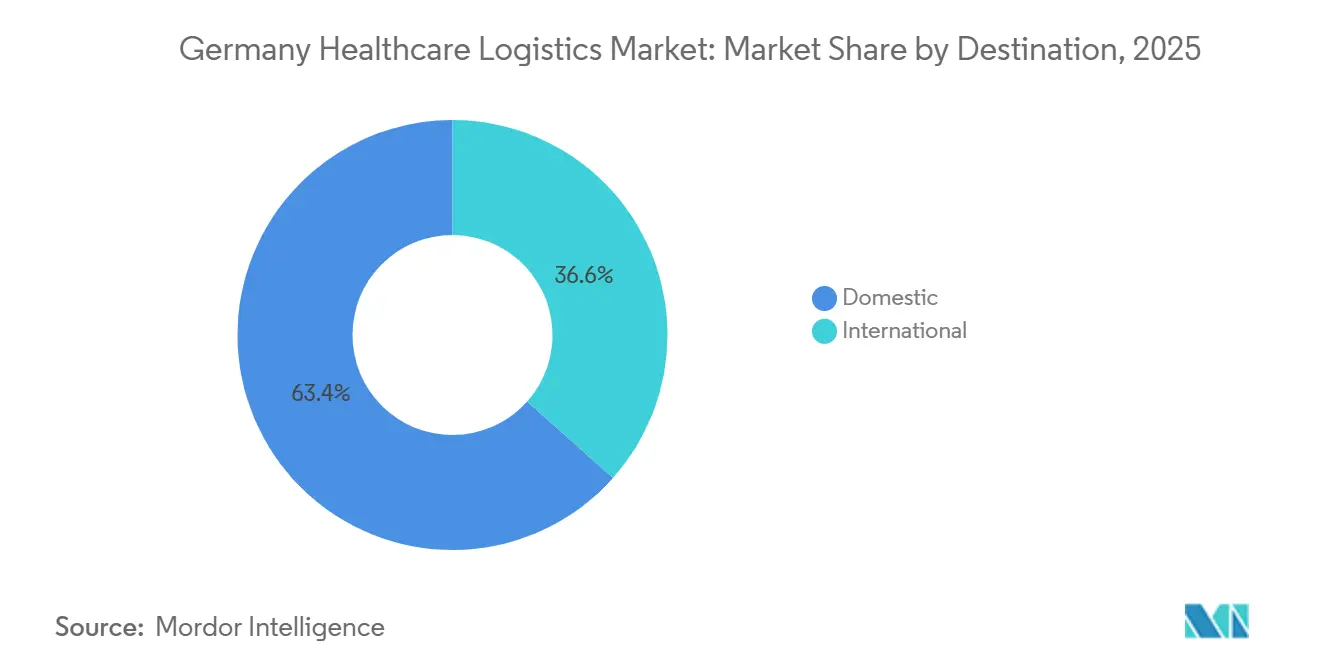

- By destination, domestic logistics held 63.41% of the Germany healthcare logistics market share in 2025, while international logistics is projected to expand at a 6.94% CAGR through 2031.

- By end user, pharmaceutical manufacturers held 36.34% of the Germany healthcare logistics market size in 2025, while biopharmaceutical manufacturers are forecast to grow at a 8.52% CAGR through 2031.

- By geography, North Rhine-Westphalia held 32.30% of the Germany healthcare logistics market share in 2025 and also recorded the highest projected CAGR at 7.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Healthcare Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Germany As a Central European Pharmaceutical Distribution Hub | +1.6% | National, with highest concentration in Frankfurt Rhine-Main, NRW, and Munich corridors | Long term (≥ 4 years) |

| Rising Direct-to-Patient and Home Delivery Models | +1.1% | National, with early gains in metropolitan areas including Berlin, Hamburg, and Munich | Medium term (2-4 years) |

| Increasing Cell and Gene Therapy Trial Logistics | +1.0% | Bavaria and Baden-Württemberg, with national distribution reach | Long term (≥ 4 years) |

| Higher Premium Tolerance for GDP-Compliant Temperature Assurance | +0.8% | National, with APAC and U.S.-origin pharmaceutical multinationals operating German distribution hubs | Medium term (2-4 years) |

| Increasing Ultra-Low-Temperature Readiness for Advanced Therapies | +0.9% | Bavaria, NRW, and Hesse | Long term (≥ 4 years) |

| Expansion of Biopharma Manufacturing in Southern Germany | +0.7% | Bavaria and Baden-Württemberg, with spillover to Hesse | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Germany As a Central European Pharmaceutical Distribution Hub

Germany’s location and transport density continue to support its role as a central European pharmaceutical distribution platform. The Germany healthcare logistics market benefits from GDP-compliant air cargo infrastructure at Frankfurt and from road links that connect western, southern, and central European trade routes[1]“Guidelines on Good Distribution Practice of Medicinal Products for Human Use,” European Medicines Agency, ema.europa.eu . Frankfurt Cargo Hub’s Pharma@FRA setup requires continuous temperature monitoring, dedicated handling procedures, and support for sensitive pharmaceutical products, which strengthens Germany’s role in high-value healthcare distribution. This operating model matters more as pharmaceutical flows shift from standard ambient products toward biologics and advanced therapies that need tighter process control. The result is a higher compliance threshold for new entrants and a stronger position for operators that already run certified sites, validated processes, and integrated transport links. The Germany healthcare logistics market therefore gains not only from geography, but also from the fact that compliance capability is now part of core network design.

Rising Direct-to-Patient and Home Delivery Models

Direct-to-patient delivery is becoming an increasingly important part of pharmaceutical fulfillment in Germany as prescription access, home-based treatment, and patient convenience gain greater weight in care delivery. The Germany healthcare logistics market is responding by moving closer to hybrid fulfillment models that can support both institutional distribution and patient-level dispatch in the same network. That shift is operationally demanding because hospital replenishment and home delivery require different pack formats, different controls, and different proof-of-delivery standards. GDP handling requirements still apply when medicinal products move outside classic wholesale channels, which means compliance cannot be relaxed simply because the shipment is smaller or consumer-facing[2]“Guidelines on Good Distribution Practice of Medicinal Products for Human Use,” European Medicines Agency, ema.europa.eu . Providers that can combine batch-level traceability, tamper-evident packaging, and time-sensitive last-mile execution are better placed to secure pharmacy and specialty care contracts. The Germany healthcare logistics market is therefore seeing home delivery as an extension of regulated pharmaceutical fulfillment rather than as a simple parcel service.

Increasing Cell and Gene Therapy Trial Logistics

Cell and gene therapy logistics is becoming one of the most technically demanding areas of the Germany healthcare logistics market. Sartorius Stedim Biotech opened a new competence center in Freiburg in 2025, investing EUR 140 million (USD 154 million) to expand production of cell and gene therapy components, including cytokines and growth factors. ProBioGen was also selected to lead GMP manufacturing operations at the Berlin Center for Gene and Cell Therapies, a facility backed by Germany’s federal research funding and scheduled to open in 2028. These developments raise logistics demand for chain-of-custody controls, real-time temperature visibility, and time-critical transport windows for patient-specific materials. Regulatory oversight for advanced therapies keeps documentation and deviation management standards high, which limits the role of general freight carriers in this part of the Germany healthcare logistics market. The effect is a market structure where capacity, compliance, and clinical handling experience must advance together.

Higher Premium Tolerance for GDP-Compliant Temperature Assurance

Pharmaceutical customers in Germany are increasingly willing to pay for certified temperature assurance when product sensitivity and regulatory exposure are high. FedEx secured an IATA CEIV Pharma Corporate Certificate in May 2025, adding its Cologne and Frankfurt facilities to its certified healthcare network for advanced biopharmaceutical and clinical-trial handling[3]“CEIV Pharma Certification Standards,” IATA, iata.org. GEODIS also completed GDP certification for pharmaceutical ocean freight logistics in Germany in 2025, thereby extending its compliance coverage across all transport modes in the country. These moves show that certification is being used as a pricing and contract-positioning tool rather than only as a quality badge. IATA’s CEIV framework has become a recognized benchmark in tender processes, especially where excursion risk and audit exposure matter most. The Germany healthcare logistics market is therefore rewarding operators that invest early in validated processes, certified sites, and documented temperature performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Costs for Refrigerated Warehousing and Transport | -0.8% | National, with highest exposure in NRW and Bavaria where cold-storage density is greatest | Short term (≤ 2 years) |

| Shortage of GDP-Trained Drivers and Cold Chain Labor | -0.7% | National, with rural federal states disproportionately affected | Long term (≥ 4 years) |

| Uneven Infrastructure Depth Across Smaller Federal States | -0.5% | Eastern and northern smaller Länder | Medium term (2-4 years) |

| Margin Pressure from Cross-Border and Regional Specialist Carriers | -0.4% | National, with highest intensity on the NRW to Netherlands to Belgium corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs for Refrigerated Warehousing and Transport

Refrigerated warehousing and transport continue to face cost pressure from elevated energy use and the need for continuous temperature control. The Germany healthcare logistics market feels this pressure most strongly in cold storage operations, where power use is built into the service model and cannot be reduced without equipment upgrades. Smaller specialist operators are more exposed because they often have narrower asset bases and less room to fund large cooling retrofits. Compliance and refrigerant rules also make facility upgrades more expensive and slower to execute, which can delay efficiency gains in parts of the network. This pushes the market toward larger operators that can absorb utility volatility and finance validated infrastructure renewal over a longer planning period. The result is short-term margin pressure and, over time, gradual consolidation pressure in temperature-controlled nodes.

Shortage of GDP-Trained Drivers and Cold Chain Labor

Labor availability remains a structural constraint for the Germany healthcare logistics market, especially where cold chain handling and GDP procedures have to be combined in one role. Under GDP standards, personnel involved in pharmaceutical distribution must be trained in deviation handling, documentation, and temperature control processes, so a general driver shortage becomes a compliance issue when healthcare loads are involved. DACHSER has highlighted the need to strengthen life science and healthcare capabilities across its network, which reflects the broader effort required to build specialized staff rather than generic transport labor. This constraint limits the flexibility of adding capacity during peak periods and underscores the importance of in-house training programs among established providers. It also favors operators that can standardize procedures across facilities and reduce dependence on a thin external labor pool. The Germany healthcare logistics market, therefore, faces a persistent operating challenge that affects service quality, not only transport availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Leads, Value-Added Services Grow Faster

Transportation accounted for 47.78% of the Germany healthcare logistics market share in 2026, making it the largest function in the market. Road freight remained the core mode within this segment because hospitals, wholesalers, and pharmacies need dense last-mile and regional replenishment coverage. Air freight still represented a smaller share, but investment intensity remained high because time-sensitive biologics and specialty shipments depend on faster international connections. Kuehne+Nagel added Frankfurt to its Inspire aircraft rotation in June 2026, creating a direct Chicago-Frankfurt link that targets sensitive pharmaceutical flows between 2 major production and distribution hubs. Sea, inland waterways, and rail kept more selective roles in bulk API movements and intermodal domestic distribution, while warehousing and distribution remained the second-largest functional category in the Germany healthcare logistics market.

Value-added services and others are forecast to grow at a 7.64% CAGR from 2026 to 2031, making it the fastest-growing function in the German healthcare logistics market. This expansion reflects the broader outsourcing of serialization, kitting, relabeling, clinical trial support, and patient-specific cold-chain packaging to specialized logistics partners. LOXXESS Pharma’s Rosengarten-Nenndorf site near Hamburg, scheduled to start in Q3 2026, includes automated cube-storage robotic picking systems and was presented as the first such system with pharmaceutical GDP approval in Germany. The commercial effect is clear, because validated automation can raise throughput and accuracy while also strengthening audit readiness. In this part of the Germany healthcare logistics industry, service depth is becoming more valuable than simple warehouse footprint because pharmaceutical customers are shifting regulated support tasks outside their own facilities.

By Temperature Type: Ambient Volume Stays High, Controlled Logistics Gains Importance

Non-temperature-controlled logistics held 88.28% of the Germany healthcare logistics market share in 2025, which kept it as the largest temperature segment in the market. That reflects the large volume of ambient pharmaceuticals, medical devices, and diagnostic products that still move through German healthcare supply chains. Even so, this lead is gradually narrowing as the product mix shifts toward biologics, specialty medicines, and other temperature-sensitive products. Chilled, standard refrigerated, and deep-frozen lanes each matter, but the sharpest capability gap sits in ultra-low-temperature handling for advanced therapies. Movianto expanded its Neunkirchen pharmaceutical refrigeration site from 7,200 to 8,000 pallet positions at 2 °C to 8 °C in May 2025, which shows continued investment in regulated cold chain capacity. The company is also building a new site in Wiesloch-Walldorf, Baden-Wurttemberg, to introduce frozen goods logistics in Germany, extending the cold chain offer beyond standard refrigerated handling.

Temperature-controlled logistics is forecast to grow at a 7.46% CAGR from 2026 to 2031, outpacing the overall Germany healthcare logistics market and gaining strategic weight. GDP guidelines for medicinal products, along with vehicle qualification and temperature monitoring requirements, shape how this capacity can be expanded and validated in practice. The Germany healthcare logistics market is therefore seeing temperature-controlled growth as a mix of infrastructure expansion, stricter monitoring, and more specialized shipment profiles. This is also one of the clearest areas where premium service capability is separating healthcare-focused providers from standard freight operators.

By Product Type: Pharmaceuticals Dominate, Cell and Gene Therapies Expand Fastest

Pharmaceuticals accounted for 81.64% of the Germany healthcare logistics market size in 2025, which gave them the largest position by product type. This segment remains anchored by Germany’s centralized wholesale structure and by dense dispatch networks that serve pharmacies, hospitals, and care institutions on recurring schedules. PHOENIX Group reported FY 2024/25 revenue of EUR 49.7 billion (USD 54.7 billion) across its European operations, demonstrating the scale of wholesale distribution networks connected to pharmaceutical logistics demand. Alliance Healthcare Deutschland’s cooperation model also drew on 27 logistics centers and daily supply capacity to more than 10,000 pharmacies in Germany, underlining the reach of the national wholesale system. The Germany healthcare logistics industry still depends heavily on this broad prescription and OTC base because it creates stable shipment frequency, regular replenishment, and repeat handling volumes.

Cell and gene therapies are forecast to grow at an 11.94% CAGR from 2026 to 2031, making it the fastest-growing product category in the Germany healthcare logistics market. Sartorius noted that cell and gene therapies already make up a large share of the global pharmaceutical development pipeline, and its Freiburg investment shows how Germany is building related manufacturing depth. ProBioGen’s role in the Berlin Center for Gene and Cell Therapies adds to that picture by linking federally supported production infrastructure with future logistics demand. Biopharmaceuticals, vaccines, clinical trial materials, blood and plasma products, medical devices, and diagnostic products remain important demand streams, but they do not change the fact that advanced therapies are setting the pace for capability upgrades. The Germany healthcare logistics market is therefore still led by conventional pharmaceutical volume, while investment priorities are increasingly shaped by smaller but more demanding therapy classes.

By Destination: Domestic Flows Anchor Revenue, International Flows Grow Faster

Domestic logistics held 63.41% of the Germany healthcare logistics market size in 2025, so it remained the larger destination segment. This position reflects the need to provide pharmacies, hospitals, wholesalers, and care providers across all 16 federal states with dependable, compliant delivery coverage. Domestic demand is also supported by the fact that medicine supply cannot be delayed easily, which gives the segment a stable base even when broader freight markets become more volatile. The domestic segment, therefore, provides recurring volume and network utilization for providers across road transport, warehousing, and last-mile distribution. Its scale also supports investment in multi-temperature storage and validated handling, as these costs can be spread across large, predictable shipment flows.

International logistics is forecast to grow at a 6.94% CAGR from 2026 to 2031 in the Germany healthcare logistics market. This faster expansion reflects Germany’s role as a redistribution hub for pan-European pharmaceutical flows, as companies rationalize warehouse networks and seek fewer, higher-quality regional hubs. Kuehne+Nagel stated that market share gains in pharma and healthcare services were a key driver of its 5.0% underlying contract logistics growth in 2025, which supports the view that healthcare-related international flows are strengthening through major hub countries. LOXXESS launched PharmaXnet in April 2026 as a GDP pharmaceutical logistics network spanning 15 countries and managed centrally from Germany, which directly ties German operations to wider European healthcare distribution. In the Germany healthcare logistics market, international growth is therefore coming from hub consolidation, cross-border compliance capability, and wider network orchestration rather than from simple export volume alone.

By End User: Pharmaceutical Manufacturers Lead, Biopharma Manufacturers Grow Faster

Pharmaceutical manufacturers held 36.34% of the Germany healthcare logistics market share in 2025, which made them the largest end-user group in the market. Their importance stems from regular shipment volumes, greater documentation requirements, and a growing preference for long-term service contracts rather than one-off freight purchases. These relationships now extend beyond transportation into packaging support, serialization-related tasks, quality documentation, and specialized handling. The segment also provides providers with a stronger foundation for network planning, as shipment profiles are more predictable than in many other healthcare channels. This keeps pharmaceutical manufacturers at the center of both domestic distribution and cross-border healthcare logistics demand.

Biopharmaceutical manufacturers are forecast to grow at an 8.52% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the Germany healthcare logistics market. That growth is linked to the expansion of biologics and biosimilars, as well as to near-shoring of higher-value pharmaceutical production in southern Germany. Hospitals and clinics remain important users of healthcare logistics, but tight procurement budgets limit providers' pricing flexibility even as product handling becomes more complex. Healthcare distributors and wholesalers also occupy a dual position because they are both customers of third-party logistics services and direct competitors in parts of the last-mile chain. The Germany healthcare logistics industry is therefore seeing its strongest end-user growth where product complexity is rising fastest and where compliance-led outsourcing creates room for specialized logistics partners.

Geography Analysis

North Rhine-Westphalia held 32.30% of the Germany healthcare logistics market share in 2025, and it is forecast to expand at a 7.18% CAGR through 2031. This makes NRW both the largest and the fastest-growing regional segment in the Germany healthcare logistics market. The region benefits from the Rhine corridor, which links pharmaceutical manufacturers, wholesale distribution centers, and major freight gateways into a single operating zone. Its logistics demand base is also broad because pharmaceutical supply in this region is tied to both domestic replenishment and cross-border movement into neighboring European markets. GDP and wholesale distribution authorization requirements raise entry costs here, which supports the position of operators that already control certified assets and established customer relationships.

Bavaria is the second-largest regional segment, supported by the pharmaceutical and biotechnology corridors in Munich, Nuremberg, and Augsburg. The region’s importance is rising because southern Germany is attracting biopharma and advanced therapy production that needs validated, temperature-controlled transport and storage. Sartorius’s new competence center in Freiburg, close to the southern corridor, adds to this pattern by increasing output linked to cell and gene therapy components. In practice, that means Bavaria and the broader southern corridor are likely to pull a higher share of specialized cold chain investment over the forecast period[4]“Sartorius Stedim Biotech Opens New Competence Center for Cell and Gene Therapy Components in Freiburg, Germany,” Sartorius Newsroom, sartorius.com.

Baden-Wurttemberg remains a major healthcare logistics region because of its border position near Switzerland and France and because of its concentration of life sciences and research activity. Movianto’s new Wiesloch-Walldorf development adds another signal that this state is important for frozen and controlled-temperature logistics build-out. The rest of the states still show a clear infrastructure gap, especially where pharmaceutical production activity is present but GDP-certified logistics depth is limited. Northern Germany is one example of that white space, and LOXXESS’s Rosengarten-Nenndorf site near Hamburg was positioned to address it with 13,000 pallet spaces and full WDA authorization from Q3 2026. The Germany healthcare logistics market therefore has its deepest infrastructure in the west and south, while the remaining states present the clearest room for selective capacity expansion.

Competitive Landscape

The Germany healthcare logistics market is moderately fragmented, with global integrators and specialist healthcare operators competing on different strengths. DHL Supply Chain, DSV after the Schenker transaction, Kuehne+Nagel, and UPS Healthcare are the most visible large-scale names, but specialist providers still matter because compliance depth and temperature capability remain uneven across the field. Deutsche Bahn confirmed completion of the DB Schenker sale to DSV in April 2025, making it one of the most important structural changes in the market’s recent competitive history. That transaction is changing network density and pricing reference points across contract logistics in Germany. Even after this step, the Germany healthcare logistics market still leaves room for mid-sized specialists because healthcare customers do not choose providers on scale alone.

A clear strategy pattern is emerging, with the largest operators seeking to combine transport, warehousing, cold chain execution, and regulated support services under a single contract model. DHL’s EUR 2 billion (USD 2.2 billion) healthcare logistics investment program demonstrates this full-network approach and positions Germany at the center of a broader life sciences build-out. FedEx strengthened its competitive position by adding Frankfurt and Cologne to its CEIV Pharma-certified healthcare footprint in 2025, while GEODIS expanded its standing through GDP-certified pharmaceutical ocean freight in Germany. These moves matter because certified capability is becoming a commercial differentiator in tenders, not just a compliance requirement.

Specialist operators are responding by focusing on validated temperature handling, automation, and niche pharmaceutical workflows rather than trying to match the largest networks site for site. LOXXESS is a clear example, with its Rosengarten-Nenndorf automation-led facility and its 2026 PharmaXnet network, both of which aim at higher-value GDP services rather than pure scale. Kuehne+Nagel’s addition of Frankfurt to its Inspire network is another example of targeted investment aimed at premium healthcare flows instead of broad generic freight expansion. The Germany healthcare logistics market is therefore competitive in a practical sense, but the advantage is moving toward providers that can combine GDP compliance, temperature assurance, and value-added execution inside one integrated offer.

Germany Healthcare Logistics Industry Leaders

DHL Group

Kuehne+Nagel

DSV A/S (Including DB Schenker)

United Parcel Service of America, Inc. (UPS)

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Kuehne+Nagel adds Frankfurt to Inspire air freight rotation. The Swiss logistics provider added a weekly Chicago-Frankfurt pharma cargo connection to its own-controlled Inspire aircraft network, directly targeting time-sensitive biologics and specialty pharmaceutical shipments between 2 of the world’s most important pharmaceutical production and distribution hubs. The expanded rotation covers Atlanta, Chicago, Frankfurt, Liege, Sharjah, and Taipei.

- April 2026: LOXXESS Pharma launched PharmaXnet. The new GDP pharmaceutical logistics network spans 15 countries and operates under centralized management from Germany, extending the company’s European reach for regulated pharmaceutical distribution.

- March 2026: Alliance Healthcare Deutschland formed a strategic alliance with Tilray Medical, CC Pharma, and 14U Pharma. Effective April 1, 2026, the cooperation integrated these partners and used Alliance Healthcare Deutschland’s 27 logistics centers and daily supply capacity to more than 10,000 pharmacies to expand access to medical cannabis and parallel-import pharmaceutical products across Germany.

- February 2026: DHL Group expanded its air freight cold chain network for cell and gene therapies. As part of its EUR 2 billion (USD 2.2 billion) healthcare logistics investment program, DHL deployed a dedicated Boeing 777 freighter on the Brussels-Cincinnati route and expanded its pharmaceutical cold chain network for advanced therapies.

Germany Healthcare Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (less than -20 °C) | |

| Non-Temperature Controlled |

| Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trial Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| Non-Temperature Controlled | ||

| By Product Type | Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trial Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States | ||

Key Questions Answered in the Report

What is the size of Germany healthcare logistics market in 2026 and 2031?

The Germany healthcare logistics market size is USD 28.63 billion in 2026 and is forecast to reach USD 38.10 billion by 2031, growing at a 5.88% CAGR over 2026-2031.

Which logistics function leads revenue in Germany healthcare logistics?

Transportation led the Germany healthcare logistics market with a 47.78% revenue share in 2025, supported primarily by road freight and expanding air cargo connections for sensitive pharmaceutical shipments.

Which product category is growing fastest in Germany healthcare logistics?

Cell and gene therapies is the fastest-growing product category, with an 11.94% CAGR through 2031, driven by expanding advanced therapy manufacturing and strict chain-of-custody needs.

Why is North Rhine-Westphalia important for healthcare logistics in Germany?

North Rhine-Westphalia held 32.30% of revenue in 2025 and is also the fastest-growing regional segment at a 7.18% CAGR, helped by the Rhine corridor and dense pharmaceutical distribution activity.

How important is temperature-controlled logistics in Germany?

Non-temperature-controlled flows still dominate revenue, but temperature-controlled logistics is growing faster at a 7.46% CAGR as biologics, vaccines, and advanced therapies require validated cold chain support.

What is shaping competition among healthcare logistics providers in Germany?

Competition is being shaped by certified compliance, cold chain capability, and value-added execution. Large operators are investing in integrated healthcare networks, while specialists are focusing on niche GDP-compliant services and automation.

Page last updated on: